Embed Size (px)

Citation preview

Examiner’s use only

Team Leader’s use only

Surname Initial(s)

Signature

Centre

No.

Candidate

No.

Turn over

Question Leave Number Blank

1

2

3

4

5

6

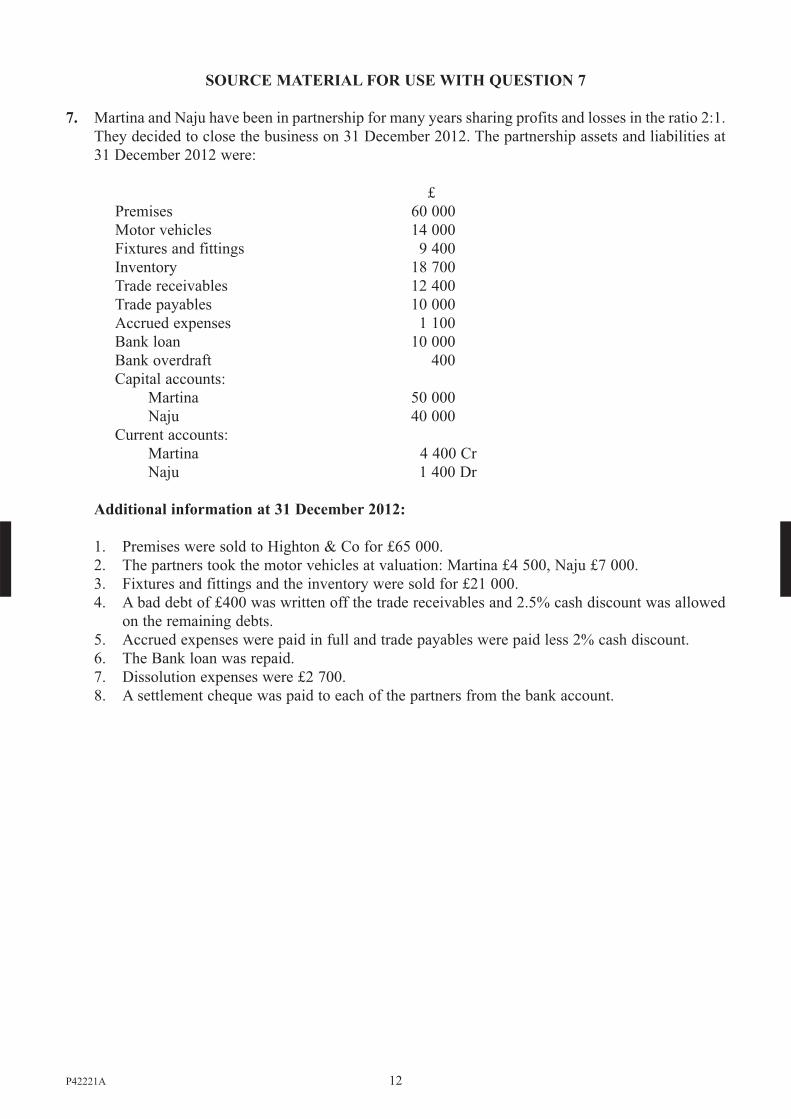

7

TotalThis publication may be reproduced only in accordance with

Pearson Education Ltd copyright policy.

©2013 Pearson Education Ltd.

Printer’s Log. No.

P42221AW850/6001/57570 1/1/1/1/1/e2

*P42221A0136*

Paper Reference(s)

6001/01

London Examinations GCEAccounting (Modular Syllabus)

Advanced Subsidiary

Unit 1: The Accounting System and

Costing

Tuesday 8 January 2013 – Afternoon

Time: 3 hours

Materials required for examination Items included with question papers

Nil Source booklet

Instructions to Candidates

In the boxes above, write your centre number, candidate number, your surname, initial(s) and signature. Check that you have the correct question paper.Answer FIVE questions, choosing TWO from Section A and THREE from Section B.Indicate which question you are answering by marking the box ( ).If you change your mind, put a line through the box ( ) and then indicate your new question with a cross ( ).All calculations must be shown.Write your answers in the spaces provided in this question paper.Do not return the insert with the question paper.

Information for Candidates

The marks for individual questions and the parts of questions are shown in round brackets: e.g. (2).There are 7 questions in this question paper. The total mark for this paper is 200. There are 36 pages in this question paper. Any blank pages are indicated.Calculators may be used.The source material for use with questions 1 to 7 is in the enclosed source booklet.

Advice to Candidates

Write your answers neatly and in good English.

Paper Reference

6 0 0 1 0 1

Leave

blank

2

*P42221A0236*

SECTION A

Answer TWO questions from this section.

If you answer question 1, put a cross in this box ( ).

Source material for question 1 is on pages 2 and 3 of the source booklet.

1. (a) Prepare the:

(i) Journal entries to record the purchase of the shop premises in 5. above. Narratives

are not required

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(6)

Leave

blank

3

*P42221A0336* Turn over

(ii) Departmental Trading Account of Organic Farm Shop showing the profit/loss of

each department for the year ended 31 December 2012

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(8)

Leave

blank

4

*P42221A0436*

(iii) Statement of Comprehensive Income for the business as a whole for the year ended

31 December 2012

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(16)

Leave

blank

5

*P42221A0536* Turn over

(iv) Statement of Financial Position at 31 December 2012.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

Leave

blank

6

*P42221A0636*

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(14)

Leave

blank

7

*P42221A0736* Turn over

(b) Evaluate the owner’s decision to purchase the shop premises as an alternative to

renting.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(8) Q1

(Total 52 marks)

Leave

blank

8

*P42221A0836*

If you answer question 2, put a cross in this box ( ).

Source material for question 2 is on pages 4 and 5 of the source booklet.

2. (a) Explain the meaning of the debit balance on the Rent receivable account on

1 January 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(4)

Leave

blank

9

*P42221A0936* Turn over

(b) Prepare the following accounts for the year ended 31 December 2012, including the

appropriate transfer to the financial statements:

(i) Sundry expenses account

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(4)

Leave

blank

10

*P42221A01036*

(ii) Premises repairs account

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(4)

(iii) Rent receivable account.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(4)

Leave

blank

11

*P42221A01136* Turn over

(c) State one accounting concept which:

(i) supports the change of depreciation method proposed by Arpan

(ii) does not support the change of depreciation method proposed by Arpan.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(4)

Leave

blank

12

*P42221A01236*

(d) Distinguish between capital expenditure and revenue expenditure.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(4)

Leave

blank

13

*P42221A01336* Turn over

(e) State, giving your reasons, whether each of the following is capital expenditure or

revenue expenditure:

� � �� ���������� ����

� � �� ��� ��������������

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(4)

Leave

blank

14

*P42221A01436*

(f) Calculate, showing clearly all workings, the:

(i) adjustment required to the provision for depreciation on the machines to

31 December 2011 to account for the change in depreciation method

(ii) depreciation charge on all the machines for the year ended 31 December 2012.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(8)

Leave

blank

15

*P42221A01536* Turn over

(g) Prepare, for the year ended 31 December 2012, the:

� � ���� ��������������

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(3)

� � ����� ����������������������������������������

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(5)

Leave

blank

16

*P42221A01636*

(h) Evaluate Arpan’s decision to change the basis of charging depreciation on machines

from the straight line method to reducing balance method.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(8) Q2

(Total 52 marks)

Leave

blank

17

*P42221A01736* Turn over

If you answer question 3, put a cross in this box ( ).

Source material for question 3 is on pages 6 and 7 of the source booklet.

3. (a) Explain the following accounting concepts. For each concept give one example from

the draft Statement of Comprehensive Income prepared by Xevena and from the

additional information given, where the concept has not been correctly applied:

(i) Realisation

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(3)

(ii) Accrual (matching)

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(3)

(iii) Going concern.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(3)

Leave

blank

18

*P42221A01836*

(b) Redraft the corrected Statement of Comprehensive Income after taking into account

the additional information given for the year ended 31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

Leave

blank

19

*P42221A01936* Turn over

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(14)

(c) Prepare the Purchases Ledger Control Account, calculating the trade payables balance at

31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(6)

Leave

blank

20

*P42221A02036*

(d) Prepare the Statement of Financial Position at 31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(15)

Leave

blank

21

*P42221A02136* Turn over

(e) Evaluate the use of accounting concepts when preparing financial statements.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(8)

TOTAL FOR SECTION A: 104 MARKS

Q3

(Total 52 marks)

Leave

blank

22

*P42221A02236*

SECTION B

Answer THREE questions from this section.

If you answer question 4, put a cross in this box ( ).

Source material for question 4 is on page 8 of the source booklet.

4. (a) Explain the term profitability.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(4)

Leave

blank

23

*P42221A02336* Turn over

(b) Prepare the Statement of Comprehensive Income for the year ended 31 December

2012, showing clearly the:

(i) value of the inventory at 31 December 2012

(ii) profit for the year.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(6)

(c) Calculate the percentage return on capital employed for the year.

................................................................................................................................

................................................................................................................................

................................................................................................................................

................................................................................................................................

(3)

Leave

blank

24

*P42221A02436*

(d) Prepare the Statement of Financial Position at 31 December 2012.

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

.......................................................................................................................................

(9)

Leave

blank

25

*P42221A02536* Turn over

(e) Calculate the:

(i) current ratio

................................................................................................................................

................................................................................................................................