Embed Size (px)

Citation preview

ldquoPaper or Plasticrdquo How We Pay InfluencesPost-Transaction Connection

AVNI M SHAHNOAH EISENKRAFTJAMES R BETTMANTANYA L CHARTRAND

Does the way that individuals pay for a good or service influence the amount ofconnection they feel after the purchase has occurred Employing a multi-methodapproach across four studies individuals who pay using a relatively more painfulform of payment (eg cash or check) increase their post-transaction connectionto the product they purchased andor the organization their purchase supports incomparison to those who pay with less painful forms of payment (eg debit orcredit card) Specifically individuals who pay with more painful forms of paymentincrease their emotional attachment to a product decrease their commitment tononchosen alternatives are more likely to publicly signal their commitment to anorganization and are more likely to make a repeat transaction Moreover theform of payment influences post-transaction connection even when the objectivemonetary cost remains constant and when the psychological cost is indirect (iedonating someone elsersquos money) Increasing the psychological pain of paymentappears to have beneficial consequences with respect to increasing downstreamproduct and brand connection

Keywords subjective value of money payment mechanism pain of paying com-

mitment economic psychology

When consumers pay for something does the form ofpayment that they usemdashfor example whether pay-

ing by cash credit card or debit cardmdashchange how muchthey value the product they bought or how committed theyfeel to the brand From consumer research consumer wel-fare and managerial perspectives this question lies at theintersection of two fundamental shifts in consumer culture(1) the decreasing use of cash for payment transactions and(2) declining brand loyalty and product retention In thisarticle we investigate whether the type of payment used tomake a purchase can increase how much people value theirpurchase and influence how connected people feel towardthe associated brandorganization

The past two decades have seen large changes in howfrequently people use plastic instead of paper money dur-ing payment transactions (Foster Schuh and Zhang 2013)In 1999 paper payments (ie cash and checks) accountedfor nearly 60 of in-store payments By 2010 that numbershrank to a little over 40 as plastic cards (ie debitcredit and gift cards) became the preferred form of

Avni M Shah (avnishahutorontoca) was a doctoral candidate in

marketing at the Fuqua School of Business Duke University when this re-

search was completed As of July 1 2015 she is an assistant professor of

marketing at the University of Toronto 1265 Military Trail Toronto ON

Canada M1C 1A4 Noah Eisenkraft (noah_eisenkraftuncedu) is an as-

sistant professor of organizational behavior at the University of North

Carolina-Chapel Hill Chapel Hill NC 27599 James R Bettman

(jrb12dukeedu) is the Burlington Industries Professor at the Fuqua

School of Business Duke University Durham NC 27708 Tanya L

Chartrand (Tanyachartranddukeedu) is the Roy J Bostock Professor at

the Fuqua School of Business Duke University Durham NC 27708

Address correspondence to Avni M Shah This article is based on the first

authorrsquos dissertation The authors would like to thank Mike Byerly and

Erin Gasch for their help as well as Marie Komori for her wonderful re-

search assistance In addition the authors would like to thank Mary

Frances Luce for her helpful comments Last but certainly not least this

work greatly benefited from the associate editor and the three anonymous

reviewers whose comments and keen insights were fundamental in im-

proving the work throughout the review process

Darren Dahl served as editor and Sharon Shavitt served as associate edi-

tor for this article

Advance Access publication November 6 2015

VC The Author 2015 Published by Oxford University Press on behalf of Journal of Consumer Research Inc

All rights reserved For permissions please e-mail journalspermissionsoupcom Vol 42 2016

DOI 101093jcrucv056

688

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

payment for a majority of in-store payments (Foster et al2013) The trend away from paper seems to be advancingwith mobile and online transactions also gainingmomentum

Over the same time period product life cycles haveshortened substantially a trend that will likely continuedue to rapid technological innovation (Bayus 1994 1998Khessina and Carroll 2008 Klepper 2007) Consumers to-day have many more brands and products to choose fromin any given product category Consequently the productturnover rate has increased and brand loyalty has decreased(Van Belleghem 2013) An ldquoout with the old in with thenewrdquo mentality has led to a more competitive marketplacegiving nascent brands an opportunity to succeed but alsomaking brand commitment and loyalty harder to achieve(Simonson and Rosen 2014)

In this article we argue that these two fundamentalshifts in consumer culture may be related In particular weargue that the way consumers pay can significantly influ-ence their post-transaction connection to the product theypurchase andor to the organization their purchase sup-ports Drawing on the pain-of-paying literature (eg Prelecand Loewenstein 1998 Raghubir and Srivastava 2008) andtheories of dissonance and self-perception (eg Bem 1967Festinger 1957) we argue that consumers justify usingmore painful forms of payment (eg paying by cash orcheck vs debitcredit card or voucher) by increasing boththeir post-transaction psychological and behavioral com-mitment We test our proposed hypotheses by employing amulti-method approach across four studies Data from afield experiment a lab experiment an online experimentand an archival data analysis suggest that consumers whouse more painful forms of payment are more psychologi-cally connected to their chosen alternative less connectedto their nonchosen alternatives and more likely to show-case their behavioral commitment either by publicly sig-naling support for a cause (ie wearing a lapel pin) or bymaking a repeat donation in comparison to those who payusing less painful forms of payment

CONCEPTUAL FRAMEWORK

Payment Form and Pain of Payment

Classic economic theory states that the utility of a con-sumption experience is determined by the sum of the expe-riencersquos benefits minus the associated costs (eg Deaton1992 Hicks 1946 Marshall 1920 von Neumann andMorgenstern 1944) Classic theory defines these costs aseconomic in nature they are a function of the price paidfor the specific good or experience For example payingless money overallmdashfor example $10 versus $20 for a pairof headphonesmdashdecreases the costs associated with anitem subsequently increasing overall utility whereas

paying more money increases costs and decreases utility(eg Doob et al 1969 Hicks 1946)

Recent research on the pain of paying suggests that thebenefits and costs of a transaction are not solely economicsubtle nuances of the payment experience can also make aconsumption experience more or less attractive When con-sumers make purchases they typically experience a pain ofpaying which refers to the negative affective reaction thatconsumers experience when parting with their money(Zellermayer 1996) This pain is psychological rather thanphysical in nature (Mazar et al 2015) and depends on fac-tors other than payment magnitude

The form of payment used for a transaction (eg cashcheck creditdebit card) is one such factor influencing thepain associated with paying (Raghubir and Srivastava2008 Soman 2001 2003 Thomas Desai and Seenivasan2011) Payment forms vary in terms of the degree of trans-parency of the payment The greater the transparency themore painful and aversive it is for the consumer to partwith money Cash the legal tender of money is consideredthe most transparent and psychologically proximal form ofpayment Consumers must physically part with cash in atransaction so they can easily feel the money they arespending during that transaction and can also easily see theamount being spent (Soman 2001) Subsequently cash isthe most painful form of payment (Raghubir andSrivastava 2008) Paying by check or voucher is less trans-parent and thus less painful than paying by cash Whereaschecks and vouchers easily show the amount or value of atransaction no physical money changes hands leading toconsumers feeling less pain of payment in comparison towhen they pay by cash (Soman 2001) Credit cards debitcards and other forms of plastic money are even less trans-parent the ritual of swiping a card obscures the cash valueof the transaction divorcing people further from its eco-nomic reality (eg Feinberg 1986 Raghubir andSrivastava 2008 Soman 2003 Thomas et al 2011)Finally some recent technological developments in con-sumer payment such as automatic payroll deductions ormobile payments have introduced payment forms that areeven less transparent than credit or debit cards becauseconsumers may not even know the payment has occurred

Although not the focus of the present research in addi-tion to payment form and payment magnitude Prelec andLoewenstein (1998) argue that the extent to which individ-uals experience pain of paying also depends on when theypay for the experience They argue that paying later for anexperience and avoiding debt in that given moment tendsto feel less painful than paying at the time of the experi-ence or before the experience has occurred even if the ob-jective cost remains fixed (Prelec and Loewenstein 1998)Although this theoretical account is consistent with the no-tion that cash is more psychologically painful than checkor credit card this account also implies that a debit cardmdashwhich like cash also immediately drains onersquos

SHAH ET AL 689

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

resourcesmdashshould be psychologically no different thancashmdashand distinct from credit card payments Howeverresearch by Thomas et al (2011) demonstrates that this isnot the case They find that individuals report less pain ofpaying with debit cards in comparison to cash Moreoverto the best of our knowledge there is no empirical supportpublished or otherwise that finds behavioral or psycholog-ical differences between debit credit and gift cards whichis consistent with the theoretical conceptualization that thepain of payment is caused by the payment form and not bypayment decoupling or time discounting of delayed pay-ment (Thomas et al 2011) Thus our research centers onthe argument that the physical form of payment can influ-ence the disutility or psychological aversion to parting withmoney creating varying levels of pain of payment for theconsumer above and beyond the psychological pain expe-rienced from the economic magnitude of the purchase

The insight that different payment forms are associatedwith different levels of pain has implications for under-standing and predicting real-world consumer behaviorScholars have shown that using less painful and less trans-parent forms of money reduces the barrier to spending in-creasing (1) the probability of making a purchase from aconsideration set (2) the decision speed and (3) theamount spent while making a purchase from a consider-ation set (Feinberg 1986 Raghubir and Srivastava 2008Shah Bettman and Payne 2015) Soman (2001) showedthat consumers who paid for a past expense using a rela-tively low-pain credit card were more likely to purchase anadditional discretionary product (eg a boxed set of CDsfrom an artist that they liked) than those who paid for thesame past expense using a relatively higher pain checkSimilarly Prelec and Simester (2001) find that individualsbid nearly twice as much money for an item in an auctionsetting when using a credit card than when using cashInterestingly even priming the notion of cash prior to aproduct evaluation leads people to focus on a productrsquoscosts and negative attributes whereas priming debitcreditcards prior to a product evaluation leads to a focus on theproductrsquos benefits and positive attributes (Chatterjee andRose 2012) In addition feeling more pain of payment candecrease immediate post-purchase satisfaction with a prod-uct (Soster Gershoff and Bearden 2014) These resultsalong with other prior work in the pain of payment litera-ture suggest that less painful forms of payment are associ-ated with positive outcomes during consumer deliberationand purchase (eg increased willingness to purchase aproduct higher willingness to pay for an item greaterpoint-of-purchase satisfaction)

However what happens after the purchase has occurredAlthough past research has demonstrated that attenuatingthe pain of payment can increase spending purchasingand positive evaluations during the consumer deliberationand purchase process it remains largely silent on the im-portant question of implications for post-purchase

outcomes To the best of our knowledge Kamleitner andErki (2013) have conducted the only scholarly researchthat investigates the role that payment form may have onproduct relationships Specifically they examined howpayment form affects attachment and psychological owner-ship of a given product In one study they found correla-tional evidence that those who paid for an item of clothingwith cash report feeling more ownership at time of pay-ment attachment and pain of payment than those whopaid for the item with a credit or debit card however painof payment did not influence the effect of payment modeon ownership when added as a covariate In a second studythey measured whether there are differences in feelings ofpsychological ownership as a function of (1) whether indi-viduals spend replica cash or a replica plastic card topay for a pen and (2) race of participants (Asian vsnon-Asian) In this study they found no main effects ofpayment mode or cultural background on psychologicalownership attachment or pain of payment but they didfind a significant interaction for ownership Non-Asian stu-dents immediately experienced a stronger sense of psycho-logical ownership for the pen when they paid by replicacash than if they had paid by replica card however Asianstudents did not show a difference which the researchershypothesized might be due to Asians viewing credit cardsas a source of investment and debt rather than as a sourceof convenience The role of cultural meanings of differentforms of payment is a very interesting topic that deservesfurther research although it is not the focus of our presentwork

Our research goes beyond Kamleitner and Erki (2013)and other previous work in several key ways First we sys-tematically manipulate the payment forms used acrossstudies (ie cash ldquoplasticrdquo voucher or check) to deter-mine whether the form of the payment has a causal role insignificantly influencing an individualrsquos connection to apurchased product As discussed earlier previous researchhas demonstrated that experiencing less pain of paymentcan have a positive impact on consumers during the delib-eration and point-of-purchase process (eg Chatterjee andRose 2013 Soster et al 2014) thus it is important to deter-mine whether experiencing increased pain of payment canlead to beneficial effects on post-transaction relationshipsSecond whereas past research has focused on ownershipand attachment to products we examine the impact thatpayment form can have on both product and organizationalrelationships Third Kamleitner and Erki (2013) find animmediate difference of payment form on psychologicalownership in their correlational study We look to fill avoid in prior pain of payment literature by investigatinghow different forms of payment influence long-term psy-chological and behavioral connection In particular acrossstudies we vary the time periods after the transaction hasoccurred in order to examine the robustness of the paymenteffect on downstream consumer relationships Fourth and

690 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

finally we examine the theoretical mechanism of the effectmore deeply by looking at the role of pain of paying in therelationship between how one pays and how connected onefeels post-transaction Thus in the sections that follow weextend the pain of payment literature by addressing the po-tential long-term consequences of paying with more or lesspainful forms of payment on post-transaction psychologi-cal and behavioral connection to a product brand andorganization

Pain Value and Commitment

We ground our hypotheses about the relationship be-tween payment form and post-transaction commitment inresearch on the long-term effects of painful experienceTheory and research in multiple disciplines support theidea that painful experiences lead somewhat paradoxi-cally to increased value and commitment (eg Bem 1967Brehm and Self 1989 Festinger 1957 Kivetz andSimonson 2002a Mischel Cantor and Feldman 1996)Research on effort justification and dissonance reductionsuggests that people justify prior feelings of investment byvaluing the chosen outcome more (Aronson 1997 Aronsonand Mills 1959 Cooper and Fazio 1984 Festinger 1957Kahneman Knetsch and Thaler 1991) Gross (1998) ar-gues that people who experience physical or emotionalpain to obtain a particular goal or outcome tend to justifythe pain of their experience psychologically by seeingmore value in the outcome they achieve This psychologi-cal connection between pain and value is consistent withthe price-quality heuristic wherein consumers value ex-pensive products more than cheap products of the samequality (Rao and Monroe 1988 Scitovsky 1945 Stiglitz1987) More expensive products are more painful to pur-chase and to justify this pain they are more valued by con-sumers Research by Koo and Fishbach (2010) suggeststhat even perceived costs can affect consumer expectationsand enjoyment

Applying this theoretical framework to pain of paymentand purchasing we argue that people who pay with morepainful forms of money will be both more psychologicallyand more behaviorally committed to their chosen alterna-tive There is empirical evidence that certain types of paincan influence commitment Regarding psychological com-mitment Aronson and Mills (1959) found that participantswho underwent a more painful and severe initiation to joina group expressed more liking and affiliation for the groupthan those who had a milder initiation or no initiation atall Similar effects have also been noted in consumer re-search (Sheth 1968) Cardozo (1965) demonstrated that ex-erting more effort in order to acquire a product during ashopping task produced more favorable initial evaluationsof the product In a recent and related example MochonNorton and Ariely (2012) found that exerting effort to cre-ate a product disproportionally increased consumersrsquo

valuation for the product Experiencing pain when makinga decision not only increases the attractiveness of the cho-sen alternative but it can also decrease the attractivenessof a rejected alternative (Harmon-Jones and Harmon-Jones2007) Brehm (1956) conducted an experiment where par-ticipants rated the desirability of different products (egtoaster or coffeemaker) The participants were then giveneither a difficult decision (ie choosing between twohighly rated alternatives) or an easy decision (ie choosingbetween one alternative that was rated high and anotherthat had a low rating) After making their choice partici-pants rerated the desirability of the products Individualswho made a psychologically easier or less painful decisiondid not change their ratings between the alternatives Incontrast individuals who made a psychologically more dif-ficult or painful decision rated the chosen option as moreattractive and the nonchosen alternative as less attractive aphenomenon known as spreading of alternatives

Regarding behavioral commitment the attitudes litera-ture suggests that psychological shifts are associated withsubsequent behavioral change congruent with this shift(Ajzen 1991 Fishbein and Ajzen 1975) Evidence for suchattitude-behavior consistency between psychological andbehavioral commitment can be found in among others re-search on the relationship between commitment to onersquosorganization and altruism toward members of that organi-zation (Organ and Ryan 1995) and research by Smith andSwinyard (1983) demonstrating that even a small directcommitment such as a product trial can increase purchasebehavior Given the close relationship between psychologi-cal and behavioral commitment we argue that increasedpain of payment will via its effect on psychological com-mitment lead to increased behavioral commitment as wellSupporting this assertion Doob and colleagues (1969)found that introducing a product at a promotional pricemdasheffectively lowering the pain of paymentmdashmay driveinitial sales but ultimately leads to decreased behavioralcommitment as represented by lower long-term sales

Integrating the previous arguments Figure 1 shows ourconceptual framework regarding the downstream conse-quences associated with the painful elements of a transac-tion We hypothesize that using a more psychologicallyproximal form of payment increases the psychological painof paying just as increasing the magnitude of paymentmakes the transaction feel more painful We furtherhypothesize that the pain of paying will increase post-transaction connection first psychologically in terms ofhow much consumers value their experiences and howcommitted they feel toward the entity they supported withtheir purchase and then behaviorally in terms of howlikely they are to signal support publicly for a cause ormake a repeat donation Regardless of whether one in-creases pain of payment by paying with a more painfulform of payment (while keeping the objective paymentvalue constant) or by paying more money overall (and in

SHAH ET AL 691

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

turn keeping the form of payment constant) we argue thatincreased pain of payment leads the consumer to be morepsychologically and behaviorally committed to a givenproduct or organization

OVERVIEW OF EXPERIMENTS

We conducted four studies to investigate how the psy-chological pain associated with different payment formsaffects psychological connection and subsequent behav-ioral commitment following an economic transaction Weuse a multi-method approach testing our hypotheses usinga field experiment a lab experiment an online experimentand archival data We also operationalize psychologicalcommitment and behavioral commitment in multiple waysemphasizing the broad applicability of our findings Wecategorize any measure that encompasses feelings and in-tentions as psychological value and commitment This in-cludes emotional attachment or feelings of connection to agiven product or brand willingness to accept or estimatedlikelihood of engaging in a future behavior (eg likelihoodto recommend a product or brand) We operationalize be-havioral commitment as any measure that captures an ac-tual observable behavior In the present researchbehavioral commitment specifically refers to wearing a la-pel pin and making a repeated donation to onersquos almamater

In study 1 we manipulate the form of payment used forpurchase in a controlled field experiment We examinewhether paying for a mug increases the psychological con-nection to the mug when the mug is purchased with onersquosown cash compared to when the mug is purchased withonersquos own ldquoplasticrdquo (ie debitcredit or student card)Study 1 also examines whether the effect of paymentmethod on post-transaction psychological connection ismediated by the pain of payment In study 2 a laboratoryexperiment we rule out the potential alternative explana-tions that income effects transaction costs or halo effectsdrive the results Study 2 examines whether the pain ofpaying effect can influence both post-transaction psycho-logical connection and behavioral commitment even when

the individual is spending someone elsersquos money and whenthe objective dollar amount is held constant This studyalso assesses whether paying with a more painful form al-ters the psychological connection for nonchosen alterna-tives In study 3 an online experiment we manipulate theprocess by which these effects occur by increasing the painof payment via both payment form and payment magni-tude in order to determine whether an increase in peoplersquospsychological commitment is due just to differences in thepayment form or more broadly to pain of payment fromany source (eg higher payment amount holding formconstant) Finally in study 4 we use archival donation datato investigate how the pain of payment influences post-transaction behavioral commitment in a real-world settingon a longer time horizon by measuring repeat donationlikelihood as a proxy for post-transaction connectionSpecifically we examine whether (1) donating in year t bycheck a more painful form of payment versus donatingusing a creditdebit card or (2) donating a larger amount ofmoney in year t increases the likelihood of donating in yeartthorn 1 Study 4 also tests whether the pain of paying effect isrobust over time in a domain that has meaningful economicconsequences Figure 2 provides a graphical summary ofthe theoretical paths that the different studies test

STUDY 1 MUG FIELD EXPERIMENT

Study 1 investigates whether paying with a more painfulform of payment increases how much consumers value aproduct after the transaction is completed To establish thatthere is a causal relationship between payment form andpost-transaction psychological value and connection wemanipulate whether consumers pay for a mug using cash orplastic card We then examine whether paying by cash in-creases the perceived value of the mug as measured by theparticipantrsquos subsequent willingness to accept the amountfor the purchased mug (ie the endowment effect) and bypurchasersrsquo rated post-transaction psychological connec-tion as measured by their emotional attachment toward themug We also examine whether the psychological pain as-sociated with payment mediates the relationship between

FIGURE 1

THE IMPACT OF PAYMENT FORM AND MAGNITUDE ON PSYCHOLOGICAL AND BEHAVIORALCOMMITMENT THROUGH PAIN OF PAYING

692 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

payment form and post-transaction perceived value andconnection

Method

Procedure and Design The study experimenter ap-proached 98 employees of a private southeastern univer-sity asking each if they would like to purchase a mug Themug was dark blue and displayed a university logoIndividuals were informed that the mug normally sold for$695 but was discounted to $2 as part of a promotionIndividuals were randomly assigned to one of two

experimental conditions In the Pay by Cash condition in-dividuals were told that they could only purchase the mugwith cash In the Pay by Plastic condition individuals weretold that they could only purchase the mug with a creditcard debit card or a prepaid university card commonlyused on campus The experimental manipulation did notsignificantly affect the proportion of the 98 potential par-ticipants who chose to purchase a mug (Propcashfrac14 60Propplasticfrac14 67 v2(1)frac14 26 pfrac14 61) which we attributeto the mugrsquos deeply discounted price (Shah et al 2015) Atotal of 63 people purchased a mug 32 in the Pay by Cardcondition and 31 in the Pay by Plastic condition

FIGURE 2

THE IMPACT OF PAYMENT FORM AND MAGNITUDE ON PSYCHOLOGICAL AND BEHAVIORAL COMMITMENTTHROUGH PAIN OF PAYING ACROSS EMPIRICAL STUDIES

SHAH ET AL 693

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

Approximately two hours after the transaction the experi-menter approached everyone who purchased a mug andasked them to complete a follow-up survey

Measures The independent variable in our analysis isPaid by Cash a dummy variable that indicates whether theparticipants used cash (Paid by Cashfrac14 1) or a form of plas-tic (Paid by Cashfrac14 0) to pay for their purchase As de-scribed earlier participants were randomly assigned to payby cash or by plastic they did not choose their form ofpayment Individuals who were instructed to pay by plasticwere allowed to pay using a debit credit or prepaid uni-versity card that was commonly accepted across campusWe asked the follow-up questionnaire to all participantswho purchased a mug (nfrac14 63) excluding the 35 partici-pants who did not make a purchase

The dependent and mediating variables were measuredon a post-transaction questionnaire We measuredPsychological Connection with two questions First weasked participants ldquoHow emotionally attached are you tothe mugrdquo (1frac14Not at all 7frac14Very attached) Second weasked the participants about the minimum price that theywould demand to give up their mug (eg their ldquowillingnessto acceptrdquo) We standardized and then averaged these mea-sures to produce an index of psychological value and con-nection (rfrac14 404 pfrac14 001)

The mediating variable is Pain of Payment Pain is tradi-tionally measured in both medical and nonmedical set-tings with single-item measures (see eg ChristianEisenkraft and Kapadia 2015 Soster Gershoff andBearden 2014 Thomas Desai and Seenivasan 2011Wong and Baker 1988) Accordingly participants de-scribed their pain by answering this question ldquoHow painfulwas paying for the mug when you originally bought itrdquo(1frac14Not at all 7frac14Very painful) Data from a separate on-line sample confirmed that responses to this question corre-late very highly (rfrac14 72 nfrac14 201 plt 001) with responsesto an adapted form of the widely used Wong and Baker(1998) Faces Pain Rating scale where people identify thecartoon face that best corresponds to their current feelingof pain (Soster et al 2014 Thomas et al 2011)

Results

We analyze the data in two stages We first investigatewhether the experimental manipulation had the predictedeffect on the Psychological Connection dependent variableWe then test whether the manipulation affected Pain ofPayment and whether Pain of Payment mediates the exper-imental manipulationrsquos effect on PsychologicalConnection

Effects of Payment Form Payment form significantlyinfluenced post-transaction valuation Individuals who paidwith cash expressed more Psychological Connection incomparison to those who paid with plastic (Mcashfrac14 046

standard deviation [SD]cashfrac14 071 Mplasticfrac14048SDplasticfrac14 068 t(610)frac14 533 plt 001 see Figure 3)This effect is both significant and relatively large in termsof economic impact To illustrate the size of this effectconsider the willingness to accept question which wasmeasured in dollars The participants in the Cash conditionasked for an average of $671 (SDfrac14 $163) to sell the mugback whereas the participants who paid with plastic askedfor only $383 (SDfrac14 $179)

Pain of Payment Before testing for mediation we as-sessed whether the experimental manipulation influencedthe participantrsquos subjective Pain of Payment ratings As ex-pected participants who paid by cash self-reported morepain than individuals who paid by plastic (Mcashfrac14 409SDcashfrac14 145 Mplasticfrac14 210 SDplasticfrac14 147 t(609)frac14544 plt 001)

Mediation Analysis We assessed whether Pain ofPayment mediates the relationships between paymentformmdashthe experimental manipulationmdashand thePsychological Connection dependent variable We usedstructural equation models and bootstrap analysis to testthe significance of the mediation (Zhao Lynch and Chen2010) A 1000-draw bootstrap suggested that Pain ofPayment significantly mediates the effect of paying bycash on Psychological Connection (Indirect effect of pay-ing by cashfrac14 031 standard error [SE]frac14 011 zfrac14 276pfrac14 006 direct effectfrac14 062 SEfrac14 021 zfrac14 303pfrac14 002) Using the language of Zhao et al (2010) thispattern of results provides evidence of ldquocomplementarymediationrdquo

Discussion of Study 1

Study 1 suggests that payment form influences the psy-chological connection individuals feel toward their chosenoption The subjective pain associated with paying medi-ated this effect Holding the price of the item constant thepsychological pain of payment increased the psychologicalconnection consumers felt toward the product theypurchased

Study 1 has several limitations First we used self-reportmeasures of post-transaction psychological connection andwere not able to assess the behavioral consequences ofpayment form Second the participants had to spend theirown money in order to participate in study 1 Although $2should be too small to create wealth and income effectswe do not know whether having people pay for the mugscreated a biased sample of participants given that we onlymeasure those who chose to purchase the mug In otherwords we do not know anything about people who did notwant a mug In addition there may also be economic dif-ferences across payment forms For example credit cardusers who have rewards points or have cash back programsmay in fact be paying less than $2 Similarly it is possible

694 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

that cash users may have limited cash available in theirwallet and thus might have to incur an automatic teller ma-chine (ATM) fee or might perceive additional transactioncosts by making an additional trip to the ATM in order tomake the cash payment For these cash users $2 may feelgreater than $2 due to these additional costs Third halo ef-fects might also be driving the results individuals may notfeel more connected to their purchases per se but ratherthey may simply have a more positive impression of theirpurchase (Nisbett and Wilson 1977) To overcome theselimitations study 2 uses a controlled laboratory experimentto examine whether donating someone elsersquos money in-creases psychological connection in turn increasing behav-ioral commitment Study 2 also tests whether increasingthe pain of payment affects connection to just the chosenalternative or whether the pain of payment also influencesconnection to the nonchosen alternatives

STUDY 2 CHARITY LABORATORYEXPERIMENT

In study 2 we test whether having individuals use moreor less painful forms of payment (ie $5 cash or a $5voucher) affects psychological connection to a chosencharity and subsequently influences behavioral commit-ment even when the donated money is not their own Inaddition we test whether psychological connection to thenonchosen alternatives is influenced by payment form We

hypothesize that increasing the pain of payment will (1) in-crease both psychological connection and behavioral com-mitment to the chosen alternative and (2) decreasepsychological connection to the nonchosen alternativesWe measure psychological connection by asking partici-pants to complete self-report measures We measure be-havioral commitment by measuring whether participantswear a ribbon lapel pin from their chosen charity one weekfollowing their initial donation (Baca-Motes et al 2013)

Method

Participants A total of 94 undergraduates (617 fe-male) from a southeastern university participated in thisbetween-subjects experiment

Experimental Manipulation The participants were ran-domly assigned to one of two payment form conditionsHalf of the participants donated to one of three charitiesusing a five-dollar bill the other half donated using a five-dollar voucher The five-dollar voucher had the same di-mensions as the five-dollar bill (614 inches long 261inches wide 004 inches thick) so as to limit potentialconfounds due to differences inferred from the size of thepayment modes

In order to rule out wealth effects none of the partici-pants in this study donated their own money However wehypothesize that transactions conducted with another per-sonrsquos money will still lead people to experience feelings of

FIGURE 3

PSYCHOLOGICAL COMMITMENT AS A FUNCTION OF PAYMENT FORM STUDY 1

SHAH ET AL 695

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

pain although the effect is likely to be smaller This beliefis grounded in research showing that conscious and non-conscious primes influence downstream behavior (LangBradley and Cuthbert 1998 Leventhal and Tomarken1986 Zemack-Ruger Bettman and Fitzsimons 2007)According to this literature concepts may be stronglylinked with specific feelings and behaviors Invoking thoseconcepts activates the associated memories and behaviorsregardless of whether the concept was consciously or sub-jectively experienced Extending this paradigm to the pre-sent study we argue that the concept of paying money isautomatically associated with pain of payment feelingsTherefore we expect that individuals who spend other peo-plersquos moneymdasheven though they do not personally experi-ence an economic lossmdashwill still experience pain via theautomatic association between payment and the subjectivepain associated with a particular payment form

Procedure and Design Participants arrived at the laband were informed that they would be taking part in a two-part study involving problem solving and evaluating threedifferent charities Upon entering the lab participants weregiven $7 (in the form of a $5 bill and two $1 dollar bills) aspayment for their participation in the study plus either anadditional $5 cash or a $5 voucher which they were toldexplicitly would be given to one of three charities of theirchoice during the second part of the experiment on behalfof the school Having participants donate money that wasnot theirs reduced concerns that wealth effects or transac-tion costs were driving the relationship between the pain ofpayment and post-transaction connection

Following the completion of the unrelated filler taskparticipants were told that they would have a chance to do-nate the $5 cashvoucher to one of three charities CancerResearch Institute Earthworks (an environmental organi-zation) or Elizabeth Glaser Pediatric AIDS FoundationAll charities are real and recently received an ldquoArdquo ratingfrom an annual charity review (httpwwwcharitywatchorgtopratedhtml) thus they did not differ in terms ofquality or effectiveness Individuals were then given threeclasp envelopes with a one-page description pasted on thefront for each charity The description for each charity wasprovided in order to ensure that the information was similaracross choices (see the online appendix for descriptions)

Participants were instructed to donate to their preferredcharity by placing their $5 cashvoucher into the associatedenvelope They could not give any more (or less) than $5and could not split the money up between one or morecharities The participants were then given a questionnaireasking them about their feelings toward the charity Thequestionnaire measured the participantrsquos post-transactionpsychological connection and positivity (see below fordetails)

After completing the questionnaire individuals weregiven a small ribbon lapel pin as a token of appreciation

from the charity organization The ribbon lapel pins wereidentical in shape and size but varied by color A purple la-pel pin corresponded to a donation to the Cancer ResearchInstitute a green lapel pin corresponded to a donation toEarthworks and a red lapel pin corresponded to theElizabeth Glaser Pediatric AIDS Foundation

One week after the experiment all participants wereemailed a follow-up questionnaire The email againthanked the participants for their participation Participantswere also informed that the charity (which remainedunspecified so that everyone could receive the same email)had a few follow-up questions This follow-up question-naire included our behavioral measures of commitment

Measures There are two sets of measures in this studyThe psychological variables were measured in the post-donation questionnaire the behavioral variables were mea-sured in the follow-up questionnaire that participantsreceived one week after the experiment

The post-donation questionnaire measured severalitems using 7 point scales (1frac14Strongly disagree7frac14Strongly agree) First the participants described theirPsychological Connection with a 3 item scale The scaleitems asked about the participantrsquos connection to the char-ityrsquos values and mission their estimated likelihood of rec-ommending the charity to a friend and their estimatedlikelihood of donating in the future to the charity(Cronbach afrac14 93) We consider the questions that referto an ldquoestimated likelihoodrdquo to be measures of psycholog-ical rather than behavioral connection because even themost sincere intentions do not always translate into actualbehaviors Second the participants described thePositivity of the charity with a 4 item scale The items onthis scale asked participants about the charityrsquos compe-tence genuineness efficiency and whether it will fulfillits goals (Cronbach afrac14 933) We measured the positivityrating of each charity to rule out the alternative explana-tion of a halo effect regarding the participantrsquos chosencharity (Nisbett and Wilson 1977) These two scales ex-hibited discriminant validity as per Fornell and Larckerrsquos(1981) test the average variance extracted (AVE) for thetwo latent constructs (AVE for commitmentfrac14 075 AVEfor positivityfrac14 070) is greater than the variance sharedby those latent constructs (Shared variancefrac14 048)Participants completed these two scales three times oncefor each of the three charities

The follow-up questionnaire asked about the partici-pantrsquos post-experiment behavior To measure post-transac-tion behavioral connection we asked participants if theywore their lapel pin during the last week (Binary outcomeYesNo) and how many days they wore the pin (1frac14 1 day2frac14 2ndash3 days 3frac14 4ndash5 days 4frac14 6thorn days) Unrelated to thepresent research we also asked the participants if theythought the charity should continue giving out ribbon pinsto donors (Binary outcome YesNo)

696 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

Results

Post-Donation Questionnaire First looking atPsychological Connection we found that individuals whodonated to charity using $5 cash felt significantly more psy-chological connection to their chosen charity than partici-pants who donated using a $5 Voucher (Mcashfrac14 581SDcashfrac14 088 Mvoucherfrac14 532 SDvoucherfrac14 129t(810)frac14 215 pfrac14 034) We also found that individualswho donated using $5 Cash felt significantly less committedto their nonchosen alternatives (using the average of the twononchosen alternatives) than those who donated to charityusing a $5 Voucher (Mcashfrac14 389 SDcashfrac14 110Mvoucherfrac14 456 SDvoucherfrac14 127 t(902)frac14277 pfrac14 007see Figure 4) Second we used the Positivity measure to in-vestigate whether payment form influences post-transactionPsychological Connection rather than producing a moregeneralized halo effect Unlike the PsychologicalConnection measure we found no evidence that individualswho donated via cash viewed their chosen charity morepositively than those who donated by voucher (Mcashfrac14586 SDcashfrac14 085 Mvoucherfrac14 576 SDvoucherfrac14 111t(863)frac14 46 pfrac14 64) Payment form also did not signifi-cantly influence positivity measures for the nonchosen alter-natives (Mcashfrac14 528 SDcashfrac14 092 Mvoucherfrac14 536SDvoucherfrac14 106 t(903)frac14403 pfrac14 69)

Post-Transaction Behavioral Commitment (ie Wearinga Lapel Pin) Of the initial 94 participants 68 respondedto the email survey (ncashfrac1439 nvoucherfrac1429) Consistent

with our hypothesis individuals who donated by cash in-stead of voucher were both significantly more likely to re-port wearing the lapel pin after one week (v2(1)frac14 866pfrac14 003 Mcashfrac14 513 Mvoucherfrac14 138) and reportedwearing the lapel pin more frequently (Mcashfrac14 131SDcashfrac14 164 Mvoucherfrac14 048 SDvoucherfrac14 127 t(658)frac14233 pfrac14 023 see Figure 5) Finally a mediation analysissuggests that increased Psychological Connection towardthe chosen alternatives mediated the effect of paymentmethod on the post-transaction behavioral commitmentmeasure (direct effectfrac14 023 SEfrac14 012 zfrac14 184pfrac14 0065 indirect effectfrac14 015 SEfrac14 007 zfrac14 213pfrac14 0033) This result suggests that payment form influ-enced post-transaction psychological connection whichthen influenced the likelihood to demonstrate post-transac-tion behavioral commitment via publicly signaling supportfor the charity

Discussion of Study 2

The results of study 2 suggest that a more transparentpayment form (cash) increases the degree of connection tothe chosen alternative beyond that associated with a lesstransparent form (voucher) even when people pay withsomeone elsersquos money Furthermore paying with cash in-creased the propensity to signal their connection publiclyand decreased the psychological connection toward thenonchosen alternatives Study 2 also ruled out two poten-tial alternative explanations for the relationship between

FIGURE 4

PSYCHOLOGICAL CONNECTION RATINGS FOR CHOSEN ALTERNATIVE AND NONCHOSEN ALTERNATIVESAS A FUNCTION OF PAYMENT FORM STUDY 2

SHAH ET AL 697

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

payment form and post-transaction connection First sinceparticipants were donating someone elsersquos money wealtheffects or transaction costs are not driving the relationshipbetween pain of payment and post-transaction connectionSecond given that payment form did not lead to significantdifferences between positivity measures the pain of pay-ment effects cannot be attributed to a halo effect

One of the limitations of study 2 is that we did not mea-sure pain of payment the mediating variable that couldbetter reveal whether the participants in the Cash conditionwere more committed because they experienced more painThis is a limitation because the participants in study 2 werespending someone elsersquos money and therefore may nothave experienced as much pain as people who spend theirown money We thank the anonymous reviewers for point-ing out this oversight Thus we do not have direct evidencefor the role of pain of payment in this study and our con-clusions regarding the process therefore must be morespeculative for study 2 However we do have direct evi-dence for the role of pain of payment in both study 1 andstudy 3

STUDY 3 ONLINE EXPERIMENTMANIPULATING FORM AND

MAGNITUDE

In study 3 we examine whether post-transaction connec-tion is driven by an effect specific to payment form or

rather as we theorized by any variable that increases thepain of payment Specifically study 3 tests whether post-transaction connection increases when pain of payment ismanipulated via either changes in payment form (as in theprevious two studies) or changes in payment magnitudeBecause we previously argued that post-transaction con-nection is related to pain of payment we hypothesize thatpaying with cash (vs a debit card) and paying more money($20 vs $10) will both increase the pain of paying therebyincreasing the psychological connection to a chosenalternative

Method

Participants We recruited 189 paid volunteers (423female) using Amazonrsquos Mechanical Turk online-surveysampling site to participate in this between-subjects experi-ment All participants were over the age of 18 and citizensof the United States

Experimental Manipulation This study had a 2 (pay-ment form cash or Visa debit card) 2 (payment magni-tude $20 or $10) between-subjects design Participantswere given a scenario where they chose a pair of head-phones to use for a business trip They were then randomlyassigned to one of four payment conditions describingwhat form was used and the amount of money that he orshe paid for the headphone purchase $20 using cash $20using a Visa debit card $10 using cash or $10 using aVisa debit card

FIGURE 5

PROPORTION WEARING A LAPEL PIN AFTER ONE WEEK AS A FUNCTION OF PAYMENT FORM STUDY 2

698 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

Procedure and Design All participants were told toimagine that they would be purchasing a new pair of head-phones to use on an upcoming business trip they thenwent through a detailed vignette styled like a picture bookParticipants were presented with information on three pairsof identically priced headphones with different featuresThey chose one pair to purchase Participants were thentold to imagine bringing their chosen pair of headphones tothe checkout counter to pay for the purchase At this pointparticipants were randomly assigned to one of the four pay-ment conditions $20 using cash $20 using a Visa debitcard $10 using cash or $10 using a Visa debit cardParticipants in different experimental conditions saw animage showing the form of payment and amount of moneyassociated with their experimental condition All partici-pants were then asked ldquoHow painful was paying for theheadphones (ie how painful was giving up your mon-ey)rdquo (1frac14Not at all painful 5frac14Very painful) After an-swering this question all participants clicked through thesame picture book vignette where they were told that theyused their headphones while running errands prior to theirtrip while they were in the airport and during the flight asthey were heading to their business trip and when they re-turned home from their business trip At the conclusion ofthe vignette participants completed a purchase experiencequestionnaire regarding their headphones The purchaseexperience questionnaire measured the participantrsquos post-transaction psychological connection

Dependent Variable In addition to the pain measuredescribed earlier (the proposed mediator) participantsrated how emotionally attached they were to their head-phones (1frac14Not at all attached 5frac14Very attached) andhow likely they were to recommend the headphones to afamily member or friend (1frac14Very unlikely 7frac14Verylikely) We created a measure of Psychological Connectionby standardizing and then averaging the responses from thetwo items (rfrac14 43 p lt001)

Results

We analyzed the data in two stages We investigatedwhether the experimental manipulations had the predictedeffect on the dependent variable of PsychologicalConnection whether the manipulation affected the Pain ofPayment mediator and whether Pain of Payment mediatesthe experimental manipulationrsquos effect on the dependentvariable

Effects on Psychological Connection The experimen-tal manipulations of payment form and payment magnitudeboth significantly influenced Psychological ConnectionRegarding payment form individuals who imagined pay-ing with cash reported significantly higher PsychologicalConnection than participants who paid with plastic regard-less of payment magnitude (Mcashfrac14 016 SDcashfrac14 084

Mplasticfrac14015 SDplasticfrac14 084 F(1 185)frac14 450pfrac14 009) These effects are consistent with our hypothesisand replicate the results from the first two experimentsRegarding payment magnitude individuals who imaginedpaying more money ($20) regardless of payment form re-ported significantly higher levels of psychologicalconnection than participants who paid less money(M$20frac14 022 SD$20frac14 095 M$10frac14023 SD$10frac14 066F(1 185)frac14 1498 plt 001) The interaction effect of pay-ment form and payment magnitude on PsychologicalConnection was not significant F(1 185)frac14 159 pfrac14 12Mcash$20frac14 028 Mplastic$20frac14 015 Mcash$10frac14 002Mplastic$10frac14048)

Effect on Pain of Payment Before testing for media-tion we assessed whether the experimental manipulationinfluenced the participantrsquos subjective Pain of Payment rat-ings As predicted participants who paid by cash reportedmore pain than individuals who paid by plastic(Mcashfrac14 198 SDcashfrac14 107 Mplasticfrac14 156 SDplasticfrac14 73F(1 185)frac14 121 plt 001) Also consistent with classiceconomic theory participants who paid more money self-reported experiencing more pain than individuals who paidless money (M$20frac14 213 SD$20frac14 100 M$10frac14 137SD$10frac14 66 F(1 185)frac14 392 plt 001) As withPsychological Connection the interaction between pay-ment form and payment magnitude did not have a signifi-cant effect on Pain of Payment F(1 185)frac14 133 pfrac14 25Mcash$20frac14 241 Mplastic$20frac14 186 Mcash$10frac14 151Mplastic$10frac14 123)

Mediation Analysis We assessed whether Pain ofPayment mediates the relationships between the two ma-nipulated variablesmdashPay by Cash and PaymentMagnitudemdashand Psychological Connection We usedstructural equation models and bootstrap analysis to testthe significance of the mediation (Zhao et al 2010) A1000-draw bootstrap suggested that Pain of Payment sig-nificantly mediates both the effect of Pay by Cash onPsychological Connection (Indirect effect of paying bycashfrac14 010 SEfrac14 004 zfrac14 262 pfrac14 009 direct ef-fectfrac14 021 SEfrac14 012 zfrac14 176 pfrac14 078) and the effect ofPayment Magnitude (Indirect effect of increased paymentmagnitudefrac14 017 SEfrac14 005 zfrac14 325 plt 001 direct ef-fectfrac14 028 SEfrac14 014 zfrac14 206 pfrac14 040) Using the lan-guage of Zhao et al (2010) there is evidence of anldquoindirect-only mediationrdquo for the relationship betweenPayment Form Pain of Paying and PsychologicalConnection and a relationship of ldquocomplementary media-tionrdquo between Payment Magnitude Pain of Paying andPsychological Connection

Discussion of Study 3

The results of study 3 replicate and extend the results ofthe previous studies in three ways First we provide

SHAH ET AL 699

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

additional evidence that the relationship between paymentform and post-transaction psychological connection is me-diated by feelings of subjective pain Second we find thatmanipulating payment form and payment magnitude havea similar effect on ratings of pain and post-transaction psy-chological connection These results suggest that manipu-lating the pain of paymentmdasheither through payment formor payment magnitudemdashincreases post-transaction psycho-logical connection Thus the effect on post-transaction con-nection is not unique to payment form

Study 3 also shares some of the limitations of study 1and study 2 Specifically all of these studies looked atrelatively low-value purchases and relatively short time-horizons The participants in study 1 purchased a $2 mugand were surveyed a few hours later the participants instudy 2 donated $5 to charity and were surveyed a weeklater the participants in study 3 imagined paying for head-phones and were asked about their psychological connec-tion approximately 10 minutes later The goal of study 4 isto provide real-world evidence that people who pay with amore painful form of money tend to exhibit longer termconnection and commitment demonstrated by their likeli-hood to make a repeat transaction

STUDY 4 ARCHIVAL DONATIONDATA ANALYSIS

Study 4 investigates the relationship between howalumni pay for a charitable donation to their alma materand their probability of making future donationsSpecifically we use an archival data set of alumni dona-tions to assess whether increasing the pain of payment bypaying with a more painful form of payment or by payingmore money in year t is associated with an increased prob-ability of donating again in year tthorn 1 Alumni donationsprovide a suitable context for testing our hypothesis aboutthe relationship between pain of payment and post-transac-tion connection because making a repeat donation is a clearmeasure of behavioral commitment to onersquos organization

Data and Variables

The alumni donations database includes informationabout all of the donations alumni contributed to a top-ranked business school between 2005 and 2013 Acrossthese nine years 9482 alumni had 71110 opportunities tomake a yearly donation to their alma mater and made a to-tal of 35113 donations The total number of donation op-portunities is 71110 rather than 85338 (9482 alumni 9donation years) because alumni do not enter the databaseuntil after they graduate

Alumni Information The data set includes informationabout alumni who donated to their business school Thedummy variable Male equals 1 if the donor is male

Graduating Class indicates the year that the donor gradu-ated from the university and the dummy variable AttendsReunions indicates whether the alumnus(a) attended any ofthe schoolrsquos reunions We include this reunion informationin our analysis as a control variable because previous re-search suggests that people who attend reunions are morelikely to donate to their university (Netzer Lattin andSrinivasan 2008)

Donation Opportunity Information The data set alsoincludes information about what the 9482 alumni did dur-ing the 71110 opportunities they had to make a yearly do-nation For each donation opportunity we use a dummyvariable Donated in Year t to indicate whether or not thealumnus(a) made a donation during that fiscal year thelogarithm plus one of the total Donation Value the alum-nus(a) contributed during that year and a series of dummyvariables to indicate the Donation Year The outcome vari-able is Future Donation a dummy variable that indicateswhether the donor made a donation in year tthorn 1

Importantly we also have information about how the do-nors paid for each donation In this data set the more pain-ful form of donation payment is paying by check whereasthe less painful form is paying by debit or credit card(Soman 2003) Although this database does not distinguishwhether a debit or credit card (ie plastic) was used tomake a particular card donation prior research suggeststhat both types of card payments are relatively low-painforms of payment in comparison to checks (Soman 2003)A small percentage of the donations were also made usingother nontraditional payment forms (eg wire transferstock gifts etc)

Analytical Strategy We had to make a series of deci-sions about how to best test our hypotheses To be as trans-parent as possible we discuss all of the analyticalstrategies we considered and why we eventually settled onour chosen alternative

The initial analytical strategy considered was to studyhow more painful forms of payment influence future dona-tion behavior with panel analysis Panel analysis would al-low us to assess the relationship between within-personvariations in payment forms and variations in future dona-tion behavior while also controlling for any individual dif-ferences that may create between-person differences in thepredictor or outcome variable (Hagenaars 1990 Kesslerand Greenberg 1981) Unfortunately the archival data arenot amenable to this analytical strategy Our review of thedata revealed that most alumni always used the same pay-ment formmdashgreatly reducing the power of our analysismdashand the few alumni who switched tended to make theirearly donations with checks and then switch to some formof plastic for their later donations This trend suggests thatany changes in payment form decision may be a proxy fora third unmeasured variable that may also be related to do-nation behavior Thus with a restricted sample and

700 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

endogeneity concerns we concluded that the data were notamenable to studying whether within-person changes inpayment form cause changes in future donation behaviorHowever with causality established by the experiments instudies 1 2 and 3 we felt that the archival data couldstill provide a real-world replication of the relationship be-tween payment form and post-transaction behavioralcommitment

We test our hypotheses by comparing the future dona-tion behaviors of the 2057 alumni who make all of theirdonations via check to the 4041 alumni who make all oftheir donations via plastic Because every donation isnested within an alumnus these analyses required a multi-level model Specifically the model must assess whether acharacteristic of the alumnimdashthat is whether they pay bycash or cardmdashinfluences the loyalty created by making adonation while also accounting for the interdependence in-herent in the data How to best model this interdependenceis not a trivial question because different communities ofscholars recommend different approaches to multileveldata Econometricians often put extensive thought intohow to properly model the interdependence among the er-ror terms to improve the robustness of the estimators andto correct potential issues of endogeneity Scholars fromthis tradition would most likely recommend that we testour hypotheses with fixed-effect models they would onlyrecommend random effects when a Hausman-style test(Hausman 1978) confirms that the random effects areuncorrelated with the predictors (Mundlak 1978)Statisticians in contrast are more likely to use ldquomixed-effectsrdquo models that use random effects to model interde-pendence and fixed-effects parameters to estimate therelationships between the predictors and the outcome(Gelman and Hill 2006) In this tradition the decision tomodel interdependence with random rather than fixed ef-fects is often based on whether the people in the data canbe considered a suitably random sample of a larger popula-tion of interest (Pinheiro and Bates 2000) Interdependence

between the predictors and the random effects is not neces-sarily a limitation of mixed-effects models Instead one ofthe features of these models is that they allow researchersto estimate the effects of predictors that both do and do notvary within-person

Given these differences we decided to use a mixed-effects model for three reasons First we would like tomodel how the individual-level characteristics of the donorsinfluence donation behavior because these associations willreplicate the findings of previous studies Second we wouldlike to use our sample of data to make inferences about thelarger population of alumni at similar institutions ratherthan restrict our estimate to the population at hand Thirdwe are not interested in trying to establish causality withthese data the primary focus of most econometricsapproaches However we acknowledge that other re-searchers may strongly prefer a fixed-effects approachTherefore we also test whether fixed-effects models pro-duce similar results to those from the mixed-effects model

Results

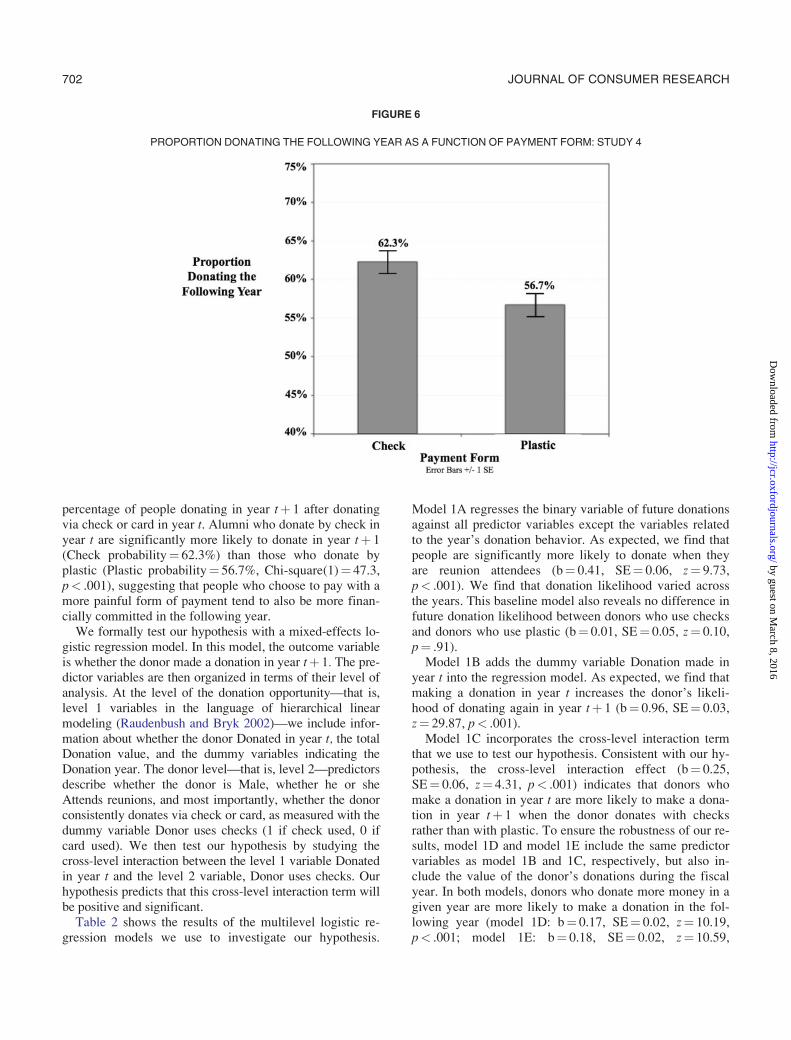

Table 1 shows the descriptive statistics for the alumniwho donate via check and via plastic In addition to high-lighting some of the differences between these groups ofalumnimdashfor example the alumni who use checks tend tobe older and less likely to attend reunionsmdashthese descrip-tive statistics are consistent with both prior research onpain of payment and our hypotheses We see that the painof payment reduces the likelihood of initiating a donationcompared to donors who use plastic donors who usechecks to make donations are less likely to start making do-nations in year t thorn 1 if they have not made a donation inyear t (Plastic probabilityfrac14 216 Check probabil-ityfrac14 189 Chi-square(1)frac14 231 plt 001) Consistentwith our hypothesis the descriptive statistics also suggestthat more painful forms of payment have a positive effecton future financial commitment Figure 6 reflects the

TABLE 1

DESCRIPTIVE STATISTICS FOR DONOR AND DONATION CHARACTERISTICS STUDY 4

All alumni Alumni who use plastic Alumni who use checks

Donor characteristicsMale 73 74 72Graduating class 19995 20024 19938Attends reunions 18 20 13Donor uses checks 34 0 100Donation characteristicsLog(donation value thorn 1) 223 234 202Donates in year tthorn1 36 35 36Donates in year tthorn1 after donating in year t 59 57 62Donates in year tthorn1 after not donating in year t 21 22 19

SHAH ET AL 701

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

percentage of people donating in year tthorn 1 after donatingvia check or card in year t Alumni who donate by check inyear t are significantly more likely to donate in year tthorn 1(Check probabilityfrac14 623) than those who donate byplastic (Plastic probabilityfrac14 567 Chi-square(1)frac14 473plt 001) suggesting that people who choose to pay with amore painful form of payment tend to also be more finan-cially committed in the following year

We formally test our hypothesis with a mixed-effects lo-gistic regression model In this model the outcome variableis whether the donor made a donation in year tthorn 1 The pre-dictor variables are then organized in terms of their level ofanalysis At the level of the donation opportunitymdashthat islevel 1 variables in the language of hierarchical linearmodeling (Raudenbush and Bryk 2002)mdashwe include infor-mation about whether the donor Donated in year t the totalDonation value and the dummy variables indicating theDonation year The donor levelmdashthat is level 2mdashpredictorsdescribe whether the donor is Male whether he or sheAttends reunions and most importantly whether the donorconsistently donates via check or card as measured with thedummy variable Donor uses checks (1 if check used 0 ifcard used) We then test our hypothesis by studying thecross-level interaction between the level 1 variable Donatedin year t and the level 2 variable Donor uses checks Ourhypothesis predicts that this cross-level interaction term willbe positive and significant

Table 2 shows the results of the multilevel logistic re-gression models we use to investigate our hypothesis

Model 1A regresses the binary variable of future donationsagainst all predictor variables except the variables relatedto the yearrsquos donation behavior As expected we find thatpeople are significantly more likely to donate when theyare reunion attendees (bfrac14 041 SEfrac14 006 zfrac14 973plt 001) We find that donation likelihood varied acrossthe years This baseline model also reveals no difference infuture donation likelihood between donors who use checksand donors who use plastic (bfrac14 001 SEfrac14 005 zfrac14 010pfrac14 91)

Model 1B adds the dummy variable Donation made inyear t into the regression model As expected we find thatmaking a donation in year t increases the donorrsquos likeli-hood of donating again in year tthorn 1 (bfrac14 096 SEfrac14 003zfrac14 2987 plt 001)

Model 1C incorporates the cross-level interaction termthat we use to test our hypothesis Consistent with our hy-pothesis the cross-level interaction effect (bfrac14 025SEfrac14 006 zfrac14 431 plt 001) indicates that donors whomake a donation in year t are more likely to make a dona-tion in year tthorn 1 when the donor donates with checksrather than with plastic To ensure the robustness of our re-sults model 1D and model 1E include the same predictorvariables as model 1B and 1C respectively but also in-clude the value of the donorrsquos donations during the fiscalyear In both models donors who donate more money in agiven year are more likely to make a donation in the fol-lowing year (model 1D bfrac14 017 SEfrac14 002 zfrac14 1019plt 001 model 1E bfrac14 018 SEfrac14 002 zfrac14 1059

FIGURE 6

PROPORTION DONATING THE FOLLOWING YEAR AS A FUNCTION OF PAYMENT FORM STUDY 4

702 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

plt 001) Controlling for the donation value does notchange the direction or significance of the cross-level inter-action effect the primary result of interest (bfrac14 030SEfrac14 006 zfrac14 519 plt 001)

As discussed earlier we also tested our hypotheses usingthe fixed-effects approach preferred by econometriciansThese models are not able to estimate the simple effects ofdonor-level variables such as whether the donor is Malewhether he or she Attends reunions and whether the Donoruses checks all of the variance that could be explained bythese donor-level variables is already accounted for by themodelrsquos fixed effects The models can however estimatethe effects of the donation-level variables and most impor-tantly the cross-level interaction relevant to ourhypotheses

Table 3 shows the results of the fixed-effect models Asin the previous analyses we find support for our hypothesisusing models that both do and do not include the size ofthe donation Model 2C does not include a donation sizecontrol Following a donation in year t the results of this

model suggest that check-using donors are significantlymore likely to make a year tthorn 1 donation than card-usingdonors (Donation in year tDonor uses checks bfrac14 013SEfrac14 006 pfrac14 041) We find the same pattern of results inmodel 2E the model that includes the donation size con-trol Controlling for the size of the donation we again findthat check-using donors are more likely than card-usingdonors to follow up a donation with a second donation(Donation in year tDonor uses checks bfrac14 015SEfrac14 006 pfrac14 016) It is worth noting that making a largerdonation in year t (ie increasing the payment magnitudeof the donation) is also associated with an increased likeli-hood of donating in the following year which is consistentwith our hypotheses and prior evidence from study 3

Discussion of Study 4

Study 4 extends the experimental findings from the firstthree studies by providing a real-world replication of therelationship between payment form payment magnitude

TABLE 2

MIXED-EFFECTS MODEL RESULTS STUDY 4

Model 1A Model 1B Model 1C Model 1D Model 1E

Intercept 304 829 731 800 680(026) (023) (023) (023) (023)

Donor-level variablesMale 002 001 001 000 000

(006) (004) (004) (004) (004)Graduating class 00013 00047 00041 00045 00039

(00001) (00001) (00001) (00001) (00001)Attends reunions 041 036 036 032 032

(006) (005) (005) (005) (005)Donor uses checks 001 001 012 000 013

(005) (004) (005) (004) (005)Donation-level variablesDonation year tfrac142006 016 007 007 008 008

(006) (005) (005) (005) (005)Donation year tfrac142007 020 008 008 009 009

(006) (005) (005) (005) (005)Donation year tfrac142008 047 032 032 033 033

(006) (005) (005) (005) (005)Donation year tfrac142009 050 030 030 029 029

(005) (005) (005) (005) (005)Donation year tfrac142010 037 016 015 015 014

(005) (005) (005) (005) (005)Donation year tfrac142011 037 019 018 018 017

(005) (005) (005) (005) (005)Donation year tfrac142012 045 026 025 026 025

(005) (005) (005) (005) (005)Donation made in year t 096 087 012 003

(003) (004) (009) (009)Log(donation value thorn 1) 017 018

(002) (002)Cross-level interactionDonation made in year t donor uses checks 025 030

(006) (006)AIC 423158 412815 412620 411559 411265BIC 424266 414009 413898 412838 412629

NOTEmdashplt 05 plt 01 plt 001

SHAH ET AL 703

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

and behavioral commitment via repeat donation likelihoodCompared to people who use a less painful form ofpayment (ie card) we found that people who use a morepainful form of payment (ie check) show increasedpost-transaction connection through greater financial com-mitment and loyalty over time It is important to note thatin any given year check-using donors are less likely to do-nate in comparison to plastic-using donors However aftercheck-using donors choose to make a donation their com-mitment to the organization increases in subsequent years(as measured by future willingness to donate) in compari-son to plastic-using donors who are less likely to make arepeat donation The results suggest that the pain of pay-ment may have an economic upside while more pain ofpayment may deter initial donation likelihood after mak-ing a donation more pain of payment may help instill theloyalty and financial commitment that charitable organiza-tions depend on over time

GENERAL DISCUSSION

In the 1970s consumers could choose between aboutfive payment forms for most transactions with cash thedominant choice (Foster et al 2013) However the finan-cial landscape has changed dramatically In todayrsquos mar-ketplace there are more than twenty potential methods ofpayment (Foster et al 2013) many of which are psycho-logically detached from the economic experience of

immediately spending money and thus are less psychologi-cally painful to use As society continues its evolution to-ward a ldquocashless economyrdquo it is important to understandwhether the way we pay influences how much we valueand feel psychologically connected to what we spend ourresources on and how likely we are to remain product andbrand loyal In this article we sought to fill a gap in currentresearch by examining whether payment form can influ-ence post-transaction connection Across field lab onlineand archival studies and across a variety of purchase con-texts (ie purchasing a mug or headphones as well as do-nating to a charity or to onersquos alma mater) wedemonstrated that the pain of paying significantly influ-ences post-transaction psychological and behavioral con-nection in a persistent and pervasive manner

In study 1 we used a field experiment selling mugs toshow that paying by cash a more painful form of paymentincreases the psychological connection to the mug In study1 we also found that the pain of paying fully mediates therelationship between payment form used for purchase andpsychological connection In study 2 we demonstrated thatdonating to a charity using a more painful form of payment($5 cash vs $5 voucher) increases the psychological con-nection and subsequent behavioral connection (ie wearingthe lapel pin) to the chosen alternative while decreasingpsychological connection to the nonchosen alternativesStudy 2 also ruled out two potential confounds First indi-viduals were asked to choose a charity to which they woulddonate $5 cash (voucher) using someone elsersquos money

TABLE 3

FIXED-EFFECTS MODEL RESULTS STUDY 4

Model 2A Model 2B Model 2C Model 2D Model 2E

Donation-level variablesDonation year tfrac142006 017 017 017 018 018

(006) (006) (006) (006) (006)Donation year tfrac142007 022 022 022 022 022

(006) (006) (006) (006) (006)Donation year tfrac142008 053 052 052 053 053

(006) (006) (006) (006) (006)Donation year tfrac142009 059 057 057 057 057

(006) (006) (006) (006) (006)Donation year tfrac142010 047 045 045 045 045

(006) (006) (006) (006) (006)Donation year tfrac142011 050 048 048 048 048

(006) (006) (006) (006) (006)Donation year tfrac142012 063 061 061 062 061

(006) (006) (006) (006) (006)Donation made in year t 013 008 023 032

(003) (004) (011) (012)Log(donation value thorn 1) 007 008

(002) (002)Cross-level interactionDonation made in year t donor uses checks 013 015

(006) (006)AIC 206832 206679 206657 206583 206545BIC 207428 207361 207424 207350 207397

NOTEmdashplt 05 plt 01 plt 001

704 JOURNAL OF CONSUMER RESEARCH

by guest on March 8 2016

httpjcroxfordjournalsorgD

ownloaded from

ruling out the possibility that wealth and income effects aredriving the results Second study 2 ruled out the possibilitythat a positivity bias or halo effects could be driving the re-sults By measuring both general positivity ratings as well aspsychological connection we demonstrated that paying by amore painful form increases only psychological and subse-quent behavioral connection measures In study 3 weshowed that increasing the pain of payment either throughpayment form or payment magnitude ($10 vs $20) can in-crease psychological connection demonstrating that this ef-fect is not due simply to a payment form effect but ratherdue to this broader pain of paying construct Finally instudy 4 we replicated our results using archival donationdata We found that paying by check (a more painful formof payment) in comparison to a debitcredit card in year t in-creases the likelihood of making a donation in the followingyear by 99 (ie 623 vs 567) in year tthorn 1 Thusstudy 4 demonstrated the robustness of our results on long-term behavioral commitment

From a theoretical perspective these findings lend sup-port to the notion that the pain of payment affects not onlydecision making during the purchase context but also howmuch value and commitment are experienced post-purchaseOur findings suggest that this psychological pain of payingcan influence how much individuals value their chosenproduct how connected they feel to it and how committedthey are over time Although increasing the pain of paymentmay decrease purchasing initially as study 4 and prior workindicates our work highlights the potential downstream ben-efits of increasing the psychological pain of payment forboth organizations and individuals Individuals are more fi-nancially psychologically and behaviorally committed toan organization and value products more when they paywith a more painful form of payment While Kamleitnerand Erki (2013) showed correlational evidence that paymentform can affect feelings of ownership of an object our workis the first to show a causal relationship between paymentform and psychological commitment to an organization andbetween payment form and downstream psychological andbehavioral connection

In addition to the pain of payment literature the notionthat the pain of payment can influence value and commit-ment contributes to psychological and behavioral researchon how value and commitment are influenced by physicaland emotional pain such as research on cognitive disso-nance and self-perception (Bem 1967 Festinger 1957Gross 1998) Our results suggest that psychological paincan influence value perceptions and subsequent commit-ment even when the individual is donating money on be-half of someone else Although it is beyond the scope ofthe present article to attempt to discriminate between disso-nance and self-perception we note that experiencing morepsychological and behavioral commitment despite donat-ing money on behalf of someone else (study 2) may bemore consistent with self-perception Individuals were not

donating their own money so there was no reason to be-lieve the donation created dissonant thoughts or a negativedrive state that needed to be reconciled through increasedpsychological connection and behavioral commitment