Embed Size (px)

Citation preview

2013/11/5

1

BUSINESS, ACCOUNTING

AND FINANCIAL STUDIES

EXAMINATION 2013

PAPER 2A

Section A

Paper 2A – Question 1(a)

State and explain the accounting

principle or concept that has been

violated and show the journal entries

to correct the above. (Narration is not

required.)

(4 marks)

2013/11/5

2

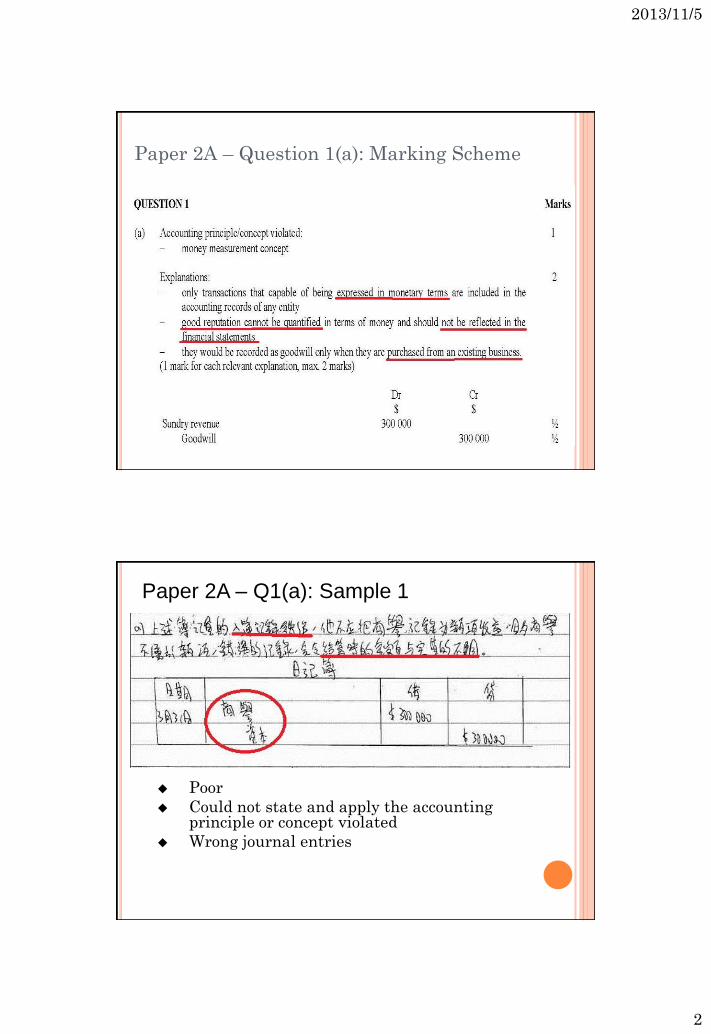

Paper 2A – Question 1(a): Marking Scheme

Poor

Could not state and apply the accounting principle or concept violated

Wrong journal entries

Paper 2A – Q1(a): Sample 1

2013/11/5

3

Good

Could state and explain the accounting principle or concept violated

Gave partly correction journal entries

Paper 2A – Q1(a): Sample 2

Very good

Prepared correction journal entries

Paper 2A – Q1(a): Sample 3

Related

explanation

2013/11/5

4

Paper 2A – Question 1(b)

Write up the cash at bank account for the

month of March 2013. (6 marks)

Paper 2A – Question 1(b): Marking Scheme

2013/11/5

5

Poor

Opposite side of opening cash at bank balance

Misinterpretation of the cheque 201542

Could not read the question carefully

Wrong account names as description for some entries

Paper 2A – Q1(b): Sample 1

Fair

Could not work out the double entries for the cheque 201542

Wrong account names as description for some entries

Paper 2A – Q1(b): Sample 2

2013/11/5

6

Good

Could not work out the double entries for the cheque 201542

Paper 2A – Q1(b): Sample 3

Paper 2A – Question 2(a) & (b)

For the retail business of Mr. Chan,

prepare the following accounts for the

year ended 31 December 2012:

(a) Equipment account (3 marks)

(b) Accumulated depreciation account – Equipment

(4 marks)

2013/11/5

7

Poor

Could not work out the double entries for disposal and depreciation expense

Was unable to distinguish between capital expenditure and revenue expenditure and the cost of the new equipment could not be correctly arrived

Paper 2A – Q2(a) & (b): Sample 1

Paper 2A – Question 2(a) & (b): Marking Scheme

2013/11/5

8

Fair

Could not work out the double entries for disposal of equipment

Wrong account names as description for the new equipment purchased

Wrongly ignored the calculation of depreciation for the new equipment

Paper 2A – Q2(a) & (b): Sample 2

Old equipment

Very good

Correct answers

Paper 2A – Q2(a) & (b): Sample 3

2013/11/5

9

Paper 2A – Question 2(c)

State and explain the accounting principle or

concept violated in the above situation.

(3 marks)

Paper 2A – Question 2(c): Marking Scheme

2013/11/5

10

Poor

Wrong spelling of the concept

Failed to give appropriate explanation

Did not explain why using different

depreciation methods to show stable operating

results continuously violated the principle

Paper 2A – Q2(c): Sample 1

Fair

Correctly identified the accounting concept violated

Failed to give appropriate explanation

Did not explain why using different depreciation methods to show stable operating results continuously violated the principle

Paper 2A – Q2(c): Sample 2

2013/11/5

11

Very good

Sufficient explanation of consistency principle

Paper 2A – Q2(c): Sample 3

Paper 2A – Question 3(a) & (b)

(a) Calculate the predetermined production overhead absorption rate for the year 2014. (2 marks)

(b) State one rationale for Hansan Ltd’s choice of using the existing absorption base to calculate its predetermined production overhead absorption rate. (2 marks)

2013/11/5

12

Paper 2A – Question 3(a) & (b): Marking Scheme

Poor

Wrongly included direct costs and administrative overheads in the calculation of predetermined production overhead absorption rate

Could not state the reason for using direct labour hours as the existing absorption base

Paper 2A – Q3(a) & (b): Sample 1

2013/11/5

13

Fair

Correctly calculated predetermined production overhead absorption rate

Could not state the reason for using direct labour hours as the existing absorption base

Paper 2A – Q3(a) & (b): Sample 2

Very good

Correctly stated using direct labour hours more than machine hours

Only failed to state the reason for using direct labour hours as the existing absorption base

Paper 2A – Q3(a) & (b): Sample 3

2013/11/5

14

Paper 2A – Question 3(c)

Calculate the selling price of this job,

showing separately the amount of:

- prime cost

- production cost

- total cost

(6 marks)

Paper 2A – Question 3(c): Marking Scheme

2013/11/5

15

Poor

Made a wrong classification of costs

Wrongly ignored the calculation of the selling price of the job

Paper 2A – Q3(c): Sample 1

Fair

Correctly calculated the prime cost

Could not apply the predetermined overhead absorption rate to calculate the production overhead for the job

Wrongly ignored the selling price of the job

Paper 2A – Q3(c): Sample 2

2013/11/5

16

Very good

Only failed to apply the net profit margin of

50% to set the price

Paper 2A – Q3(c): Sample 3

BUSINESS, ACCOUNTING

AND FINANCIAL STUDIES

EXAMINATION 2013

PAPER 2A

Section B

2013/11/5

17

33

Paper 2A – Question 4 (a&b)

34

Paper 2A – Question 4 (a&b)

*

*

*

2013/11/5

18

35

Paper 2A – Question 4 (a): Marking Scheme

*

*

*

*

36

Paper 2A – Question 4 (b): Marking Scheme

2013/11/5

19

PAPER 2A- QUESTION 4(A): SAMPLE 1

• Failed to deal with revaluation and goodwill adjustments for partner changes

• Wrong entry for bank payment to retiring partner

PAPER 2A- QUESTION 4(A): SAMPLE 2

• Failed to deal with revaluation adjustments:

i) Ignored allowance for trade receivable

ii) Misinterpreted loss on revaluation of equipment “ decreased by 20% ”, NOT “decreased to 20%”

2013/11/5

20

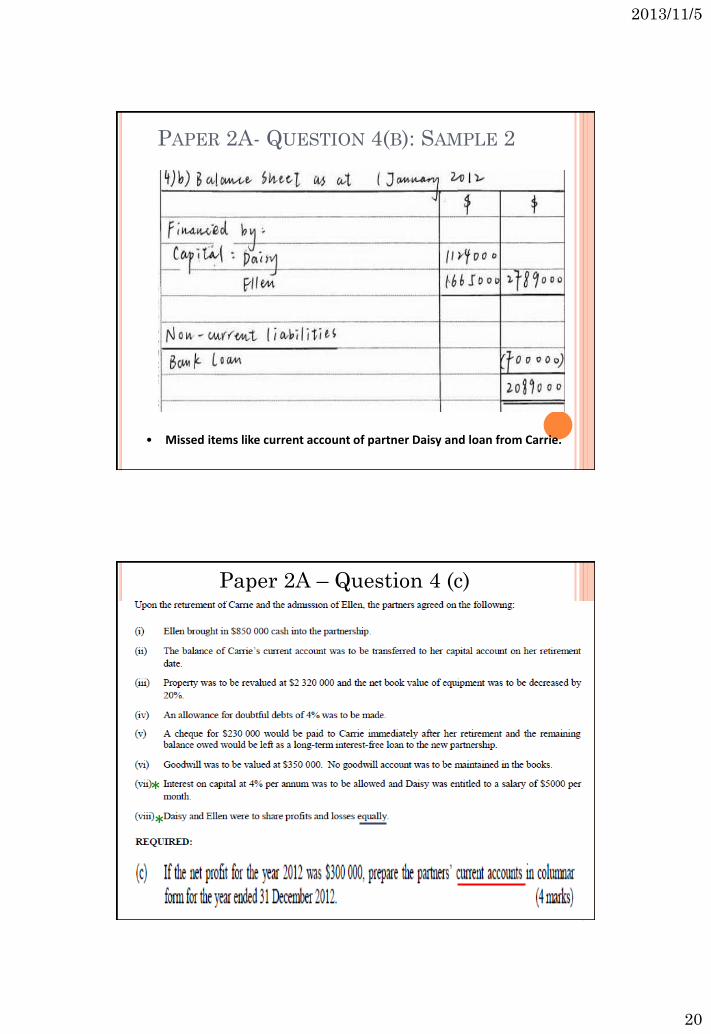

PAPER 2A- QUESTION 4(B): SAMPLE 2

• Missed items like current account of partner Daisy and loan from Carrie.

40

Paper 2A – Question 4 (c)

*

*

2013/11/5

21

41

Paper 2A – Question 4 (c): Marking Scheme

PAPER 2A- QUESTION 4: SAMPLE 1

• Unable to record profit appropriation properly in the current account.

2013/11/5

22

Paper 2A- Question 4: Sample 2

• Able to include all the appropriated profit elements, but

i) interest on capital based wrongly on current account balance.

ii) failed to deduct partner’s salary and interest on capital before sharing profit $300,000

• Wrongly captured the cash injection by Ellen in current account.

44

Paper 2A – Question 4 (d)

(d) Give one reason why asset revaluation is necessary

upon the retirement of a partner.

(2 marks)

Marking Scheme

2013/11/5

23

PAPER 2A- QUESTION 4: SAMPLE 1

• Got confused in asset revaluation and profit and loss sharing issues in dealing with retirement of partner.

PAPER 2A- QUESTION 4: SAMPLE 2

• Wrong focus of the answer. The question focused on:

i) retirement of partner, not admission of partner.

ii) asset revaluation, not cost of goods

2013/11/5

24

PAPER 2A- QUESTION 4: SAMPLE 3

• Well answered

48

Paper 2A – Question 5

2013/11/5

25

49

Paper 2A – Question 5 (continued)

50

Paper 2A – Question 5 (a): Marking Scheme

2013/11/5

26

51

Paper 2A – Question 5 (a): Marking Scheme

52

Paper 2A – Question 5 (b): Marking Scheme

2013/11/5

27

PAPER 2A – QUESTION 5: SAMPLE 1

• Unable to identify and determine the amount of sales and expenses items from incomplete records.

PAPER 2A – QUESTION 5: SAMPLE 1

• Unable to draw up proper T account for trade payable. The debits and credits were completely reversed.

2013/11/5

28

55

PAPER 2A – QUESTION 5: SAMPLE 1

• Unable to draw up proper T accounts for cash and bank.

PAPER 2A – QUESTION 5: SAMPLE 2

• Understood the pricing policy of mark-up of 40%.

• Unable to determine cash loss and failed to include all expenses like depreciation.

2013/11/5

29

PAPER 2A – QUESTION 5: SAMPLE 2

• Omitted insurance claim receivable in the current assets.

• Ignored note (i), all sales were made on cash basis.

• Depreciation wrongly computed based on reducing balance method.

58

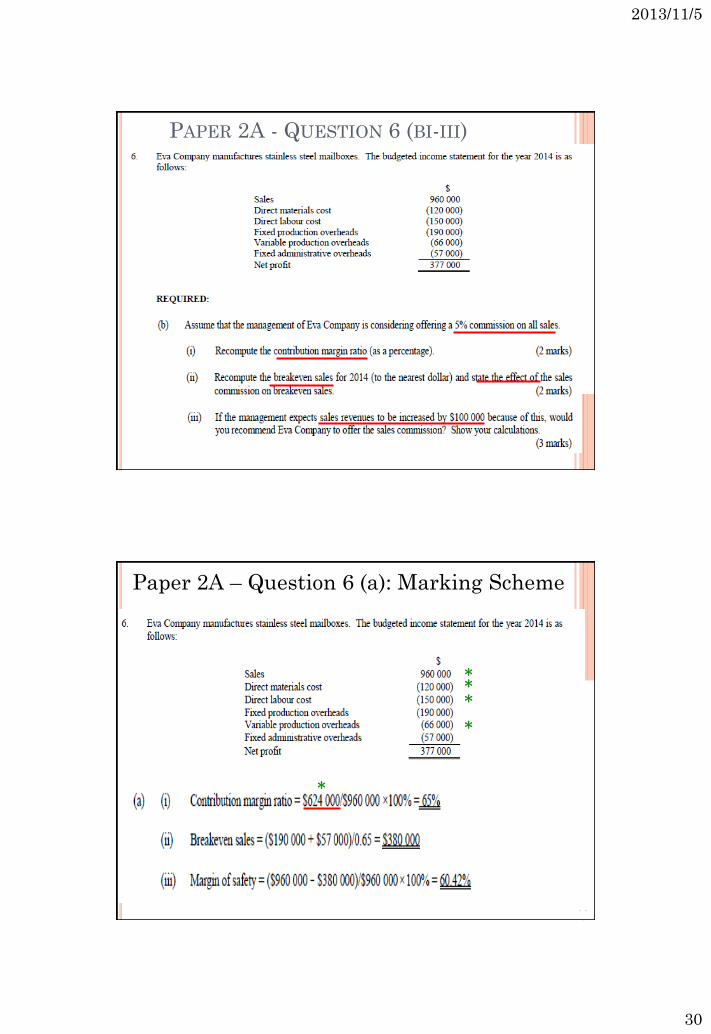

PAPER 2A - QUESTION 6 (AI-III)

2013/11/5

30

59

PAPER 2A - QUESTION 6 (BI-III)

60

Paper 2A – Question 6 (a): Marking Scheme

* *

*

*

*

2013/11/5

31

61

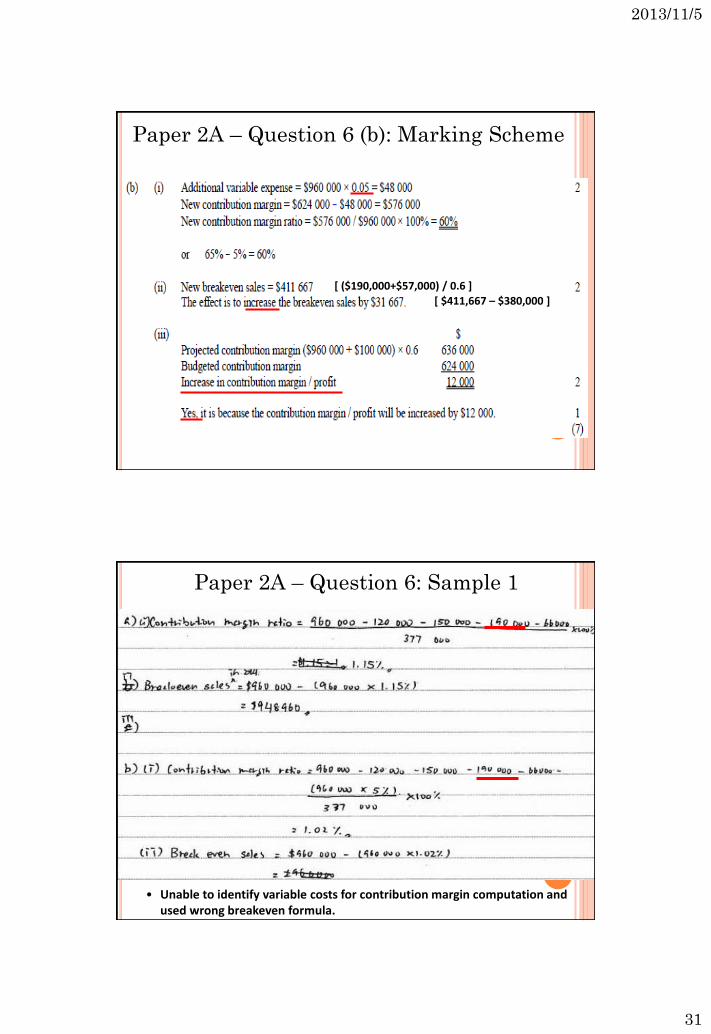

Paper 2A – Question 6 (b): Marking Scheme

[ ($190,000+$57,000) / 0.6 ]

[ $411,667 – $380,000 ]

62

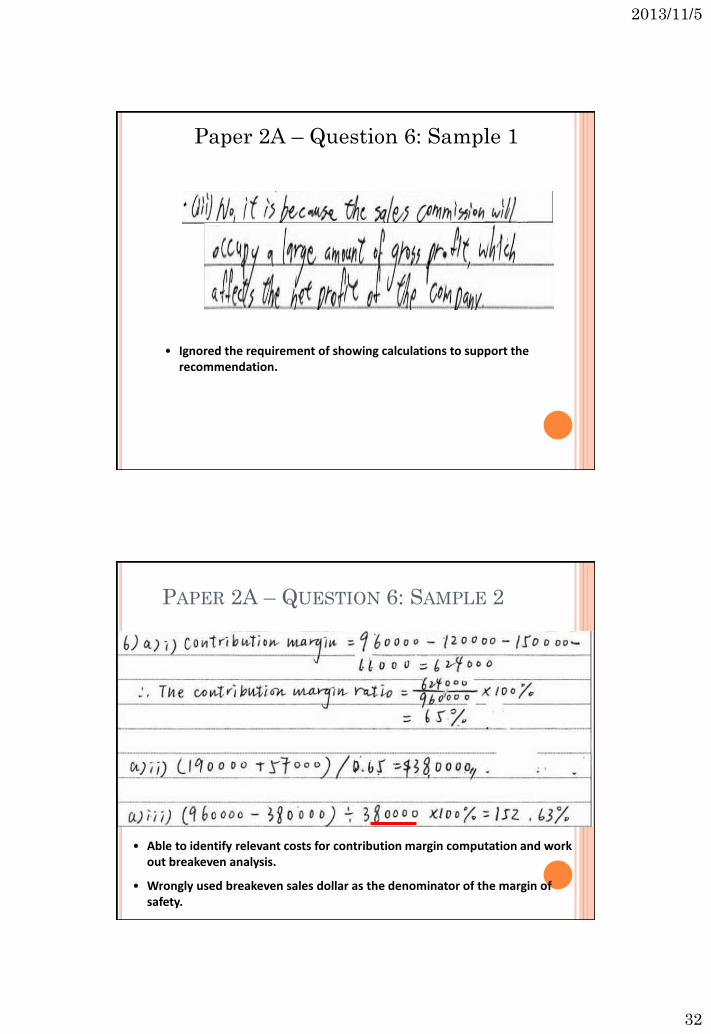

Paper 2A – Question 6: Sample 1

• Unable to identify variable costs for contribution margin computation and used wrong breakeven formula.

2013/11/5

32

Paper 2A – Question 6: Sample 1

• Ignored the requirement of showing calculations to support the recommendation.

PAPER 2A – QUESTION 6: SAMPLE 2

• Able to identify relevant costs for contribution margin computation and work out breakeven analysis.

• Wrongly used breakeven sales dollar as the denominator of the margin of safety.

2013/11/5

33

Paper 2A – Question 6: Sample 2

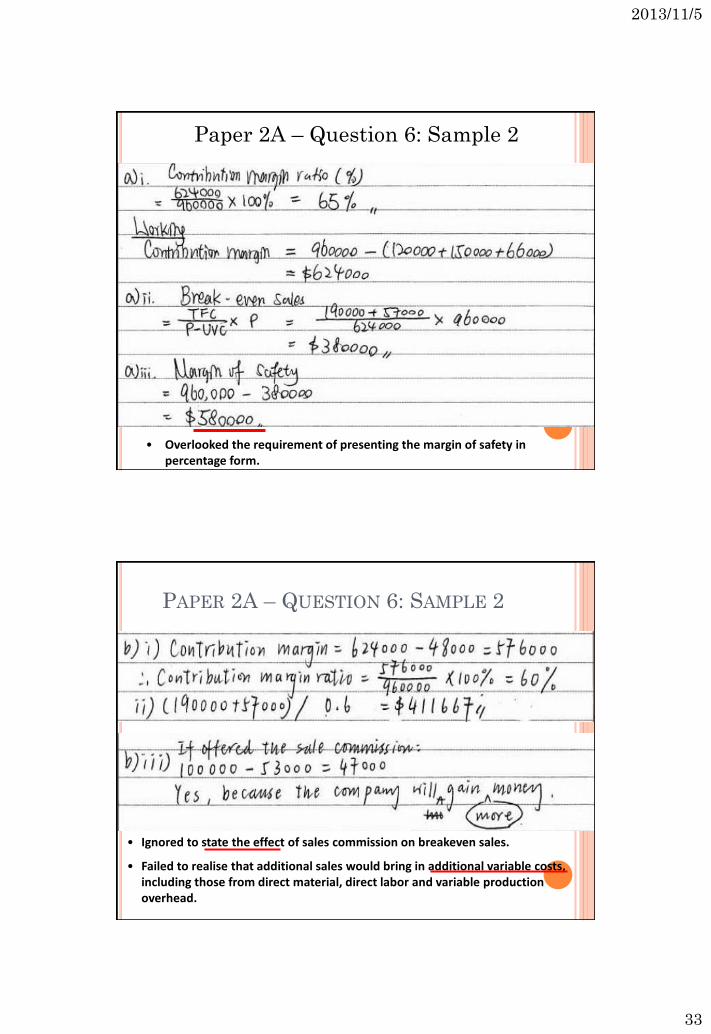

• Overlooked the requirement of presenting the margin of safety in percentage form.

PAPER 2A – QUESTION 6: SAMPLE 2

• Ignored to state the effect of sales commission on breakeven sales.

• Failed to realise that additional sales would bring in additional variable costs, including those from direct material, direct labor and variable production overhead.

2013/11/5

34

Paper 2A – Question 6: Sample 2

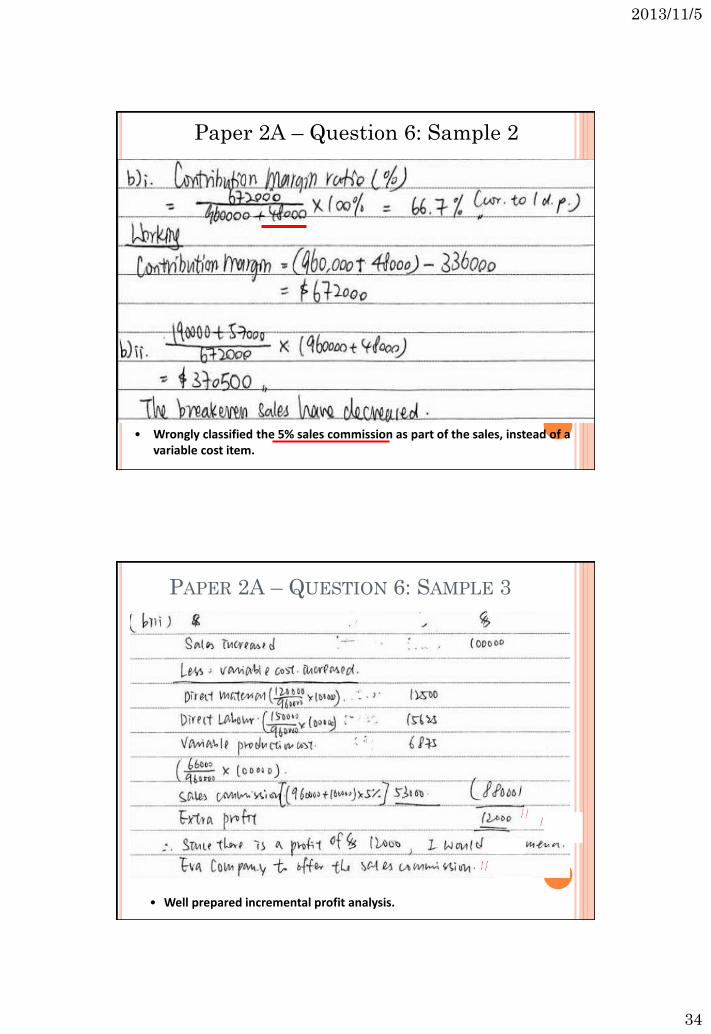

• Wrongly classified the 5% sales commission as part of the sales, instead of a variable cost item.

PAPER 2A – QUESTION 6: SAMPLE 3

• Well prepared incremental profit analysis.

2013/11/5

35

PAPER 2A – QUESTION 6

(c) Why is a decline in the margin of safety an issue

of concern to the management of a company?

(2 marks)

Marking Scheme

PAPER 2A – QUESTION 6: SAMPLE 1

• Wrong interpretation of the decline of margin of safety

2013/11/5

36

PAPER 2A – QUESTION 6: SAMPLE 2

• Failed to identify or explain the impact brought on by the decline of margin of safety.

• A very general description of margin of safety. Failed to indicate that a decline of margin of safety would mean a decrease in profit and an increase in the possibility of having a loss.

PAPER 2A – QUESTION 6: SAMPLE 3

• Able to identify and explain the impact brought on by the decline of margin of safety.

2013/11/5

37

BUSINESS, ACCOUNTING

AND FINANCIAL STUDIES

EXAMINATION 2013

PAPER 2A

Section C

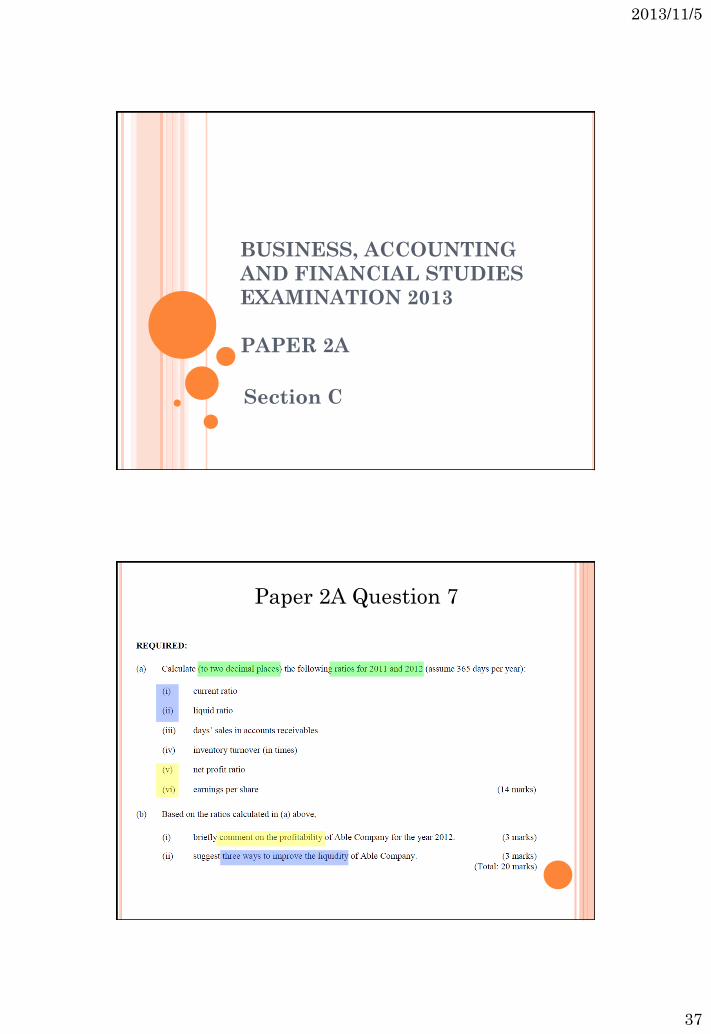

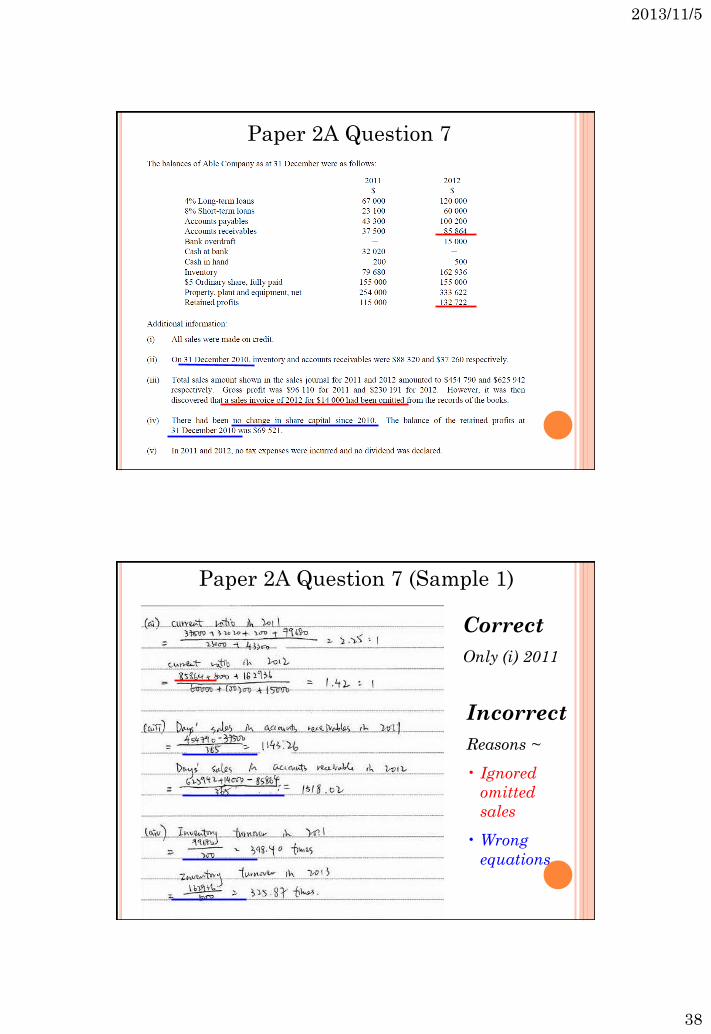

Paper 2A Question 7

2013/11/5

38

Paper 2A Question 7

Paper 2A Question 7 (Sample 1)

Correct

Only (i) 2011

Incorrect

Reasons ~

• Ignored

omitted

sales

• Wrong

equations

2013/11/5

39

Paper 2A Question 7 (Sample 1)

ALL incorrect

Wrong equations

Paper 2A Question 7 (Sample 1)

Incorrect

(b) (i) Not making the comparison

(b) (ii) Not mentioning the correct ways to reduce

current liabilities

2013/11/5

40

Paper 2A Question 7 (Sample 2)

ALL

correct!

Paper 2A Question 7 (Sample 2)

Correct

Only (iv) 2011

Incorrect

Reasons ~

• Ignored the effect on

gross profit

• Retained profit for the

year vs. Retained

profits carried forward

to next year

2013/11/5

41

Paper 2A Question 7 (Sample 2)

Incorrect

(b) (i) Not giving an accurate conclusion

(b) (ii) Not mentioning the correct ways to reduce

current liabilities

Paper 2A Question 7 (Sample 3)

ALL correct except for two highlighted figures

GOOD practice ??

2013/11/5

42

Paper 2A Question 7 (Sample 3)

Paper 2A Question 8

2013/11/5

43

Paper 2A Question 8

Paper 2A Question 8

2013/11/5

44

Paper 2A Question 8

Paper 2A Question 8

2013/11/5

45

Paper 2A Question 8 (Sample 1)

Could not obtain the correct gross profit

ratio and sales commission in %

Paper 2A Question 8 (Sample 1)

Many mistakes, in particular, omitted all

unavoidable costs (e.g. 4/5 office expenses of

shop C) and forfeited rental deposit

2013/11/5

46

Paper 2A Question 8 (Sample 1)

Incorrect

(c) No supporting reason for making conclusion

(d) Not answering the question

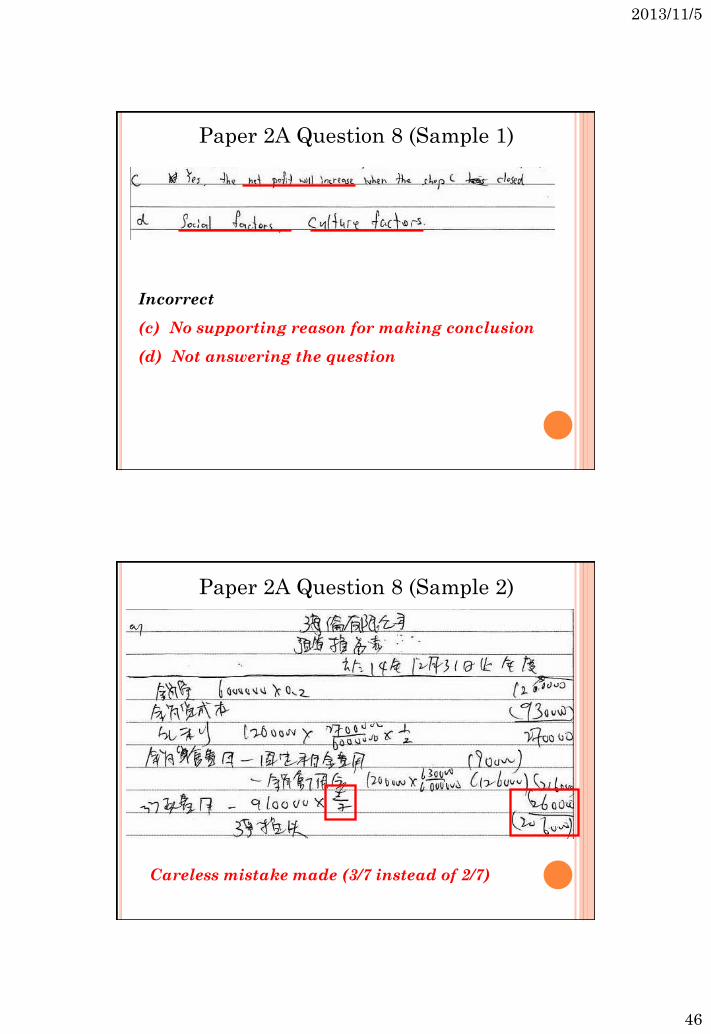

Paper 2A Question 8 (Sample 2)

Careless mistake made (3/7 instead of 2/7)

2013/11/5

47

Paper 2A Question 8 (Sample 2)

Mistakes made:

sales, salary

per month

instead of per

year and same

careless

mistake as in (a)

Paper 2A Question 8 (Sample 2)

Incorrect

Wrong conclusion

2013/11/5

48

Paper 2A Question 8 (Sample 2)

Incorrect

Not justifiable assumptions and explanations

Paper 2A Question 8 (Sample 3)

2013/11/5

49

Paper 2A Question 8 (Sample 3)

Incorrect ~

Forfeited

rental

deposit

Salary per

month

instead of

per year

Sales

commission

rate

Paper 2A Question 8 (Sample 3)

![PTS 2a Mock SBA Series 2020 Paper 3- [Answers]- Version 1 · PTS 2a Mock SBA Series 2020 Paper 3- [Answers]- Version 1 Marking Instructions: • Award 1 mark for each question on](https://img.dokumen.tips/doc/110x75/5f827399b3ccd11ccc377a29/pts-2a-mock-sba-series-2020-paper-3-answers-version-1-pts-2a-mock-sba-series.jpg)

![PTS 2a Mock SBA Series 2020 Paper î- [Answers]- Version í · PTS 2a Mock SBA Series 2020 Paper î- [Answers]- Version í Marking Instructions: • Award 1 mark for each question](https://img.dokumen.tips/doc/110x75/5f08fbe67e708231d424ac25/pts-2a-mock-sba-series-2020-paper-answers-version-pts-2a-mock-sba-series.jpg)