Embed Size (px)

DESCRIPTION

power point slides on pakistan textile industry

Citation preview

The textile sector is the back bone of the Pakistan’s Economy.

It is the largest industry in the country. Pakistan currently ranks fourth among

world cotton producers and third among world cotton consumers

EXPORTS: 62.1% OF TOTAL EXPORTS (US $ 10.211 BILLION)

MANUFACTURING: 46% OF TOTAL MANUFACTURING

EMPLOYMENT: 38% OF TOTAL LABOUR FORCE GDP: 8.5% OF TOTAL GDP INVESTMENT: US $ 0.771 BILLION MARKET CAPITALIZATION: 5.11% OF TOTAL

MARKET CAPITALIZATION CONTRIBUTION TO R&D: RS. 263 MILLION PER

ANNUM

The growth of the textile industry in Pakistan has followed the macro economic situation of the country over the years.

INSTALLED CAPACITY (in 000) WORKING CAPACITY (in 000)

Period Units

Spindles

Growth%

Rotors

Growth%

Looms Growth%

Spindles

Growth%

Rotors

Growth%

Looms

Growth%

2001-02

450

9060

5.34

141

-3.42

10

0

7440

7.62

66

-5.71

5

25.00

2002-03

453

9260

2.21

148

4.96

10

0

7676

3.17

70

6.06

5

0

2003-04

456

9592

3.59

146

-1.35

10

0

8009

4.34

66

-5.71

4

-20.00

2004-05

458

10485

9.31

155

6.16

9

-10.00

8492

6.08

79

19.70

4

0

2005-06

461

10437

0.46

155

0.00

9

-11.11

9415

10.87

77

-2.53

4

0

2006-07

461

10514

0.74

150

-3.23

8

0.00

7989

-15.15

70

-9.09

3

-25.00

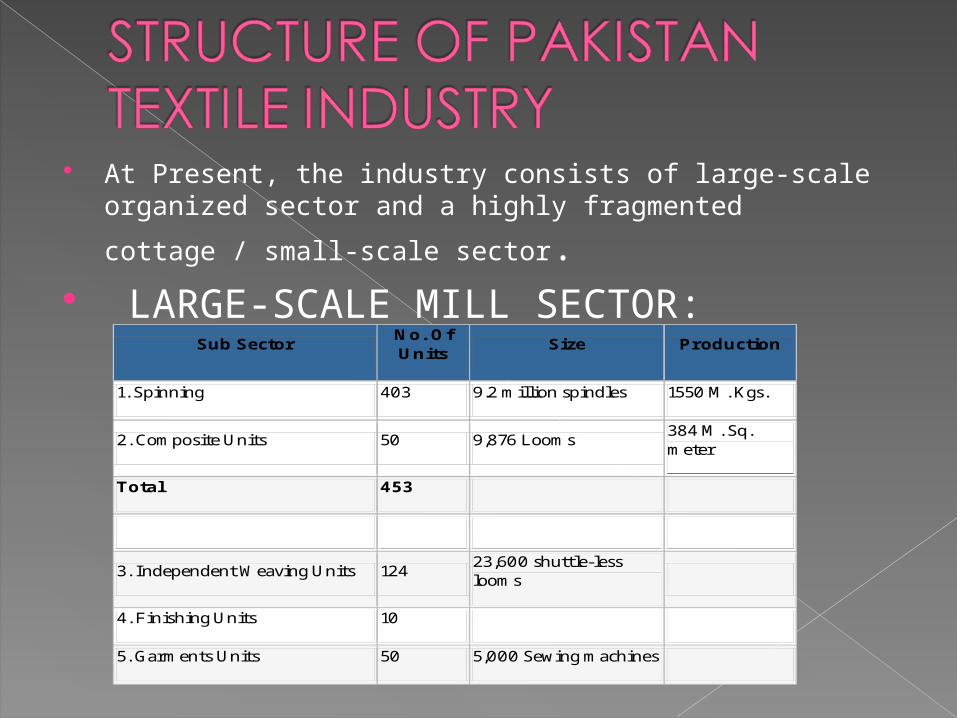

At Present, the industry consists of large-scale organized sector and a highly fragmented cottage / small-scale

sector. LARGE-SCALE MILL SECTOR:

Sub Sector No. Of Units

Size Production

1. Spinning 403 9.2 million spindles 1550 M. Kgs.

2. Composite Units 50 9,876 Looms 384 M. Sq. meter

Total 453

3. Independent Weaving Units 124 23,600 shuttle-less looms

4. Finishing Units 10

5. Garments Units 50 5,000 Sewing machines

COTTAGE/SMALL-SCALE SECTOR:

Sub Sector No. Of Units

Size Production

1. Independent Weaving Units

453 50,000 Looms 3600 M. Sq. meter

2. Power Looms 20,600 175,200 Looms

Total 21053 225,200

3. Finishing 625 Cotton 2700 M. Sq. meter

4. Terry Towels 400 7,602 Looms 53 M. Kgs.

5. Garments 2,500 300,000 Sewing machines

600 M. Pcs.

6. Knitwear 600 12,000 Knitting machines

400 M. PCs.

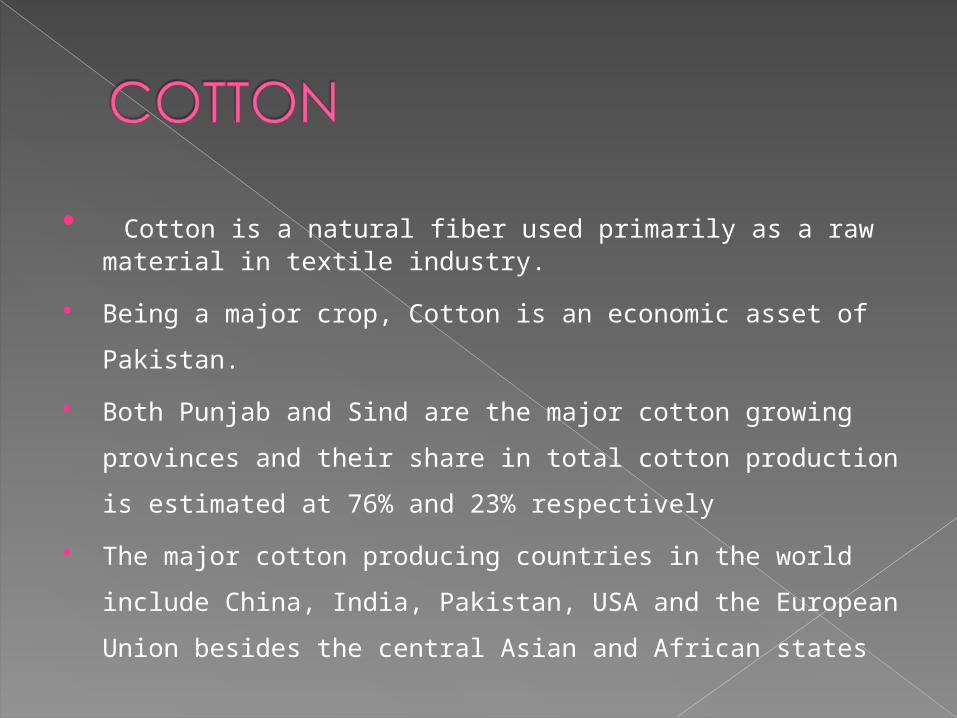

Cotton is a natural fiber used primarily as a raw material in textile industry.

Being a major crop, Cotton is an economic asset of

Pakistan.

Both Punjab and Sind are the major cotton growing

provinces and their share in total cotton production is

estimated at 76% and 23% respectively

The major cotton producing countries in the world include

China, India, Pakistan, USA and the European Union

besides the central Asian and African states

Cotton, Area, Production And Yield

Area Production Yield Year (000

Hectare) %

Change (000 Bales)

% Change

(Kgs/Hec) % Change

2002-03

2794 -10.3 10211 -3.8 622 7.4

2003-04

2989 7.0 10048 -1.6 572 -8.0

2004-05

3193 6.8 14265 42.0 760 32.9

2005-06 (P)

3096 -3.0 12417 -13.0 682 -10.3

Pakistan's cotton is regarded as the best among varieties of cottons of similar staples grown elsewhere in the world. Pakistan's textile industry enjoys several advantages over those of many other countries as far as the production of quality fabrics and yarn is concerned and is a world leader in the export of cotton yarn, including coarse, medium and fine varieties. Pakistan's leading buyers are Japan, Republic of Korea and Hong Kong.

PRODUCTION, EXPORTS & DOMESTIC REQUIREMENT OF YARN Fig: in '000' Kgs

PERIOD PRODUCTION CONSUMED IN MILL SECTOR EXPORTS AVAILABLE FOR LOCAL MARKET

QUANTITY % OF PROD. QUANTITY % OF PROD. QUANTITY % OF PROD. 2000-01 1,729,129 68,275 3.95 545,134 31.59 1,115,720 64.52

2001-02 1,818,345 77,328 4.25 539,500 29.67 1,201,517 66.08 2002-03 1,924,936 79,435 4.13 525,130 27.28 1,320,369 68.59 2003-04 1,938,908 93,141 4.80 514,279 26.52 1,331,487 68.67 2004-05 2,290,340 105,362 4.60 520,782 22.74 1,664,196 72.66 2005-06 2,216,605 95,710 4.32 691,492 31.20 1,429,403 64.49 2006-07 2,727,566 104,423 3.83 699,259 25.64 1,923,874 70.53

The growing demand for blended yarn and fabrics has shifted the raw-material source towards the Man-Made or Synthetic Fiber in Pakistan.

The MMF industry in Pakistan has gradually developed during the last decade but still Pakistan usage is currently at 74% cotton and 26% man-made fibers

CONSUMPTION OF RAW MATERIAL (PAKISTAN)

(Fig. in '000' Kgs) RAW MATERIAL GROWTH % % OF TOTAL

Period Cotton Fiber Total Cotton Fiber Cotton Fiber

1997-98 1,471,169 318,923 1,790,092 2 35 82 18

1998-99 1,441,923 407,686 1,849,609 -2 28 78 22

1999-00 1,566,348 404,008 1,970,356 9 -1 79 21

2000-01

1,673,280 405,038 2,078,318 7 0 81 19

2001-02 1,755,669 409,557 2,165,226 5 1 81 19

2002-03

1,943,197 449,424 2,392,621 11 10 81 19

2003-04

1,938,678 468,984 2,407,662 0 4 81 19

2004-05

2,099,380 488,804 2,588,184 8 4 81 19

2005-06

2,407,560 525,000 2,932,560 15 7 82 18

2006-07

2,563,510 580,000 3,143,510 6 10 82 18

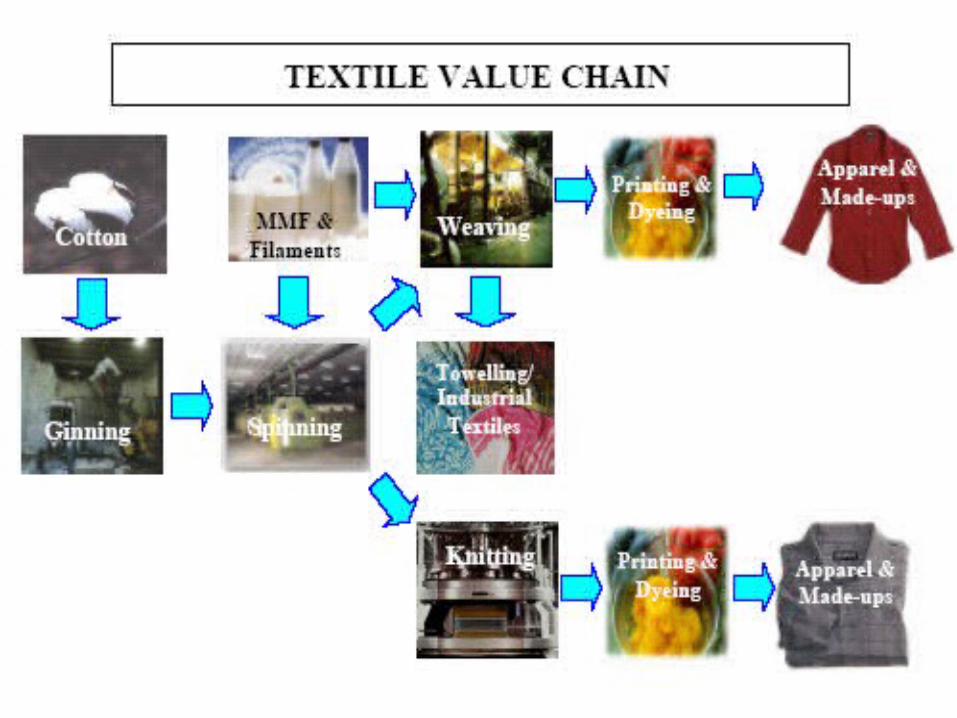

The first mechanical process involved in the processing of cotton is ginning.

Ginning is the process for separating lint from seed to cotton.

This component of local textile industry is the most neglected and antiquated.

Spinning is the process of converting fibers into yarn.

If spinning industry produces sub-standard yarn, its effect goes right across the entire value chain.

Pakistan is the third largest player in Asia with a spinning capacity of 5% of the total world and 7.6% of the capacity in Asia.

The exports of woven fabrics and other related woven made-ups form a major portion of textile exports from Pakistan.

There are three different sub-sectors in weaving i.e., Integrated, independent Weaving Units, and Power Loom Units. Installed and Capacity Worked in Weaving Sector

Category Installed Capacity

Effective/ Capacity Worked

(a) Integrated Textile Units 9050 4350 (b) Independent Weaving

Units 27500 27000

(c) Power Loom Sector 295442 285442 Total 331992 316792

Source: Textile Commissioner Organization

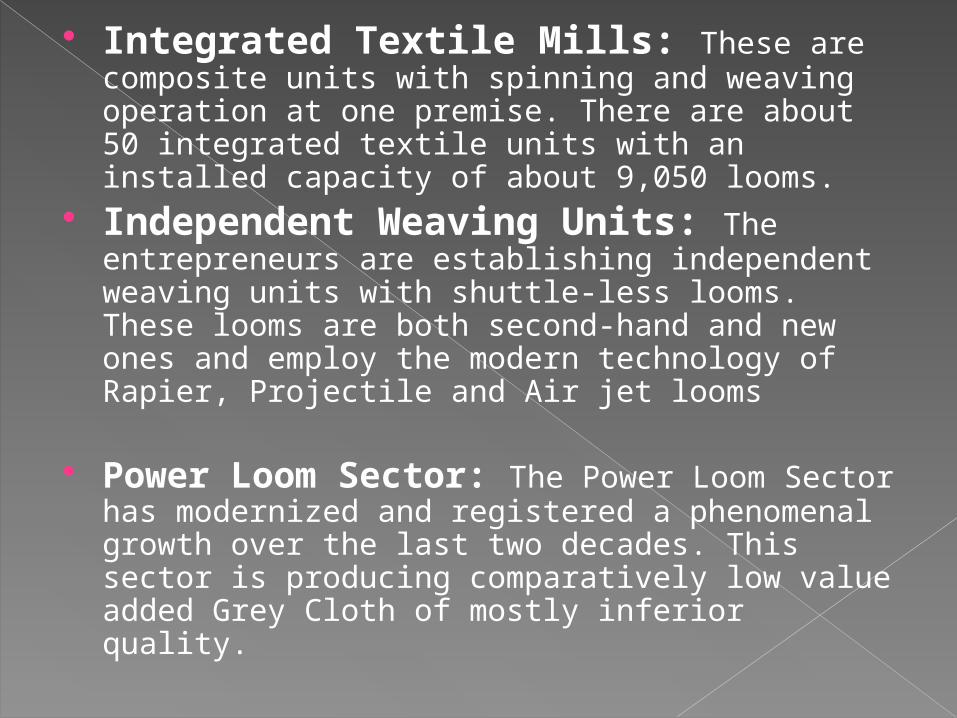

Integrated Textile Mills: These are composite units with spinning and weaving operation at one premise. There are about 50 integrated textile units with an installed capacity of about 9,050 looms.

Independent Weaving Units: The entrepreneurs are establishing independent weaving units with shuttle-less looms. These looms are both second-hand and new ones and employ the modern technology of Rapier, Projectile and Air jet looms

Power Loom Sector: The Power Loom Sector has modernized and registered a phenomenal growth over the last two decades. This sector is producing comparatively low value added Grey Cloth of mostly inferior quality.

Ready Made Garments Hosiery and Knitwear Bed wear Cotton Fabrics Soft/Stuffed Toys Cotton Bags Terry Towel Cotton Yarn

STRENGTHS: Pakistan is the fourth largest producer of cotton

yarn and cloth in the world. Pakistan’s share in the world yarn trade is about

30% and the share in cloth is 8%. This describes its competitive position in international market and future potentials for improvements & growth.

There is ample availability of cheap labor in Pakistan.

It has large well-equipped finishing sector with recent wider width capacity.

The cotton trade in Pakistan is free which is a major benefit to the spinning sector.

WEAKNESSES: Although labour is available and labour costs are

amongst the lowest in the world, the benefit is being wasted through operational inefficiency. Proper training is necessary to develop skill, required to have desired production efficiency.

Pakistan textile industry is facing problem of Low productivity due to its obsolete textile machineries

The factor of high power cost, high interest cost and high cost of inputs like Gas and Water are not accounted for rebates to facilitate industry

Non-availability of good quality soft water for the textile industry.

Inadequate and unreliable power supply, a major constraint, is getting worse and causing poor competitive rating.

OPPURTUNITIES: The Global opportunity is tremendous

which requires the Textile Industry in Pakistan to provide competitive and quality products to the Global Markets.

According to the Pakistan Ministry of Textiles, an export target of 13 billion USD has been fixed for the year 2007-08. Hence, the textile units in Pakistan have an opportunity to expand their scope.

The demand for textiles, which is presently around US $ 19trillion per annum is growing globally at an average rate of 2.5%.

THREATS: The Pakistan textile industry is facing tough

competition from the Indian, Bangladeshi and Chinese textile industries.

Our trained professionals are going to Bangladesh and Russia to run their factories.

There is also the need for greater value addition in its products.

The NON-AVAILABILTY of compatible market access to our Textile Manufacturers.

The collapsing infrastructure on which the Governments does not seem to be paying attention is KILLING the Textile Industry slowly but surely.

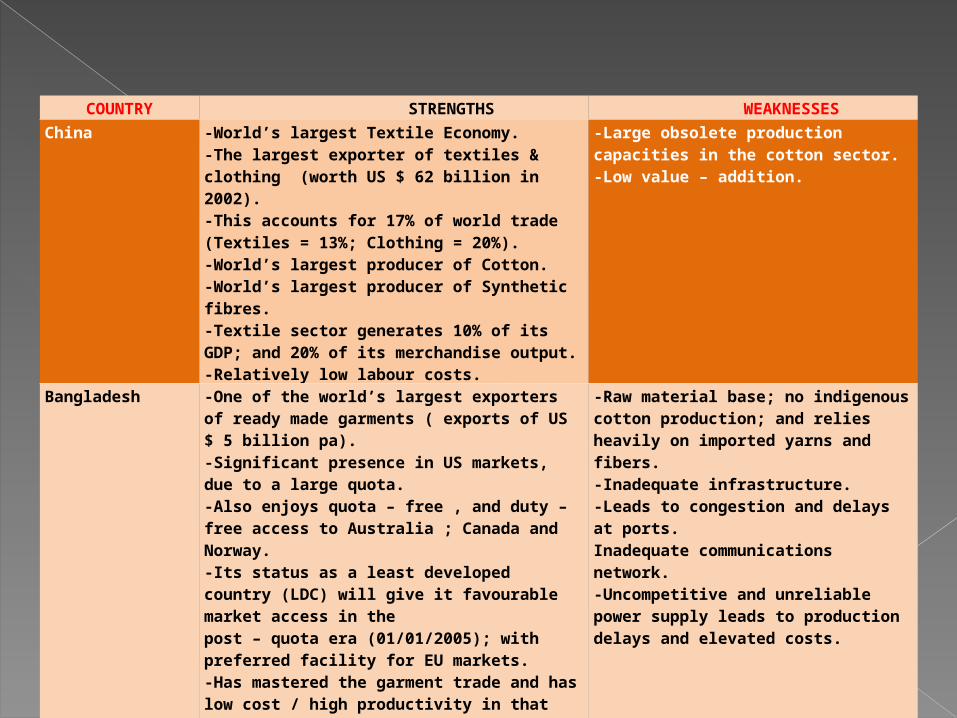

COUNTRY STRENGTHS WEAKNESSES

China -World’s largest Textile Economy.-The largest exporter of textiles & clothing (worth US $ 62 billion in 2002).-This accounts for 17% of world trade (Textiles = 13%; Clothing = 20%).-World’s largest producer of Cotton.-World’s largest producer of Synthetic fibres.-Textile sector generates 10% of its GDP; and 20% of its merchandise output.-Relatively low labour costs.

-Large obsolete production capacities in the cotton sector.-Low value – addition.

Bangladesh -One of the world’s largest exporters of ready made garments ( exports of US $ 5 billion pa).-Significant presence in US markets, due to a large quota.-Also enjoys quota – free , and duty – free access to Australia ; Canada and Norway.-Its status as a least developed country (LDC) will give it favourable market access in thepost – quota era (01/01/2005); with preferred facility for EU markets.-Has mastered the garment trade and has low cost / high productivity in that sector.

-Raw material base; no indigenous cotton production; and relies heavily on imported yarns and fibers.-Inadequate infrastructure.-Leads to congestion and delays at ports.Inadequate communications network.-Uncompetitive and unreliable power supply leads to production delays and elevated costs.

Sri Lanka -Textile and Apparel Industry has crucial part of country’s economy.-It is the country’s biggest employer in manufacturing; and number 1 export earner.-In 2001 it accounted for 69% of the country’s industrial exports and 53% of its total exports.-Relatively secure markets in with USA; EU and Canada through bilateral agreements.

-Small domestic fabric base.Relies heavily on yarn and fabric imports.-Industry is seeing decline in competitiveness due to its heavy reliance on quota categories, concentration on a few markets, inability to develop new markets or major purchasers because of direct marketing contacts.-Relatively small domestic market, little cash generation to support investment in developing export markets.

India -India has been producing record crops every season and in 2007-2008 season its production is estimated around 31.0 million 170-kg bales the best crop in 60 years.-In comparison with Pakistan, India improved its yield by 117 percent in 8 years-India has the largest area under cotton in the world around 9.0 million hectares, is the second largest in world production, second largest in raw cotton exports and the second largest in raw cotton consumption in the world

-Indian textile industry is led by small scale companies. Smaller companies do not have the fiscal resources to enhance technology or invest in the high-end engineering of processes. -India seriously lacks in trade pact memberships, which leads to restricted access to the other major markets.

Pakistan is exporting around US $ 10 billion of textile goods each year .

The exports of composed of both basic textile products such as yarn and value added exports including made-ups.

EXPORTS DESTINATION: In terms of export destination, Pakistan is

heavily dependent on European countries, USA and the Middle East. In addition to clothes Pakistan also exports cotton yarn and basic textiles to East Asian countries.

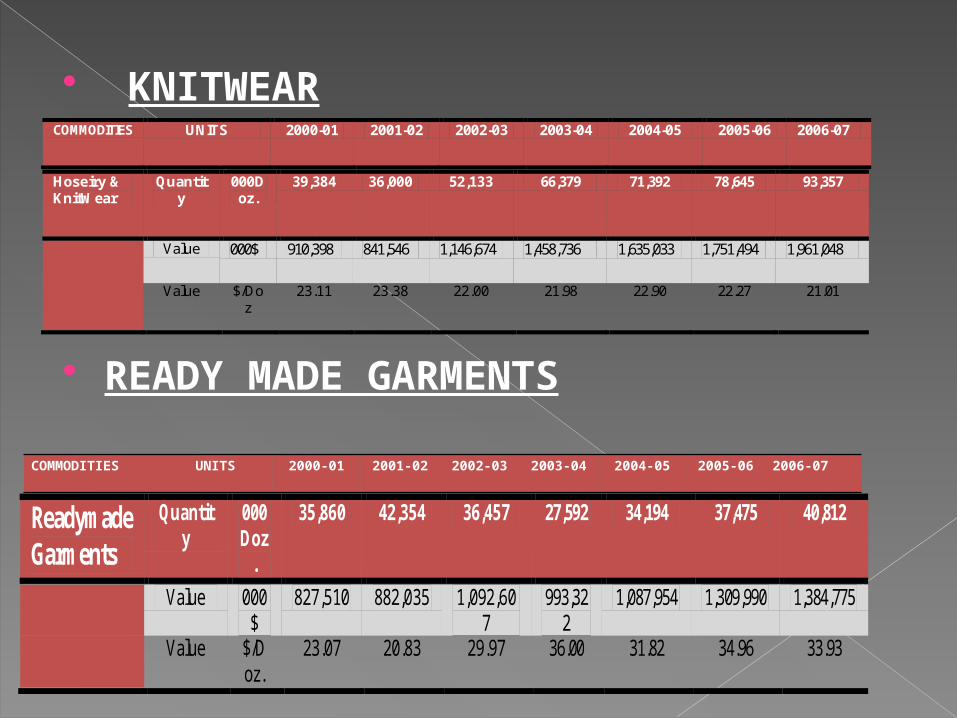

KNITWEAR

READY MADE GARMENTS

Hoseiry & KnitWear

Quantity

000Doz.

39,384 36,000 52,133 66,379 71,392 78,645 93,357

Value 000$ 910,398 841,546 1,146,674 1,458,736 1,635,033 1,751,494 1,961,048

Value $/Doz

23.11 23.38 22.00 21.98 22.90 22.27 21.01

COMMODITIES UNITS 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07

Readymade Garments

Quantity

000Doz

.

35,860 42,354 36,457 27,592 34,194 37,475 40,812

Value 000$

827,510 882,035 1,092,607

993,322

1,087,954 1,309,990 1,384,775

Value $/Doz.

23.07 20.83 29.97 36.00 31.82 34.96 33.93

COMMODITIES UNITS 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07

TOWELS

BED WEAR

COMMODITIES UNITS 2000-01

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07

Towels Quantity Tons 67,460 79,526 100,586 101,806 139,168 158,778 159,471

Value 000$ 243,025 269,823 374,839 403,500 520,480 587,641 602,547

Value $/KG. 3.60 3.39 3.73 3.96 3.74 3.70 3.78

COMMODITIES

UNITS 2000-01

2001-02

2002-03

2003-04

2004-05 2005-06

2006-07

Bed Wear Quantity

Tons

147,933

181,627

241,886

244,207

264,442 365,.237

365,232

Value

000$

734,919

918,505

1,329,064

1,383,334

1,449,533

2,038,064

1,995,899

Value

$/KG.

4.97 5.06 5.49 5.66 5.57 5.58 5.46

Maximum efforts should be mobilized to increase the production of raw cotton with regards to increase in yield per acre and fiber quality.

Ginning research institution should be established to support ginning industry.

Availability of uninterrupted gas and economical power and soft water for the textile industry should be provided on war footing.

The Government should encourage and provide incentives to the Engineering Industry to bring in foreign investment and know-how to manufacture quality Textile machinery locally.

Labour training institutes, poly techniques and universities with minimal or no charges and scholarships and stipends should be established across the country by the Government in collaboration with the private sector, philanthropists and overseas educationl grants.

Import of machinery older than 10 years should be banned.

Promote air jet weaving machinery for cotton and blended fabric.

Upgrade smaller units of power looms to auto looms.

Priority should be given to stitching industry sector that leads to high value addition and incentives for labour training to increase productivity and improve quality should be made available.

Efforts on part of the Government should me made to provide market access for our manufacturers and the benefits enjoyed by our competitors in overseas markets should be made available for our local textile industry.

Incentives should be provided by the Government to find new markets across the Globe for our textile products.

Mark-up on loans for the Textile Industry should be reduced.