Embed Size (px)

Citation preview

Paint Industry – India

February 2015

2 PAINT INDUSTRY IN INDIA 2015. PPT

Executive Summary

Market

The paint industry in India was estimated to be valued at around INR x bn and is expected to attain a CAGR of about xx% to reach INR y bn by 2018

In 2013, decorative paints accounted for about aa% of the overall market

The overall decorative paint segment is price sensitive, whereas the industrial paint segment is heavily technology oriented

Drivers & Challenges

Competition

Drivers – Growth in Real-estate Construction – Growth in Automotive Industry – Increase in Disposable Income – Increased Government Expenditure

on Infrastructure – Growth in Industrial Sector – Low Penetration

Challenges

– Increase in input prices

– Stringent environmental regulations

Major Players

Company A Company B Company C

Company D Company E Company F

Color experimentation

Customer participation with value added services

Environment friendly paint

Trends

New trademarks and patents flood the sector

Increasing demand for emulsions

Small size packs

3 PAINT INDUSTRY IN INDIA 2015. PPT

•Macro Economic Indicators

•Introduction

•Market Overview

•Import-Export

•Drivers & Challenges

•Trends

•Competition

•Strategic Recommendations

•Appendix

4

Economic Indicators (-/-)

GDP at Factor Cost: Quarterly

Inflation Rate: Monthly

11

12

13

14

15

INR tn

Q4

c4

d2 c2

b2 a2

Q1

d1 b4

a4

Q3

c3

b3

a3

Q2

c1

b1

a1

2013-14 2012-13 2011-12 2010-11

0.0

0.5

1.0

1.5

2.0

%

Oct 2013 - Nov 2013

t

Sep 2013 - Oct 2013

s

Aug 2013 - Sep 2013

r

Jul 2013 - Aug 2013

q

Jun 2013 - Jul 2013

p

PAINT INDUSTRY IN INDIA 2015. PPT

5 PAINT INDUSTRY IN INDIA 2015. PPT

Indian paints industry has been successful in registering double digit growth figures

Paints Industry India – Overview

Paints Industry India – Market Size Paints Industry India – Segmentation (2013)

0

100

200

300

400

500

600

INR bn

X

2018e

a6

2017e

a5

2016e

a4

2015e

a3

2014e

a2

2013

a1

X

Y

YY XX

• The Indian paints market is poised to grow at a steady CAGR of about xx% during 2013 – 18, wherein the decorative paints segment will continue to dominate the overall market

Currently, about x% of the overall market is dominated by the decorative paints segment, wherein the demand for such paints mainly arises from household paintings, architectural and other display purposes – The demand curve reaches its peak during the festive season in India

The remaining market comprises mainly of the industrial paints, wherein the demand comes mostly from automotive engineering and consumer durable segments

• The overall decorative paint segment is price sensitive, whereas the industrial paint segment is heavily technology oriented

6 PAINT INDUSTRY IN INDIA 2015. PPT

Paint Industry – Supply Chain

• X

Decorative Products: XX

• XX • XX • XX • XX

Major Inputs Major Products End User

• X

• X

Industrial Products:

XX

• XX • XX • XX • XX

7 PAINT INDUSTRY IN INDIA 2015. PPT

Sales and distribution channels that organizations have established towards maximizing revenues

X

Dealers Modern Retail Format

• XX

• XX

• XX

• XX

• XX

• XX

• XX

• XX

• XX

• XX

• XX

• XX

XX

8 PAINT INDUSTRY IN INDIA 2015. PPT

Indian Paint Industry – Exports & Imports

E

D

C

B

A

0%

HS Code XX

c1

c2

c3

c4

HS Code XX

b1

b2

b3

b4

HS Code XX

a1

a2

a3

a4

2013 - 2014 2012 - 2013 2011 - 2012 2010 - 2011

Paints Industry India – Imports

HS Code Total Import – Last 4 years (INR bn)

XX XX

XX XX

XX XX

E

D

C

B

A

0%

HS Code XX

c1

c2

c3

c4

HS Code XX

b1

b2

b3

b4

HS Code XX

a1

a2

a3

a4

2013 - 2014 2012 - 2013 2011 - 2012 2010 - 2011

Paints Industry India – Exports

HS Code Total Export– Last 4 years (INR bn)

XX XX

XX XX

XX XX

9 PAINT INDUSTRY IN INDIA 2015. PPT

Boom in Indian real estate sector, specifically housing, has been a key driver for growth of decorative paint

• XX

• XX

• XX

• XX

• XX

• XX

• XX

Growth in Real - estate Construction Impact

Real - estate Market – Segregation Real - estate Market – Size & Growth

Real-estate

Residential

• XX • XX • XX

Commercial

• XX • XX • XX

C

B

A

0

INR tn

X

2018e

a6

2017e

a5

2016e

a4

2015e

a3

2014e

a2

2013

a1

10

Increased spending by government on infrastructure provides a fillip to paint sector

• Post 2014 general elections, there has been a solid stabilization political scenario, which in turn

has initiated the roll out of an array of infrastructural projects across the country

• With more Government spending on infrastructure and higher manufacturing activities, paint

industry is expected to be uplifted

Growth in infrastructure activities would refer to more demand for industrial paints

• Furthermore, the decision of encouraging the adoption of public private partnership based

models for the ongoing projects is expected to drive faster completion of the projects

Increased Government Expenditure on Infrastructure Impact

PAINT INDUSTRY IN INDIA 2015. PPT

Government Investment – Infrastructure Sector

D

C

B

A

0.0

INR tn

XX

2014-2015

y

2013-2014

x • XX • XX • XX • XX • XX • XX • XX • XX • XX

11

SAMPLE

PAINT INDUSTRY IN INDIA 2015. PPT

• There are certain environmental regulations that govern the paint sector in India

• In India, there are some agencies that conduct standard and quality checks regularly to determine whether standards are being met by the players or not

Some such environmental agencies include the Ministry of Environment and Forests, Central Pollution Control Board, National Referral Centre on Lead Poisoning, and other state government agencies – Various companies in this segment need to comply with the set standards in order to remain in business and be competitive

Stringent Environmental Regulations Impact

Concerns

National Referral Centre for Lead Poisoning in India (NRCLPI)

• X

Bureau of Indian Standards (BIS)

• X

Department of Industrial Promotion and Policy (DIPP)

• X

Environmental regulations pose as a deterrent to this market

12

SAMPLE

PAINT INDUSTRY IN INDIA 2015. PPT

Colour is the most expressive option of personalizing one’s home and giving it an individualized touch

• Consumers look to develop a unique identity and have shown interest in experimenting with colours

This is forcing paint companies to look at new colors and different finishes

• Recent trends show that conservative paints make way for unique preferences

Emulsion paints for interiors are being preferred more than distempers

For exteriors, emulsion based coatings are preferred against conventional cement based coatings

• With continuous lookout for superior quality as well as diversified products, consumers are switching to marginally higher priced emulsions with higher durability and wider range of colors

• Geography, fashion and home architecture primarily determines color preferences in India

Colour experimentation

Exclusivity drives color preferences

• BB

• BB

• BB

XX

• CC

• CC

• CC

XX

• AA

• AA

• AA

XX

13

SAMPLE In a bid to garner high revenues, players are turning towards water based paints

• Major players are seen to shift their focus towards emulsions with a view to expand operating margins in the future

• Demand for emulsions continue to outnumber enamels and distempers as water based paint is not only a high growth category but also generates higher margins compared to solvent based paints

Increasing demand for emulsions

Emulsions to overpower

enamels and primers

X X X

X X X

XX

PAINT INDUSTRY IN INDIA 2015. PPT

14

SAMPLE Porter’s Five Forces Analysis

PAINT INDUSTRY IN INDIA 2015. PPT

Competitive Rivalry • X

Bargaining Power of Suppliers • X

Bargaining Power of Buyers • X

Threat of New Entrants • X

Impact XX

Impact XX

Impact XX

Impact XX

Threat of Substitutes • X

Impact XX

15

SAMPLE Competitive Benchmarking (-/-)

Public Trading Comparables (FY 2014)

Company A Company B Company C

Market Capitalization

(INR mn) XX XX XX

Share Price (INR) XX XX XX

EV/EBITDA (x) XX XX XX

EV/Revenue (x) XX XX XX

PE Ratio XX XX XX

Note: Top 3 Public companies based on the revenue; Market Capitalization and Share Price is as on 27/10/2014; PE Ratio is as on 5/11/2014

PAINT INDUSTRY IN INDIA 2015. PPT

16

SAMPLE Key Ratios of Top 3 Companies – Operational Basis (FY 2014) (1/4)

Competitive Benchmarking (-/-)

0

D

C

B

A

Company C

c3 c2

c1

Company B

b3 b2

b1

Company A

a3 a2

% a1

Net Margin Operating Margin Gross Margin

• XX

• XX

• XX

• XX

PAINT INDUSTRY IN INDIA 2015. PPT

17

SAMPLE

Key People

Products and Services

Corporate Address XX

Tel No. XX

Fax No. XX

Website XX

Year of Incorporation XX

Ticker Symbol XX

Stock Exchange XX

Name Designation

XX XX

XX XX

XX XX

Head Office

Gurgaon

Category Products/Services

XX XX

XX XX

Company Information Offices and Centres – India

PAINT INDUSTRY IN INDIA 2015. PPT

Public: Domestic Company – Company A (1/5)

18

SAMPLE Financial Snapshot Key Ratios

Financial Summary

• The company earned a net profit of INR 1.5 bn in FY 2014, as compared to net profit of INR 2.2 bn in FY 2013

• The company reported total income of INR 26.1 bn in FY 2014, as compared to INR 25 bn in FY 2013

• The company earned an operating margin of 6.01% in FY 2014, a decrease of 0.10 percentage points over FY 2013

Key Financial Performance Indicators

Indicators Value (27/10/2014) Market Capitalization (INR mn) 63,106.2

Total Enterprise Value (INR mn) 56,598.2

EPS (INR)* 36.55

PE Ratio (Absolute)* 35.15

Particulars y-o-y change

(2014-13) 2014 2013 2012 2011

Profitability Ratios

Operating Margin -0.10 6.01% 6.11% 6.43% 9.42%

Net Margin -2.99 5.75% 8.74% 8.89% 13.49%

Profit Before Tax Margin -3.37 7.79% 11.15% 10.85% 16.79%

Return on Equity -2.08 17.72% 19.80% 14.00% 16.18%

Return on Capital Employed 3.83 16.66% 12.83% 9.56% 10.59%

Return on Working Capital 20.46 61.92% 41.45% 15.35% 13.55%

Return on Assets 1.07 7.70% 6.63% 6.61% 8.01%

Return on Fixed Assets -3.75 29.43% 33.18% 39.32% 78.84%

Cost Ratios

Operating costs (% of Sales) 0.37 93.46% 93.10% 92.60% 88.66%

Administration costs (% of Sales)

0.28 25.23% 24.96% 25.48% 29.90%

Interest costs (% of Sales) -0.34 0.02% 0.36% 0.15% 0.07%

Liquidity Ratios

Current Ratio -7.50% 1.23 1.33 2.39 3.42

Cash Ratio -31.02% 0.64 0.93 1.58 2.70

Leverage Ratios

Debt to Equity Ratio N.A. N.A. N.A. N.A. N.A.

Debt to Capital Ratio N.A. N.A. N.A. N.A. N.A.

Interest Coverage Ratio 1269.1% 261.50 19.10 48.63 154.13

Efficiency Ratios

Fixed Asset Turnover -6.33% 4.50 4.81 5.31 6.95

Asset Turnover 22.60% 1.18 0.96 0.89 0.71

Current Asset Turnover 19.05% 1.78 1.49 1.21 0.85

Working Capital Turnover 57.73% 9.47 6.01 2.07 1.19

Capital Employed Turnover 41.37% 2.83 2.00 1.37 1.00

Improved Decline

Net Profit/Loss Total Income

0

3

2

1

30

20

10

0

INR bn INR bn

2014

1.5

26.1

2013

2.2

25.0

2012

2.0

22.7

2011

1.8

13.1

Public: Domestic Company – Company A (2/5)

PAINT INDUSTRY IN INDIA 2015. PPT

*: Data corresponds to 05/11/2014

19

SAMPLE

98% 96% 96% 96%

0%

50%

100%

2014

4%

2013

4%

2012

4%

2011

2%

100% 97% 96% 98%

0%

50%

100%

2014

2%

2013

4%

2012

3%

2011

0%

Outside India India

Business Highlights (1/2)

Description News

Overview

•XX

•XX

•XX

•XX

•XX

Others Coatings

Key Business Segments Key Geographic Segments

Public: Domestic Company – Company A (3/5)

PAINT INDUSTRY IN INDIA 2015. PPT

20

SAMPLE Description News

Product Portfolio •XX

Prior Investors •XX

Current and Pending Subsidiaries/ Investments •XX

Business Highlights (2/2)

Public: Domestic Company – Company A (4/5)

PAINT INDUSTRY IN INDIA 2015. PPT

21

SAMPLE

• XX • XX

• XX • XX

T O

W S Strength Weakness

Opportunity Threat

Public: Domestic Company – Company A (5/5)

PAINT INDUSTRY IN INDIA 2015. PPT

22

SAMPLE Private: Domestic Company – Company B(1/5)

Corporate Address XX

Tel No. XX

Fax No. XX

Website XX

Year of Incorporation XX

Company Information Offices and Centres – India

Head Office

Mumbai

Key People

Products and Services

Name Designation

XX XX

XX XX

XX XX

Category Products/Services

XX XX

XX XX

PAINT INDUSTRY IN INDIA 2015. PPT

23

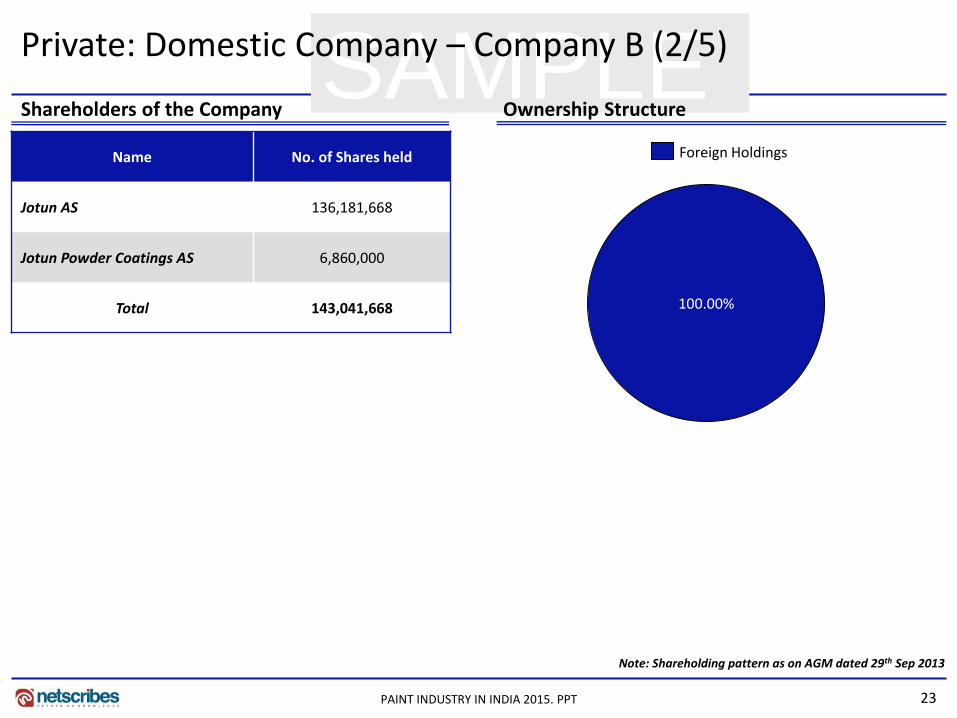

SAMPLE Name No. of Shares held

Jotun AS 136,181,668

Jotun Powder Coatings AS 6,860,000

Total 143,041,668 100.00%

Foreign Holdings

Note: Shareholding pattern as on AGM dated 29th Sep 2013

Private: Domestic Company – Company B (2/5)

Shareholders of the Company Ownership Structure

PAINT INDUSTRY IN INDIA 2015. PPT

24

SAMPLE Private: Domestic Company – Company B (3/5)

Financial Snapshot Key Ratios

Financial Summary

• The company incurred a net profit of negative INR 526.6 mn in FY 2014, as compared to net profit of negative INR 461.9 mn in FY 2013

• The company reported total income of INR 2964 mn in FY 2014, as compared to INR 2929.4 mn in FY 2013

• The company earned an operating margin of negative 10.03% in FY 2014, a decrease of 0.05 percentage points over FY 2013

• The company reported debt to equity ratio of 1.21 in FY 2014, as compared to 2 in FY 2013

Particulars y-o-y change

(2013-12) 2013 2012 2011 2010

Profitability Ratios

Operating Margin -0.05 -10.03% -9.99% -5.46% -1.21%

Net Margin -2.00 -17.77% -15.77% -13.43% -9.27%

Profit Before Tax Margin -2.68 -8.33% -5.65% -5.19% -1.00%

Return on Equity 7.96 -47.79% -55.75% -86.95% -27.04%

Return on Capital Employed -0.46 -12.22% -11.75% -7.68% -1.78%

Return on Working Capital 5.14 -26.10% -31.24% -60.47% -5.55%

Return on Assets -0.19 -9.20% -9.00% -5.47% -1.27%

Return on Fixed Assets 4.70 -36.49% -41.20% -23.25% -4.34%

Cost Ratios

Operating costs (% of Sales) -0.23 110.21% 110.44% 105.48% 101.22%

Administration costs (% of Sales)

N.A. N.A. N.A. N.A. N.A.

Interest costs (% of Sales) N.A. N.A. N.A. N.A. N.A.

Liquidity Ratios

Current Ratio 20.02% 1.93 1.61 1.14 1.48

Cash Ratio 13.87% 0.37 0.32 0.03 0.15

Leverage Ratios

Debt to Equity Ratio -39.67% 1.21 2.00 3.60 0.99

Debt to Capital Ratio -17.96% 0.55 0.67 0.78 0.50

Interest Coverage Ratio N.A. N.A. N.A. N.A. N.A.

Efficiency Ratios

Fixed Asset Turnover -9.41% 3.58 3.95 4.25 3.57

Asset Turnover 4.45% 0.90 0.86 1.00 1.04

Current Asset Turnover 8.84% 1.23 1.13 1.33 1.49

Working Capital Turnover -14.57% 2.56 2.99 11.04 4.57

Capital Employed Turnover -21.83% 2.64 3.38 6.46 2.91

Improved Decline

PAINT INDUSTRY IN INDIA 2015. PPT

Net Profit/Loss Total Income

-200

-400

-600 0

4,000 0

2,000

-410.2

INR mn

2,929.4

2012

3,053.7

-526.6

2,964.0

2011

INR mn

2014 2013

-461.9 -238.4

2,572.6

25

SAMPLE Private: Domestic Company – Company B (4/5)

Business Highlights

PAINT INDUSTRY IN INDIA 2015. PPT

Description News

Overview XX

Extended Product Segments XX

26

SAMPLE

XX XX

XX XX

T O

W S

Private: Domestic Company – Company B (5/5)

Strength Weakness

Opportunity Threat

PAINT INDUSTRY IN INDIA 2015. PPT

27

Thank you for the attention

About Netscribes, Inc. Netscribes, Inc. is a knowledge-consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment & business research, business & corporate intelligence, content-management services, and knowledge-software services. At its core lies a true value proposition that draws upon a vast knowledge base. Netscribes, Inc. is a one-stop shop designed to fulfil clients’ profitability and growth objectives.

Paint Industry – India report is part of Netscribes’ Retail and Services Series. For any queries or customized research requirements, contact us at:

Disclaimer: This report is published for general information only. Although high standards have been used in the preparation, “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the sole property of Netscribes and prior permission is required for guidelines on reproduction.

Phone: +91 22 4098 7600 E-Mail: [email protected]

PAINT INDUSTRY IN INDIA 2015. PPT