Embed Size (px)

Citation preview

abcGlobal Research

“Things change quickly in this business, Coco… As long as you have a seat at the table,

you have a chance. The greatest value in shipping is option value” – The Shipping Man

Time to reassess: We have been underweight on Pacific Basin since end-2012 as we saw at

least two years of earnings disappointment at the time. The earnings compression was worse

than we thought but is about to pass. We are still 33-40% below consensus on 2015-16e EPS

and believe the Street’s optimism doesn’t factor in the ease of supply creation in the sector. On

the positive side, however, we beliepve a volatile path to mid-single-digit RoE is intact since

the worst of supply growth is over. A PB of 0.8x also appears to be attractive relative to the

stock’s historical valuation.

Resilience of valuations: Our target prices in the past two years have been in the range of

a 0.5-0.6x PB, which we deemed appropriate for a low-single-digit RoE firm with a cost

of equity of c.8%. But the stock has held onto its typical post-crisis PB range of 0.8-1.1x

despite much weaker fundamentals. One of the reasons why this has happened could be

the stock’s good record of return generation when acquired at a PB of less than 0.67x.

Market-wide multiple expansion could be another reason – our analysis shows a clear

uplift in multiples even in stocks with no earnings improvement.

The value of volatility: There could be one more reason for the higher valuations.

Investors possibly appreciate the value that an unanticipated surge in freight rates can

create. It’s not just the possibility of windfall profits but also of beefy stock returns. Much

like the freight rate spike in 4Q13, short-term rallies masquerade as a recovery and are even

priced like a one. This volatility adds an option to bulk equities – it’s an option which

prices the known unknowns and known unknowns are rather frequent in bulk markets.

Raise TP to HKD4.93 (from HKD3.0) at a PB of 1.0x; upgrade to OW from UW: The

complex nature of demand and supply and the inability to forecast near-term rates crystallize

investor focus on valuations. Multiple expansion and a consistent post-crisis trading range have

raised the PB floor to 0.8x. Investors can argue that a target PB of 1.0x looks excessive for a

single-digit RoE company. But, we believe this is true only till one discovers that volatility has

a value too. We think the current low rates will trigger slow-steaming and yet another rate

spike as well as a rerating towards the top of the trading band of 0.8-1.1x.

Pacific Basin (2343 HK)

Upgrade to OW: Recalibrating valuations

We have been right on earnings for the last two years…

…but wrong on valuation, so we are changing our approach

Upgrade to Overweight from Underweight with TP of HKD4.93 (from HKD3.0), implying a 2015e PB of 1.0x

Industrials Marine Equity – Hong Kong

Company report

Index^ HANG SENG INDEXIndex level 22,933RIC 2343.HKBloomberg 2343 HK

Source: HSBC

Overweight Target price (HKD) 4.93 Share price (HKD) 3.98 Forecast dividend yield (%) 2.0 Potential return (%) 25.9

Note: Potential return equals the percentage difference between the current share price and the target price, plus the forecast dividend yield

Dec 2013 a 2014 e 2015 e

HSBC EPS 0.00 -0.01 0.03 HSBC PE 18.8

Performance 1M 3M 12M

Absolute (%) -16.2 -17.1 -24.2 Relative^ (%) -7.5 -14.9 -23.3

Enterprise value (USDm) 1575Free float (%) 98Market cap (USDm) 993Market cap (HKDm) 7,709

Source: HSBC

6 October 2014

Shishir Singh* Analyst The Hongkong and Shanghai Banking Corporation Limited +852 2822 4292 [email protected]

Mark Webb* Head of Conglomerate and Transport Research, Asia Pacific The Hongkong and Shanghai Banking Corporation Limited +852 2996 6574 [email protected]

View HSBC Global Research at: http://www.research.hsbc.com

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

2

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Financials & valuation Financial statements

Year to 12/2013a 12/2014e 12/2015e 12/2016e

Profit & loss summary (USDm)

Revenue 1,709 1,757 1,744 1,831EBITDA 123 113 196 230Depreciation & amortisation -81 -101 -104 -111Operating profit/EBIT 42 12 91 119Net interest -37 -33 -37 -43PBT 3 -84 54 77HSBC PBT 0 -18 54 77Taxation -1 -1 -1 -2Net profit 2 -84 53 75HSBC net profit -1 -18 53 75

Cash flow summary (USDm)

Cash flow from operations -36 148 209 284Capex -458 -213 -192 -277Cash flow from investment -114 -198 -192 -277Dividends -12 -12 -20 -21Change in net debt 374 84 39 56FCF equity -402 -195 -37 -91

Balance sheet summary (USDm)

Intangible fixed assets 25 25 25 25Tangible fixed assets 1,714 1,717 1,803 1,967Current assets 765 529 523 505Cash & others 485 302 302 302Total assets 2,537 2,327 2,406 2,519Operating liabilities 196 191 200 219Gross debt 1,037 938 977 1,033Net debt 552 636 676 732Shareholders funds 1,304 1,197 1,229 1,266Invested capital 1,823 1,779 1,850 1,976

Ratio, growth and per share analysis

Year to 12/2013a 12/2014e 12/2015e 12/2016e

Y-o-y % change

Revenue 18.4 2.8 -0.8 5.0EBITDA -7.2 -8.3 73.9 17.6Operating profit -39.8 -72.0 676.2 30.7PBT -3136.2 42.3HSBC EPS -102.1 42.3

Ratios (%)

Revenue/IC (x) 1.0 1.0 1.0 1.0ROIC 2.5 0.7 5.0 6.2ROE -0.1 -1.5 4.4 6.0ROA 1.3 0.1 3.8 4.7EBITDA margin 7.2 6.4 11.2 12.6Operating profit margin 2.5 0.7 5.2 6.5EBITDA/net interest (x) 3.3 3.4 5.2 5.4Net debt/equity 42.4 53.2 55.0 57.8Net debt/EBITDA (x) 4.5 5.7 3.5 3.2CF from operations/net debt 23.2 30.9 38.8

Per share data (USD)

EPS reported (fully diluted) 0.00 -0.04 0.03 0.04HSBC EPS (fully diluted) 0.00 -0.01 0.03 0.04DPS 0.01 0.01 0.01 0.02Book value 0.68 0.62 0.64 0.66

Key forecast drivers

Year to 12/2013a 12/2014e 12/2015e 12/2016e

Handysize revenue days 52,550 54,200 54,810 57,150Handysize Avg TCE (USD/day) 9,520 10,100 10,088 10,595Handymax revenue days 20,660 23,160 23,850 24,750Handymax Avg TCE (USD/day) 10,744 11,181 12,372 12,625Handysize Spot (USD/day) 8,191 8,977 9,426 9,898Handymax Spot (USD/day) 10,296 10,903 11,449 12,021

Valuation data

Year to 12/2013a 12/2014e 12/2015e 12/2016e

EV/sales 0.9 0.9 0.9 0.9EV/EBITDA 12.3 14.0 8.3 7.4EV/IC 0.8 0.9 0.9 0.9PE* 18.8 13.2P/Book value 0.8 0.8 0.8 0.8FCF yield (%) -41.9 -20.8 -3.9 -9.4Dividend yield (%) 1.3 2.0 2.1 3.8

Note: * = Based on HSBC EPS (fully diluted)

Price relative

Source: HSBC Note: price at close of 03 Oct 2014

22.533.544.555.566.5

22.5

33.5

44.5

55.5

66.5

2012 2013 2014 2015Pacific Basin Shipping Rel to HANG SENG INDEX

3

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Earnings compression passes; off to mid-single-digit RoEs now

Pacific Basin has led the sector in buying vessels during the most recent freight rate upturn. The company

has close to doubled its fleet by buying used vessels from the sale and purchase market in 2013 and has

ordered new builds, which should take its tally to 100 Handysize and Handymax ships by 2016. The rapid

build-out of the company’s fleet shows management’s confidence in the dry bulk recovery. The rise in

new orders last year is a signal that this confidence was rather broad-based. The pace of recovery,

however, has underwhelmed most and resulted in a much-needed slowdown in new orders.

The company’s fleet expansion over the last two years has built in substantial operating leverage and

earnings ability, if rates were to move up. A fleet of 100 owned ships in 2016 would be capable of

generating around 35,000 revenue days in a year at a fixed all-in cost of USD9,200-9,500/day, one third

of which is non-cash depreciation. This means that if the company’s future performance is similar to its

worst in the past, the company would barely cover its costs and achieve break-even on the net profit level

(i.e. its RoE would be around 0%).

Recalibrating valuations

Although we were right in forecasting earnings compression in

2013-14, we have been wrong on valuation

Market-wide multiple expansion and hope of recovery has helped

the stock remain well-supported in a PB range of 0.8-1.1x

We shift to new valuation approach which accounts for these

factors and raise our target price to HKD4.93, implying a 1.0x PB

Pacific Basin owned fleet - number of ships New orders (DWT mn) have slowed down in the sector

Source: Company (includes Newbuildings on order in 2014-16) Source: Clarksons

0

20

40

60

80

100

120

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Handysize Handymax

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

H'size H'max P'max C'size

New orders in 2013 revisited the highs lastseen during early 2010

4

Pacific Basin (2343 HK) Marine 6 October 2014

abc

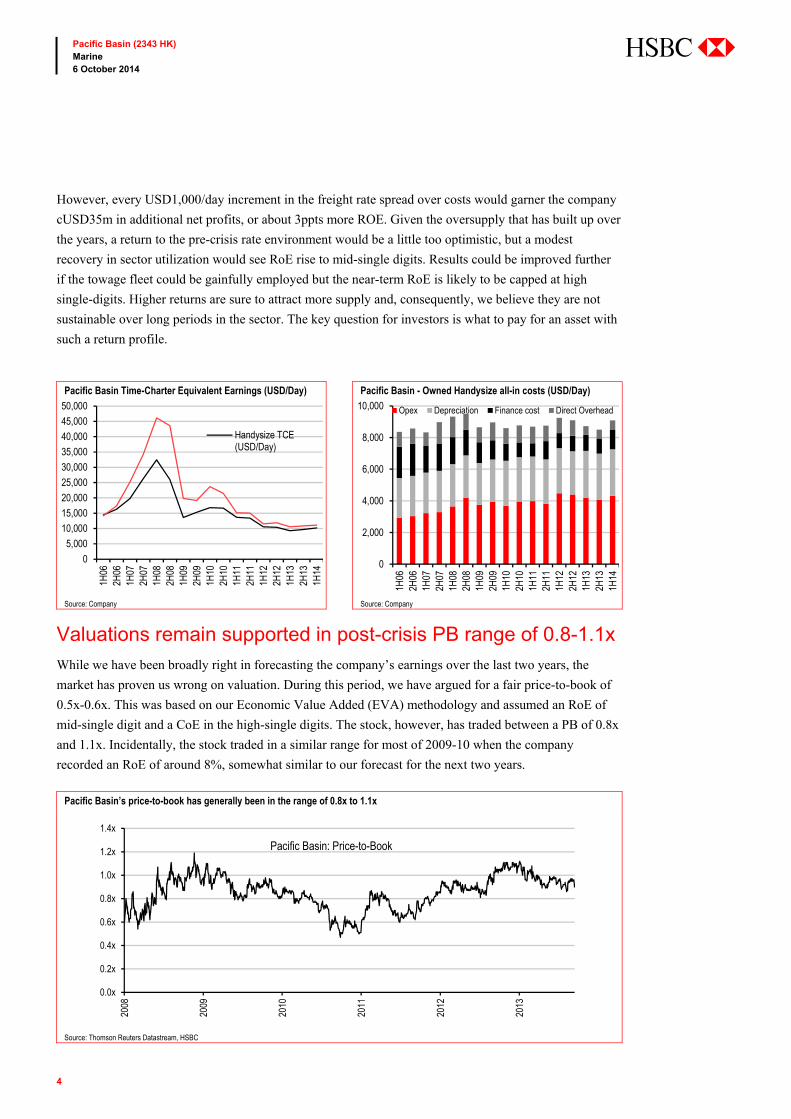

However, every USD1,000/day increment in the freight rate spread over costs would garner the company

cUSD35m in additional net profits, or about 3ppts more ROE. Given the oversupply that has built up over

the years, a return to the pre-crisis rate environment would be a little too optimistic, but a modest

recovery in sector utilization would see RoE rise to mid-single digits. Results could be improved further

if the towage fleet could be gainfully employed but the near-term RoE is likely to be capped at high

single-digits. Higher returns are sure to attract more supply and, consequently, we believe they are not

sustainable over long periods in the sector. The key question for investors is what to pay for an asset with

such a return profile.

Valuations remain supported in post-crisis PB range of 0.8-1.1x

While we have been broadly right in forecasting the company’s earnings over the last two years, the

market has proven us wrong on valuation. During this period, we have argued for a fair price-to-book of

0.5x-0.6x. This was based on our Economic Value Added (EVA) methodology and assumed an RoE of

mid-single digit and a CoE in the high-single digits. The stock, however, has traded between a PB of 0.8x

and 1.1x. Incidentally, the stock traded in a similar range for most of 2009-10 when the company

recorded an RoE of around 8%, somewhat similar to our forecast for the next two years.

Pacific Basin Time-Charter Equivalent Earnings (USD/Day) Pacific Basin - Owned Handysize all-in costs (USD/Day)

Source: Company Source: Company

Pacific Basin’s price-to-book has generally been in the range of 0.8x to 1.1x

Source: Thomson Reuters Datastream, HSBC

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1H06

2H06

1H07

2H07

1H08

2H08

1H09

2H09

1H10

2H10

1H11

2H11

1H12

2H12

1H13

2H13

1H14

Handysize TCE(USD/Day)

0

2,000

4,000

6,000

8,000

10,0001H

062H

061H

072H

071H

082H

081H

092H

091H

102H

101H

112H

111H

122H

121H

132H

131H

14

Opex Depreciation Finance cost Direct Overhead

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

1.4x

2008

2009

2010

2011

2012

2013

Pacific Basin: Price-to-Book

5

Pacific Basin (2343 HK) Marine 6 October 2014

abc

The divergence between our valuation view and that of the market has forced us to reconsider our

valuation methodology. The regression analysis on last nine years of data suggests that buying Pacific

Basin between a price-to-book of 0.67x-1.0x in the post-crisis period would have generated positive

returns over a 6-month period. Admittedly, this is a fairly wide range which involves both the good and

the bad years. 2011, for example, was a difficult year from a return generation perspective, since any

purchase of Pacific Basin stock over a price-to-book of 0.67x yielded negative returns. On the other hand,

2013 was a fairly good year with the valuation threshold for generating positive returns being at a higher

PB level of 0.88x.

We have tried to capture the gist of this analysis through the chart above. The channel described by the

two thick red lines for 2009 and 2011 underscores that a PB of 0.67x has been a fairly attractive level to

buy the stock in post-crisis period. At the same time, an acquisition price over a PB valuation of 1x has

typically resulted in negative returns.

2011: 6m returns generally negative above a PB of 0.67x 2013: 6m returns generally negative above a PB of 0.88x

Source: Thomson Reuters Datastream, HSBC Source: Thomson Reuters Datastream, HSBC

Depending upon how bad or good a year has been, the 6-month forward returns would be positive if the valuation of Pacific Basin stock at the time of buying the stock was in the price-to-book range of 0.67x-1.00x

Source: Thomson Reuters Datastream, HSBC

y = -152.85x + 98.48

-60

-40

-20

0

20

40

60

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

6m p

rice

retu

rn (%

)

Price-to-Book (trailing)

y = -140.29x + 139.2

-30

-20

-10

0

10

20

30

40

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

6m p

rice

retu

rn (%

)Price-to-Book (trailing)

-250.0

-200.0

-150.0

-100.0

-50.0

0.0

50.0

100.0

150.0

200.0

250.0

0.00

x0.

05x

0.10

x0.

15x

0.20

x0.

25x

0.30

x0.

35x

0.40

x0.

45x

0.50

x0.

55x

0.60

x0.

65x

0.70

x0.

75x

0.80

x0.

85x

0.90

x0.

95x

1.00

x1.

05x

1.10

x1.

15x

1.20

x1.

25x

1.30

x1.

35x

1.40

x1.

45x

1.50

x1.

55x

1.60

x1.

65x

1.70

x1.

75x

1.80

x1.

85x

1.90

x1.

95x

2.00

x

6-m

onth

retu

rns

(%)

Trailing Price-to-Book 2005 2013 2006 2007 2008 2009 2010 2011 2012

6

Pacific Basin (2343 HK) Marine 6 October 2014

abc

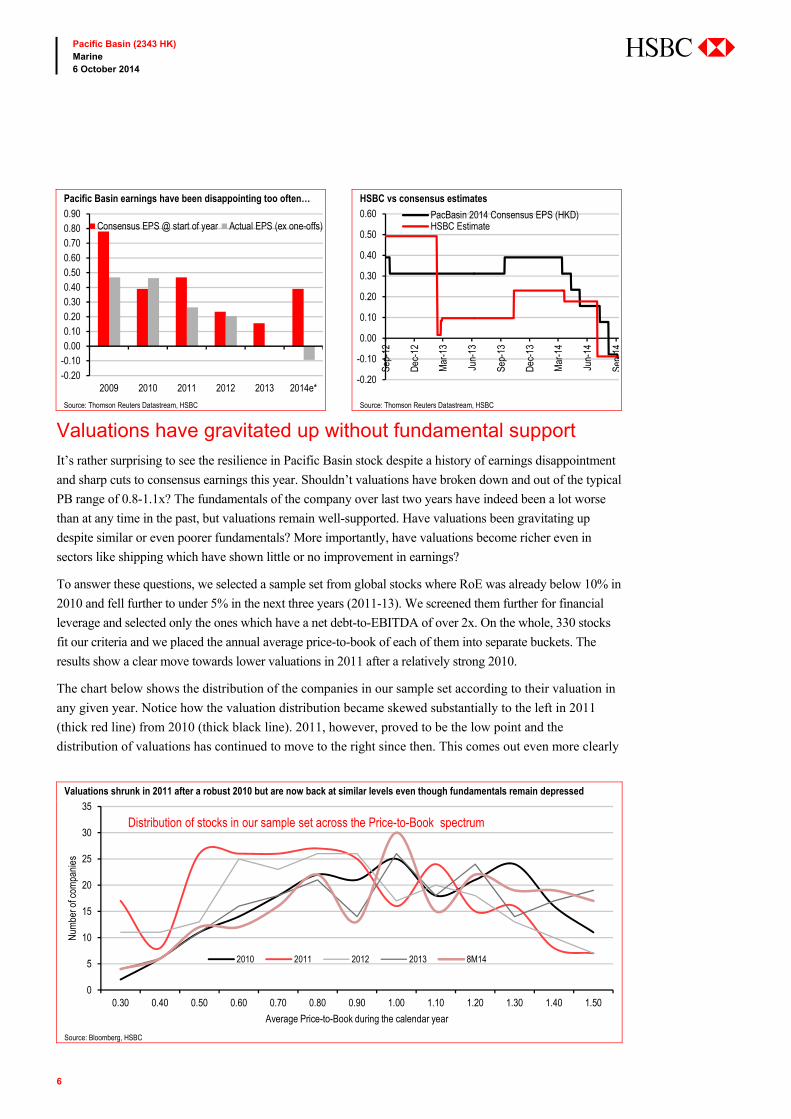

Valuations have gravitated up without fundamental support It’s rather surprising to see the resilience in Pacific Basin stock despite a history of earnings disappointment

and sharp cuts to consensus earnings this year. Shouldn’t valuations have broken down and out of the typical

PB range of 0.8-1.1x? The fundamentals of the company over last two years have indeed been a lot worse

than at any time in the past, but valuations remain well-supported. Have valuations been gravitating up

despite similar or even poorer fundamentals? More importantly, have valuations become richer even in

sectors like shipping which have shown little or no improvement in earnings?

To answer these questions, we selected a sample set from global stocks where RoE was already below 10% in

2010 and fell further to under 5% in the next three years (2011-13). We screened them further for financial

leverage and selected only the ones which have a net debt-to-EBITDA of over 2x. On the whole, 330 stocks

fit our criteria and we placed the annual average price-to-book of each of them into separate buckets. The

results show a clear move towards lower valuations in 2011 after a relatively strong 2010.

The chart below shows the distribution of the companies in our sample set according to their valuation in

any given year. Notice how the valuation distribution became skewed substantially to the left in 2011

(thick red line) from 2010 (thick black line). 2011, however, proved to be the low point and the

distribution of valuations has continued to move to the right since then. This comes out even more clearly

Valuations shrunk in 2011 after a robust 2010 but are now back at similar levels even though fundamentals remain depressed

Source: Bloomberg, HSBC

Pacific Basin earnings have been disappointing too often… HSBC vs consensus estimates

Source: Thomson Reuters Datastream, HSBC Source: Thomson Reuters Datastream, HSBC

0

5

10

15

20

25

30

35

0.30 0.40 0.50 0.60 0.70 0.80 0.90 1.00 1.10 1.20 1.30 1.40 1.50

Num

ber o

f com

pani

es

Average Price-to-Book during the calendar year

2010 2011 2012 2013 8M14

Distribution of stocks in our sample set across the Price-to-Book spectrum

-0.20-0.100.000.100.200.300.400.500.600.700.800.90

2009 2010 2011 2012 2013 2014e*

Consensus EPS @ start of year Actual EPS (ex one-offs)

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

PacBasin 2014 Consensus EPS (HKD)HSBC Estimate

7

Pacific Basin (2343 HK) Marine 6 October 2014

abc

in a 37% increase in the median price-to-book in the first eight months of 2014 compared to 2011. Both

the median PB and the proportion of companies trading above a PB of 0.9x are higher now than in 2010.

A relevant question from the previous section is whether the multiple expansion has come along with any

improvement in fundamentals at all. Since we were interested in valuation of companies or sectors which

haven’t see much fundamental improvement, our sample selection process already excludes the stocks

which may have shown a RoE inflexion; however, here, we are more interested in the direction of RoE

over the last three years. After all, it’s easier to justify a build-up in valuation with even a marginal

improvement than nothing at all. However, unlike the valuation distribution which has moved towards

richer multiples, the distribution of RoE has remained largely unchanged between 2010 and 2013.

The results show through in the lower median RoE and the lower proportion of positive RoE companies

in 2013 when compared to 2010. The bottom line from our rather simplistic but broad-based analysis is

that multiples have expanded even where the fundamentals have gone in the other direction. In our view,

this has been the case with Pacific Basin as well.

Median PB of companies in our sample set % of companies in our sample set with PB of more than 0.9x

Source: Bloomberg, HSBC Source: Bloomberg, HSBC

Proportion of positive RoE companies has shrunk… …and the median RoE has turned negative during this time

Source: Bloomberg, HSBC Source: Bloomberg, HSBC

1.17x

0.92x1.04x

1.23x 1.26x

0.00x

0.20x

0.40x

0.60x

0.80x

1.00x

1.20x

1.40x

2010 2011 2012 2013 8M14

Median PB 76.2

58.966.0

76.5 77.8

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2010 2011 2012 2013 8M14

% Companies with PB>0.9x

63.058.8

48.8 50.9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2010 2011 2012 2013

+ve RoE % 1.05

0.14

-1.22

-0.79

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2010 2011 2012 2013

Median RoE (%)

8

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Pricing the known unknown

A good record of generating equity returns below an acquisition price-to-book of 0.67x and market-wide

multiple expansion seem to have contributed to the resilience of Pacific Basin’s stock despite weaker

fundamentals during 2013-14. Yet, there could be a third and a more fundamental reason for relatively pricier

valuation of dry bulk shipping stocks despite chronic oversupply and weak mid-term fundamentals.

Current price-to-book of dry bulk shipping stocks relative to their peak and trough since end of 2009

Source: Thomson Reuters Datastream, HSBC

Bulk shipping, by its nature, is a volatile sector with the possibility of generating ‘unpredictable’ windfall

gains from volatile rates and largely fixed costs. For example, as mentioned earlier in the report, Pacific

Basin’s owned fleet can add 3 percentage points of RoE through a mere USD1,000/day increase in rates.

A quick look at the distribution of rates even during the depressed down-cycle since 2011 is enough to

prove that shipping rates are a lot more volatile than that.

Distribution of Handysize & Handymax rates (USD/Day) since start of 2011

Source: Clarksons

0.89x

0.52x

1.08x

0.57x

1.57x1.68x

1.38x

0.72x 0.68x0.43x

0.81x

0.00x

0.50x

1.00x

1.50x

2.00x

2.50x

Paci

fic B

asin

Sino

trans

Shi

ppin

g

Chi

na C

osco

Chi

na S

hipp

ing

Dev

elop

men

t

U-M

ing

Prec

ious

Shi

ppin

g

Thor

esen

Tha

i

Nor

den

Nav

ios

Mrt,

. Hld

gs

Dry

Ship

s

Med

ian

0

20

40

60

80

100

120

140

160

180

200

<6000 6000-7000 7000-8000 8000-9000 9000-10000 10000-1100011000-1200012000-1300013000-14000 >14000

Num

ber o

f day

s si

nce

the

star

t of 2

011

Freight rates (USD/Day)

Handysize Handymax

9

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Investors need to recognize that bulk shipping rates are determined by the confluence of two complex factors:

Demand represented by multiple commodities spread across multiple geographic locations, and

Supply of ships, which is anything but constant due to slow-steaming and idling

It is true that the current oversupply in the sector, the ease of supply creation and availability of low-cost

credit are likely to cap a sustained increase in sector RoE, but it is also true that the above-mentioned

factors make forecasting rates and RoE in the short term nearly impossible. Add the persistent hopes of a

recovery to this inability to forecast near-term rates and it is easy to understand why many rate spikes in

the past have triggered a re-pricing of bulk equities. Much like the freight rate rally in 4Q13, short-term

deviations from the trend of single-digit RoE masquerade as a recovery and are even priced like a

recovery even though over-supply keeps reinforcing the longer-term trend.

We believe the unpredictable rate and return volatility warrants that the valuation in this sector be looked

in two parts:

Value of an equity generating mid-single-digit RoE, say, priced at a PB of 0.8x

Value of a call option on a higher RoE equity exercisable at a PB of 0.8x

Simplistically and alternatively, investors can view the valuation through a lens of probabilities:

Say, a 70% chance that they end up holding a mid-single-digit RoE equity over the next 12 months

And, a 30% chance that they end up holding a double-digit RoE equity

In our view, there is little merit in the precise quantification of the option value and the true benefit to the

investor is simply in cognizance of these two separate value components. Before we close this rather

academic-looking section, we must mention two important points on assessing the value of the call option:

The value of the call option is influenced by likely volatility of freight rates in the ‘future’ (not

historical volatility).

Oversupply curbs volatility and, hence, reduces the value of the option i.e. the greater the number of

ships relative to demand, the lesser the chances of an unpredictable surge in rates.

10

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Recalibrating valuations: Accounting for historical range, multiple expansion and the optionality in shipping equities

Given the lack of success of our EVA valuation methodology over the last two years, we discard it in

favour of a new approach based on factors identified in prior sections. In doing so, we wish to bridge the

difference between our view on Pacific Basin’s valuations and that of the market. At the expense of

repetition, these three factors are:

Typical historical trading range: Depending on how bad or good the year was for equity markets,

Pacific Basin shares have generated a positive return when acquired in the PB valuation range of

0.67-1.0x. Furthermore, the shares have commanded a PB in the range of 0.8x-1.1x irrespective of

the fundamentals since 2008 crisis.

Multiple-expansion in equity markets: Our cross-sector analysis suggests that valuations have

indeed gravitated up even in cases where fundamentals have deteriorated. Multiple expansion in

equity markets has helped justify valuations well over book value for stocks with depressed, near-

zero RoEs. Consequently, a bottom-of-the-cycle PB valuation doesn’t appear excessive.

Shipping option value: Bulk shipping equities are likely to be stuck at single-digit RoE levels but

investors may pay a premium for their ability to escape the long-term trend and generate windfall profits

from time to time. The value of this optionality has declined due to chronic oversupply, but we believe

the rate rally in 4Q13 is proof enough that the sector retains the ability to surprise in the short term.

Bulk shipping stocks like Pacific Basin trade on the basis hope and fear during typically long down-cycles

Source: HSBC

ValuePrice-to-Book

Downcycle Downcycle Downcycle Downcycle

Short-term demand-supply mismatch delivers windfall,

triggers hopes of recovery and, typically, higher valuations

Base equity value

Value of bulk shipping stocks

Time

4Q13 …NowPB~0.8x

PB~1.1x

Δ 4Q111H10

11

Pacific Basin (2343 HK) Marine 6 October 2014

abc

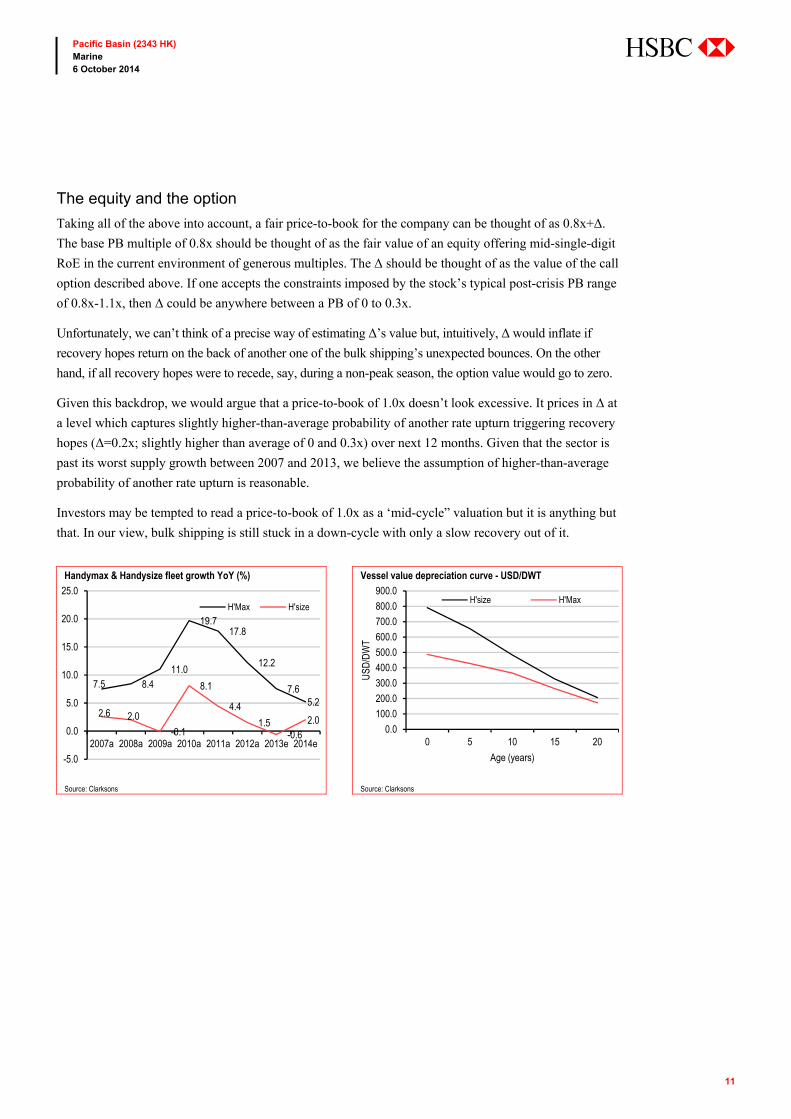

The equity and the option

Taking all of the above into account, a fair price-to-book for the company can be thought of as 0.8x+Δ.

The base PB multiple of 0.8x should be thought of as the fair value of an equity offering mid-single-digit

RoE in the current environment of generous multiples. The Δ should be thought of as the value of the call

option described above. If one accepts the constraints imposed by the stock’s typical post-crisis PB range

of 0.8x-1.1x, then Δ could be anywhere between a PB of 0 to 0.3x.

Unfortunately, we can’t think of a precise way of estimating Δ’s value but, intuitively, Δ would inflate if

recovery hopes return on the back of another one of the bulk shipping’s unexpected bounces. On the other

hand, if all recovery hopes were to recede, say, during a non-peak season, the option value would go to zero.

Given this backdrop, we would argue that a price-to-book of 1.0x doesn’t look excessive. It prices in Δ at

a level which captures slightly higher-than-average probability of another rate upturn triggering recovery

hopes (Δ=0.2x; slightly higher than average of 0 and 0.3x) over next 12 months. Given that the sector is

past its worst supply growth between 2007 and 2013, we believe the assumption of higher-than-average

probability of another rate upturn is reasonable.

Investors may be tempted to read a price-to-book of 1.0x as a ‘mid-cycle” valuation but it is anything but

that. In our view, bulk shipping is still stuck in a down-cycle with only a slow recovery out of it.

Handymax & Handysize fleet growth YoY (%) Vessel value depreciation curve - USD/DWT

Source: Clarksons Source: Clarksons

7.5 8.411.0

19.717.8

12.2

7.65.2

2.6 2.0

-0.1

8.1

4.4

1.5-0.6

2.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

2007a 2008a 2009a 2010a 2011a 2012a 2013e 2014e

H'Max H'size

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

0 5 10 15 20

USD

/DW

T

Age (years)

H'size H'Max

12

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Fleet value-based approach is more of an art than science

Another way to look at valuations is through the value of company’s fleet, as indicated by current sale

and purchase market. Based on Clarksons data on asset values, we estimate the company’s dry bulk fleet

has a value of close to USD1.8bn. The towage fleet is valued at a book value of HKD0.55/share or

USD137m, taking the total enterprise value to USD1.9bn including the yet-to-be-delivered newbuildings. Pacific Basin fleet value (Sep 2014) at current asset prices excluding any contribution from chartered fleet

Dry Bulk Fleet Value (Aug-2014) USDm USD/Vsl

Handymax (Owned) 350 23.3 Handymax New Buildings (Owned) 163 27.2 Handysize (Owned) 900 14.1 Handysize Newbuildings (Owned) 367 28.2 Total 1,779 Less: Current Net Debt (all allocated to dry bulk) -655 Less: Current Capex Commitments -410 Current Market Value (USD m) – Dry Bulk Fleet 714 Current MV/share (HKD) - Dry bulk 2.87 Current MV/share (HKD) – Towage – at book value 0.55 Fleet Value/Share (HKD) 3.41

Source: Clarksons, HSBC estimates

We reduce the company’s net debt of USD655m and its capex commitments of USD410m to arrive at a

market value for its fleet of HKD3.41/share. Although these estimates suggest that the company’s equity

is trading at a substantial premium to its fleet value, we must caution that two factors are debatable: 1) Is

the secondary market value a reliable assessment? 2) Should there be a value of the chartered fleet?

Our fleet value estimate implies a price of USD14m for each of the 64 Handysize vessels owned by

the company (average age at eight years). This may look too low considering that a five-year old

Handysize is valued at USD19m and a new one is priced north of USD25m, however, the data from

Clarksons suggests a steep depreciation curve for the Handysize vessels in particular (say, relative to

Handymax). The presence of modern substitutes could be one of the reasons for the depressed value

of older Handysizes since Handymax vessels have grown rapidly in the last few years. However, we

have always pointed out that asset values are not the most reliable indicator particularly because they

are assessed by a far more illiquid and inefficient market compared to the equity market. A valuation

of merely USD1m/Handysize vessel more could add another HKD0.25/share and, if a slow recovery

takes hold as we think, history suggests that there would be upside to current asset values.

Charter rate less charter costs (USD/day) Second-hand Handysize asset values (USDm)

Source: Company, HSBC estimates Source: Clarksons

-5,000

0

5,000

10,000

15,000

20,000

2H06

1H07

2H07

1H08

2H08

1H09

2H09

1H10

2H10

1H11

2H11

1H12

2H12

1H13

2H13

1H14

2H14

1H15

2H15

1H16

2H16

1H17

2H17

Handymax Handysize

0.0

10.0

20.0

30.0

40.0

50.0

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

10 Yr Handysize 5 Yr Handysize

13

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Yet another value contribution can possibly be argued for the contributions of chartered fleet. The

chartered fleet would account for more than 60% of revenue days in 2014e and while it has found it

difficult to earn a profit in volatile markets of the last three years, it’s worth remembering that the

situation can normalize if markets start trending up in a slow but sustained manner. On our forecasts

of charter spread (charter rate – charter cost) of USD500-600/day, the business would generate

USD25-30m of net profit annually over the next two years. At a conservative PE of 5x, such

chartered fleet earnings would add HKD0.50-0.60/share to the company’s valuation.

Pacific Basin fair value/share (HKD) based on its fleet valuation in slow recovery (including contribution from chartered fleet)

Source: Company, Clarksons, HSBC estimates

The chart above highlights our fleet-based valuation and its challenges. It offers a fairly wide value range

from HKD3.41/share to HKD4.53/share, implying a price-to-book of 0.73x-0.94x. The equity market’s

view is likely to vary depending on the trajectory of asset prices as well as its view on the stage of the

cycle and company’s ability to make money on its chartered fleet.

3.61

1.40

1.47

0.650.55

0.510.60

2.63

1.64

4.53

0

1

2

3

4

5

6

7

8

9

10

H'Size H'Max H'Size-NB H'Max-NB Towage Higher H'sizevaln

($16mn/ship)

Charteredfleet valn @

5x PE

Net Debt CapexCommitments

FairValue/Share

These components of valuation are debatable but justified if a recovery takes hold

14

Pacific Basin (2343 HK) Marine 6 October 2014

abc

We account for multiple expansion; raise TP and upgrade rating

Given the lack of success of EVA valuation methodology, we discard it in favour of the approach

accounting for historical trading range, market-wise multiple expansion and the optionality in shipping

equities. As discussed earlier, this implies a target 2015e price-to-book of 1.0x and a target price of

HKD4.93 (HKD3.0 earlier).

We also note that the new target price is at a 9% premium to the higher end of our fleet value-based range

of HKD3.41-4.53. This, in our view, prices in a modest recovery (higher asset prices and chartered fleet

value) in dry bulk markets which would see the company’s RoE go towards 7% in 2016e.

New vs. Old estimates

Old 2014e 2015e 2016e

Sales 1,844 1,918 2,015 EBITDA 177 194 232 Operating Profit 79 95 130 Net Profit -22 49 77 EPS (USD) -0.01 0.03 0.04

New 2014e 2015e 2016e

Sales 1,757 1,744 1,831 EBITDA 113 196 230 Operating Profit 12 91 119 Net Profit -84 53 75 EPS (USD) -0.04 0.03 0.04

New vs. old (%) 2014e 2015e 2016e

Sales -4.7 -9.1 -9.1 EBITDA -36.3 0.8 -0.8 Operating Profit -85.2 -4.3 -8.1 Net Profit 285.5 8.4 -3.0 EPS (USD) 285.5 8.4 -3.0

Source: HSBC estimates

Apart from factoring in weaker-than-expected first half results, we have made only made marginal

changes to our estimates and continue to forecast a RoE recovery over the next two years.

Under our research model, the Neutral band for non-volatile stocks equals the local hurdle rate (average

cost of equity) set by our Global Equity Strategy team (8.5% for Hong Kong), plus or minus 5ppt. This

translates into a potential return of 3.5-13.5% for stocks meriting a Neutral rating. Our target price of

HKD4.93 (including the forecast dividend yield of 2%), implies a potential return of 25.9%, which is

above the Neutral band; we therefore upgrade the stock to Overweight from Underweight. Potential return

equals the percentage difference between the current share price and the target price, including the

forecast dividend yield.

Upside catalysts include slow-steaming persisting or higher minor bulk demand materializing. Downside

risks include shrinking demand for Handysize ships.

15

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Disclosure appendix Analyst Certification The following analyst(s), economist(s), and/or strategist(s) who is(are) primarily responsible for this report, certifies(y) that the opinion(s) on the subject security(ies) or issuer(s) and/or any other views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Shishir Singh and Mark Webb

Important disclosures

Equities: Stock ratings and basis for financial analysis

HSBC believes that investors utilise various disciplines and investment horizons when making investment decisions, which depend largely on individual circumstances such as the investor's existing holdings, risk tolerance and other considerations. Given these differences, HSBC has two principal aims in its equity research: 1) to identify long-term investment opportunities based on particular themes or ideas that may affect the future earnings or cash flows of companies on a 12 month time horizon; and 2) from time to time to identify short-term investment opportunities that are derived from fundamental, quantitative, technical or event-driven techniques on a 0-3 month time horizon and which may differ from our long-term investment rating. HSBC has assigned ratings for its long-term investment opportunities as described below.

This report addresses only the long-term investment opportunities of the companies referred to in the report. As and when HSBC publishes a short-term trading idea the stocks to which these relate are identified on the website at www.hsbcnet.com/research. Details of these short-term investment opportunities can be found under the Reports section of this website.

HSBC believes an investor's decision to buy or sell a stock should depend on individual circumstances such as the investor's existing holdings and other considerations. Different securities firms use a variety of ratings terms as well as different rating systems to describe their recommendations. Investors should carefully read the definitions of the ratings used in each research report. In addition, because research reports contain more complete information concerning the analysts' views, investors should carefully read the entire research report and should not infer its contents from the rating. In any case, ratings should not be used or relied on in isolation as investment advice.

Rating definitions for long-term investment opportunities

Stock ratings HSBC assigns ratings to its stocks in this sector on the following basis:

For each stock we set a required rate of return calculated from the cost of equity for that stock’s domestic or, as appropriate, regional market established by our strategy team. The price target for a stock represents the value the analyst expects the stock to reach over our performance horizon. The performance horizon is 12 months. For a stock to be classified as Overweight, the potential return, which equals the percentage difference between the current share price and the target price, including the forecast dividend yield when indicated, must exceed the required return by at least 5 percentage points over the next 12 months (or 10 percentage points for a stock classified as Volatile*). For a stock to be classified as Underweight, the stock must be expected to underperform its required return by at least 5 percentage points over the next 12 months (or 10 percentage points for a stock classified as Volatile*). Stocks between these bands are classified as Neutral.

Our ratings are re-calibrated against these bands at the time of any 'material change' (initiation of coverage, change of volatility status or change in price target). Notwithstanding this, and although ratings are subject to ongoing management review, expected returns will be permitted to move outside the bands as a result of normal share price fluctuations without necessarily triggering a rating change.

16

Pacific Basin (2343 HK) Marine 6 October 2014

abc

*A stock will be classified as volatile if its historical volatility has exceeded 40%, if the stock has been listed for less than 12 months (unless it is in an industry or sector where volatility is low) or if the analyst expects significant volatility. However, stocks which we do not consider volatile may in fact also behave in such a way. Historical volatility is defined as the past month's average of the daily 365-day moving average volatilities. In order to avoid misleadingly frequent changes in rating, however, volatility has to move 2.5 percentage points past the 40% benchmark in either direction for a stock's status to change.

Rating distribution for long-term investment opportunities

As of 03 October 2014, the distribution of all ratings published is as follows: Overweight (Buy) 45% (30% of these provided with Investment Banking Services)

Neutral (Hold) 37% (30% of these provided with Investment Banking Services)

Underweight (Sell) 18% (20% of these provided with Investment Banking Services)

Share price and rating changes for long-term investment opportunities

Pacific Basin Shipping (2343.HK) Share Price performance HKD Vs HSBC

rating history

Recommendation & price target history

From To Date

N/A Neutral 18 October 2011 Neutral Overweight 05 December 2011 Overweight Neutral 01 March 2012 Neutral Underweight 10 April 2012 Underweight Overweight (V) 11 June 2012 Overweight (V) Neutral (V) 01 August 2012 Neutral (V) Underweight (V) 11 December 2012 Underweight (V) Underweight 28 February 2013 Target Price Value Date

Price 1 4.06 18 October 2011 Price 2 4.12 01 March 2012 Price 3 4.12 19 June 2012 Price 4 3.56 01 August 2012 Price 5 3.00 17 February 2013 Price 6 3.20 28 January 2014 Price 7 3.30 26 March 2014 Price 8 3.00 08 July 2014

Source: HSBC

Source: HSBC

2

4

6

8

10

12

14

16

18

Oct

-09

Oct

-10

Oct

-11

Oct

-12

Oct

-13

Oct

-14

17

Pacific Basin (2343 HK) Marine 6 October 2014

abc

HSBC & Analyst disclosures Disclosure checklist

Company Ticker Recent price Price Date Disclosure

PACIFIC BASIN SHIPPING 2343.HK 4.20 01-Oct-2014 4, 6, 7

Source: HSBC

1 HSBC has managed or co-managed a public offering of securities for this company within the past 12 months. 2 HSBC expects to receive or intends to seek compensation for investment banking services from this company in the next

3 months. 3 At the time of publication of this report, HSBC Securities (USA) Inc. is a Market Maker in securities issued by this

company. 4 As of 31 August 2014 HSBC beneficially owned 1% or more of a class of common equity securities of this company. 5 As of 31 August 2014, this company was a client of HSBC or had during the preceding 12 month period been a client of

and/or paid compensation to HSBC in respect of investment banking services. 6 As of 31 August 2014, this company was a client of HSBC or had during the preceding 12 month period been a client of

and/or paid compensation to HSBC in respect of non-investment banking securities-related services. 7 As of 31 August 2014, this company was a client of HSBC or had during the preceding 12 month period been a client of

and/or paid compensation to HSBC in respect of non-securities services. 8 A covering analyst/s has received compensation from this company in the past 12 months. 9 A covering analyst/s or a member of his/her household has a financial interest in the securities of this company, as

detailed below. 10 A covering analyst/s or a member of his/her household is an officer, director or supervisory board member of this

company, as detailed below. 11 At the time of publication of this report, HSBC is a non-US Market Maker in securities issued by this company and/or in

securities in respect of this company HSBC and its affiliates will from time to time sell to and buy from customers the securities/instruments (including derivatives) of companies covered in HSBC Research on a principal or agency basis.

Analysts, economists, and strategists are paid in part by reference to the profitability of HSBC which includes investment banking revenues.

Whether, or in what time frame, an update of this analysis will be published is not determined in advance.

For disclosures in respect of any company mentioned in this report, please see the most recently published report on that company available at www.hsbcnet.com/research.

Additional disclosures 1 This report is dated as at 06 October 2014. 2 All market data included in this report are dated as at close 03 October 2014, unless otherwise indicated in the report. 3 HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its

Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier procedures are in place between the Investment Banking and Research businesses to ensure that any confidential and/or price sensitive information is handled in an appropriate manner.

18

Pacific Basin (2343 HK) Marine 6 October 2014

abc

Disclaimer * Legal entities as at 30 May 2014 ‘UAE’ HSBC Bank Middle East Limited, Dubai; ‘HK’ The Hongkong and Shanghai Banking Corporation Limited, Hong Kong; ‘TW’ HSBC Securities (Taiwan) Corporation Limited; 'CA' HSBC Bank Canada, Toronto; HSBC Bank, Paris Branch; HSBC France; ‘DE’ HSBC Trinkaus & Burkhardt AG, Düsseldorf; 000 HSBC Bank (RR), Moscow; ‘IN’ HSBC Securities and Capital Markets (India) Private Limited, Mumbai; ‘JP’ HSBC Securities (Japan) Limited, Tokyo; ‘EG’ HSBC Securities Egypt SAE, Cairo; ‘CN’ HSBC Investment Bank Asia Limited, Beijing Representative Office; The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch; HSBC Securities (South Africa) (Pty) Ltd, Johannesburg; HSBC Bank plc, London, Madrid, Milan, Stockholm, Tel Aviv; ‘US’ HSBC Securities (USA) Inc, New York; HSBC Yatirim Menkul Degerler AS, Istanbul; HSBC México, SA, Institución de Banca Múltiple, Grupo Financiero HSBC; HSBC Bank Brasil SA – Banco Múltiplo; HSBC Bank Australia Limited; HSBC Bank Argentina SA; HSBC Saudi Arabia Limited; The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch incorporated in Hong Kong SAR; The Hongkong and Shanghai Banking Corporation Limited, Bangkok Branch

Issuer of report

The Hongkong and Shanghai Banking Corporation Limited Level 19, 1 Queen’s Road Central

Hong Kong SAR

Telephone: +852 2843 9111

Telex: 75100 CAPEL HX

Fax: +852 2596 0200

Website: www.research.hsbc.com

This document has been issued by The Hongkong and Shanghai Banking Corporation Limited (“HSBC”) in the conduct of its Hong Kong regulated business for the information of its institutional and professional investor (as defined by Securities and Future Ordinance (Chapter 571)) customers; it is not intended for and should not be distributed to retail customers in Hong Kong. The Hongkong and Shanghai Banking Corporation Limited is regulated by the Hong Kong Monetary Authority. All enquires by recipients in Hong Kong must be directed to your HSBC contact in Hong Kong. If it is received by a customer of an affiliate of HSBC, its provision to the recipient is subject to the terms of business in place between the recipient and such affiliate. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. HSBC has based this document on information obtained from sources it believes to be reliable but which it has not independently verified; HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of the Research Division of HSBC only and are subject to change without notice. HSBC and its affiliates and/or their officers, directors and employees may have positions in any securities mentioned in this document (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). HSBC and its affiliates may act as market maker or have assumed an underwriting commitment in the securities of companies discussed in this document (or in related investments), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or underwriting services for or relating to those companies. HSBC Securities (USA) Inc. accepts responsibility for the content of this research report prepared by its non-US foreign affiliate. All U.S. persons receiving and/or accessing this report and wishing to effect transactions in any security discussed herein should do so with HSBC Securities (USA) Inc. in the United States and not with its non-US foreign affiliate, the issuer of this report. In the UK this report may only be distributed to persons of a kind described in Article 19(5) of the Financial Services and Markets Act 2000 (FinancialPromotion) Order 2005. The protections afforded by the UK regulatory regime are available only to those dealing with a representative of HSBC Bank plc in the UK. In Singapore, this publication is distributed by The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch for the general information of institutional investors or other persons specified in Sections 274 and 304 of the Securities and Futures Act (Chapter 289) (“SFA”) and accredited investors and other persons in accordance with the conditions specified in Sections 275 and 305 of the SFA. This publication is not a prospectus as defined in the SFA. It may not be further distributed in whole or in part for any purpose. The Hongkong and Shanghai Banking Corporation Limited Singapore Branch is regulated by the Monetary Authority of Singapore. Recipients in Singapore should contact a "Hongkong and Shanghai Banking Corporation Limited, Singapore Branch" representative in respect of any matters arising from, or in connection with this report. In Australia, this publication has been distributed by The Hongkong and Shanghai Banking Corporation Limited (ABN 65 117 925 970, AFSL 301737) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). Where distributed to retail customers, this research is distributed by HSBC Bank Australia Limited (AFSL No. 232595). These respective entities make no representations that the products or services mentioned in this document are available to persons in Australia or are necessarily suitable for any particular person or appropriate in accordance with local law. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. This publication is distributed in New Zealand by The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch incorporated in Hong Kong SAR. In Japan, this publication has been distributed by HSBC Securities (Japan) Limited. It may not be further distributed in whole or in part for any purpose. In Korea, this publication is distributed by The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch ("HBAP SLS") for the general information of professional investors specified in Article 9 of the Financial Investment Services and Capital Markets Act (“FSCMA”). This publication is not a prospectus as defined in the FSCMA. It may not be further distributed in whole or in part for any purpose. HBAP SLS is regulated by the Financial Services Commission and the Financial Supervisory Service of Korea. In Canada, this document has been distributed by HSBC Bank Canada and/or its affiliates. Where this document contains market updates/overviews, or similar materials (collectively deemed “Commentary” in Canada although other affiliate jurisdictions may term “Commentary” as either “macro-research” or “research”), the Commentary is not an offer to sell, or a solicitation of an offer to sell or subscribe for, any financial product or instrument (including, without limitation, any currencies, securities, commodities or other financial instruments). © Copyright 2014, The Hongkong and Shanghai Banking Corporation Limited, ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited. MICA (P) 157/06/2014, MICA (P) 171/04/2014 and MICA (P) 077/01/2014

abc

Industrials Colin Gibson Global Sector Head, Industrials +44 20 7991 6592 [email protected]

Sean McLoughlin Analyst +44 20 7991 3464 [email protected]

Michael Hagmann Analyst +44 20 7991 2405 [email protected]

Mark Webb Analyst +852 2996 6574 [email protected]

Parash Jain Analyst +852 2996 6717 [email protected]

Shishir Singh Analyst +852 2822 4292 [email protected]

Walden Shing Analyst +852 2996 6751 [email protected]

Stephen Wan Analyst +852 2996 6566 [email protected]

Thomas Zhu, CFA Analyst +852 2822 4325 [email protected]

Carrie Liu Analyst +8862 6631 2864 [email protected]

Brian Cho Head of Research, Korea +822 3706 8750 [email protected]

Paul Choi Analyst +822 3706 8758 [email protected]

Yeon Lee Analyst +822 3706 8778 [email protected]

Sinyoung Park Analyst +822 3706 8770 [email protected]

Incheol Yu Associate +822 3706 8756 [email protected]

Thilan Wickramasinghe Analyst +65 6658 0609 [email protected]

Kristy Lee Analyst +65 6658 0616 [email protected]

Puneet Gulati Analyst +91 22 2268 1235 [email protected]

Joerg-Andre Finke Analyst +49 211 910 3722 [email protected]

Richard Schramm Analyst +49 211 910 2837 [email protected]

Juergen Siebrecht Analyst +49 211 910 3350 [email protected]

Autos Niels Fehre Analyst +49 211 910 3426 [email protected]

Horst Schneider Analyst +49 211 910 3285 [email protected]

Carson Ng Analyst +852 2822 4397 [email protected]

Yogesh Aggarwal Analyst +91 22 2268 1246 [email protected]

Transportation Andrew Lobbenberg Analyst +44 20 7991 6816 [email protected]

Joe Thomas Analyst +44 20 7992 3618 [email protected]

Wei Sim Analyst +852 2996 6602 [email protected]

Shishir Singh +852 2822 4292 [email protected]

Achal Kumar Analyst +91 80 3001 3722 [email protected]

Rajani Khetan Analyst +852 3941 0830 [email protected]

Jingyuan Zhai Associate +852 3941 7009 [email protected]

Aric Hui Associate +852 2822 3165 [email protected]

Construction & Engineering Neel Sinha Head of Equity Research, South East Asia +65 6658 0606 [email protected]

Pierre Bosset Head of French Research +33 1 56 52 43 10 [email protected]

Tarun Bhatnagar Analyst +65 6658 0614 [email protected]

John Fraser-Andrews Analyst +44 20 7991 6732 [email protected]

Jeffrey Davis Analyst +44 207 991 6837 [email protected]

Ivan Enriquez +52 55 5721 2397 [email protected]

Claudia Navarrete Analyst +52 55 5721 2422 [email protected]

Anderson Chow Analyst +852 2996 6669 [email protected]

Lesley Liu Analyst +852 2822 4524 [email protected]

Raj Sinha Analyst +971 4423 6932 [email protected]

Levent Bayar Analyst +90 212 376 46 17 [email protected]

Ashutosh Narkar Analyst +91 22 2268 1474 [email protected]

Tobias Loskamp Analyst +49 211 910 2828 [email protected]

Specialist Sales Rod Turnbull +44 20 7991 5363 [email protected]

Oliver Magis +49 21 1910 4402 [email protected]

Billal Ismail +44 20 7991 5362 [email protected]

Jean Gael Tabet 44 20 7991 5342 [email protected]

Global Industrials Research Team

![RECALIBRATING VACCINATION LAWS - Boston University2017] RECALIBRATING VACCINATION LAWS 2155 their infancy,2 and lawmakers heavily favored corporate welfare and deregulation over consumer](https://img.dokumen.tips/doc/110x75/5ee2513fad6a402d666cd801/recalibrating-vaccination-laws-boston-2017-recalibrating-vaccination-laws-2155.jpg)

![Digital [un]Marketing: Recalibrating Perspectives](https://img.dokumen.tips/doc/110x75/587bfdb41a28ab7c668b5e85/digital-unmarketing-recalibrating-perspectives.jpg)