Embed Size (px)

Citation preview

P. Todd Reed, CPPO, CPPB

CONTRACT INSURANCECertificates, Endorsements, and

Policies

No one set of answersAgency driven

Provide guidance, examples, and interaction

Best practicesSB 425 - Chapter 1811 Texas

Insurance CodeCertificate vs. endorsement vs.

policies ISO and other forms

Overview

TDI approved – ACORD Form 25 dated 2010/05 or 2014/01

Summary only and are for information purposes only.

An insurance policy may exist with certain coverages and limits.

Not a policy

Certificates of Insurance

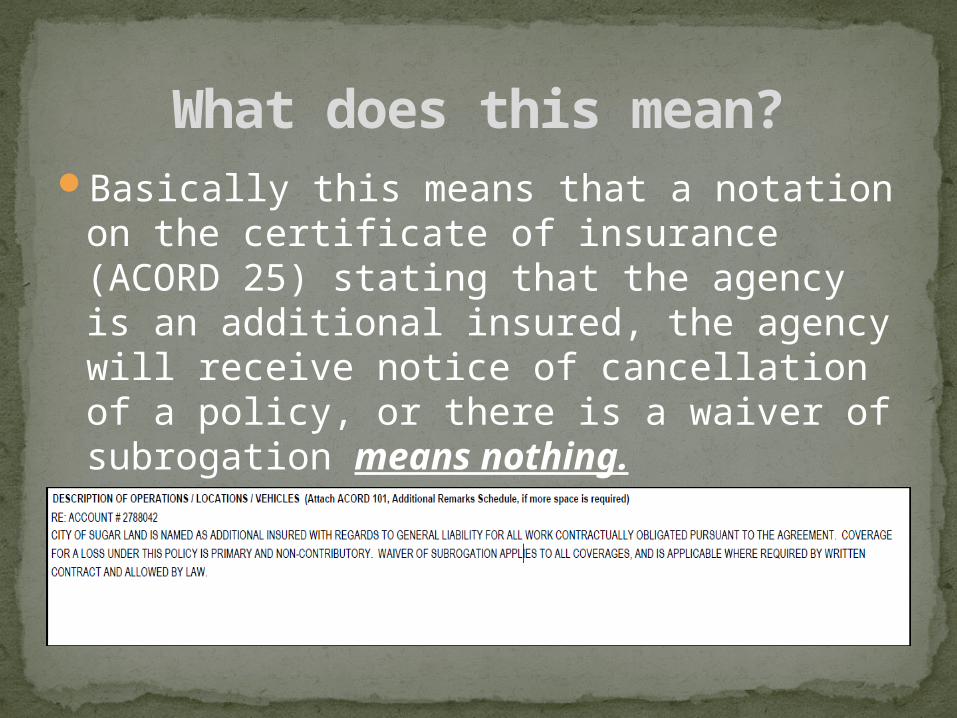

Basically this means that a notation on the certificate of insurance (ACORD 25) stating that the agency is an additional insured, the agency will receive notice of cancellation of a policy, or there is a waiver of subrogation means nothing.

Not a breach of contract and virtually no legal recourse

What does this mean?

Commercial General LiabilityAutomobile LiabilityUmbrella-ExcessWorkers CompProfessional LiabilityPollution LiabilityBuilders RiskGarage Liability for Bodily Injury & Property

DamageGarage Keepers Coverage

Watch for Exclusions

Insurance – Types and Requirements

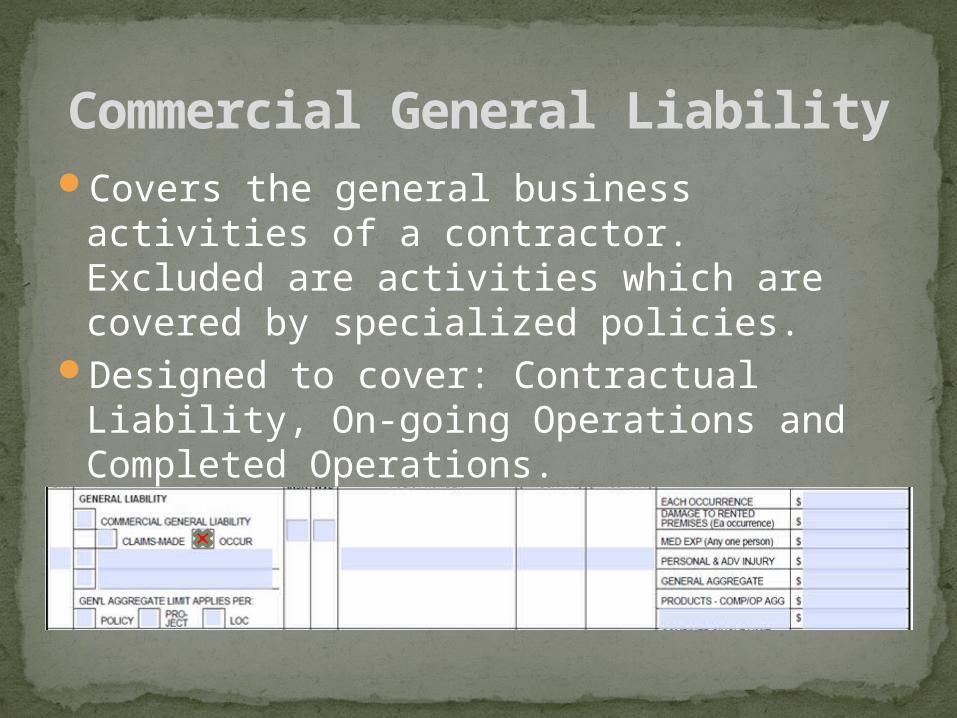

Covers the general business activities of a contractor. Excluded are activities which are covered by specialized policies.

Designed to cover: Contractual Liability, On-going Operations and Completed Operations.

Commercial General Liability

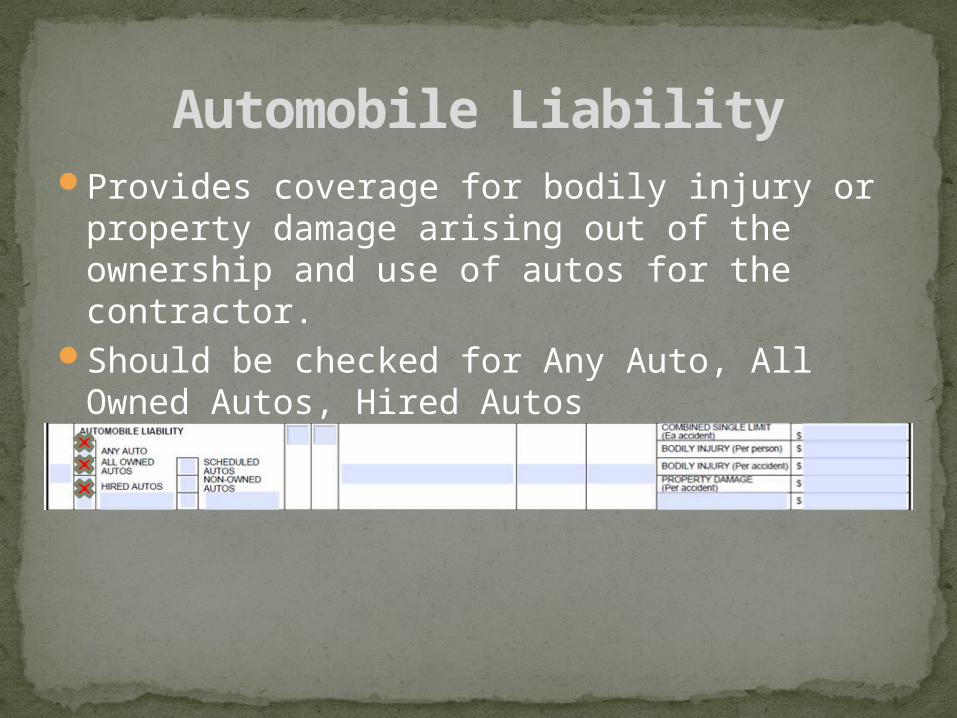

Provides coverage for bodily injury or property damage arising out of the ownership and use of autos for the contractor.

Should be checked for Any Auto, All Owned Autos, Hired Autos

Automobile Liability

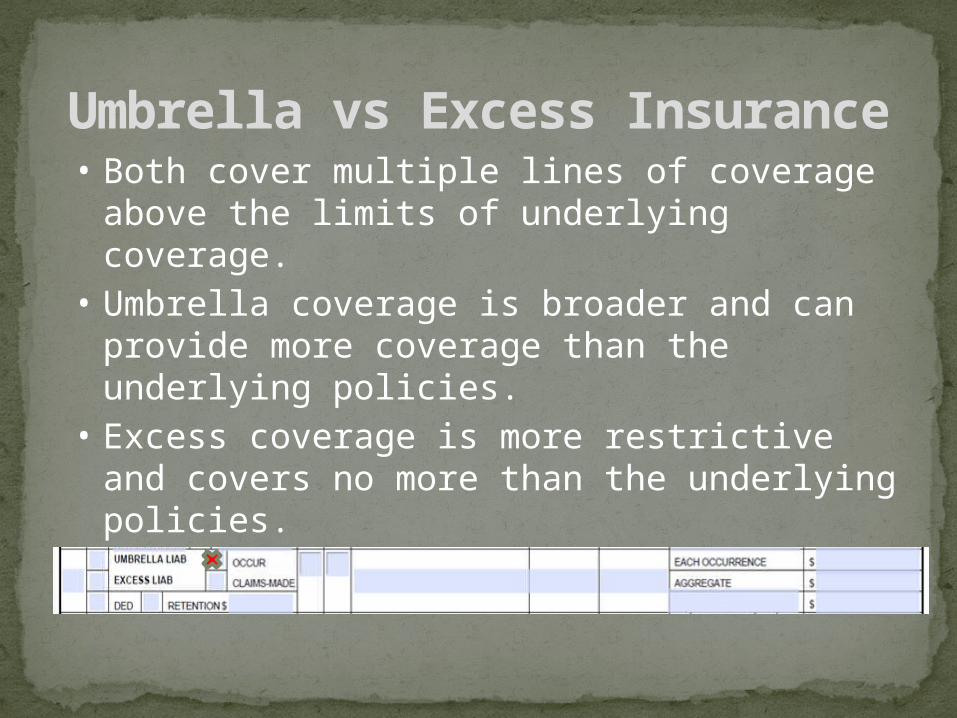

Umbrella vs Excess Insurance• Both cover multiple lines of coverage

above the limits of underlying coverage. • Umbrella coverage is broader and can

provide more coverage than the underlying policies.

• Excess coverage is more restrictive and covers no more than the underlying policies.

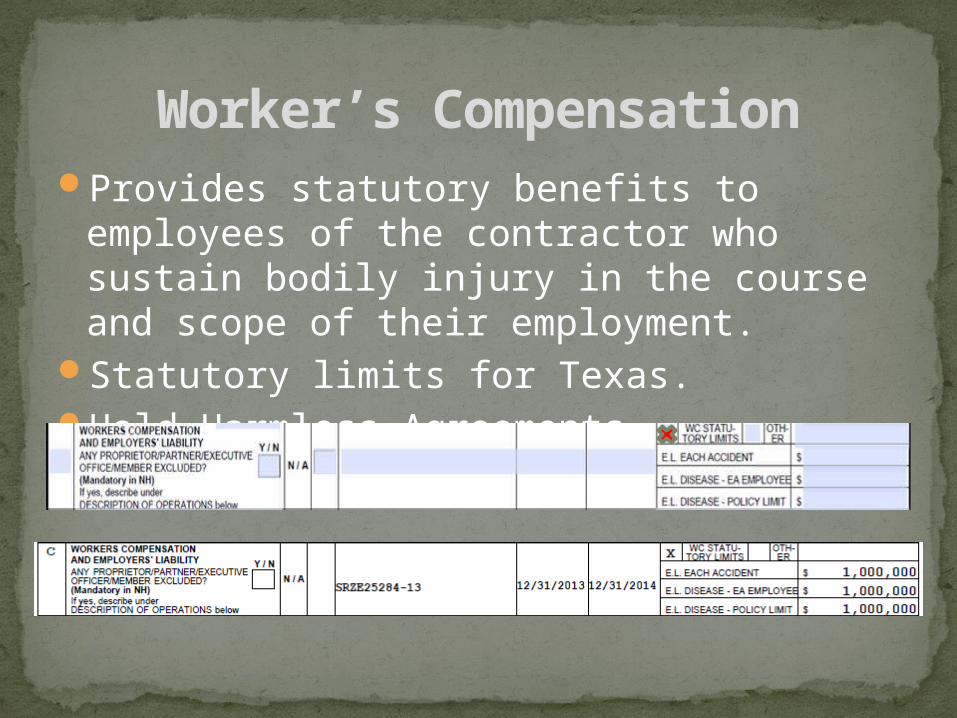

Provides statutory benefits to employees of the contractor who sustain bodily injury in the course and scope of their employment.

Statutory limits for Texas.Hold Harmless Agreements

Worker’s Compensation

Insurance to cover the negligent acts (errors & omissions) that injure their clients from the rendering of, or failure to render, professional services.

Coverage should be maintained at least two (2) years after the project is completed.

Professional Liability E&O

Environmental Impairment/Pollution Liability Coverage for liability arising from bodily injury and property damage caused by the discharge of hazardous materials or pollutants including clean up costs.(if project entails possible contamination of air, soil or ground or as determined by the agency.)

Very limited if included in CGL

Pollution Liability

• Covers property in the course of construction.• at the construction site, • off-site storage locations, • and in transit.

• If project entails vertical construction, including but not limited to bridges and tunnels or as determined by the agency.

Whatever required of GC needs to extend to subs

Builders Risk

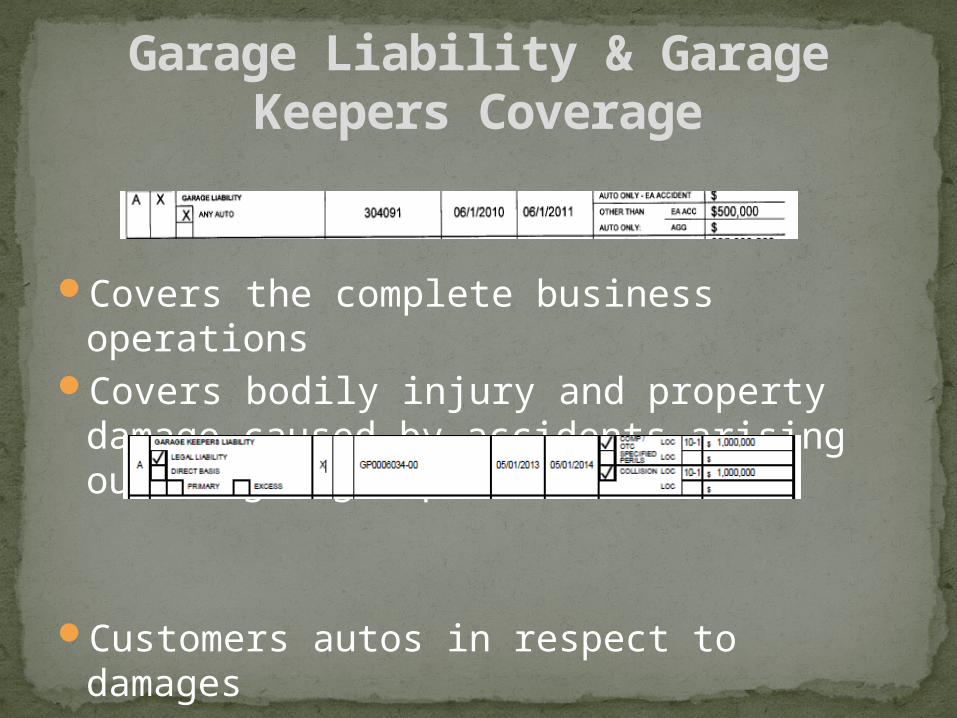

Covers the complete business operationsCovers bodily injury and property damage

caused by accidents arising out of garage operations.

Customers autos in respect to damages

Garage Liability & Garage Keepers Coverage

CG Forms should be used

Declaration Page

Right to inspect Policies

Should be required when on agency property

Leverage exists prior to the contract being signed

Verify policy numbers and dates

Miscellaneous

General Liability:Agency is Additional InsuredCoverage is Primary and non-contributoryWaiver of Subrogation in favor of the agency30 day written notice of cancellation or non-

renewal of insuranceAuto Liability:

Agency is Additional InsuredWaiver of Subrogation in favor of the agency30 day written notice of cancellation or non-

renewal of insurance

Endorsements

Workers Compensation:Waiver of Subrogation in favor of the

agency30 day written notice of cancellation or

non-renewal of insurance

Multiple carriers would require same endorsements from each

Blanket Endorsements

Endorsements

The contractor is required to extend additional insured coverage to the agency pursuant to a contract.

Claims against the agency must be first made against the contractor’s insurance.

Agency’s insurance does not have to contribute to the claim covered by the contractor’s insurance policy(ies).

Additional Insured

Without this endorsement the agency will not be covered under the contractor’s general liability or automobile liability insurance policies and claims may be made directly against the agency’s insurance carrier (Risk Pool).

Only contractor (insured) or agency (additional insured) can make a claim

Other additional insureds

Additional Insured

Stipulates the order in which multiple policies triggered by the same loss are to respond.

Contractors policies must payContractors policies can not seek

contribution from agency policies. There is no standard ISO form for

this endorsement.

Primary & Non-Contributory

Insulates the agency from the contactors insurance company coming back to the agency to get reimbursed.

The waiver of subrogation condition in current standard policies is referred to as "transfer of rights of recovery."

Greatest ability to control risk on the job site is the contractor.

Waiver of Subrogation

Renewals-material changes

Term Contract vs. Spot Contract

Notice of Cancellation

http://www.irmi.com/forms/online/insurance-glossary/terms.aspx

http://www.tdi.texas.gov/certificates/index.html

http://www.tdi.texas.gov/commercial/indexamusement.html

http://www.ambest.com/https://eapps.naic.org/cis/

Links

Questions?