Embed Size (px)

Citation preview

Overview & Outlook for the P/C Insurance Industry:

Trends, Challenges, and Trumponomics

Robert P. Hartwig, Ph.D., CPCUClinical Associate Professor of Finance, Risk Management & Insurance

Darla Moore School of Business ♦ University of South [email protected] ♦ 803.777.6782

Risk Managers Information MeetingEnergy Insurance Mutual

Orlando, FLFebruary 26, 2018

2

P/C Insurance Industry Highlights P/C Insurers: Financially Strong Despite Record CATs Pricing and capacity trends (primary and reinsurance) CAT update

Financial Market Pressures: Rising interest ratesRising volatility

Strengthening Growth Opportunities in 2018 Drivers of Commercial Lines Growth: Price, Exposure

The Economy and “Trumponomics” as a Growth Driver

Impacts of Recent Tax Reform Legislation on Insurers and Utility Sector

Electricity: Peek Into Markets (& Insurance) at Mid-Century

3

P/C Insurance Industry Financial Overview

CATS, Non-CAT Underwriting Losses Impacted Insurer Balance Sheets

Industry Remains Strong

3

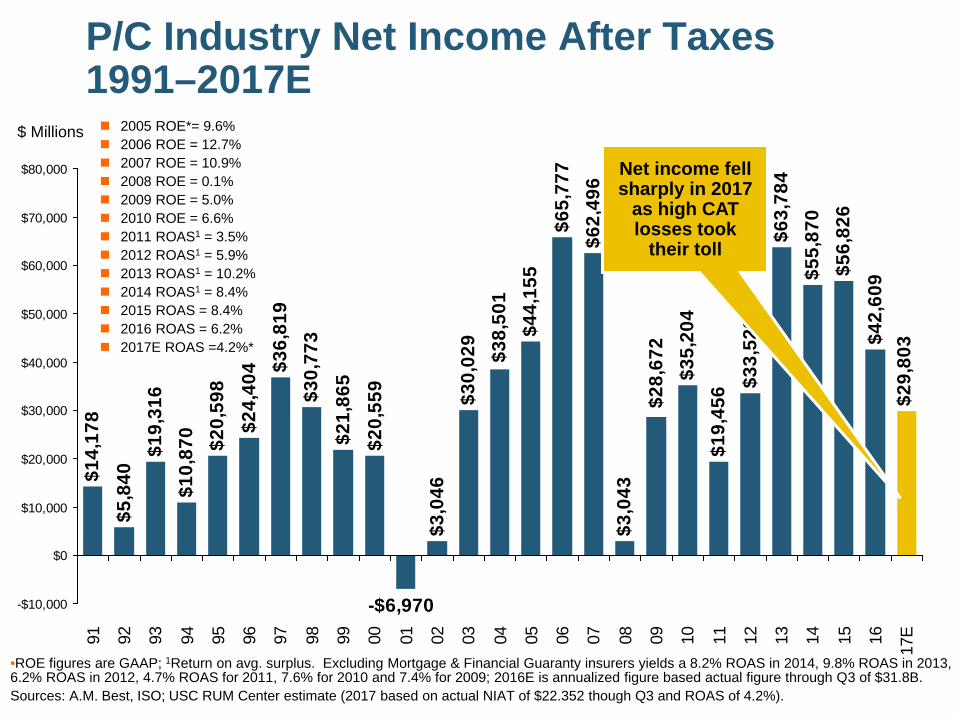

P/C Industry Net Income After Taxes1991–2017E 2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.1% 2009 ROE = 5.0% 2010 ROE = 6.6% 2011 ROAS1 = 3.5% 2012 ROAS1 = 5.9% 2013 ROAS1 = 10.2% 2014 ROAS1 = 8.4% 2015 ROAS = 8.4% 2016 ROAS = 6.2% 2017E ROAS =4.2%*

•ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 8.2% ROAS in 2014, 9.8% ROAS in 2013, 6.2% ROAS in 2012, 4.7% ROAS for 2011, 7.6% for 2010 and 7.4% for 2009; 2016E is annualized figure based actual figure through Q3 of $31.8B.Sources: A.M. Best, ISO; USC RUM Center estimate (2017 based on actual NIAT of $22.352 though Q3 and ROAS of 4.2%).

$14,

178

$5,8

40$1

9,31

6$1

0,87

0 $20,

598

$24,

404 $3

6,81

9$3

0,77

3$2

1,86

5

$3,0

46$3

0,02

9

$62,

496

$3,0

43

$35,

204

$19,

456 $3

3,52

2$6

3,78

4$5

5,87

0$5

6,82

6$4

2,60

9$2

9,80

3

$38,

501

$20,

559

$44,

155

$65,

777

-$6,970

$28,

672

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17E

Net income fell sharply in 2017

as high CAT losses took

their toll

$ Millions

-5%

0%

5%

10%

15%

20%

25%

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17*

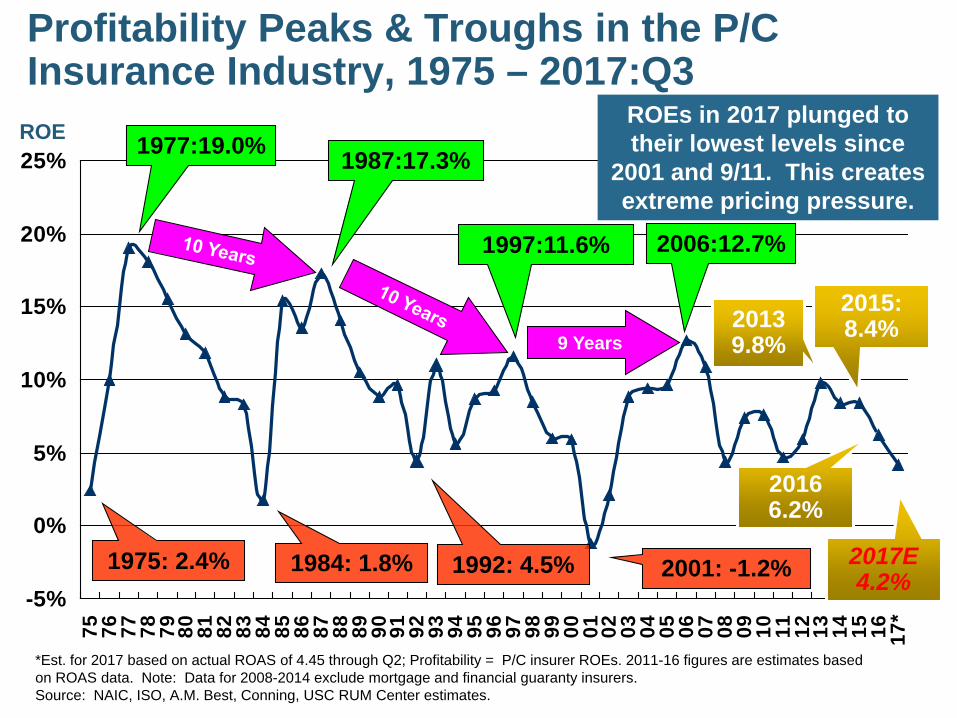

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2017:Q3

*Est. for 2017 based on actual ROAS of 4.45 through Q2; Profitability = P/C insurer ROEs. 2011-16 figures are estimates based on ROAS data. Note: Data for 2008-2014 exclude mortgage and financial guaranty insurers.Source: NAIC, ISO, A.M. Best, Conning, USC RUM Center estimates.

1977:19.0% 1987:17.3%

1997:11.6% 2006:12.7%

1984: 1.8% 1992: 4.5% 2001: -1.2%

9 Years

ROEs in 2017 plunged to their lowest levels since

2001 and 9/11. This creates extreme pricing pressure.

ROE

1975: 2.4%

2013 9.8%

2016 6.2%

2015: 8.4%

2017E 4.2%

6

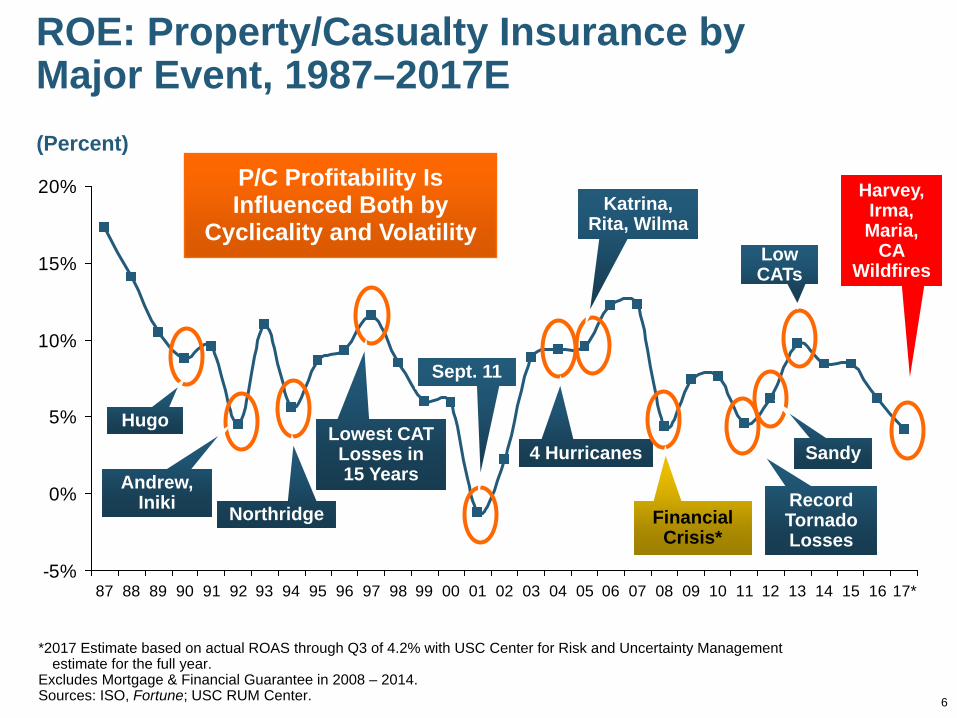

ROE: Property/Casualty Insurance by Major Event, 1987–2017E

*2017 Estimate based on actual ROAS through Q3 of 4.2% with USC Center for Risk and Uncertainty Management estimate for the full year.

Excludes Mortgage & Financial Guarantee in 2008 – 2014. Sources: ISO, Fortune; USC RUM Center.

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17*

P/C Profitability Is Influenced Both by

Cyclicality and Volatility

Hugo

Andrew, Iniki Northridge

Lowest CAT Losses in 15 Years

Sept. 11

Katrina, Rita, Wilma

4 Hurricanes

Financial Crisis*

(Percent)

Record Tornado Losses

Sandy

Low CATs

Harvey, Irma, Maria,

CA Wildfires

7

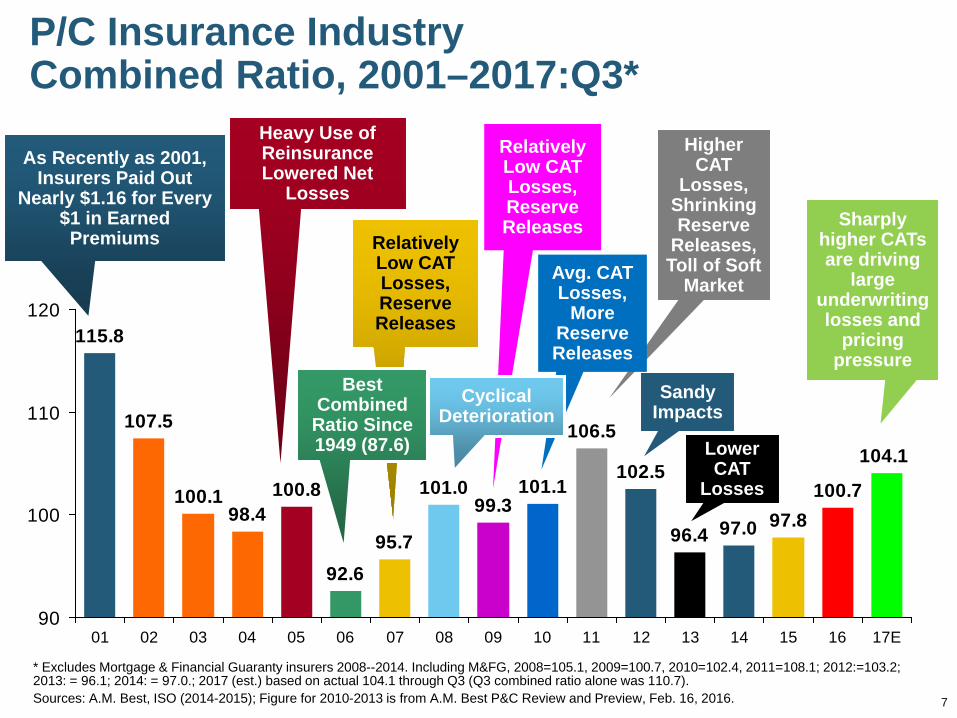

P/C Insurance Industry Combined Ratio, 2001–2017:Q3*

* Excludes Mortgage & Financial Guaranty insurers 2008--2014. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4, 2011=108.1; 2012:=103.2; 2013: = 96.1; 2014: = 97.0.; 2017 (est.) based on actual 104.1 through Q3 (Q3 combined ratio alone was 110.7). Sources: A.M. Best, ISO (2014-2015); Figure for 2010-2013 is from A.M. Best P&C Review and Preview, Feb. 16, 2016.

95.7

99.3101.1

106.5

102.5

96.4 97.0 97.8100.7

104.1101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17E

As Recently as 2001, Insurers Paid Out

Nearly $1.16 for Every $1 in Earned Premiums Relatively

Low CAT Losses, Reserve Releases

Heavy Use of Reinsurance Lowered Net

Losses

Relatively Low CAT Losses, Reserve Releases

Higher CAT

Losses, Shrinking Reserve

Releases, Toll of Soft

Market

Sandy Impacts

Lower CAT

Losses

Best Combined

Ratio Since 1949 (87.6)

Avg. CAT Losses,

More Reserve Releases

Cyclical Deterioration

Sharply higher CATs are driving

large underwriting losses and

pricing pressure

109.

411

0.2

118.

810

9.5 11

2.5

110.

210

7.6

104.

110

9.7

110.

2

102.

5 105.

491

.194

.510

4.4

100.

7 103.

8 107.

310

5.4

96.3

96.0

95.1

99.1

106.

2

102.

0

111.

1

112.

3

122.

3

90

95

100

105

110

115

120

125

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

17E

Com

mer

cial

Lin

es C

ombi

ned

Rat

io

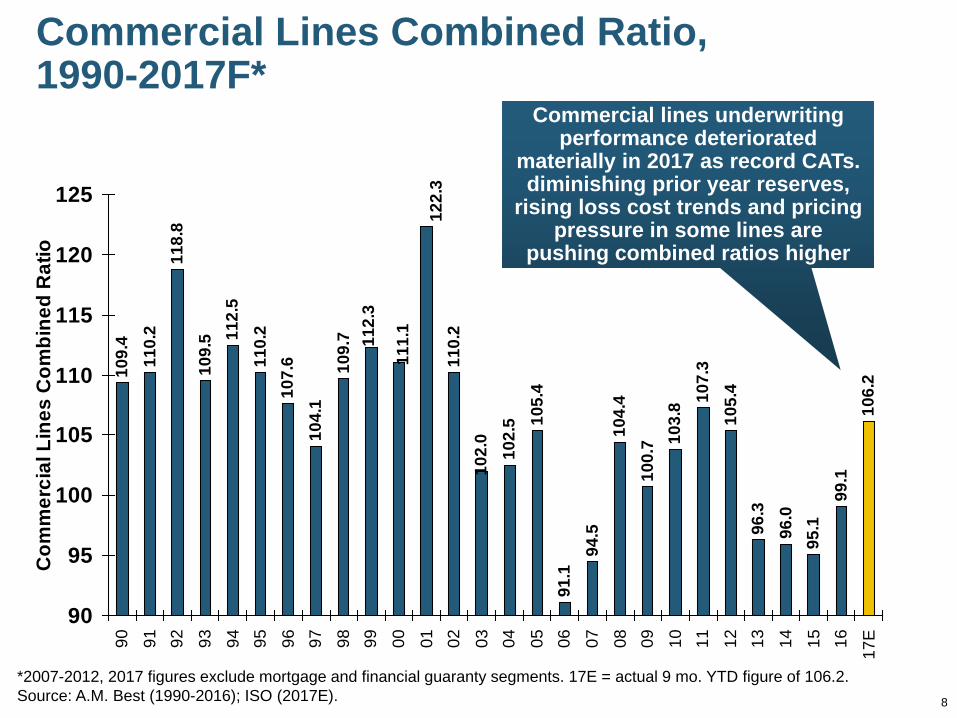

*2007-2012, 2017 figures exclude mortgage and financial guaranty segments. 17E = actual 9 mo. YTD figure of 106.2.Source: A.M. Best (1990-2016); ISO (2017E).

Commercial Lines Combined Ratio, 1990-2017F*

Commercial lines underwriting performance deteriorated

materially in 2017 as record CATs. diminishing prior year reserves,

rising loss cost trends and pricing pressure in some lines are

pushing combined ratios higher

8

9

Policyholder Surplus, 2006:Q4–2017:Q3

Sources: ISO, A.M .Best; 2018 estimate from the Center for Risk and Uncertainty Management, University of South Carolina.

($ Billions)$4

87.1

$496

.6

$512

.8

$521

.8

$478

.5

$455

.6

$437

.1 $463

.0 $490

.8 $511

.5 $540

.7

$530

.5

$544

.8

$559

.2

$559

.1

$538

.6

$550

.3

$567

.8

$583

.5

$586

.9 $607

.7

$614

.0

$624

.4 $653

.4

$671

.6

$673

.9

$675

.2

$674

.2

$673

.7

$676

.3 $700

.9

$717

.0

$719

.4

$662

.0

$570

.7

$566

.5

$505

.0

$515

.6

$517

.9

$400

$450

$500

$550

$600

$650

$700

06:Q

4

07:Q

1

07:Q

2

07:Q

3

07:Q

4

08:Q

1

08:Q

2

08:Q

3

08:Q

4

09:Q

1

09:Q

2

09:Q

3

09:Q

4

10:Q

1

10:Q

2

10:Q

3

10:Q

4

11:Q

1

11:Q

2

11:Q

3

11:Q

4

12:Q

1

12:Q

2

12:Q

3

12:Q

4

13:Q

1

13:Q

2

13:Q

3

13:Q

4

14:Q

1

14:Q

2

14:Q

3

14:Q

4

15:Q

2

15:Q

4

16:Q

1

16:Q

4

17:Q

2

17:Q

4

Financial Crisis

Surplus (Capacity) as of 9/30/17 reached a new record

of $719.4B despite record CAT losses

2010:Q1 data includes $22.5B of paid-in capital from a holding company parent for one insurer’s investment in a non-insurance business .

Drop due to near-record 2011 CAT losses

Capacity/Capital “shocks” typically do not on their own drive a sustained firming of

the pricing environment

INVESTMENTS: THE NEW REALITY

10

Investment Performance is a Key Driver of Insurer Profitability

The “Trump Bump” Has Lifted Stock Markets and Interest Rates

Will the Gains Help Insurers?10

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18*

*Through Feb. 23, 2018.Source: NYU Stern School of Business: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html Ins. Info. Inst.

Tech Bubble Implosion

Financial Crisis

Annual Return

Energy Crisis

2016: +9.5%2017: 19.4%

2018 YTD: 2.8%

S&P 500 Index Returns, 1950 – 2018*

Fed Raises Rate

Stock markets rose sharply following the 2016 election and continued to rise throughout 2017 and into 2018

Trump Bump: Sharp surge in stock post-election

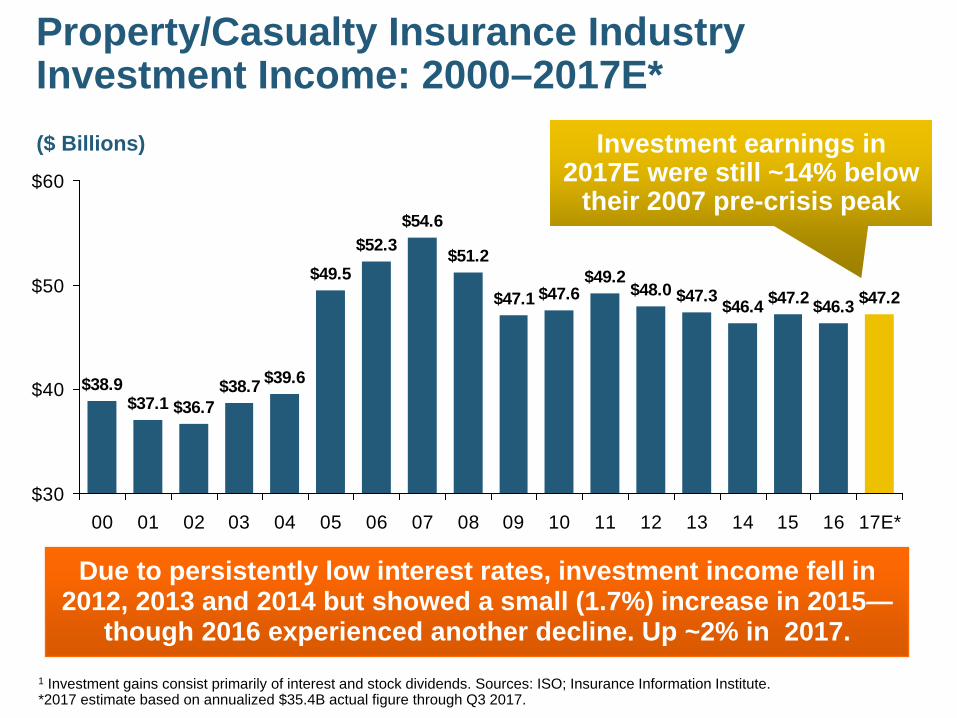

Property/Casualty Insurance Industry Investment Income: 2000–2017E*

$38.9$37.1 $36.7

$38.7

$54.6

$51.2

$47.1 $47.6$49.2

$48.0 $47.3 $46.4 $47.2 $46.3 $47.2

$39.6

$49.5$52.3

$30

$40

$50

$60

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17E*

Due to persistently low interest rates, investment income fell in 2012, 2013 and 2014 but showed a small (1.7%) increase in 2015—

though 2016 experienced another decline. Up ~2% in 2017.1 Investment gains consist primarily of interest and stock dividends. Sources: ISO; Insurance Information Institute.*2017 estimate based on annualized $35.4B actual figure through Q3 2017.

($ Billions) Investment earnings in 2017E were still ~14% below

their 2007 pre-crisis peak

13

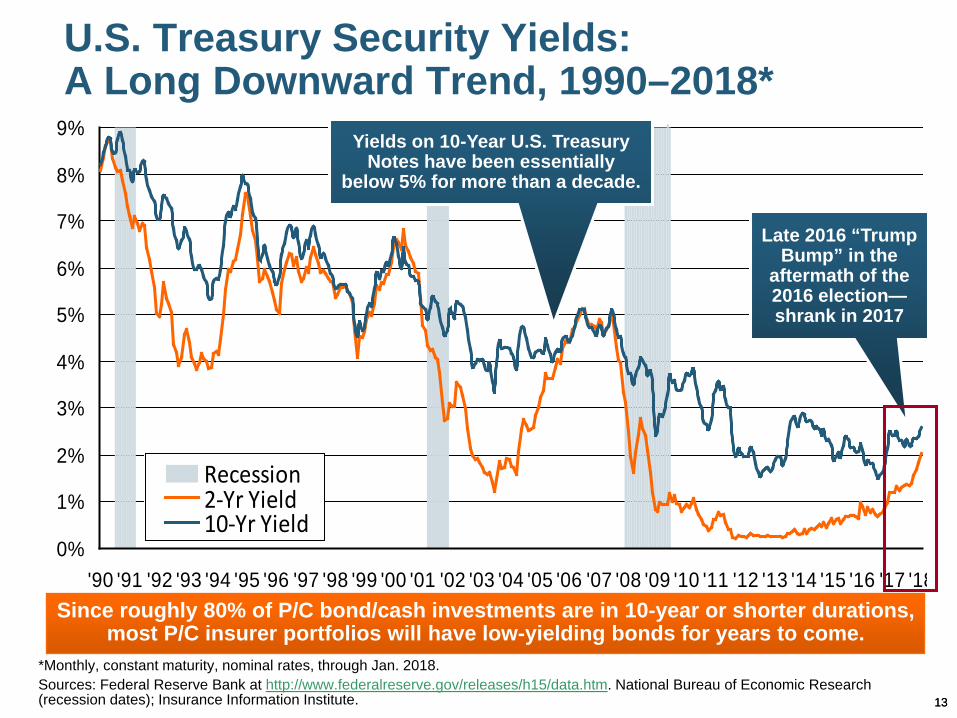

U.S. Treasury Security Yields:A Long Downward Trend, 1990–2018*

*Monthly, constant maturity, nominal rates, through Jan. 2018.Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data.htm. National Bureau of Economic Research (recession dates); Insurance Information Institute.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

Recession2-Yr Yield10-Yr Yield

Yields on 10-Year U.S. Treasury Notes have been essentially

below 5% for more than a decade.

Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come.

Late 2016 “Trump Bump” in the

aftermath of the 2016 election—shrank in 2017

13

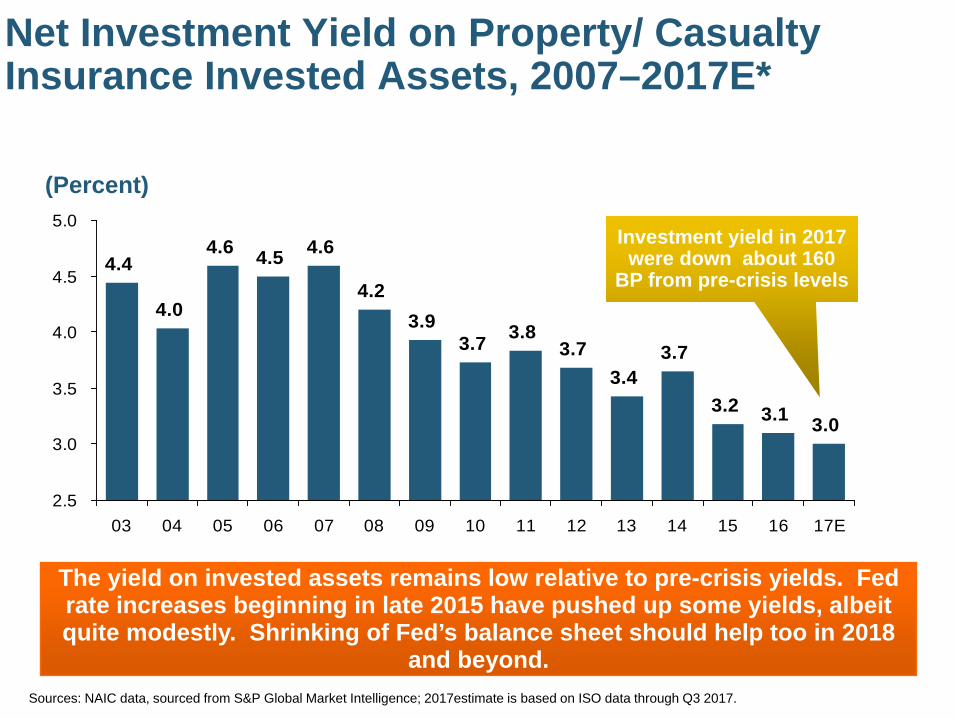

Net Investment Yield on Property/ Casualty Insurance Invested Assets, 2007–2017E*

4.4

4.0

4.6 4.5

3.7 3.83.7

3.43.7

3.2 3.1 3.0

4.6

4.23.9

2.5

3.0

3.5

4.0

4.5

5.0

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17E

The yield on invested assets remains low relative to pre-crisis yields. Fed rate increases beginning in late 2015 have pushed up some yields, albeit quite modestly. Shrinking of Fed’s balance sheet should help too in 2018

and beyond.Sources: NAIC data, sourced from S&P Global Market Intelligence; 2017estimate is based on ISO data through Q3 2017.

(Percent)

Investment yield in 2017 were down about 160

BP from pre-crisis levels

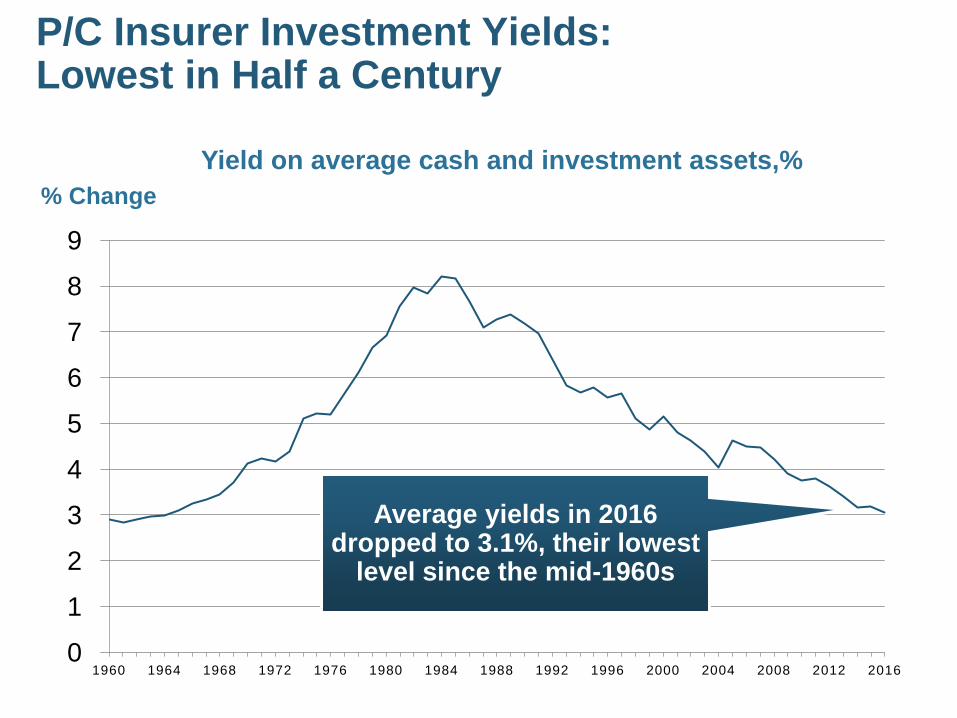

P/C Insurer Investment Yields:Lowest in Half a Century

0

1

2

3

4

5

6

7

8

9

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Yield on average cash and investment assets,%

Average yields in 2016 dropped to 3.1%, their lowest

level since the mid-1960s

% Change

16

P/C Insurance Growth Overview and Outlook

Drivers of Growth in 2018

Economic Growth Fuels Exposure & Record CAT Losses Are Pressuring Rates

Price Competition Remains Rational

16

17

-5%

0%

5%

10%

15%

20%

25%

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 1617

E18

F

Net Premium Growth (All P/C Lines): Annual Change, 1971—2018F(Percent)

1975-78 1984-87 2000-03

*Q3:2017 over Q3:2016. Shaded areas denote “hard market” periodsSources: A.M. Best (1971-2013), ISO (2014-16).

Net Written Premiums Fell 0.7% in 2007 (First Decline

Since 1943) by 2.0% in 2008, and 4.2% in 2009, the First 3-Year Decline Since 1930-33.

2018F: 4.5%2017:Q3: 4.1%

2016: 2.7%2015: 3.5%2014: 4.2

2013: 4.4%2012: +4.2%

Outlook2017E: 4.1%2018F: 4.5%

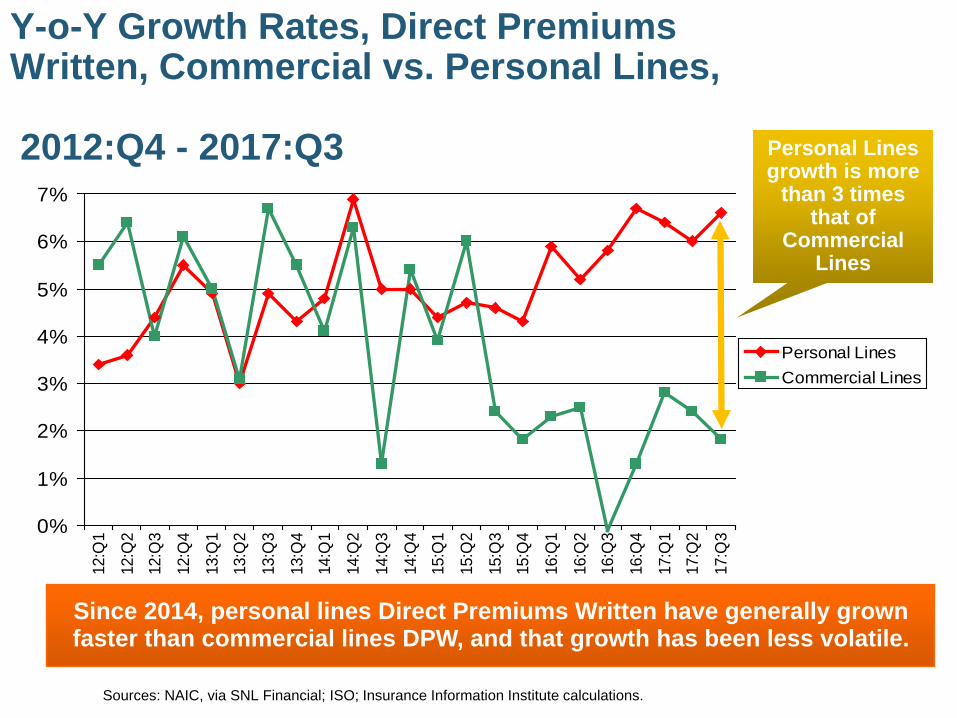

Y-o-Y Growth Rates, Direct Premiums Written, Commercial vs. Personal Lines,

2012:Q4 - 2017:Q3

0%

1%

2%

3%

4%

5%

6%

7%

12:Q

1

12:Q

2

12:Q

3

12:Q

4

13:Q

1

13:Q

2

13:Q

3

13:Q

4

14:Q

1

14:Q

2

14:Q

3

14:Q

4

15:Q

1

15:Q

2

15:Q

3

15:Q

4

16:Q

1

16:Q

2

16:Q

3

16:Q

4

17:Q

1

17:Q

2

17:Q

3

Personal LinesCommercial Lines

Sources: NAIC, via SNL Financial; ISO; Insurance Information Institute calculations.

Since 2014, personal lines Direct Premiums Written have generally grown faster than commercial lines DPW, and that growth has been less volatile.

Personal Lines growth is more

than 3 times that of

Commercial Lines

19

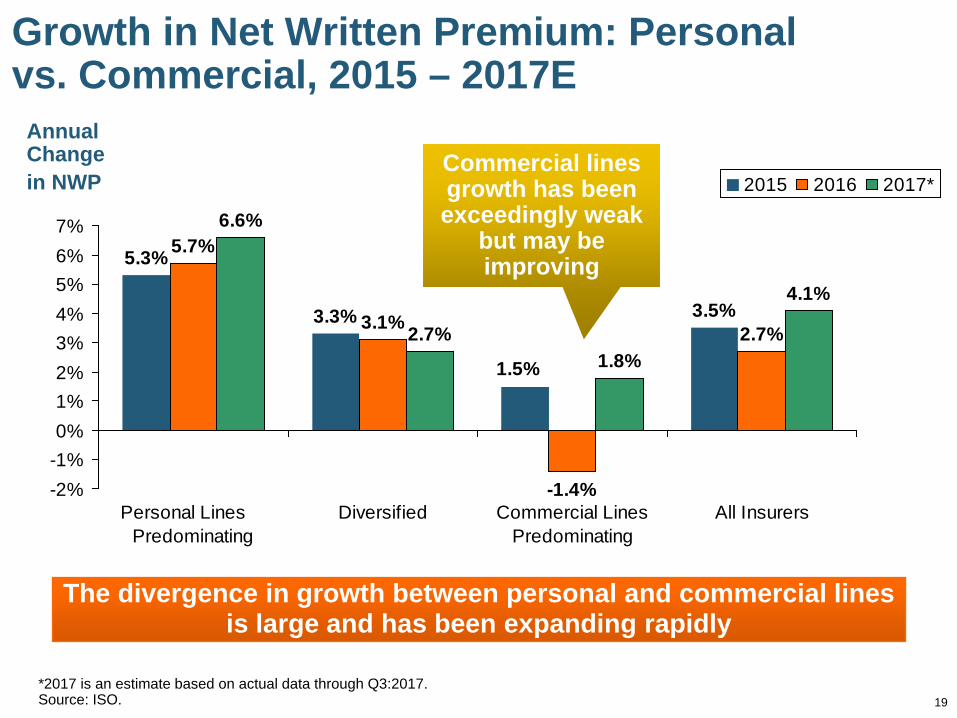

Growth in Net Written Premium: Personal vs. Commercial, 2015 – 2017E

5.7%

3.1%

-1.4%

2.7%

6.6%

2.7%1.8%

4.1%

5.3%

3.3%

1.5%

3.5%

-2%-1%0%1%2%3%4%5%6%7%

Personal Lines Predominating

Diversified Commercial LinesPredominating

All Insurers

2015 2016 2017*

Annual Change in NWP

The divergence in growth between personal and commercial lines is large and has been expanding rapidly

*2017 is an estimate based on actual data through Q3:2017.Source: ISO.

Commercial lines growth has been exceedingly weak

but may be improving

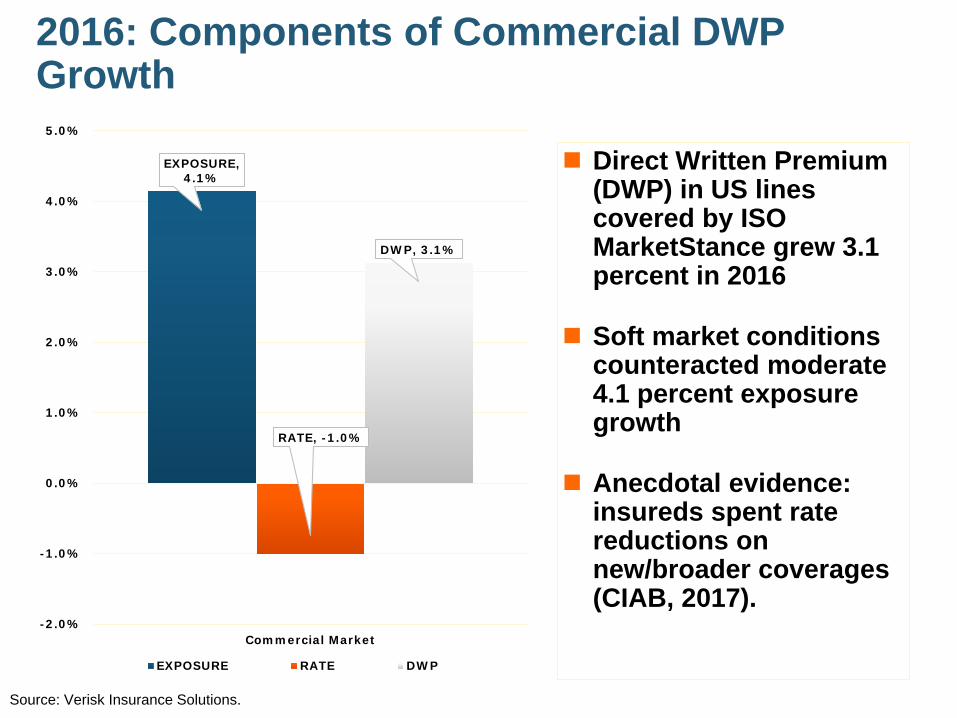

2016: Components of Commercial DWP Growth

EXPOSURE, 4.1%

RATE, -1.0%

DWP, 3.1%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Commercial Market

EXPOSURE RATE DWP

Direct Written Premium (DWP) in US lines covered by ISO MarketStance grew 3.1 percent in 2016

Soft market conditions counteracted moderate 4.1 percent exposure growth

Anecdotal evidence: insureds spent rate reductions on new/broader coverages (CIAB, 2017).

Source: Verisk Insurance Solutions.

21

M&A Trends

Consolidation Among P&C (Re)Insurers and Within

Distribution Channels Will Likely Continue at a Modest Pace

22

U.S. INSURANCE MERGERS AND ACQUISITIONS,P/C SECTOR, 1994-2016 (1)

$5,1

00

$11,

534

$8,0

59

$30,

873

$19,

118

$40,

032

$1,2

49

$486

$20,

353

$425

$9,2

64

$35,

221

$13,

615

$16,

294

$3,5

07 $6,4

19

$12,

458

$4,6

85

$4,3

93

$6,7

23

$40,

006

$8,4

98

$55,825

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Tran

sact

ion

valu

es

0

20

40

60

80

100

120

140

Num

ber of transactions

($ Millions)

(1) Includes transactions where a U.S. company was the acquirer and/or the target.

Source: Conning proprietary database.

M&A activity in the P/C sector in 2015 totaled $39.6B, its highest level since

2000, but fell sharply in 2016 in dollar terms

23

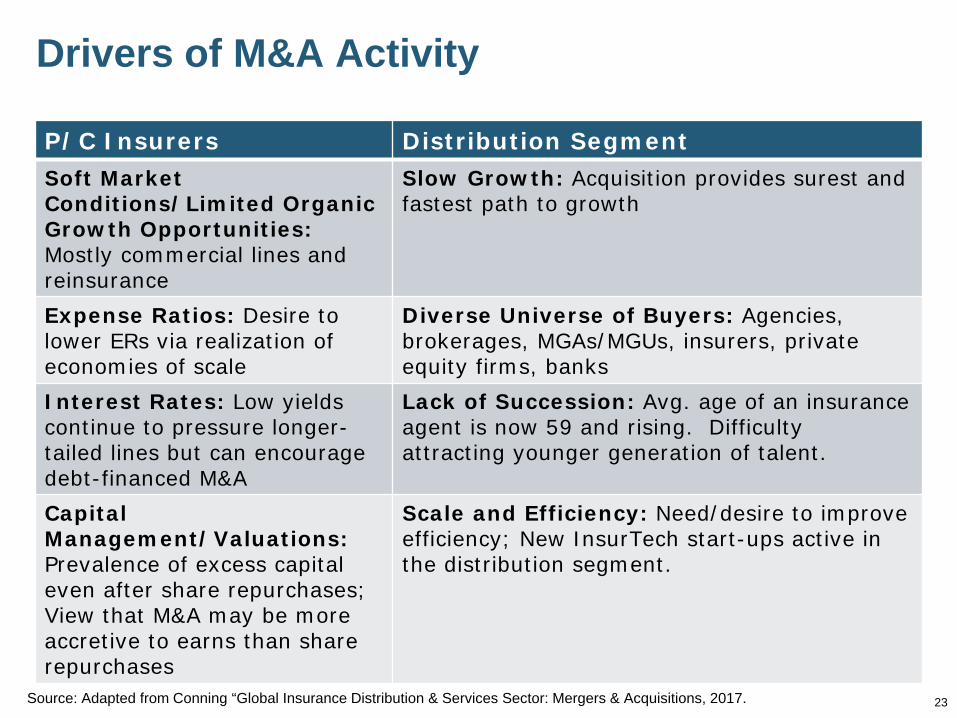

Drivers of M&A Activity

P/C Insurers Distribution SegmentSoft Market Conditions/Limited Organic Growth Opportunities:Mostly commercial lines and reinsurance

Slow Growth: Acquisition provides surest and fastest path to growth

Expense Ratios: Desire to lower ERs via realization of economies of scale

Diverse Universe of Buyers: Agencies, brokerages, MGAs/MGUs, insurers, private equity firms, banks

Interest Rates: Low yields continue to pressure longer-tailed lines but can encourage debt-financed M&A

Lack of Succession: Avg. age of an insuranceagent is now 59 and rising. Difficulty attracting younger generation of talent.

Capital Management/Valuations: Prevalence of excess capital even after share repurchases; View that M&A may be more accretive to earns than share repurchases

Scale and Efficiency: Need/desire to improve efficiency; New InsurTech start-ups active in the distribution segment.

Source: Adapted from Conning “Global Insurance Distribution & Services Sector: Mergers & Acquisitions, 2017.

24

Commercial Lines Growth, Underwriting Performance

& Pricing Cyclicality

Cyclicality in Growth, Price Are the NormRising Rates Are a Normal Part of

Adjustment Process

24

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15 17E

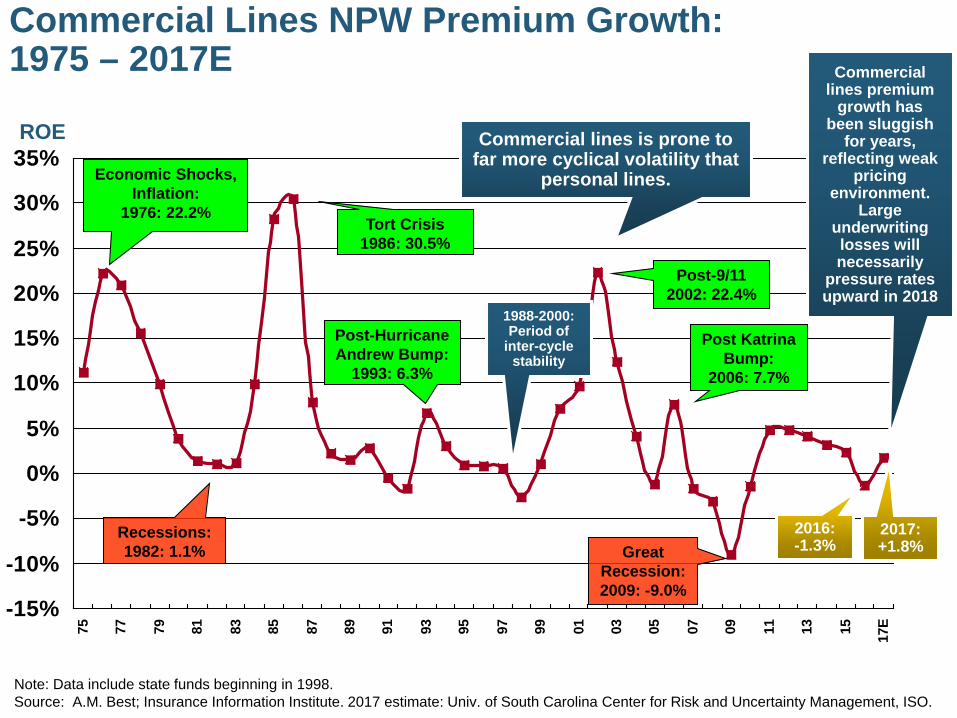

Economic Shocks, Inflation:

1976: 22.2%Tort Crisis

1986: 30.5%

Post-9/112002: 22.4%

Great Recession:2009: -9.0%

ROE

2017: +1.8%

Commercial Lines NPW Premium Growth:1975 – 2017E

Recessions:1982: 1.1%

Commercial lines is prone to far more cyclical volatility that

personal lines.

1988-2000: Period of

inter-cycle stability

Commercial lines premium

growth has been sluggish

for years, reflecting weak

pricing environment.

Large underwriting losses will necessarily

pressure rates upward in 2018

Note: Data include state funds beginning in 1998. Source: A.M. Best; Insurance Information Institute. 2017 estimate: Univ. of South Carolina Center for Risk and Uncertainty Management, ISO.

Post-Hurricane Andrew Bump:

1993: 6.3%

Post Katrina Bump:

2006: 7.7%

2016: -1.3%

26

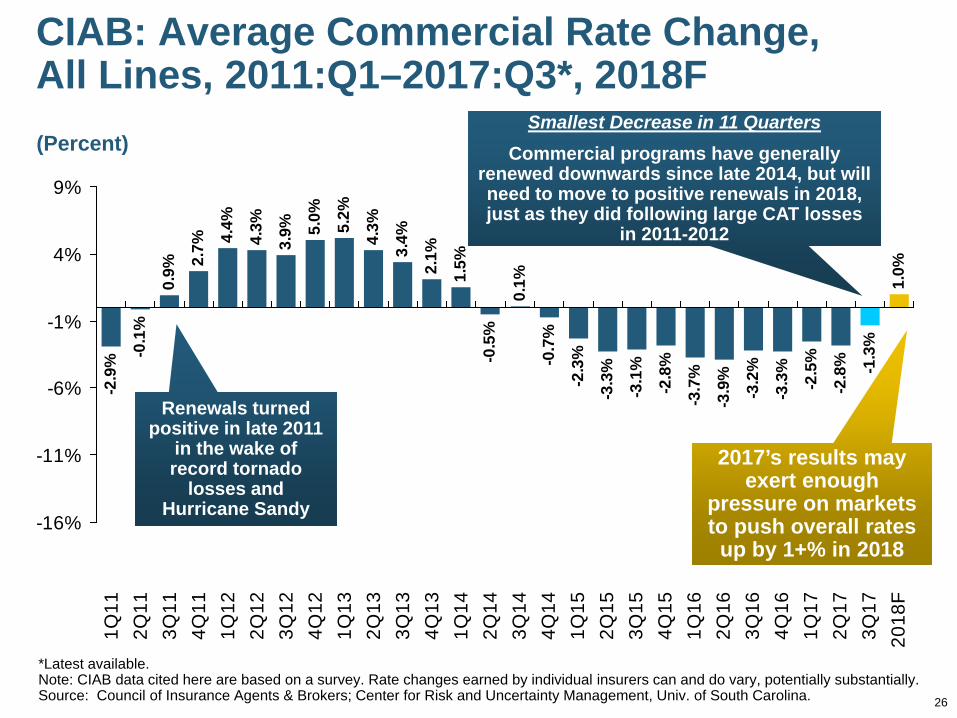

CIAB: Average Commercial Rate Change, All Lines, 2011:Q1–2017:Q3*, 2018F

-0.1

%

0.9% 2.

7% 4.4%

4.3%

3.9% 5.

0% 5.2%

4.3%

3.4%

2.1%

1.5%

-0.5

%

0.1%

-0.7

%

-2.3

%

-3.3

%

-3.1

%

-2.8

%

-3.7

%

-3.9

%

-3.2

%

-3.3

%

-2.5

%

-2.8

% -1.3

%

1.0%

-2.9

%

-16%

-11%

-6%

-1%

4%

9%

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

2018

F

*Latest available.Note: CIAB data cited here are based on a survey. Rate changes earned by individual insurers can and do vary, potentially substantially.Source: Council of Insurance Agents & Brokers; Center for Risk and Uncertainty Management, Univ. of South Carolina.

Smallest Decrease in 11 QuartersCommercial programs have generally

renewed downwards since late 2014, but will need to move to positive renewals in 2018, just as they did following large CAT losses

in 2011-2012

(Percent)

Renewals turned positive in late 2011

in the wake of record tornado

losses and Hurricane Sandy

2017’s results may exert enough

pressure on markets to push overall rates

up by 1+% in 2018

27

Change in Commercial Rate Renewals, by Line: 2017:Q3

Source: Council of Insurance Agents and Brokers; USC Center for Risk and Uncertainty Management.

Percentage Change (%)

0.4% 0.4% 0.7% 0.9%

7.3%

-2.3%-0.8% -0.7% -0.4%

0.1% 0.1%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Wor

kers

Com

p

Gen

eral

Liab

ility

Cyb

er

Um

brel

la

Sur

ety

Bus

ines

sIn

terru

ptio

n

Con

stru

ctio

n

D&

O

EP

L

Com

mer

cial

Pro

perty

Com

mer

cial

Aut

o

Commercial Property, Business Interruption

will need to reflect record CAT losses and

pressure from reinsurance markets

Note: CIAB data cited here are based on a survey. Rate changes earned by individual insurers can and do vary, potentially substantially.

Commercial Auto was only major line with materially positive renewals in 2017

28

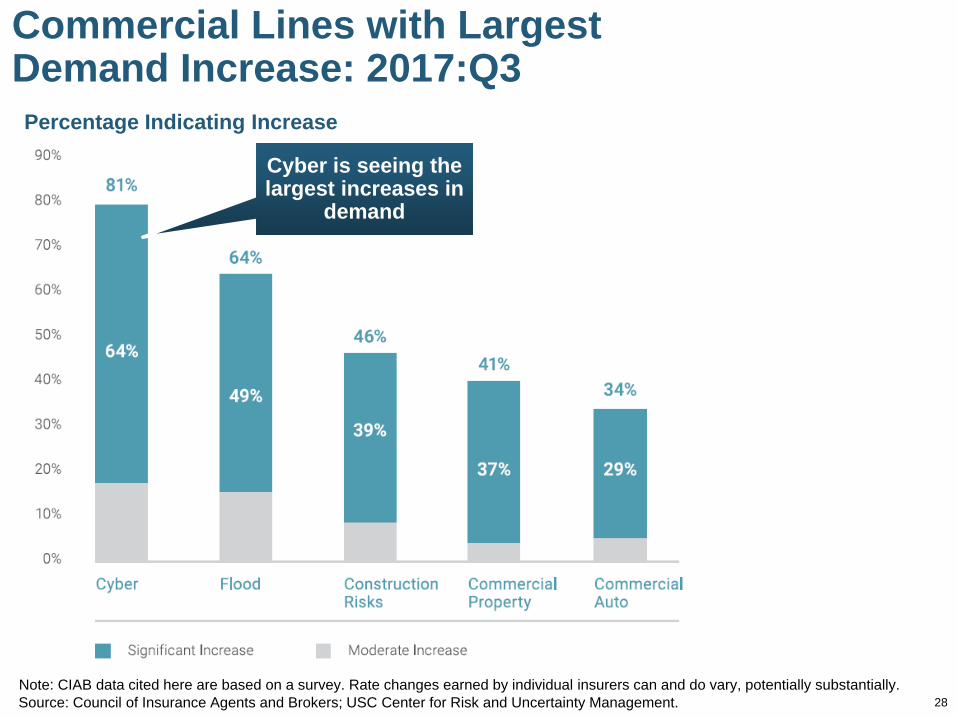

Commercial Lines with Largest Demand Increase: 2017:Q3

Source: Council of Insurance Agents and Brokers; USC Center for Risk and Uncertainty Management.Note: CIAB data cited here are based on a survey. Rate changes earned by individual insurers can and do vary, potentially substantially.

Percentage Indicating Increase

Peak = 2001:Q4 +28.5%

Cyber is seeing the largest increases in

demand

29

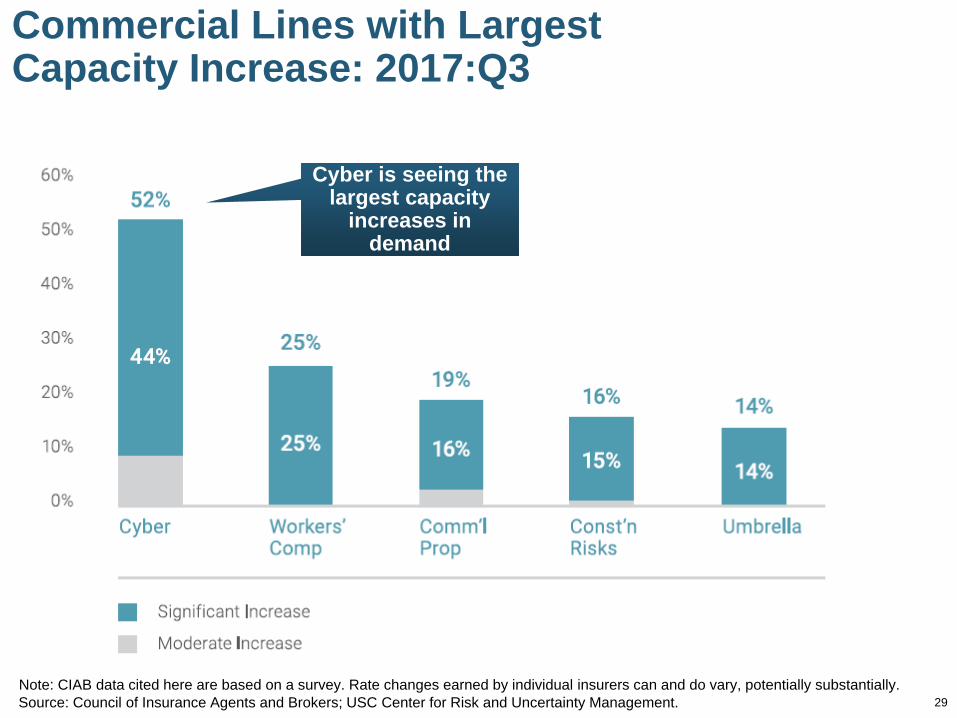

Commercial Lines with LargestCapacity Increase: 2017:Q3

Source: Council of Insurance Agents and Brokers; USC Center for Risk and Uncertainty Management.Note: CIAB data cited here are based on a survey. Rate changes earned by individual insurers can and do vary, potentially substantially.

Cyber is seeing the largest capacity

increases in demand

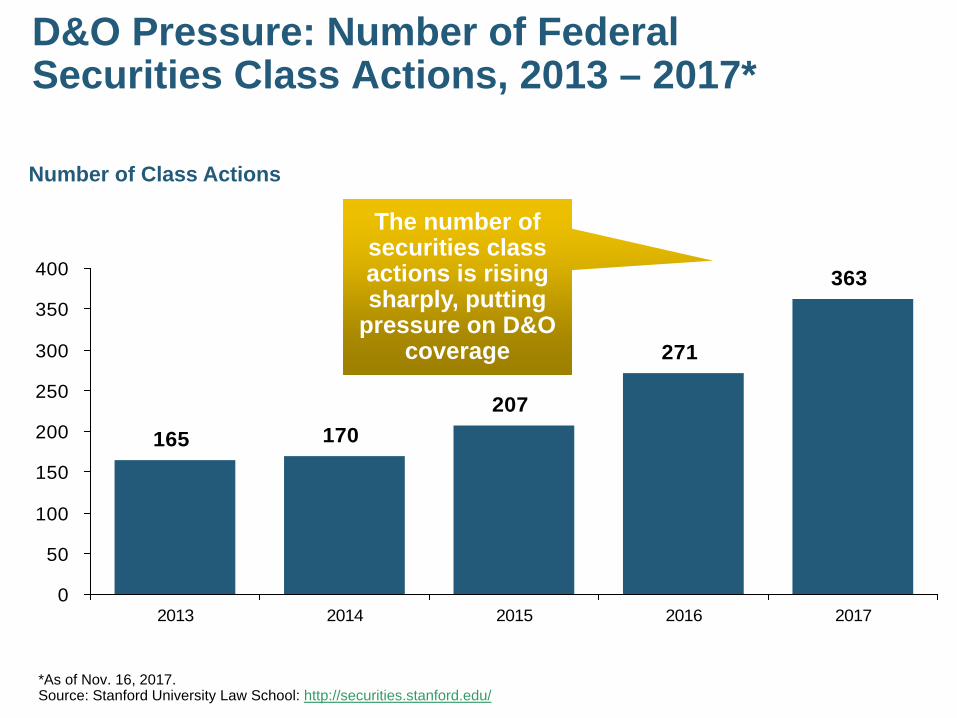

D&O Pressure: Number of Federal Securities Class Actions, 2013 – 2017*

Number of Class Actions

*As of Nov. 16, 2017.Source: Stanford University Law School: http://securities.stanford.edu/

165 170207

271

363

0

50

100

150

200

250

300

350

400

2013 2014 2015 2016 2017

The number of securities class actions is rising sharply, putting

pressure on D&O coverage

31

Workers Comp Spotlight

Underwriting Results Remain Strong

Exposure Outlook Is Outstanding as Job Growth Continues and

Wage Gains Accelerate

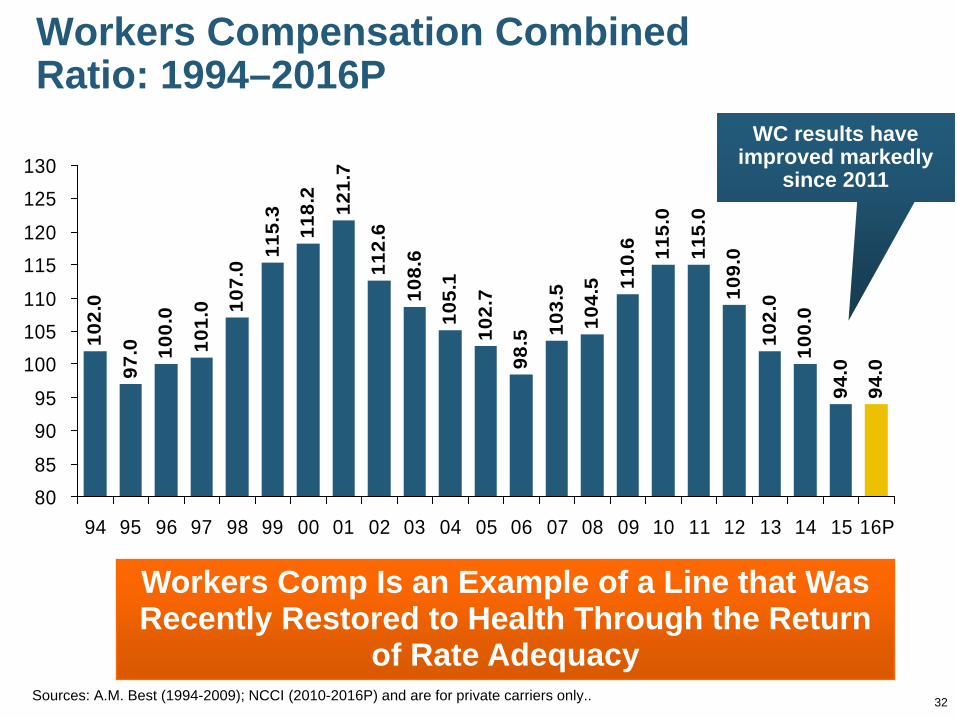

Workers Compensation Combined Ratio: 1994–2016P

102.

0

97.0 10

0.0

101.

0

112.

6

108.

6

105.

1

102.

7

98.5 10

3.5

104.

5 110.

6 115.

0

115.

0

109.

0

102.

0

100.

0

94.0

94.0

121.

7

107.

0

115.

3

118.

2

8085

9095

100105110

115120

125130

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16P

Workers Comp Is an Example of a Line that Was Recently Restored to Health Through the Return

of Rate AdequacySources: A.M. Best (1994-2009); NCCI (2010-2016P) and are for private carriers only.. 32

WC results have improved markedly

since 2011

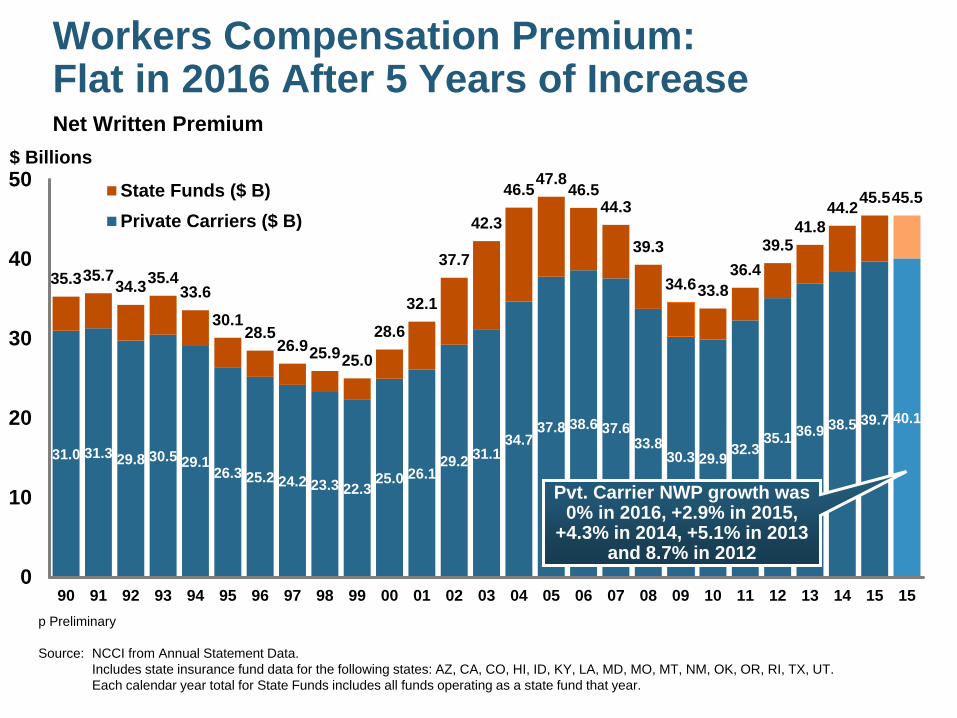

Workers Compensation Premium: Flat in 2016 After 5 Years of IncreaseNet Written Premium

31.0 31.3 29.8 30.5 29.126.3 25.2 24.2 23.3 22.3

25.0 26.129.2 31.1

34.737.8 38.6 37.6

33.830.3 29.9 32.3

35.1 36.9 38.5 39.7 40.1

35.335.734.335.4

33.6

30.128.5

26.925.925.0

28.6

32.1

37.7

42.3

46.547.846.544.3

39.3

34.633.836.4

39.541.8

44.245.545.5

0

10

20

30

40

50

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 15

State Funds ($ B)Private Carriers ($ B)

Pvt. Carrier NWP growth was 0% in 2016, +2.9% in 2015,

+4.3% in 2014, +5.1% in 2013 and 8.7% in 2012

$ Billions

Calendar Yearp Preliminary

Source: NCCI from Annual Statement Data.Includes state insurance fund data for the following states: AZ, CA, CO, HI, ID, KY, LA, MD, MO, MT, NM, OK, OR, RI, TX, UT.Each calendar year total for State Funds includes all funds operating as a state fund that year.

THE ECONOMY

34

The Strength of the Economy Will Greatly Influence Growth in Insurers’ Exposure

Base Across Most Lines

How Is “Trumponomics” Impactingthe Industry?

34

Awakening America’s“Animal Spirits”

3535

Economic Policy and the Insurance Industry

Consumer and Business Confidence Are Key

36

Animal Spirits: Unleashed from the Oval Office?

Source: https://twitter.com/realDonaldTrump

37

Animal Spirits: Unleashed from the Oval Office?

Source: https://twitter.com/realDonaldTrump

38

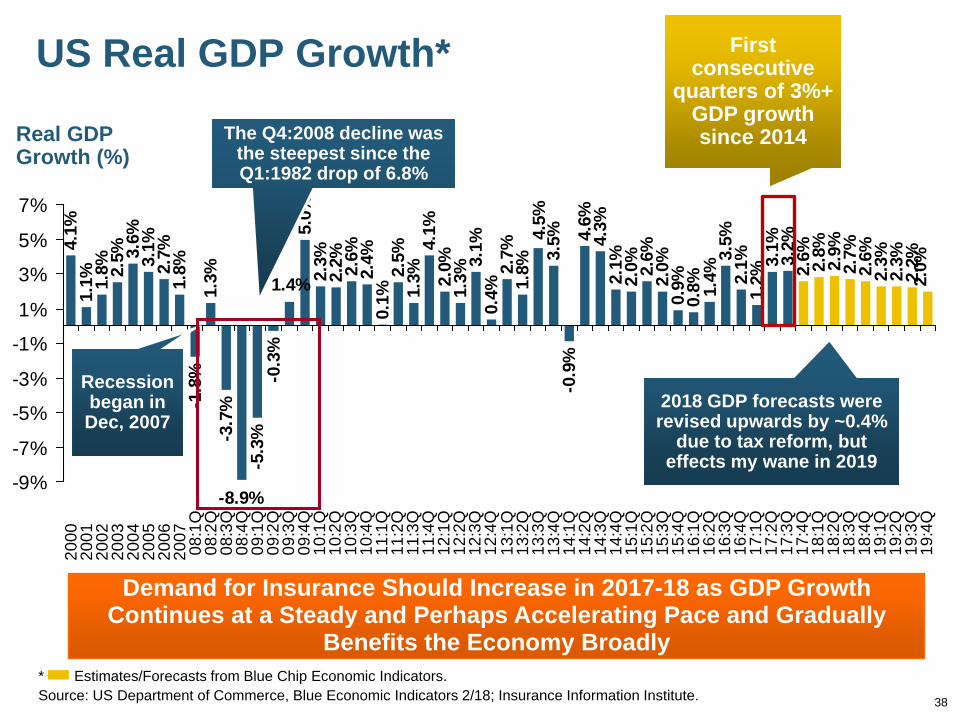

US Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 2/18; Insurance Information Institute.

2.7%

1.8%

-1.8

%1.

3%-3

.7%

-5.3

%-0

.3%

5.0%

2.3%

2.2% 2.6%

2.4%

0.1%

2.5%

1.3%

4.1%

2.0%

1.3%

3.1%

0.4%

2.7%

1.8%

3.5%

-0.9

%4.

6%4.

3%2.

1%2.

0% 2.6%

2.0%

0.9%

0.8% 1.

4%3.

5%2.

1%1.

2%3.

1%3.

2%2.

6% 2.8%

2.9%

2.7%

2.6%

2.3%

2.3%

2.2%

2.0%

-8.9%

4.5%

1.4%

4.1%

1.1% 1.

8% 2.5% 3.

6%3.

1%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

08:1

Q08

:2Q

08:3

Q08

:4Q

09:1

Q09

:2Q

09:3

Q09

:4Q

10:1

Q10

:2Q

10:3

Q10

:4Q

11:1

Q11

:2Q

11:3

Q11

:4Q

12:1

Q12

:2Q

12:3

Q12

:4Q

13:1

Q13

:2Q

13:3

Q13

:4Q

14:1

Q14

:2Q

14:3

Q14

:4Q

15:1

Q15

:2Q

15:3

Q15

:4Q

16:1

Q16

:2Q

16:3

Q16

:4Q

17:1

Q17

:2Q

17:3

Q17

:4Q

18:1

Q18

:2Q

18:3

Q18

:4Q

19:1

Q19

:2Q

19:3

Q19

:4Q

Demand for Insurance Should Increase in 2017-18 as GDP Growth Continues at a Steady and Perhaps Accelerating Pace and Gradually

Benefits the Economy Broadly

Real GDP Growth (%)

Recession began in Dec, 2007

The Q4:2008 decline was the steepest since the Q1:1982 drop of 6.8%

2018 GDP forecasts were revised upwards by ~0.4%

due to tax reform, but effects my wane in 2019

First consecutive

quarters of 3%+ GDP growth since 2014

The Economy Drives P/C InsuranceIndustry Premiums: 2006:Q1 – 2017:Q2Direct Premium Growth (All P/C Lines) vs. Nominal GDP: Quarterly Y-o-Y Pct. Change

Sources: SNL Financial; U.S. Commerce Dept., Bureau of Economic Analysis; I.I.I.

-6%

-3%

0%

3%

6%

9%

12%

2006:Q1

2006:Q3

2007:Q1

2007:Q3

2008:Q1

2008:Q3

2009:Q1

2009:Q3

2010:Q1

2010:Q3

2011:Q1

2011:Q3

2012:Q1

2012:Q3

2013:Q1

2013:Q3

2014:Q1

2014:Q3

2015:Q1

2015:Q3

2016:Q1

2016:Q3

2017:Q1

DWP y-o-y change y-o-y nominal GDP growth

Direct Written Premiums track Nominal GDP—not quarter by quarter but overall fairly well.

40

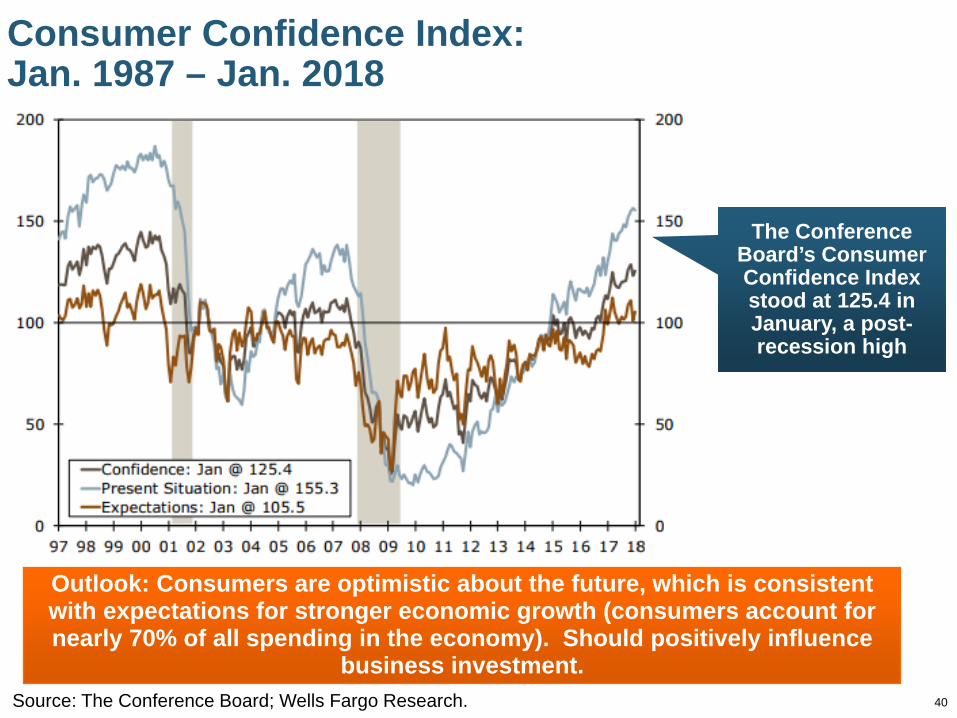

Consumer Confidence Index:Jan. 1987 – Jan. 2018

Source: The Conference Board; Wells Fargo Research.

Outlook: Consumers are optimistic about the future, which is consistent with expectations for stronger economic growth (consumers account for nearly 70% of all spending in the economy). Should positively influence

business investment.

The Conference Board’s Consumer Confidence Index stood at 125.4 in January, a post-recession high

41

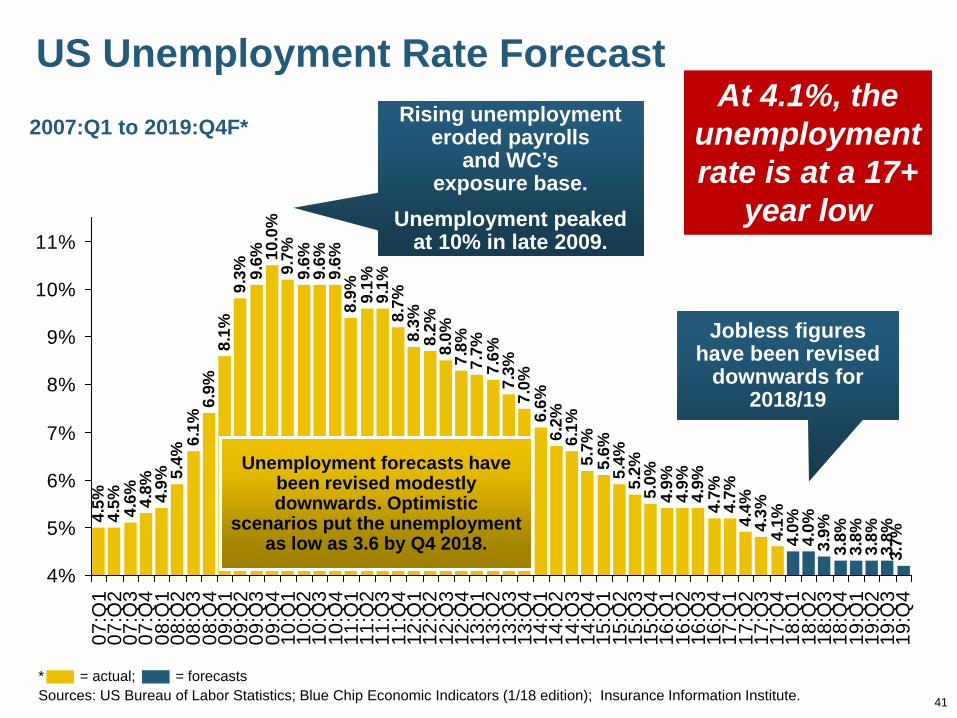

US Unemployment Rate Forecast4.

5%4.

5% 4.6% 4.

8% 4.9% 5.

4%6.

1%6.

9%8.

1%9.

3% 9.6% 10

.0%

9.7%

9.6%

9.6%

8.9% 9.

1%9.

1%8.

7%8.

3%8.

2%8.

0%7.

8%7.

7%7.

6%7.

3%7.

0%6.

6%6.

2%6.

1%5.

7%5.

6%5.

4%5.

2%5.

0%4.

9%4.

9%4.

9%4.

7%4.

7%4.

4%4.

3%4.

1%4.

0%4.

0%3.

9%3.

8%3.

8%3.

8%3.

8%3.

7%

9.6%

4%

5%

6%

7%

8%

9%

10%

11%

07:Q

107

:Q2

07:Q

307

:Q4

08:Q

108

:Q2

08:Q

308

:Q4

09:Q

109

:Q2

09:Q

309

:Q4

10:Q

110

:Q2

10:Q

310

:Q4

11:Q

111

:Q2

11:Q

311

:Q4

12:Q

112

:Q2

12:Q

312

:Q4

13:Q

113

:Q2

13:Q

313

:Q4

14:Q

114

:Q2

14:Q

314

:Q4

15:Q

115

:Q2

15:Q

315

:Q4

16:Q

116

:Q2

16:Q

316

:Q4

17:Q

117

:Q2

17:Q

317

:Q4

18:Q

118

:Q2

18:Q

318

:Q4

19:Q

119

:Q2

19:Q

319

:Q4

Rising unemployment eroded payrolls

and WC’s exposure base.

Unemployment peaked at 10% in late 2009.

* = actual; = forecastsSources: US Bureau of Labor Statistics; Blue Chip Economic Indicators (1/18 edition); Insurance Information Institute.

2007:Q1 to 2019:Q4F*

Unemployment forecasts have been revised modestly downwards. Optimistic

scenarios put the unemployment as low as 3.6 by Q4 2018.

Jobless figures have been revised

downwards for 2018/19

At 4.1%, the unemployment rate is at a 17+

year low

42

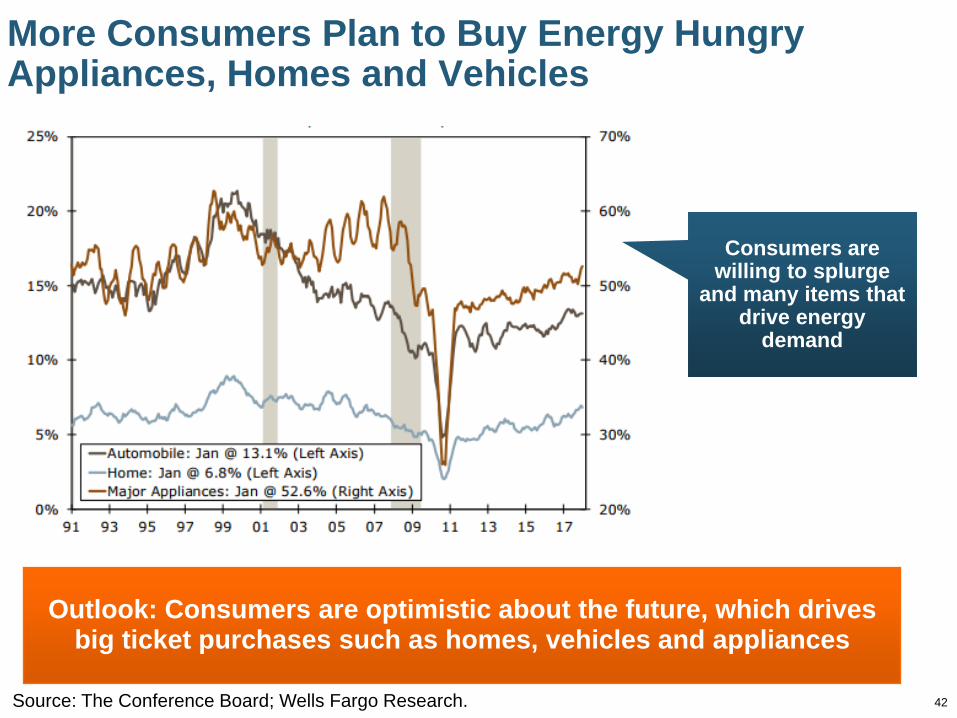

More Consumers Plan to Buy Energy Hungry Appliances, Homes and Vehicles

Source: The Conference Board; Wells Fargo Research.

Outlook: Consumers are optimistic about the future, which drives big ticket purchases such as homes, vehicles and appliances

Consumers are willing to splurge

and many items that drive energy

demand

43

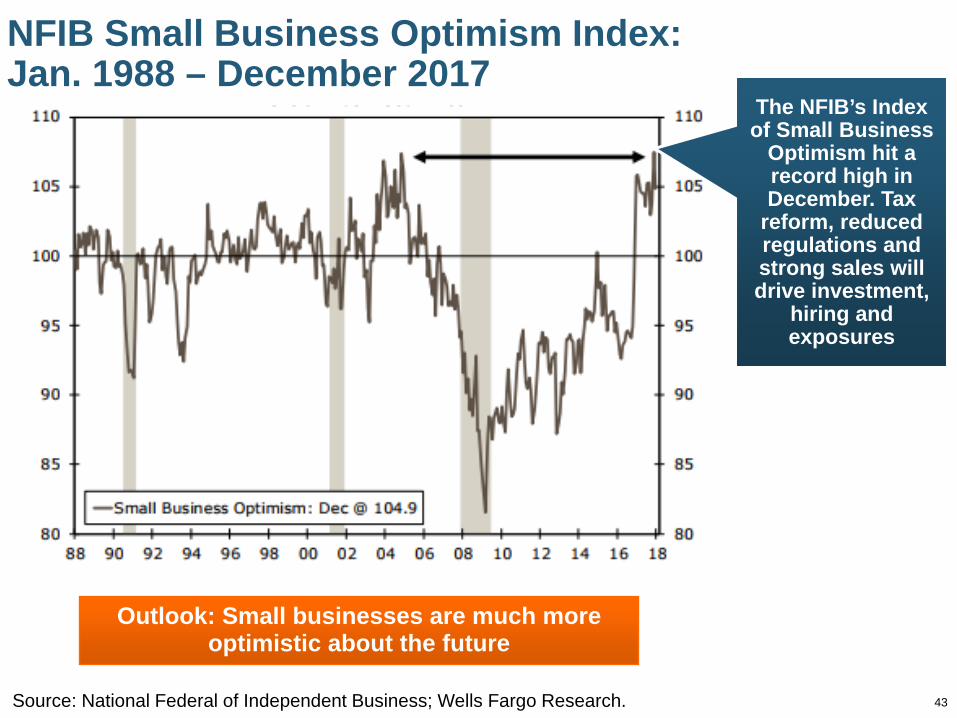

NFIB Small Business Optimism Index:Jan. 1988 – December 2017

Source: National Federal of Independent Business; Wells Fargo Research.

Outlook: Small businesses are much more optimistic about the future

The NFIB’s Index of Small Business

Optimism hit a record high in December. Tax

reform, reduced regulations and strong sales will drive investment,

hiring and exposures

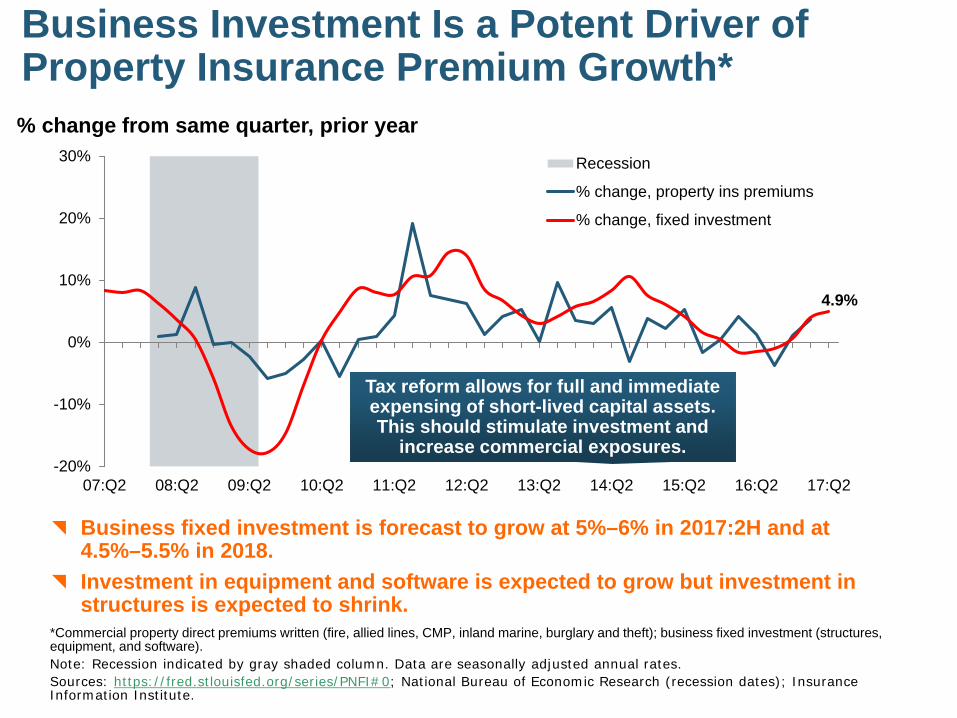

Business Investment Is a Potent Driver of Property Insurance Premium Growth*

*Commercial property direct premiums written (fire, allied lines, CMP, inland marine, burglary and theft); business fixed investment (structures, equipment, and software).Note: Recession indicated by gray shaded column. Data are seasonally adjusted annual rates.Sources: https://fred.stlouisfed.org/series/PNFI#0; National Bureau of Economic Research (recession dates); Insurance Information Institute.

-20%

-10%

0%

10%

20%

30%

07:Q2 08:Q2 09:Q2 10:Q2 11:Q2 12:Q2 13:Q2 14:Q2 15:Q2 16:Q2 17:Q2

Recession

% change, property ins premiums

% change, fixed investment

4.9%

Tax reform allows for full and immediate expensing of short-lived capital assets. This should stimulate investment and

increase commercial exposures.

% change from same quarter, prior year

Business fixed investment is forecast to grow at 5%–6% in 2017:2H and at 4.5%–5.5% in 2018.

Investment in equipment and software is expected to grow but investment in structures is expected to shrink.

46

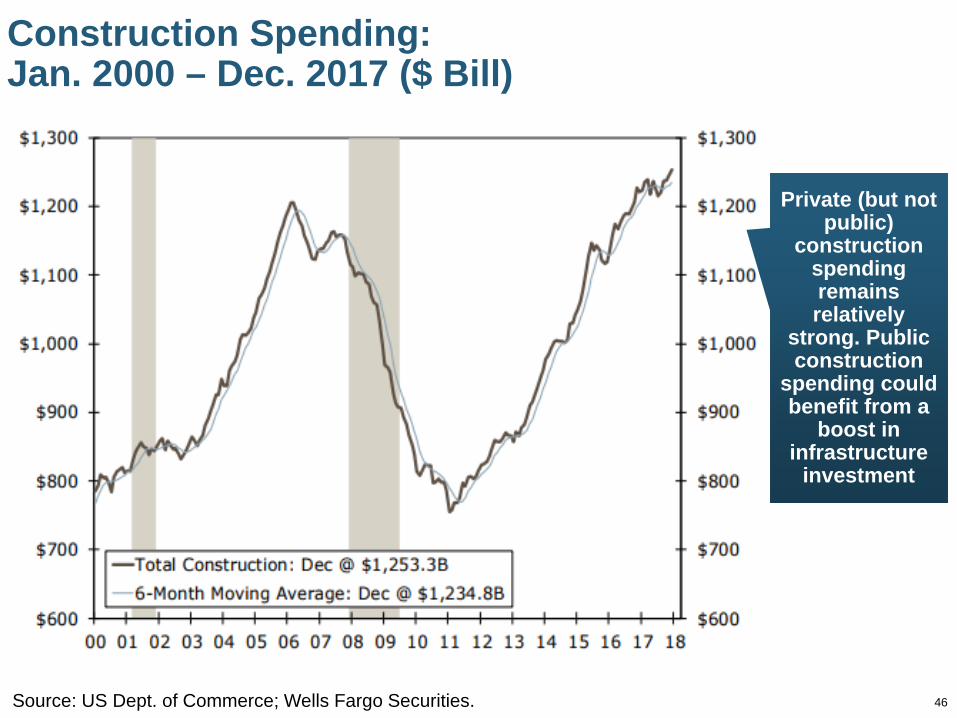

Construction Spending:Jan. 2000 – Dec. 2017 ($ Bill)

Source: US Dept. of Commerce; Wells Fargo Securities.

Private (but not public)

construction spending remains relatively

strong. Public construction

spending could benefit from a

boost in infrastructure

investment

47

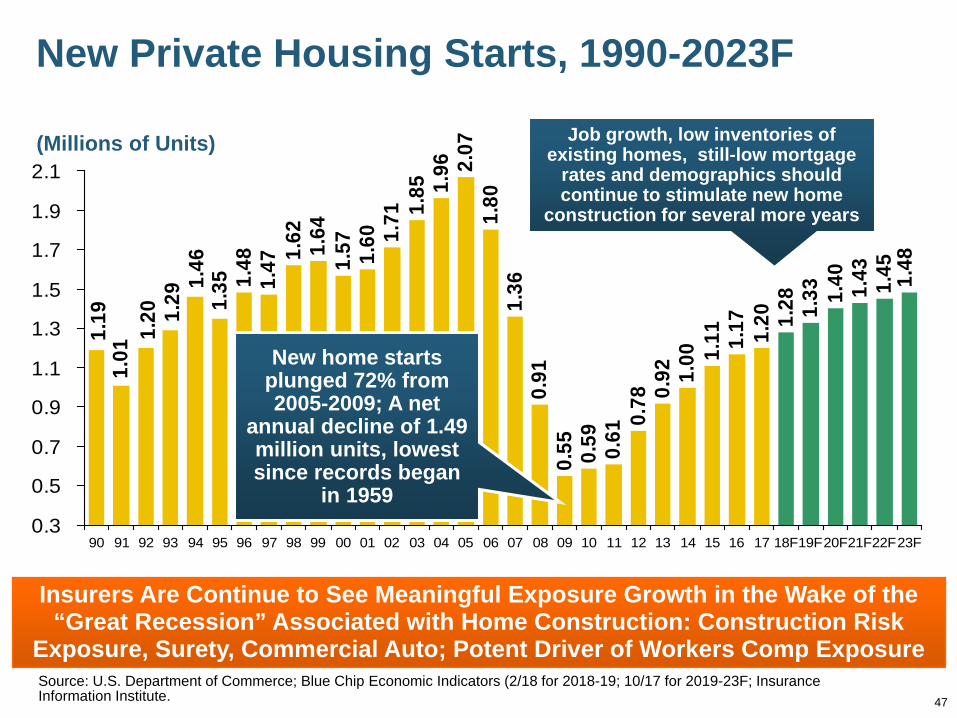

(Millions of Units)

New Private Housing Starts, 1990-2023F

1.48

1.47 1.

62 1.64

1.57 1.60 1.

71 1.85 1.

96 2.07

1.80

1.36

0.91

0.55 0.59 0.61

0.78 0.

92 1.00 1.

11 1.17 1.20 1.

28 1.33 1.

40 1.43 1.45 1.48

1.351.

461.

291.

201.

011.

19

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18F19F20F21F22F23F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (2/18 for 2018-19; 10/17 for 2019-23F; Insurance Information Institute.

Insurers Are Continue to See Meaningful Exposure Growth in the Wake of the “Great Recession” Associated with Home Construction: Construction Risk

Exposure, Surety, Commercial Auto; Potent Driver of Workers Comp Exposure

New home starts plunged 72% from 2005-2009; A net

annual decline of 1.49 million units, lowest since records began

in 1959

Job growth, low inventories of existing homes, still-low mortgage

rates and demographics should continue to stimulate new home

construction for several more years

48

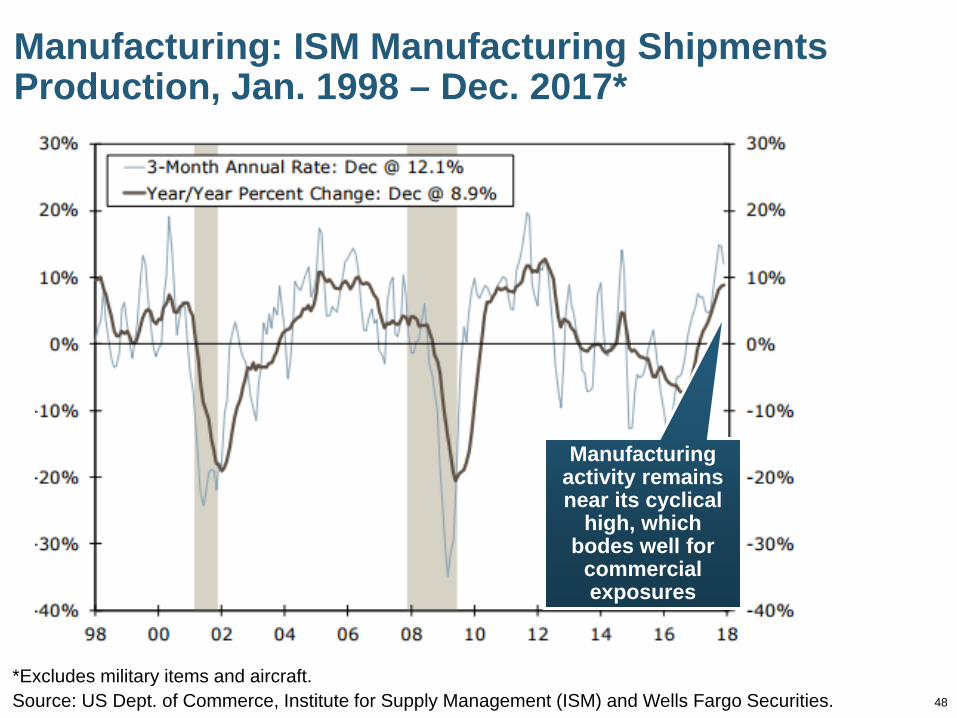

Manufacturing: ISM Manufacturing Shipments Production, Jan. 1998 – Dec. 2017*

*Excludes military items and aircraft.Source: US Dept. of Commerce, Institute for Supply Management (ISM) and Wells Fargo Securities.

Manufacturing activity remains near its cyclical

high, which bodes well for

commercial exposures

49

16.9

16.5

16.1

13.2

10.4

11.6 12

.714

.4 15.5 16

.4 17.4

17.5

17.2

17.0

16.7

16.7

16.7

16.7

16.9

16.9

16.617

.117.5

17.8

17.4

910111213141516171819

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18F 19F 20F21F 22F 22F

(Millions of Units)

Auto/Light Truck Sales, 1999-2023F

New auto/light truck sales fell to the lowest level since the

late 1960s. Forecast for 2014-15 is still below 1999-2007 average of 17 million units,

but a robust recovery is well underway.

Job growth and improved credit market conditions

boosted auto sales to near record levels in

recent years

Truck, SUV purchases remain strong but have slumped a bit

Yearly car/light truck sales are slowing slightly, as demand tapers following the recovery from the recession. PP Auto premium might

grow by 3.5% - 5%.

Sales have returned to pre-

crisis levels

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (2/18 for 2018-19; 10/17 for 2019-23F; Insurance Information Institute.

Electric Car Stock in the US: 2005–2016*

1.1

1.1

1.1

2.6

74.7

171.

4

290.

2 404.

1

563.

7

2.6

3.8 21

.5

0

100

200

300

400

500

600

05 06 07 08 09 10 11 12 13 14 15 16

Household energy demand arising from vehicles will continue to soar

*Includes plug-inn vehicles and hybrids.Source: International Energy Agency, 2017 Global Electric Vehicle Outlook accessed at:

https://www.iea.org/publications/freepublications/publication/GlobalEVOutlook2017.pdf; USC RUM. 50

(Thousands of Cars)The number of EVs in the US is increasing

exponentially

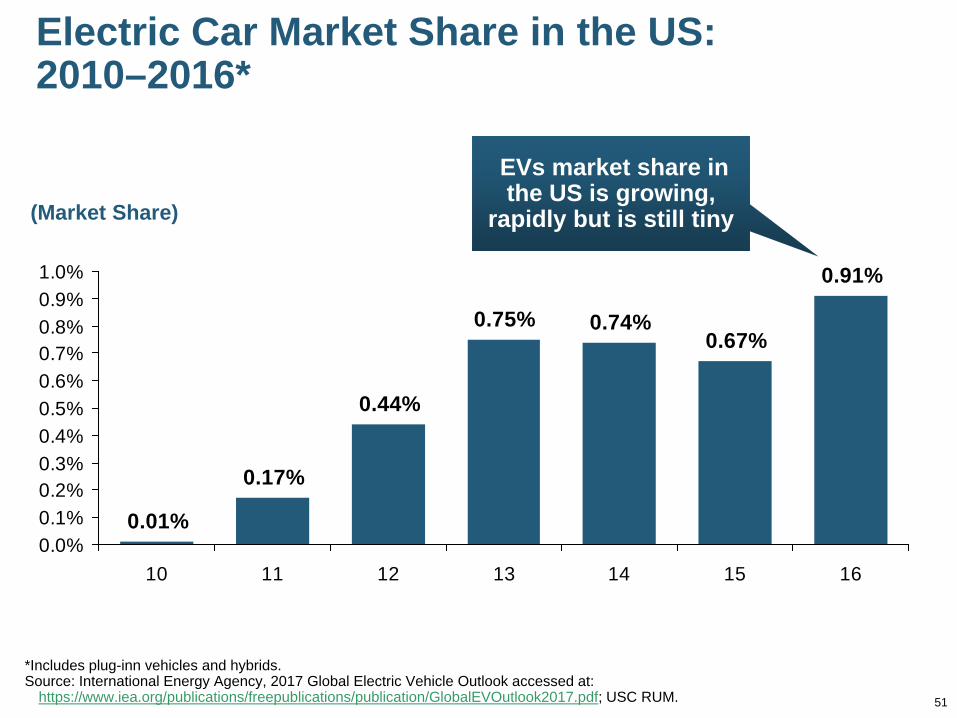

Electric Car Market Share in the US: 2010–2016*

0.01%

0.17%

0.44%

0.75% 0.74%0.67%

0.91%

0.0%0.1%0.2%0.3%0.4%0.5%0.6%0.7%0.8%0.9%1.0%

10 11 12 13 14 15 16

*Includes plug-inn vehicles and hybrids.Source: International Energy Agency, 2017 Global Electric Vehicle Outlook accessed at:

https://www.iea.org/publications/freepublications/publication/GlobalEVOutlook2017.pdf; USC RUM. 51

(Market Share)

EVs market share in the US is growing,

rapidly but is still tiny

52

Electric Vehicles and Electric Utilities

EV vehicle sales are growing exponentially in the US

Unambiguous demand driver for electricity—Or is it?

EVs still account for only a sliver of the US personal auto market share (0.91% in 2016 but up from .01% in 2010)

Market share should grow but is partially subsidy and mandate dependent, and impacted by gasoline prices

But electricity demand from EVs in the long-term will be determined largely by how consumer transportation preferences change as autonomous vehicle technologies evolve

Consumers, vehicle manufacturers and TNCs may eventually find economics of “on demand” vehicles compelling, resulting in far fewer registered vehicles

53

Catastrophe Loss Update: Major Driver of Rate Pressure

2017 Was One of the Costliest Years Ever for US Insurers

Hurricanes Harvey, Irma and Maria, California Wildfires Exact a Huge Toll

53

54

$21 $3

5

$60

$30

$55

$137

$76

$46

$37

$38

$135

$55

$18

$52

$23 $28

$63

$136

$0

$20

$40

$60

$80

$100

$120

$140

$160

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17*

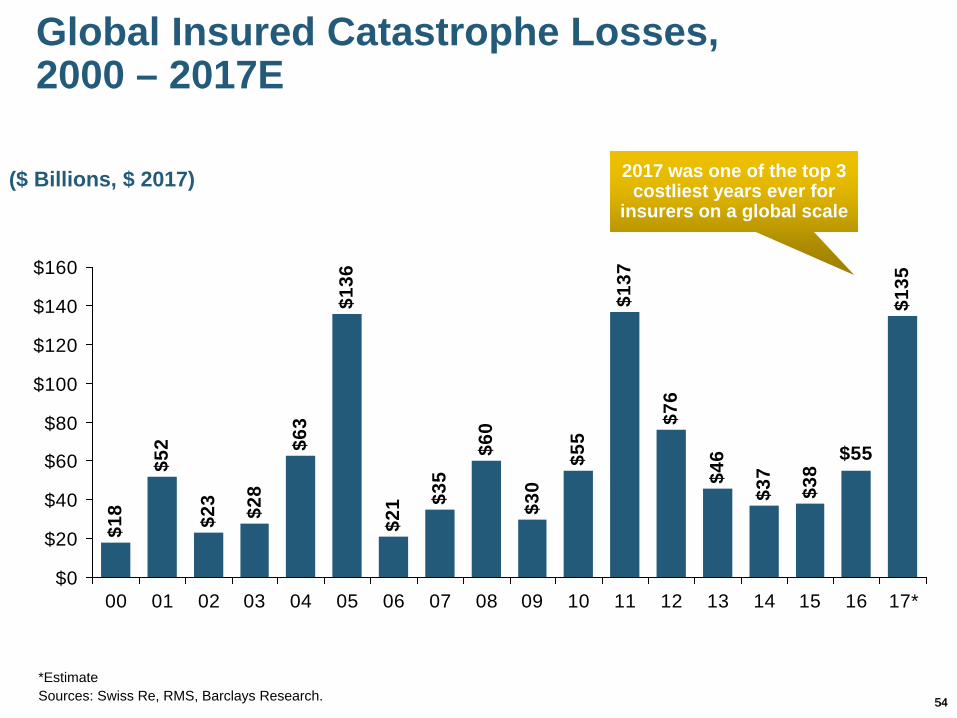

Global Insured Catastrophe Losses, 2000 – 2017E

*EstimateSources: Swiss Re, RMS, Barclays Research.

2017 was one of the top 3 costliest years ever for

insurers on a global scale($ Billions, $ 2017)

54

55

$13.

0$1

1.3

$3.9

$14.

8$1

1.9

$6.3

$35.

8$7

.8 $16.

8$3

4.7

$10.

9$7

.7$3

0.1

$11.

8$1

4.9

$34.

6$3

6.1

$13.

1$1

5.5

$15.

2 $21.

6$7

1.8$75.7

$14.

4$5

.0 $8.2

$38.

9$9

.1$2

7.2

$0

$10

$20

$30

$40

$50

$60

$70

$80

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17*

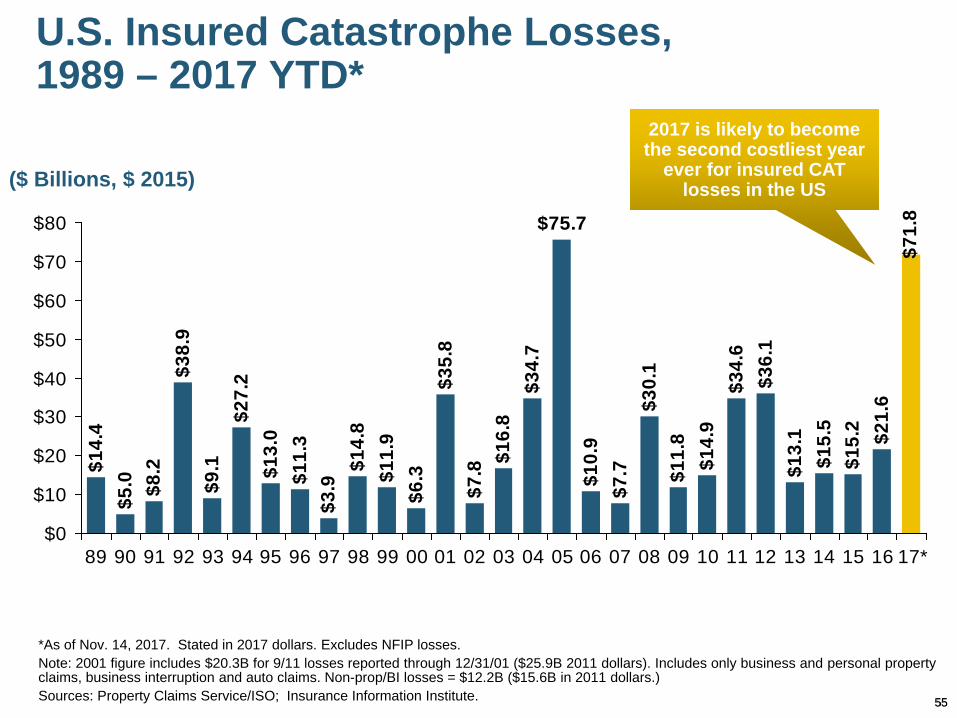

U.S. Insured Catastrophe Losses, 1989 – 2017 YTD*

*As of Nov. 14, 2017. Stated in 2017 dollars. Excludes NFIP losses.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01 ($25.9B 2011 dollars). Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B ($15.6B in 2011 dollars.) Sources: Property Claims Service/ISO; Insurance Information Institute.

2017 is likely to become the second costliest year

ever for insured CAT losses in the US($ Billions, $ 2015)

55

56

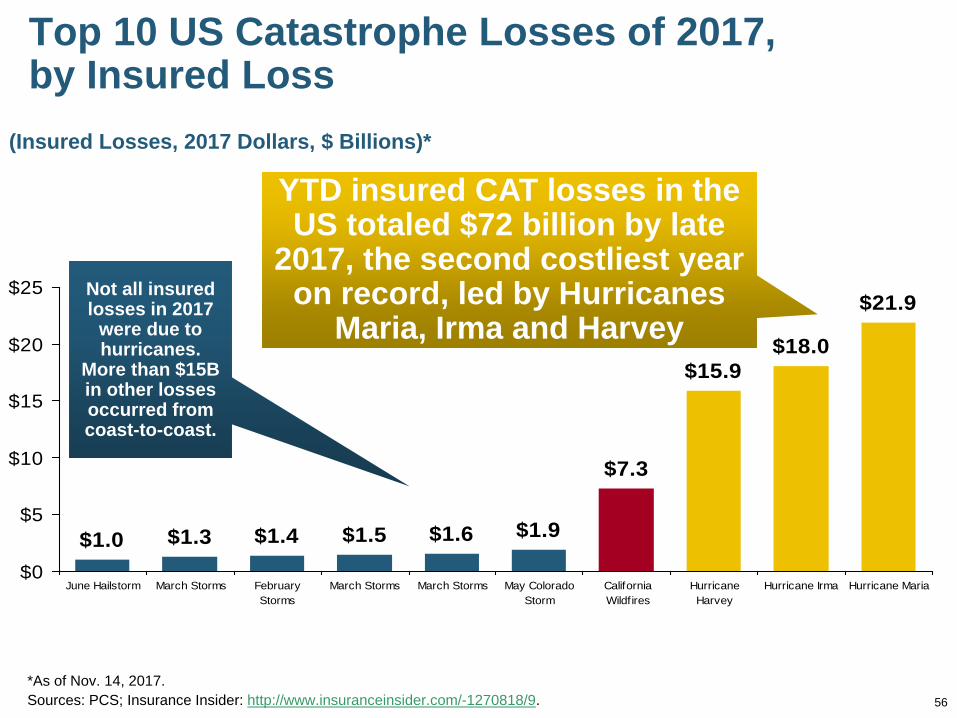

Top 10 US Catastrophe Losses of 2017,by Insured Loss

(Insured Losses, 2017 Dollars, $ Billions)*

$7.3

$15.9$18.0

$21.9

$1.9$1.6$1.5$1.4$1.3$1.0$0

$5

$10

$15

$20

$25

June Hailstorm March Storms FebruaryStorms

March Storms March Storms May ColoradoStorm

CaliforniaWildfires

HurricaneHarvey

Hurricane Irma Hurricane Maria

YTD insured CAT losses in the US totaled $72 billion by late

2017, the second costliest year on record, led by Hurricanes

Maria, Irma and HarveyNot all insured losses in 2017

were due to hurricanes.

More than $15B in other losses occurred from coast-to-coast.

*As of Nov. 14, 2017.Sources: PCS; Insurance Insider: http://www.insuranceinsider.com/-1270818/9.

57

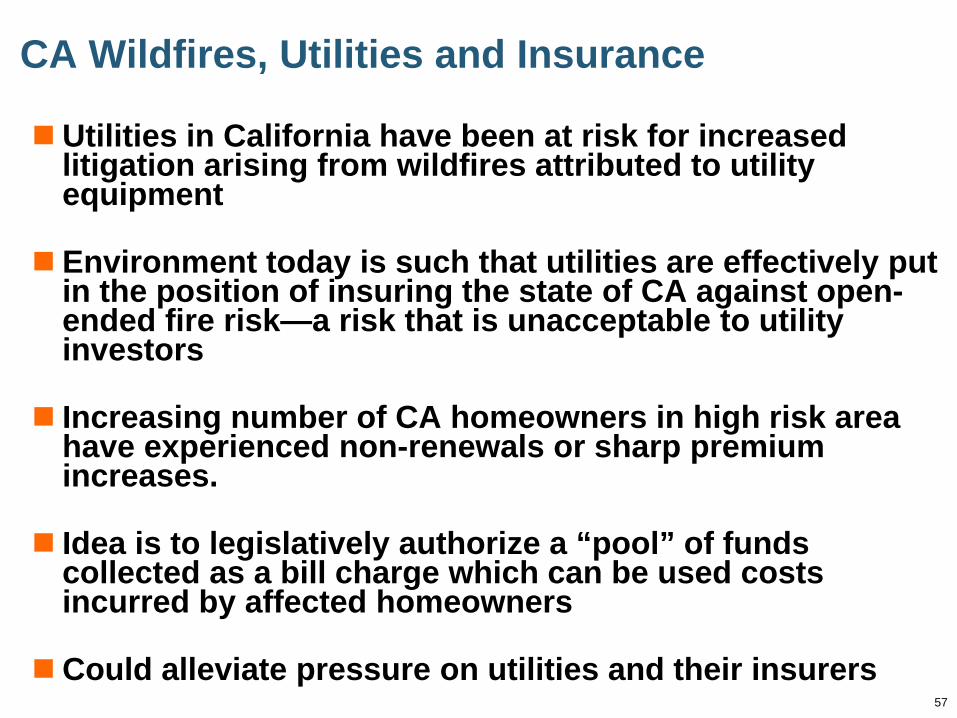

CA Wildfires, Utilities and Insurance

Utilities in California have been at risk for increased litigation arising from wildfires attributed to utility equipment

Environment today is such that utilities are effectively put in the position of insuring the state of CA against open-ended fire risk—a risk that is unacceptable to utility investors

Increasing number of CA homeowners in high risk area have experienced non-renewals or sharp premium increases.

Idea is to legislatively authorize a “pool” of funds collected as a bill charge which can be used costs incurred by affected homeowners

Could alleviate pressure on utilities and their insurers

58

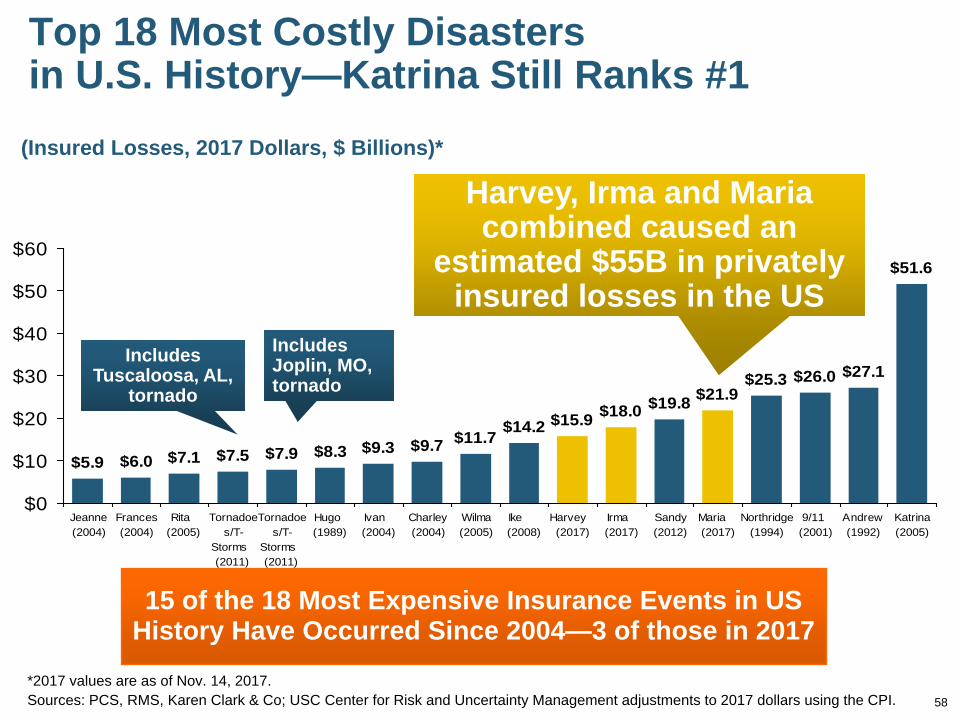

Top 18 Most Costly Disastersin U.S. History—Katrina Still Ranks #1

(Insured Losses, 2017 Dollars, $ Billions)*

$9.3 $9.7 $11.7 $14.2 $15.9 $18.0 $19.8 $21.9$25.3 $26.0 $27.1

$51.6

$8.3$7.9$7.5$7.1$6.0$5.9

$0

$10

$20

$30

$40

$50

$60

Jeanne(2004)

Frances(2004)

Rita (2005)

Tornadoes/T-

Storms (2011)

Tornadoes/T-

Storms (2011)

Hugo (1989)

Ivan (2004)

Charley(2004)

Wilma(2005)

Ike (2008)

Harvey (2017)

Irma (2017)

Sandy(2012)

Maria (2017)

Northridge(1994)

9/11 (2001)

Andrew(1992)

Katrina(2005)

Harvey, Irma and Maria combined caused an

estimated $55B in privately insured losses in the US

Includes Tuscaloosa, AL,

tornado

Includes Joplin, MO, tornado

15 of the 18 Most Expensive Insurance Events in US History Have Occurred Since 2004—3 of those in 2017

*2017 values are as of Nov. 14, 2017.Sources: PCS, RMS, Karen Clark & Co; USC Center for Risk and Uncertainty Management adjustments to 2017 dollars using the CPI.

59

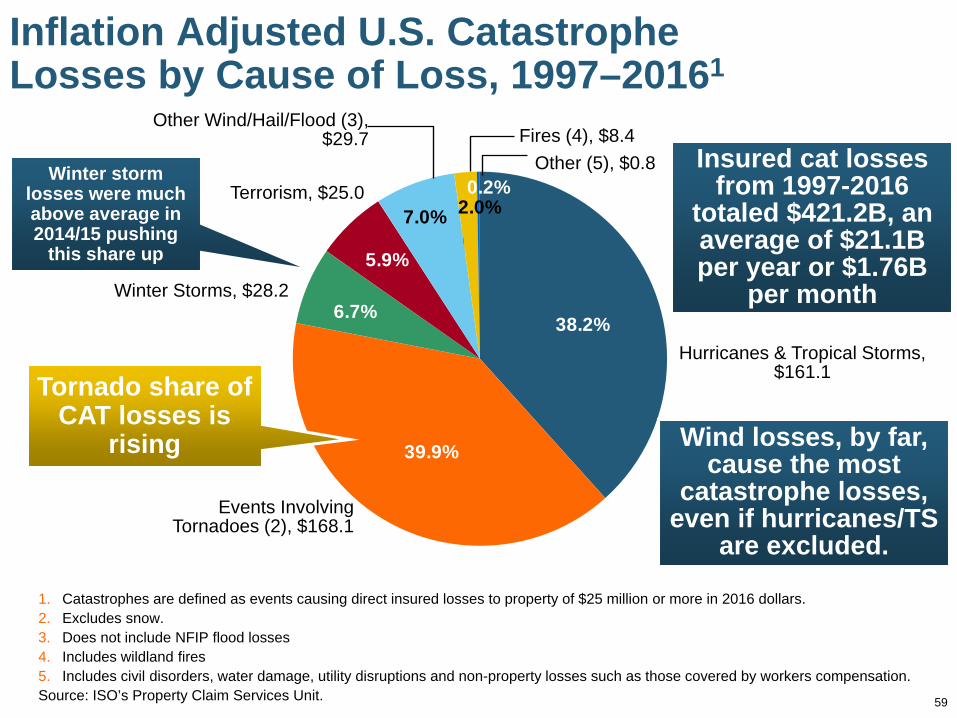

Inflation Adjusted U.S. Catastrophe Losses by Cause of Loss, 1997–20161

0.2%2.0%7.0%

5.9%

6.7%

39.9%

38.2%

1. Catastrophes are defined as events causing direct insured losses to property of $25 million or more in 2016 dollars.2. Excludes snow.3. Does not include NFIP flood losses4. Includes wildland fires5. Includes civil disorders, water damage, utility disruptions and non-property losses such as those covered by workers compensation.Source: ISO’s Property Claim Services Unit.

Hurricanes & Tropical Storms, $161.1

Fires (4), $8.4

Events Involving Tornadoes (2), $168.1

Winter Storms, $28.2

Terrorism, $25.0

Other Wind/Hail/Flood (3), $29.7

Other (5), $0.8

Wind losses, by far, cause the most

catastrophe losses, even if hurricanes/TS

are excluded.

Tornado share of CAT losses is

rising

Insured cat losses from 1997-2016

totaled $421.2B, an average of $21.1B per year or $1.76B

per month

Winter storm losses were much above average in 2014/15 pushing

this share up

60

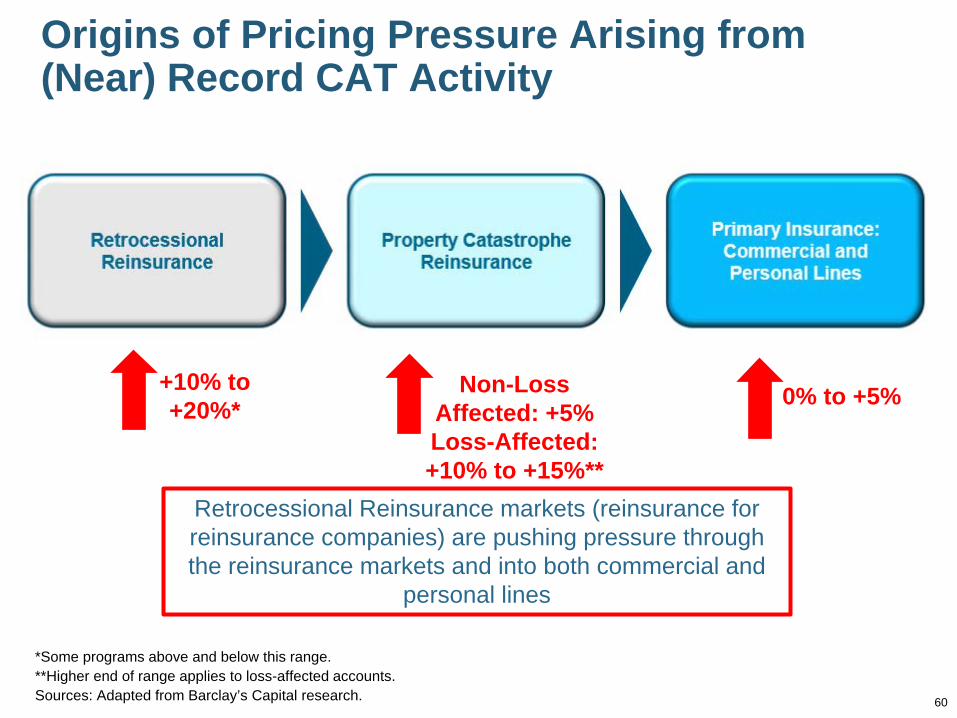

Origins of Pricing Pressure Arising from (Near) Record CAT Activity

*Some programs above and below this range.**Higher end of range applies to loss-affected accounts.Sources: Adapted from Barclay’s Capital research.

+10% to +20%*

Non-Loss Affected: +5% Loss-Affected: +10% to +15%**

0% to +5%

Retrocessional Reinsurance markets (reinsurance for reinsurance companies) are pushing pressure through the reinsurance markets and into both commercial and

personal lines

61

0

50

100

150

200

250

300

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18*

(Percent)

US Reinsurance Pricing Is Sensitive to CAT Activity and Ultimately Impacts Primary Insurance Pricing, Terms and Conditions

Post-Andrew surge

US Property Catastrophe Rate-on-Line Index: 1990 – 2018*

*As of January 1 each year. 2018 is a full-year estimate (Barclay’s Capital).Source: Guy Carpenter; Artimes.bm accessed at: http://www.artemis.bm/indices/regional-property-cat-rate-on-line-index.html

Post-9/11 Adjustment

Post Katrina, Rita, Wilma

period

Post-Ike adjustment

Adjustment following

record tornado losses in 2011 and Sandy in

2012

Near-Record CATs in 2017 will likely lead US reinsurance prices in

2018 to increase

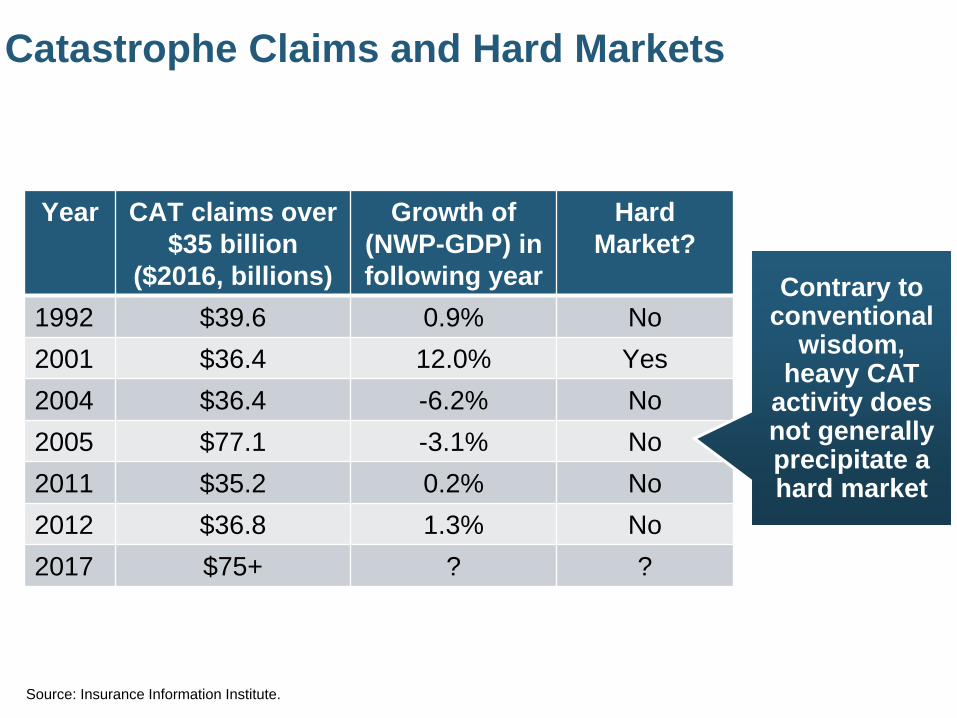

Catastrophe Claims and Hard Markets

Year CAT claims over $35 billion

($2016, billions)

Growth of (NWP-GDP) in following year

Hard Market?

1992 $39.6 0.9% No2001 $36.4 12.0% Yes2004 $36.4 -6.2% No2005 $77.1 -3.1% No2011 $35.2 0.2% No2012 $36.8 1.3% No2017 $75+ ? ?

Contrary to conventional

wisdom, heavy CAT

activity does not generally precipitate a hard market

Source: Insurance Information Institute.

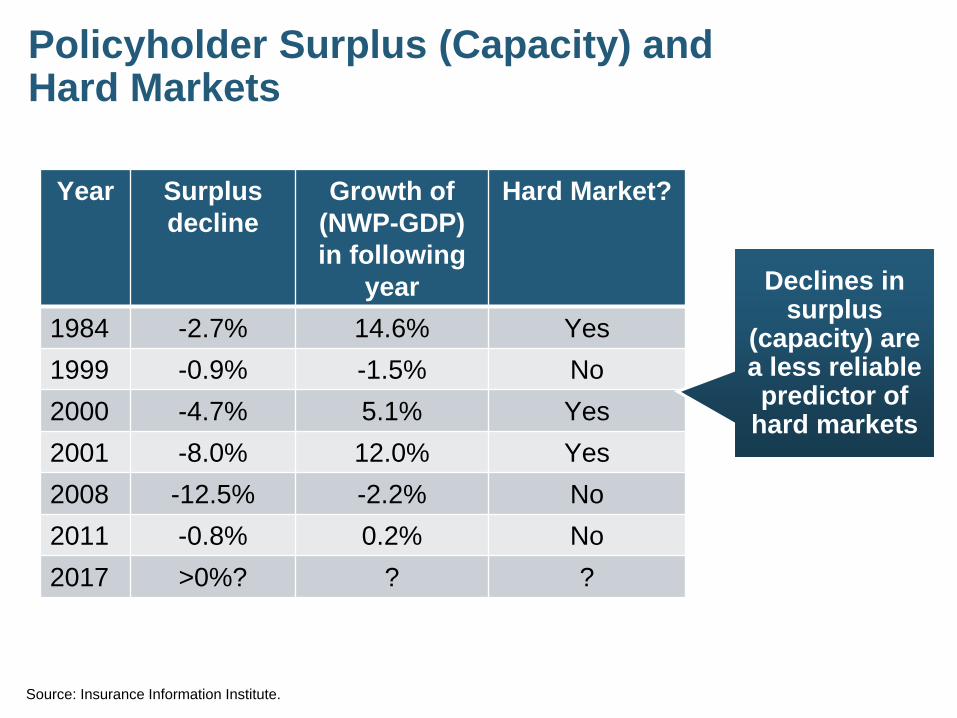

Policyholder Surplus (Capacity) andHard Markets

Year Surplus decline

Growth of (NWP-GDP)in following

year

Hard Market?

1984 -2.7% 14.6% Yes1999 -0.9% -1.5% No2000 -4.7% 5.1% Yes2001 -8.0% 12.0% Yes2008 -12.5% -2.2% No2011 -0.8% 0.2% No2017 >0%? ? ?

Declines in surplus

(capacity) are a less reliable predictor of

hard markets

Source: Insurance Information Institute.

P/C Insurance Industry ROE and Hard Markets

Year P/C Industry ROE less than 4%

Growth of (NWP-GDP)in following

year

Hard Market?

1975 2.4% 10.7% Yes1984 1.8% 14.6% Yes2001 -1.2% 12.0% Yes2002 2.1% 5.1% Yes2017 ~4% ? ?

Source: Insurance Information Institute.

Depressed ROEs are a historically

reliable predictor of

hard markets

Hard Markets: Conclusion & Implications for 2018 Low ROE is the best predictor of a hard market (likely

around 4% in 2017), but does this mean a hard market is a sure thing? No…but some “correction” is possible

Surplus in 2017 was nearly flat to slightly up Capacity remains generally abundant and seems likely to

grow–not drop–due to asset value growth, implying that a true hard market is unlikely to develop as a result of depleted capacity

CAT Losses: 2017 was one of the worst years on record for cat losses–implying a hard market–but this predictor does not appear to be an accurate one, at least in isolation Greatest impacts are driven through property cat reinsurance

and retro markets on loss impacted areas and accounts

Trumponomics, Insurance and Politics

6666

How Might the Trump Presidency Impact the Insurance Industry?

67

Trumponomics: The Essential Elements

5 Elements Tax ReformDeregulation Infrastructure InvestmentHealthcare Fair Trade Immigration

Reform/Enforcement

Most of these have direct impacts for insurers

Tax Reform…and More

6868

Tax Reform Could Favorably Impact the Insurance Industry

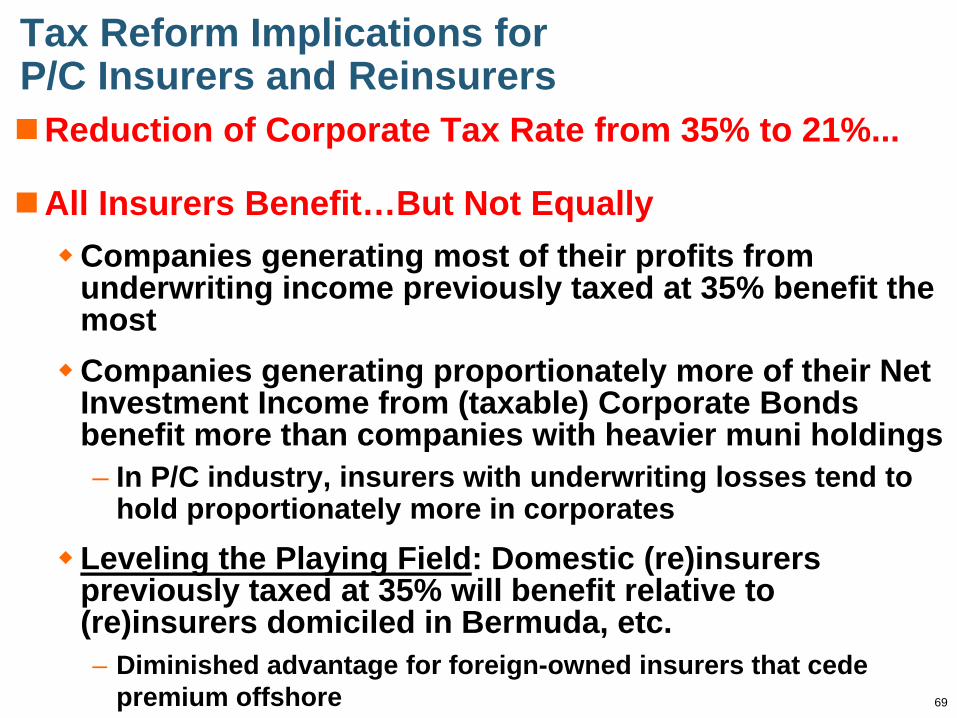

69

Tax Reform Implications for P/C Insurers and ReinsurersReduction of Corporate Tax Rate from 35% to 21%...

All Insurers Benefit…But Not EquallyCompanies generating most of their profits from

underwriting income previously taxed at 35% benefit the mostCompanies generating proportionately more of their Net

Investment Income from (taxable) Corporate Bonds benefit more than companies with heavier muni holdings– In P/C industry, insurers with underwriting losses tend to

hold proportionately more in corporatesLeveling the Playing Field: Domestic (re)insurers

previously taxed at 35% will benefit relative to (re)insurers domiciled in Bermuda, etc.– Diminished advantage for foreign-owned insurers that cede

premium offshore

70

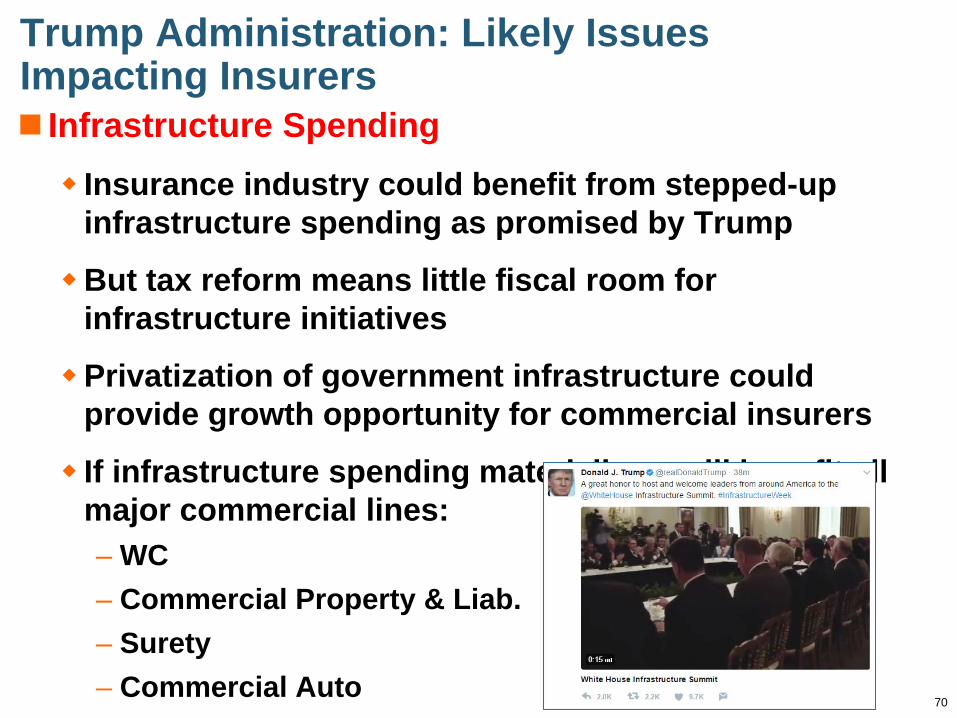

Trump Administration: Likely Issues Impacting Insurers Infrastructure Spending Insurance industry could benefit from stepped-up

infrastructure spending as promised by Trump

But tax reform means little fiscal room for infrastructure initiatives

Privatization of government infrastructure could provide growth opportunity for commercial insurers

If infrastructure spending materializes, will benefit all major commercial lines:– WC– Commercial Property & Liab.– Surety– Commercial Auto

Tax Reform: Utility Sector Highlights

7171

Beyond the Headline Tax Cut, New Law Has Mixed Impacts

on Utilities

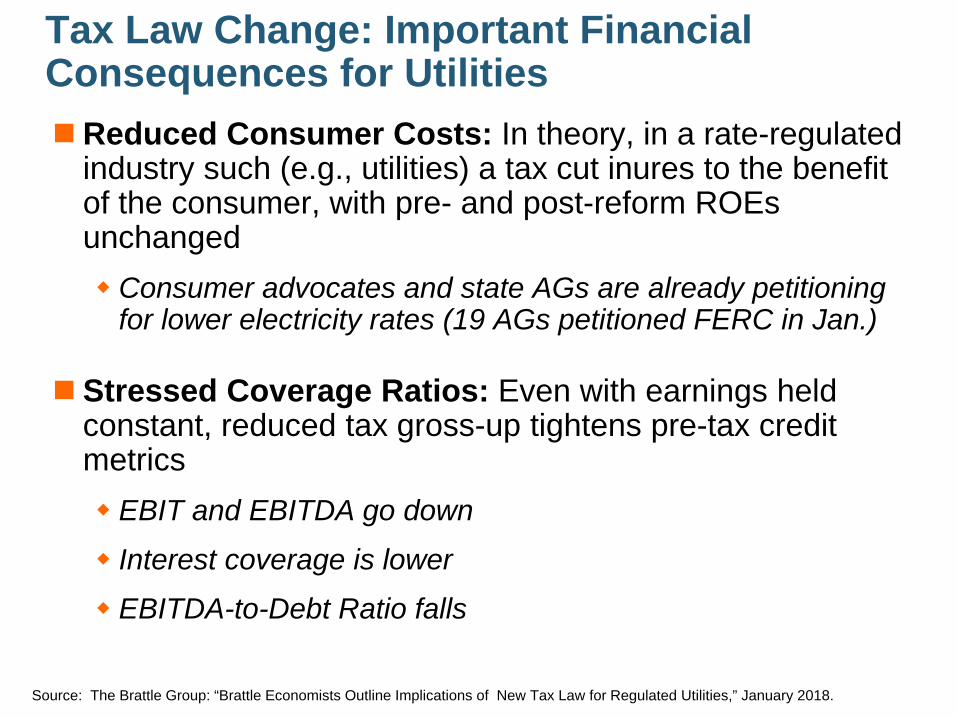

Tax Law Change: Important Financial Consequences for UtilitiesReduced Consumer Costs: In theory, in a rate-regulated

industry such (e.g., utilities) a tax cut inures to the benefit of the consumer, with pre- and post-reform ROEs unchanged Consumer advocates and state AGs are already petitioning

for lower electricity rates (19 AGs petitioned FERC in Jan.)

Stressed Coverage Ratios: Even with earnings held constant, reduced tax gross-up tightens pre-tax credit metrics EBIT and EBITDA go down

Interest coverage is lower

EBITDA-to-Debt Ratio falls

Source: The Brattle Group: “Brattle Economists Outline Implications of New Tax Law for Regulated Utilities,” January 2018.

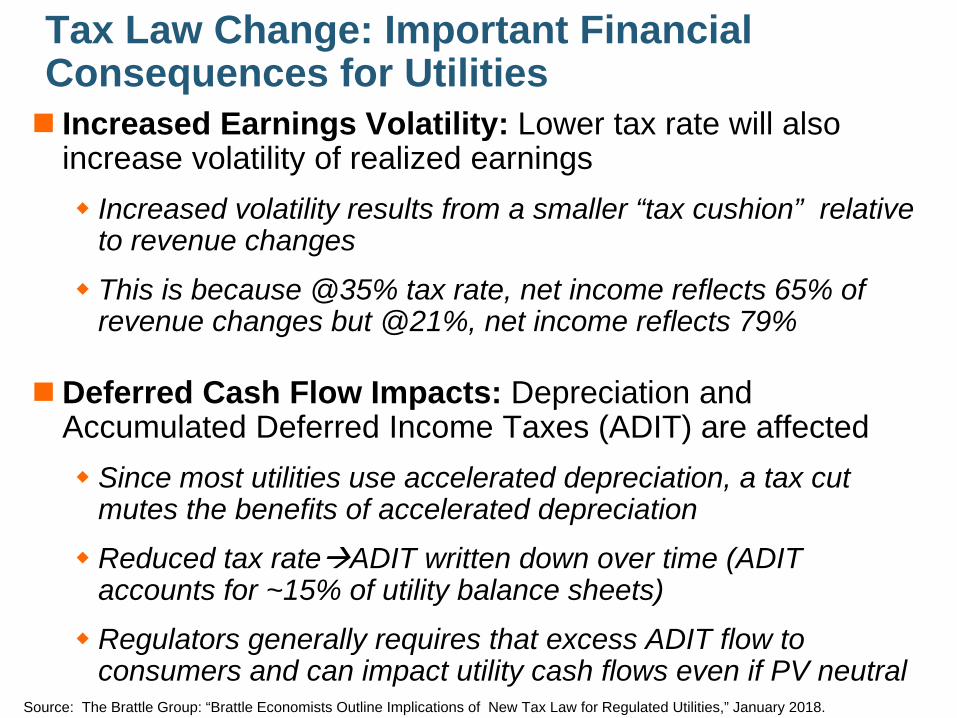

Tax Law Change: Important Financial Consequences for Utilities Increased Earnings Volatility: Lower tax rate will also

increase volatility of realized earnings Increased volatility results from a smaller “tax cushion” relative

to revenue changes

This is because @35% tax rate, net income reflects 65% of revenue changes but @21%, net income reflects 79%

Deferred Cash Flow Impacts: Depreciation and Accumulated Deferred Income Taxes (ADIT) are affected Since most utilities use accelerated depreciation, a tax cut

mutes the benefits of accelerated depreciation

Reduced tax rateADIT written down over time (ADIT accounts for ~15% of utility balance sheets)

Regulators generally requires that excess ADIT flow to consumers and can impact utility cash flows even if PV neutral

Source: The Brattle Group: “Brattle Economists Outline Implications of New Tax Law for Regulated Utilities,” January 2018.

Tax Law Change: Important Financial Consequences for Utilities Stressed Credit Assessments: Moody’s in January 2018

lowered the outlook on 24 regulated utilitiesMoody cited “incremental cash flow shortfall caused by tax

reform on projected financial metrics…”

Excess deferred tax liabilities become a liability on the balance sheet, likely resulting consumer refunds

Possibly Weakened Rationales to Build: Tax law appears to tip buy/build assessment toward buy, especially for tax-advantaged assets like renewables But there can be offsetting factors

Source: The Brattle Group: “Brattle Economists Outline Implications of New Tax Law for Regulated Utilities,” January 2018.

75

Energy Market Overview, the Economy and Insurance

Energy Markets Are Undergoing a Long-Run Transformation in Terms of Fuels, Sources, Generation and Transmission

Overall Demand Remains Robust75

76

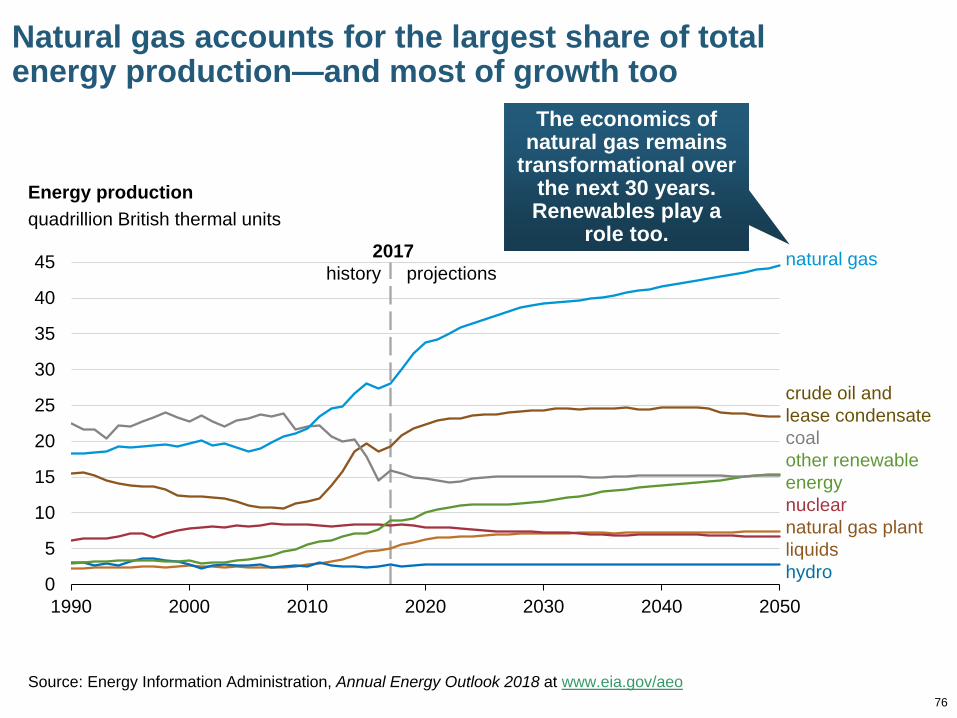

Energy production quadrillion British thermal units

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

Natural gas accounts for the largest share of totalenergy production—and most of growth too

0

5

10

15

20

25

30

35

40

45

1990 2000 2010 2020 2030 2040 2050

natural gas

crude oil and lease condensatecoalother renewable energynuclearnatural gas plant liquidshydro

2017history projections

The economics of natural gas remains

transformational over the next 30 years. Renewables play a

role too.

77

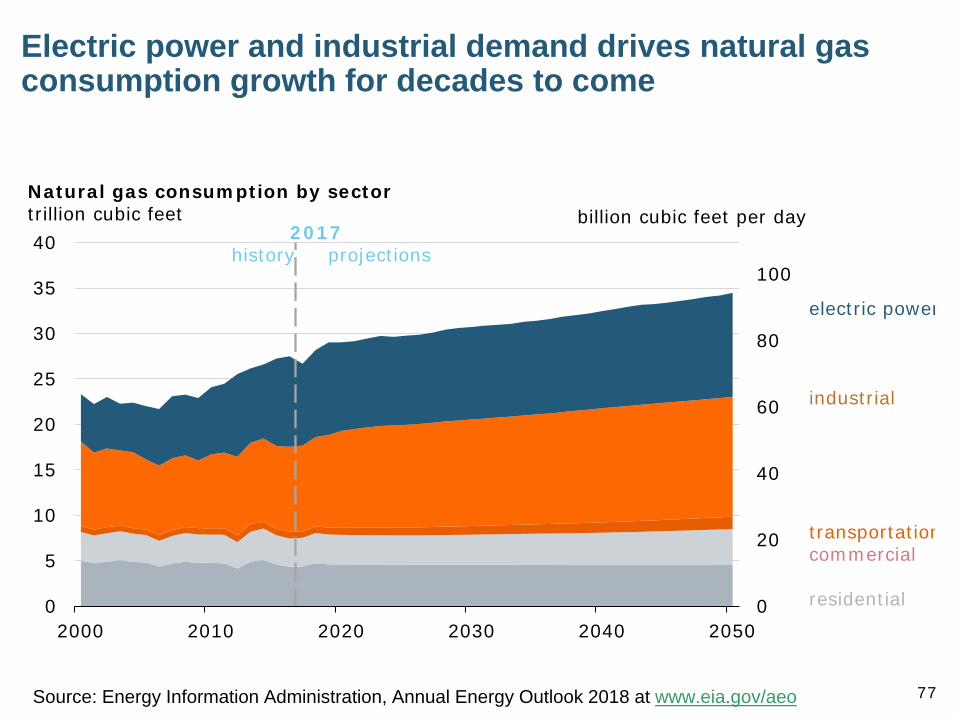

Electric power and industrial demand drives natural gas consumption growth for decades to come

0

20

40

60

80

100

0

5

10

15

20

25

30

35

40

2000 2010 2020 2030 2040 2050

Natural gas consumption by sector trillion cubic feet

electric power

industrial

transportationcommercial

residential

billion cubic feet per day2017

history projections

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

78

Electricity: The Transformation Continues

Economics, Technology, Politics and Regulation Will Reshape Electricity

Generation and Transmission for Decades to Come

A Peek into the Industry at Mid-Century78

79

After Decades of Slowing Growth, Electricity Use is Expected to Grow Steadily through 2050—

0200400600800

1,0001,2001,4001,6001,8002,000

1990

2017

2050

1990

2017

2050

1990

2017

2050

1990

2017

2050

Electricity use by end-use demand sector billion kilowatthours

direct use

electricity sales

residential industrialcommercial transport-1

0

1

2

3

4

5

1990 2000 2010 2020 2030 2040 2050

Electricity use growth rate percent growth (three-year rolling average)

2017history projections

High Economic GrowthReference Low Economic Growth

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

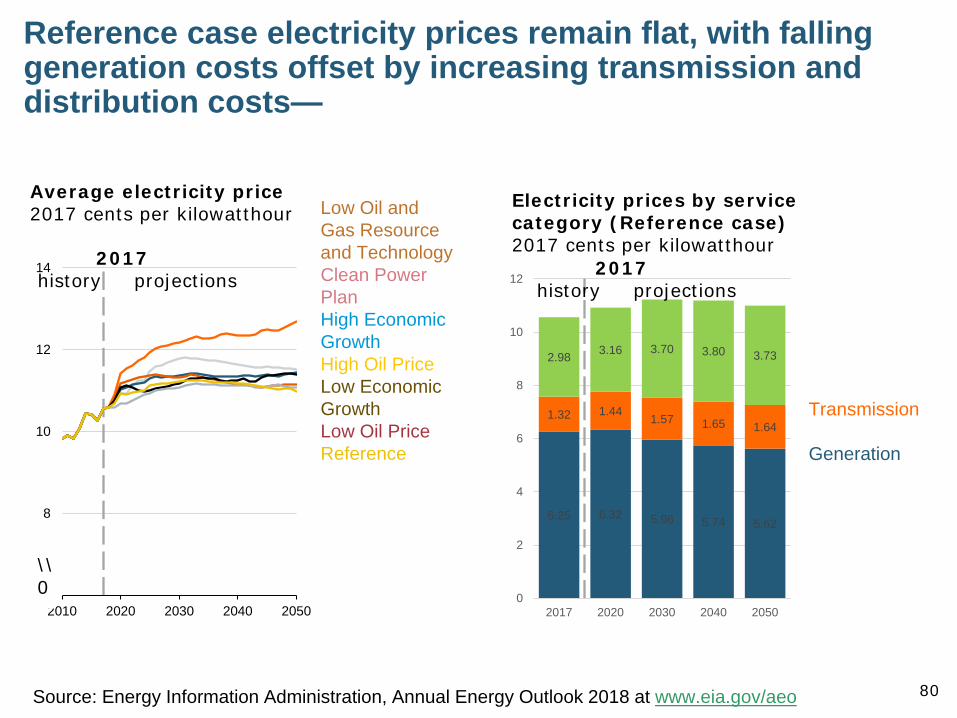

80

Reference case electricity prices remain flat, with falling generation costs offset by increasing transmission and distribution costs—

6

8

10

12

14

2010 2020 2030 2040 2050

Average electricity price2017 cents per kilowatthour

2017history projections

Low Oil and Gas Resource and TechnologyClean Power PlanHigh Economic GrowthHigh Oil PriceLow Economic GrowthLow Oil PriceReferenceHigh Oil and Gas Resource and Technology

\\0

6.25 6.32 5.96 5.74 5.62

1.32 1.441.57 1.65 1.64

2.98 3.16 3.70 3.80 3.73

0

2

4

6

8

10

12

2017 2020 2030 2040 2050

Electricity prices by service category (Reference case)2017 cents per kilowatthour

Distribution

Transmission

Generation

2017history projections

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

81

Projected mix of electricity generation technologies shows natural gas and renewables gaining share through 2050

0

500

1,000

1,500

2,000

2,500

3,000

1990 2000 2010 2020 2030 2040 2050

2017history projections

Reference case

Electricity generation from selected fuelsbillion kilowatthours

natural gas

coal

nuclear

renewables renewables

Electricity generation market share moves

strongly toward natural gas and

renewables and away from coal and nuclear

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

82

Coal-fired electric generating capacity decreases through 2030, even without the Clean Power Plan or lower natural gas prices—

0

50

100

150

200

250

300

350

2010 2020 2030 2040 2050

Coal generation capacitygigawatts

2017history projections

Low Oil and Gas Resource and TechnologyReference High Oil and Gas Resource and Technology

without Clean Power Plan with Clean Power Plan

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

83

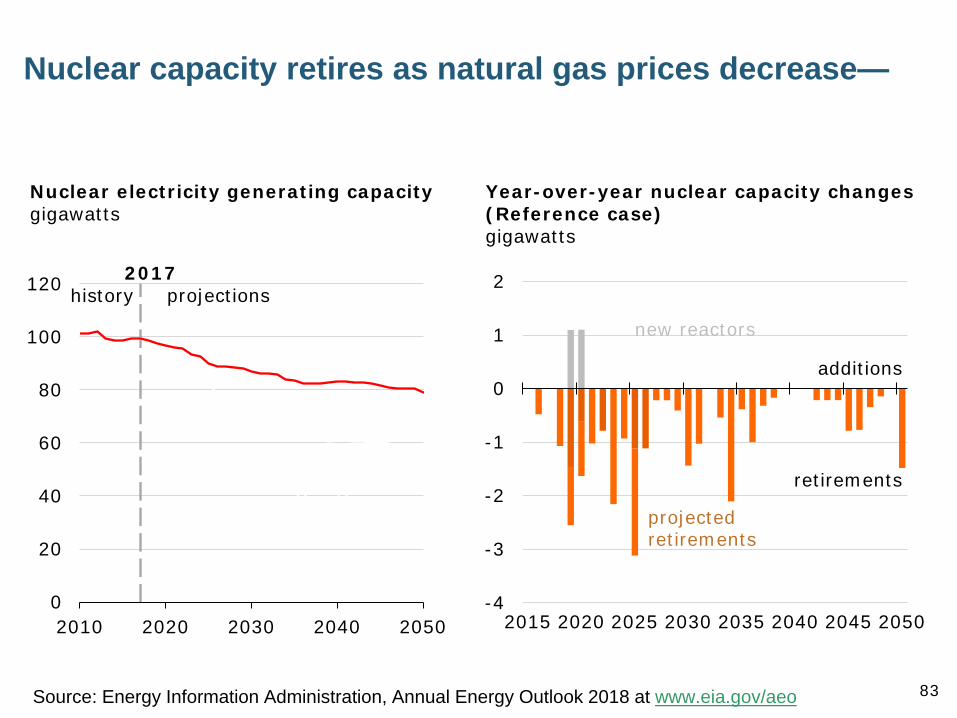

Nuclear capacity retires as natural gas prices decrease—

0

20

40

60

80

100

120

2010 2020 2030 2040 2050

Nuclear electricity generating capacitygigawatts

2017history projections

High Oil and Gas Resource and Technology

-4

-3

-2

-1

0

1

2

2015 2020 2025 2030 2035 2040 2045 2050

Year-over-year nuclear capacity changes (Reference case)gigawatts

additions

retirements

assumed upratesnew reactors

projectedretirements

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

84

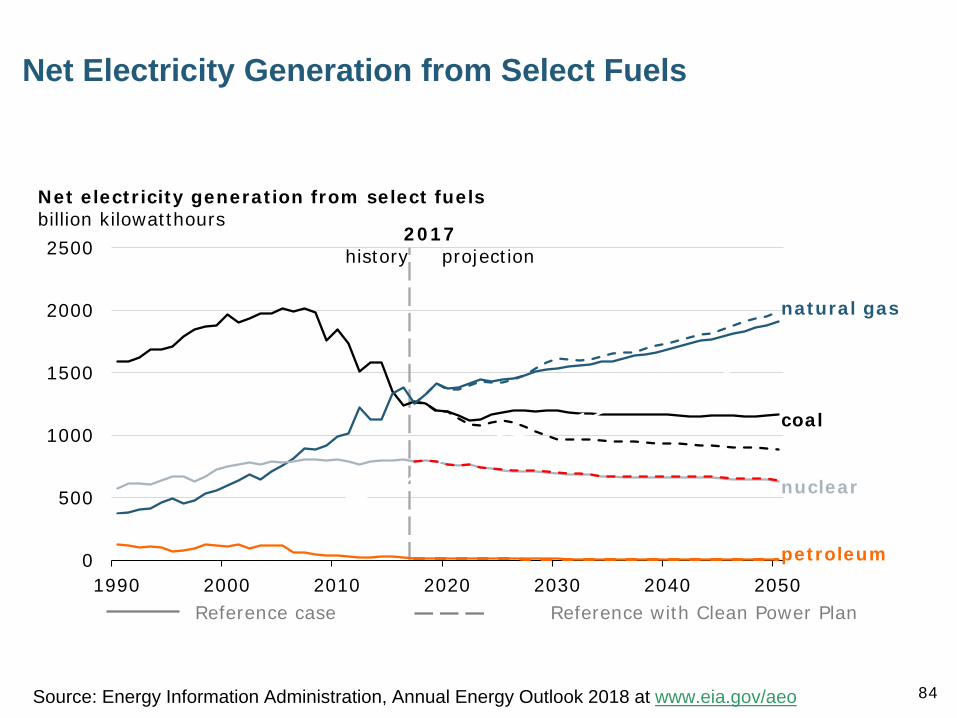

Net Electricity Generation from Select Fuels

0

500

1000

1500

2000

2500

1990 2000 2010 2020 2030 2040 2050

Net electricity generation from select fuelsbillion kilowatthours

2017history projection

Reference case Reference with Clean Power Plan

natural gas

renewables

coal

nuclear

petroleum

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

85

Generation from renewable sources grows across all cases, led by growth in wind and solar photovoltaic generation—

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2010 2020 2030 2040 2050

Total renewables generation, including end-use generationbillion kilowatthours

2017history projections

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2010 2020 2030 2040 2050

Renewable electricity generation, including end-use generation (Referenc billion kilowatthours

2017history projections

solar PV

wind

geothermalhydroelectric

other

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

86

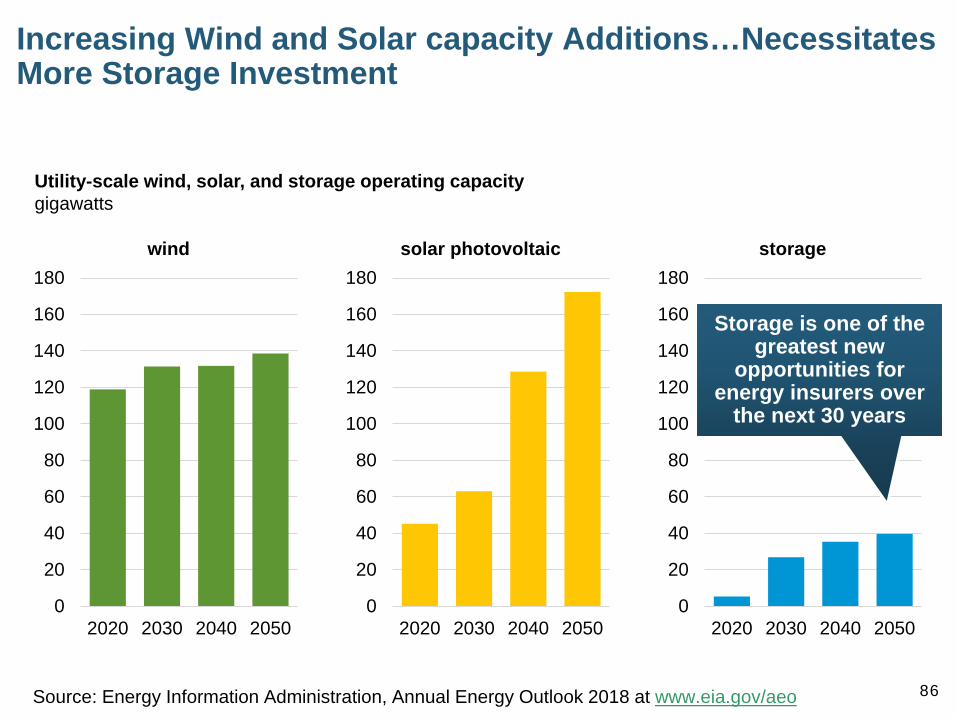

Increasing Wind and Solar capacity Additions…Necessitates More Storage Investment

0

20

40

60

80

100

120

140

160

180

2020 2030 2040 2050

wind

0

20

40

60

80

100

120

140

160

180

2020 2030 2040 2050

storage

0

20

40

60

80

100

120

140

160

180

2020 2030 2040 2050

solar photovoltaic

Utility-scale wind, solar, and storage operating capacitygigawatts

Storage is one of the greatest new

opportunities for energy insurers over

the next 30 years

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

87

From 2020 to 2050, utility-scale wind capacity is projected to grow by 20 GW (~17%), and utility-scale solar photovoltaic capacity is projected to grow by 127 GW (>300%) Over this same period, utility-scale storage capacity is projected to grow by 34 GW (~400%).

Battery-based storage costs are expected to continue to decline as utility-scale energy storage markets grow.

Policies such as storage mandates in California and market participation rules in the PJM electricity market support near-term growth in storage systems to stabilize grid operations, improve utilization of existing generators, and integrate intermittent technologies such as wind and solar into the grid.

In the longer term, wind and solar growth are projected to support economic opportunities for storage systems that can provide several hours of storage and enable renewables generation produced during the hours with high wind or solar output to supply electricity at times of peak electricity demand.

The Business Case for Storage

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

88

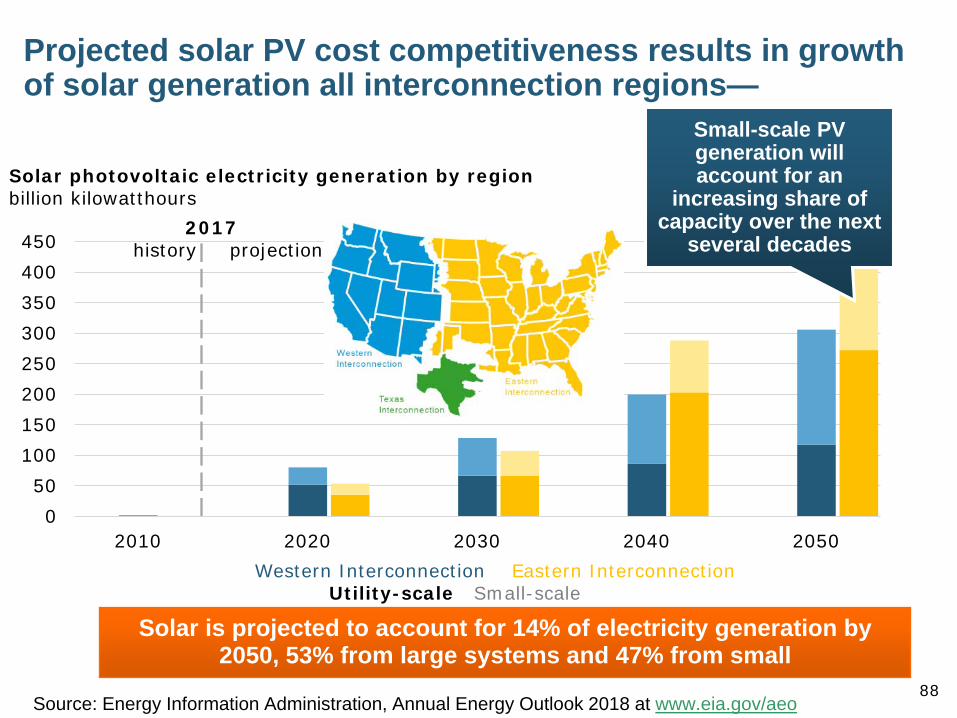

Projected solar PV cost competitiveness results in growth of solar generation all interconnection regions—

050

100150200250300350400450

2010 2020 2030 2040 2050Texas Western Interconnection Eastern Interconnection

Utility-scale Small-scale

Solar photovoltaic electricity generation by regionbillion kilowatthours

2017history projections

Small-scale PV generation will account for an

increasing share of capacity over the next

several decades

Solar is projected to account for 14% of electricity generation by 2050, 53% from large systems and 47% from small

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

89

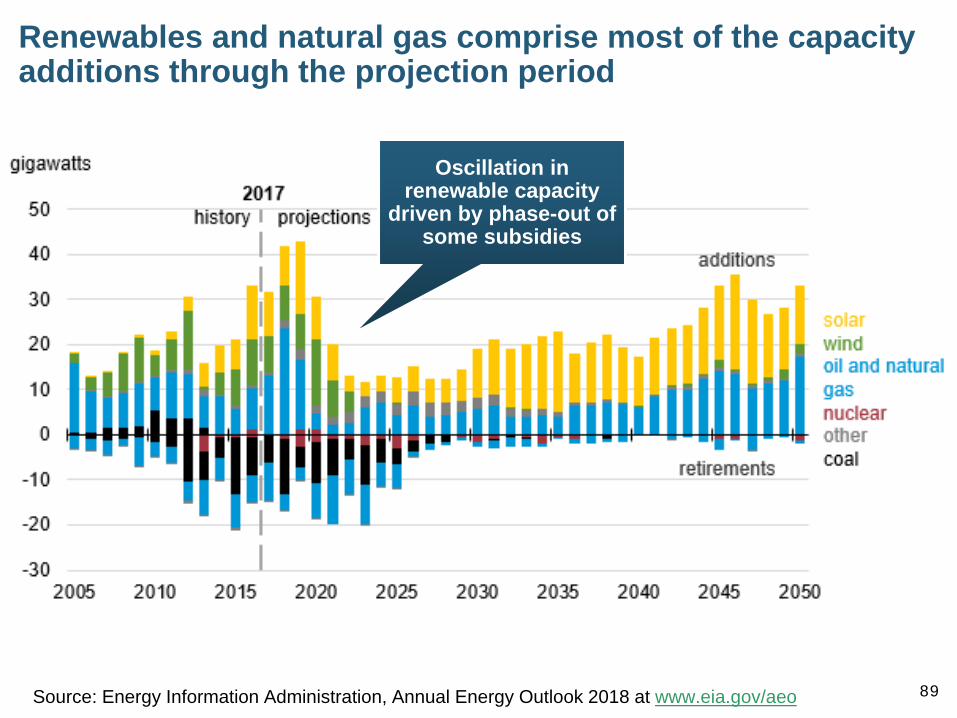

Renewables and natural gas comprise most of the capacity additions through the projection period

Source: Energy Information Administration, Annual Energy Outlook 2018 at www.eia.gov/aeo

Oscillation in renewable capacity

driven by phase-out of some subsidies

90

Summary P/C Insurers and Reinsurance Remain Financially Strong

Despite Record CATs

Financial Market Pressures Remain and Volatility Returns

Robust Insurer Growth Opportunities in 2018-2019

Near-Term Economic Picture Remains Bright

“Trumponomics” is a Near-Term Growth Driver

Energy Sector Is in the Midst of a Multi-Decade Transformation Driven by Economics, Technology and Geo-Politics

Electricity: Growth & Transformation through Mid-Century

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwigFor a copy of this presentation, email me at [email protected]

91