Embed Size (px)

Citation preview

Overview of Global Trends in Services Economy and Indonesia’s Negotiations on Trade in Services: Opportunities and ChallengesJakarta, 22 November 2016

Prepared by Herliza Aman, Director, Directorate of Trade in Services Negotiations

DIRECTORATE GENERAL OF INTERNATIONAL TRADE NEGOTIATIONMINISTRY OF TRADE

I. Importance of trade in services in economic development for Indonesia

II. Role of global value chains and trade in services in Indonesia

III. Indonesia’s negotiations on trade in services and commitments made so far

IV. Current status and key issues of Indonesia’s services negotiations: the way forward

V. Indonesia’s participation in trade in services negotiations: opportunities and challenges

Outlines

2

The Importance of trade in services in economic development for Indonesia

Section I

3

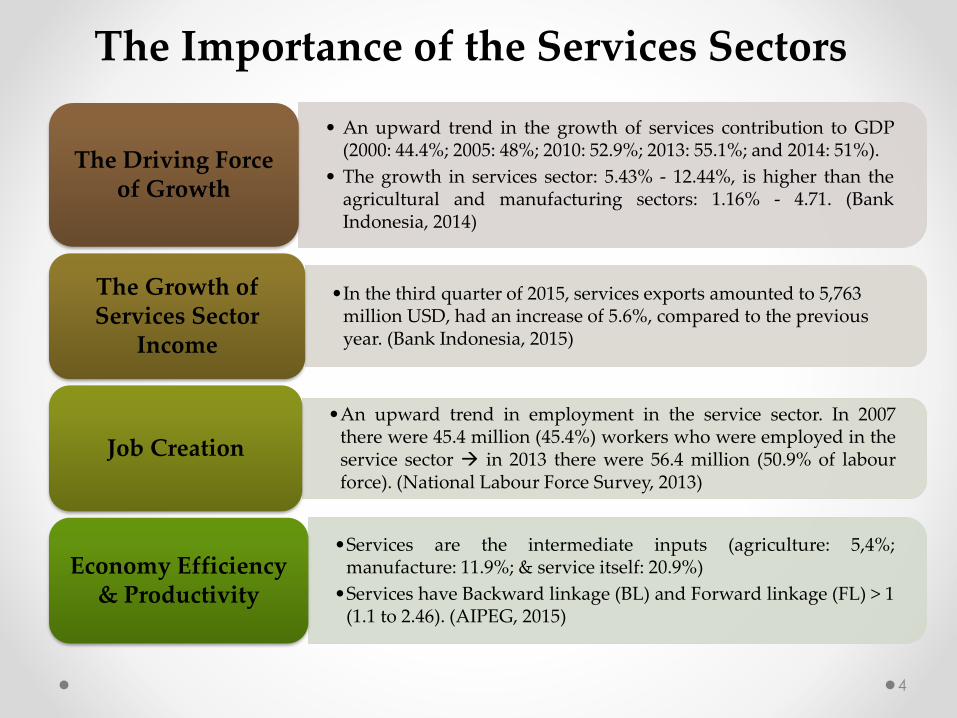

The Importance of the Services Sectors

• An upward trend in the growth of services contribution to GDP(2000: 44.4%; 2005: 48%; 2010: 52.9%; 2013: 55.1%; and 2014: 51%).

• The growth in services sector: 5.43% - 12.44%, is higher than theagricultural and manufacturing sectors: 1.16% - 4.71. (BankIndonesia, 2014)

The Driving Force of Growth

•In the third quarter of 2015, services exports amounted to 5,763 million USD, had an increase of 5.6%, compared to the previous year. (Bank Indonesia, 2015)

The Growth of Services Sector

Income

•An upward trend in employment in the service sector. In 2007there were 45.4 million (45.4%) workers who were employed in theservice sector in 2013 there were 56.4 million (50.9% of labourforce). (National Labour Force Survey, 2013)

Job Creation

•Services are the intermediate inputs (agriculture: 5,4%;manufacture: 11.9%; & service itself: 20.9%)

•Services have Backward linkage (BL) and Forward linkage (FL) > 1(1.1 to 2.46). (AIPEG, 2015)

Economy Efficiency & Productivity

4

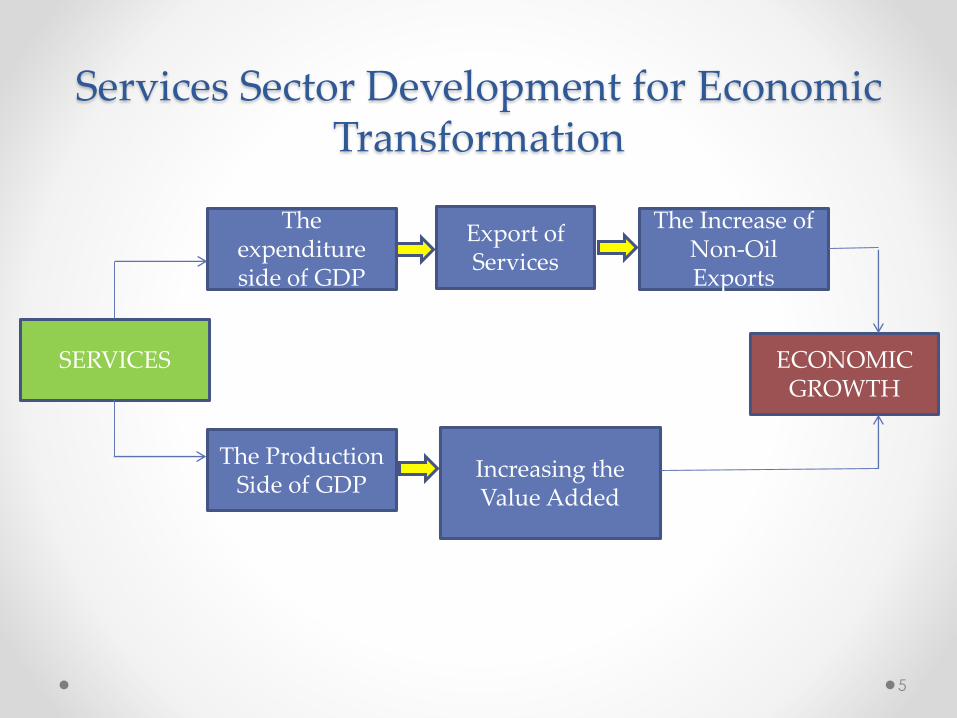

Services Sector Development for Economic Transformation

SERVICES

The Production Side of GDP

Increasing the Value Added

The expenditure side of GDP

ECONOMIC GROWTH

Export of Services

The Increase of Non-Oil Exports

5

SERVICES SECTORS IN THE MID-TERM NATIONAL DEVELOPMENT PLAN (2015-2019): DEVELOPMENT STRATEGY IN SUPPORTING

FOREIGN TRADE POLICY

The increasing quantity and quality of priority services sectors: 1. Services as an export booster: Transportation services, tourism

services and construction services

2. Services as a facilitator of trade and economic productivity: logistic services, distribution

services and financial services

Enhancing coordination among respective Ministries

in developing and implementing services

sectors roadmap

Participation in services global value

chain in order to enhance the

competitiveness of services sectors

Utilizing the services commitments in

international trade agreements

Increasing the quality of human resources related to services

sectors, as value add of services exports

Increasing the quality of trade in services

statistics to provide an accurate data and

information

6

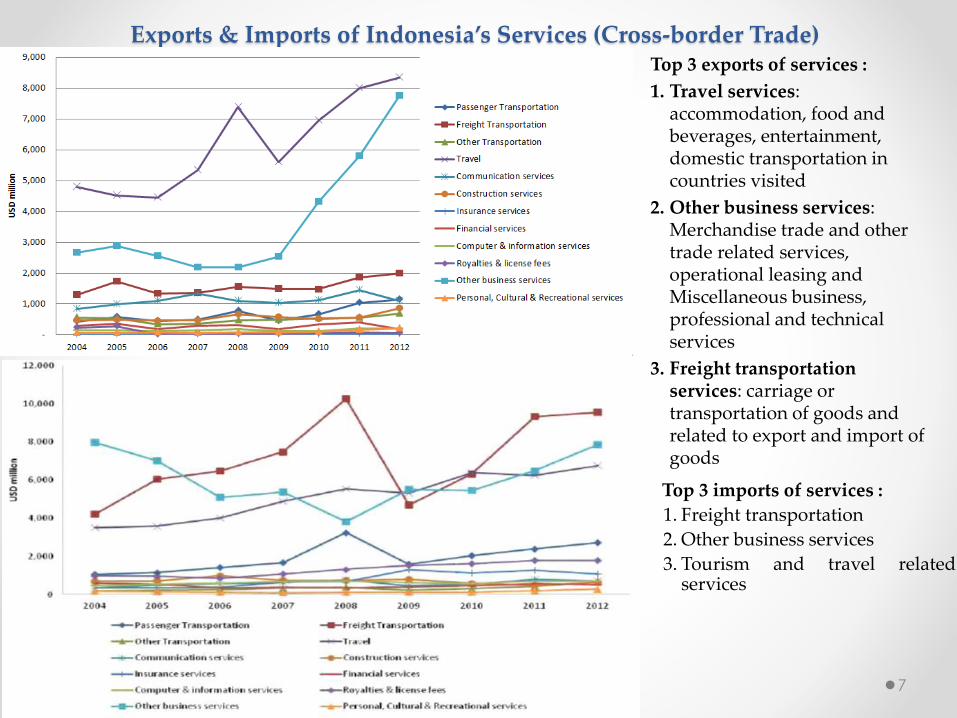

Exports & Imports of Indonesia’s Services (Cross-border Trade)

Source: Bank Indonesia

Top 3 exports of services :

1. Travel services: accommodation, food and beverages, entertainment, domestic transportation in countries visited

2. Other business services: Merchandise trade and other trade related services, operational leasing and Miscellaneous business, professional and technical services

3. Freight transportation services: carriage or transportation of goods and related to export and import of goods

Top 3 imports of services :

1. Freight transportation

2. Other business services

3. Tourism and travel relatedservices

7

Role of global value chains and trade in services in Indonesia

Section II

8

The Role of GVC and TIS• Global Value Chains (GVCs) are a strong driver of growth and productivity and

support job creation.

• The expansion of global value chains (GVCs) has become an important aspect of the current stage of economic globalization, driven by new technological opportunities and the old benefits of economic specialization.

• The whole process of producing goods, from raw materials to finished products, is increasingly carried out wherever the necessary skills and materials are available at competitive cost and quality.

• Similarly, trade in services is essential for the efficient functioning of GVCs, not only because services link activities across countries but also because they help companies to increase the value of their products.

• Services, and particularly GVC-enabling services such as business, transport and logistics, legal and communications services, are the links that forge global value chains.

• The role of services as input into manufacturing production, is substantial with services value added accounting for almost a third of manufacturing exports in developed countries and 26% in developing economies.

• GVCs can play an important role in the structural transformation of developing economies, but the capacity of such countries to benefit from GVCs should not be taken for granted.

• Open trade and investment policies, as well as regulatory simplicity and efficiency, are vitally important to allow services to be the enablers of global value chains 9

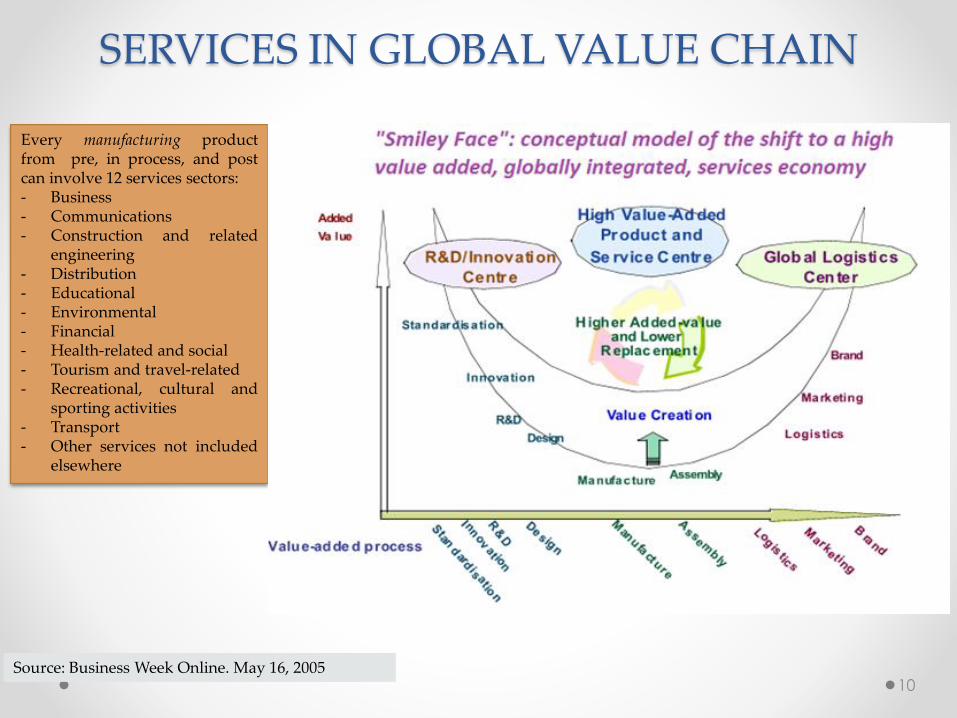

SERVICES IN GLOBAL VALUE CHAIN

Every manufacturing productfrom pre, in process, and postcan involve 12 services sectors:- Business- Communications- Construction and related

engineering- Distribution- Educational- Environmental- Financial- Health-related and social- Tourism and travel-related- Recreational, cultural and

sporting activities- Transport- Other services not included

elsewhere

Source: Business Week Online. May 16, 2005 10

Nomenclature of services

Source: APEC PSU Study: Services, Manufacturing and Productivity, 2015 11

SERVICES AS INPUTS TO NATIONAL PRIORITY SECTORS

Priority Sectors Goods Input

Direct and Indirect Services Inputs

Other Input Cost

Angkutan laut*) 47,68% 23,31% 29,01%

Automotive 48 % 12.5 % 41 %

Electronic 52.47 % 19.03 % 28.5 %

Textile 44.39 % 16.31 % 39.3 %

Chemicals 59.44 % 11.46 % 29.1 %

Food Processing 53.15 % 15.35 % 31.5 %

Bamboo, wood, and rattan

39.34 % 18.46 % 42.2 %

Rubber and plastic 58.48 % 14.12 % 27.4 %

Source: Based on Table 2. Total Transaction based on producer prices (BPS 2009)

Services are needed for goods to be high value and competitive

*) Based on Table 2. Total Transaction based on producer prices (BPS 2005) 12

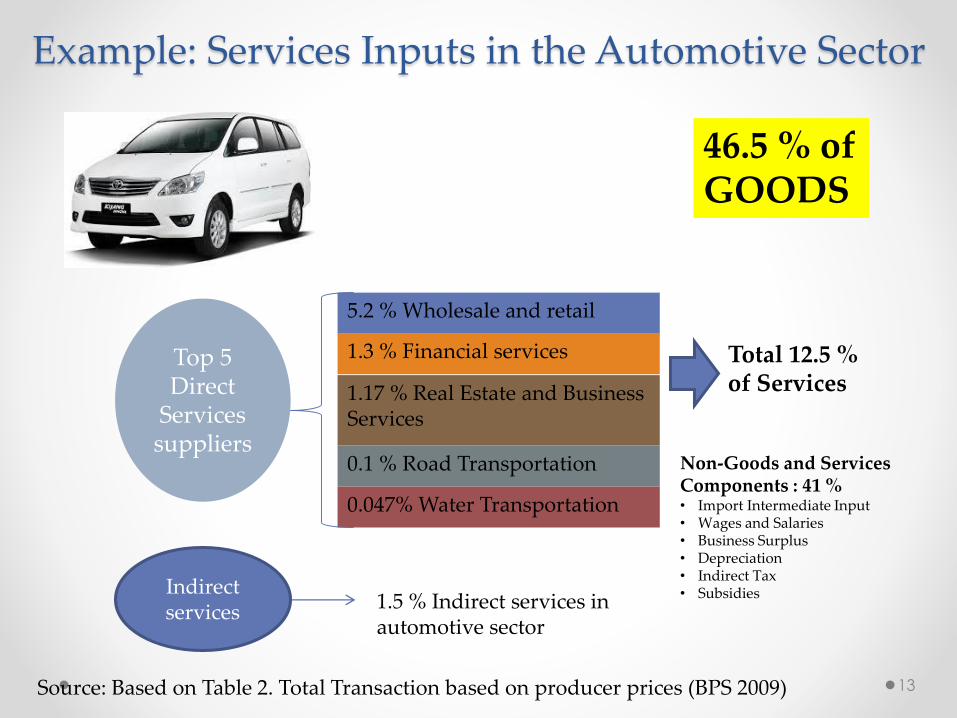

Example: Services Inputs in the Automotive Sector

Source: Based on Table 2. Total Transaction based on producer prices (BPS 2009)

46.5 % ofGOODS

Total 12.5 % of Services

Top 5 Direct

Services suppliers

Non-Goods and Services Components : 41 %• Import Intermediate Input• Wages and Salaries• Business Surplus• Depreciation• Indirect Tax• SubsidiesIndirect

services 1.5 % Indirect services in automotive sector

1.3 % Financial services

5.2 % Wholesale and retail

1.17 % Real Estate and Business Services

0.1 % Road Transportation

0.047% Water Transportation

13

How does Indonesia’s Use of Services Compare with Global Practices

Indonesia’s shares of

services for automotive

sector is only 12.5 %

Share of services in the automotive sector in the global industry is 3 times higher than that in Indonesia

14

Indonesia’s negotiations on trade in services and

commitments made so far

Section III

15

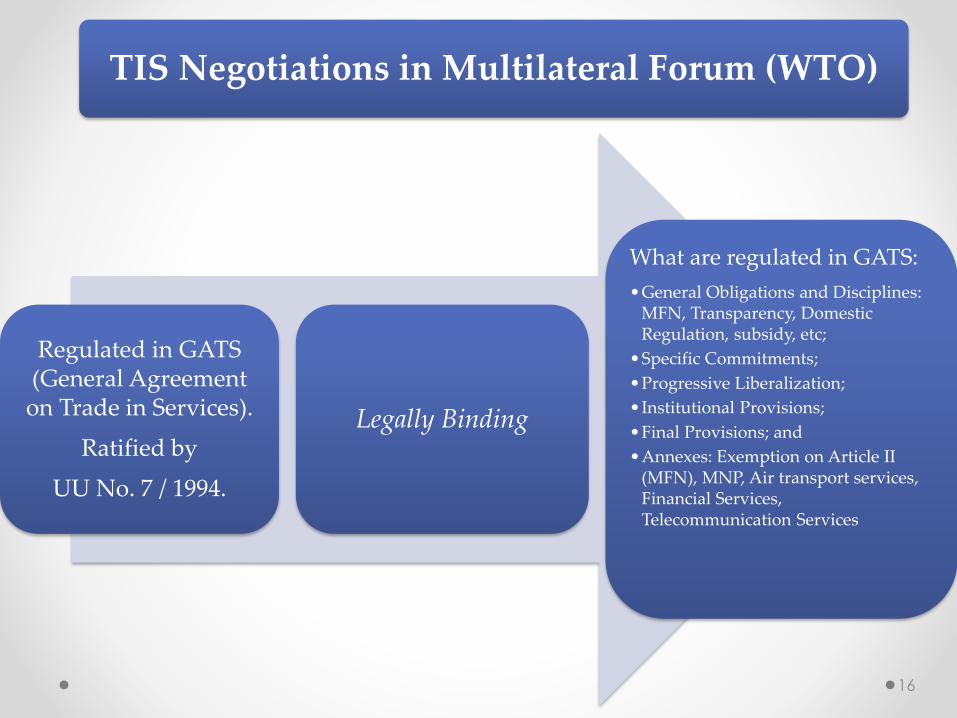

TIS Negotiations in Multilateral Forum (WTO)

Regulated in GATS (General Agreement on Trade in Services).

Ratified by

UU No. 7 / 1994.

Legally Binding

What are regulated in GATS:

•General Obligations and Disciplines: MFN, Transparency, Domestic Regulation, subsidy, etc;

•Specific Commitments;

•Progressive Liberalization;

•Institutional Provisions;

•Final Provisions; and

•Annexes: Exemption on Article II (MFN), MNP, Air transport services, Financial Services, Telecommunication Services

16

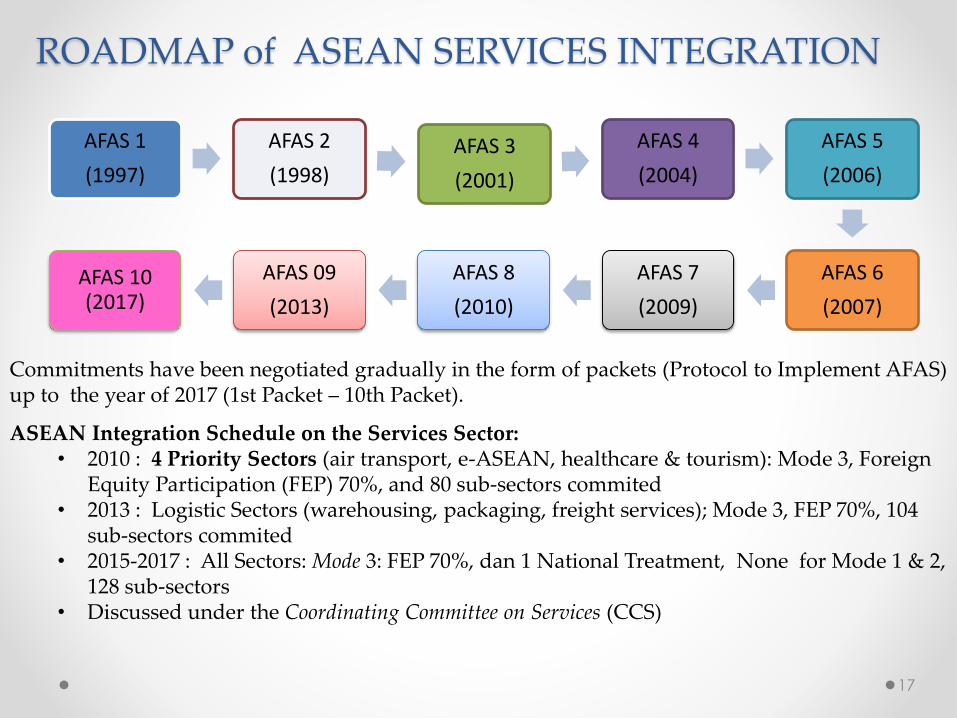

ROADMAP of ASEAN SERVICES INTEGRATION

AFAS 1

(1997)

AFAS 2

(1998)

AFAS 3

(2001)

AFAS 4

(2004)

AFAS 5

(2006)

AFAS 6

(2007)

AFAS 7

(2009)

AFAS 8

(2010)

AFAS 09

(2013)

AFAS 10 (2017)

Commitments have been negotiated gradually in the form of packets (Protocol to Implement AFAS) up to the year of 2017 (1st Packet – 10th Packet).

ASEAN Integration Schedule on the Services Sector:• 2010 : 4 Priority Sectors (air transport, e-ASEAN, healthcare & tourism): Mode 3, Foreign

Equity Participation (FEP) 70%, and 80 sub-sectors commited• 2013 : Logistic Sectors (warehousing, packaging, freight services); Mode 3, FEP 70%, 104

sub-sectors commited• 2015-2017 : All Sectors: Mode 3: FEP 70%, dan 1 National Treatment, None for Mode 1 & 2,

128 sub-sectors • Discussed under the Coordinating Committee on Services (CCS)

17

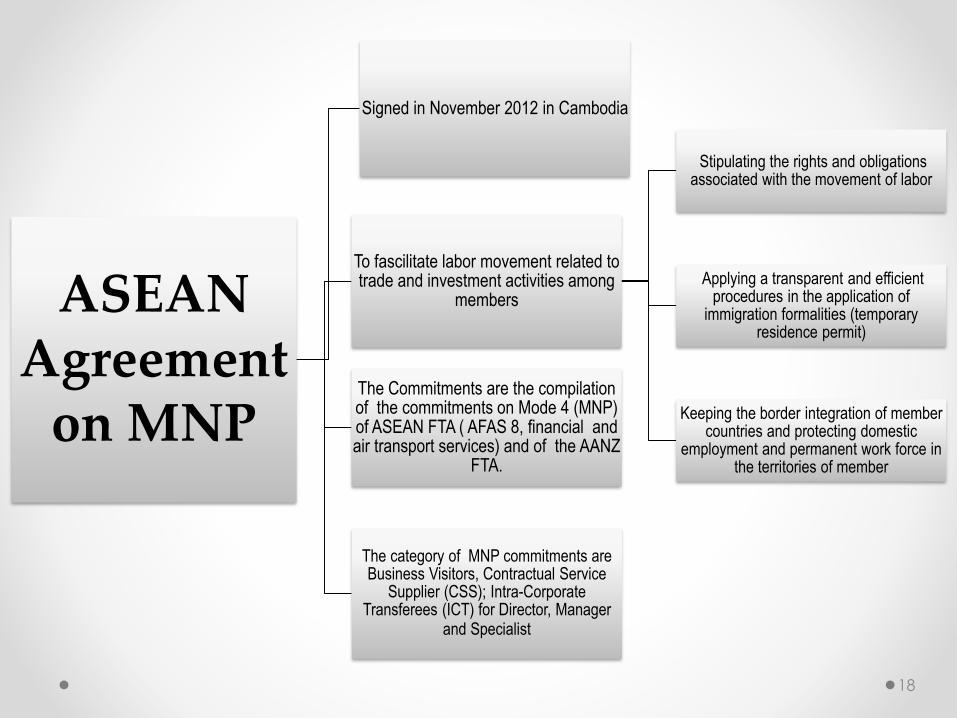

ASEAN Agreement

on MNP

Signed in November 2012 in Cambodia

To fascilitate labor movement related to trade and investment activities among

members

Stipulating the rights and obligations associated with the movement of labor

Applying a transparent and efficient procedures in the application of

immigration formalities (temporary residence permit)

Keeping the border integration of member countries and protecting domestic

employment and permanent work force in the territories of member

The Commitments are the compilation of the commitments on Mode 4 (MNP) of ASEAN FTA ( AFAS 8, financial and air transport services) and of the AANZ

FTA.

The category of MNP commitments are Business Visitors, Contractual Service

Supplier (CSS); Intra-Corporate Transferees (ICT) for Director, Manager

and Specialist

18

19

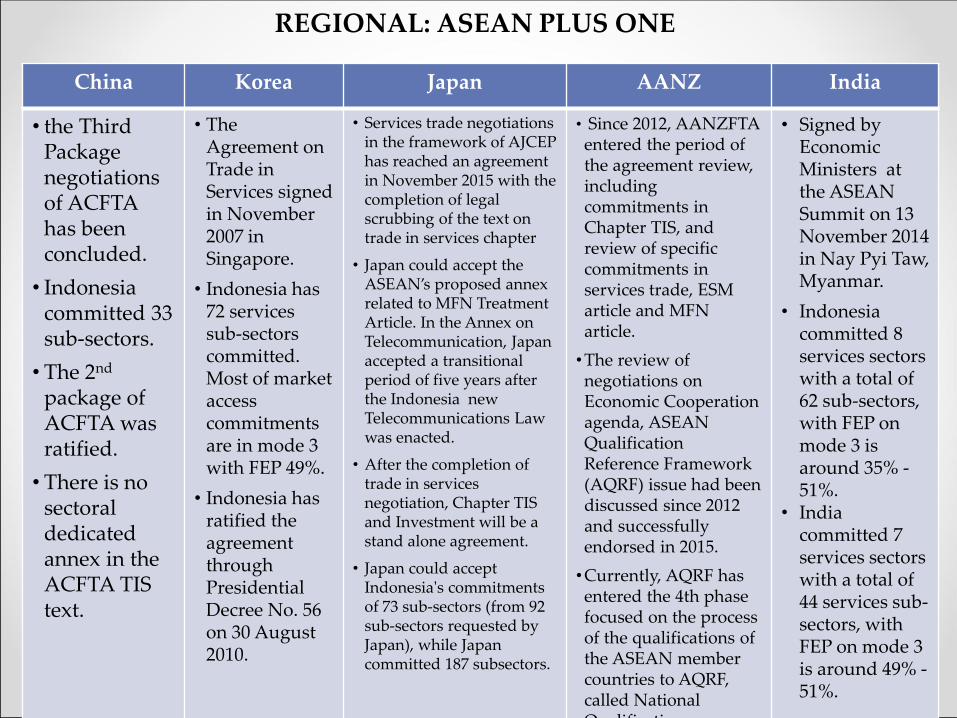

China Korea Japan AANZ India

• the Third Package negotiationsof ACFTA has been concluded.

• Indonesia committed 33 sub-sectors.

• The 2nd

package ofACFTA wasratified.

• There is no sectoral dedicated annex in the ACFTA TIS text.

• The Agreement on Trade in Services signed in November 2007 in Singapore.

• Indonesia has 72 services sub-sectorscommitted.Most of market access commitments are in mode 3 with FEP 49%.

• Indonesia has ratified the agreement through Presidential Decree No. 56 on 30 August 2010.

• Services trade negotiations in the framework of AJCEP has reached an agreement in November 2015 with the completion of legal scrubbing of the text on trade in services chapter

• Japan could accept the ASEAN’s proposed annex related to MFN TreatmentArticle. In the Annex on Telecommunication, Japan accepted a transitional period of five years after the Indonesia new Telecommunications Lawwas enacted.

• After the completion of trade in servicesnegotiation, Chapter TIS and Investment will be a stand alone agreement.

• Japan could accept Indonesia's commitments of 73 sub-sectors (from 92 sub-sectors requested by Japan), while Japan committed 187 subsectors.

• Since 2012, AANZFTA entered the period of the agreement review,including commitments inChapter TIS, and review of specific commitments in services trade, ESM article and MFNarticle.

•The review of negotiations on Economic Cooperation agenda, ASEAN Qualification Reference Framework (AQRF) issue had been discussed since 2012 and successfully endorsed in 2015.

•Currently, AQRF has entered the 4th phase focused on the process of the qualifications of the ASEAN member countries to AQRF, called National Qualification

• Signed by Economic Ministers at the ASEAN Summit on 13 November 2014 in Nay Pyi Taw, Myanmar.

• Indonesia committed 8 services sectorswith a total of 62 sub-sectors, with FEP on mode 3 isaround 35% -51%.

• India committed 7services sectorswith a total of 44 services sub-sectors, with FEP on mode 3 is around 49% -51%.

REGIONAL: ASEAN PLUS ONE

BILATERAL– INDONESIA-JAPAN EPA

Based on Article 151 on Indonesia-Japan Economic Partnership Agreement (IJEPA) regarding General Review (GR), IJEPA will be reviewed within five (5) years after entry into force (EIF) particularly to review the implementation of the Agreement (2008-2013).

The Japanese government has formally approved the review requested by Indonesia (July 2013) through a Diplomatic Note dated on 9 December 2013.

One of the objectives of this review is to re-evaluate the implementation and operation of the EPA including the possibility to increase the commitment of the EPA and the improvement of the text of the Agreement.

Through several preparatory meetings with related ministries in 2014, it was arranged that the position of Indonesia in GR for the services sector has not been directed to revise the text and commitments,bear in mind that IJEPA is the most opened agreement for Indonesia,hence the GR does not necessarily lead to progressive liberalization.

20

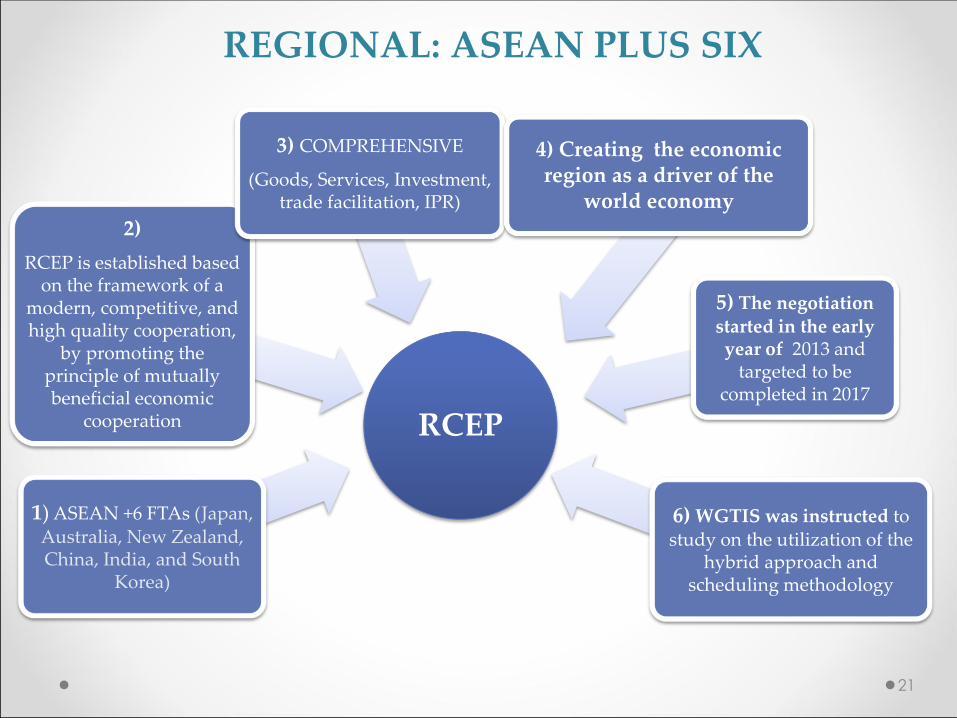

RCEP

1) ASEAN +6 FTAs (Japan, Australia, New Zealand, China, India, and South

Korea)

2)

RCEP is established based on the framework of a

modern, competitive, and high quality cooperation,

by promoting the principle of mutually beneficial economic

cooperation

3) COMPREHENSIVE

(Goods, Services, Investment, trade facilitation, IPR)

4) Creating the economic region as a driver of the

world economy

5) The negotiation started in the early year of 2013 and

targeted to be completed in 2017

6) WGTIS was instructed to study on the utilization of the

hybrid approach and scheduling methodology

REGIONAL: ASEAN PLUS SIX

21

Current status and key issues of Indonesia’s services

negotiations: the way forward

Section IV

22

Current Status: AFAS• In the AFAS negotiations, ASEAN member states are obliged to

fulfill threshold in finalizing each package of commitments. In

AFAS 10 negotiations, Indonesia is facing problems in fulfilling

the obligations.

• In priority integration sectors (PIS), where it is obliged to

committed 70% FEP, it is uneasy to convince respective

Ministries to make such commitments, although some sub

sectors/sectors are not regulated or openly regulated (high

level of FEP in DNI).

• AFAS will be replaced by ASEAN on Trade in Services

Agreement (ATISA), and at the time, it is being negotiated on

the draft text including the modality.23

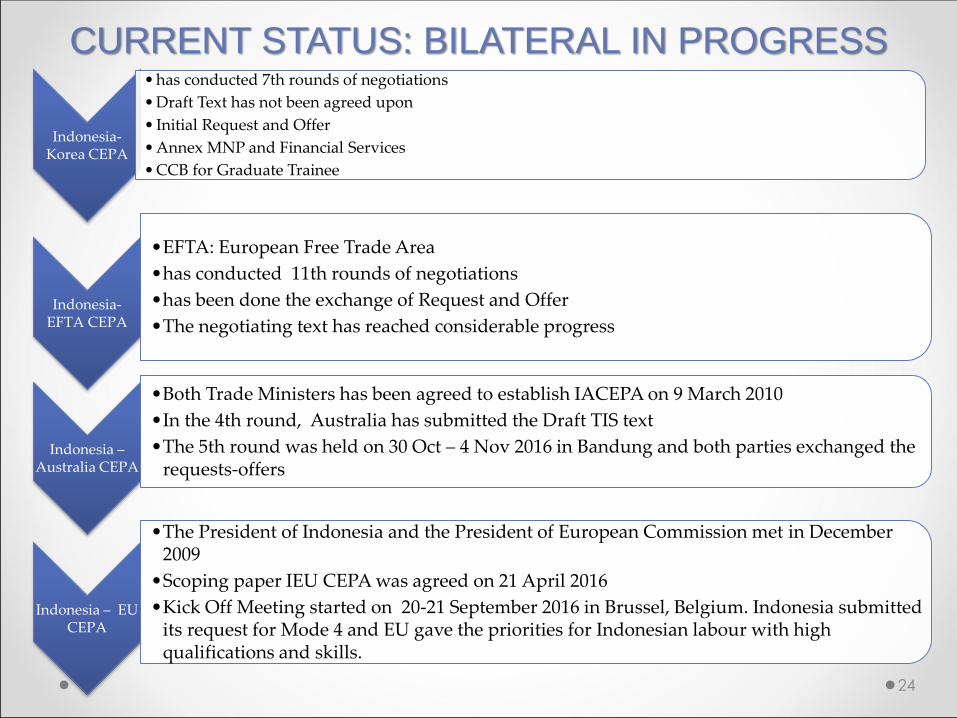

Indonesia-Korea CEPA

• has conducted 7th rounds of negotiations

• Draft Text has not been agreed upon

• Initial Request and Offer

• Annex MNP and Financial Services

• CCB for Graduate Trainee

Indonesia-EFTA CEPA

•EFTA: European Free Trade Area

•has conducted 11th rounds of negotiations

•has been done the exchange of Request and Offer

•The negotiating text has reached considerable progress

Indonesia –Australia CEPA

•Both Trade Ministers has been agreed to establish IACEPA on 9 March 2010

•In the 4th round, Australia has submitted the Draft TIS text

•The 5th round was held on 30 Oct – 4 Nov 2016 in Bandung and both parties exchanged therequests-offers

Indonesia – EU CEPA

•The President of Indonesia and the President of European Commission met in December 2009

•Scoping paper IEU CEPA was agreed on 21 April 2016

•Kick Off Meeting started on 20-21 September 2016 in Brussel, Belgium. Indonesia submitted its request for Mode 4 and EU gave the priorities for Indonesian labour with high qualifications and skills.

CURRENT STATUS: BILATERAL IN PROGRESS

24

Current Status: RCEP

• The negotiation process of trade in services is still ongoing and is targeted

for completion by 2017.

• RCEP is one of the most comprehensive negotiations with new provisions

in its trade in services text, such automatic MFN, Future Liberalization,

Transparency List as well as the possibility of a transition system of

scheduling commitments from the positive list to the negative list.

• In the context of market access, RCEP Parties are expected to commit to

about 100 subsectors. The parties are also expected to provide value

adds commitments in their subsectors. Value adds are ratchet,

transparency list, and the automatic granting MFN. Given the obligations

of the parties is to choose 2 of the 3 value adds, Indonesia chose ratchet

and create a transparency list.

25

Key Issues• Relationship between mode 3 (commercial presence and investment)

• Different regimes in liberalizing trade in services and investment

• Trade in services: positive list approach, Investment: negative list approach

• However, domestically, investment regime also applies to services sectors in committing

an autonomous liberalization (Perpres No. 44/2016, includes all sectors)

• The negative list approach is more on the perspective of inviting investors in establishing

companies while trade in services has a broader perspective yet having natural

persons/professionals in supplying services

• Indonesia has a defensive strategy in trade in services negotiations

• Negotiators are facing problems in determining country’s position that is mostly

influenced by unwillingness of line Ministries in making commitments as well as requesting

for market access of services sectors.

• It is understood that common mindset about trade agreement (FTA) is that it will “threat”

domestic suppliers competitiveness as there will be participation of foreign suppliers in

domestic market.

• This condition results in a less level of commitments in international trade compared to

existing regulations (policy space/water)

• Many countries argue that policy space reflects an uncertainty and unpredictable

conditions for services suppliers/foreign investors in supplying services 26

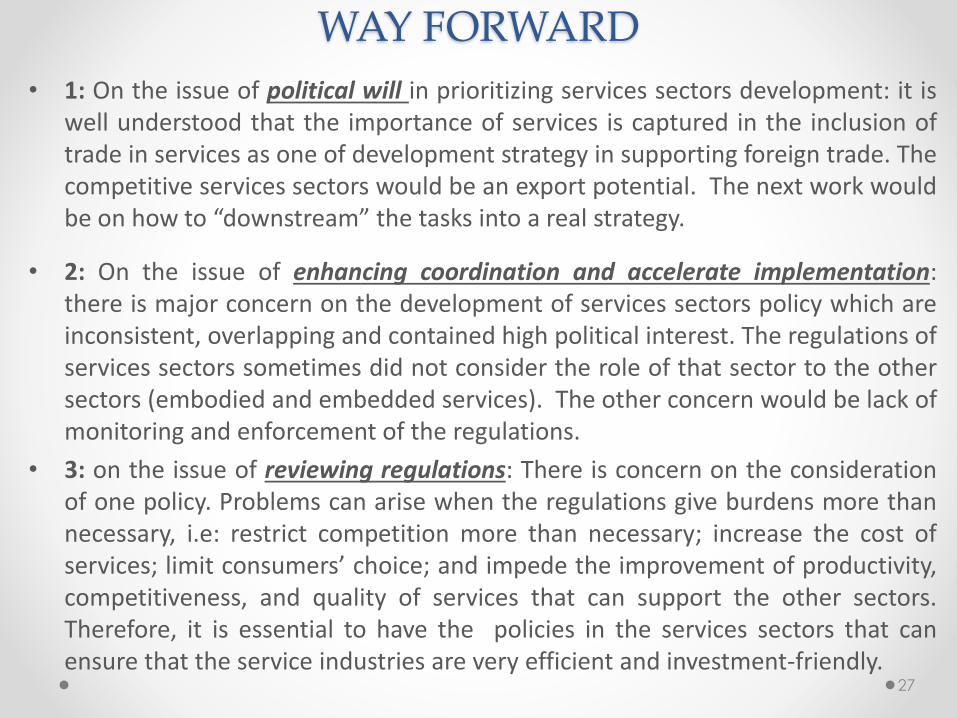

WAY FORWARD

• 1: On the issue of political will in prioritizing services sectors development: it iswell understood that the importance of services is captured in the inclusion oftrade in services as one of development strategy in supporting foreign trade. Thecompetitive services sectors would be an export potential. The next work wouldbe on how to “downstream” the tasks into a real strategy.

• 2: On the issue of enhancing coordination and accelerate implementation:there is major concern on the development of services sectors policy which areinconsistent, overlapping and contained high political interest. The regulations ofservices sectors sometimes did not consider the role of that sector to the othersectors (embodied and embedded services). The other concern would be lack ofmonitoring and enforcement of the regulations.

• 3: on the issue of reviewing regulations: There is concern on the considerationof one policy. Problems can arise when the regulations give burdens more thannecessary, i.e: restrict competition more than necessary; increase the cost ofservices; limit consumers’ choice; and impede the improvement of productivity,competitiveness, and quality of services that can support the other sectors.Therefore, it is essential to have the policies in the services sectors that canensure that the service industries are very efficient and investment-friendly.

27

Indonesia’s participation in trade in services

negotiations: opportunities and challenges

Section V

28

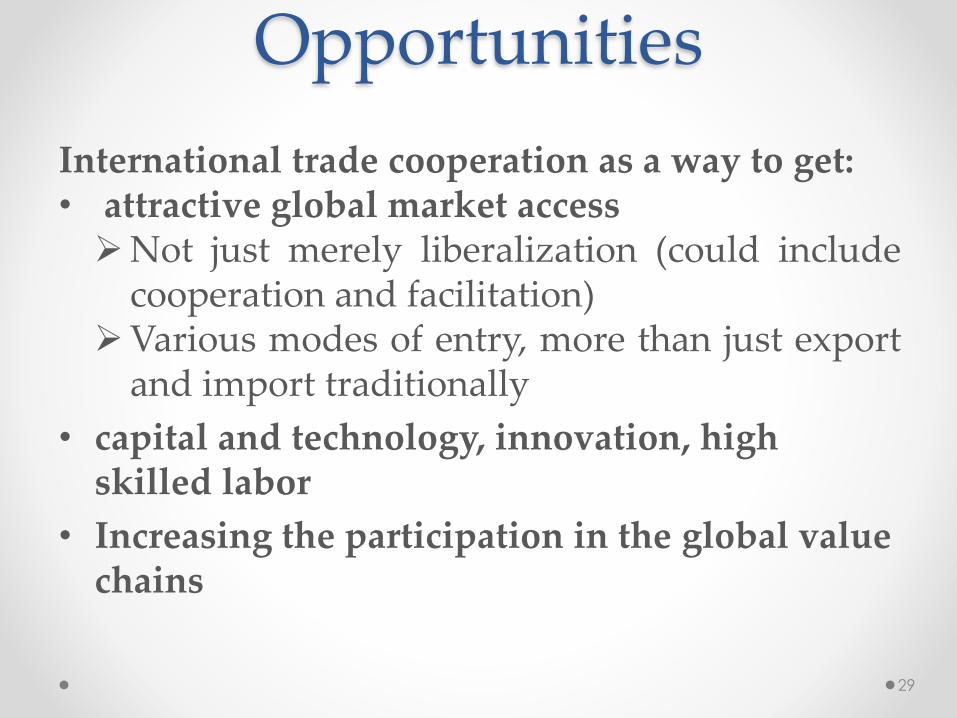

Opportunities

International trade cooperation as a way to get:• attractive global market accessNot just merely liberalization (could include

cooperation and facilitation)Various modes of entry, more than just export

and import traditionally

• capital and technology, innovation, high skilled labor

• Increasing the participation in the global value chains

29

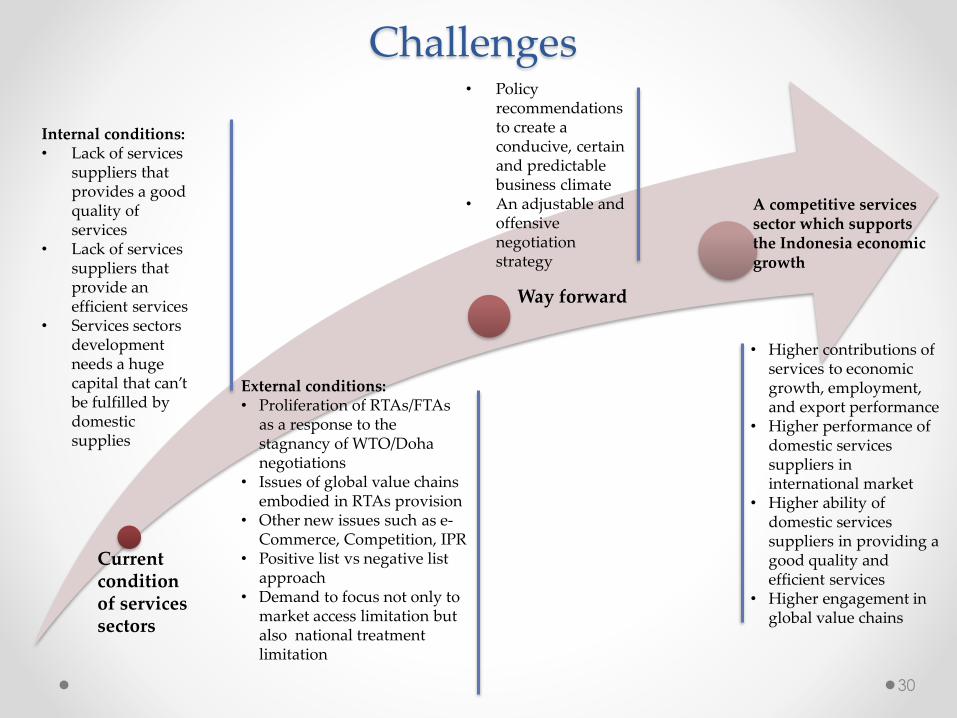

Challenges

Way forward

A competitive services sector which supports the Indonesia economic growth

Internal conditions:• Lack of services

suppliers that provides a good quality of services

• Lack of services suppliers that provide an efficient services

• Services sectors development needs a huge capital that can’t be fulfilled by domestic supplies

External conditions:• Proliferation of RTAs/FTAs

as a response to the stagnancy of WTO/Doha negotiations

• Issues of global value chains embodied in RTAs provision

• Other new issues such as e-Commerce, Competition, IPR

• Positive list vs negative list approach

• Demand to focus not only to market access limitation but also national treatment limitation

• Policy recommendations to create a conducive, certain and predictable business climate

• An adjustable and offensive negotiation strategy

• Higher contributions of services to economic growth, employment, and export performance

• Higher performance of domestic services suppliers in international market

• Higher ability of domestic services suppliers in providing a good quality and efficient services

• Higher engagement in global value chains

Current condition of services sectors

30

Conclusions• It is crucial to negotiate trade agreements actively with

important trade partners in order to have greater market access and to avoid trade diversionNote: Indonesia does not have many trade agreements, compared with other ASEAN Members

• In order to have free trade agreements with importanttrade partners (i.e. IEUCEPA, TPP, RCEP), Indonesia mustbe ready to enter ambitious and comprehensive tradeagreements

• The difficulties in building trade in services agreements,among others, are giving substansial commitments(no/limited waters), new approaches (positive vsnegative list), new features (separate chapters: financialservices, telecommunication services, temporary MNP;Services related disciplines found in separate chapters:investment, government procurement, etc.) 31

Thank You

32