Embed Size (px)

Citation preview

OVERSEAS DIRECT INVESTMENT

[email protected] 1 December 4, 2017

CA. Deepender Kumar DEEPENDER ANIL & ASSOCIATES (Chartered Accountants) Head Office: 101, E-36, Jawahar park, Laxmi Nagar, Delhi-110092 Branch Office: Plot-5A, IInd Floor, Sector-3A, Rachna, Vaishali, Ghaziabad (UP)- 201010 Mob No: 9910099584 [email protected] www.deepanilassociates.com

CONTENTS- • Overseas investments - references

• Meaning of ODI

• Points to be considered for ODI

• Routes of Investment through ODI

• Important Definitions

• Sectors in which ODIs are allowed with prior RBI approval

• General Permission

• Limit up to which Indian Party may make Financial Commitment(FC) in JV/WOS Methods of Funding Overseas Investments-

• Methods of Funding Overseas Investments

• Valuation of shares

• Reporting Requirement

• Obligations of the Indian party

• ODI- Related Matters

2

• ODI by Financial Sectors

• ODI By Indian Mutual Funds

• INVESTMENT THROUGH SPV • OVERSEAS DIRECT INVESTMENT AS FINANCIAL TOOL Hedging of Overseas Direct

Investments • Capitalisation of exports and other dues • Creation of charge on shares of JV / WOS / step down subsidiary (SDS) in

favour of domestic / overseas lender • Creation of charge on the domestic assets in favour of overseas lenders to

the JV / WOS / step down subsidiary • Creation of charge on overseas assets in favour of domestic lender • Post investment changes / additional investment in existing JV / WOS • Different modes of disinvestments from the JV / WOS abroad • Rollover of Guarantees • Foreign Currency Account by Indian Party- • Setting up office/ branch outside India • Routing of fund raised abroad to India • Other Points • Top Ten ODI Destination Countries • Sectorwise ODI

3

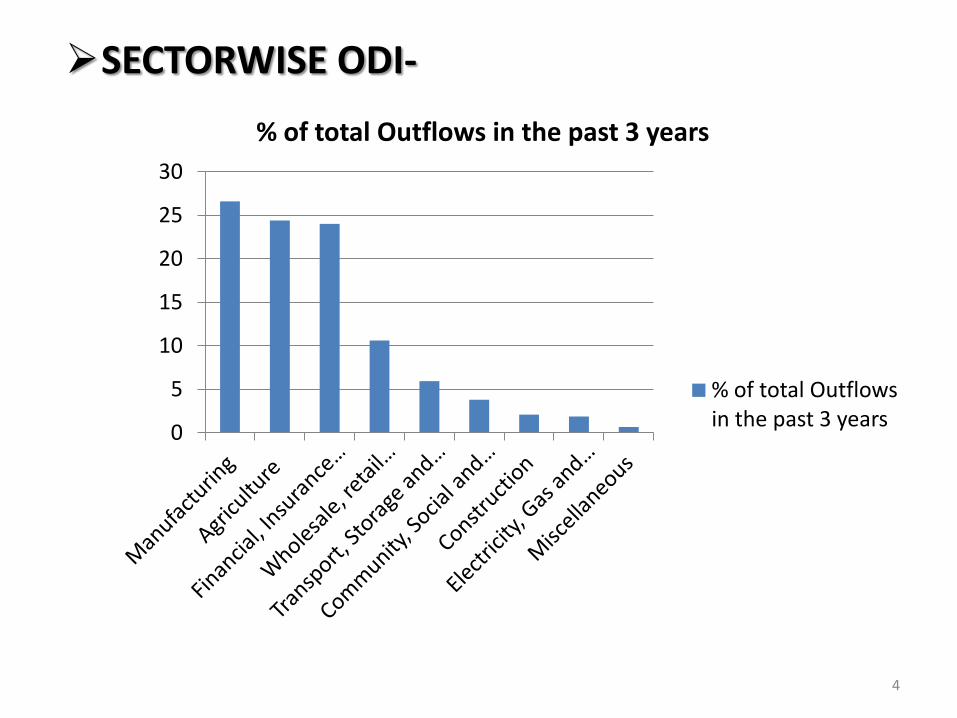

SECTORWISE ODI-

0

5

10

15

20

25

30

% of total Outflows in the past 3 years

% of total Outflows in the past 3 years

4

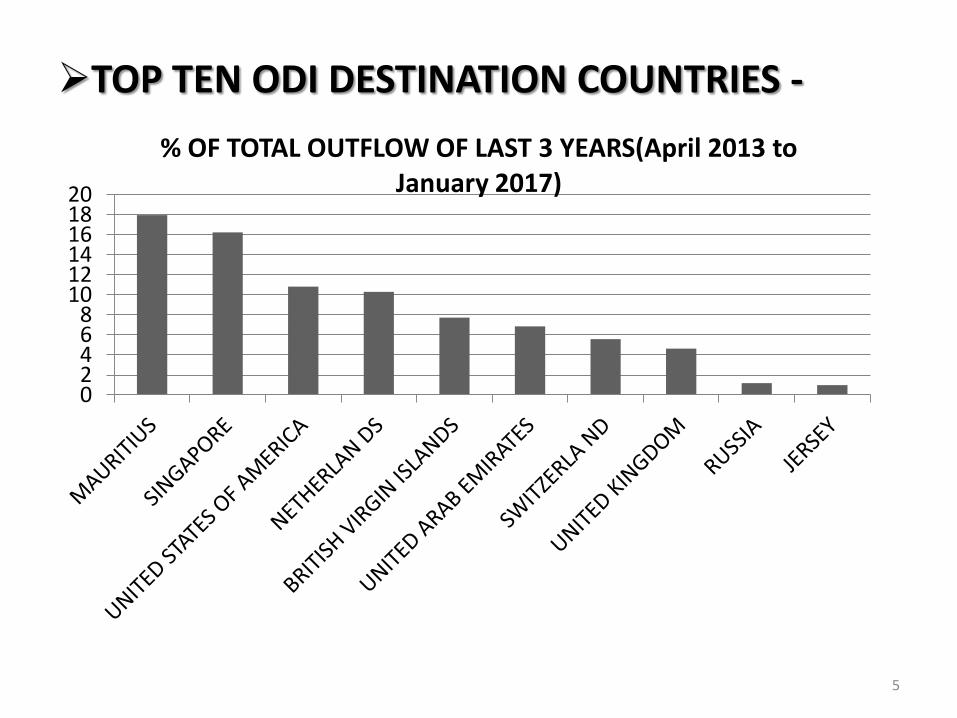

TOP TEN ODI DESTINATION COUNTRIES -

0 2 4 6 8

10 12 14 16 18 20

% OF TOTAL OUTFLOW OF LAST 3 YEARS(April 2013 to January 2017)

5

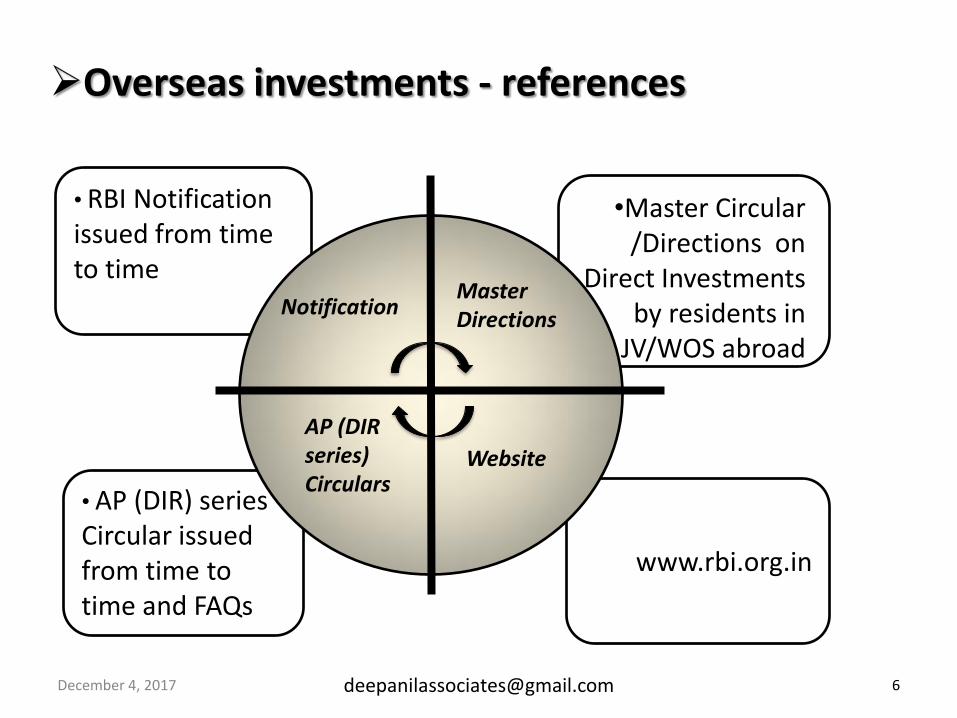

Overseas investments - references

• RBI Notification issued from time to time

www.rbi.org.in

•Master Circular /Directions on

Direct Investments by residents in

JV/WOS abroad

• AP (DIR) series Circular issued from time to time and FAQs

Notification Master Directions

AP (DIR series) Circulars

Website

[email protected] 6 December 4, 2017

Meaning of ODI-

Direct investment outside India means investments, either under the Automatic Route or the Approval Route, by way of contribution to the capital or subscription to the Memorandum of Association of a foreign entity, signifying a long-term interest in the overseas entity (setting up / acquiring a Joint Venture (JV) or a Wholly Owned Subsidiary (WOS).

[email protected] 7 December 4, 2017

Points to be considered for ODI-

• Investments can be made in new or existing entity.

• Indian entity can invest in any bonafide activity (except real estate other than development of township, construction of residential/ commercial premises, road or bridges). Also in case of financial

service sector, certain additional conditions to be fulfilled.

[email protected] 8 December 4, 2017

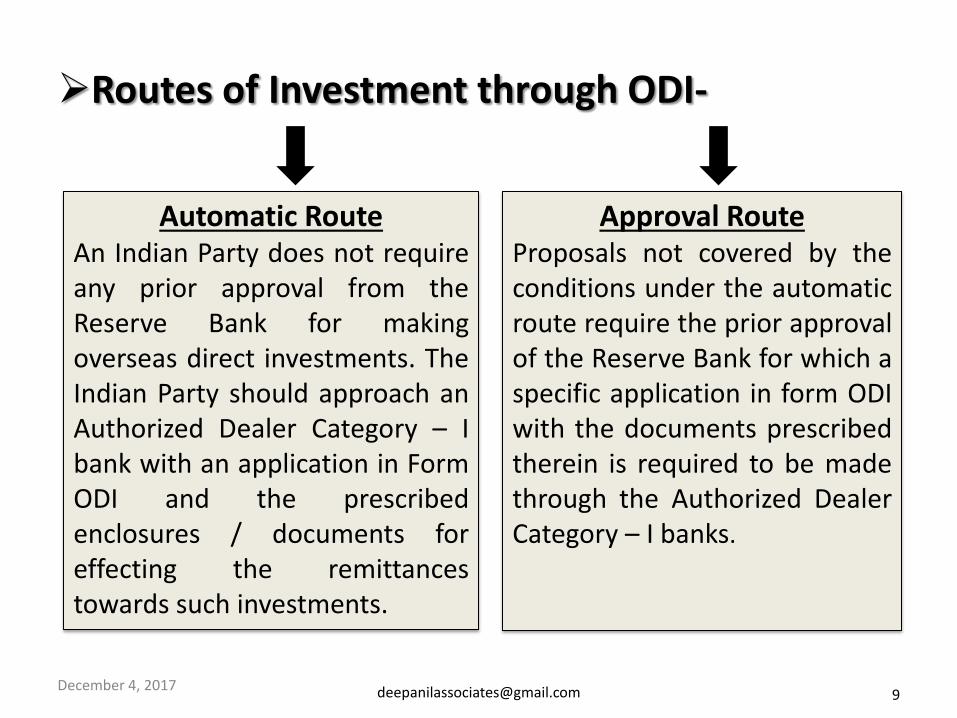

Routes of Investment through ODI-

Automatic Route An Indian Party does not require any prior approval from the Reserve Bank for making overseas direct investments. The Indian Party should approach an Authorized Dealer Category – I bank with an application in Form ODI and the prescribed enclosures / documents for effecting the remittances towards such investments.

Approval Route Proposals not covered by the conditions under the automatic route require the prior approval of the Reserve Bank for which a specific application in form ODI with the documents prescribed therein is required to be made through the Authorized Dealer Category – I banks.

9 December 4, 2017

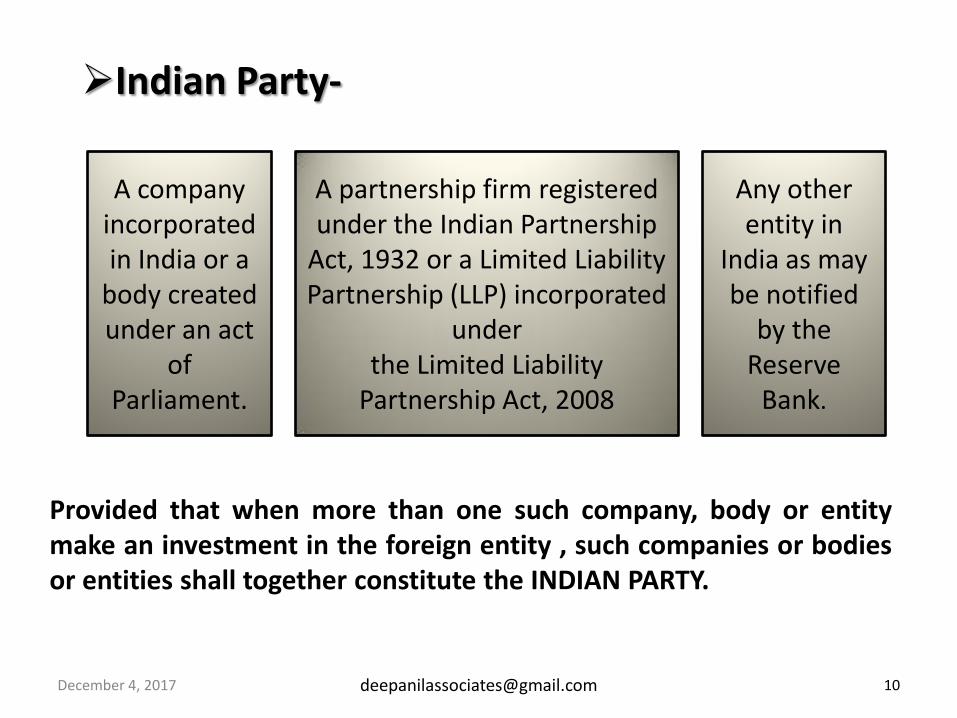

Indian Party-

Provided that when more than one such company, body or entity make an investment in the foreign entity , such companies or bodies or entities shall together constitute the INDIAN PARTY.

A company incorporated in India or a

body created under an act

of Parliament.

A partnership firm registered under the Indian Partnership

Act, 1932 or a Limited Liability Partnership (LLP) incorporated

under the Limited Liability

Partnership Act, 2008

Any other entity in

India as may be notified

by the Reserve

Bank.

December 4, 2017

• ‘Joint Venture ‘

Joint Venture (JV)' means a foreign entity formed, registered or incorporated in accordance with the laws and regulations of the host country in which the Indian party makes a direct investment.

• ‘Wholly Owned Subsidiary’

‘Wholly Owned Subsidiary (WOS)' means a foreign entity formed, registered or incorporated in accordance with the laws and regulations of the host country, whose entire capital is held by the Indian party.

[email protected] 11 December 4, 2017

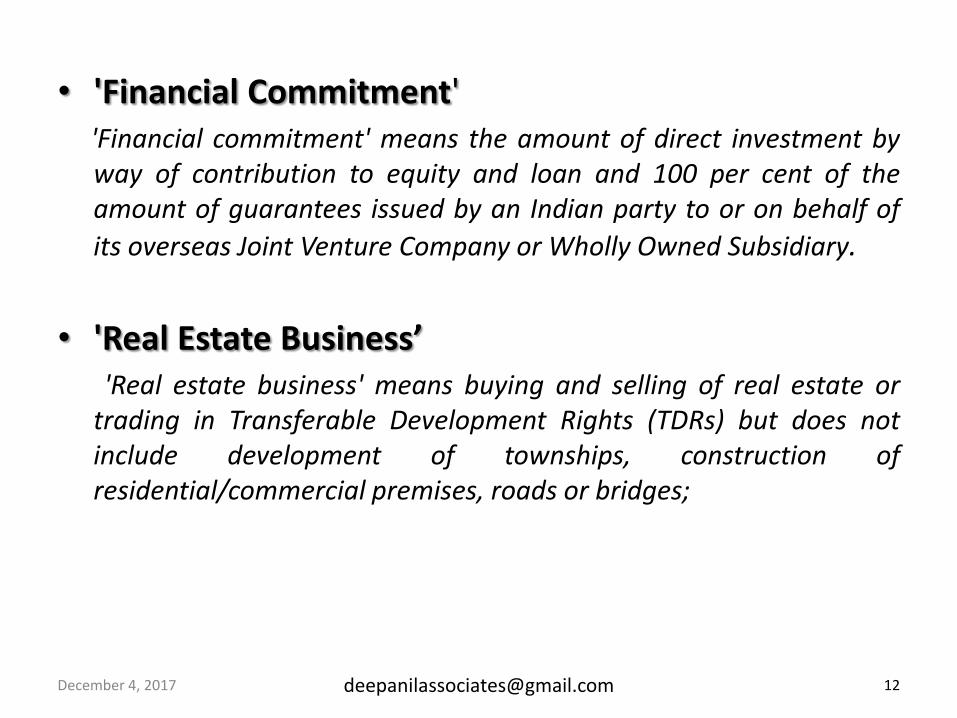

• 'Financial Commitment' 'Financial commitment' means the amount of direct investment by

way of contribution to equity and loan and 100 per cent of the amount of guarantees issued by an Indian party to or on behalf of

its overseas Joint Venture Company or Wholly Owned Subsidiary.

• 'Real Estate Business’ 'Real estate business' means buying and selling of real estate or

trading in Transferable Development Rights (TDRs) but does not include development of townships, construction of residential/commercial premises, roads or bridges;

[email protected] 12 December 4, 2017

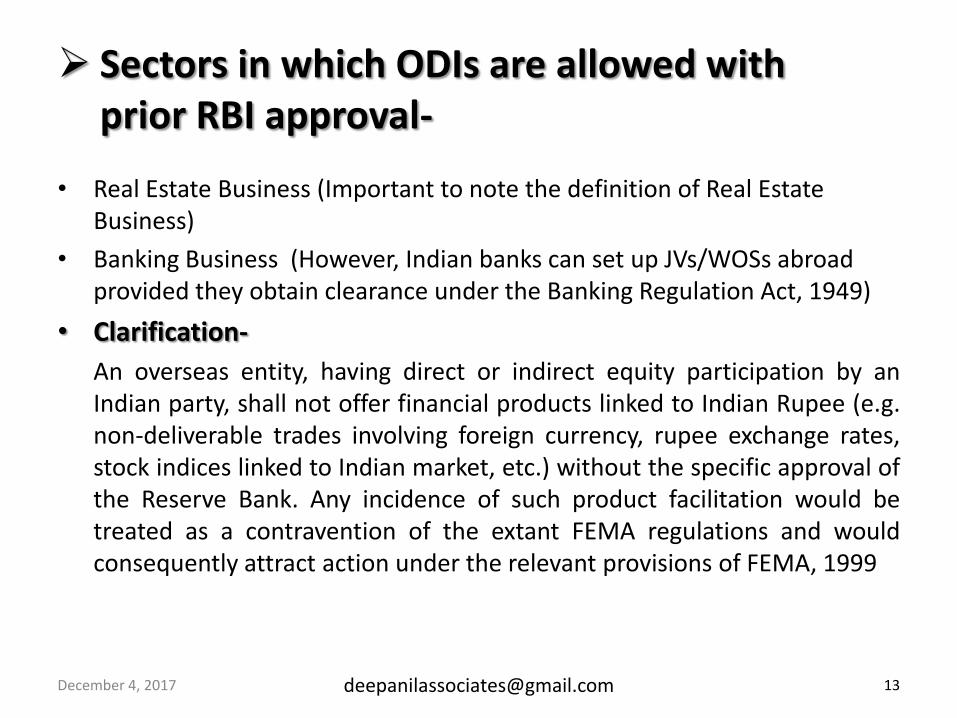

Sectors in which ODIs are allowed with prior RBI approval-

• Real Estate Business (Important to note the definition of Real Estate Business)

• Banking Business (However, Indian banks can set up JVs/WOSs abroad provided they obtain clearance under the Banking Regulation Act, 1949)

• Clarification-

An overseas entity, having direct or indirect equity participation by an Indian party, shall not offer financial products linked to Indian Rupee (e.g. non-deliverable trades involving foreign currency, rupee exchange rates, stock indices linked to Indian market, etc.) without the specific approval of the Reserve Bank. Any incidence of such product facilitation would be treated as a contravention of the extant FEMA regulations and would consequently attract action under the relevant provisions of FEMA, 1999

[email protected] 13 December 4, 2017

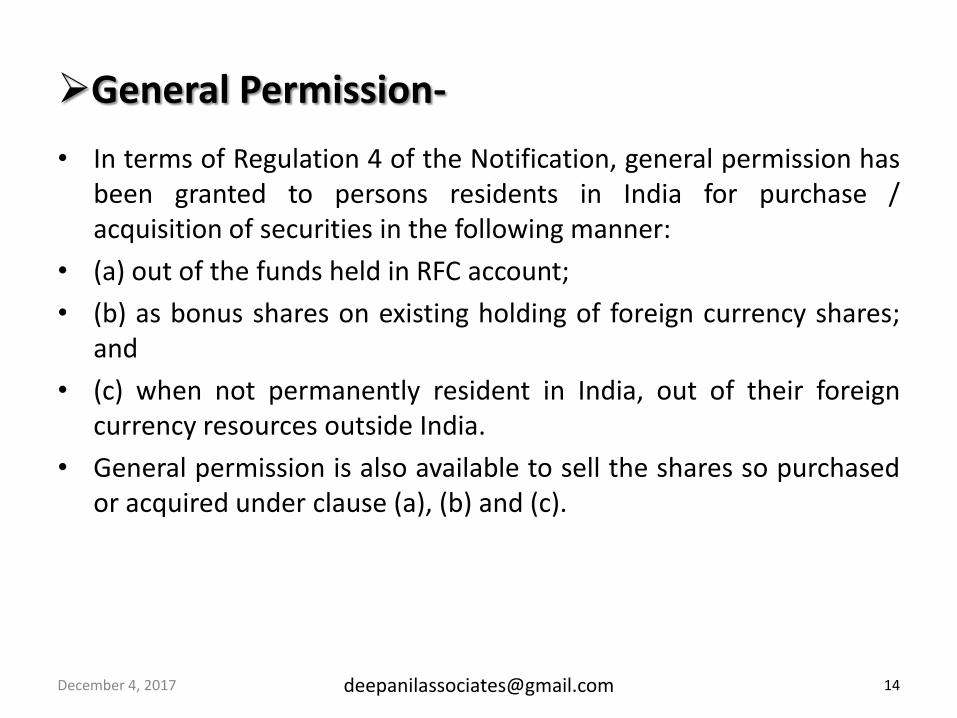

General Permission-

• In terms of Regulation 4 of the Notification, general permission has been granted to persons residents in India for purchase / acquisition of securities in the following manner:

• (a) out of the funds held in RFC account;

• (b) as bonus shares on existing holding of foreign currency shares; and

• (c) when not permanently resident in India, out of their foreign currency resources outside India.

• General permission is also available to sell the shares so purchased or acquired under clause (a), (b) and (c).

[email protected] 14 December 4, 2017

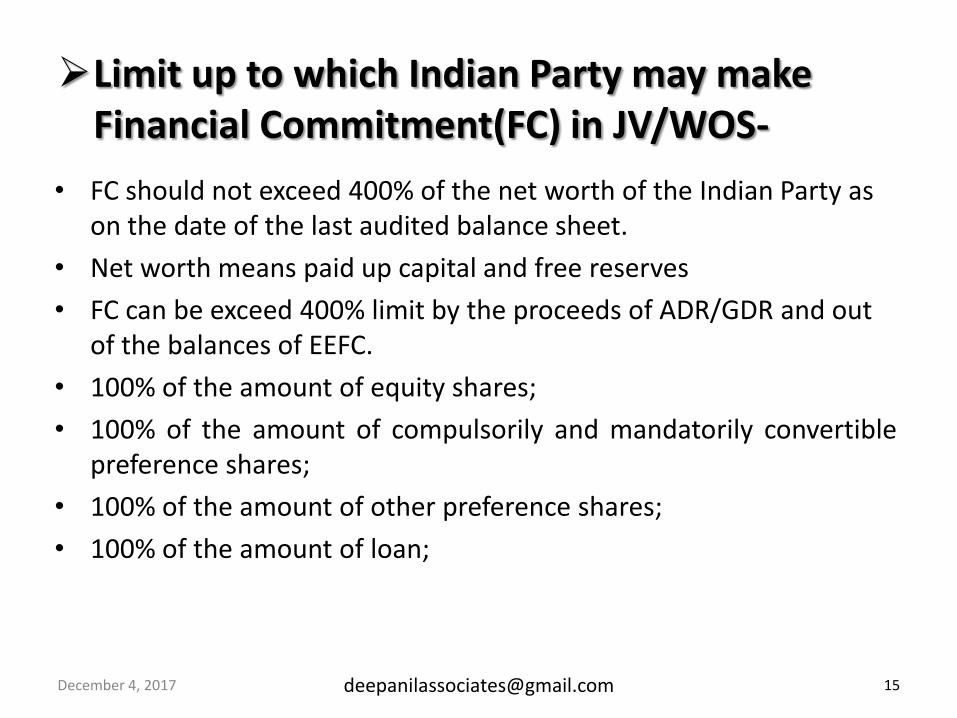

Limit up to which Indian Party may make Financial Commitment(FC) in JV/WOS- • FC should not exceed 400% of the net worth of the Indian Party as on the date of the last audited balance sheet.

• Net worth means paid up capital and free reserves

• FC can be exceed 400% limit by the proceeds of ADR/GDR and out of the balances of EEFC.

• 100% of the amount of equity shares;

• 100% of the amount of compulsorily and mandatorily convertible preference shares;

• 100% of the amount of other preference shares;

• 100% of the amount of loan;

[email protected] 15 December 4, 2017

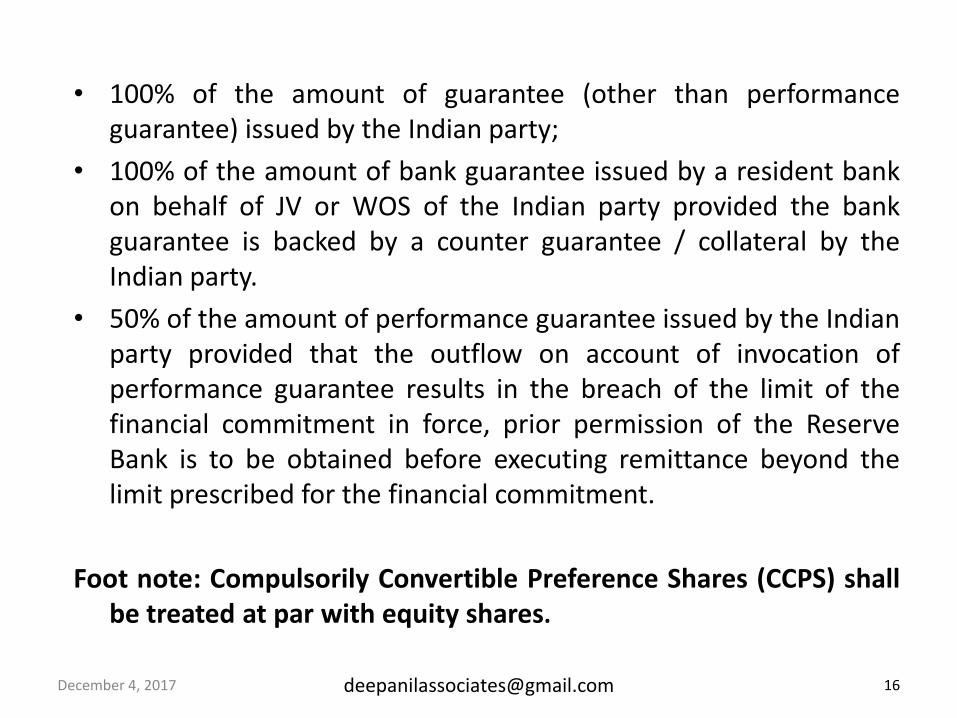

• 100% of the amount of guarantee (other than performance guarantee) issued by the Indian party;

• 100% of the amount of bank guarantee issued by a resident bank on behalf of JV or WOS of the Indian party provided the bank guarantee is backed by a counter guarantee / collateral by the Indian party.

• 50% of the amount of performance guarantee issued by the Indian party provided that the outflow on account of invocation of performance guarantee results in the breach of the limit of the financial commitment in force, prior permission of the Reserve Bank is to be obtained before executing remittance beyond the limit prescribed for the financial commitment.

Foot note: Compulsorily Convertible Preference Shares (CCPS) shall be treated at par with equity shares.

[email protected] 16 December 4, 2017

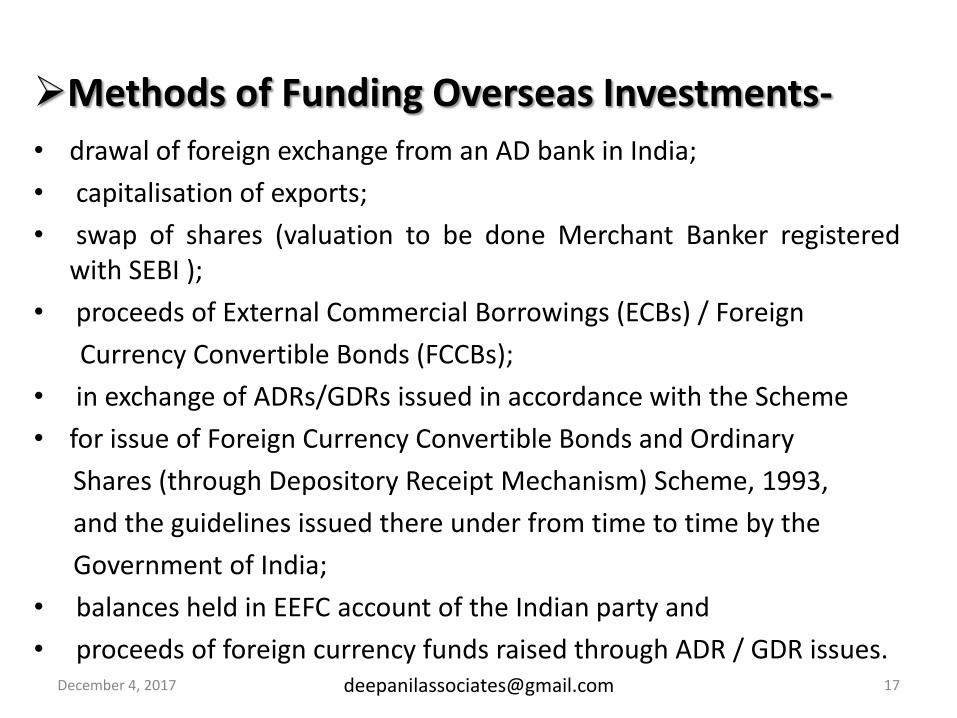

Methods of Funding Overseas Investments-

• drawal of foreign exchange from an AD bank in India;

• capitalisation of exports;

• swap of shares (valuation to be done Merchant Banker registered with SEBI );

• proceeds of External Commercial Borrowings (ECBs) / Foreign

Currency Convertible Bonds (FCCBs);

• in exchange of ADRs/GDRs issued in accordance with the Scheme

• for issue of Foreign Currency Convertible Bonds and Ordinary

Shares (through Depository Receipt Mechanism) Scheme, 1993,

and the guidelines issued there under from time to time by the

Government of India;

• balances held in EEFC account of the Indian party and

• proceeds of foreign currency funds raised through ADR / GDR issues. [email protected] 17 December 4, 2017

Other terms & Conditions-

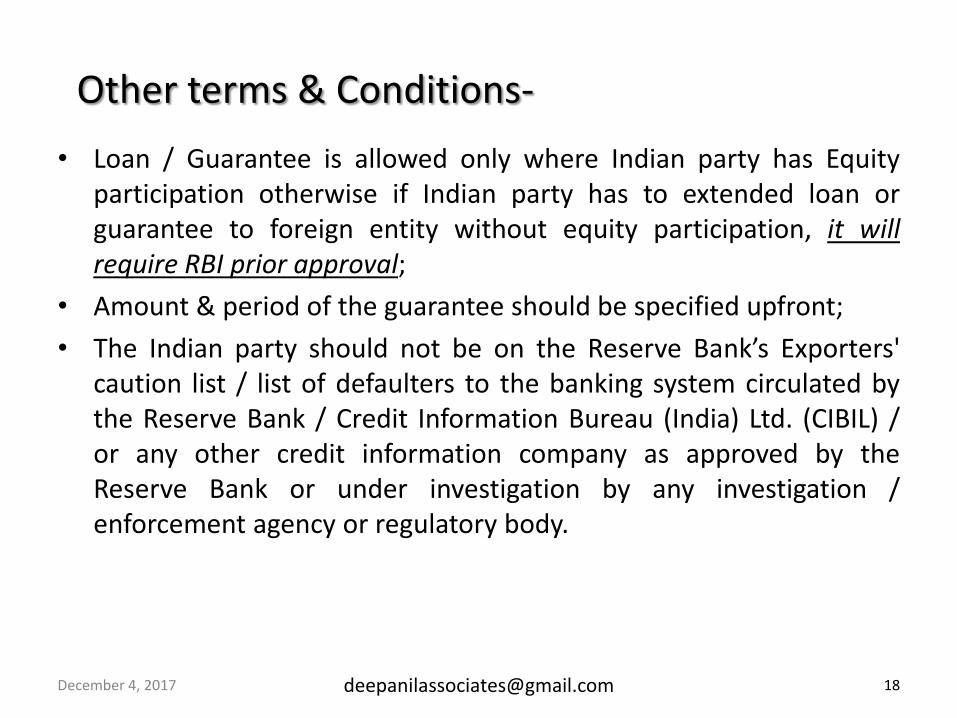

• Loan / Guarantee is allowed only where Indian party has Equity participation otherwise if Indian party has to extended loan or guarantee to foreign entity without equity participation, it will require RBI prior approval;

• Amount & period of the guarantee should be specified upfront;

• The Indian party should not be on the Reserve Bank’s Exporters' caution list / list of defaulters to the banking system circulated by the Reserve Bank / Credit Information Bureau (India) Ltd. (CIBIL) / or any other credit information company as approved by the Reserve Bank or under investigation by any investigation / enforcement agency or regulatory body.

[email protected] 18 December 4, 2017

Other Conditions….

• All transactions relating to a JV / WOS should be routed through one branch of an Authorised Dealer bank to be designated by the Indian party.

• In cases of investment by way of swap of shares, irrespective of the amount, valuation of the shares will have to be made by a Category I Merchant Banker registered with SEBI or an Investment Banker outside India registered with the appropriate regulatory authority in the host country. Approval of the Foreign Investment Promotion Board (FIPB) will also be a prerequisite for investment by swap of shares.

[email protected] 19 December 4, 2017

Valuation of shares-

• In case of partial / full acquisition of an existing foreign company, where the investment is more than USD 5 million, valuation of the shares of the company shall be made by a Category I Merchant Banker registered with SEBI or an Investment Banker / Merchant Banker outside India registered with the appropriate regulatory authority in the host country; and, in all other cases by a Chartered Accountant or a Certified Public Accountant.

[email protected] 20 December 4, 2017

Approval Route – Factors considered for Approval-

• Prima facie viability of the Joint Venture (JV)/ Wholly Owned Subsidiary (WOS) Outside India.

• Contribution to external trade and other benefits which will accrue to India through such investment.

• Financial position and business track record of the Indian party and the foreign entity.

• Expertise and experience of the Indian party in the same or related

line of activity of the JV/WOS outside India.

[email protected] 21 December 4, 2017

Indian Party’s Obligations-

•EVIDENCE: •Filling up of ODI Form to RBI, duly supported by certified board resolution, statutory auditors certificate and valuation report, through AD – I Bank •Receive share Certificate • Any other documents as an evidence of investment • Within six months of investments

• APR & FLA: •Submit Annual Performance Report of overseas entity to the Reserve Bank of India through AD Bank • Every year after annual accounts are prepared • 31ST December every year (based on audited annual accounts) •Submit annual return on Foreign Liabilities and foreign Assets •15th July every year (through mail)

DUES: •Repatriate to India all dues viz. dividends, royalty, technical fees, etc. • Within 60 days of falling due.

[email protected] 22 December 4, 2017

Conti….. APR-

An Indian party, which has set up / acquired a Joint Venture (JV) or Wholly Owned Subsidiary (WOS) overseas in terms of the Regulations of the Notification ibid, shall submit, to the designated Authorised Dealer every year, an Annual Performance Report (APR) in Form ODI Part II in respect of each JV or WOS outside India and other reports or documents as may be specified by the Reserve Bank from time to time, on or before the 31st of December each year. The APR, so required to be submitted, has to be based on the latest audited annual accounts of the JV / WOS, unless specifically exempted by the Reserve Bank. Where the law of the host country does not mandatorily require auditing of the books of accounts of JV / WOS, the : a. The Statutory Auditors of the Indian party certify that ‘The un-audited Annual Performance Report (APR) may be submitted by the Indian party based on the un-audited annual accounts of the JV / WOS provided annual accounts of the JV / WOS reflect the true and fair picture of the affairs of the JV / WOS’ and

December 4, 2017

Obligation on Indian Party Conti…..

b. That the un-audited annual accounts of the JV / WOS has been adopted and ratified by the Board of the Indian party. Reporting requirements including submission of Annual Performance Report are also applicable for investors in unincorporated entities in the oil sector. FLA: Indian companies which have made overseas direct investments, shall submit an Annual return on Foreign Liabilities and Assets in the format as Prescribed by RBI (available in RBI’s website (www.rbi.org.in → Forms category → FEMA Forms) which can be duly filled-in, validated and sent by e-mail, by July 15 every year.( Email id is :[email protected]) (Note: If an Resident Individual Making Investment under ODI route then he has to comply all requirement , as an Indian Party does)

December 4, 2017

Obligation on Indian Party Conti…..

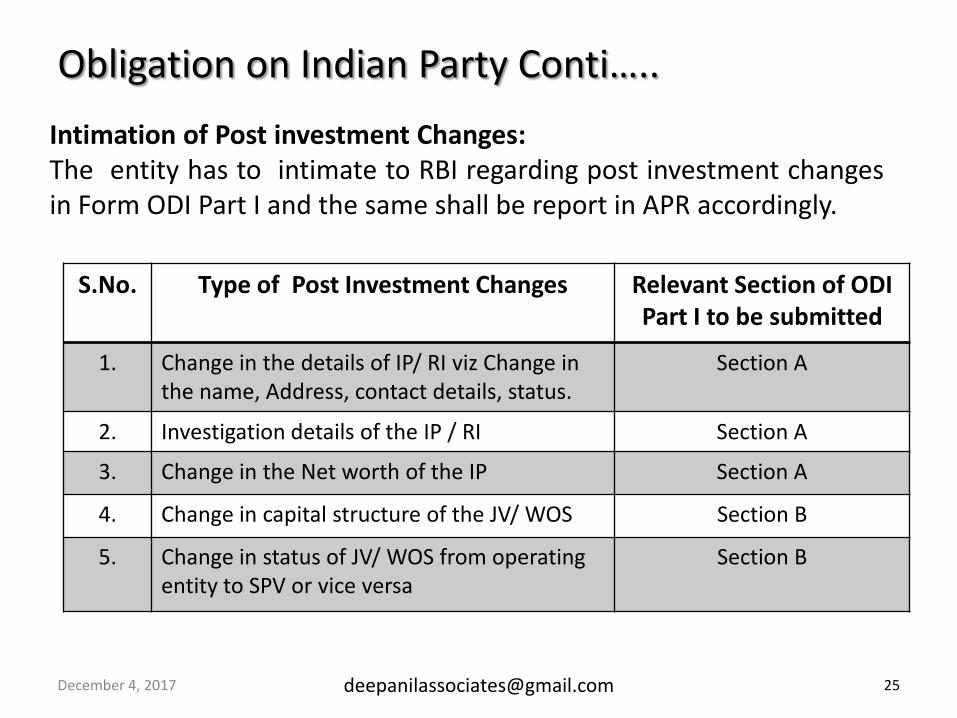

Intimation of Post investment Changes: The entity has to intimate to RBI regarding post investment changes in Form ODI Part I and the same shall be report in APR accordingly.

December 4, 2017

S.No. Type of Post Investment Changes Relevant Section of ODI Part I to be submitted

1. Change in the details of IP/ RI viz Change in the name, Address, contact details, status.

Section A

2. Investigation details of the IP / RI Section A

3. Change in the Net worth of the IP Section A

4. Change in capital structure of the JV/ WOS Section B

5. Change in status of JV/ WOS from operating entity to SPV or vice versa

Section B

Obligation on Indian Party Conti…..

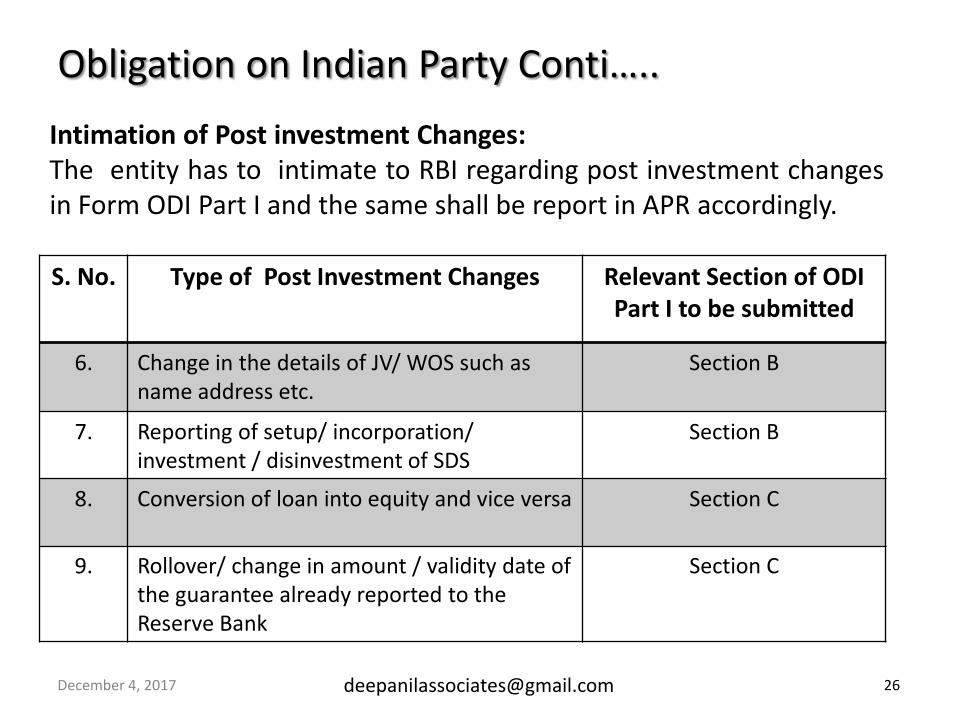

Intimation of Post investment Changes: The entity has to intimate to RBI regarding post investment changes in Form ODI Part I and the same shall be report in APR accordingly.

December 4, 2017

S. No. Type of Post Investment Changes Relevant Section of ODI Part I to be submitted

6. Change in the details of JV/ WOS such as name address etc.

Section B

7. Reporting of setup/ incorporation/ investment / disinvestment of SDS

Section B

8. Conversion of loan into equity and vice versa Section C

9. Rollover/ change in amount / validity date of the guarantee already reported to the Reserve Bank

Section C

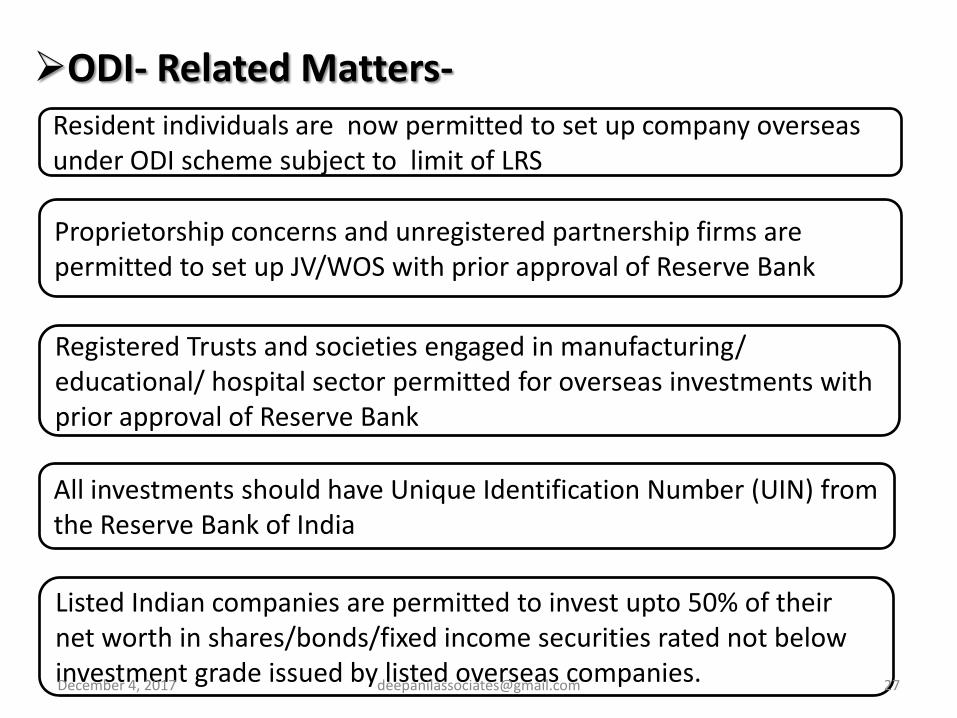

ODI- Related Matters- Resident individuals are now permitted to set up company overseas under ODI scheme subject to limit of LRS

Proprietorship concerns and unregistered partnership firms are permitted to set up JV/WOS with prior approval of Reserve Bank

Registered Trusts and societies engaged in manufacturing/ educational/ hospital sector permitted for overseas investments with prior approval of Reserve Bank

All investments should have Unique Identification Number (UIN) from the Reserve Bank of India

Listed Indian companies are permitted to invest upto 50% of their net worth in shares/bonds/fixed income securities rated not below investment grade issued by listed overseas companies.

27 [email protected] December 4, 2017

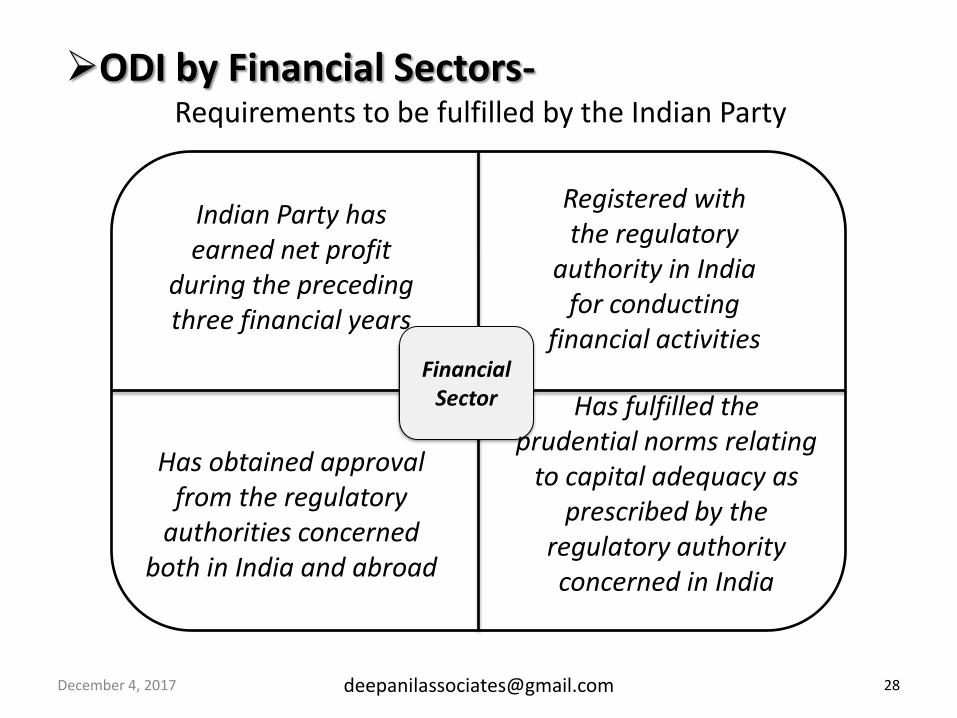

ODI by Financial Sectors- Requirements to be fulfilled by the Indian Party

Financial Sector

Indian Party has earned net profit

during the preceding three financial years

Registered with the regulatory

authority in India for conducting

financial activities

Has obtained approval from the regulatory

authorities concerned both in India and abroad

Has fulfilled the prudential norms relating

to capital adequacy as prescribed by the

regulatory authority concerned in India

[email protected] 28 December 4, 2017

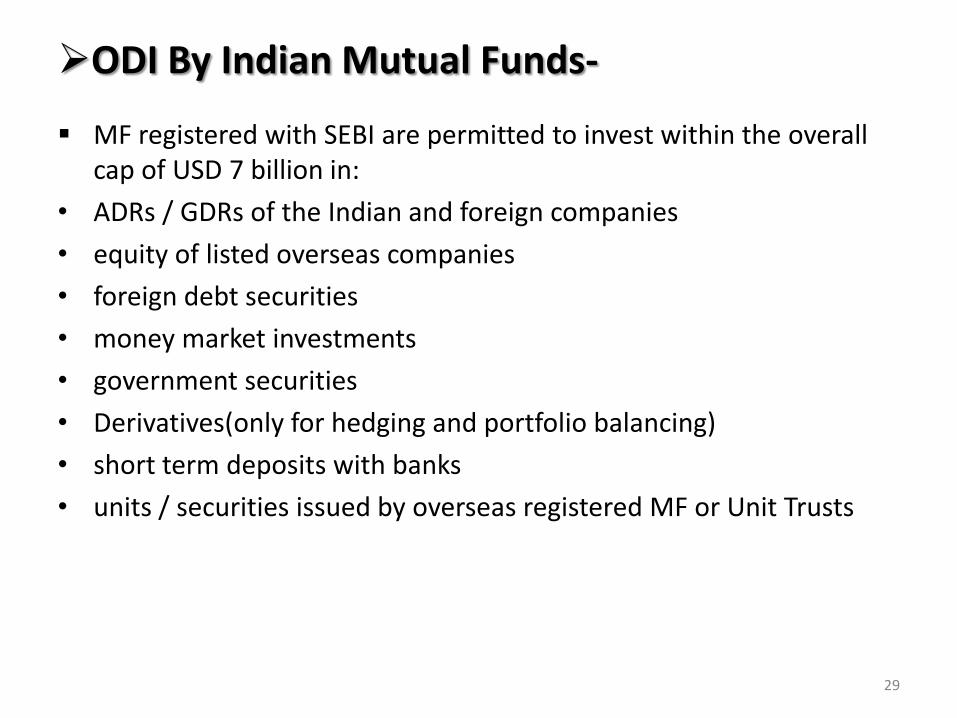

ODI By Indian Mutual Funds- MF registered with SEBI are permitted to invest within the overall

cap of USD 7 billion in:

• ADRs / GDRs of the Indian and foreign companies

• equity of listed overseas companies

• foreign debt securities

• money market investments

• government securities

• Derivatives(only for hedging and portfolio balancing)

• short term deposits with banks

• units / securities issued by overseas registered MF or Unit Trusts

29

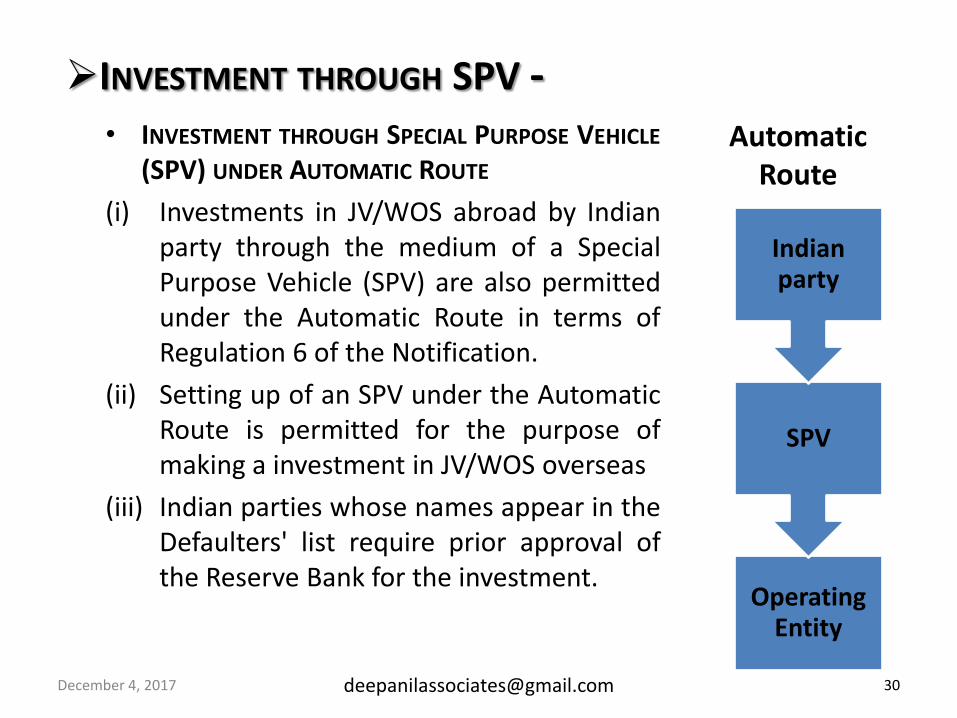

• INVESTMENT THROUGH SPECIAL PURPOSE VEHICLE (SPV) UNDER AUTOMATIC ROUTE

(i) Investments in JV/WOS abroad by Indian party through the medium of a Special Purpose Vehicle (SPV) are also permitted under the Automatic Route in terms of Regulation 6 of the Notification.

(ii) Setting up of an SPV under the Automatic Route is permitted for the purpose of making a investment in JV/WOS overseas

(iii) Indian parties whose names appear in the Defaulters' list require prior approval of the Reserve Bank for the investment.

Automatic Route

Operating Entity

SPV

Indian party

[email protected] 30 December 4, 2017

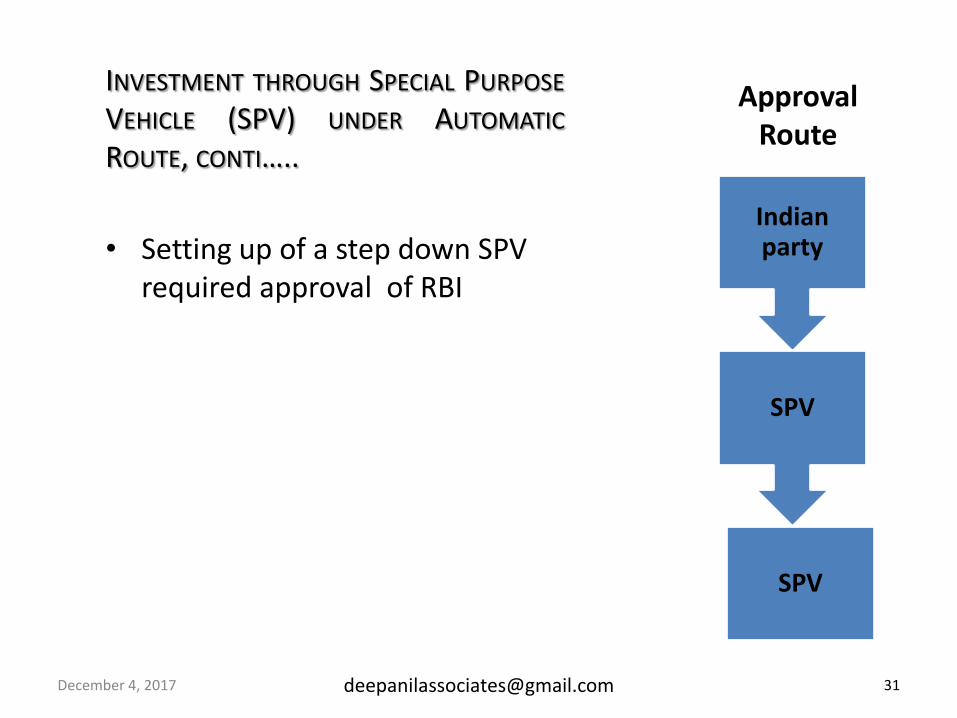

INVESTMENT THROUGH SPV -

INVESTMENT THROUGH SPECIAL PURPOSE VEHICLE (SPV) UNDER AUTOMATIC ROUTE, CONTI…..

• Setting up of a step down SPV required approval of RBI

Approval Route

[email protected] 31 December 4, 2017

Indian party

SPV

SPV

(a)Indian Parties are permitted to issue corporate guarantees on behalf of their first level step down operating JV /WOS set up by their JV / WOS operating as a Special Purpose Vehicle (SPV) under the Automatic Route, subject to the condition that the financial commitment of the Indian Party is within the extant limit for overseas direct investment. It has been decided that irrespective of whether the direct subsidiary is an operating company or a SPV, the Indian promoter entity may extend corporate guarantee on behalf of the first generation step down operating company under the Automatic Route, within the prevailing limit for overseas direct investment. Such guarantees will have to be reported to the Reserve Bank in Form ODI, as hitherto, through the designated AD Category – I bank concerned.

As in the case of corporate guarantees, all guarantees (including performance Guarantees and Bank Guarantees / SBLC) are required to be reported to the Reserve Bank, in Form ODI-Part II. Guarantees issued by banks in India in favour of WOSs / JVs outside India, and would be subject to prudential norms, issued by the Reserve Bank (DBOD) from time to time.

[email protected] 32 December 4, 2017

OVERSEAS DIRECT INVESTMENT AS FINANCIAL TOOL:

(b) Further, the issuance of corporate guarantee on behalf of second generation or subsequent level step down operating subsidiaries will be considered under the Approval Route, provided the Indian Party directly or indirectly holds 51 per cent or more stake in the overseas subsidiary for which such guarantee is intended to be issued.

• (Note :The Indian party / entity may extend loan / guarantee only to an overseas JV / WOS in which it has equity participation.)

• Proposals from the Indian party for undertaking financial commitment without equity contribution in JV / WOS may be considered by the Reserve Bank under the approval route.

OVERSEAS DIRECT INVESTMENT AS FINANCIAL TOOL CONTI......

[email protected] 33 December 4, 2017

Hedging of Overseas Direct Investments-

(1) Resident entities having overseas direct investments are permitted to hedge the foreign exchange rate risk arising out of such investments. AD Category - I banks may enter into forward / option contracts with resident entities who wish to hedge their overseas direct investments (in equity and loan), subject to verification of such exposure.

(2) If a hedge becomes naked in part or full owing to shrinking of the

market value of the overseas direct investment, the hedge may continue to the original maturity. Rollovers on the due date are permitted up to the extent of market value as on that date.

[email protected] 34 December 4, 2017

Capitalisation of exports and other dues- (1) Indian party is permitted to capitalise the payments due from the

foreign entity towards exports, fees, royalties or any other dues from the foreign entity for supply of technical know-how, consultancy, managerial and other services within the ceilings applicable. Capitalisation of export proceeds remaining unrealised beyond the prescribed period of realization will require prior approval of the Reserve Bank.

(2) Indian software exporters are permitted to receive 25 per cent of the value of their exports to an overseas software start-up company in the form of shares without entering into Joint Venture Agreements, with prior approval of the Reserve Bank.

[email protected] 35 December 4, 2017

Creation of charge on shares of JV / WOS / step down subsidiary (SDS) in favour of domestic / overseas lender-

• In terms of the extant FEMA provisions, creation of charge (pledge) on the shares of an JV / WOS of an Indian party in favour of domestic / overseas lender for the purpose of availing facilities (funded or non-funded) by the Indian party and / or the concerned JV / WOS is under the automatic route.

• It has been decided that the designated AD bank may permit creation of charge / pledge on the shares of the JV / WOS / SDS (irrespective of the level) of an Indian party in favour of a domestic or overseas lender for securing the funded and / or non-funded facility to be availed of by the Indian party or by its group companies / sister concerns / associate concerns or by any of its JV / WOS / SDS (irrespective of the level) under the automatic route subject to the following:

[email protected] 36 December 4, 2017

• The Indian party is complying with the provisions under Regulation 6 (and Regulation 7, if applicable) of the Notification ibid for undertaking financial commitment;

• Compliance to the provisions under Regulation 18 of the Notification ibid;

• The period of charge, if not specified upfront, may be co-terminus with the period of end use (like loan or other facility) for which charge has been created;

• The loan / facility availed by the JV / WOS / SDS from the domestic / overseas lender shall be utilized only for its core business activities overseas and not for investing back in India in any manner whatsoever;

• A certificate from the Statutory Auditors’ of the Indian party, to the effect that the loan / facility availed by the JV / WOS / SDS has not been utilized for direct or indirect investments in India, is to be obtained and kept by the designated AD;

[email protected] 37 December 4, 2017

• The invocation of charge resulting into the domestic lender acquiring the shares of the overseas JV / WOS / step down subsidiary shall be governed by the extant FEMA provisions / regulations issued by the Reserve Bank from time to time;

• The facilities (funded or non-funded) extended by the domestic lender to the Indian party or to its group / sister / associate concern or to any of its overseas JV / WOS / SDS shall also be governed by the prudential norms and other guidelines issued by the Department of Banking Regulation (DBR, the erstwhile DBOD), Reserve Bank of India from time to time; and

• The matter relating to the setting up / acquiring the multi-layered structure of overseas entities by the Indian party, wherever applicable, is under the examination of the Reserve Bank and the decision taken in this regard shall be conveyed in due course for necessary compliance at AD / Indian party level.

[email protected] 38 December 4, 2017

Creation of charge on the domestic assets in favour of overseas lenders to the JV / WOS / step down subsidiary-

• The designated AD bank may permit creation of charge (by way of pledge, hypothecation, mortgage, or otherwise) on the domestic assets of an Indian party (or its group companies / sister concerns / associate concerns including the individual promoters / directors) in favour of an overseas lender for securing the funded and / or non-funded facility to be availed of by the JV / WOS / SDS (irrespective of the level) of the Indian party under the automatic route subject to the following:

[email protected] 39 December 4, 2017

• The Indian party is complying with the provisions under Regulation 6 (and Regulation 7, if applicable) of the Notification ibid for undertaking the financial commitment;

• Compliance to the provisions under Regulation 18A(1) of the Notification FEMA /120 – RB dated 07/07/2004;

• The domestic assets, on which charge is being created, are not securitized;

• The period of charge, if not specified upfront, may be co-terminus with the period of end use (like loan or other facility) for which charge has been created;

• The loan / funds raised overseas by the JV / WOS / SDS shall be utilized only for its core business activities overseas and not for investing back in India in any manner whatsoever;

• A certificate from the Statutory Auditors’ of the Indian party, to the effect that the loan / funds raised overseas by the JV / WOS / SDS has not been utilized for direct or indirect investments in India, is to be obtained and kept by the designated AD;

[email protected] 40 December 4, 2017

• The overseas lender undertakes that, in the event of enforcement of charge, they shall transfer the domestic assets by way of sale to a resident only;

• In case of invocation of charge, the resultant remittance of the proceeds exceeding the prescribed limit of the financial commitment of the Indian party (prevailed at the time of creation of charge) shall require prior approval of the Reserve Bank;

• Wherever creation of charge involves pledge of shares of an Indian company, the pledge shall also be governed by the extant FEMA provisions / regulations issued by the Reserve Bank and the consolidated Foreign Direct Investment (FDI) policy issued by the Government of India from time to time; and

• The matter relating to the setting up / acquiring the multi-layered structure of overseas entities by the Indian party, wherever applicable, is under the examination of the Reserve Bank and the decision taken in this regard shall be conveyed in due course for necessary compliance at AD / Indian party level.

[email protected] 41 December 4, 2017

Creation of charge on overseas assets in favour of domestic lender-

• The designated AD bank may permit creation of charge (by way of hypothecation, mortgage, or otherwise) on the overseas assets (excluding the shares) of the JV / WOS / SDS (irrespective of the level) of an Indian party in favour of a domestic lender for securing the funded and / or non-funded facility to be availed of by the Indian party or by its group companies / sister concerns / associate concerns or by any of its overseas JV / WOS / SDS (irrespective of the level) under the automatic route subject to the following:

[email protected] 42 December 4, 2017

• The Indian party is complying with the provisions under Regulation 6 (and Regulation 7, if applicable) of the Notification ibid for undertaking financial commitment;

• Compliance to the provisions under Regulation 18A(2) of the Notification ibid;

• The overseas assets, on which charge is being created, are not securitized;

• The period of charge, if not specified upfront, may be co-terminus with the period of end use (like loan or other facility) for which charge has been created;

• The loan / facility availed by the JV / WOS / SDS from the domestic lender shall be utilized only for its core business activities overseas and not for investing back in India in any manner whatsoever;

[email protected] 43 December 4, 2017

• A certificate from the Statutory Auditors’ of the Indian party, to the effect that the loan / facility availed by the JV / WOS / SDS has not been utilized for direct or indirect investments in India, is to be obtained and kept by the designated AD;

• The invocation of charge resulting into the domestic lender acquiring the overseas assets shall require prior approval of the Reserve Bank; and

• The matter relating to the setting up / acquiring the multi-layered structure of overseas entities by the Indian party, wherever applicable, is under the examination of the Reserve Bank and the decision taken in this regard shall be conveyed in due course for necessary compliance at AD / Indian party level.

[email protected] 44 December 4, 2017

Post investment changes / additional investment in existing JV / WOS-

• A JV / WOS set up by the Indian Party as per the Regulations may diversify its activities / set up step down subsidiary / alter the shareholding pattern in the overseas entity (subject to compliance of Regulation 7 of the Notification ibid, in the case of financial services sector companies).

• The IP should report to the RBI through the AD Category - I bank, the details of such decisions within 30 days of the approval of those decisions by the competent authority of the JV / WOS concerned in terms of local laws of the host country and include the same in the Annual Performance Report (APR - Part II of Form ODI) required to be forwarded to the AD Category-I bank

45

Different modes of disinvestments from the JV / WOS abroad-

• Disinvestment by the Indian party from its JV / WOS abroad may be by way of transfer / sale of equity shares to a non-resident / resident or by way of liquidation / merger / amalgamation of the JV / WOS abroad.

[email protected] 46 December 4, 2017

Can an Indian Party disinvest in case where write off is not involved

• Yes. The Indian Party can disinvest in cases where write off is not involved without prior approval from Reserve Bank subject to the following:

• the sale is to be effected through a stock exchange where the shares of the overseas JV/ WOS are listed;

• if the shares are not listed on the stock exchange and the shares are disinvested by a private arrangement, the share price is not less than the value certified by a Chartered Accountant / Certified Public Accountant as the fair value of the shares based on the latest audited financial statements of the JV / WOS;

• the Indian Party does not have any outstanding dues by way of dividend, technical know-how fees, royalty, consultancy, commission or other entitlements and / or export proceeds from the JV or WOS;

[email protected] 47 December 4, 2017

• the overseas concern has been in operation for at least one full year and the Annual Performance Report together with the audited accounts for that year has been submitted to the Reserve Bank; and

• the Indian party is not under investigation by CBI / DoE/ SEBI / IRDA or any other regulatory authority in India.

[email protected] 48 December 4, 2017

In case of disinvestment of stake in overseas JV/WOS, can an Indian party disinvest with write off of part of

investment

• Indian Party may disinvest without prior approval of the Reserve Bank, in the under noted cases, where the amount repatriated on disinvestment is less than the amount of the original investment:

• i) in cases where the JV / WOS is listed in the overseas stock exchange;

• ii) in cases where the Indian Party is listed on a stock exchange in India and has a net worth of not less than Rs.100 crore;

• iii) where the Indian Party is an unlisted company and the investment in the overseas JV / WOS does not exceed USD 10 million and

• iv) where the Indian Party is a listed company with net worth of less than Rs.100 crore but investment in an overseas JV/WOS does not exceed USD 10 million.

[email protected] 49 December 4, 2017

Whether restructuring of the balance sheet of the JV / WOS abroad involving write-off of capital and

receivables is allowed

• Indian company which has set up WOS abroad or has at least 51% stake in an overseas JV may write off capital (equity / preference shares) or other receivables (such as loans, royalty, technical knowhow fees and management fees in respect of the JV /WOS) even while such JV / WOS continue to function subject to the following:

• (i) Listed Indian companies are permitted to write off capital and other receivables up to 25% of the equity investment in the JV /WOS under the Automatic Route; and

• (ii) Unlisted companies are permitted to write off capital and other receivables up to 25% of the equity investment in the JV /WOS with prior approval of the Reserve Bank.

[email protected] 50 December 4, 2017

• The write-off / restructuring have to be reported to the Reserve Bank through the designated AD bank within 30 days of write-off / restructuring. The write-off / restructuring is subject to the condition that the Indian Party should submit the following documents for scrutiny along with the applications to the designated AD Category – I bank under the Automatic as well as the Approval Routes:

• a) A certified copy of the balance sheet showing the loss in the overseas WOS/JV set up by the Indian Party; and

• b) Projections for the next five years indicating benefit accruing to the Indian company consequent to such write off / restructuring.

[email protected] 51 December 4, 2017

Rollover of Guarantees-

W.E.F. 3rd January 2014, vide A.P DIR CIRCULAR NO- 83

• It has been decided not to treat / reckon the renewal / rollover of an existing / original guarantee, which is part of the total financial commitment of the Indian party in terms of Regulation 6 of the Notification 120/RB dated 07/07/2004, as a fresh financial commitment, provided that :

• the existing / original guarantee was issued in terms of the then extant / prevailing FEMA guidelines.

• there is no change in the end use of the guarantee, i.e. the facilities availed by the JV / WOS / Step Down Subsidiary;

• there is no change in any of the terms & conditions, including the amount of the guarantee except the validity period;

• the reporting of the rolled over guarantee would be done as a fresh financial commitment in Part II of Form ODI, as hitherto; and

[email protected] 52 December 4, 2017

Cont……

• if the Indian party is under investigation by any investigation / enforcement agency or regulatory body, the concerned agency / body shall be kept informed about the same.

(In case, however, the above conditions are not met, the Indian party shall obtain prior approval of the Reserve Bank for rollover / renewal of the existing guarantee through the designated AD bank.)

[email protected] 53 December 4, 2017

Foreign Currency Account by Indian Party-

• Opening of Foreign Currency Account abroad by an Indian party Wherever, the host country Regulations stipulate that the investments into the country are required to be routed through a designated account, an Indian party is allowed to open, hold and maintain Foreign Currency Account (FCA) abroad for the purpose of overseas direct investments subject to certain terms and conditions stipulated under A.P. (DIR Series) Circular No. 101 dated April 02,

2012.

[email protected] 54 December 4, 2017

Setting up office/ branch outside India-

(i) At the time of setting up of the office, AD Category – I banks may allow remittances towards initial expenses up to fifteen per cent of the average annual sales/income or turnover during the last two financial years or up to twenty-five per cent of the net worth, whichever is higher.

(ii) For recurring expenses, remittances up to ten per cent of the average annual sales/income or turnover during the last two financial years may be sent for the purpose of normal business operations of the office (trading/non-trading)/branch or representative office outside India subject to the following terms and conditions:

a. The overseas branch/office has been set up or representative is posted overseas for conducting normal business activities of the Indian entity;

[email protected] 55 December 4, 2017

b. The overseas branch/office/representative shall not enter into any contract or agreement in contravention of the Act, Rules or Regulations made there under;

c. The overseas office (trading / non-trading) / branch / representative should not create any financial liabilities, contingent or otherwise, for the head office in India and also not invest surplus funds abroad without prior approval of the Reserve Bank. Any funds rendered surplus should be repatriated to India.

(iii) The details of bank accounts opened in the overseas country should be promptly reported to the AD Bank.

(iv) AD Category – I banks may also allow remittances by a company incorporated in India having overseas offices, within the above limits for initial and recurring expenses, to acquire immovable property outside India for its business and for residential purpose of its staff.

[email protected] 56 December 4, 2017

(v) The overseas office / branch of software exporter company/firm may repatriate to India 100 per cent of the contract value of each ‘off-site’ contract.

(vi) In case of companies taking up ‘on site’ contracts, they should repatriate the profits of such ‘on site’ contracts after the completion of the said contracts.

(vii) An audited yearly statement showing receipts under ‘off-site’ and ‘on-site’ contracts undertaken by the overseas office, expenses and repatriation thereon may be sent to the AD Category – I banks.

[email protected] 57 December 4, 2017

Routing of fund raised abroad to India-

• Section 8 of Foreign Exchange Management Act, 1999 read with regulation 3 of Foreign Exchange Management (Realisation, Repatriation and surrender of Foreign Exchange) Regulations, 2000

• Save as otherwise provided in this Act, where any amount of foreign exchange is due or has accrued to any person resident in India, such person shall take all reasonable steps to realise and repatriate to India such foreign exchange within such period and in such manner as may be specified by the Reserve Bank.

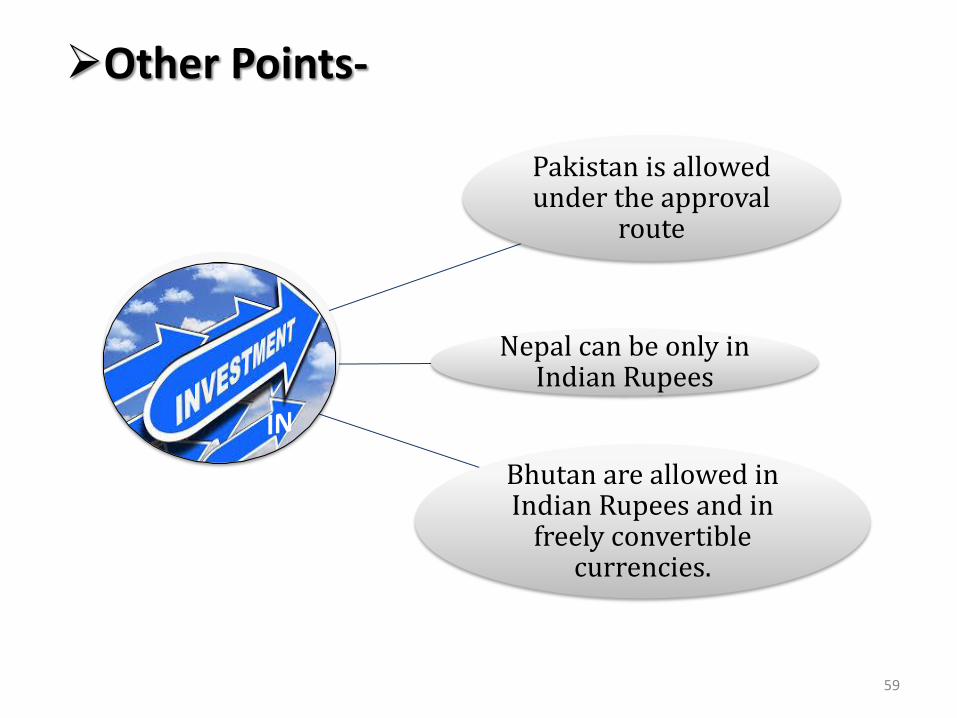

Other Points-

Pakistan is allowed under the approval

route

Nepal can be only in Indian Rupees

Bhutan are allowed in Indian Rupees and in

freely convertible currencies.

59

[email protected] 60 December 4, 2017