Embed Size (px)

Citation preview

1

RESEARCH

June 18, 2015

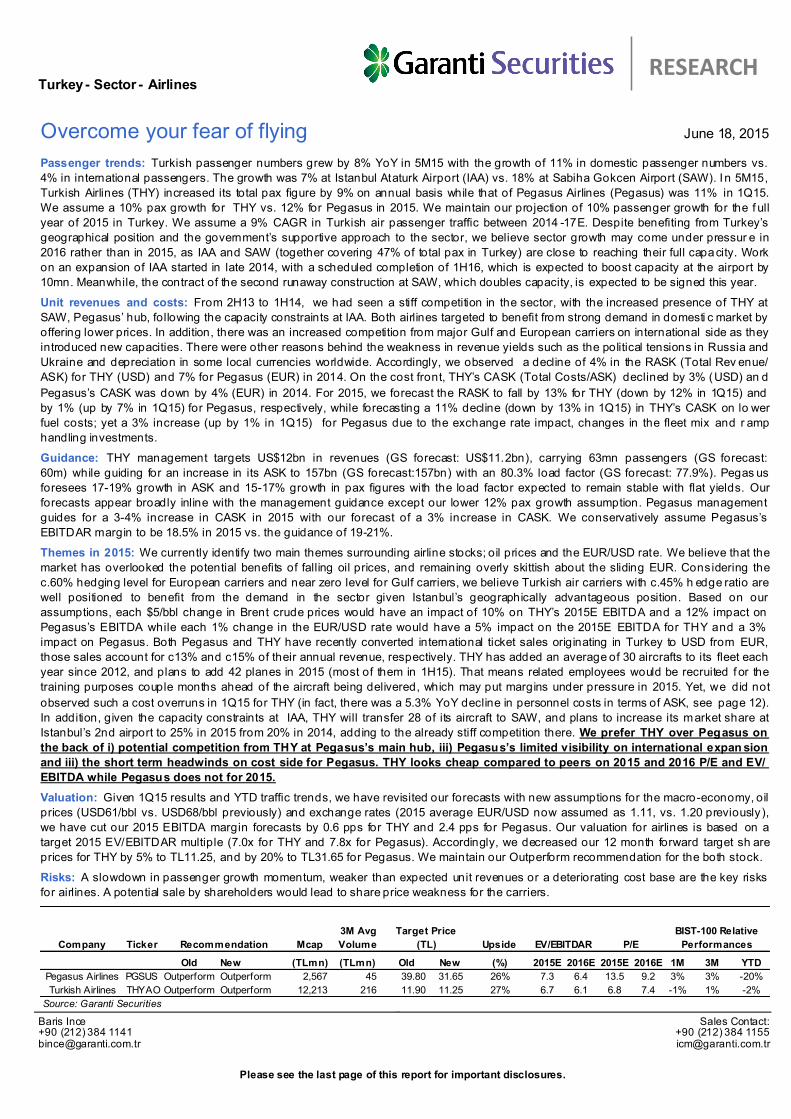

Overcome your fear of flying

Turkey - Sector - Airlines

Baris Ince +90 (212) 384 1141 [email protected]

Sales Contact: +90 (212) 384 1155 [email protected]

Please see the last page of this report for important disclosures.

Passenger trends: Turkish passenger numbers grew by 8% YoY in 5M15 with the growth of 11% in domestic passenger numbers vs.

4% in international passengers. The growth was 7% at Istanbul Ataturk Airport (IAA) vs. 18% at Sabiha Gokcen Airport (SAW). I n 5M15,

Turkish Airlines (THY) increased its total pax figure by 9% on annual basis while that of Pegasus Airlines (Pegasus) was 11% in 1Q15.

We assume a 10% pax growth for THY vs. 12% for Pegasus in 2015. We maintain our projection of 10% passenger growth for the f ull

year of 2015 in Turkey. We assume a 9% CAGR in Turkish air passenger traffic between 2014 -17E. Despite benefiting from Turkey’s

geographical position and the government’s supportive approach to the sector, we believe sector growth may come under pressur e in

2016 rather than in 2015, as IAA and SAW (together covering 47% of total pax in Turkey) are close to reaching their full capacity. Work

on an expansion of IAA started in late 2014, with a scheduled completion of 1H16, which is expected to boost capacity at the airport by

10mn. Meanwhile, the contract of the second runaway construction at SAW, which doubles capacity, is expected to be signed this year.

Unit revenues and costs: From 2H13 to 1H14, we had seen a stiff competition in the sector, with the increased presence of THY at

SAW, Pegasus’ hub, following the capacity constraints at IAA. Both airlines targeted to benefit from strong demand in domesti c market by

offering lower prices. In addition, there was an increased competition from major Gulf and European carriers on international side as they

introduced new capacities. There were other reasons behind the weakness in revenue yields such as the political tensions in Russia and

Ukraine and depreciation in some local currencies worldwide. Accordingly, we observed a decline of 4% in the RASK (Total Rev enue/

ASK) for THY (USD) and 7% for Pegasus (EUR) in 2014. On the cost front, THY’s CASK (Total Costs/ASK) declined by 3% (USD) an d

Pegasus’s CASK was down by 4% (EUR) in 2014. For 2015, we forecast the RASK to fall by 13% for THY (down by 12% in 1Q15) and

by 1% (up by 7% in 1Q15) for Pegasus, respectively, while forecasting a 11% decline (down by 13% in 1Q15) in THY’s CASK on lo wer

fuel costs; yet a 3% increase (up by 1% in 1Q15) for Pegasus due to the exchange rate impact, changes in the fleet mix and r amp

handling investments.

Guidance: THY management targets US$12bn in revenues (GS forecast: US$11.2bn), carrying 63mn passengers (GS forecast:

60m) while guiding for an increase in its ASK to 157bn (GS forecast:157bn) with an 80.3% load factor (GS forecast: 77.9%). Pegas us

foresees 17-19% growth in ASK and 15-17% growth in pax figures with the load factor expected to remain stable with flat yields. Our

forecasts appear broadly inline with the management guidance except our lower 12% pax growth assumption. Pegasus management

guides for a 3-4% increase in CASK in 2015 with our forecast of a 3% increase in CASK. We conservatively assume Pegasus’s

EBITDAR margin to be 18.5% in 2015 vs. the guidance of 19-21%.

Themes in 2015: We currently identify two main themes surrounding airline stocks; oil prices and the EUR/USD rate. We believe that the

market has overlooked the potential benefits of falling oil prices, and remaining overly skittish about the sliding EUR. Considering the

c.60% hedging level for European carriers and near zero level for Gulf carriers, we believe Turkish air carriers with c.45% h edge ratio are

well positioned to benefit from the demand in the sector given Istanbul’s geographically advantageous position. Based on our

assumptions, each $5/bbl change in Brent crude prices would have an impact of 10% on THY’s 2015E EBITDA and a 12% impact on

Pegasus’s EBITDA while each 1% change in the EUR/USD rate would have a 5% impact on the 2015E EBITDA for THY and a 3%

impact on Pegasus. Both Pegasus and THY have recently converted international ticket sales originating in Turkey to USD from EUR,

those sales account for c13% and c15% of their annual revenue, respectively. THY has added an average of 30 aircrafts to its fleet each

year since 2012, and plans to add 42 planes in 2015 (most of them in 1H15). That means related employees would be recruited f or the

training purposes couple months ahead of the aircraft being delivered, which may put margins under pressure in 2015. Yet, we did not

observed such a cost overruns in 1Q15 for THY (in fact, there was a 5.3% YoY decline in personnel costs in terms of ASK, see page 12).

In addition, given the capacity constraints at IAA, THY will transfer 28 of its aircraft to SAW, and plans to increase its market share at

Istanbul’s 2nd airport to 25% in 2015 from 20% in 2014, adding to the already stiff competition there. We prefer THY over Pegasus on

the back of i) potential competition from THY at Pegasus’s main hub, iii) Pegasus’s limited visibility on international expan sion

and iii) the short term headwinds on cost side for Pegasus. THY looks cheap compared to peers on 2015 and 2016 P/E and EV/

EBITDA while Pegasus does not for 2015.

Valuation: Given 1Q15 results and YTD traffic trends, we have revisited our forecasts with new assumptions for the macro -economy, oil

prices (USD61/bbl vs. USD68/bbl previously) and exchange rates (2015 average EUR/USD now assumed as 1.11, vs. 1.20 previously),

we have cut our 2015 EBITDA margin forecasts by 0.6 pps for THY and 2.4 pps for Pegasus. Our valuation for airlines is based on a

target 2015 EV/EBITDAR multiple (7.0x for THY and 7.8x for Pegasus). Accordingly, we decreased our 12 month forward target sh are

prices for THY by 5% to TL11.25, and by 20% to TL31.65 for Pegasus. We maintain our Outperform recommendation for the both stock.

Risks: A slowdown in passenger growth momentum, weaker than expected unit revenues or a deteriorating cost base are the key risks

for airlines. A potential sale by shareholders would lead to share price weakness for the carriers.

Company Ticker Mcap

3M Avg

Volume Upside

Old New (TLmn) (TLmn) Old New (%) 2015E 2016E 2015E 2016E 1M 3M YTD

Pegasus Airlines PGSUS Outperform Outperform 2,567 45 39.80 31.65 26% 7.3 6.4 13.5 9.2 3% 3% -20%

Turkish Airlines THYAO Outperform Outperform 12,213 216 11.90 11.25 27% 6.7 6.1 6.8 7.4 -1% 1% -2%

Source: Garanti Securities

Target Price

(TL)Recommendation EV/EBITDAR P/E

BIST-100 Relative

Performances

2

RESEARCH

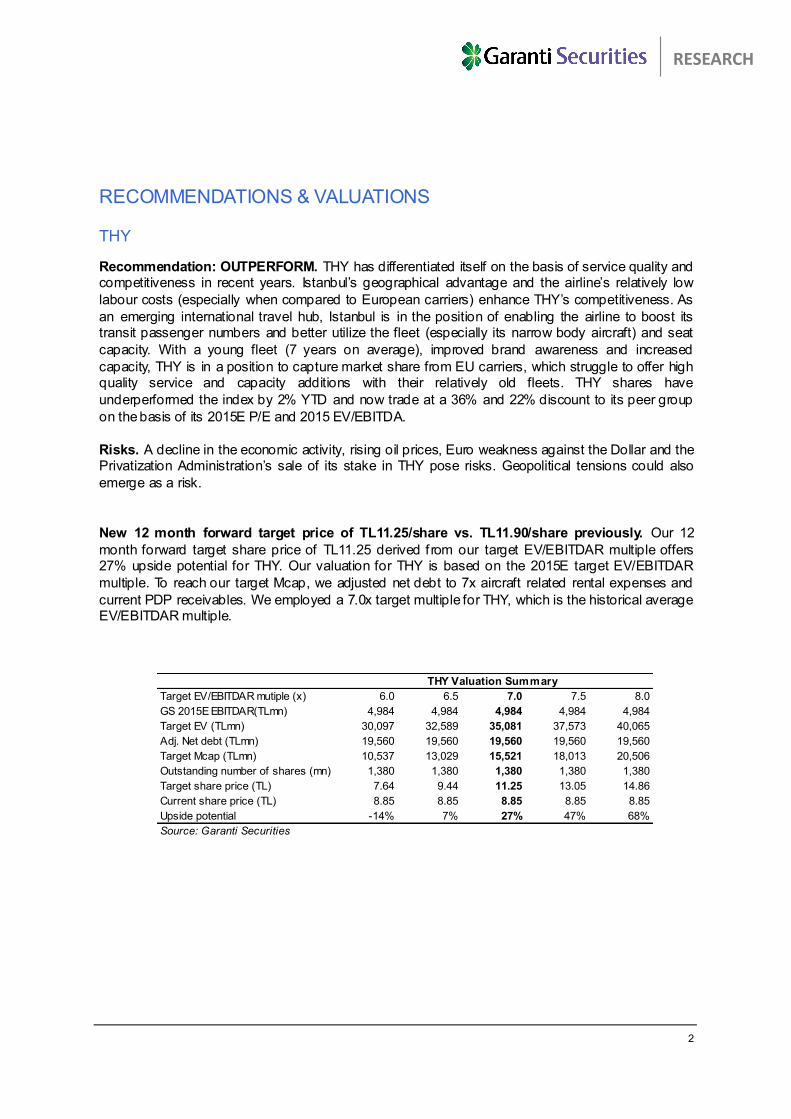

RECOMMENDATIONS & VALUATIONS THY Recommendation: OUTPERFORM. THY has differentiated itself on the basis of service quality and competitiveness in recent years. Istanbul’s geographical advantage and the airline’s relatively low

labour costs (especially when compared to European carriers) enhance THY’s competitiveness. As

an emerging international travel hub, Istanbul is in the position of enabling the airline to boost its transit passenger numbers and better utilize the fleet (especially its narrow body aircraft) and seat

capacity. With a young fleet (7 years on average), improved brand awareness and increased

capacity, THY is in a position to capture market share from EU carriers, which struggle to offer high quality service and capacity additions with their relatively old fleets. THY shares have

underperformed the index by 2% YTD and now trade at a 36% and 22% discount to its peer group

on the basis of its 2015E P/E and 2015 EV/EBITDA.

Risks. A decline in the economic activity, rising oil prices, Euro weakness against the Dollar and the Privatization Administration’s sale of its stake in THY pose risks. Geopolitical tensions could also

emerge as a risk.

New 12 month forward target price of TL11.25/share vs. TL11.90/share previously. Our 12

month forward target share price of TL11.25 derived f rom our target EV/EBITDAR multiple offers 27% upside potential for THY. Our valuation for THY is based on the 2015E target EV/EBITDAR

multiple. To reach our target Mcap, we adjusted net debt to 7x aircraft related rental expenses and

current PDP receivables. We employed a 7.0x target multiple for THY, which is the historical average EV/EBITDAR multiple.

Target EV/EBITDAR mutiple (x) 6.0 6.5 7.0 7.5 8.0

GS 2015E EBITDAR(TLmn) 4,984 4,984 4,984 4,984 4,984

Target EV (TLmn) 30,097 32,589 35,081 37,573 40,065

Adj. Net debt (TLmn) 19,560 19,560 19,560 19,560 19,560

Target Mcap (TLmn) 10,537 13,029 15,521 18,013 20,506

Outstanding number of shares (mn) 1,380 1,380 1,380 1,380 1,380

Target share price (TL) 7.64 9.44 11.25 13.05 14.86

Current share price (TL) 8.85 8.85 8.85 8.85 8.85

Upside potential -14% 7% 27% 47% 68%

Source: Garanti Securities

THY Valuation Summary

3

RESEARCH

Pegasus Airlines Recommendation: OUTPERFORM. Given its proven track record on growth, we believe that Pegasus stands out as a preferred play in an underpenetrated sector coupled with its ambitious

expansion plans and effective cost management. As the number one LCC and second largest carrier in Turkey, Pegasus will be one of the key beneficiaries of increasing GDP and attractive

demographics, which bodes well for discount carriers. Using Istanbul Sabiha Gokcen Airport (SAW)

as its main hub, Pegasus differentiates itself f rom an ordinary LCC whose business models are based on only point to point travel; Pegasus operates like both a network and point to point carrier,

thanks to Istanbul’s geographical advantage connecting 50 countries within a 3 hour flight.

Furthermore, we think Pegasus’ low cost management enables the airline to boast one of the lowest CASK levels on the back of its young fleet and low labour costs. Despite our conservative

assumptions given the likely increased competition and cost pressures f rom exchange rates, the

changes in the fleet and ramp handling investments, we believe the current levels offer a good entry point to accumulate the stock for the long-term investors. We maintain our recommendation for

Pegasus as Outperform.

Risks. The key risks would be an increase in oil prices, unrest in Turkey and neighbouring countries,

stiff competition, limited international expansion and EUR weakness against the USD. About 14.5%

of Pegasus shares were registered to the Central Securities Depository in mid-February 2015 with no intention for immediate sale, yet a potential stake sale could result in an overhang for the shares.

New 12 month forward target price of TL31.65/share vs. TL39.80/share previously. We value

Pegasus using a 2015E target EV/EBITDAR multiple. On our EV/EBITDAR multiple valuation, we

apply a 2015E EV/EBITDAR multiple of 7.8x, in line with the historical average. Finally, to reach our target Mcap, we adjusted the net debt for 7x aircraft related rental expenses PDP receivables.

EV/EBITDAR multiple (x) 7.30 7.55 7.80 8.05 8.30

GS 2015E EBITDAR (TLmn) 660 660 660 660 660

Target EV (TLmn) 4,816 4,981 5,147 5,312 5,477

Adj. Net debt (TLmn) 1,917 1,917 1,917 1,917 1,917

Minorities (TLmn) -7 -7 -7 -7 -7

Target Mcap (TLmn) 2,907 3,072 3,237 3,402 3,567

Outstanding number of shares (mn) 102 102 102 102 102

Target share price (TL) 28.42 30.04 31.65 33.26 34.88

Current share price (TL) 25.10 25.10 25.10 25.10 25.10

Upside potential 13% 20% 26% 33% 39%

Source: Garanti Securities

Pegasus Valuation Summary

4

RESEARCH

PEER COMPARISON We present the multiples of international carriers in an attempt to put the valuations of THY and

Pegasus into perspective. THY trades at a discount to its emerging peers on the basis of its 2015E

on a P/E multiples, but Pegasus does not. On an EV/EBITDA comparison, THY trades at an average discount of 24% vs. 9% of Pegasus.

Company Country MCAP (US$mn) 2015 2016 2015 2016 2015 2016

Full Service Carriers (FSC)

Developed 0.6 0.6 4.3 4.1 9.1 7.3

Deutsche Lufthansa AG GERMANY 6,088 0.3 0.3 2.7 2.5 5.8 5.2

Air France-KLM FRANCE 2,169 0.4 0.3 4.2 3.4 n.a 5.3

International Consolidated Airlines Group SA BRITAIN 15,912 0.7 0.7 4.6 4.1 10.0 8.1

Air Berlin PLC GERMANY 146 0.2 0.2 n.a 83.4 n.a n.a

Qantas Airways Ltd AUSTRALIA 5,316 0.7 0.6 4.4 3.6 10.4 6.5

Virgin Australia Holdings Ltd AUSTRALIA 1,170 0.6 0.6 9.0 5.6 n.a 14.8

Emerging 1.9 1.7 8.5 7.9 10.6 9.8

Cathay Pacific Airways Ltd HONG KONG 9,651 1.1 1.0 6.3 5.9 10.8 9.6

Air China Ltd CHINA 24,361 2.1 1.9 8.6 8.2 11.0 10.4

Aeroflot - Russian Airlines OJSC RUSSIA 812 0.4 0.4 5.5 4.1 n.a 5.3

Gol Linhas Aereas Inteligentes SA BRAZIL 710 0.7 0.7 8.7 6.6 n.a n.a

China Airlines Ltd TAIWAN 2,123 1.2 1.1 5.5 5.4 7.1 7.1

China Eastern Airlines Corp Ltd CHINA 21,733 2.1 1.9 9.9 9.1 11.0 10.2

China South City Holdings Ltd HONG KONG 2,776 2.5 2.0 6.6 5.5 7.4 6.2

Low cost carriers (LCC)

Developed 1.9 1.7 8.1 7.2 14.5 12.5

Ryanair Holdings PLC IRELAND 17,702 2.6 2.4 10.4 9.3 18.4 15.7

easyJet PLC BRITAIN 9,715 1.2 1.2 7.4 6.7 12.1 10.9

AirAsia Bhd MALAYSIA 1,242 2.9 2.7 8.7 8.2 6.9 5.9

Spirit Airlines Inc UNITED STATES 4,556 1.8 1.5 6.3 5.4 12.9 11.5

JetBlue Airways Corp UNITED STATES 6,121 1.1 1.0 4.8 4.4 11.1 10.0

Norwegian Air Shuttle ASA NORWAY 1,429 1.1 1.0 13.1 8.7 22.6 11.2

WestJet Airlines Ltd CANADA 2,782 0.8 0.7 3.5 3.4 8.2 8.1

Emerging 1.9 1.8 7.7 7.1 10.7 9.8

Cebu Air Inc PHILIPPINES 1,165 1.4 1.3 6.2 6.0 8.5 7.7

Air Arabia PJSC UAE 2,122 2.2 2.0 8.5 7.6 11.8 11.0

THYAO multiples 4,466 0.8 0.7 6.6 5.8 6.8 7.4

Discount/Premium to Developed FSC 28% 16% 53% 41% -25% 1%

Discount/Premium to Emerging FSC -59% -60% -22% -27% -36% -25%

PGSUS multiples 939 0.8 0.7 7.5 5.9 13.5 9.2

Discount/Premium to Developed LCC -59% -61% -7% -17% -7% -26%

Discount/Premium to Emerging LCC -60% -62% -2% -16% 27% -6%

Source: Bloomberg, Garanti Securities

EV/SALES EV/EBITDA P/E

5

RESEARCH

The impact of lower oil prices and EUR/USD rate for Turkish air carriers in brief

Fuel expenses represent the largest cost item for airlines. Fuel expenses account for around 40% of the total costs for both THY and Pegasus.

Hedging. The airlines have an active hedging strategy for their fuel costs through swaps and options. The fuel surcharge is also a part of their policy. THY has currently hedged 45% of its fuel

expenses for 2015 compared to 46% for Pegasus. THY’s blended oil price is USD79/bbl under the

assumption of an average Brent price of USD71/bbl vs. our blended price of USD74/bbl as we assume USD61 per barrel for Brent on average for 2015. According to our calculations, the blended

price for Pegasus is USD77/bbl as the Company hedges itself at USD96/bbl. The airlines have an

active hedging strategy for their fuel costs through swaps and options.

Impact on financials. Our base case scenario assumes an average Brent price of $61/bbl in 2015.

All else being equal, each USD5/bbl change in our assumption for oil prices results in a 10% change in the 2015E EBITDA for THYAO, or a 12% change in that of PGSUS. That translates into a 1.1 pps

EBITDA margin difference for THYAO vs. the 1.2 pps difference for PGSUS. Meanwhile, each 1% change in the EUR/USD exchange rate would have a 5% impact on the projected 2015E EBITDA

for THY and a 3% impact on the same multiple for Pegasus. Our sensitivity analysis regarding the

the change in the 2015E average Brent price and EUR/USD rate is tabulated below.

Pegasus' fuel cost

Source: Garanti Securities

44.4% 43.9% 44.6% 44.7%

41.1%

36.6% 36.2%38.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2011 2012 2013 2014

as % of sales as% of cogs

THY's fuel cost

Source: Garanti Securities

40.8%

44.0% 42.9% 42.4%

33.9% 34.9% 35.0% 34.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2011 2012 2013 2014

as % of sales as % of cogs

6

RESEARCH

THY

%ch 2015 EBITDA 46 51 56 61 66 71

1.05 -1% -11% -21% -31% -40% -50%

1.06 4% -6% -16% -26% -35% -45%

1.07 9% -1% -11% -21% -30% -40%

1.08 14% 4% -6% -15% -25% -35%

1.09 19% 9% -1% -10% -20% -30%

1.10 24% 14% 5% -5% -15% -25%

1.11 29% 19% 10% 0% -10% -19%

1.13 34% 25% 15% 5% -5% -14%

1.14 40% 30% 20% 10% 1% -9%

1.15 45% 35% 26% 16% 6% -4%

1.16 50% 41% 31% 21% 11% 2%

THY

2015 EBITDA margin 46 51 56 61 66 71

1.05 11.4% 10.2% 9.1% 8.0% 6.9% 5.8%

1.06 11.9% 10.8% 9.7% 8.6% 7.5% 6.3%

1.07 12.5% 11.4% 10.3% 9.2% 8.0% 6.9%

1.08 13.1% 12.0% 10.9% 9.7% 8.6% 7.5%

1.09 13.7% 12.6% 11.4% 10.3% 9.2% 8.1%

1.10 14.3% 13.2% 12.0% 10.9% 9.8% 8.7%

1.11 14.9% 13.8% 12.6% 11.5% 10.4% 9.3%

1.13 15.5% 14.4% 13.2% 12.1% 11.0% 9.9%

1.14 16.1% 15.0% 13.8% 12.7% 11.6% 10.5%

1.15 16.7% 15.6% 14.5% 13.3% 12.2% 11.1%

1.16 17.3% 16.2% 15.1% 14.0% 12.8% 11.7%

Brent Price Assumptions (USD)

EU

R/U

SD

Assu

mp

tio

ns

EU

R/U

SD

Assu

mp

tio

ns

Brent Price Assumptions (USD)

Pegasus

%ch 2015 EBITDA 46 51 56 61 66 71

1.05 19% 6% -6% -18% -30% -42%

1.06 21% 9% -3% -15% -27% -39%

1.07 24% 12% 0% -12% -24% -36%

1.08 27% 15% 3% -9% -21% -33%

1.09 30% 18% 6% -6% -18% -30%

1.10 33% 21% 9% -3% -15% -27%

1.11 37% 24% 12% 0% -12% -24%

1.13 40% 27% 15% 3% -9% -21%

1.14 43% 31% 18% 6% -6% -18%

1.15 46% 34% 21% 9% -3% -15%

1.16 49% 37% 25% 12% 0% -12%

Pegasus

2015 EBITDA margin 46 51 56 61 66 71

1.05 12.1% 10.8% 9.6% 8.4% 7.1% 5.9%

1.06 12.4% 11.1% 9.9% 8.7% 7.4% 6.2%

1.07 12.7% 11.4% 10.2% 9.0% 7.7% 6.5%

1.08 13.0% 11.7% 10.5% 9.3% 8.0% 6.8%

1.09 13.3% 12.1% 10.8% 9.6% 8.3% 7.1%

1.10 13.6% 12.4% 11.1% 9.9% 8.6% 7.4%

1.11 13.9% 12.7% 11.4% 10.2% 8.9% 7.7%

1.13 14.2% 13.0% 11.7% 10.5% 9.3% 8.0%

1.14 14.5% 13.3% 12.1% 10.8% 9.6% 8.3%

1.15 14.9% 13.6% 12.4% 11.1% 9.9% 8.7%

1.16 15.2% 13.9% 12.7% 11.5% 10.2% 9.0%

Brent Price Assumptions (USD)

EU

R/U

SD

Assu

mp

tio

ns

Brent Price Assumptions (USD)

EU

R/U

SD

Assu

mp

tio

ns

7

June 18, 2015

Turkish Airlines Outperform (Maintained)

Current Price TL 8.85TL

12M Target Price TL 11.25TL

Potential Return TL 27%

Current Mcap (TLmn) 12,213

Current EV (TLmn) 31,773

4,466

Bloomberg/Reuters:

1 mth 3 mth 12mth

-1% 1% 28%

81.7

YTD TL Return: -8%

1,380

Free Float (%): 51

73%

Financials and Ratios 2013 2014 2015E 2016E

Net Sales (TLmn) 18,777 24,158 29,321 33,485

EBITDA (TLmn) 2,330 2,910 3,378 3,912 Research Analyst: Baris Ince

EBITDAR (TLmn) 3,192 4,095 4,984 5,690 +90 (212) 384 1141

Net Income (TLmn) 683 1,819 1,793 1,651 [email protected]

EBITDA Margin 12.4% 12.0% 11.5% 11.7%

EBITDAR Margin 17.0% 17.0% 17.0% 17.0% Sales Contact:

P/E (x) 17.9 6.7 6.8 7.4 +90 (212) 384 1155-58

EV/EBITDA (x) 9.1 7.9 6.6 5.8 [email protected]

EV/Sales (x) 1.13 0.95 0.76 0.67

EPS (TL) 0.49 1.32 1.30 1.20

DPS (TL) 0.13 0.00 0.00 0.00

Foreign Ow nership in Free Float :

Stock Market Data

THYAO.TI / THYAO.IS

Relative Performance:

52 Week Range (TL): 6.08 / 10.2

Average Daily Vol (US$mn) 3 mth:

Shares Outstanding (mn):

Current Mcap (US$mn)

Price Performance (TL)

5.00

6.20

7.40

8.60

9.80

11.00

12.1

3

02.1

4

04.1

4

06.1

4

08.1

4

10.1

4

12.1

4

02.1

5

04.1

5

THYAO BIST-100

Flying high

We maintain our Outperform recommendation for Turkish

Airlines with a 5% lower 12 month forward target share price of

TL11.25, indicating 27% upside.

There is almost no change to our EBITDA and net income forecasts for 2015.

The stock trades at a 22% and 36% discount to its emerging peers, based on its 2015E EV/EBITDA and P/E.

Weak pricing/traffic figures concerns to offset by solid cost discipline

Despite the weakness in revenue yields in 1Q15, we have seen a good

start to the year in terms of profitability thanks to not only lower oil prices

but also strong cost management (EBITDA margin up by 290 bps in

1Q15). Pax growth came in at 8.7% YoY in 5M15 with a load factor of

77.6% (down 1.0 pps YoY). We attribute part of this underperformance to

a high base and the harsh winter. The airline targets 15% pax growth (vs.

our 10% forecast) with a 80.3% load factor (vs. our forecast of 77.9%) in

2015. We assume the growth will gain some momentum on the back of

attractive fares and the addition of wide body aircraft to the fleet. The

guidance provided by the airline was based on a fleet of 293 aircraft at the

end of 2015; this has been revised up to a fleet of 303. Most of the new

aircraft will have joined the fleet in 1H15, raising the prospect of further

upside to our traffic assumptions. We believe that our projections are

already included any potential cost overruns in relation to personnel

expenses (given fleet additions, 16% increase in personnel number is

guided) and unfavourable exchange rate movements as we assume

flattish margins in 2015 although in 1Q15, we have seen a sharp decline

in all cost items in terms of ASK except G&A and depreciation. THY plans

to shift 28 of its aircraft to SAW in 2015 and increase its market share at

Istanbul’s second airport by 5 pps to 25%. We believe after the weakness

in yields, we will see better yields from 3Q14 on the high demand and

normalization of the base. We project 13% (12% in 1Q15) and 11% (13%

in 1Q15) decline in RASK and CASK in 2015. The Company hedges 45%

of its 2015 budgeted fuel consumption. Blended oil price is around

USD79. All else being equal, each USD5/bbl and 1% change in our

assumption for oil prices and EUR/USD result in a 10% and 5% change in

the 2015E EBITDA for THY (see page 6). The Company has recently

converted international ticket sales originating in Turkey to USD from

EUR. Such sales account for c15% of its revenue. This will reduce the

negative impacts of currency mismatch on operations. 40% and 16% of

revenues were in EUR and USD, respectively, in 2014 while those of

costs were 14% and 56%.

RESEARCH

Turkey - Equity - Airline

Company Update

Please see the last page of this report for important disclosures.

Please see the last page of this report for important disclosures.

8

RESEARCH

SUMMARY FINANCIALS (TL mn)

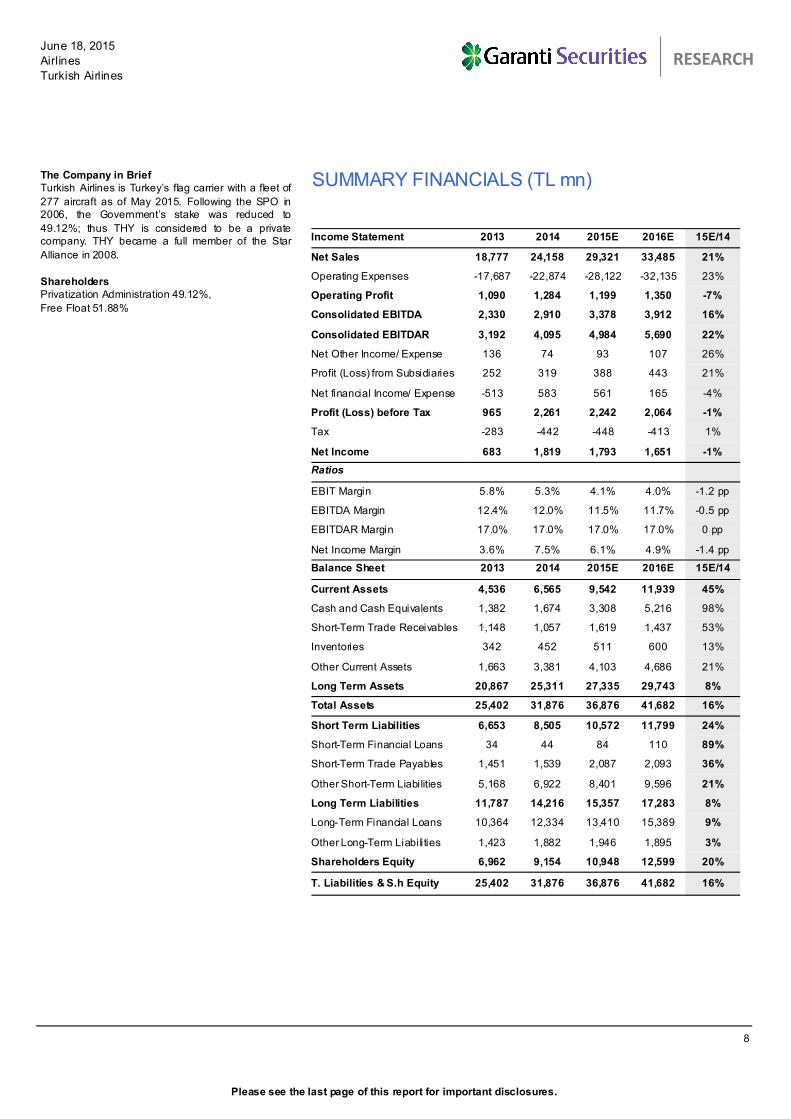

The Company in Brief

Turkish Airlines is Turkey’s flag carrier with a fleet of

277 aircraft as of May 2015. Following the SPO in

2006, the Government’s stake was reduced to

49.12%; thus THY is considered to be a private

company. THY became a full member of the Star

Alliance in 2008.

Shareholders

Privatization Administration 49.12%,

Free Float 51.88%

June 18, 2015

Airlines

Turkish Airlines

Income Statement 2013 2014 2015E 2016E 15E/14

Net Sales 18,777 24,158 29,321 33,485 21%

Operating Expenses -17,687 -22,874 -28,122 -32,135 23%

Operating Profit 1,090 1,284 1,199 1,350 -7%

Consolidated EBITDA 2,330 2,910 3,378 3,912 16%

Consolidated EBITDAR 3,192 4,095 4,984 5,690 22%

Net Other Income/ Expense 136 74 93 107 26%

Profit (Loss) from Subsidiaries 252 319 388 443 21%

Net financial Income/ Expense -513 583 561 165 -4%

Profit (Loss) before Tax 965 2,261 2,242 2,064 -1%

Tax -283 -442 -448 -413 1%

Net Income 683 1,819 1,793 1,651 -1%

Ratios

EBIT Margin 5.8% 5.3% 4.1% 4.0% -1.2 pp

EBITDA Margin 12.4% 12.0% 11.5% 11.7% -0.5 pp

EBITDAR Margin 17.0% 17.0% 17.0% 17.0% 0 pp

Net Income Margin 3.6% 7.5% 6.1% 4.9% -1.4 pp

Balance Sheet 2013 2014 2015E 2016E 15E/14

Current Assets 4,536 6,565 9,542 11,939 45%

Cash and Cash Equivalents 1,382 1,674 3,308 5,216 98%

Short-Term Trade Receivables 1,148 1,057 1,619 1,437 53%

Inventories 342 452 511 600 13%

Other Current Assets 1,663 3,381 4,103 4,686 21%

Long Term Assets 20,867 25,311 27,335 29,743 8%

Total Assets 25,402 31,876 36,876 41,682 16%

Short Term Liabilities 6,653 8,505 10,572 11,799 24%

Short-Term Financial Loans 34 44 84 110 89%

Short-Term Trade Payables 1,451 1,539 2,087 2,093 36%

Other Short-Term Liabilities 5,168 6,922 8,401 9,596 21%

Long Term Liabilities 11,787 14,216 15,357 17,283 8%

Long-Term Financial Loans 10,364 12,334 13,410 15,389 9%

Other Long-Term Liabilities 1,423 1,882 1,946 1,895 3%

Shareholders Equity 6,962 9,154 10,948 12,599 20%

T. Liabilities & S.h Equity 25,402 31,876 36,876 41,682 16%

Please see the last page of this report for important disclosures.

9

RESEARCH

June 18, 2015

Airlines

Turkish Airlines

REVISIONS TO FORECASTS As shown below, we have fine tuned our forecasts based on the our new macroeconomic and traffic assumptions.

2011 2012 2013 2014 2015E 2016E

# of total passengers (mn) - new 32.7 39.0 48.3 54.7 60.2 68.1

# of total passengers (mn) - old 32.7 39.0 48.3 54.8 62.3 72.5

Difference 0.0% 0.0% 0.0% -0.3% -3.4% -6.1%

YoY 12.2% 19.6% 23.6% 13.3% 10.0% 13.2%

Load factor - new 72.6% 77.7% 79.0% 78.9% 77.9% 78.4%

Load factor - old 72.6% 77.7% 79.0% 79.7% 79.9% 80.0%

Difference 0.0 pps 0.0 pps 0.0 pps -0.8 pps -2.0 pps -1.6 pps

YoY (pps) -1.1 pps 5.1 pps 1.3 pps -0.1 pps -1.0 pps 0.5 pps

ASK (mn) - new 81,167 96,131 116,399 135,330 156,838 182,554

ASK (mn) - old 81,167 96,131 116,399 135,764 153,858 179,989

Difference 0.0% 0.0% 0.0% -0.3% 1.9% 1.4%

YoY 24.7% 18.4% 21.1% 16.3% 15.9% 16.4%

RPK (mn) - new 58,918 74,705 91,962 106,826 122,163 143,107

RPK (mn) - old 58,918 74,705 91,962 108,202 122,858 144,000

Difference 0.0% 0.0% 0.0% -1.3% -0.6% -0.6%

YoY 22.8% 26.8% 23.1% 16.2% 14.4% 17.1%

RASK (US cents) - new 8.7 8.6 8.5 8.2 7.1 6.8

RASK (US cents) - old 8.7 8.6 8.5 8.4 8.3 8.2

Difference 0.0% 0.0% 0.0% -3.1% -14.2% -16.6%

YoY 1.0% -1.6% -1.1% -3.8% -12.5% -4.3%

CASK (US cents) - new 8.4 7.9 8.0 7.7 6.8 6.6

CASK (US cents) - old 8.4 7.9 8.0 7.9 7.8 7.8

Difference 0.0% 0.0% 0.0% -2.3% -12.2% -15.7%

YoY 3.6% -6.0% 0.6% -3.3% -11.4% -4.2%

CASK-ex fuel (US cents) - new 5.5 4.9 5.0 4.9 4.7 4.5

CASK-ex fuel (US cents) - old 5.5 4.9 5.0 5.1 5.3 5.2

Difference 0.0% 0.0% 0.0% -4.2% -11.6% -12.9%

YoY -7.4% -10.0% 1.5% -2.6% -4.0% -3.6%

ROAE - new 0.4% 23.3% 11.0% 22.6% 17.8% 14.0%

ROAE - old 0.4% 23.3% 11.0% 21.2% 19.8% 17.8%

Difference 0.0 pps 0.0 pps 0.0 pps 1.4 pps -1.9 pps -3.7 pps

YoY (pps) -7.5 pps 22.9 pps -12.3 pps 11.5 pps -4.7 pps -3.8 pps

Average Brent price (USD) - new 111 112 108 99 61 67

Average Brent price (USD) - old 111 112 108 103 68 80

Difference 0.0% 0.0% 0.0% -3.4% -10.6% -16.3%

YoY 38% 1% -3% -9% -39% 10%

Source: The Company, Garanti Securities

*Figures are based on our own calculations may differ from company's figures

*2014 old figures are our previous assumptions, new figures are actual

Revisions in model assumptions at a glance*

Please see the last page of this report for important disclosures.

10

RESEARCH

June 18, 2015

Airlines

Turkish Airlines

We are conservative compared to the management in our forecasts.

We have revised our 2015-16 Sales and EBITDA forecasts to take account of our new macro assumptions and traffic f igures.

Bloomberg vs. Garanti Forecasts

Our forecasts for both 2015 and 2016 are in line with the market estimates at the top line, but lower at the EBITDA level when compared to the

market consensus. We believe the consensus has incorporated no

potential cost overruns resulting from the high level of additions to the fleet or included the other income line into the calculation. However, our

net income estimate is higher than the market in both 2015 and 2016,

most probably owing to our estimate of higher FX gains and profits from associates. Our target price of TL11.25 is 2% higher than the Bloomberg

consensus of TL11.01.

2015E

Guidance Garanti Diff.

Total Pax (mn) 62.9 60.2 -4%

-Domestic 25.9 25.6 -1%

-International 36.0 34.5 -4%

- Hajj and charter f lights pax 1.0

Revenue (US$bn) 12.0 11.2 -7%

Total ASK (bn) 157 157 0%

Load Factor 80.3% 77.9% -2.4%

Source: The Company, Garanti Securities

Revision in Estimates

THYAO

(TLmn) 2015E 2016E 2015E 2016E 2015E 2016E

Net Sales 29,378 35,162 29,321 33,485 0% -5%

EBITDA 3,574 3,874 3,378 3,912 -5% 1%

Net Profit 1774 1849 1793 1651 1% -11%

EBITDA Margin 12.2% 11.0% 11.5% 11.7% -0.6% 0.7%

Net Income Margin 6.0% 5.3% 6.1% 4.9% 0.1% -0.3%

Target Price

Source: Bloomberg, Garanti Securities

OLD NEW % Change

11.90 11.25 -5%

Consensus vs. Our estimates

THYAO

(TLmn) 2015E 2016E 2015E 2016E 2015E 2016E

Net Sales 28,484 34,446 29,321 33,485 3% -3%

EBITDA 3,982 4,981 3,378 3,912 -15% -21%

Net Profit 1,731 1,475 1,793 1,651 4% 12%

EBITDA Margin 14.0% 14.5% 11.5% 11.7% -2.5 pps -2.8 pps

Net Income Margin 6.1% 4.3% 6.1% 4.9% 0.0 pps 0.6 pps

Target Price

Source: Bloomberg, Garanti Securities

Bloomberg Garanti Securities Difference

11.01 11.25 2%

Please see the last page of this report for important disclosures.

11

RESEARCH

June 18, 2015

Airlines

Turkish Airlines

Turkish Airlines 1Q15 Results Review Turkish Airlines reported a net prof it of TL373mn in 1Q15, better than the consensus estimate of a TL319mn net profit and in line with our estimate

of a TL380mn net prof it. The airline generated TL5,456mn of revenues in the quarter – in between the consensus and our expectation. 1Q15

EBITDA was broadly in line with our estimate while exceeded the

consensus by 23%. According to our calculations, the 1Q15 EBITDAR came in at TL594mn with a flattish margin YoY at 10.9%.

The Company recorded TL642mn of net financial income in the quarter compared to TL130mn expense a year ago, mainly due to FX gains.

Recall that, the airline’s functional currency is USD and the Company had

a TL9.3bn short FX position - mostly based in EUR and JPY - as of 1Q15.

In 1Q15, based on the Company’s calculations, unit revenues

decreased by 11% YoY (2% excluding currency impact) while CASK declined by 13% YoY thanks to lower oil prices. CASK (ex-fuel)

declined by 7% in 1Q15. According to the Company, on annual basis, 1Q operating profit was hit by US$89mn f rom currency and US$69mn

f rom unit revenue (ex-currency) weakness vs. positive impact of

favourable fuel prices at US$242mn.

The Company shared some information regarding its regional yield

development in 1Q15 vs. 1Q14. Accordingly, all markets generated negative contribution to revenue. Africa was the worst performer with a

decline of 17% in RASK, followed by 14% in Europe&CIS, 12% in

America and Asia&Far East. The declines were 6% in Middle East and 2% in Turkey, respectively.

Turk Hava Yollari Summary Financials

(mn TL) 1Q14 2Q14 3Q14 4Q14 1Q15 1Q15/1Q14 1Q15/4Q14

Net Sales 5,128 6,139 7,171 5,721 5,456 6% -5%

Gross Profit 511 1,223 1,878 729 662 30% -9%

Operating Profit -226 438 1,157 -85 -176 n.m. n.m.

EBITDA 157 831 1,567 355 324 106% -9%

EBITDAR 570 999 1,919 607 594 4% -2%

Net Other Income/Expense 43 57 -3 -23 128 195% n.m.

Profit (Loss) from Subsidiaries -18 59 102 18 -33 n.m. n.m.

Financial Inc./ Exp. (net) -130 -127 478 362 642 n.m. 77%

PROFIT BEFORE TAX FROM CONTINUING OPERATIONS -303 455 1,762 348 592 n.m. 70%

Tax 77 -57 -388 -74 -219 n.m. n.m.

Net Income -226 398 1,373 274 373 n.m. 36%

Net Cash -10,927 -10,741 -11,449 -12,125 -13,978

Working Capital 415 322 172 -29 578

Shareholders Equity 6,909 7,155 9,221 9,154 10,924

Ratios

Gross Margin 10.0% 19.9% 26.2% 12.7% 12.1% 2.2 pp -0.6 pp

Operating Margin n.m. 7.1% 16.1% n.m. n.m. n.m. n.m.

EBITDA Margin 3.1% 13.5% 21.9% 6.2% 5.9% 2.9 pp -0.3 pp

EBITDAR Margin 11.1% 16.3% 26.8% 10.6% 10.9% -0.2 pp 0.3 pp

Net Profit Margin n.m. 6.5% 19.2% 4.8% 6.8% n.m. 2.1 pp

Change

Please see the last page of this report for important disclosures.

12

RESEARCH

June 18, 2015

Airlines

Turkish Airlines

Revenue Development (1Q14 vs 1Q15) (USDmn)

Source: Turkish Airlines

2,315

2,219

181

-15-62

-200

2,000

2,050

2,100

2,150

2,200

2,250

2,300

2,350

2,400

2,450

2,500

1Q14 Volume Decrease in Cargo andOther Rev.

Unit Revenue (R/Y) Currency 1Q15

Net Operating Profit Bridge (USDmn)

Source: Turkish Airlines

-103

-89

-69

-24 -14-13

242

-70

0

100

200

300

400

500

600

1Q14 Currency Unit Revenue(R/Y)

Utilization L/F Ex-fuel Unit Cost(ex-currency ex-

utilization)

Fuel 1Q15

CASK Breakdown (USc) 1Q14 1Q15 Change

Fuel 2.93 2.18 -25.8%

Personnel 1.32 1.25 -5.3%

Aircraft Ow nership 1.00 0.95 -4.9%

Airports & Air Navigation 0.72 0.61 -15.2%

Sales & Marketing 0.64 0.60 -5.2%

Ground Handling 0.48 0.44 -9.2%

Passenger Services & Catering 0.42 0.41 -0.6%

Maintenance 0.31 0.29 -6.6%

General Administration 0.06 0.07 21.9%

Other Cost of Sales 0.13 0.12 -1.3%

TOTAL 8.00 6.92 -13.4%

Source: Turkish Airlines

Please see the last page of this report for important disclosures.

13

RESEARCH

June 18, 2015

Airlines

Turkish Airlines

Scheduled Services Unit Revenue Development

Source: Turkish Airlines

7.11

6.31

1Q14 1Q15

RASK (USc)

7.11

6.97

1Q14 1Q15

RASK ex-currency (USc)

-2.0%

8.70

7.77

1Q14 1Q15

R/Y (USc)

-10.8%

8.70

8.57

1Q14 1Q15

R/Y ex-currency (USc)

-1.5%

-11.2%

Regional Yield Development in USD (1Q’14 vs 1Q’15)

Source: Turkish Airlines

Please see the last page of this report for important disclosures.

14

RESEARCH

June 18, 2015

Airlines

Turkish Airlines

Source: The Company, Garanti Securities

Quarterly Figures

7.7

8.7

9.3

8.48.1

8.69.0

8.07.7

8.59.1

7.4

6.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

US

ce

nt

RASK

8.38.0

7.2

8.4 8.27.8 7.6

8.28.0 7.9

7.6 7.5

6.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

US

ce

nt

CASK

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

US

ce

nts

EBITDAR margin RASK-CASK (rhs)

5.3

4.8

4.4

5.4

5.2

4.9

4.7

5.2

5.15.0

4.7

4.9

4.7

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

5.6

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

US

cen

t

non-fuel CASK

68.0%

70.0%

72.0%

74.0%

76.0%

78.0%

80.0%

82.0%

84.0%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

mn

ASK Load factor (rhs)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

RASK/CASK EUR/USD - avg (rhs)

Turkish Airlines Traffic Figures

TOTAL

May.14 May.15 YoY Apr.15 MoM 5M14 5M15 YoY

Number of Landing 35,632 39,395 10.6% 36,648 7.5% 163,998 173,789 6.0%

Available Seat Km ('000) 11,482,373 13,098,265 14.1% 12,060,761 8.6% 52,539,502 57,877,353 10.2%

Revenue Passenger Km ('000) 9,134,608 10,293,260 12.7% 9,443,385 9.0% 41,279,017 44,898,239 8.8%

Passenger Load Factor (%) 79.6% 78.6% -0.9p 78.3% 0.28p 78.6% 77.6% -0.9p

Passengers Carried 4,735,840 5,404,402 14.1% 4,955,005 9.1% 21,354,513 23,212,782 8.7%

Cargo and Mail (Tons) 58,012 65,321 12.6% 59,282 10.2% 271,165 284,198 4.8%

Km Flow n ('000) 67,040 72,835 8.6% 68,743 6.0% 310,750 331,974 6.8%

Int-to-Int Transfer Passengers Carried 1,123,383 1,327,959 18.2% 1,282,180 3.6% 5,509,329 6,137,552 11.4%

Source: Turkish Airlines, Garanti Securities

Please see the last page of this report for important disclosures.

15

RESEARCH

June 18, 2015

Airlines

Turkish Airlines

Source: The Company, Garanti Securities

Yearly Figures

8.6 8.58.2

7.16.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2012 2013 2014 2015E 2016E

US

ce

nt

RASK

7.9 8.07.7

6.86.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2012 2013 2014 2015E 2016E

US

ce

nt

CASK

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2012 2013 2014 2015E 2016E

US

ce

nts

EBITDAR margin RASK-CASK (rhs)

4.9

5.0

4.9

4.7

4.5

4.2

4.3

4.4

4.5

4.6

4.7

4.8

4.9

5.0

5.1

2012 2013 2014 2015E 2016E

US

cen

t

non-fuel CASK

77.0%

77.5%

78.0%

78.5%

79.0%

79.5%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2012 2013 2014 2015E 2016E

mn

ASK Load factor (rhs)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.02

1.03

1.04

1.05

1.06

1.07

1.08

1.09

2012 2013 2014 2015E 2016E

RASK/CASK EUR/USD - avg (rhs)

THY Revenue by currency THY Expenses by currency

Source: The Company data

EURO, 40%

USD, 16%

TL, 14%

Other, 30%

2014

EURO, 14%

USD, 56%

TL, 24%

Other, 6%

2014

16

June 18, 2015

Pegasus Airlines Outperform (Maintained)

Current Price TL 25.10TL

12M Target Price TL 31.65TL

Potential Return TL 26%

Current Mcap (TLmn) 2,567

Current EV (TLmn) 4,477

939

Bloomberg/Reuters:

1 mth 3 mth 12mth

3% 1% -14%

16.9

YTD TL Return: -24%

102

Free Float (%): 35

41%

Financials and Ratios 2013 2014 2015E 2016E

Net Sales (TLmn) 2,394 3,082 3,564 4,113

EBITDA (TLmn) 412 412 363 463 Research Analyst: Baris Ince

EBITDAR (TLmn) 528 600 660 828 +90 (212) 384 1141

Net Income (TLmn) 92 143 190 279 [email protected]

EBITDA Margin 17.2% 13.4% 10.2% 11.3%

EBITDAR Margin 22.1% 19.5% 18.5% 20.1% Sales Contact:

P/E (x) 28.0 17.9 13.5 9.2 +90 (212) 384 1155-58

EV/EBITDA (x) 7.6 7.0 7.5 5.9 [email protected]

EV/Sales (x) 1.31 0.94 0.77 0.67

EPS (TL) 0.90 1.40 1.85 2.72

DPS (TL) 0.00 0.00 0.00 0.00

Current Mcap (US$mn)

Price Performance (TL)

Stock Market Data

PGSUS.TI / PGSUS.IS

Relative Performance:

52 Week Range (TL): 23.35 / 34.95

Average Daily Vol (US$mn) 3 mth:

Shares Outstanding (mn):

Foreign Ow nership in Free Float :

20.00

26.00

32.00

38.00

44.00

50.00

12.1

3

01.1

4

02.1

4

03.1

4

04.1

4

05.1

4

06.1

4

07.1

4

08.1

4

09.1

4

10.1

4

11.1

4

12.1

4

01.1

5

02.1

5

03.1

5

04.1

5

05.1

5

PGSUS BIST-100

Still attractive, yet ST risks dominate the agenda

We maintained Outperform rating for Pegasus Airlines with a 20%

lower 12 month forward target price of TL31.65/share, indicating

26% upside potential.

We find the airline’s growth prospects attractive, however, we doubt

that Pegasus will be able to achieve cost efficiencies over its

competitors in 2015 due to exchange rate pressure, changes in the fleet mix and initial ramp handling investments. Potential

competition from THY could also pressure the airline. Despite

aforementioned headwinds on cost side, we believe that the current

levels offer a good entry point for the LT investors. The stock trades

on par vs. peers, on its 2015E EV/EBITDA vs. 17% discount in 2016.

We reduced our estimates mainly on profitability side rather than

top line. The Company guides for stable yields compared to a c3 -4%

increase in unit costs. We trimmed our EBITDA and net income forecasts by a 18% and 35% for 2015.

Margins would be under pressure this year

Pegasus Airlines faced stiff competition from Turkish Airlines (THY) in 2014 with the flag carrier moving to form a second hub at SAW given the capacity

constraints at its IAA hub. THY plans to increase its market share at SAW by

5pps to 25% in 2015 with 28 aircraft operating from the terminal - which will

mean more pressure on revenue yields this year as well. In addition to

exchange rate movements and the change in the fleet mix, initial ramp

handling investments may burden Pegasus Airlines with additional cost

pressures in the short term. With our conservative assumptions, we cut our EBITDAR margin forecasts by 0.8 pps to 18.5% (vs. 19-21% guidance). On

the other hand, Pegasus enjoys strong ancillary revenues at EUR10.2/pax

(EUR9.3 in 2014), which are expected to remain between EUR10 -12 in the

next 2 years (we forecast EUR11.0/pax in 2016). We assume a 1% lower

RASK in 2015, but, 3% increase in CASK. The airline guides for a stable

yields and a 3-4% increase in CASK with a stable load factor. The Company

targets 15-17% growth in pax figures in 2015 (vs. our 12%). Pegasus recorded a net loss of TL147mn from derivative contracts on fuel and the

currency in 2014. As of 1Q15, Pegasus had a TL34mn liability under its

equity in connection with its derivatives contracts to be released to the P&L

in 2015 if realized, we conservatively reflected the amount of TL34mn to

2015E net income forecast (TL28mn in 1Q15). The Company hedges %45 of

its 2015 budgeted fuel consumption. Hedged price is around USD96. All else

being equal, each USD5/bbl and 1% change in our assumption for oil prices and EUR/USD result in a 12% and 3% change in the 2015E EBITDA for

Pegasus. (see page 6).The Company has recently converted international

ticket sales originating in Turkey to USD from EUR. Such sales account for

c13% of its revenue. This will reduce the negative impacts of currency

mismatch on operations. 39% and 15% of revenues were in EUR and USD,

respectively, in 2014 while those of costs were 23% and 56%.

RESEARCH

Turkey - Equity - Airlines

Company Update

Please see the last page of this report for important disclosures.

17

RESEARCH

SUMMARY FINANCIALS (TL mn)

The Company in Brief

Pegasus Airlines is a low cost carrier with a fleet of

61 aircrafts as April 2015. Founded in 1990 to

provide charter services, Pegasus’s business model

was changed following its acquisition by Esas

Holding in 2005. The airline uses Istanbul Sabiha

Gokcen Airport as main hub, and flies to 91 routes in

37 countries. Pegasus carried c.20mn passengers in

2014. In 2012, Pegasus placed an order for 100

aircraft (75 firm + 25 optional orders) to be delivered

between 2016 and 2022.

Shareholders

Esas Holding 62.92%,

Sabancı Family Members 2.57%

Free Float 34.51%

June 18, 2015

Airlines

Pegasus Airlines

Income Statement 2013 2014 2015E 2016E 15E/14

Net Sales 2,394 3,082 3,564 4,113 16%

Operating Expenses -2,118 -2,834 -3,407 -3,905 20%

Operating Profit 276 247 157 208 -37%

Consolidated EBITDA 412 412 363 463 -12%

Consolidated EBITDAR 528 600 660 828 10%

Net Other Income/ Expense -18 77 71 82 -8%

Profit (Loss) from Subsidiaries -5 9 24 28 178%

Net financial Income/ Expense -99 -198 -15 30 -92%

Profit (Loss) before Tax 155 136 237 348 75%

Tax -66 8 -47 -70 n.m.

Minority Interests -3 0 0 0 0%

Net Income 92 143 190 279 32%

Ratios

EBIT Margin 11.5% 8.0% 4.4% 5.1% -3.6 pp

EBITDA Margin 17.2% 13.4% 10.2% 11.3% -3.2 pp

EBITDAR Margin 22.1% 19.5% 18.5% 20.1% -0.9 pp

Net Income Margin 3.8% 4.7% 5.3% 6.8% 0.7 pp

Balance Sheet 2013 2014 2015E 2016E 15E/14

Current Assets 1,227 1,509 2,319 3,032 54%

Cash and Cash Equivalents 877 857 1,579 2,165 84%

Short-Term Trade Receivables 191 233 258 309 10%

Inventories 4 8 6 10 -16%

Other Current Assets 154 411 475 549 16%

Long Term Assets 2,278 2,026 2,160 2,297 7%

Total Assets 3,505 3,535 4,479 5,328 27%

Short Term Liabilities 684 863 1,230 1,449 43%

Short-Term Financial Loans 4 5 175 235 3783%

Short-Term Trade Payables 167 196 242 259 23%

Other Short-Term Liabilities 513 662 814 955 23%

Long Term Liabilities 1,674 1,511 1,898 2,439 26%

Long-Term Financial Loans 1,441 1,187 1,574 2,116 33%

Other Long-Term Liabilities 233 324 324 324 0%

Shareholders Equity 1,146 1,161 1,351 1,440 16%

T. Liabilities & S.h Equity 3,504 3,535 4,479 5,328 27%

Please see the last page of this report for important disclosures.

18

RESEARCH

June 18, 2015

Airlines

Pegasus Airlines

REVISIONS TO FORECASTS

2011 2012 2013 2014 2015E 2016E

# of total passengers (mn) - new 10.7 13.6 16.8 19.7 22.2 25.2

# of total passengers (mn) - old 10.7 13.6 16.8 19.9 22.9 26.4

Difference 0.0% 0.0% 0.0% -0.8% -3.2% -4.4%

YoY 33.7% 26.8% 23.9% 17.4% 12.3% 13.8%

Load factor - new 74.9% 78.2% 80.2% 80.0% 79.4% 79.9%

Load factor - old 74.9% 78.2% 80.2% 80.7% 81.2% 81.7%

Difference 0.0 pps 0.0 pps 0.0 pps -0.7 pps -1.7 pps -1.8 pps

YoY (pps) -0.8 pps 3.3 pps 2.0 pps -0.3 pps -0.5 pps 0.5 pps

ASK (bn) - new 13.5 16.4 20.2 24.4 28.4 33.1

ASK (bn) - old 13.5 16.4 20.2 23.8 28.0 32.8

Difference 0.0% 0.0% 0.0% 2.2% 1.4% 0.9%

YoY 26.6% 22.0% 22.7% 20.9% 16.5% 16.5%

RPK (bn) - new 10.1 12.8 16.2 19.5 22.6 26.4

RPK (bn) - old 10.1 12.8 16.2 19.2 22.7 26.8

Difference 0.0% 0.0% 0.0% 1.3% -0.7% -1.3%

YoY 25.3% 27.3% 25.9% 20.5% 15.8% 17.2%

RASK (EUR cents) - new 4.7 5.1 4.7 4.4 4.3 4.3

RASK (EUR cents) - old 4.7 5.1 4.7 4.5 4.5 4.5

Difference 0.0% 0.0% 0.0% -2.7% -5.0% -4.4%

YoY 2.6% 7.0% -7.4% -7.4% -1.3% 0.8%

Ancillenary revenue/pax (EUR) - new 5.9 7.4 8.0 9.3 10.0 11.0

Ancillenary revenue/pax (EUR) - old 5.9 7.4 8.0 9.1 10.8 11.4

Difference 0.0% 0.0% 0.0% 1.7% -7.1% -3.7%

YoY -0.6% 25.4% 8.8% 16.0% 7.8% 9.9%

CASK (EUR cents) - new 4.8 4.6 4.2 4.0 4.1 4.1

CASK (EUR cents) - old 4.8 4.6 4.2 4.1 4.1 4.1

Difference 0.0% 0.0% 0.0% -3.1% -0.1% 0.5%

YoY 6.9% -3.9% -9.1% -3.7% 2.6% 0.1%

CASK-ex fuel (EUR cents) - new 2.8 2.7 2.5 2.3 2.6 2.7

CASK-ex fuel (EUR cents) - old 2.8 2.7 2.5 2.6 2.6 2.5

Difference 0.0% 0.0% 0.0% -9.6% -0.1% 6.3%

YoY -1.6% -3.2% -10% -4.3% 10.1% 4.2%

ROAE - new -8.6% 46.1% 12.4% 12.4% 15.1% 20.0%

ROAE - old -8.6% 46.1% 12.4% 20.1% 18.9% 21.2%

Difference 0.0 pps 0.0 pps 0.0 pps -7.6 pps -3.8 pps -1.3 pps

YoY (pps) n.m 54.6 pps -33.6 pps 0.0 pps 2.7 pps 4.9 pps

Average Brent price (USD) - new 111 112 108 99 61 67

Average Brent price (USD) - old 111 112 108 103 68 80

Difference 0.0% 0.0% 0.0% -3.4% -10.6% -16.3%

Source: The Company, Garanti Securities

*Figures are based on our own calculations may differ from company's figures

*2014 old figures are our previous assumptions, new figures are actual

Revisions in model assumptions at a glance*

Please see the last page of this report for important disclosures.

19

RESEARCH

June 18, 2015

Airlines

Pegasus Airlines

As shown above, we have fine tuned some of our forecasts based on the our new macroeconomic assumptions and new guidance. We have

revised our traffic assumptions for the 2015-2016 period, while lowering

our RASK (EUR) forecasts by 5.0% and 4.4% for 2015 and 2016 while keeping our forecast for the CASK flat for 2015 but increasing it by 0.5%

for 2016. Those imply a 1% YoY lower RASK for 2015, compared to a 2.6% increase in CASK in the same period; for 2016, we expect a 0.8%

increase in the RASK and 0.1% increase in the CASK. The management

aims to post a stable yield, while securing a 3-4% increase in the CASK figures in 2015, with no change in the load factor.

While we have slightly revised our 2015-16 sales, we have trimmed our EBITDA forecast by 18% for 2015 and 14% for 2016 given the anticipated

further cost pressures f rom the exchange rate effect, change in the fleet

mix and ramp handling investments. We have slashed our net income forecasts for 2015-2016 on weaker profitability, losses f rom derivative

operations and new exchange rate assumptions.

2015E Guidance Garanti

Total Pax growth c15-17% 12%

Total ASK growth c17-19% 17%

Load Factor flat (c80%) 79%

Yields flat flat

Ancillary revenue per pax (EUR) 10 10

CASK (EUR) growth 3-4% 3%

EBITDAR margin 19-21% 18.5%

Source: The Company, Garanti Securities

Revision in Estimates

PGSUS

(TLmn) 2015E 2016E 2015E 2016E 2015E 2016E

Net Sales 3,532 4,302 3,564 4,113 1% -4%

EBITDA 444 540 363 463 -18% -14%

Net Profit 292 368 190 279 -35% -24%

EBITDA Margin 12.6% 12.6% 10.2% 11.3% -2.4% -1.3%

Net Income Margin 8.3% 8.6% 5.3% 6.8% -2.9% -1.8%

Target Price

Source: Bloomberg, Garanti Securities

OLD NEW % Change

39.80 31.65 -20%

Please see the last page of this report for important disclosures.

20

RESEARCH

June 18, 2015

Airlines

Pegasus Airlines

Bloomberg vs. Garanti Forecasts

Our forecasts are inline with the market consensus in terms of sales yet,

lower in terms of EBITDA and net income in 2015. We believe that the

consensus does not fully reflect the likely competition and further cost pressures. Different losses f rom derivative operations would be another

reason behind the deviation between net income forecasts. Meanwhile,

our target price of TL31.65 is 2% higher than the Bloomberg consensus of TL31.09.

Pegasus Airlines 1Q15 Results Review Pegasus reported a net loss of TL74mn in 1Q15, lower than the

consensus estimate of TL43mn net loss and our estimate of TL20mn net

loss. The Company generated TL583mn of revenues in the quarter – in line with both our own and the consensus estimate. EBITDA was weaker

compared to both consensus and our forecasts, yet, losses from

derivative operations and higher effective tax rate were the main reasons behind the worse than expected botomline.

Based on our calculations, EBITDAR margin turned to positive at 2% in 1Q15. The Company recorded TL82mn net other income which is driven

by FX gains in the quarter vs. TL13mn expense a year ago. Recall that, the Company’s functional currency is EUR and it has TL842mn long

position - most of which based in USD.

Pegasus recorded TL28mn losses f rom derivative operations. There was

tax expense of TL34mn (vs. TL10mn income in 1Q14) and minority

interest of TL6mn (vs. TL2mn in 1Q14) in the quarter vs. TL46mn loss before tax.

Consensus vs. Our estimates

PGSUS

(TLmn) 2015E 2016E 2015E 2016E 2015E 2016E

Net Sales 3,603 4,389 3,564 4,113 -1% -6%

EBITDA 410 485 363 463 -11% -4%

Net Profit 212 241 190 266 -11% 10%

EBITDA Margin 11.4% 11.1% 10.2% 11.3% -1.2 pps 0.2 pps

Net Income Margin 5.9% 5.5% 5.3% 6.5% -0.6 pps 1.0 pps

Target Share Price

Source: Bloomberg, Garanti Securities

Bloomberg Garanti Securities Difference

31.09 31.65 2%

Please see the last page of this report for important disclosures.

21

RESEARCH

June 18, 2015

Airlines

Pegasus Airlines

According to our calculations, domestic RASK (in TL) decreased by 3% YoY in 1Q15 (vs. 6% decline in 1Q14) while that of international was up

by 9% in EUR terms (vs. 18% decline in 1Q15). On cost front, CASK

increased by 1% in EUR terms in 1Q15 after 3% decline in 1Q14. Non-fuel CASK rose by 9% in 1Q15 due to the increased leasing expenses.

On the other hand, ancillary revenues per passenger increased by 13% to EUR10.2 and ancillary revenues accounts for 22% of total revenues in

1Q15 similar to 1Q14.

Pegasus Hava Tasimaciligi Summary Financials

(mn TL) 1Q14 2Q14 3Q14 4Q14 1Q15 1Q15/1Q14 1Q15/4Q14

Net Sales 511 800 1,109 662 583 14% -12%

Gross Profit -51 137 339 38 -35 n.m. n.m.

Operating Profit -113 81 293 -14 -93 n.m. n.m.

EBITDA -71 122 335 26 -53 n.m. n.m.

EBITDAR -30 169 384 77 11 n.m. -85%

Net Other Income/Expense -13 21 38 31 82 n.m. n.m.

Financial Inc./ Exp. (net) 9 9 -25 -190 -45 n.m. n.m.

Tax 10 -22 -60 81 -34 n.m. n.m.

Net Income -103 87 251 -92 -74 n.m. n.m.

Net Cash -758 -493 -261 -497 -408

Working Capital 87 114 82 44 82

Shareholders Equity 1,070 1,117 1,340 1,161 1,111

Ratios

Gross Margin n.m. 17.2% 30.6% 5.7% n.m. n.m. n.m.

Operating Margin n.m. 10.1% 26.4% n.m. n.m. n.m. n.m.

EBITDA Margin n.m. 15.3% 30.2% 3.9% n.m. n.m. n.m.

EBITDAR Margin n.m. 21.1% 34.7% 11.6% 2.0% n.m. -9.6 pp

Net Profit Margin n.m. 10.9% 22.6% n.m. n.m. n.m. n.m.

Change

Please see the last page of this report for important disclosures.

22

RESEARCH

June 18, 2015

Airlines

Pegasus Airlines

CASK non-fuel Analysis (EUR cents)

Source: Pegasus Airlines

2.63

2.85

0.05 0.03

0.14

2.00

2.10

2.20

2.30

2.40

2.50

2.60

2.70

2.80

2.90

3.00

2014 Q1 CASK nonfuel

Escalation on TLcost base (*)

Structural changes(**)

Fx & Other 2015 Q1 CASK nonfuel

1Q EBITDAR Evolution (TLmn)

-29.4

-4.8 10

66.9

-8.6-3.5

-19.4 11.3

-60

-40

-20

0

20

40

60

Source: Pegasus Airlines

Please see the last page of this report for important disclosures.

23

RESEARCH

June 18, 2015

Airlines

Pegasus Airlines

Source: The Company, Garanti Securities

Quarterly Figures

4.0

5.2

5.9

4.8

4.4

4.85.2

4.1

3.5

4.3

5.4

3.93.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

EU

R c

en

t

RASK

5.24.9

4.14.4 4.4

4.13.8

4.3 4.3

3.9 3.9 4.04.3

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

EU

R c

en

t

CASK

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

EU

R c

en

ts

EBITDAR margin RASK-CASK (rhs)

3.3

3.0

2.3

2.6 2.62.4

2.2

2.7 2.6

2.3 2.2 2.3

2.9

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

EUR

ce

nt

non-fuel CASK

70.0%

72.0%

74.0%

76.0%

78.0%

80.0%

82.0%

84.0%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

mn

ASK Load factor (rhs)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

RASK/CASK EUR/USD - avg (rhs)

1Q15 1Q14 YoY

4,52 4,08 10,8%

5,81 5,18 12,1%

77,8% 78,7% -0,9%

31.302 27.880 12,3%

144 146 -1,3%

5.645 4.807 17,4%

54.996 47.213 16,5%

11,6 10,9 5,7%

89 80 11,3%

Source: The Company data

Pax (mio)

Utilization

Destinations Flow n

Seat (mio)

Load factor (%)

Cycle

Pax per cycle

ASK (mio)

Block Hour

Pegasus Airlines Traffic

Please see the last page of this report for important disclosures.

24

RESEARCH

June 18, 2015

Airlines

Pegasus Airlines

Source: The Company, Garanti Securities

Yearly Figures

5.1

4.7

4.44.3 4.3

3.8

4.0

4.2

4.4

4.6

4.8

5.0

5.2

2012 2013 2014 2015E 2016E

EU

R c

en

t

RASK

4.6

4.2

4.0

4.1 4.1

3.7

3.8

3.9

4.0

4.1

4.2

4.3

4.4

4.5

4.6

4.7

2012 2013 2014 2015E 2016E

EU

R c

en

t

CASK

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2012 2013 2014 2015E 2016E

EU

R c

en

ts

EBITDAR margin RASK-CASK (rhs)

2.7

2.5

2.3

2.6

2.7

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2012 2013 2014 2015E 2016E

EUR

ce

nt

non-fuel CASK

72.0%

73.0%

74.0%

75.0%

76.0%

77.0%

78.0%

79.0%

80.0%

81.0%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2012 2013 2014 2015E 2016E

mn

ASK Load factor (rhs)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.00

1.02

1.04

1.06

1.08

1.10

1.12

1.14

2012 2013 2014 2015E 2016E

RASK/CASK EUR/USD - avg (rhs)

Pegasus Revenue exposure Pegasus Expenses exposure

Source: The Company data

EURO, 39%

USD, 15%

TL, 41%

Other, 5%

2014

EURO, 23%

USD, 56%

TL, 19%

Other, 2%

2014

25

RESEARCH

Disclaimer

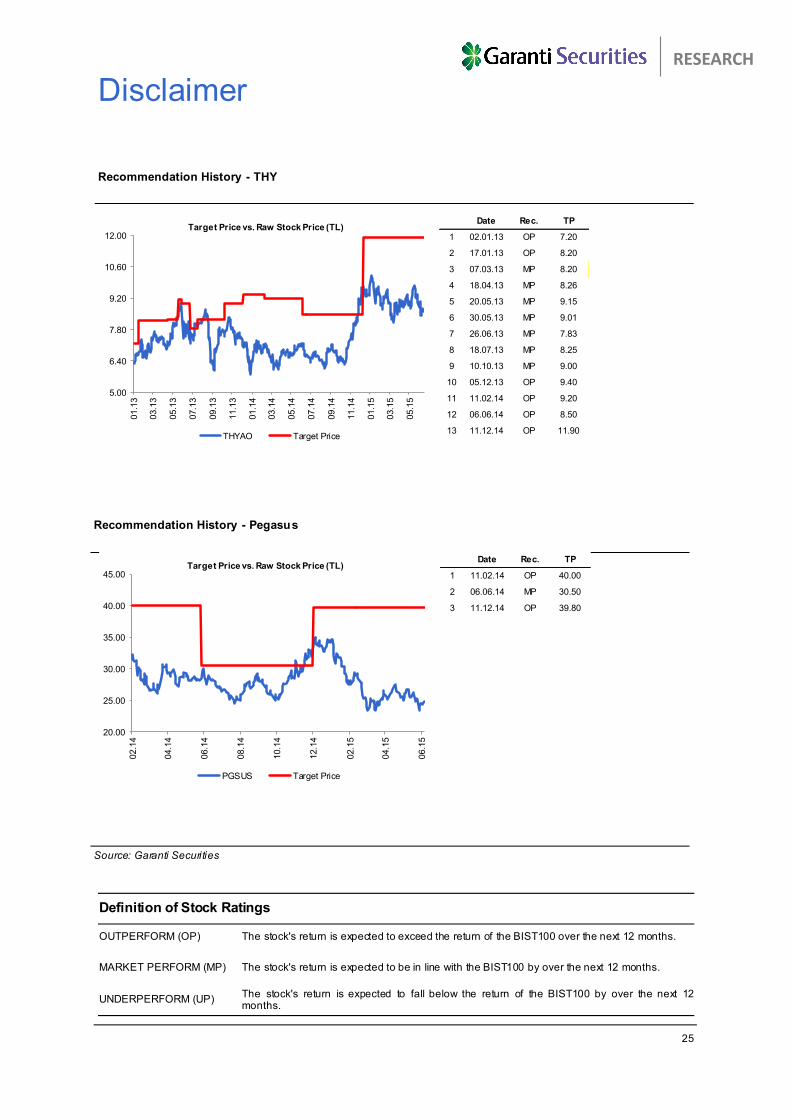

Recommendation History - THY

Definition of Stock Ratings

OUTPERFORM (OP) The stock's return is expected to exceed the return of the BIST100 over the next 12 months.

MARKET PERFORM (MP) The stock's return is expected to be in line with the BIST100 by over the next 12 months.

UNDERPERFORM (UP) The stock's return is expected to fall below the return of the BIST100 by over the next 12 months.

Recommendation History - Pegasus

Source: Garanti Securities

Date Rec. TP

1 02.01.13 OP 7.20

2 17.01.13 OP 8.20

3 07.03.13 MP 8.20

4 18.04.13 MP 8.26

5 20.05.13 MP 9.15

6 30.05.13 MP 9.01

7 26.06.13 MP 7.83

8 18.07.13 MP 8.25

9 10.10.13 MP 9.00

10 05.12.13 OP 9.40

11 11.02.14 OP 9.20

12 06.06.14 OP 8.50

13 11.12.14 OP 11.90

5.00

6.40

7.80

9.20

10.60

12.00

01.1

3

03.1

3

05.1

3

07.1

3

09.1

3

11.1

3

01.1

4

03.1

4

05.1

4

07.1

4

09.1

4

11.1

4

01.1

5

03.1

5

05.1

5

Target Price vs. Raw Stock Price (TL)

THYAO Target Price

Date Rec. TP

1 11.02.14 OP 40.00

2 06.06.14 MP 30.50

3 11.12.14 OP 39.80

20.00

25.00

30.00

35.00

40.00

45.00

02.1

4

04.1

4

06.1

4

08.1

4

10.1

4

12.1

4

02.1

5

04.1

5

06.1

5

Target Price vs. Raw Stock Price (TL)

PGSUS Target Price

Please see the last page of this report for important disclosures.

26

RESEARCH

Disclaimer

This document and the information, opinions, estimates and recommendations expressed herein,

have been prepared by Garanti Securities Research Department, to provide its customers with general information regarding the date of issue of the report and are subject to changes without prior

notice. All opinions and estimates included in this report constitute our judgment as of this date and are subject to change without notice.

This document and its contents do not constitute an offer, invitation or solicitation to purchase or subscribe to any securities or other instruments, or to undertake or divest investments. Neither shall

this document nor its contents form the basis of any contract, commitment or decision of any kind.

Investors who have access to this document should be aware that the securities, instruments or

investments to which it refers may not be appropriate for them due to their specif ic investment goals,

financial positions or risk prof iles, as these have not been taken into account to prepare this report. Therefore, investors should make their own investment decisions considering the said circumstances

and obtaining such specialized advice as may be necessary. The information in this report has been

obtained by Garanti Securities Research Department f rom sources believed to be reliable. However, Garanti Securities cannot guarantee the accuracy, adequacy, or completeness of such information,

and cannot be responsible for the results of investment decisions made on account of this report.

The market prices of securities or instruments or the results of investments could fluctuate against

the interests of investors. Investors should be aware that they could even face a loss of their investment. Transactions in futures, options and securities or high-yield securities can involve high

risks and are not appropriate for every investor. Indeed, in the case of some investments, the

potential losses may exceed the amount of initial investment and, in such circumstances, investors may be required to pay more money to support those losses. Thus, before undertaking any

transaction with these instruments, investors should be aware of their operation, as well as the rights,

liabilities and risks implied by the same and the underlying stocks. Investors should also be aware that secondary markets for the said instruments may be limited or even not exist.

This report is to be distributed to professional emerging markets investors only. This report is for private use only and intended solely for the individual(s). No information in this report may be copied,

modified, republished or exploited in anyway without the prior consent of Garanti Securities.

Additionally, with respect to our statements above, all our claims and plea rights are covered in the regulations which apply in the countries that this report has been sent to.

Garanti Securities

Etiler Mah. Tepecik Yolu

Demirkent Sokak No:1 34337 Besiktas, Istanbul / Turkey

Phone: +90 (212) 384-1155

Fax: +90 (212) 352-4240

RESEARCH

![OUTPERFORM [V] INITIATION](https://img.dokumen.tips/doc/110x75/6189e5c61eda5f71d25deb98/outperform-v-initiation.jpg)