Embed Size (px)

Citation preview

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 1/12

For auto racers, truck drivers, and youngchildren on a family road trip, pit stopsare an inevitable part of life. The mostrecent batch of U.S. economic data seemsto suggest that the economy is taking apit stop, and having to rummage underthe seats to pay the bill at the pump.Average U.S. retail gasoline prices areclosing in on $4 per gallon nationally,and are already over that in Californiaand the Midwest.

Whether it’s the psychological or finan-

cial effects of wallet-draining gasolineprices, the recent rise in oil past $110 abarrel is starting to make itself felt, andthe economy is responding. “The recoveryis still moving along,” says Standard &Poor’s Economist Beth Ann Bovino, “but

we’re starting to feel the hit from high oilprices.”

Following disappointing, and mostly dis-regarded, first-quarter gross domestic prod-uct growth of just 1.8% on an annualbasis, several recent reports also paint aless-than-robust picture of the economy’scurrent state: the ISM Nonmanufacturingindex — a measure of the increasinglyimportant service economy — fell inMarch, productivity gains slowed, and job-less claims made a surprising jump to an

eight-month high. Persistently low Treasuryyields — the yield on the 10-year note hasactually fallen in 2011 — are another signof concern about the true strength of theU.S. economy.

The OutlookIntelligence for the Individual Investor

May 11, 2011

Volume 83

Number 17

Please see page 3 for required researchanalyst certification disclosures.

For important regulatory information, pleasego to: www.standardandpoors.com and clickon “Regulatory Affairs and Disclaimers.”

Taking a Pit StopOil prices hit the U.S. economy and then pull back.

(Continued on page 10

What’s Inside

Intelligencer 2

Observatory 3

Mutual Fund Strategies 4

ETF Strategies 5

Weak Dollar 6

Nordstrom 7

Supermajor Oils 8

Marcellus Shale 9

Stock Screen 10

Master List 11

Top Ten Portfolio 12

S&P Equity ResearchRecommended AssetAllocation

Foreign

Equities

15%

U.S. Equities45%

Cash15%

Bonds25%

Vaughan ScullyS&P Editorial

S&P 500 GICS SECTOR PERFORMANCES AND RECOMMENDED SECTOR WEIGHTINGSE2011 P/E TO ACTUAL RECOMMENDED

% CHANGE P/E ON PROJ. 5-YR. SECTOR % S&P SECTOR OVER/UNS&P 500 SECTOR MAY YTD 2010 E2011 EPS EPS GROWTH WEIGHTINGS EMPHASIS WEIGH

Consumer Discretionary -0.2 8.2 25.7 15.7 1.0 10.6 Underweight -2%

Consumer Staples 0.5 7.4 10.7 15.2 1.6 10.5 Marketweight 0%Energy -3.6 13.7 17.9 13.4 1.2 12.7 Overweight +1%Financials 0.0 2.7 10.8 12.4 1.3 15.5 Marketweight 0%Health Care 0.7 12.6 0.7 12.5 1.4 11.4 Marketweight 0%Industrials -0.5 10.6 23.9 16.0 1.3 11.2 Overweight +1%Information Technology -0.6 5.6 9.1 13.7 1.0 18.1 Marketweight 0%Materials -1.6 4.5 19.9 14.4 1.5 3.6 Overweight +1%Telecommunication Services 1.3 5.6 12.3 17.7 2.9 3.0 Marketweight 0%Utilities 0.7 6.3 0.9 13.2 3.5 3.3 Underweight -1%S&P Composite 1500 -0.7 8.1 14.2 17.1 1.3S&P 500 -0.5 7.9 12.8 14.0 1.3S&P MidCap 400 -1.6 10.1 24.8 18.7 1.4S&P SmallCap 600 -2.0 7.9 25.0 19.7 1.5

Sector recommendations are market-capweighted, influenced by economic,fundamental, and technical consideration

Data as of 5/3/11. Source: Standard & Poor’s Equity Research

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 2/12

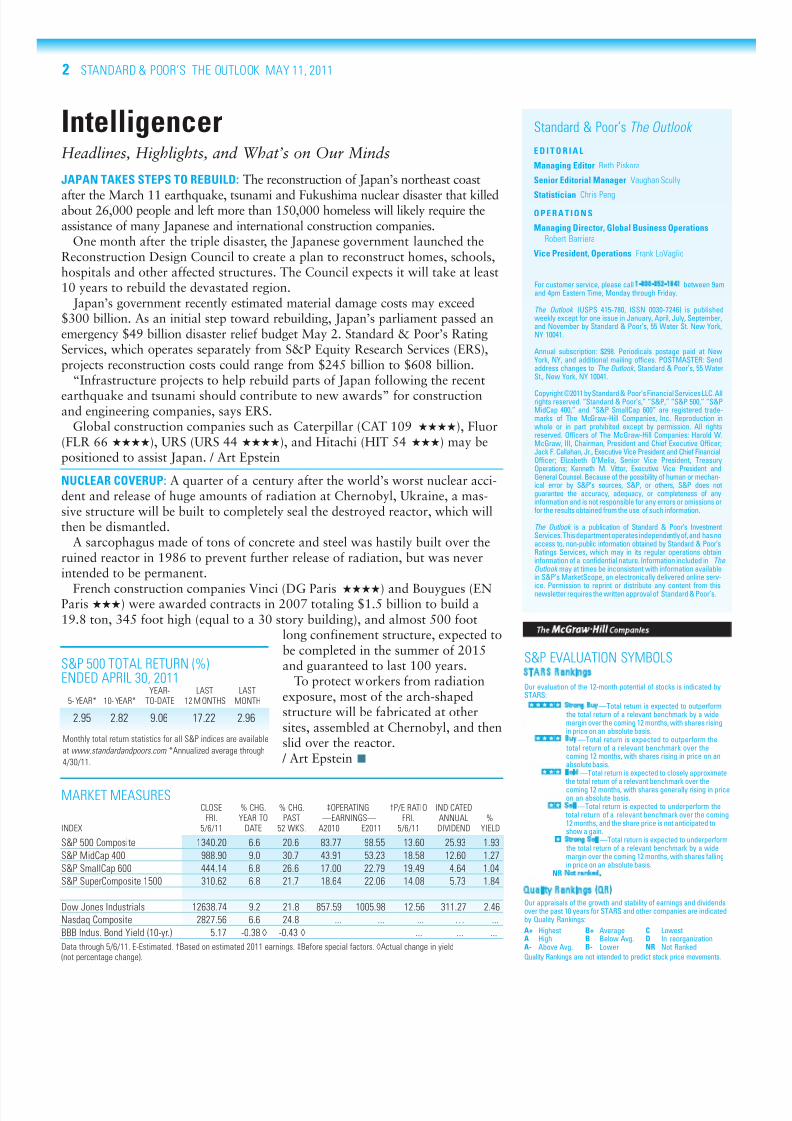

2 STANDARD & POOR’S THE OUTLOOK MAY 11, 2011

IntelligencerHeadlines, Highlights, and What’s on Our Minds

JAPAN TAKES STEPS TO REBUILD: The reconstruction of Japan’s northeast coast

after the March 11 earthquake, tsunami and Fukushima nuclear disaster that killedabout 26,000 people and left more than 150,000 homeless will likely require theassistance of many Japanese and international construction companies.

One month after the triple disaster, the Japanese government launched theReconstruction Design Council to create a plan to reconstruct homes, schools,hospitals and other affected structures. The Council expects it will take at least10 years to rebuild the devastated region.

Japan’s government recently estimated material damage costs may exceed$300 billion. As an initial step toward rebuilding, Japan’s parliament passed anemergency $49 billion disaster relief budget May 2. Standard & Poor’s RatingServices, which operates separately from S&P Equity Research Services (ERS),projects reconstruction costs could range from $245 billion to $608 billion.

“Infrastructure projects to help rebuild parts of Japan following the recent

earthquake and tsunami should contribute to new awards” for constructionand engineering companies, says ERS.

Global construction companies such as Caterpillar (CAT 109 ★★★★), Fluor(FLR 66 ★★★★), URS (URS 44 ★★★★), and Hitachi (HIT 54 ★★★) may bepositioned to assist Japan. / Art Epstein

NUCLEAR COVERUP: A quarter of a century after the world’s worst nuclear acci-dent and release of huge amounts of radiation at Chernobyl, Ukraine, a mas-sive structure will be built to completely seal the destroyed reactor, which willthen be dismantled.

A sarcophagus made of tons of concrete and steel was hastily built over theruined reactor in 1986 to prevent further release of radiation, but was neverintended to be permanent.

French construction companies Vinci (DG Paris ★★★★) and Bouygues (ENParis ★★★) were awarded contracts in 2007 totaling $1.5 billion to build a19.8 ton, 345 foot high (equal to a 30 story building), and almost 500 foot

long confinement structure, expected tobe completed in the summer of 2015and guaranteed to last 100 years.

To protect workers from radiationexposure, most of the arch-shapedstructure will be fabricated at othersites, assembled at Chernobyl, and thenslid over the reactor.

/ Art Epstein ■

S&P EVALUATION SYMBOLSSTARS Rankings

Our evaluation of the 12-month potential of stocks is indicated bySTARS:

Strong Buy—Total return is expected to outperform the total return of a relevant benchmark by a widemargin over the coming 12 months, with shares risingin price on an absolute basis.Buy—Total return is expected to outperform the

total return of a relevant benchmark over thecoming 12 months, with shares rising in price on anabsolute basis.Hold—Total return is expected to closely approximate

the total return of a relevant benchmark over thecoming 12 months, with shares generally rising in priceon an absolute basis.Sell—Total return is expected to underperform the

total return of a relevant benchmark over the coming12 months, and the share price is not anticipated toshow a gain.Strong Sell—Total return is expected to underperform

the total return of a relevant benchmark by a widemargin over the coming 12 months, with shares fallingin price on an absolute basis.

NR Not ranked.

Quality Rankings (QR)Our appraisals of the growth and stability of earnings and dividendsover the past 10 years for STARS and other companies are indicatedby Quality Rankings:

A+ Highest B+ Average C LowestA High B Below Avg. D In reorganizationA- Above Avg. B- Lower NR Not Ranked

Quality Rankings are not intended to predict stock price movements.

S&P 500 TOTAL RETURN (%)ENDED APRIL 30, 2011

Monthly total return statistics for all S&P indices are available

at www.standardandpoors.com . *Annualized average through

4/30/11.

YEAR- LAST LAST5-YEAR* 10-YEAR* TO-DATE 12 MONTHS MONTH

2.95 2.82 9.06 17.22 2.96

MARKET MEASURESCLOSE % CHG. % CHG. ‡OPERATING †P/E RATIO INDICATED

FRI. YEAR TO PAST —EARNINGS— FRI. ANNUAL %INDEX 5/6/11 DATE 52 WKS. A2010 E2011 5/6/11 DIVIDEND YIELD

S&P 500 Composite 1340.20 6.6 20.6 83.77 98.55 13.60 25.93 1.93

S&P MidCap 400 988.90 9.0 30.7 43.91 53.23 18.58 12.60 1.27

S&P SmallCap 600 444.14 6.8 26.6 17.00 22.79 19.49 4.64 1.04

S&P SuperComposite 1500 310.62 6.8 21.7 18.64 22.06 14.08 5.73 1.84

Dow Jones Industrials 12638.74 9.2 21.8 857.59 1005.98 12.56 311.27 2.46

Nasdaq Composite 2827.56 6.6 24.8 ... ... ... … ...

BBB Indus. Bond Yield (10-yr.) 5.17 -0.38 ◊ -0.43 ◊ ... ... ...

Data through 5/6/11. E-Estimated. †Based on estimated 2011 earnings. ‡Before special factors. ◊Actual change in yield(not percentage change).

E D I T O R I A L

Managing Editor Beth Piskora

Senior Editorial Manager Vaughan Scully

Statistician Chris Peng

O P E R A T IO N S

Managing Director, Global Business Operations

Robert Barriera

Vice President, Operations Frank LoVaglio

Standard & Poor’s The Outlook

For customer service, please call 1-800-852-1641between 9amand 4pm Eastern Time, Monday through Friday.

The Outlook (USPS 415-780, ISSN 0030-7246) is publishedweekly except for one issue in January, April, July, September,and November by Standard & Poor’s, 55 Water St. New York,NY 10041.

Annual subscription: $298. Periodicals postage paid at NewYork, NY, and additional mailing offices. POSTMASTER: Sendaddress changes to The Outlook , Standard & Poor’s, 55 WaterSt., New York, NY 10041.

Copyright ©2011 by Standard & Poor’s Financial Services LLC. Allrights reserved. “Standard & Poor’s,” “S&P,” “S&P 500,” “S&PMidCap 400,” and “S&P SmallCap 600” are registered trade-marks of The McGraw-Hill Companies, Inc. Reproduction inwhole or in part prohibited except by permission. All rightsreserved. Officers of The McGraw-Hill Companies: Harold W.McGraw, III, Chairman, President and Chief Executive Officer;Jack F. Callahan, Jr., Executive Vice President and Chief FinancialOfficer; Elizabeth O’Melia, Senior Vice President, TreasuryOperations; Kenneth M. Vittor, Executive Vice President andGeneral Counsel. Because of the possibility of human or mechan-ical error by S&P’s sources, S&P, or others, S&P does notguarantee the accuracy, adequacy, or completeness of anyinformation and is not responsible for any errors or omissions orfor the results obtained from the use of such information.

The Outlook is a publication of Standard & Poor’s InvestmentServices. This department operates independently of, and has noaccess to, non-public information obtained by Standard & Poor’sRatings Services, which may in its regular operations obtaininformation of a confidential nature. Information included in The

Outlook may at times be inconsistent with information availablein S&P’s MarketScope, an electronically delivered online serv-

ice. Permission to reprint or distribute any content from thisnewsletter requires the written approval of Standard & Poor’s.

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 3/12

STANDARD & POOR’S THE OUTLOOK MAY 11, 2011 3

For daily STARS changes, subscribers can call The Outlook hotline, 800-618-7827, and put in your subscriber access code.

S&P Observatory provides a selection of analytical actions — upgrades, downgrades, initiations — from S&P Equity Research. Stoc ks featured in S&PObservatory are selected by The Outlook according to factors including, but not limited to, newsworthiness, capitalization, and inclusion in a portfolio publishedby The Outlook . Please note that all investments carry risks. Investors should seek financial advice before investing.

All of the views expressed in this research report accurately reflect the research analysts’ personal views regarding any and a ll of the subject securities or issuers.No part of the analysts’ compensation was, is, or will be, directly or indirectly , related to the specific recommendations or v iews expressed in this research report.

AGL Resources AGL 41 2 3 5/4/11 A

Airtran Holdings AAI 7 NR 3 5/2/11 C

Alaska Communications ALSK 9 2 1 4/29/11 B

Alpha Natural Resources ANR 52 3 4 5/3/11 NR

Armstrong World AWI 46 4 3 5/2/11 NR

Avon Products AVP 29 3 2 5/3/11 A-

Chart Industries GTLS 49 4 3 5/4/11 NR

Compass Minerals International CMP 92 3 2 5/2/11 NR

Electronic Arts ERTS 21 2 1 5/5/11 B+

Entertainment Properties EPR 47 3 2 5/3/11 A-

Fidelity National Information FIS 33 3 4 5/2/11 NR

Fresenius Medical Care FMS 73 3 4 5/4/11 NR

Hain Celestial HAIN 35 3 2 5/4/11 B-

Human Genome Sciences HGSI 28 3 4 4/29/11 C

Innophos IPHS 44 4 3 5/3/11 NR

Kyocera KYO 109 4 5 5/3/11 NR

LDK Solar LDK 10 4 5 5/2/11 NR

Leggett & Platt LEG 26 4 2 4/29/11 B

Magna International MGA 51 5 4 5/4/11 B

Massey Energy MEE 62 3 4 5/3/11 B-

MasterCard MA 278 3 4 5/3/11 NR

Merck MRK 36 4 3 4/29/11 B

Monolithic Power Systems MPWR 16 4 5 4/29/11 NR

Monro Muffler Brake MNRO 30 3 2 5/3/11 B+

Oneok Partners OKS 82 4 3 5/4/11 NROverseas Shipholding OSG 30 3 4 5/4/11 B

Potash POT 54 4 3 4/29/11 B+

priceline.com PCLN 539 3 2 5/5/11 B

Regeneron Pharmaceuticals REGN 48 3 4 5/3/11 C

Rowan RDC 38 4 3 5/4/11 B-

Sears SHLD 78 2 3 5/3/11 NR

Shanda Interactive Entertainment SNDA 45 3 2 5/3/11 NR

Silgan SLGN 45 4 3 5/4/11 B+

Skywest SKYW 16 3 4 5/4/11 B+

Sonus Networks SONS 3 3 4 5/4/11 B

Sun Healthcare Group SUNH 11 4 3 4/29/11 NR

Tenneco TEN 43 4 3 5/4/11 C

Timberland TBL 29 4 3 5/5/11 BTrimble Navigation TRMB 43 2 3 4/29/11 B

Varian Semiconductor VSEA 61 3 4 5/5/11 B

WebMD WBMD 56 4 5 5/2/11 B-

Westlake Chemical WLK 59 4 3 5/4/11 NR

STARSCURRENT NEW OLD CHANGE QUALITY

NAME SYMBOL PRICE ($) STARS STARS DATE RANK

The ObservatorySelected actions for April 29 through May 5.

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 4/12

4 STANDARD & POOR’S THE OUTLOOK MAY 11, 2011

Looking around shops these days,it’s hard not to notice that pricesfor many of the items we useevery day have increased recently,some dramatically.

Grocery shopping is one areaof noticeably higher prices, as aregas stations. S&P’s Economicsteam forecasts a rise in consumer

prices, as measured by the con-sumer price index, of 2.9% in2011 and 2.1% in 2012 after twoyears of only modest increases.For those concerned about theeffect of rising prices on the pur-chasing power of investmentincome, investing in TreasuryInflation-Protected Securities(TIPS) may be a solution worthyof consideration. TIPS provideprotection against inflation byadjusting their principal value

according to changes in the con-sumer price index.

To identify some attractiveTIPS funds, we looked for fundthat were a leader in one of four different categories: the topperformer over the past threeyears, the lowest standard devi-ation for reduced volatility, thelowest costs (as measured bynet expense ratio), and the high-est 30-day SEC yields. Weexcluded institutional shareclasses as well as those closed tonew investors.

PIMCO Real Return FundWhen we search for top per-

forming funds over the threeyears ended April 29, PIMCOReal Return Fund stands out.Over that span, it has returned6.11% annually, outpacing theaverage TIPS fund by more than150 basis points. It also bested its

peers over one, five, and ten-yeartime frames, as well as since itsinception in January, 1997. Thefund’s net expense ratio of 0.90%is comparable to its peers’ aver-age of 0.83%, though we note itdoes have a maximum sales loadof 3.75%.

Franklin Real Return FundInvestors who are more con-

cerned about the volatility of theirfunds may want to take a look at

Franklin Real Return Fund, whichhas a standard deviation that isabout 30% below the peer aver-age. Additionally, the fund man-aged to outpace its peers over thetrailing five-year period endedApril 29 on an annualized basisby about 20 basis points, althoughit has trailed the group over thepast three years. Like the PIMCOfund, it has a Sharpe ratio that ishigher than the group. Its expenseratio of 0.90% is slightly abovethe peer average, and it sports amaximum sales load of 4.25%.

Vanguard Inflation-Protected

Securities FundThe low-cost option is unques-

tionably the Vanguard Inflation-Protected Securities Fund.Specifically, its net expense ratioof 0.22% is well below the peergroup average of 0.83%, and ithas no sales load. We also note

the turnover rate of 29% is abouta quarter of the TIPS funds’ aver-age of 115%. Despite its lowcosts, the fund outpaced thegroup over the three years endedApril 29 by nearly 50 basis pointson an annualized basis. Thefund’s standard deviation andSharpe ratio are both in line withthe TIPS funds average.

TIAA-CREF Inflation-Linked

Bond Fund

This fund had a 30-day SECyield of 5.2% as of March 31,which compares very favorablywith the group’s average of 3.2%.Given its much higher-than-peersyield, it is no surprise that thisfund outdistanced its peers on anannualized basis over the trailingone-, three-, and five-year timespans. Moreover, it accomplishedthis with a net expense ratio of 0.49%, notably below the peeraverage. Finally, its standard devi-ation and Sharpe ratio are com-parable to the group. ■

Inflation at the ‘TIPS’ing PointFour funds for the inflation weary investor.

Dylan CathersS&P Mutual Fund Analyst

FUND

STRATEGIES

POSITIVE POTENTIAL IMPLICATIONSGROSS

S&P *TOTAL RETURN CURRENT EXPENSE **YIELDFUND NAME / TICKER RANKING YTD 1-YEAR 3-YEAR 5-YEAR PRICE RATIO %

Franklin Real Return Fund; A / FRRAX NR 2.94 7.46 3.7 5.53 11 1.08 2.1

PIMCO Real Return Fund; A / PRTNX NR 4.32 7.73 5.97 7.02 12 0.93 4.1

TIAA-CREF Inflation-Linked Bond; Retail / TCILX NR 4.65 7.64 4.94 6.35 11 0.48 5.2

Vanguard Inflation-Protected Securities; Inv. / VIPSX NR 4.63 7.84 5.03 6.56 14 0.25 NA

Data through 5/5/11. *Total returns include reinvested dividends and capital gains, all annualized; calculations do not reflect the effect of sales charges. **As of 3/31/11.

NA-Not available. Source: S&P MarketScope Advisor.

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 5/12

STANDARD & POOR’S THE OUTLOOK MAY 11, 2011 5

Standard & Poor’s EquityStrategy believes a low dollarenvironment is likely to keepdriving gains for domestic equitysectors that have outperformedthus far in 2011, and viewsexchange traded funds that ownAmerican Depositary Receipts of shares in companies in foreign,

developed world economies as agood way to play a the dollar’sweakness.

Cyclical sectors with largeglobal revenue footprints havebeen the leaders of the domesticequity market so far this yearand are likely to stay ahead of the pack in the coming months,according to S&P EquityStrategy. Those sectors includematerials, information technolo-gy, industrials, and energy, most

of which are also benefiting fromhigher commodity prices.

“Large cap stocks, which havebeen in the cat-bird seat benefit-ing from a high percentage of non-U.S. earnings, large cashpositions, and an ability to raiseinvestor-friendly dividends, willlikely continue to outperform,with late economic-cycle sectorsdoing the best,” says StephenBiggar, global director of S&Pequity research.

Those sectors maximize lever-age to strong emerging-marketdemand and dollar weakness and,as a result, are enjoying thebiggest positive first-quarter earn-ings-per-share growth revisions.They are also expected to chalkup the largest year-over-yearearnings gains, according to S&PEquity Strategy.

On the flip side, other domesticsectors have seen their profit out-

looks barely budge while somehave seen a downward revision,namely the consumer discre-tionary, financials, telecommuni-cations, and utilities sectors. Inaddition, despite a large globalpresence, positive earnings revi-sions for consumer staples com-panies have been tempered by ris-

ing input costs.S&P International Equity

Strategist Alec Young believesthat one of the best ways to playdollar weakness is to invest in abasket of foreign stocks, espe-cially in developed markets, suchas Europe.

“When U.S. investors buyAmerican depositary receipts(ADRs), or foreign equityexchange-traded funds (ETFs),their returns are boosted when

overseas currencies rise againstthe U.S. dollar,” Young explains.

As the greenback declined,developed international equitiesenjoyed a major currency tailwind,rising by 8.4% in U.S. dollars forthe year through April 29 com-pared to a much smaller 1.8%gain in local currency terms.Meanwhile, emerging-marketequities enjoyed a much smallerforeign-currency tailwind of only3.7%, rising 4.6% in U.S. dollarvs. 0.9% in local currency terms.

There are currently a dozen orso ETFs that invest in interna-

tional (global ex-US) markets forwhich S&P has an “Overweight”recommendation, most of whichtracking indices of large-cap,developed world stocks. Two of those funds stand out for theircombination of strong 1-yearperformance, high yield, and lowannual expense ratio.

The SPDR DJ Euro Stoxx 50ETF, which invests in some of the50 largest European companies,has the strongest 12-monthreturn (23.6%) among interna-tional ETFs with an Overweightrank, as well as one of the fivehighest yields and five lowestannual cost. Its top three hold-ings as of May 3rd were Frenchoil supermajor Total (TOT 60★★★★), German industrial con-glomerate Siemens (SI 138 NR),

and Spanish telecom giantTelefonica (TEF 25 ★★★★).

The Vanguard FTSE All WorldEx-US ETF is more diversified,with more than 2300 individualholdings. Its 1-year return of 19.34% ranks sixth among inter-national ETFs rankedOverweight, and its annualexpenses are among the lowest of similar funds. Its top three hold-ings as of March 31 were globalmining and resources companyBHP-Billton (BHP 94 NR), RoyalDutch Shell (RDS.A 73 ★★★),and Nestle (NSRGY 62 NR). ■

ETFs for a Weak Dollar EnvironmentS&P sees large-cap, developed world companies as a good bet.

Isabelle SenderS&P Editorial

ETF

STRATEGIE

POSITIVE POTENTIAL IMPLICATIONS

SPDR DJ Euro Stoxx 50 ETF / FEZ MW 14.6 28.7 -7.4 0.3 43 0.29

Vanguard FTSE All-World ex-US ETF / VEU OW 4.4 23.1 -2.7 NA 51 0.22

Data through 5/5/11. *Total returns include reinvested dividends and capital gains, all annualized; calculations do not

reflect the effect of sales charges. OW-Overweight. NA-Not available. Sources: S&P MarketScope Advisor.

S&P *TOTAL RETURN CURRENT EXPENSE

FUND NAME / TICKER RANKING YTD 1-YEAR 3-YEAR 5-YEAR PRICE RATIO

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 6/12

6 STANDARD & POOR’S THE OUTLOOK MAY 11, 2011

The weakness of the U.S. dollar hasraised concern about the health of theU.S. economy and the potentially infla-tionary consequences of flooding themarket with billions of U.S. dollars tokeep interest rates low. It has alsoserved to boost revenue for companiesthat derive a significant portion of their revenue from overseas markets,since a weak dollar magnifies the valueof sales earned in a stronger currency.

A further decline in the value of theU.S. dollar against key trading part-

ners would benefit some stocks andsectors while hurting others, S&PEquity Research believes. Oil produc-ers and service companies would ben-efit, for example, while refiners mightsuffer. Apparel retailers could take ahit, but a weak dollar would proba-bly be a net positive for consumerstaples. Export oriented chemicals,industrials, and technology companiesmight gain, as would gold miners.

“A depreciating dollar is normallyassociated with rising oil prices,”says Michael Kay, the S&P equityanalyst who follows integrated oilcompanies. “In turn, rising oil pricescan be a catalyst for integrated oilsand the exploration and productioncompanies, which are leveraged tocrude prices. The risk, of course, isoil prices rising so far that theychoke off demand.” So far, that hasnot been the case, he says, and hisfundamental outlook for the inte-grated oil and gas industry for the

next 12 months is positive.Oil services companies benefit as aweakening dollar drives up long-term expectations for high crudeprices, since it is those expectationsthat give exploration and productioncompanies the confidence to startnew, capital-intensive projects.

“Even a modest reversal in the dol-lar, which would suggest a downtickin oil prices, would not change senti-ment,” says Stewart Glickman, S&P’s

head of energy equity analysis. “Oilprices would have to collapse, per-haps down to the $65-70 per barrellevel, for upstream companies to startreconsidering some of their moreexpensive projects, such as drilling inultra-deepwater.”

U.S.-based oil refiners that do nothave their own production will haveto spend more to buy importedcrude oil if the dollar weakens fur-ther, says S&P energy equity analystTanjila Shafi. That tends to narrow

profit margins and weaken demandas the costs are passed on to con-sumers in the form of higher retailgasoline prices and other refinedproducts.

“The concern here is what happensif retail prices rise so far as to chokeoff demand,” she says. “To theextent that a rising dollar signals animproving economy and improvingdemand, refiners would benefit froma stronger, not a weaker, dollar.”

As consumers face more “pain atthe pump,” they may cut back onspending in other areas. Some retailersare already feeling the effect in theirsame-store sales statistics, says MarieDriscoll, S&P’s head of consumer dis-cretionary-retail equity analysis. S&P’sfundamental outlook for apparelretailer stocks is neutral. Driscoll seesonly a modest 3%-4% rise in sales forspecialty retailers this year and has a

neutral outlook for apparel retailers.For consumer staples companies,

many of which garner significant rev-enues overseas, it’s a more complicat-ed story. Profits from overseas salesmay rise, says Tom Graves, S&P’shead of consumer staples, but somecompanies already have currencyhedges in place, and a correspondingrise in oil prices may drive up a widerange of input costs, he says. “Puttingall the variables together, we view aweaker dollar as a net positive for

U.S.-based multinational consumerstaples companies,” Graves says.

Exports are a big business forchemicals, industrial, and technologycompanies, who would gain fromfurther dollar weakness. “We thinkmultinational technology companieshave been benefiting from a weakdollar,” says Scott Kessler, S&P’shead of technology equity research.“Their non-U.S. customers havebeen able to more easily afford andspend on offerings, and tax rates onrelated profits tend to be lower.”

Lastly, a persistent decline in thedollar would boost gold and goldstocks, according to Leo Larkin,S&P’s metals equity analyst. “Steelcompanies would also benefit,because a lower dollar would makesteel imports more expensive andenable U.S. steel companies to gainshare against foreign competition.” ■

The Weak Dollar: Sector by SectorWho wins, who loses in a weak dollar environment.

Beth PiskoraS&P Editorial

US DOLLAR PERFORMANCE VS. A BASKET OF SIX MAJOR CURRENCIES5

0

5

0

5

0

M a y ‘ 1 0

J u n ’ 1 0

J u l ‘ 1 0

A u g ’ 1 0

S e p t ‘ 1 0

O c t ’ 1 0

N o v ‘ 1 0

D e c ’ 1 0

J a n ‘ 1 1

F e b ’ 1 1

M a r ‘ 1 1

A p r ’ 1 1

M a y ‘ 1 1

Source: S&P ER, Bloomberg.

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 7/12

STANDARD & POOR’S THE OUTLOOK MAY 11, 2011 7

We see fashion retailer Nordstrombenefiting from improved consumerconfidence and a correspondingincrease in discretionary spending byits higher-income customers. We alsothink the company is successfullymeeting the needs of value-seekingshoppers through expansion in theoff-price retail channel. Nordstrom’svaluation is compelling; based onour 12-month target price of $57,the shares have implied potentialappreciation of about 20% from

recent levels.Nordstrom has a multi-channel

retail strategy with 116 full-linestores, Nordstrom Direct(www.nordstrom.com), and 91 off-price Nordstrom Rack stores as of April 8, 2011. With Nordstrom’semphasis on high-quality merchan-dise and customer service, we believeit is increasing its “wallet share”among affluent baby boomers whomwe consider to be its core customers.

We also think it is attracting youngercustomers through a broader offer-ing of contemporary fashions, anenhanced online shopping experi-ence, and investments in technologysuch as the recent addition of in-store WiFi access and mobile checkout now in testing.

As part of its efforts to improvethe online customer shopping experi-ence, Nordstrom acquiredHauteLook, Inc., a leader inthe online private sales mar-

ketplace, for $180 million incompany stock in March2011. Meanwhile,Nordstrom is using theNordstrom Rack business toexpand its presence in exist-ing markets and to enternew markets (e.g., Delawarein April 2011). We believethere is limited overlapbetween Nordstrom andRack customers.

While Nordstrom has been nega-tively impacted in past years by thedownturn in the U.S. economy,channel diversification has proved tobe a plus for the company, as theweak performance from Nordstrom’sfull-line stores was partially offset byrelative strength in NordstromDirect and the Rack stores.

By delivering the merchandise itscustomers want, however they wantto shop, and at the prices they arewilling to pay, we expect the compa-

ny to sustain its positive same-storesales momentum, maintain above-peer margins, and capture marketshare in its fiscal 2012 year whichbegan on January 30. We seeNordstrom’s retail sales increasing by9% in fiscal 2012 to $10.1 billion,supported by 5% growth in totalsame-store sales and new store open-ings. We expect the company tomaintain positive momentum in itsNordstrom and Rack businesses by

focusing on its most productivebrands, by flowing receipts more fre-quently in-season to create a sense of newness for shoppers, and by makingfurther improvements to the customershopping experience.

We look forabout a4% gainin retail

selling square footage in fiscal 2012,based on Nordstrom’s plan to openthree new Nordstrom full-line storesand 17 new Rack stores, and to relo-cate two Rack stores. We expectcredit card revenue growth to mod-erate as improving economic condi-tions support a recovery in customerpayment rates. All told, we see rev-enue climbing 8% to $10.5 billion.

We project a flat gross margin ratein fiscal 2012. We expect close align-ment of inventory with sales trends to

support full-price selling. However,occupancy costs will be higher due tonew stores. The rapidly growing Rackbusiness also has a lower gross mar-gin rate than the Nordstrom business.

While Nordstrom plans to increasetechnology and marketing spendingto improve the customer shoppingexperience, we expect operating mar-gins to expand to 8.6% in fiscal 2012from 7.8% in fiscal 2011, supportedby cost controls, expense leverage off

projected same-store sales growth,and improvement in credit trends.Assuming no share activity under thecompany’s existing $411 millionrepurchase authorization, we estimateearnings per share of $3.15 in fiscal2012, versus $2.75 in fiscal 2011.

Over the past 10 years,Nordstrom has traded in aforward price/earnings ratio of 6.4 to 22.7 times earnings.Given our view that the com-pany is capturing market share

through superior multi-channel merchandising andcustomer service, we think theshares deserve to trade at thehigher end of that range, aswell as at premium to the 15.6peer group median. Applyinga forward P/E multiple of 18our fiscal 2012 earnings pershare estimate of $3.15, wearrive at our 12 month targetprice of $57. ■

Nordstrom Gains from Online, Discount StoresNordstrom Rack, online store bring upscale retailer new customers.

Jason AsaedaS&P Equity Analyst

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 8/12

8 STANDARD & POOR’S THE OUTLOOK MAY 11, 2011

First-quarter earnings for several of the “supermajor” oil companiesare in, and the high price of oil isgenerating super-sized profits. Overthe past year alone, the price of oilhas jumped more than 30% andnow stands well above $100 a bar-rel. Comparisons are being drawnwith mid 2008, when oil hit $147a barrel.

According to the U.S. EnergyInformation Administration (EIA),the global economic recovery is

boosting gasoline and diesel fuelconsumption, which says crude oiland liquid fuels consumption roseby an estimated 2.3 million barrelsper day (bbls/d) in 2010 to arecord-high 86.7 million bbls/d.EIA expects world liquid fuels con-sumption will rise by another 1.5million bbls/d in 2011 and an addi-tional 1.6 million bbls/d again in2012. EIA sees oil markets tighten-ing as rising world oil demand out-paces supply growth from oil pro-ducing countries outside of theOrganization of the PetroleumExporting Countries (OPEC).

Political protests in NorthernAfrica and the Middle East,increased scarcity of worldwide oilsupplies, and rising U.S. refiningcosts all helped push gasoline priceshigher, says Standard & Poor’sEquity Research Services (ERS), con-tributing to the huge profits forsupermajor oil companies.

ExxonMobil, one of the world’s

largest oil and gas companies, sawits profits balloon 69% to $10.65billion in the first quarter, or $2.14per share. In response, S&P equityanalyst Michael Kay raised his fullyear earnings estimate by 24% to$8.75 per share, and his 2012 esti-mate by 25% to $9.70 per share.He also raised his target price forshares in ExxonMobil to $103, cit-ing “upward pressure on pricesand volume as catalysts.” Risks tothe recommendation and target

price include deterioration in eco-nomic, industry, and operatingconditions, such as difficultyreplacing reserves or increasedproduction costs.

First-quarter earnings forNetherlands-based Royal DutchShell jumped 41% to $6.93 billion$2.04 per American Depositoryshare, above Kay’s estimate. Kayraised his estimates for full yearearnings in 2011 and 2012 as well ashis target price. He kept his “Hold”recommendation on the shares, how-ever, because the company has rela-tively large exposure to natural gasand “challenges await as it is in themidst of an $8B restructuring to sell15% of refining capacity in Africaand the European Union.” Risks tothe recommendation include a pro-longed global recession, geopoliticalrisks, inflation, lower crude oilprices, operational problems, and/oracts of terrorism.

Chevron followed closely behind,

reporting a first-quarter earningsgain of 36% to 46.21 billion. Kayraised his estimates and target pricefor Chevron as well and kept his“Strong Buy” recommendation onthe shares. Risks to the target priceand recommendation include weakereconomic, industry, and operatingconditions. In February, Chevronlost a court case in Ecuador and wasordered to pay damages of about$8.6 billion. The company hasappealed what it calls an “illegiti-

mate” decision and countersued inNew York. Kay sees little near-termimpact since the company has nooperations there.

Profits of French oil giant Totallagged behind the above companies,but were still a hefty $4.2 billion,34% above the prior-year period onrising hydrocarbon prices, accord-ing to the company. “Growinggeopolitical tensions and the after-math of the earthquake in Japanwill shift the balance of the globalenergy markets,” Total’s Chairmanand CEO Christophe de Margeriesaid in the earnings release. “In theface of these new challenges, Totalconfirms its strategy of investing toincrease its production to betterrespond to changes in energydemand and in the energy mix.”Kay also raised his 2011 earningsper share estimate for Total, andlifted his target price by $4 to $69.He has a “buy” recommendation

on the stock. ■

Supermajor Oils See Profit SurgeHigh oil prices drive strong gains in first-quarter earnings.

Art EpsteinS&P Editorial

POSITIVE POTENTIAL IMPLICATIONS12-MONTH

‡QUALITY CURRENT TARGET †P/E YIELDCOMPANY / TICKER ‡STARS RANKING *RISK STYLE PRICE PRICE RATIO (%)

• Chevron / CVX 5 A Low Blend 103 128 7.8 3.0

• ExxonMobil / XOM 5 A+ Low Blend 83 103 9.5 2.3

Royal Dutch Shell / RDS.A 3 NR Low Foreign 73 83 7.4 3.9

Total / TOT 4 NR Low Foreign 60 69 8.1 4.4

• Master List issue. *Based on our analysts’ assessment of qualitative factors, including financial strength, potential share vol atility, competitive position, industry cyclicality, regulatory/legal issues, and

other factors. Please note that all investments carry risks. ‡See definitions on page 2. †Based on S&P estimated fiscal 2011 ea rnings. Source: S&P Equity Research.

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 9/12

STANDARD & POOR’S THE OUTLOOK MAY 11, 2011 9

Natural gas production from theMarcellus Shale — a roughly 95,000square mile area extending fromWest Virginia through Ohio intoNew York — is growing rapidly,bringing a large new source of sup-ply onto the market and helping tokeep gas prices low. This is having apotent impact on natural gas pro-ducers and utilities, as well as inde-pendent power producers that burnnatural gas to generate electricity.

Standard & Poor’s Equity Research

believes that gas wells in theMarcellus shale are delivering strongreturns to producers, keeping activitylevels high despite the weak priceenvironment. Gas utilities and mid-stream storage companies in the areaare benefitting from the new supplyas well, but independent power pro-ducers are being hurt as low naturalgas prices hold down electricityprices and hurt their revenue.

According to the Pennsylvania

Department of EnvironmentalProtection, total Marcellus Shalenatural gas production in the last sixmonths of 2010 was 256.4 billioncubic feet (Bcf), compared with194.6 Bcf in the full year ended June2010.

National Fuel Gas, through itsSeneca Resources subsidiary,increased its daily production of Marcellus shale gas from nothing atthe beginning of October 2009, to53 million cubic feet equivalent

(MMcfe) by November 2010. Senecaplans to increase annual production

to 25 to 30 Bcfe in 2011, from 7.2Bcfe in 2010. NFG’s gas transporta-tion and storage business is likely tobenefit from opportunities to buildnatural gas gathering pipelines,expand existing pipelines, andexpand compression capabilities. Asof November 2010, NFG planned tospend close to $500 million on suchprojects through 2013.

NiSource owns mineral rights inthe Marcellus shale and is leasingthose rights to exploration and pro-

duction companies. NiSource alsoplans to spend $2 billion through2014 on gas gathering, transporta-tion, storage and other projects.These projects may help position thecompany to raise its dividend, whichwe project will not occur until 2016.

EQT Corp has 12.2 Tcfe (Trillion)in proved, probable, and possiblereserves in 520,000 acres in theMarcellus shale, accounting for 58%of the company’s total. Its midstream

business is adding gas gatheringpipelines and is expanding itsEquitrans pipeline in West Virginia.EQT’s $970 million of 2011 plannedcapital spending is focused mostly onexploration and production (about$700 million), but also targets asignificant amount of spending on itsmidstream business (about $235million).

One utility we see benefitting fromincreased Marcellus shale develop-ment is UGI Holdings. We believe

UGI’s service area, located in thenorthern and eastern portions of

Pennsylvania’s Marcellus Shale terri-tory, will allow the company to con-nect gathering pipelines to UGI’sutility mains and subsequently inter-state pipelines. UGI is teaming upwith NiSource to build a pipeline toprovide Marcellus Shale producers inPennsylvania better access to high-value northeastern markets. UGIplans to spend $300 million onMarcellus shale development by2013, and we expect additional proj-ects to be announced.

On the flip side, we believe thathigh natural gas storage levels andnew production coming from theMarcellus Shale will keep natural gasprices from rising dramatically in thenear future. Independent power pro-ducers (IPPs) have been struggling todeal with relatively low power pricesduring times of peak usage. Whenfuel costs decline, power marketprices also decline, forcing powerproducers sell their uncontracted

capacity at lower prices. S&P seesnatural gas prices staying below $5per MMcf through the end of 2012.

In addition to the positive impacton specific gas utilities listed above,we think relatively low gas pricescould have a negative affect on AES(AES 13 ★★★★), TransAlta (TAC 22★★★), GenOn (GEN 4 ★★★★),NRG Energy (NRG 24 ★★★), andDynegy (DYN 6 ★). We thinkDynegy may even violate debtcovenants due to lower earning

power caused in part by weak gasand power prices. ■

Marcellus Shale Gas Keeps Prices LowNatural gas producers, utilities benefit, while power producers suffer.

Christopher Muirand Michael Kay

S&P Equity Analysts

POSITIVE POTENTIAL IMPLICATIONS12-MONTH

‡QUALITY CURRENT TARGET †P/E YIELDCOMPANY / TICKER ‡STARS RANKING *RISK STYLE PRICE PRICE RATIO (%)

EQT / EQT 3 B+ Medium Growth 52 53 27.4 1.7

NiSource / NI 2 B Low Value 20 17 15.5 4.6

National Fuel Gas / NFG 3 B+ Low Blend 72 72 27.1 1.9

UGI / UGI 5 A Medium Blend 32 37 13.7 3.3

*Based on our analysts’ assessment of qualitative factors, including financial strength, potential share volatility , competitive position, industry cyclicality, regulatory/legal issues, and other factors. Please

note that all investments carry risks. ‡See definitions on page 2. †Based on S&P estimated fiscal 2011 earnings. Source: S&P Eq uity Research.

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 10/12

10 STANDARD & POOR’S THE OUTLOOK MAY 11, 2011

Amazon may be the “most admired”company in the country, accordingto Forbes magazine, but that doesn’tmean the stock is worth buying at itscurrent price, according to Standard& Poor’s Equity Research.

Forbes recently published itsannual ranking of the country’s“most admired” companies, basedon a poll of more than 30,000consumers who were asked aboutcompanies for which they hadtrust, esteem, admiration, andgood feeling. Amazon, Kraft Foods,and Johnson & Johnson top theForbes list.

However, S&P Equity Researchhas “hold” rankings on all three,due to a view they are appropriatelyvalued at their current stock prices.In fact, the top five on Forbes list areranked “hold” by S&P EquityResearch, as are six of the top 10and 12 of the top 20.

Of the top 20 in the Forbes list,S&P has “buy” or “strong buy”rankings on eight. They are listed inthe table.

“Our STARS ranking methodology

includes analysis of both a compa-ny’s fundamentals and its valuationto determine whether the sharesshould be bought, held or sold. It isquite possible for a company to haveoutstanding fundamental traits, yethave its shares be fairly priced oroverpriced,” says Tom Smith,

Associate Director of U.S. EquityResearch at S&P.This year through the end of April,

S&P’s 5-STARS stocks outperformedthe S&P 500 by 222 basis points,

while 1-STARS stocks underper-formed by 608 basis points. Thelong-term performance trends alsobear out S&P’s stockpickingprowess. From December 31, 1986,when the STARS system was firstlaunched, to March 31, 2011, 5-STARS stocks posted an average

annual gain of 13.5%, outperform-ing the S&P 500’s 7.3%. In the sametimeframe, 1-STARS stocks postedan average annual gain of only0.5%. ■

Admirable Stocks?Forbes published its list of the country’s “most-admired” companies, and S&P

Equity Research cross-referenced the list against its STARS recommendations.

Beth PiskoraS&P Editorial

POSITIVE POTENTIAL IMPLICATIONS12-MONTH

‡QUALITY CURRENT TARGET †P/E YIELDCOMPANY / TICKER ‡STARS RANKING *RISK STYLE PRICE PRICE RATIO (%)

Caterpillar / CAT 4 A+ Medium Blend 112 142 15.8 1.6

Disney (Walt) / DIS 4 A Medium Growth 43 50 16.1 0.9

FedEx / FDX 5 B+ Low Growth 95 113 19.1 0.5

General Mills / GIS 5 A Low Blend 38 41 15.4 2.9

Google / GOOG 5 NR High Growth 540 700 18.2 Nil

Kohl’s / KSS 4 B+ Medium Growth 53 61 12.2 1.9

• United Parcel / UPS 4 B+ Low Growth 74 92 17.0 2.8

Whirlpool / WHR 4 B+ Medium Blend 84 105 37.5 2.4

● Master List issue. *Based on our analysts' assessment of qualitative factors, including financial strength, potential share vol atility,

competitive position, industry cyclicality, regulatory/legal issues, and other factors. Please note that all investments carry risks. ‡See

definitions on page 2. †Based on S&P estimated fiscal 2011 earnings. Source: S&P Equity Research.

S&P’s Chief Investment Strategist

Sam Stovall sees investors nowlooking past the strength of firstquarter earnings reports to an econ-omy laboring under “the dampen-ing effects of higher oil prices onconsumer spending, the windingdown of stimulus measures, the lackof progress on the U.S. deficit, aswell as increasing global inflationand the rate-tightening responses bycentral banks.”

So far, investors have yet to feel

much pain from the bad news, and itmay be fleeting: job growth – the allimportant indicator – was strong inApril, even though the unemploy-ment rate ticked up to 9%. S&PEquity Strategist Alec Young sayshe’s still “moderately bullish” onstocks, in part because stocks aren’tlavishly valued.

This may even be a self correctingprocess. Signs of weakness in U.S.

economy have served to undercut

expectations of tightening commodi-ty markets, sending prices for oil, aswell as copper, coffee, corn andcocoa, into swift if perhaps tempo-rary retreat. Balancing the desire forstronger economic growth with thecorresponding increase in demandfor raw materials will be a majorchallenge for policy makers through-out the rest of 2011. Maybe a pitstop will help. ■

Taking a Pit Stop (Continued from cover)

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 11/12

STANDARD & POOR’S THE OUTLOOK MAY 11, 2011 11

To enter the High-Quality Capital AppreciationPortfolio, a stock must have an S&P Quality Rankingof A- or better, which indicates an above-average 10-year history of earnings and dividend growth and stabil-ity. A recent S&P study showed that over the long term,stocks with the best S&P Quality Rankings outperformlower quality stocks on a risk-adjusted basis. Stocksmust have a four- or five-STARS ranking to enter thisportfolio. S&P’s Senior Portfolio Group may replaceany stock in the portfolio with another stock at any

time, for reasons that can include a downgrade in theS&P STARS and S&P Quality Ranking of the consti-tuents or other fundamental factors.

The High-Quality Capital Appreciation Portfolioslightly underperformed its benchmark from the begin-ning of the year through April 29, rising 8.1% vs. an8.4% advance in the S&P 500. The data we have pro-vided show which stocks contributed to, or detractedfrom, the portfolio’s performance year-to-date throughApril 29. ■

High-Quality Capital Appreciation Portfolio12/31/2010 — 4/29/2011

Base Currency: US Dollar

CURRENT HIGH-QUALITY CAPITAL APPRECIATION PORTFOLIO

*Based on our analysts’ assessment of qualitative factors, including financial strength, potential share volatility , competitive position, industry cyclicality, regulatory/legal issues, and other factors. Please

note that all investments carry risks. †Price/earnings ratios are based on Standard & Poor's estimated fiscal 2011 per -share earnings. ‡See definitions on page 2. Source: S&P Equity Research.

12-MONTH‡QUALITY CURRENT TARGET †P/E YIELD

COMPANY / TICKER ‡STARS RANKING *RISK STYLE PRICE PRICE RATIO (%)

Apache / APA 5 A- High Blend 127 160 11.4 0.5

C.H. Robinson Worldwide / CHRW 4 A+ Low Growth 79 95 29.4 1.5

Church & Dwight / CHD 5 A+ Low Growth 79 82 18.0 1.7

CVS Caremark / CVS 5 A+ Medium Blend 37 42 13.2 1.4

Express Scripts / ESRX 5 A- Medium Growth 57 65 17.5 Nil

Fastenal / FAST 5 A Medium Growth 66 85 28.1 1.4

Hudson City Bancorp / HCBK 4 A Low Blend 10 12 12.7 3.2

Int’l Business Machines / IBM 4 A+ Medium Growth 168 196 12.7 1.8

McKesson / MCK 5 A- Medium Blend 83 96 13.4 0.9

Mylan / MYL 5 A- Medium Growth 24 29 12.0 Nil

Nike / NKE 4 A+ Medium Growth 83 99 19.8 1.5Oracle / ORCL 5 A- Medium Growth 35 39 16.8 0.7

United Technologies / UTX 4 A+ Low Growth 89 96 16.6 2.2

VF / VFC 5 A Medium Blend 101 120 14.0 2.5

Wal-Mart Stores / WMT 5 A+ Low Blend 55 65 12.3 2.7

LEADERS

Church & Dwight 19.50

McKesson 17.95

Mylan 17.94

VF 16.69Int’l Business Machines 16.23

Oracle 14.89

United Technologies 13.80

Fastenal 11.98

Apache 4.55

CVS Caremark 4.17

Express Scripts 3.31

Wal-Mart Stores 1.95

Occidental Petroleum* 0.46

COMPANY NAME YTD RETURN (%)

LAGGARDS

C.H. Robinson Worldwide -0.01

Procter & Gamble** -0.51

Nike -3.63

Hudson City Bancorp -25.20

COMPANY NAME YTD RETURN (%)

The YTD Return column represents the performance for the period of time the security was in the portfolio, so if the security w as not in the portfolio for the full YTD period, it’ s the performance of the secu-

rity from when it was added to the portfolio to 4/29/11. *Replaced on January 18. **Replaced on April 18.

TheOutlookIntelligence for the Individual Investor

8/6/2019 Outlook_090511

http://slidepdf.com/reader/full/outlook090511 12/12

12 STANDARD & POOR’S THE OUTLOOK MAY 11, 2011

A dynamic, actively managed portfo-lio, the S&P Top Ten Portfolio com-prises stocks that S&P EquityResearch believes to be well posi-tioned for solid capital appreciationover the next 12 months.

Stocks must have a five-STARSranking to enter the portfolio. If theranking drops below four STARS,the stock will be removed. In addi-tion, any stock in the portfolio maybe replaced with a five-STARS stockat any time. With the exception of

Akamai Technologies, AppliedMaterials, Domino’s Pizza, andInternational Business Machines, theother stocks are currently rankedfive STARS.

The goal of the Top Ten Portfoliois to outperform the S&P 500 indexon a capital appreciation basis.

S&P’s Senior Portfolio Group, a sub-committee of our Investment PolicyCommittee, selects the stocks. Theintention of the portfolio is to befairly balanced among economicsectors.

The portfolio currently has sevenlarge-cap stocks, one mid-cap andtwo small-cap issues. It has threestocks from the information technol-ogy sector; two issues each from theconsumer discretionary, industrials,

and consumer staples sectors, andone telecommunication servicesstock.

The best-performing stock in theportfolio this year through April 29was Domino’s Pizza (+16.4%). Theworst-performing stock over thesame period was AkamaiTechnologies (-13.9%). On April 21,2011, Akamai replaced TevaPharmaceutical in the portfolio.

From its inception through April29, 2011, the portfolio rose 2.2% on

an annualized basis vs. a 1.9% gainfor the S&P 500.

This year through April 29, theportfolio rose 3.0%, while thebenchmark climbed 8.4%.

Readers should note that past per-formance is no guarantee of futureresults. ■

Top Ten PortfolioS&P launched this focused list on December 31, 2001.

Performance calculations do not take into account reinvestment of dividends, capital gains taxes or brokerage commissions and f ees. If the foregoing had been factored into the portfolio’s investment

performance, it would have been lower. This performance calculat ion also does not take into account timing differences between the portfolio selections and purchases made based on those selection

by actual investors. Over certain periods, the portfolio incurred losses and over time the portfolio is expected to continue to pose a risk of negative investment returns. Because the portfolio has a high

turnover rate, it is best suited for tax-deferred accounts such as IRAs and is less suited for other accounts. Investors should seek financial advice before investing based on the portfolio. This portfolio

does not address the specific investment objectives, financial situation, and particular needs of any person. Stocks in the por tfolio will not be suitable for all investors. Past performance is

no guarantee of future results.

The goal of the Top Ten

Portfolio is to outperform the

S&P 500 index on a capital

appreciation basis.

TOP TEN PORTFOLIO12-MONTH

‡QUALITY †P/E CURRENT TARGETCOMPANY / TICKER RANKING *RISK STYLE RATIO PRICE PRICE FUNDAMENTAL SNAPSHOT

Akamai Technologies / AKAM B- High Growth 33.3 35 42 Leader in Internet content delivery services

American Tower / AMT B High Blend 55.8 53 70 Market leader in wireless tower industry

Applied Materials / AMAT B- Medium Blend 9.9 15 20 We see rising flash memory orders and China-based solar sales

Coach / COH B+ Medium Growth 20.3 59 67 Coach is the number one luxury accessories brand in the U.S.

• Coca-Cola / KO A+ Low Growth 17.0 67 75 We expect sales growth of more than 20% in 2011.

• Domino’s Pizza / DPZ NR Medium Blend 13.7 21 24 We expect strong customer traffic trends for this pizza delivery company

General Mills / GIS A Low Blend 15.4 38 41 We expect more at-home eating by consumers

• Int’l Business Machines / IBM A+ Medium Growth 12.7 168 196 Should benefit from revenue growth in emerging markets

• Kelly Services / KELYA B- Medium Value 17.3 19 29 We see its primary nonprofessional client market leading the labor recovery

USG / USG C Medium Growth NM 15 23 We expect sales to start a modest revival in the near -term

● Master List issue. *Based on our analysts’ assessment of qualitative factors, including financial strength, potential share vol atility, competitive position, industry cyclicality, regulatory/legal

issues, and other factors. Please note that all investments carry risks. †Based on S&P estimated fiscal 2011 earnings. ‡See def initions on page 2. NM-Not meaningful. Source: S&P Equity

Research.