Embed Size (px)

Citation preview

Outlook and impactof changes in Nigeriataxation landscape for2020

Outlook and impact of changes in Nigeria taxation landscape for 2020

03

Contents

05Nigeria’s FinanceAct 2019

19Mutual AgreementProcedure andclaiming taxbenefits

16Revision ofTransfer PricingRegulations

20The AfricaContinentalFree Trade Area

16Country byCountry ReportingObligations inNigeria

21New ExecutiveChairman for theFederal InlandRevenue Service

17Common ReportingStandards Regulationsin Nigeria

Page 05 Page 17 Page 21

There are fundamental changes in Nigeria’s tax landscape with far-reach-ing impact on the economy and business performance in 2020 and beyond. As though the country was gearing up for the shocking fall in crude oil prices aggravated by the outbreak of the Novel Coronavirus (COVID-19), the taxation landscape was a beehive of activities in the preceding twelve months. As expected, the business community has continued to discuss the impact of the changes on the business environment and the econo-my at large.

For the first time in over 20 years, Nigeria has a new Finance Act 2019 (the Act). The Act makes sweeping changes to seven tax laws, showing strong indications that Nigeria is set for major transformation of its tax landscape. This came at the same time the country’s apex tax body, Federal Inland Revenue Services (FIRS) welcomed its new Chief Executive. As expected with such

change of guard, fresh ideas are being injected into tax administration with the ultimate aim of driving tax penetration, closing the gaps on tax default and raising the bar on revenue generation.

There is also renewed focus on taxation of multi-nationals and curbing illicit financial flows. With country-by-country reporting, review and strengthening of transfer pricing regulations and the demand for increased transparency in tax reporting, Nigeria has continued to increase the heat on aggressive tax planning. There is an ongoing nation-wide taxpayer registration and database consolidation that will bring more people into the tax net. Imple-mentation of Common Reporting Standards and Automatic Exchange of Information are part of the efforts that are all geared towards closing the gaps on illicit financial flow and tax evasion.

The signing of Africa Continental Free Trade Area (AfCFTA) agreement is

another milestone development for the continent and particularly for Nigeria. The agreement establishing the AfCFTA is arguably the most discussed economic subject out of Africa, touted as the largest free trade agreement since creation of the World Trade Organisation (WTO). Debates have continued on the impact of border closure in Nigeria and its impact on the regional trade agreements and the new continental free trade agreement. In addition to changes made in Nigeria’s indirect tax legislation such as value added tax and customs and excise laws, more reforms are still in view that may affect duties and levies payable on imported and locally manufactured goods in Nigeria.

We examine the outlook and impact of the changes happening in Nigeria’s taxation landscape, with an in-depth analysis of each schematic area.

Outlook and impact of changes in Nigeria taxation landscape for 2020

04

Nigeria's Changing Fiscal Landscape

The changes introduced by the Finance Act 2019 are intended to promote fiscal equity, align domestic laws with global best practices, and support Micro, Small and Medium-sized businesses. Other major objectives of the Act include increasing government revenues and stakeholder investments in the capital market.

The President submitted a bill to amend certain sections of Nigeria tax laws together with the 2020 Annual Appropriation Bill. Although the Annual Budget was the first to be passed by the National Assembly, passage of the Finance Bill 2019 was soon to follow as the National Assembly transmitted the harmonized Finance Bill to the President on 20 December 2019. The Bill was subsequently assented by the President on 13 January 2020 with the official gazette becoming available to the public on 4 February,2020.

While the Act came into force on 13 January 2020, the Minister of Finance, Budget and National Planning announced a commencement date of 1 February 2020 as the effective date for the new VAT rate. It is understood that this ministerial directive is being formalized by a request to the National Assembly for proper legal backing via an amendment to the Act.

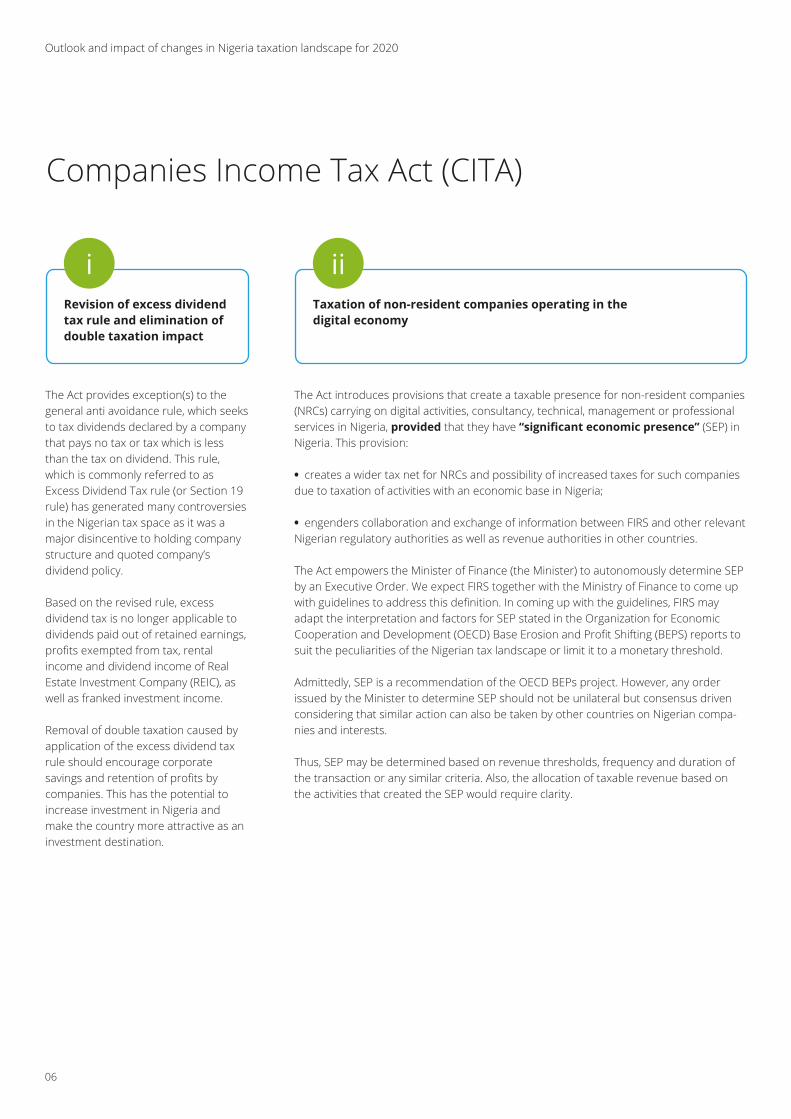

The Act contains 57 sections, 55 of which made changes cutting across seven (7) Nigeria tax laws. These include: Compa-nies Income Tax Act (CITA), Personal Income Tax Act (PITA), Petroleum Profits Tax Act (PPTA), Capital Gains Tax Act (CGTA), Value Added Tax Act (VATA), Customs and Excise Duties Act (CETA) and Stamp Duties Act (SDA). The bulk of the changes were effected in CITA accounting for 22 out of the 55 changes. PITA and VATA have 8 and 15 changes, respective-ly. There was only 1 change in PPTA while 3 changes were effected in CGTA; 1 in CETA and 5 in SDA.

Outlook and impact of changes in Nigeria taxation landscape for 2020

05

Nigeria’s FinanceAct 2019

PITA

VATA

8

22

15

5

311

CITA

CETAPPTACGTA

SDA

Outlook and impact of changes in Nigeria taxation landscape for 2020

06

The Act provides exception(s) to the general anti avoidance rule, which seeks to tax dividends declared by a company that pays no tax or tax which is less than the tax on dividend. This rule, which is commonly referred to as Excess Dividend Tax rule (or Section 19 rule) has generated many controversies in the Nigerian tax space as it was a major disincentive to holding company structure and quoted company’s dividend policy.

Based on the revised rule, excess dividend tax is no longer applicable to dividends paid out of retained earnings, profits exempted from tax, rental income and dividend income of Real Estate Investment Company (REIC), as well as franked investment income.

Removal of double taxation caused by application of the excess dividend tax rule should encourage corporate savings and retention of profits by companies. This has the potential to increase investment in Nigeria and make the country more attractive as an investment destination.

iRevision of excess dividendtax rule and elimination ofdouble taxation impact

The Act introduces provisions that create a taxable presence for non-resident companies (NRCs) carrying on digital activities, consultancy, technical, management or professional services in Nigeria, provided that they have “significant economic presence” (SEP) in Nigeria. This provision:

• creates a wider tax net for NRCs and possibility of increased taxes for such companies due to taxation of activities with an economic base in Nigeria;

• engenders collaboration and exchange of information between FIRS and other relevant Nigerian regulatory authorities as well as revenue authorities in other countries.

The Act empowers the Minister of Finance (the Minister) to autonomously determine SEP by an Executive Order. We expect FIRS together with the Ministry of Finance to come up with guidelines to address this definition. In coming up with the guidelines, FIRS may adapt the interpretation and factors for SEP stated in the Organization for Economic Cooperation and Development (OECD) Base Erosion and Profit Shifting (BEPS) reports to suit the peculiarities of the Nigerian tax landscape or limit it to a monetary threshold.

Admittedly, SEP is a recommendation of the OECD BEPs project. However, any order issued by the Minister to determine SEP should not be unilateral but consensus driven considering that similar action can also be taken by other countries on Nigerian compa-nies and interests.

Thus, SEP may be determined based on revenue thresholds, frequency and duration of the transaction or any similar criteria. Also, the allocation of taxable revenue based on the activities that created the SEP would require clarity.

iiTaxation of non-resident companies operating in the digital economy

Companies Income Tax Act (CITA)

Outlook and impact of changes in Nigeria taxation landscape for 2020

07

The Act introduces thin capitalisation rules by disallowing “excess interest” on foreign related party lending. “Excess interest” is any amount paid or payable as interest on foreign loan, which exceeds 30% of Earnings Before Interest Tax Depreciation and Amortisa-tion (EBITDA).

Where the company is unable to fully deduct the interest based on the restriction, it may carry forward such unabsorbed interest for a maximum of 5 years.

ivIntroduction of thincapitalisation rules

The old rules of determining accessible profits during the first three (commencement) and last two (cessa-tion) tax years of carrying on a business have been replaced with a new basis for computing the assessable profits of companies just starting or ending their business. Under the defunct system, the profits of a new company or a company ceasing business are typically subject to multiple taxation. The amendment under the Finance Act 2019 eliminated the risk of multiple taxation of such companies.

This is particularly commendable as it encourages the growth of new compa-nies by avoiding excessive tax burden within their first three years of opera-tion. However, there are practical transitionary challenges that will be faced by companies who have just recently commenced business and have partly applied the old provisions.

vRevision of commencementand cessation rules

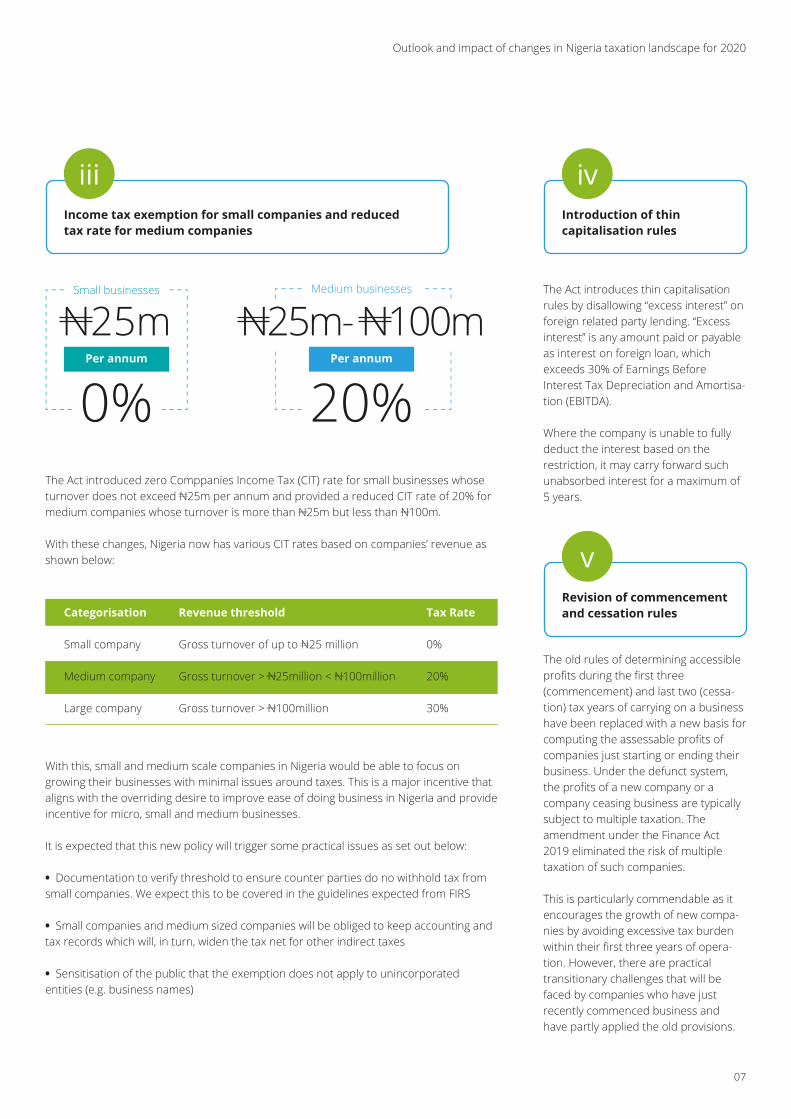

The Act introduced zero Comppanies Income Tax (CIT) rate for small businesses whose turnover does not exceed N25m per annum and provided a reduced CIT rate of 20% for medium companies whose turnover is more than N25m but less than N100m.

With these changes, Nigeria now has various CIT rates based on companies’ revenue as shown below:

With this, small and medium scale companies in Nigeria would be able to focus on growing their businesses with minimal issues around taxes. This is a major incentive that aligns with the overriding desire to improve ease of doing business in Nigeria and provide incentive for micro, small and medium businesses.

It is expected that this new policy will trigger some practical issues as set out below:

• Documentation to verify threshold to ensure counter parties do no withhold tax from small companies. We expect this to be covered in the guidelines expected from FIRS

• Small companies and medium sized companies will be obliged to keep accounting and tax records which will, in turn, widen the tax net for other indirect taxes

• Sensitisation of the public that the exemption does not apply to unincorporated entities (e.g. business names)

iiiIncome tax exemption for small companies and reducedtax rate for medium companies

Small company

Medium company

Large company

Gross turnover of up to N25 million

Gross turnover > N25million < N100million

Gross turnover > N100million

Categorisation Revenue threshold

0%

20%

30%

Tax Rate

N25mSmall businesses

Per annum Per annum

0%N25m- N100m

Medium businesses

20%

Outlook and impact of changes in Nigeria taxation landscape for 2020

08

The old minimum tax rule has been changed to eliminate the incidence of tax on capital and net assets. The new rule is simpler but more potent.

Minimum tax is now to be calculated as 0.5% of a company’s gross turnover less franked investment income. The Act defines gross turnover as “the gross inflow of economic benefits (cash, revenue, receivables and other assets) arising from the operating activities of a company, including sales of goods, supply of services, receipt of interest, rent, royalties or dividends”. The definition of gross turnover essentially covers all forms of income sources from “operating activities” and lists certain exam-ples.

Ultimately, while minimum tax is now going to be a lot easier to calculate, the revenue base may still generate controversies, and it may turn out to be a burden on companies, particularly those with slim margins or in loss making positions.

Tax authorities may want to adopt a wider definition of income from all sources, while tax payers would want to limit it to income from operating activities. IAS 7 defines “operating activities” as income from normal operations and excludes income from investment or financing activities.

viNew minimum tax rule

The Act exempts from tax dividends and rental income received by a REIC on behalf of its shareholders provided 75% of the income is distributed to shareholders within 12 months of earning the income. On the other hand, the amendment to section 24 of CITA would allow, “dividends or mandatory distributions made by REICs…” for tax deductions.

The Act however does not define the scope of REICs, including whether it would cover Real Estate Investment Trust (REITs). We expect that this would be covered in guidelines to be issued by FIRS.

viiReal Estate InvestmentCompanies

The Act seeks to enhance the financial position of insurance companies by amending provisions that now entitles insurance companies to indefinite carry forward of losses as opposed to the 4-year restriction previously in place.

The Act also promotes fairness as it amended the restrictive minimum tax provision for life and non-life business, recommending general minimum tax similar to other compa-nies.

Furthermore, “taxable investment income” is now limited to “income derived from the investment of shareholders’ funds”. This provides clarity on taxable income and limits it to income accruing to the insurance companies as against income accruing to insurance funds.

viiiRemoval of disincentiveprovisions in relationto insurance industry

Outlook and impact of changes in Nigeria taxation landscape for 2020

09

The Act expands categories of exempt income to include profit of a small company and dividends declared from small manufacturing companies. The exemption also covers rental income and dividends of REICs and secondary payments under “Securities Lending” transaction. This has eliminated the potential double taxation on compen-sating payment mimicking interest and dividends.

ixExpansion of the categoriesof exempt income

Taxpayers who pay their tax liability at least 90 days before due date would be entitled to bonus of 2% and 1% of the tax paid for medium and large compa-nies, respectively.

While this is laudable, it may not achieve its aim of timely payment of tax. This is because the bonus may not be as beneficial to the taxpayer as the interest the tax payable would yield if invested, even in risk free securities.

xiEarly tax payment bonus

The Act provides that companies engaged in “agricultural production” can enjoy an initial tax free period of 5 years, subject to an additional maximum period of 3 years. The implication is that companies engaged in agricultural production may enjoy a tax holiday of up to 8 years.

However, the Act does not define agricultural production and does not provide the mode of granting the initial 5-year incentive and subsequent renewal for 3 years. The administrative requirements could be addressed under the guidelines expected from FIRS or the Minister.

xiiTax holiday for companiesin agricultural production

The Act removes the Ministerial approval requirement, for expenses incurred relating to management services between non-related parties before such expenses could be tax-deductible. This implies that any entity who enters into a management service agreement with an unrelated entity would be able to claim tax deductions for management fees without Ministerial approval or the National Office for Technology Acquisi-tion and Promotion’s (NOTAP) approval.

This would be a great relief for compa-nies given NOTAP’s refusal to approve management services agreement in recent times. However, where the agreement is with a non-resident company (NRC), companies would still battle settlement obligations especially with sourcing foreign exchange (forex) as NOTAP approval remains a major requirement for sourcing forex from the authorised dealers in order to pay management fees.

xMinisterial approval formanagement fees deduction,no longer required

Outlook and impact of changes in Nigeria taxation landscape for 2020

10

With the requirement for TIN on business documents, coupled with the creation of TIN for newly incorporated companies, the Act has gone further to request companies to display their TIN as evidence of tax registration. Thus, the requirement for a company to display its TIN covers all documents, statements, returns and any corre-spondence with a government agency.

In this regard, any document (including bank correspondence) without TIN is invalid and banks may disregard it. This is more so as FIRS issued a notice for existing companies to register for a TIN by April, 2020.

xiiiRequirement to display Taxidentification number (TIN)

The Act revised the WHT applicable on construction contracts to 2.5%. This provision was previously introduced in January 2015 via a regulation, but was withdrawn in November 2016. Reintro-duction of the reduced WHT rate of 2.5% into the Act protects the construc-tion companies from the risk of accumulated tax credits with the attendant practical refund challenges.

xivWithholding (WHT) tax onconstruction contracts

The Act introduced provisions that qualifies non-deductible penalties as those resulting from violation of any Act of the National Assembly. Relying on the rule of interpretation which suggests that “express mention of one excludes all others”, it is arguable that other forms of penalties, such as contractual penalties (e.g. demurrage), penalties arising from breach of state laws / local government edicts (e.g. land use charge penalties) are deductible.

xvNon-deductibility of penaltiesfor various infractions

Outlook and impact of changes in Nigeria taxation landscape for 2020

11

Contributions to pension, provident and other retirement benefits funds, societies or schemes would constitute allowable deductions for tax purposes. The deductibility of such contributions would not be contingent on its approval by the Joint Tax Board. Companies that contribute to private pension funds and other private schemes would be able to enjoy maximum tax relief for such contributions in arriving at their tax payable.

iDeductibility ofpension contributions

iiIntroduction of a requirementto obtain TIN by banks

In 2011, PITA was amended to introduce a consolidated tax free allowance of N200,000 or 1% of gross income, whichever is higher; plus 20% of the gross income. Prior to 2011, individuals claimed both children and dependent relatives benefits of N10,000 (capped at N2,500 per child with a maximum of 4 children) and N4,000 respectively. Though negligible, these two benefits were not removed by the 2011 amendment and could be claimed by individuals.

Many stakeholders were of the opinion that it was the intention of the legisla-ture to replace the children and dependent relatives’ benefits with the erstwhile new consolidated relief allowance. However, in the absence of anything contrary in the old PITA, individuals were at liberty to claim the relief.

The Act deleted three sub-sections relating to personal relief (i.e. sub-sec-tions (4) – (6) of section 33, PITA). However, due to poor legislative drafting, the 2011 PITA amendment did not properly renumber the sub-sec-tions to track the amendment. Thus, there are two subsections (4) under PITA.

It is arguable however, that both sub-sections (4) including the provision relating to claims of child benefit and dependent relative allowance are no longer applicable.

iiiDeletion of provisions thatgrant certain personal reliefs

Personal Income Tax Act (PITA)

Prior to the passing into law of the Act, Nigerian banks usually requested for TIN from prospective customers in order to open bank accounts as a KYC requirement. The Act has made this requirement a mandatory obligation on all businesses as a pre-condition for opening a new bank account. Also, existing bank account holders are to provide their TIN as a precondition to continue operating their bank accounts. However, FIRS released a public notice mandating banks to obtain the TIN of all companies/businesses not later than 12 April 2020.

While this is the practice, the proposed amendment is a welcome development, as it gives a legal basis to the practice.

Outlook and impact of changes in Nigeria taxation landscape for 2020

12

Section 60 of the PPTA which exempts dividends paid out of profits derived from petroleum operations from WHT has been deleted. Companies engaged in oil explorative operation and liable to tax under PPTA are now saddled with the responsibility of withholding tax when paying dividends to their shareholders.

PetroleumProfits Tax Act(PPTA)

Transfer of assets during reorganization within a group of companies would be exempt from capital gains tax. However, an anti-avoidance provision (365 day holding period) was included to ensure companies do not create fictitious group structures to take advantage of the exemption.

iExemption on tax arisingfrom re-organisation

Compensation received for loss of employment of up to N10million would be exempted from CGT. This creates an incentive for payment of compensation for loss of employment below the N10million threshold as termination benefits rather than terminal benefits, would have been subjected to PIT.

iiTermination benefits

Capital Gains Tax Act (CGTA)

Outlook and impact of changes in Nigeria taxation landscape for 2020

13

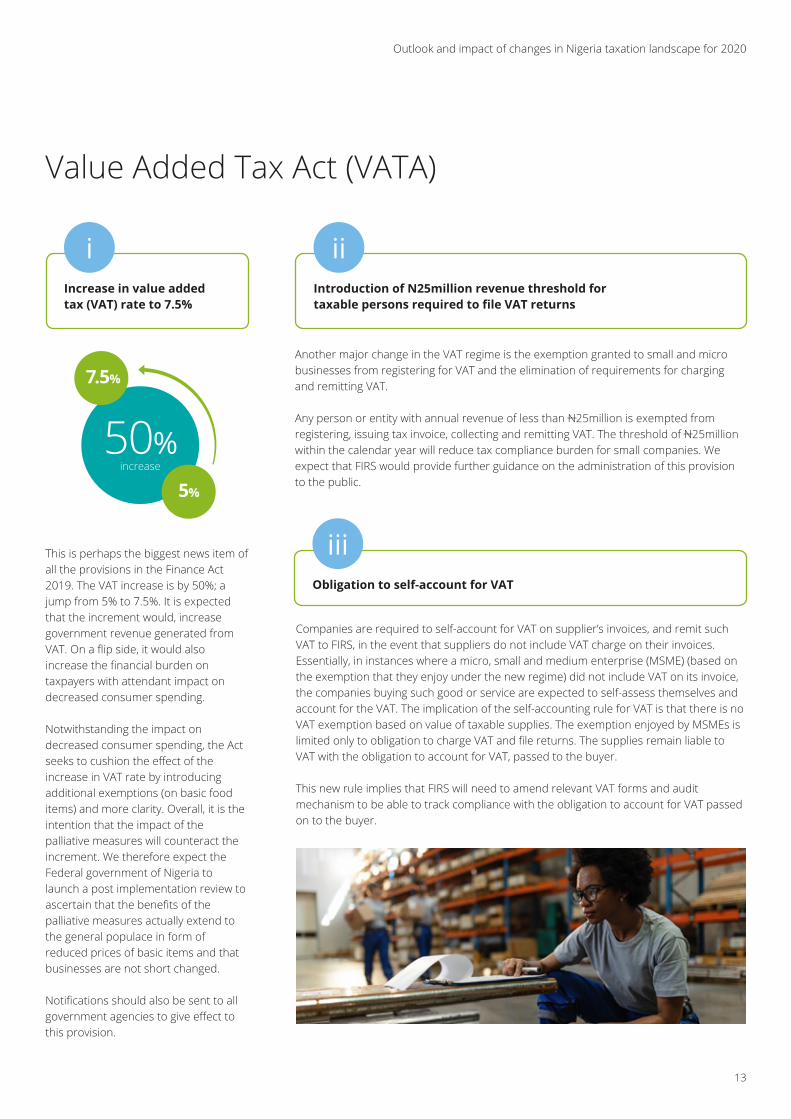

This is perhaps the biggest news item of all the provisions in the Finance Act 2019. The VAT increase is by 50%; a jump from 5% to 7.5%. It is expected that the increment would, increase government revenue generated from VAT. On a flip side, it would also increase the financial burden on taxpayers with attendant impact on decreased consumer spending.

Notwithstanding the impact on decreased consumer spending, the Act seeks to cushion the effect of the increase in VAT rate by introducing additional exemptions (on basic food items) and more clarity. Overall, it is the intention that the impact of the palliative measures will counteract the increment. We therefore expect the Federal government of Nigeria to launch a post implementation review to ascertain that the benefits of the palliative measures actually extend to the general populace in form of reduced prices of basic items and that businesses are not short changed.

Notifications should also be sent to all government agencies to give effect to this provision.

iIncrease in value addedtax (VAT) rate to 7.5%

Companies are required to self-account for VAT on supplier’s invoices, and remit such VAT to FIRS, in the event that suppliers do not include VAT charge on their invoices. Essentially, in instances where a micro, small and medium enterprise (MSME) (based on the exemption that they enjoy under the new regime) did not include VAT on its invoice, the companies buying such good or service are expected to self-assess themselves and account for the VAT. The implication of the self-accounting rule for VAT is that there is no VAT exemption based on value of taxable supplies. The exemption enjoyed by MSMEs is limited only to obligation to charge VAT and file returns. The supplies remain liable to VAT with the obligation to account for VAT, passed to the buyer. This new rule implies that FIRS will need to amend relevant VAT forms and audit mechanism to be able to track compliance with the obligation to account for VAT passed on to the buyer.

iiiObligation to self-account for VAT

Another major change in the VAT regime is the exemption granted to small and micro businesses from registering for VAT and the elimination of requirements for charging and remitting VAT.

Any person or entity with annual revenue of less than N25million is exempted from registering, issuing tax invoice, collecting and remitting VAT. The threshold of N25million within the calendar year will reduce tax compliance burden for small companies. We expect that FIRS would provide further guidance on the administration of this provision to the public.

iiIntroduction of N25million revenue threshold fortaxable persons required to file VAT returns

Value Added Tax Act (VATA)

50%5%

7.5%

increase

Outlook and impact of changes in Nigeria taxation landscape for 2020

14

The inclusion of the definition of “goods” and “services” in VATA is expected to eliminate ambiguity with respect to the application of VAT to certain transactions. However, some issues are still not so clear. For instance, there have been issues around the liability of shares to VAT. The Act, on one hand, defines “goods” as “all forms of tangible property that are move-able...but does not include securities”.

It can be argued from this definition that shares should not be liable to VAT, being a security. On the other hand, “goods” is defined as “any intangi-ble…….asset or property over which a person has ownership or rights...he derives economic benefits…can be transferred… except interest in land”. This could also be interpreted to mean shares would become liable to VAT. Consequently, the new definition may lead to further confusion if not well addressed.

Some have also expressed the view that buildings or mineral concessions form part of “interest in land” , thus so long as such “interest in land” is exempt, buildings/mineral concessions should also be exempt as they are immoveable. This interpretation appears questionable as land is a different asset, while building/concession is another – such separation is also effected in financial statement and capital allowance computations.

ivInclusion of definition of“goods” and “services”

The Act defines “exported service” as “a service rendered within or outside Nigeria by a person resident in Nigeria to a person outside Nigeria”. This would eliminate ambiguity in the application of the current definition.

vClarification on exportedservices

The Act exempts assets sold or transferred to a related party in a restructuring exercise from VAT. This is on the condition that the underlying assets are not sold by the acquiring company within 365 days after the date of restructuring. This welcome develop-ment will aid group restructuring in Nigeria.

viExemption of assets sold ina restructuring exercise

The Act increases the penalties for non-registration for VAT, failure to notify FIRS of change in address within 30 days, failure to notify FIRS of permanent cessation of business or failure to file VAT returns to N50,000 in the first month of default and N25,000 subsequently from the previous penalty of N10,000 in the first month and N5,000 in subsequent months. This shows that Government is serious about making infractions with the law more punitive in nature with the up to 500% increase in penalties.

viiIncrease in penalties fornon-compliance with VAT

Outlook and impact of changes in Nigeria taxation landscape for 2020

15

The main change in CETCA is the expansion of goods liable to excise duties to include imported goods. This eliminates any unfair advantage on imported products over local products. It ensures a level playing field between local producers and importers.

However, it needs to be clear if goods already subject to high import duties (sometimes up to 70%) will also be subject to such excise or if the import duty rates will be revisited.

Customs and ExciseTariffs etc. (Consolidation)Act (CETCA)

The Act increases the stamp duty on receipts to N50 on every transaction of N10,000 and above; and expands the definition of receipt to cover electronic transactions. This gives a legal basis to what is already being practised by Nigerian banks, but raises the threshold to N10,000 from N1,000.

However, it does not address the controversy on stamp duty administration by FIRS and Nigerian Postal Service (NIPOST) as adhesive stamp (sold by NIPOST) is still applicable and FIRS has the power to charge and collect stamp duties. However, we envisage that the realistic controversies will be limited as the populace hardly rely on adhesive stamps.

Stamp Duties Act (SDA)

Outlook and impact of changes in Nigeria taxation landscape for 2020

16

The changes to transfer pricing (TP) regime in Nigeria came to a head in 2018, with the introduction of new regulations with its attendant huge penalty provisions for non-compliance. In recent times, tax authorities have been more insistent on companies complying with their filing and documentary obligations under the Nigerian TP rules. Going forward and considering the revenue drive of the FIRS, we expect more of such actions from FIRS in the current year.

Also, the approved 2020 budget has a provision for fines and penalties as a source of almost 3% of proposed government revenue. Thus, the tax authorities have been seeking to enforce the penalty provisions. This is evident in the creation of various units within FIRS to deal with non-compliance with the TP regulations and other relevant guidelines. Taxpayers would do well to ensure that their records and compliance status are in order.

Country-by-country (CbCR) Regulations was released in 2018, introducing reporting and notification obligations for members of multinational entities (MNE) groups, with penalties for default ranging from N10,000 daily to N10million depending on the infraction. The obligations apply when the consolidated revenue of the MNE group exceeds N160billion

The OECD Peer Review Report recommended that Nigeria amends its CbCR Regulations due to the country’s non-reciprocal status in exchanging CbC reports. If the amendment is effected in the current year, it is expected that local filing obligation on constituent entities in Nigeria will be expunged – currently constituent entities may be obliged to file CbC reports in Nigeria even though they are not the Ultimate Parent Entity (UPE) of the MNE group (where certain conditions exist).

It remains to be seen if expected amendments will also relax notification obligations as Nigeria will not receive CbC reports submitted to tax authorities in other jurisdictions, making notification to FIRS of the MNE group’s UPE jurisdiction unnecessary in such cases.

Revision ofTransfer PricingRegulations

Country-by-Country Reporting

Outlook and impact of changes in Nigeria taxation landscape for 2020

17

In an attempt to manage potential tax evasion brought about by globalization, members of the OECD came together and agreed to exchange information by signing the Multilateral Convention on Mutual Administrative Assistance in Tax Matters. This was the basis for developing the Common Reporting Standard (CRS) by the OECD Council on 15 July 2014, requiring jurisdictions to obtain information from their financial institutions and automatically exchange that information with other jurisdictions on an annual basis.

Although not an OECD member, Nigeria signed the Multilateral Convention on Mutual Administrative Assistance in Tax Matters (MAC) and the Multilateral Competent Authority Agreement (MCAA) on the Automatic Exchange of Financial Account Information (AEOI) on 17 August 2017 and agreed to commence reporting in 2019.

Subsequently, the Income Tax (Common Reporting Standard) Regulations, 2019 (“the Regulations” or “CRS Regulations”), was issued by the FIRS, to provide a legal basis for Nigerian Financial Institutions (NFIs) to transmit information to the FIRS and also to drive compliance with the rules relating to the CRS in Nigeria.

Common Reporting StandardsRegulations in Nigeria

Outlook and impact of changes in Nigeria taxation landscape for 2020

18

Strict compliance to the CRS Regulations would require an investment by the NFIs in terms of money, time and manpower. However, non-compliance would come at even a bigger cost, with significant fines and penalties resulting in financial burden and reputa-tional damage to defaulting organisations.

The penalties for non-compliance are as follows:

With the coming into effect of CRS, each Reporting Financial Institutions (RFI) in Nigeria is expected to carry out 3 major obligations under the Regulations as follows:

• Due-diligence: Establish, maintain and document a due diligence framework on its financial accounts that will determine the extent of background information required for reporting purposes.

• Reporting: Prepare annual information return relating to Reportable Accounts, in specific format with effect from 2019 calendar year. Thereafter, submit the annual information returns electroni-cally using technology provided or approved by FIRS no later than 31 May of the year following the calendar year which the returns relate. In essence the first return is due to be submitted on or before 31 May, 2020

• Record keeping: Store records relating to the returns, for at least 6 calendar years from the last year in which the records were relevant

Non-compliance with a duty or an obligation

Late filing of returns

False statement or report

Non-compliance with FIRS’ requirements in the performance of its functions (e.g. not providing additional information)

Failure to keep records

N10,000,000 in the first month and N1,000,000 for every month in which the failure continues

N10,000,000 in the first month and N1,000,000 for every month in which the failure continues

N5,000,000

N1,000,000 in the first month of default and N100,000 for each subsequent day of default

N10,000,000 in the first month and N1,000,000 for every month in which the failure continues

Offence Penalties

Outlook and impact of changes in Nigeria taxation landscape for 2020

19

With the increased regulatory scrutiny on taxpayers by the tax authorities, incessant TP audits, more focus on treaty benefit claims and possible exposure of foreign entities to Nigerian taxes, there is bound to be tax adjustments which would impact non-resident companies adversely.

The adverse impact, inconsistent with the provisions of relevant double tax treaties (DTTs), may arise from the interpretation or application of DTTs by either or both relevant tax authorities of the treaty partners. In this regard, it becomes incumbent for taxpayers to take advantage of any benefit or any incentive that they can enjoy. The Mutual Agreement Procedure (MAP) guidelines provide the procedures for resolving disputes under tax treaties and seeking relief for actions of tax authorities which may result in implications not contemplated under the tax treaties.

This is especially relevant for the following circumstances:

• companies with TP arrangements• taxpayers with dual residency• taxpayers with WHT credit• taxation where permanent establishment (PE) is not created• tax on different classification of income

With this window opened for Nigerians and taxpayers in countries with which Nigeria has DTTs, we expect a more robust application of MAPs, collaboration between relevant tax authorities and a more business friendly environment in Nigeria.

MutualAgreementProcedureand claimingtax benefits

Outlook and impact of changes in Nigeria taxation landscape for 2020

20

The agreement establishing the The Africa Continental Free TradeArea (AfCFTA) is arguably the most discussed economic subject out of Africa. Now the largest free trade agreement (FTA) since creation of the World Trade Organisation (WTO), it is easy to understand the attention. The AfCFTA, which came into force on 30 May 2019 was designed to be a legal instrument which would foster economic integration by creating a single market for goods and services, vide progressive elimination of tariffs barriers (TBs) and non-tariff barriers (NTBs) to trade and investment in Africa.

While negotiations on major annexes to some protocols in Phase I are ongoing, the secretariat seems to be almost ready for trading in July 2020, with the location of the AfCFTA secretariat decided and appointment of the first Secretary General of the Secretariat. Nonetheless prominent state parties

The AfricaContinentalFree TradeArea

and proposed state parties to the Agreement seem to be having challeng-es in preparing for trade commence-ment under the Agreement in July 2020.

Nigeria, being the largest market in terms of population and Gross Domestic Product (GDP) in Africa, signed the Agreement in July 2019 and is expected to ratify the Agreement shortly. However, the country has recently closed its borders with neighbouring countries as a way of curbing smuggling activities around the border. It is noteworthy that this approach to managing smuggling activities around Nigeria’s borders appears to be against the letters of the AfCFTA. It therefore triggers doubts and questions about Nigeria’s commitment to the Agreement.

Despite provisions contained in the Agreement to protect state parties against smuggling and illegal importa-

tion of non-Africa originating goods and services under the AfCFTA, there seem to be general scepticism about the practicality of its implementation.

On the basis that not all goods and services will be liberalized, it goes without saying that the impact of the AfCFTA on any business would depend on the outcome of ongoing negotia-tions. It is also noteworthy that the provisions of the agreement is only binding on state parties (i.e. African Union member states that have signed and ratified the Agreement), hence there may be predictable delay of implementation in Nigeria.

It is our view that whilst the issue with border closure and ratification may linger, it helps provide ample time for businesses to prepare for continental competition - follow the conversation, evaluate the impact of ongoing negotiations, and importantly plan to conquer the new market.

Outlook and impact of changes in Nigeria taxation landscape for 2020

21

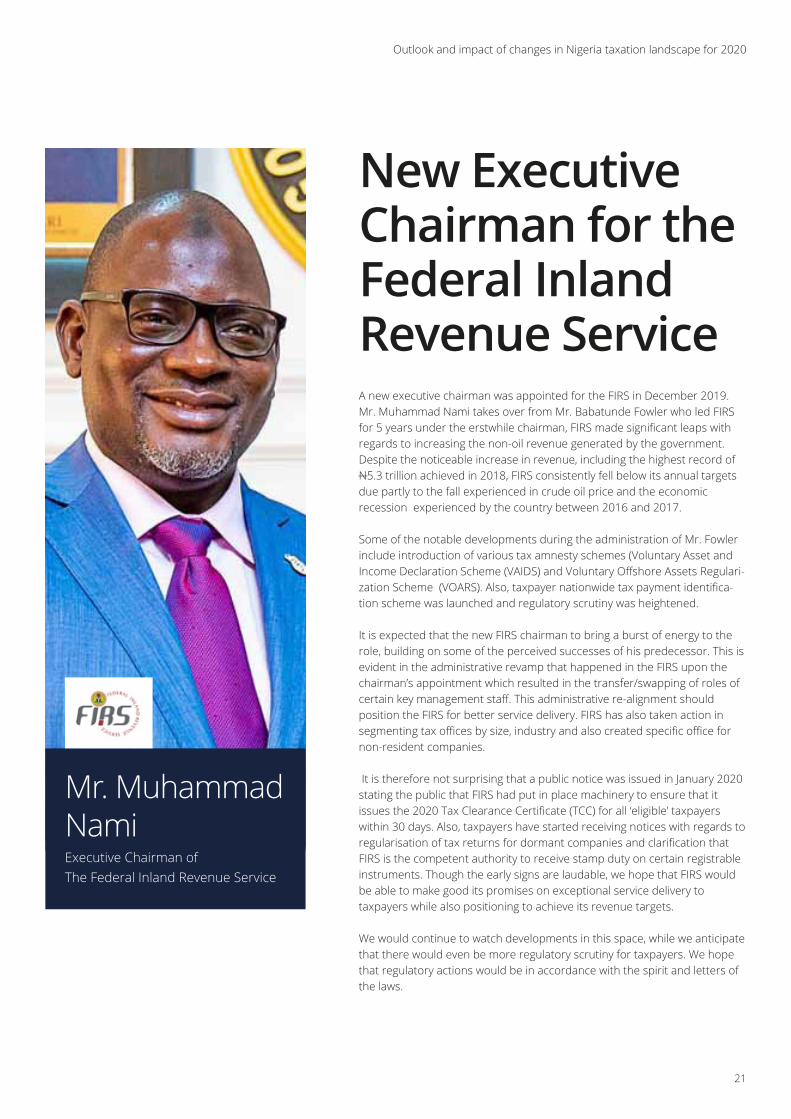

A new executive chairman was appointed for the FIRS in December 2019. Mr. Muhammad Nami takes over from Mr. Babatunde Fowler who led FIRS for 5 years under the erstwhile chairman, FIRS made significant leaps with regards to increasing the non-oil revenue generated by the government. Despite the noticeable increase in revenue, including the highest record of N5.3 trillion achieved in 2018, FIRS consistently fell below its annual targets due partly to the fall experienced in crude oil price and the economic recession experienced by the country between 2016 and 2017.

Some of the notable developments during the administration of Mr. Fowler include introduction of various tax amnesty schemes (Voluntary Asset and Income Declaration Scheme (VAIDS) and Voluntary Offshore Assets Regulari-zation Scheme (VOARS). Also, taxpayer nationwide tax payment identifica-tion scheme was launched and regulatory scrutiny was heightened.

It is expected that the new FIRS chairman to bring a burst of energy to the role, building on some of the perceived successes of his predecessor. This is evident in the administrative revamp that happened in the FIRS upon the chairman’s appointment which resulted in the transfer/swapping of roles of certain key management staff. This administrative re-alignment should position the FIRS for better service delivery. FIRS has also taken action in segmenting tax offices by size, industry and also created specific office for non-resident companies.

It is therefore not surprising that a public notice was issued in January 2020 stating the public that FIRS had put in place machinery to ensure that it issues the 2020 Tax Clearance Certificate (TCC) for all ‘eligible’ taxpayers within 30 days. Also, taxpayers have started receiving notices with regards to regularisation of tax returns for dormant companies and clarification that FIRS is the competent authority to receive stamp duty on certain registrable instruments. Though the early signs are laudable, we hope that FIRS would be able to make good its promises on exceptional service delivery to taxpayers while also positioning to achieve its revenue targets.

We would continue to watch developments in this space, while we anticipate that there would even be more regulatory scrutiny for taxpayers. We hope that regulatory actions would be in accordance with the spirit and letters of the laws.

New ExecutiveChairman for theFederal InlandRevenue Service

Mr. MuhammadNamiExecutive Chairman ofThe Federal Inland Revenue Service

Outlook and impact of changes in Nigeria taxation landscape for 2020

22

The fiscal landscape will continue to face thecombined effect of volatility, uncertainty, complexity and ambiguity (VUCA). A good place to start would be to understand the rules in order to tackle the concerns generated. Businesses must design effective strategies that anticipate changes, block leakages and respond appropriately.

Mapping the way forward

Create response mechanism for

expected increase in regulatory pressure

and scrutiny

CBlock

compliance leakages through appropriate

strategies that optimises tax

position

B

Anticipateand sense changes

in the global and local economy

A

If you would like to discuss the impact of these changes on your business and how you could leverage the opportunities that they offer, please reach out to the following:

Deloitte Nigeria www2.deloitte.com/ng

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk advisory, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500® companies through a globally connected network of member firms in more than 150 countries and territories bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges. To learn more about how Deloitte’s approximately 245,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2020. For more information, contact Deloitte Touche Tohmatsu Limited.

Contacts

Yomi OlugbenroPartner & West Africa Tax Leader+234 1 904 [email protected]

Patrick NzehPartner, Tax & Regulatory Services+234 1 904 [email protected]

Olukunle OgunbamawoPartner, Tax & Regulatory Services+234 1 904 [email protected]

Oluseye ArowoloPartner, Tax & Regulatory Services+234 1 904 [email protected]

Taiwo OkunadePartner, Tax & Regulatory Services+234 1 904 [email protected]

Funke OladokePartner, Tax & Regulatory Services+234 1 904 [email protected]

Yomi Olugbenro@YomiOlugbenro

Oluseye Arowolo@oluseyeArowolo

Patrick Nzeh@pnzeh

Taiwo Okunade@taiwookuns

Funke Oladoke@FOladoke

Olukune Ogunbamowo@KunleBamowo