Embed Size (px)

Citation preview

Topic 1 Topic 2 Topic 3 Contact

1www.EUbusinessinJapan.eu

Topic 4

Outline of Tax Reform 2017

Lyckle GriekProject Manager, Japan Tax & Public Procurement (JTPP) Helpdesk

Topic 1 Topic 2 Topic 3 Contact

2www.EUbusinessinJapan.eu

Topic 4

Today’s topics

• Corporate taxation• Consumption taxation• Individual taxation• Other changes• Q&A

Outline of tax reform 2017

Topic 1 Topic 2 Topic 3 Contact

• Revision of R&D Tax credit• Revision of fiscal incentives to promote salary

increases• Fiscal measures to promote SME investments

3www.EUbusinessinJapan.eu

Topic 4

Corporate taxation

Change of general tax credit rate

Topic 1 Topic 2 Topic 3 Contact

Before After

Tax credit rate 12%(Large businesses: 8-10%)

12-17%(large businesses 6-14%)

Maximum 25% (regular R&D expenses) 25% (regular expenses)However, SMEs additional 10%, if increase in R&D ≥ 5%OrR&D expenditures are ≥10% of average turnover

4www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Revisions of R&D Tax credit

Topic 1 Topic 2 Topic 3 Contact

• Addition of R&D for development of new services (4th Industrial Revolution)

• Internet of Things (IoT)• Artificial Intelligence (AI)• Big data

• Examples:• Automatic data gathering with sensors• Specialist analysis using information analysis

technologies

5www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Revisions of R&D Tax credit

Topic 1 Topic 2 Topic 3 Contact

Before After

SMEs Conditions:1. Increases above 2-3% in overall

salary expenditures since 20122. Increase in overall salary

expenditure if compared with previous year

3. Average salary expenditures amount ≥ previous year

Tax credit of 10% from FY 2012 overall amount of salaries paid

Conditions:Unchanged

Tax credit of 10% however if the salary increase is more than 2% in FY2017, additional bonus of 12% in tax credit is given making a total of 22%

6www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Revision of fiscal incentives to promote salary increase

Topic 1 Topic 2 Topic 3 Contact

7www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Revision of fiscal incentives to promote salary increase

In case the average salary increase per worker is JPY 50,000

In case the average salary increase per worker is JPY 350,000

Here with the base year 2012(PY104m-100m)*10%=JPY 400,000 in tax credits

Here with the base year 2012:(JPY103m-100m)*10%+(JPY110m-103m)*22%=1.840,000 in tax credits

Topic 1 Topic 2 Topic 3 Contact

• Fiscal incentives to promote investments for companies designated as “chukaku” companies (Regional Area Core Companies)

• 4% tax credits for machinery, or special amortization at 40%• 2% for structures/buildings, or special amortization at 20%

8www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Fiscal measures to promote SME investments

Topic 1 Topic 2 Topic 3 Contact

• Expansion of scope of assets available for special investment tax credit

• Current measure is expanded to also include investments in equipment and building improvement (fixtures) for coming two years.

9www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Fiscal measures to promote SME investments

Topic 1 Topic 2 Topic 3 Contact

Immediate depreciation deduction

Tax credit of7 or 10%*

Aimed at capital investment that is based upon an approved plan under the SME Management Enhancement Law- Investments to improve productivityShould leave to an improvement of more than 1% on average (for example energy saving measures)- Investment to enhance earning capabilitiesFacilities pertaining investment plans that where the capital income ratio is higher than 5%

Special depreciation30%* or

Tax credit7%*

SME Investment promotion tax programme(Programme where SMEs can apply special depreciation of 30% and 7% of tax credits when acquiring special devices etc.)

Retail and service business Agricultural, Forestry and Fisheries revitalization tax programme(Programme where SMEs running a retail, service or AFF company SMEs can apply special depreciation of 30% and 7% of tax credits when investing in capital to improve their operations.

*For enterprises with less than 30 million ¥in capitalization

Investment in automobiles, software, devices, tools (measuring/research), fixtures and furniture

10www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Fiscal measures to promote SME investments

Topic 1 Topic 2 Topic 3 Contact

Example:Company wants to make an investment in buying self-service cash registers for JPY15 million. This would be regarded as an investment to improve operations, it is possible to either choose immediate depreciation deduction, by including it in the business costs or a tax credit of 10% (JPY1.5 million) from the corporate tax due.In case of companies being in the red:It is possible to use the exception for fixed assets tax, where in case of purchases of new capital to improve operations, fixed asset tax is halved for three years. In the case of the example, JPY170,000 can be deducted over three years.

11www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Fiscal measures to promote SME investments

Topic 1 Topic 2 Topic 3 Contact

Continuation of existing fiscal measure to promote relocation of companies to the region

• Tax credits regarding offices are kept at the current level of 7% in case of moving and 4% in case of strengthening regional offices

• The amount of tax credit in case new full-time unlimited employment is generated is increased.

• Requirements to use this measure are relaxed, that it will no longer require that more half the employees are moved outside of Tokyo wards, but instead will include new employees at the new location as well in the calculation.

12www.EUbusinessinJapan.eu

Topic 4

Corporate taxation:Expansion of regional stronghold strengthening programme

Topic 1 Topic 2 Topic 3 Contact

• Increase in consumption tax postponed until 2019• Liquor tax reform• Fiscal stimulus for regional revitalization

13www.EUbusinessinJapan.eu

Topic 4

Consumption Tax

Topic 1 Topic 2 Topic 3 Contact

14www.EUbusinessinJapan.eu

Topic 4

Consumption Tax:Liquor tax reform

Product Definition Tax rate(¥, per 350 ml unit)

Presently 2026 Presently 2026Beer Only malt, hop, water and legal

materials;Malt ratio ≥67%

Only malt, hop, water and legal materials (partly expanded);Malt ratio ≥50%

77 54.25

Happoshu Usage of malt Usage of maltUsage of hopProduct similar to other beers

46.99 54.25

“New genre” beers and Mixers (chuhai)

Usage of pea protein, hopMix of happoshu and low-malt spiritsOthers (Chuhai)

Others (Chushai) 28.00 35.00

Beer and Beer-type beverages: One tax rate in October 2026Sake and Wine: One rate in October 2023 (Wine is going up, while sake is going down)Mixers (Chuhai) and low-alcoholic drinks: tax increase in October 2016

“Definitions of beer”

Topic 1 Topic 2 Topic 3 Contact

• Exemption of liquor tax for locally produced sake and beer sold to foreign tourists

• Establishment of shochu special districts

15www.EUbusinessinJapan.eu

Topic 4

Consumption Tax:Fiscal stimulus for regional revitalization

Topic 1 Topic 2 Topic 3 Contact

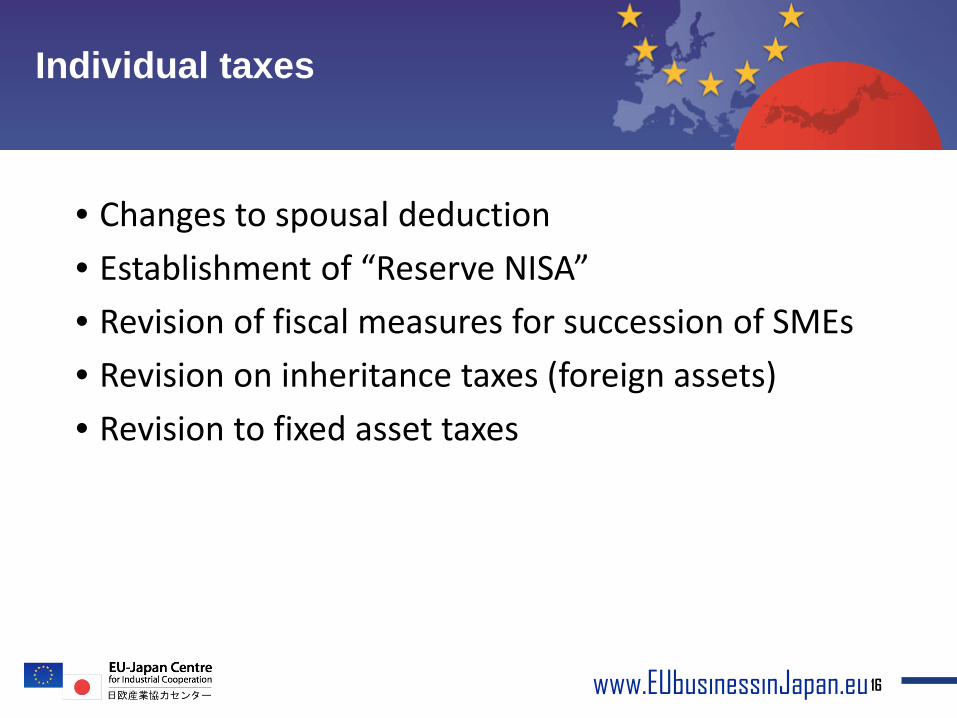

• Changes to spousal deduction• Establishment of “Reserve NISA”• Revision of fiscal measures for succession of SMEs• Revision on inheritance taxes (foreign assets)• Revision to fixed asset taxes

16www.EUbusinessinJapan.eu

Topic 4

Individual taxes

Topic 1 Topic 2 Topic 3 Contact

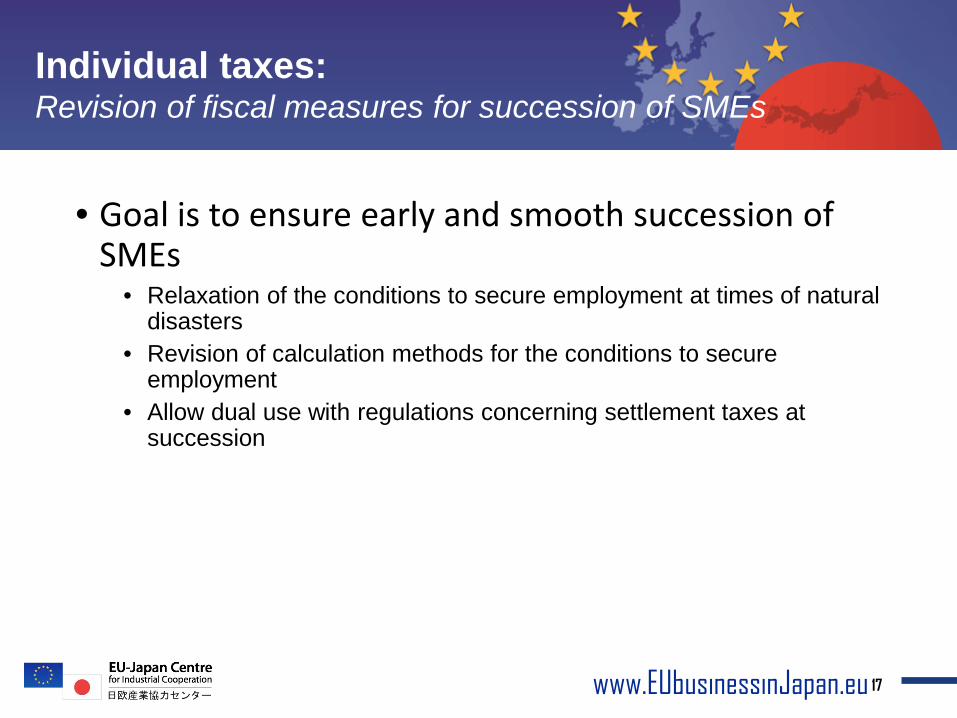

• Goal is to ensure early and smooth succession of SMEs

• Relaxation of the conditions to secure employment at times of natural disasters

• Revision of calculation methods for the conditions to secure employment

• Allow dual use with regulations concerning settlement taxes at succession

17www.EUbusinessinJapan.eu

Topic 4

Individual taxes:Revision of fiscal measures for succession of SMEs

Topic 1 Topic 2 Topic 3 Contact

18www.EUbusinessinJapan.eu

Topic 4

Individual taxes:Revision on inheritance taxes (foreign assets)

Topic 1 Topic 2 Topic 3 Contact

• Changes to spousal deduction• Establishment of “Reserve NISA”• Revision of fiscal measures for succession of SMEs• Revision on inheritance taxes (foreign assets)• Revision to fixed asset taxes

• High-rise mansions• Addition of items to special fixed asset taxes measures

regarding depreciable assets in local taxation• Beside machinery and devices also certain fixtures and tools.

19www.EUbusinessinJapan.eu

Topic 4

Individual taxes

Topic 1 Topic 2 Topic 3 Contact

• Extension of Filing due date of the corporate tax returns

• (Current 2 months, will be 6 months max)

• Fiscal facilities for remuneration of directors• Introduction of new reorganization rules: Tax Free

Corporate Spin-off• Limitation of the scope of SMEs eligible for Special

Taxation Measures• Revisions to the controlled foreign corporation and “tax

haven” rules (international tax)

20www.EUbusinessinJapan.eu

Topic 4

Other changes

Topic 1 Topic 2 Topic 3 Contact

21www.EUbusinessinJapan.eu

Topic 4

Outline of tax reform 2017Q&A

Q&A

Topic 1 Topic 2 Topic 3 Contact

JTPP Helpdesk

http://www.eubusinessinjapan.eu/issues/financial-issues/taxes-accounting

Email:[email protected]

22www.EUbusinessinJapan.eu

Topic 4

Outline of tax reform 2017