Embed Size (px)

Citation preview

Our Beliefs About InvestingThe 1st Global Philosophy for Disciplined, Long-Term Investors

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc.

Contents

Introduction and Purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Philosophy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Intellectual Rigor, Discipline, Patience and a Faith in the Future Matter . . . . . . . . . . . . . . . . . . . . . . . . 2

Emotions Influence Actions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Diversification, Asset Allocation and Efficiency Are Separate and Distinct Concepts . . . . . . . . . . . . . . . . . 3

Asset Allocation Matters More than Product Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Disciplined and Automated Rebalancing Improves Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Avoiding or Minimizing Losses Improves the Compounding Power of Wealth . . . . . . . . . . . . . . . . . . . . . 5

Annual Equity Market Returns Are Normally Distributed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Mean Reversion Happens. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

No One Can Predict the Future; Anyone Who Claims to Is Lying. If They Could, They Would Have Wealth Beyond

the Wildest Human Imaginings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Market Timing Does Not Work Over the Long Term, and Those Who Extol Its Virtues Suffer

from a Fallacy of Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Anyone Can Find Confirming Evidence, Especially Over the Short Term . . . . . . . . . . . . . . . . . . . . . . . . 8

Investment Skill Can Only Be Measured Over Long Time Periods . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Skillful Managers Can Be Identified . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Listening and Advice Are the Most Critical Factors in Developing and Executing a Plan to Honor Promises . . . . 8

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 1

Introduction and PurposeIt is an undeniable truth that the future is inherently uncertain. None of us can truly know with certainty what will happen next decade, next year, next month, next week, tomorrow or even a minute from now. As people, the reality of our uncertain future often creates feelings of anxiety. To manage these feelings, we take action to bring order, clarity and reason to the future beyond our control. When we think about our families, those around us we care about and the institutions we belong to, like our church or alma mater, we feel a sense of responsibility to their futures, not just to our own. To create certainty where uncertainty exists, we all take a simple action: we make promises. Promises to reach deep into our retirement and never be a burden to our loved ones, promises to give back charitably to our communities, promises to save the down payment for our first house and promises to send our children to any school they dream of. These promises are intensely personal to each of us, and for each of us they serve as a bond of honor, where our commitment to their reality stands firm in the face of uncertainty. 1st Global’s purpose is clear: to help the clients of our partner firms honor the important promises they make.

The purpose of this paper is to define our beliefs about investing. Called our philosophy, these 14 beliefs reflect the following definition: a “system of beliefs, values or tenets.”1 However, our beliefs also reach into the more classical definition of philosophy: “the rational investigation of the truths and principles of being, knowledge or conduct.”2

PhilosophyPhilosophers have for years debated the concept of certainty. As Ludwig Wittgenstein said, “No one but a philosopher would say ‘I know that I have two hands…’.”3 While we too could debate the philosophical concepts of certainty and knowledge, for purposes of this paper, we operate with the belief that investing with certainty is an unattainable goal.

Instead, in our context, we are concerned with describing a series of beliefs that guide our actions over the short, medium and long term. These actions are important, not only because they determine the actions of 1st Global and our Investment Committee, but more importantly because we can deliver the greatest results for our clients when we have mutual agreement as to these beliefs. We also do hold our beliefs in the more traditional sense of a philosophy as we continue to further our understanding, rationally, of the truths and principles behind investing. Investing is both a science and an art and has a rich history of brilliant minds that have shaped the past and influenced the future. We believe there is much yet to be learned, and at 1st Global we are committed to this philosophy as a journey.

“He who believes is strong; he who doubts is weak. Strong convictions precede great actions.”- Louisa May Alcott

Long-term investing is a journey, filled with roadblocks, doubts, errors and chance. But by knowing what you believe, you see the path before you more clearly and your conviction precedes the great action of honoring a promise. Here is what we at 1st Global believe:

1. Intellectual rigor, discipline, patience and a faith in the future matter.2. Emotions influence actions.3. Diversification, asset allocation and efficiency are separate and distinct concepts.4. Asset allocation matters more than product selection.5. Disciplined and automated rebalancing improves results.6. Avoiding or minimizing losses improves the compounding power of wealth.7. Annual equity market returns are normally distributed.8. Mean reversion happens.

1 philosophy. (n.d.). Collins English Dictionary - Complete & Unabridged 10th Edition. Retrieved August 28, 2010, from Dictionary.com Web site: http://dictionary.reference.com/browse/philosophy.

2 philosophy. (n.d.). Dictionary.com Unabridged. Retrieved August 28, 2010, from Dictionary.com Web site: http://dictionary.reference.com/browse/philosophy.3 Wittgenstein, Ludwig (1967). “Zettel” 405.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 2

9. No one can predict the future; anyone who claims to is lying. If they could, they would have wealth beyond the wildest human imaginings.

10. Market timing does not work over the long term, and those who extol its virtues suffer from a fallacy of composition.11. Anyone can find confirming evidence, especially over the short term.12. Investment skill can only be measured over long time periods.13. Skillful managers can be identified.14. Listening and advice are the most critical factors in developing and executing a plan to honor promises.

Intellectual Rigor, Discipline, Patience and a Faith in the Future MatterINTELLECTUAL RIGOR – Collins English Dictionary defines rigor with the following meanings: “strictness in judgment or conduct” or “maths, logic: logical validity or accuracy.”4 For our purpose, intellectual rigor means being thorough in exploring the science, whether economic, mathematical or behavioral, behind investment planning, asset allocation and investment manager due diligence. Shortcuts and opinions abound; however, it is only those truly committed to discovering the strict truths behind their actions who maximize their probability of success over the long term.

DISCIPLINE – To honor promises, we believe the discipline to save, to invest, to budget and to plan are critical. Reducing short-term temptations and delaying gratification is, and has been, a critical factor in helping the emerging affluent and affluent make the uncertain future certain. Continuing with a comprehensive plan, in the face of short-term fears, is discipline.

PATIENCE – Our invested wealth is predominantly designed to fund long-term future promises, as our short-term promises are usually funded from stable sources such as money markets or bank accounts. For many of us, our invested wealth is funding promises 10, 20, 30 or more years away. In fact, a 61-year-old couple has a joint life expectancy of 30 years; a 72-year-old couple, 20, and an 86-year-old couple, 10. Surely this highlights the reality that long-term plans are critical for many of us. So why would we be interested in short-term momentum and noise and pay the price of giving up what has historically worked?

FAITH IN THE FUTURE MATTER – Nick Murray sums this up best when he says, “This is the first characteristic of all successful long-term investors. It is impossible to invest successfully in a future of which one is fundamentally afraid. Thus, the great enemy of investment success isn’t ignorance, but fear. All human experience goes to teach us faith in the future, and especially faith in the American economy and its markets. The problem arises when media suggests that some economic or market setback is new and different: terrible in an unprecedented way, and therefore a disaster you’d better jump clear of.”5

Emotions Influence ActionsFor the 20 years ending December 31, 2010, the average investor in equity funds earned an annual return of 3.83 percent, compared with an average return of 9.14 percent for the S&P 500 over the same time period.6 So what accounts for the astonishing and depressing difference of 5.31 percent between the return of the stock market and the return of investors in equity funds? The answer is simple. Irrational investor behavior. When stock markets dropped during this 20-year time frame (as they often do), investors became fearful and sold their equity mutual funds. After markets fall, they have historically risen, and when they rose enough, investors became greedy and purchased equity mutual funds. This cycle continued to repeat itself, all the while reducing the average investor’s return over time due to the twin factors of fear and greed.

4 rigor. (n.d.). Collins English Dictionary - Complete & Unabridged 10th Edition. Retrieved August 27, 2010, from Dictionary.com Web site: http://dictionary.reference.com/browse/rigor.

5 Murray, Nick. 2007. “Six Steps to the Ninety-Ninth Percentile.” Nick Murray Interactive, February 2007. 6 “Quantitative Analysis of Investor Behavior, 2011” DALBAR, Inc. www.dalbar.com. Please see page 9 for additional disclosure.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 3

Diversification, Asset Allocation and Efficiency Are Separate and Distinct ConceptsWhile academically correct to consider these as a single, comprehensive concept, to ensure a complete understanding of the power of portfolio efficiency, it is important to eliminate naiveté by understanding the possible distinctions between these concepts.

Diversification is analogous simply to the age-old adage, “Don’t put all your eggs in one basket.” Naïve investors often practice diversification by selecting more than one financial advisor, and naïve financial advisors often practice diversification through product proliferation. At its core, diversification allows investors to reduce business-specific risk. This means that the fortunes of any single company will not have a significant impact on an investor’s fortune. Many studies have been done on random investments in securities and have found that as the number of investments increase, business-specific risk decreases. Indeed, because diversification can be accomplished easily, business-specific risk is also considered uncompensated risk. This is the basis of index investing, which reduces business-specific risk to a high degree and substantially provides investors with exposure to a “market.” This is a solid principle, but in isolation it is incomplete.

Asset allocation builds on the notion of diversification in that it looks at security or investment risks in the context of a portfolio rather than in isolation. Asset allocation incorporates the idea that the relationships between investments (called “correlations”) matter in creating a portfolio. By combining investments that exhibit low correlations, portfolio volatility can be reduced. However, too often the process naively stops here.

Efficiency is the answer. Armed with a set of beliefs about the future, such as projected returns of various asset classes, the volatility of these asset classes and the returns of each asset class in response to all others, we can construct a set of portfolios for which there is none that yields a higher likely return and a lower uncertainty of return.7 While portfolios can be naively diversified or illogically allocated and still offer some investor benefit, these approaches create inefficient (or sub-optimal) portfolios. As advisor to 1st Global’s Investment Committee, Dr. Harry Markowitz said in in his Nobel Prize-winning work, “it cannot be said of two efficient portfolios that ‘the first is clearly better than the second since it has a larger likely return and less uncertainty.’ All such cases have been eliminated.”8

Asset Allocation Matters More than Product SelectionIn a 2000 study conducted by Roger Ibbotson and Paul Kaplan,9 defended in 2010 by James Xiong, Thomas Idzorek, Peng Chen and Ibbotson, they described the importance of asset allocation policy decisions. In these important studies, they asked how much of a fund’s return is determined by their decisions about how to allocate investments among various broad asset classes. Their answer revealed a critical difference from the often-cited 1986 study by Gary Brinson, L. Randolph Hood and Gilbert Beebower.10 The 2010 Xiong, Ibbotson, Idzorek and Chen study looked at the three major components of return (the market, asset allocation decisions and active management), and concluded that “taken together, market return and asset allocation policy return in excess of market return dominate active portfolio management.”11

In fact, “the market movement component accounts for about 80 percent of the total return variations and dominates both detailed asset allocation policy differences and active portfolio management.”12 While this important study did go on to say that “within a peer group, asset allocation policy return in excess of market return and active portfolio management are equally important,” we must further explore the meaning of this statement.

First, we recognize that this study confirms our belief that asset allocation decisions matter, as it says that taken together with the market, these two components can account for 100 percent of return.

7 Markowitz, Harry M. “Portfolio Selection.” 1959: p. 6.8 Ibid.9 Ibbotson, Roger G., and Paul D. Kaplan. “Does Asset Allocation Policy Explain 40, 90, or 100 Percent of Performance?” Financial Analysts Journal Vol. 56. No. 1

(January/February 2000): 26–33.10 Brinson, Gary P., L. Randolph Hood, and Gilbert L. Beebower.“Determinants of Portfolio Performance.”Financial Analysts Journal. Vol. 42. No. 4 (July/August 1986): 39–44.11 Xiong, James X., Roger G. Ibbotson, Thomas M. Idzorek, and Peng Chen. “The Equal Importance of Asset Allocation and Active Management.”Financial Analysts

Journal. Vol. 66. No. 2 (March/April 2010): 22-30.12 Ibid.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 4

So, what about the seemingly equal weight of active portfolio management? While active management has the potential to matter, as properly indicated by this study, risk-adjusted excess return is a zero-sum game (before accounting for fees), where one manager’s outperformance is balanced by another’s underperformance. While active portfolio management matters, it is equally positive for some and negative for others (hence the reason that the market and asset allocation can account for 100 percent of return). This highlights the need to be invested in the proper asset allocation (positive) before considering active manager due diligence (positive or negative), should you choose to consider pursuing this component of returns. For more information on 1st Global’s active manager due diligence process, please see our companion paper, “The 1st Global Investment Manager Due Diligence Process: Enabling Promises Through Intellectual Rigor and Institutional Standards.”

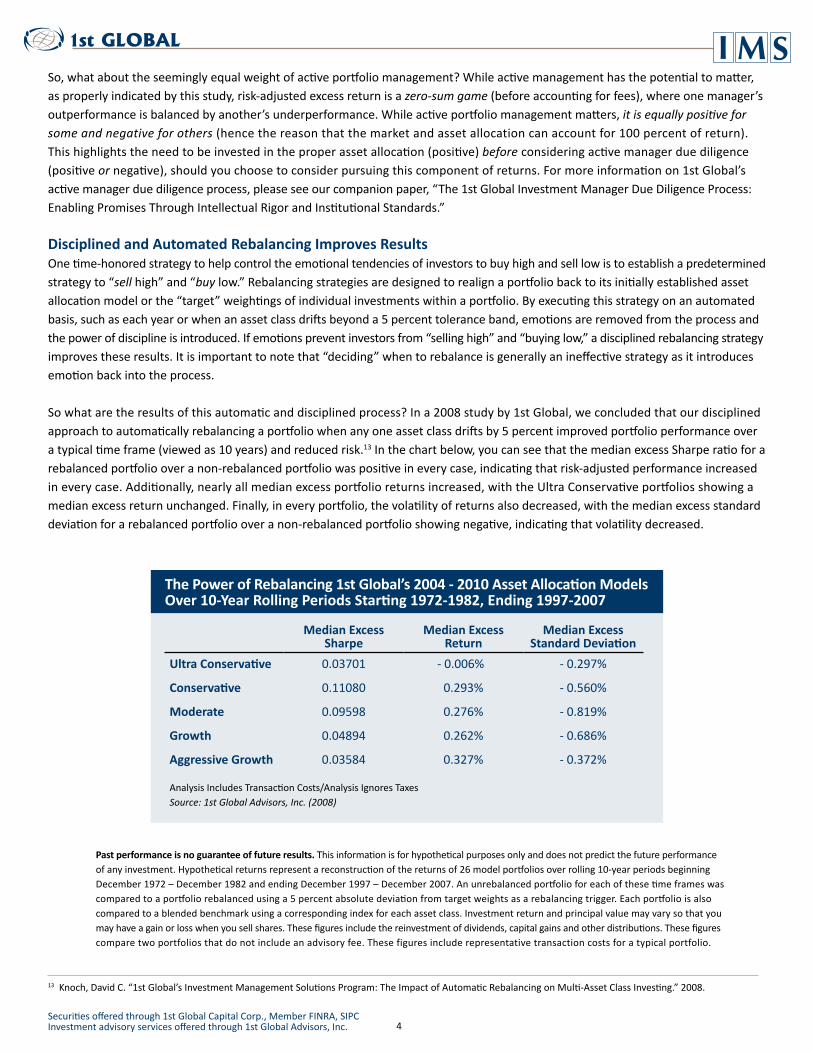

Disciplined and Automated Rebalancing Improves ResultsOne time-honored strategy to help control the emotional tendencies of investors to buy high and sell low is to establish a predetermined strategy to “sell high” and “buy low.” Rebalancing strategies are designed to realign a portfolio back to its initially established asset allocation model or the “target” weightings of individual investments within a portfolio. By executing this strategy on an automated basis, such as each year or when an asset class drifts beyond a 5 percent tolerance band, emotions are removed from the process and the power of discipline is introduced. If emotions prevent investors from “selling high” and “buying low,” a disciplined rebalancing strategy improves these results. It is important to note that “deciding” when to rebalance is generally an ineffective strategy as it introduces emotion back into the process.

So what are the results of this automatic and disciplined process? In a 2008 study by 1st Global, we concluded that our disciplined approach to automatically rebalancing a portfolio when any one asset class drifts by 5 percent improved portfolio performance over a typical time frame (viewed as 10 years) and reduced risk.13 In the chart below, you can see that the median excess Sharpe ratio for a rebalanced portfolio over a non-rebalanced portfolio was positive in every case, indicating that risk-adjusted performance increased in every case. Additionally, nearly all median excess portfolio returns increased, with the Ultra Conservative portfolios showing a median excess return unchanged. Finally, in every portfolio, the volatility of returns also decreased, with the median excess standard deviation for a rebalanced portfolio over a non-rebalanced portfolio showing negative, indicating that volatility decreased.

The Power of Rebalancing 1st Global’s 2004 - 2010 Asset Allocation Models Over 10-Year Rolling Periods Starting 1972-1982, Ending 1997-2007

Median Excess Sharpe

Median Excess Return

Median Excess Standard Deviation

Ultra Conservative 0.03701 - 0.006% - 0.297%

Conservative 0.11080 0.293% - 0.560%

Moderate 0.09598 0.276% - 0.819%

Growth 0.04894 0.262% - 0.686%

Aggressive Growth 0.03584 0.327% - 0.372%

Analysis Includes Transaction Costs/Analysis Ignores Taxes Source: 1st Global Advisors, Inc. (2008)

Past performance is no guarantee of future results. This information is for hypothetical purposes only and does not predict the future performance of any investment. Hypothetical returns represent a reconstruction of the returns of 26 model portfolios over rolling 10-year periods beginning December 1972 – December 1982 and ending December 1997 – December 2007. An unrebalanced portfolio for each of these time frames was compared to a portfolio rebalanced using a 5 percent absolute deviation from target weights as a rebalancing trigger. Each portfolio is also compared to a blended benchmark using a corresponding index for each asset class. Investment return and principal value may vary so that you may have a gain or loss when you sell shares. These figures include the reinvestment of dividends, capital gains and other distributions. These figures compare two portfolios that do not include an advisory fee. These figures include representative transaction costs for a typical portfolio.

13 Knoch, David C. “1st Global’s Investment Management Solutions Program: The Impact of Automatic Rebalancing on Multi-Asset Class Investing.” 2008.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 5

The information compiled cannot be considered as an indication of the investment ability of 1st Global Advisors, Inc. (hereinafter “1st Global”), and does not result from actual investment decisions by the firm. The investment results of 1st Global’s clients were materially different from the results portrayed in the model. THESE RESULTS ARE NOT THE ACTUAL PERFORMANCE FIGURES FOR ANY OF THE FIRM’S CLIENTS, AND IT SHOULD NOT BE ASSUMED THAT RECOMMENDATIONS MADE IN THE FUTURE WILL BE PROFITABLE. The above figures do not take tax effects into consideration. These results do not represent actual trading and do not reflect the impact that material economic and market factors might have had on the firm’s decision-making if the firm were managing a client’s money. The client’s own objectives, risk tolerance and financial circumstances may change over time, causing a change in the investment allocation that is used to manage that particular client’s portfolio. Each of the allocation models above represents one possible asset allocation strategy, and other strategies may have performed better or worse than the above portfolios over the same time period. The returns of the actual mutual funds selected as part of your portfolio will vary. Before investing in any mutual fund, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses contain this and other information about the funds and may be obtained from your financial advisor.

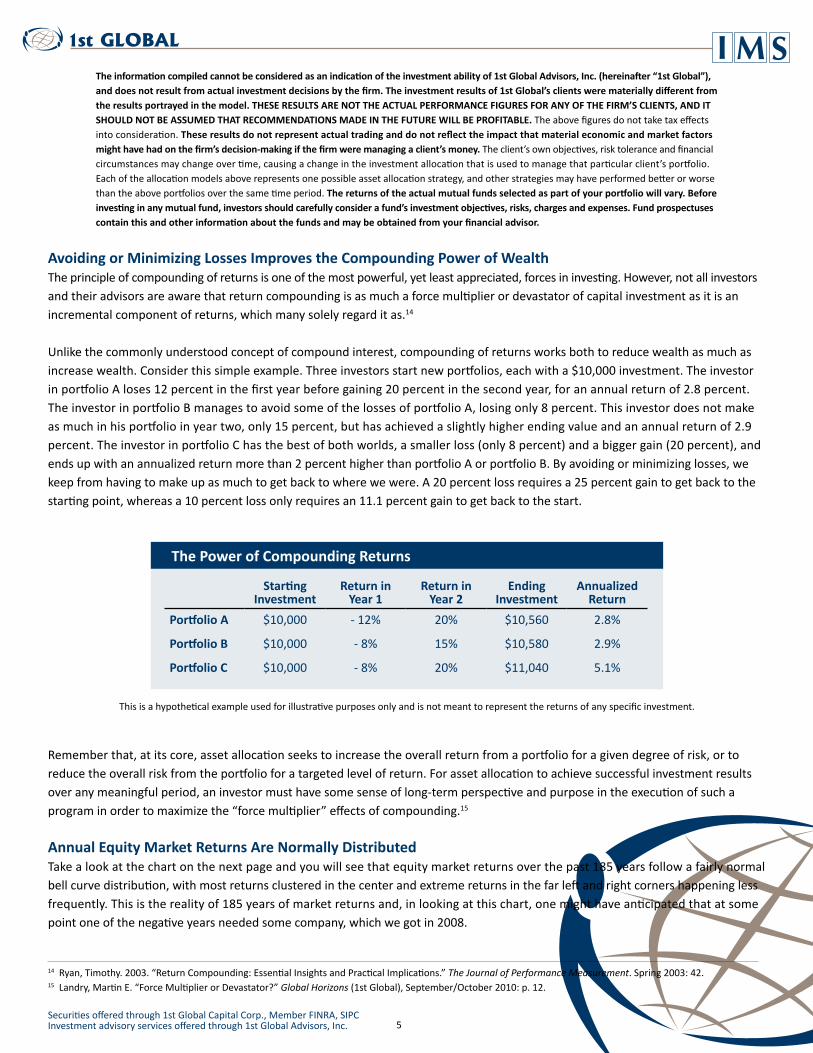

Avoiding or Minimizing Losses Improves the Compounding Power of WealthThe principle of compounding of returns is one of the most powerful, yet least appreciated, forces in investing. However, not all investors and their advisors are aware that return compounding is as much a force multiplier or devastator of capital investment as it is an incremental component of returns, which many solely regard it as.14

Unlike the commonly understood concept of compound interest, compounding of returns works both to reduce wealth as much as increase wealth. Consider this simple example. Three investors start new portfolios, each with a $10,000 investment. The investor in portfolio A loses 12 percent in the first year before gaining 20 percent in the second year, for an annual return of 2.8 percent. The investor in portfolio B manages to avoid some of the losses of portfolio A, losing only 8 percent. This investor does not make as much in his portfolio in year two, only 15 percent, but has achieved a slightly higher ending value and an annual return of 2.9 percent. The investor in portfolio C has the best of both worlds, a smaller loss (only 8 percent) and a bigger gain (20 percent), and ends up with an annualized return more than 2 percent higher than portfolio A or portfolio B. By avoiding or minimizing losses, we keep from having to make up as much to get back to where we were. A 20 percent loss requires a 25 percent gain to get back to the starting point, whereas a 10 percent loss only requires an 11.1 percent gain to get back to the start.

The Power of Compounding Returns

Starting Investment

Return in Year 1

Return in Year 2

Ending Investment

Annualized Return

Portfolio A $10,000 - 12% 20% $10,560 2.8%

Portfolio B $10,000 - 8% 15% $10,580 2.9%

Portfolio C $10,000 - 8% 20% $11,040 5.1%

This is a hypothetical example used for illustrative purposes only and is not meant to represent the returns of any specific investment.

Remember that, at its core, asset allocation seeks to increase the overall return from a portfolio for a given degree of risk, or to reduce the overall risk from the portfolio for a targeted level of return. For asset allocation to achieve successful investment results over any meaningful period, an investor must have some sense of long-term perspective and purpose in the execution of such a program in order to maximize the “force multiplier” effects of compounding.15

Annual Equity Market Returns Are Normally DistributedTake a look at the chart on the next page and you will see that equity market returns over the past 185 years follow a fairly normal bell curve distribution, with most returns clustered in the center and extreme returns in the far left and right corners happening less frequently. This is the reality of 185 years of market returns and, in looking at this chart, one might have anticipated that at some point one of the negative years needed some company, which we got in 2008.

14 Ryan, Timothy. 2003. “Return Compounding: Essential Insights and Practical Implications.” The Journal of Performance Measurement. Spring 2003: 42. 15 Landry, Martin E. “Force Multiplier or Devastator?” Global Horizons (1st Global), September/October 2010: p. 12.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 6

Source: Value Square Asset Management, A New Historical Database for the NYSE 1815 to 1925: Performance and Predictability, Yale School of Management working paper 2000; Ibbotson & Associates SBBI data. Past performance is no guarantee of future results. This chart is for illustration purposes only and does not represent returns of any speci�c investments.

1st Global Capital Corp., Member FINRA, SIPC

2009: 24 %

38%2008:

193120081937

200219741930190718571839

20011973196619571941192019171910189318841873185418411837183118281825

2007200519941993199219871984197819701960195619481947192319161912191119061902189918961895189418911889188818871881187718751874187218711870186918681867186618651859185618441842184018361826

2000199019811977196919621953194619401939193419321929191419131903189018831882187618611860185318511845183518331827

20062010

20041988198619791972197119681965196419591952194919441926192119191918190519041898189718921886187818641858185518501849184818471838183418321829

200920031999199819961983198219761967196319611951194319421925192419221915190919011900188018521846

199719951991198919851980197519551950194519381936192719081830

19581935192818631843

19541933188518791862

(50)-(40)% (40)-(30)% (30)-(20)% (20)-(10)% (10)-0% 0-10% 10-20% 20-30% 30-40% 40-50% 50-60%

Providing Perspective on Equity Returns

(1825-2010)

Source: Value Square Asset Management, A New Historical Database for the NYSE 1815 to 1925: Performance and Predictability, Yale School of Management working paper 2000; Ibbotson & Associates SBBI data. Past performance is no guarantee of future results. This is for illustration purposes only. 1st Global Capital Corp., Member FINRA, SIPC

The point of this chart is that the average return in the equity markets has followed a reasonably predictable pattern over time. This pattern has two distinct characteristics that have always been true. Most returns are pretty close to the average return, which is why we see the largest stack of returns in the 0 to 10 percent range, where the long-term average falls. Big wins and big losses occur less frequently than average wins do. This is important because this pattern has historically repeated. The bigger the win or the bigger the loss, the more unlikely it becomes. You cannot predict when the numbers will fall out, but as shown in this chart, they will indeed fall out. The second characteristic is that most of the returns are greater than zero. This pattern has also historically repeated itself. While past performance is no guarantee of future results, the stock market has historically rebounded after periods of negative performance. This is the empirical proof behind our belief in intellectual rigor, discipline, patience and faith in the future.

Mean Reversion HappensReversion to the mean (average), also called regression to the mean, is the statistical phenomenon stating that the greater a random variable deviates from its mean, the greater the likelihood that the next variable will be closer to the mean. In other words, an extreme event is likely to be followed by a less extreme event.16

An intuitive way to think about mean reversion in the value of investments is to assume that returns react to any deviation from the long-term average. If the return is above the average in one period, there is a force that pushes it downward in following periods; if the return is below the average, it is pushed upward.17 The implications of this for investors are contained in our belief that emotions impact returns. If investors buy when values are above the mean, they increase the probability of losing money, and if they sell below the mean, they also increase the probability of losing money. If cheap investments will probably rise and expensive investments will probably fall, these factors play a critical role in behavior, expectations and timing. If things will turn out OK in the end, you need to wait for the end.

16 Weisstein, Eric W. “Reversion to the Mean.” From MathWorld—A Wolfram Web Resource. http://mathworld.wolfram.com/ReversiontotheMean.html.17 Koijen, Ralph S. J., Juan Carlos Rodriguez, and Alessandro Sbuelz. “Momentum and Mean-Reversion in Strategic Asset Allocation.” EFA 2006 Zurich Meetings.

January 27, 2009. Available at SSRN: http://ssrn.com/abstract=687205.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 7

In a 2009 study by Koijen, Rodriguez and Sbuelz, they concluded that strategic asset allocation decisions were significant over periods greater than five years. This is because as time passes, momentum tends to influence the value of investments more in the short-term and reversion to the mean tends to influence the value of investments more over the long-term. This study shows that short-term investors should respond to price momentums, while long-term (more than five years) investors should ignore momentum in favor of mean reversion.18

No One Can Predict the Future; Anyone Who Claims to Is Lying. If They Could, They Would Have Wealth Beyond the Wildest Human ImaginingsWhile an age-old temptation, we believe firmly that humans have not yet acquired the knowledge to predict the future. However, as logical as this statement appears, this is not recognized as a universal truth. Performing a simple Web search on the concept will bring up everything from tarot cards, to palm readers to psychics, to readers of Fibonacci spirals, to science fiction and neuroscience. This is not to say that mathematic and scientific advances have not dramatically improved our ability to forecast and forewarn, merely that certainty about our tomorrows is ultimately unknowable.

This concept is a perpetual temptation in the world of investing, and practitioners of investment hocus-pocus prey upon the very need for certainty described in the introduction. But they are wrong, and experiential evidence tells us so. Consider this: if these alchemic promises were true, why share it? Wouldn’t those who hold this source of knowledge have long used it to enrich themselves before others?

Now to the world of reality. What does this mean for the investment manager selection process? In a 1995 article from the Financial Analysts Journal, Kahn and Rudd state that using only historical information, there is no evidence of performance persistence for equity mutual funds, concluding that there can only be two possible decisions when choosing equity mutual funds for investment: use index funds or include information beyond historical performance.19 The latter is a critical mission of 1st Global’s due diligence process.

Market Timing Does Not Work Over the Long Term, and Those Who Extol Its Virtues Suffer from a Fallacy of CompositionThe promise of market timing has long held appeal for retail investors. Perhaps you’ve heard the stories of market prognosticators who can help you sell at the top and buy at the bottom, or the theory of the market acting as a living organism demonstrating Fibonacci spirals just like seashells, or the late-night advertisements for trading classes designed to quickly make you millions.

Well-Known Empirical Studies Documenting Unprofitability of Market-Timing Strategy, on Average

Authors (Year)Group that FAILS to Successfully Time the Market, on Average

Treynor and Mazuy (1966) Mutual funds

Hendricksson and Merton (1981) Mutual funds

Kon (1983) Mutual funds

Chang and Lewellen (1984) Mutual funds

Becker, et al. (1998) Asset allocation funds

Coggin and Hunter (1993) Equity pension funds

Barber and Odean (2000) Investment clubs

Graham and Harvey (1996, 1997) Investment newsletters

Chance and Hemler (2001) Professional market-timers

Source: Vanguard Investment Counseling & Research

18 Koijen, Ralph S. J., Juan Carlos Rodriguez, and Alessandro Sbuelz. “Momentum and Mean-Reversion in Strategic Asset Allocation.” EFA 2006 Zurich Meetings. January 27, 2009. Available at SSRN: http://ssrn.com/abstract=687205.

19 Kahn, Ronald N., and Andrew Rudd. “Does Historical Performance Predict Future Performance?” Financial Analysts Journal. Vol. 51, No. 6 (Nov. - Dec., 1995): p. 43-52.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 8

But empirical evidence shows that market timing follows the age-old adage, “If it looks too good to be true, it probably is.” In a seminal 1966 study on market timing, Treynor and Mazuy found significant market-timing ability in only one of 57 mutual funds;20 and in another mutual fund study, Hendricksson and Merton (1981) documented positive ability in only three of 116 mutual funds.21

Anyone Can Find Confirming Evidence, Especially Over the Short TermConfirmation bias is a problematic aspect of human reasoning whereby one selectively gathers, or gives undue weight to, evidence that supports one’s position while neglecting to gather, or discounting, evidence that would tell against it.22 As humans, we suffer from a natural tendency to look for evidence that is directly supportive of hypotheses we favor.23 This is particularly relevant in the world of investing, where opinions abound railing against the science of investing, the value of strategic asset allocation, the truth about long-term investing and the reality that this time is not different. The same old tried-and-true methods that have worked for years are boring and dull, while the get-rich-quick schemes and the beliefs about clairvoyant forecasting prey upon the average investor. We believe that each of the points of our philosophy holds the simple answers to helping clients honor the important promises they make.

Investment Skill Can Only Be Measured Over Long Time PeriodsConsider a season of professional baseball. Do we play only three or four games before beginning the World Series? No. To separate luck and skill, we play 162 games before beginning the playoffs. In separating investment skill from investment luck, the same need for many points of data exists. In fact, to determine with 95 percent confidence that a manager belongs in the top quartile will require 16 years of observations24—just more than a baseball season’s worth of monthly returns.

Skillful Managers Can Be IdentifiedThe belief most relevant to our investment manager due diligence process is that we believe skillful managers can be identified. Not with certainty and not with a precise prediction about their future performance, but we can develop a disciplined process, applied with consistency, rigor and skill, to find those investment managers with the greatest chance, in our view, of helping clients honor their promises. Our companion paper, “The 1st Global Investment Manager Due Diligence Process: Enabling Promises Through Intellectual Rigor and Institutional Standards,” endeavors to enlighten you on our process.

Listening and Advice Are the Most Critical Factors in Developing and Executing a Plan to Honor PromisesIt is our belief that the most skilled wealth management professionals in the world will fail to help their clients honor the promises they make unless they listen carefully to understand those promises. Once a wealth management professional understands their clients’ promises and what matters to them about money, the next most critical factor is the ability to pair this understanding with a comprehensive and competent plan for action. Only when these twin imperatives have been executed to a level of excellence will asset allocation and due diligence to determine product selection ever matter. All the best listening and advice will enable a client a real chance of honoring promises, even when paired with average due diligence and product selection. However, the wrong listening and the wrong advice paired with the world’s most spectacular due diligence and product selection is unlikely to ever allow a client to honor his or her promises.

ConclusionIn summary, before beginning any journey, before committing any wealth of money or time, before taking action that will change your life, know what you believe. Armed with your conviction, you will possess the clarity you need to persevere in your journey, your change, your investment plan, your promise. At 1st Global, our investment management programs are shaped by our beliefs. Knowing our purpose, we define our philosophy. Armed with our philosophy, we shape our process and create the actions that define accountability and deliver results, and we are steadfast in our commitment because we have purpose and we have beliefs. With our process, we find the people to deliver excellence. Our philosophy supports our purpose to help the clients of our partner firms honor the important promises they make.

“People create their own questions because they are afraid to look straight. All you have to do is look straight and see the road, and when you see it, don’t sit looking at it—walk.”

- Ayn Rand

20 Treynor, J.L., and K. Mazuy. “Can Mutual Funds Outguess the Market?” Harvard Business Review. 1966: 44:131–36.21 Henriksson, Roy D., and Robert C. Merton. “On Market Timing and Investment Performance. II. Statistical Procedures for Evaluating Forecasting Skills.” Journal of

Business. 54 (4, October): 513–33. 22 Nickerson, Raymond S. “Confirmation Bias: A Ubiquitous Phenomenon in Many Guises.” Review of General Psychology 1998. Vol. 2, No. 2:175-220.23 Ibid.24 Grinold, Richard C., and Ronald N.Kahn. “Active Portfolio Management – A Quantitative Approach for Producing Superior Returns and Controlling Risk, Second Edition,” p. 480.

Securities offered through 1st Global Capital Corp., Member FINRA, SIPCInvestment advisory services offered through 1st Global Advisors, Inc. 9

DisclosuresThe indexes described in this paper are unmanaged indexes of common stocks, bonds or other securities. The volatility of the indexes may be materially different from the individual performance attained by a specific investor. In addition, the investor’s holdings may differ significantly from the securities that comprise the indexes. The indexes are disclosed to allow for comparison of the investor’s performance to that of certain well-known and widely recognized benchmarks of investment performance.

Emerging Market Stocks: Involve greater risk than investing in more established foreign market stocks. Such risks include currency exchange rates, political and economic upheaval, the lack of information about companies, low market liquidity and differences in financial and accounting standards.

High-Yield Bonds: Have a greater risk of price fluctuation and loss of principal and income when compared to U.S. government securities such as U.S. Treasury bonds and bills, which offer a guarantee of repayment of principal and interest if held to maturity.

International Stocks: Additional investing risks include fluctuations in the value of the U.S. dollar relative to the values of other currencies, custody arrangements made for foreign holdings, political risks, differences in accounting procedures and the amount of public information disclosed by non-U.S. exchange-listed companies.

Microcap Stocks: May involve risks not associated with investing in more established companies. These stocks may be more volatile because they may be less liquid or financially secure and their product lines are not as diverse. Microcap stock investments can be highly speculative.

Disclosure for “Quantitative Analysis of Investor Behavior, 2011.” DALBAR, Inc. www.dalbar.com

Equity benchmark performance and systematic equity investing examples are represented by the Standard & Poor’s 500 Composite Index, an unmanaged index of 500 common stocks generally considered representative of the U.S. stock market. Indexes do not take into account the fees and expenses associated with investing, and individuals cannot invest directly in any index. Past performance cannot guarantee future results.

Bond benchmark performance and systematic bond investing examples are represented by the Barclays Aggregate Bond Index, an unmanaged index of bonds generally considered representative of the bond market. Indexes do not take into account the fees and expenses associated with investing, and individuals cannot invest directly in any index. Past performance cannot guarantee future results.

Average stock investor, average bond investor and average asset allocation investor performance results are based on a DALBAR study, “Quantitative Analysis of Investor Behavior (QAIB), 2011.” DALBAR is an independent, Boston-based financial research firm. Using monthly fund data supplied by the Investment Company Institute, QAIB calculates investor returns as the change in assets after excluding sales, redemptions and exchanges. This method of calculation captures realized and unrealized capital gains, dividends, interest, trading costs, sales charges, fees, expenses and any other costs. After calculating investor returns in dollar terms, two percentages are calculated for the period examined: total investor return rate and annualized investor return rate. Total return rate is determined by calculating the investor return dollars as a percentage of the net of the sales, redemptions and exchanges for the period.

The returns of the actual investments selected as part of your portfolio will vary. Before investing in any mutual fund, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses contain this and other information about the funds and may be obtained from your financial advisor.

Neither asset allocation nor diversification assures a profit or protects against a loss in declining markets.

©2011 1st Global Advisors, Inc.

This paper was prepared by 1st Global’s Investment Management Research Group and was reviewed and approved by the 1st Global Advisors, Inc. Investment Committee.

Securities offered through 1st Global Capital Corp. Member FINRA/SIPCinvestment Advisory Services offered through 1st Global Advisors Inc.

8150 N. Central Expy. Suite 500

Dallas, Texas 75206(877) 959-8400

www.1stGlobal.com