Embed Size (px)

Citation preview

Abdul Ghafur Memorial Lecture 2018

The Uncomfortable Truth Recent Economic Growth Performance

of Bangladesh

by Debapriya Bhattacharya, PhD

Distinguished Fellow Centre for Policy Dialogue (CPD) <[email protected]>

Organised by

4 November 2018

ii D. Bhattacharya: The Uncomfortable Truth

Published by

Bangladesh Institute of Development Studies

E-17, Agargaon, Sher-e-Bangla Nagar

G.P.O. Box No. 3854, Dhaka - 1207, Bangladesh

Phone: 9143441-8

Fax: 880-2-8141722

E-mail: [email protected]

Website: www.bids.org.bd

Copyright Debapriya Bhattacharya, November 2018

This document has been set in Cambria

Cover and design concept by Avra Bhattacharjee, CPD.

Printed in Al-Helal Enterprise, 4 Sobhanbag, Mirpur Road, Dhaka-1207.

D. Bhattacharya: The Uncomfortable Truth iii

Dr Abdul Ghafur (1935–2002)

Dr Abdul Ghafur is no more with us. He passed away in Dhaka on 27

February 2002 in his sixty-seventh year. Dr Ghafur was born on 25 March

1935 in Barisal. He obtained an M.A. in Economics from the University of

Dhaka in 1961 and a Ph.D. from the University of Iowa, U.S.A. in 1973.

Dr Ghafur joined PIDE as a Staff Economist in 1963. He became a Research

Director at BIDS in 1984 and served in this position till his retirement in

1995. As a prominent member of its research staff, he had a long and close

association with the Institute. He holds us in debt for the many contributions

he made to further the interests of BIDS.

Dr Ghafur was the president of the Bangladesh Economic Association during

1979–81; a member of the Industrial Wage and Productivity Commission in

1981/82; a fellow of Equity, Diversity, and Inclusion (EDI) and directed EDI

sponsored BIDS training programme for a number of years. Dr Ghafur

published a number of articles in the area of informal trade, public

expenditure policies, food policy and project impact evaluation. He was one

of the very few economists in Bangladesh, thoroughly conversant with both

neo-classical and Marxian economics.

Throughout his professional career, Dr Ghafur was well-known for deep

social commitments and radical social ideas. He was associated with

progressive social and civic movements since his student days as activist

and, later, along with other titans of the Bangladesh economics profession,

emerged as an influential advocate of the rights of the most disadvantaged

social and ethnic groups in our society. A passionate social thinker dedicated

to the advancements of the downtrodden people, he raised his voice in

various professional and social forums in the course of the last three decades

in their struggle for human rights and social justice.

In his death, the profession has lost an eminent economist and the people —

a champion of their cause. We join the nation in mourning this profound loss

to our profession.

iv D. Bhattacharya: The Uncomfortable Truth

List of Publications

Ghafur, A., Roy, D. K., Mohammad, Y., Raihan, A., Saha, S. C., & Roy, R. K. (1996). Socio-economic impact of fourth flood control and drainage project. (Working paper new series no. 18). Dhaka: Bangladesh Institute of Development Studies (BIDS). Ghafur, A., Roy, D. K., & Mohammad, Y. (1995). Fourth flood control and drainage project: An evaluation. Dhaka: Bangladesh Institute of Development Studies (BIDS). Ghafur, A. (1995). The barind integrated area development project: an evaluation. Dhaka: BIDS. Ghafur, A. (1995). Financial Sector Reform: An Overview. Experiences with Economic Reform: A Review of Bangladesh’s Development 1995, 87-100. Dhaka: Centre for Policy Dialogue (CPD) & University Press Limited (UPL). Ghafur, A., Chowdhury, O. H., Roy, D. K., & Center on Integrated Rural Development for Asia and the Pacific. & International Development Research Centre (Canada). (1994). Public expenditure and poverty alleviation in Bangladesh. Dhaka: Centre on Integrated Rural Development for Asia and the Pacific. Ghafur, A., Islam, M., Faiz, N. (1991). Illegal international trade in Bangladesh: Impact on the domestic economy (phase-II): Draft report. Dhaka: Bangladesh Institute of Development Studies (BIDS). Ghafur, A., Islam, M., Faiz, N. (1990). Illegal international trade in Bangladesh: impact on the domestic economy (phase-I): Final report. Dhaka: Bangladesh Institute of Development Studies (BIDS). Ghafur, A. (1987). Financing of public sector development expenditure: The case of Bangladesh. Dhaka: BIDS. Ghafur, A. (1987). Amader swadhinata sangram (Our liberation struggle). Dhaka: Islamic Foundation Bangladesh. Ghafur, A. (1973). Dynamic differential tax incidence: theory and applications. Iowa: Iowa University, Graduate College.

D. Bhattacharya: The Uncomfortable Truth v

Contents

1. Remembering Ghafur Bhai 1

2. Revisiting Bangladesh’s Recent Growth Performance ........................... 3

3. The Nature of Recent Economic Growth ................................................... 12

4. In Search of a Conclusion ............................................................................... 29

References ............................................................................................................... 34

vi D. Bhattacharya: The Uncomfortable Truth

List of tables

Table 1: Ranking of Bangladesh According to GDP/GNI and Per 3

Capita GDP/GNI

Table 2: Countries Surpassed by Bangladesh in Terms of GDP Per 4

Capita

Table 3: Projected Ranking Changes by 2030 Compared to 2018 5

Table 4: Average Growth Rates (1991–2017): GDP/GNI, GDP/GNI 6

Per Capita and GDP/GNI Growth Rates

Table 5: Changing Configuration of Source of GDP Growth (in 8

percentage point)

Table 6: Changes in Sector-wise GDP Share (%) 9

Table 7: Poverty Rate (%) in Bangladesh by Residence 10

Table 8: GDP Growth and Poverty Reduction (in percentage point) 11

Trends in Bangladesh

Table 9: Percentage Share of Consumption at Household Level (%), 13

and Gini Coefficient by Residence

Table 10: Per Capita GNI and Income Gini Index 14

Table 11: Percentage Share of Income at Household Level (%), and 15

Gini Coefficient by Residence

Table 12: Average Household Real Income Per Month (adjusted to 16

2015-16 CPI)

Table 13: Percentage Share of Wealth at Household Level (%), and 17

Gini Coefficient by Residence

Table 14: Employment by Broad Economic Sectors 18

Table 15: Distribution of Youth Unemployment by Education Level (% 20

of total unemployed youth)

Table 16: Under- Five Mortality Rate and Neonatal Mortality Rate 22

(deaths per 1,000 live births) by Wealth Status

Table 17: Prevalence of Stunting and Wasting among Children Under 24

Five Years of Age by Wealth Status

Table 18: Enrolment of Children Aged 6-10 and Aged 11-15 Years 25

by Residence and Poverty Status, 2016

Table 19: Poverty Rate (%) in Bangladesh by Division 27

D. Bhattacharya: The Uncomfortable Truth vii

List of figures

Figure 1: Per Capita GDP and Per Capita GNI 7

Figure 2: Change in Real General Wage Rate Index (WRI) (%) 21

Figure 3: Latin American Countries: Initial Income Inequality and 30

Reduction Level (2000 to 2010)

Figure 4: Voice and Accountability Index of Bangladesh (Estimate 32

and Ranking)

Acknowledgement

The author is grateful to Mr Suman Biswas, former Research Associate, CPD

and Mr Syed Muhtasim Fuad, Programme Associate, CPD for data support.

Research assistance was provided by Ms Ismum Nawar, Programme

Associate, CPD.

viii D. Bhattacharya: The Uncomfortable Truth

1. Remembering Ghafur Bhai

It is a privilege and a joy for me to join all of you here today to celebrate the

life and works of late Dr Abdul Ghafur. Dr Ghafur was a talented economist;

he sought to put his expertise to the service of the marginalised and working

people of Bangladesh. In 1971, he actively organised the overseas movement

in favour of the Liberation War.

Dr Ghafur was a mentor, a comrade and a friend. He always extended his

uninhibited support and cooperation to his junior colleagues. Dr Ghafur was

a generous, caring and likeable person who earnestly walked the talk. I am

humbled by BIDS’s thoughtful decision to invite me to deliver the third

lecture (2018) in memory of Dr Ghafur.

I came to know Dr Ghafur or rather Ghafur Bhai in 1984 on my return from

abroad and at the beginning of my association with BIDS. I fondly remember

the late afternoons of the second half of 1980s when we were deeply

engaged in trying to develop an economic manifesto for the toiling people of

Bangladesh. In the later part of the 1980s, we worked together to imbue the

anti-autocracy agenda with livelihood concerns of the working class. He used

to provide guidance on how to embed pro-poor economic issues in political

declarations and manifestos – a task that we are obliged to pursue till date

as an expression of our respect to Ghafur Bhai.

Indeed, a large part of my interactions with Ghafur Bhai was to take place at

the meeting of the Economists’ Group of the Communist Party of Bangladesh.

We used to look up to him for leadership and advice as he had an exceptional

2 D. Bhattacharya: The Uncomfortable Truth

quality of interpreting practical policy issues from the socio-economic class

approach.

Dr Ghafur was a professional leader. I have had the privilege of closely

working with him when he was the President of the Bangladesh Economic

Association (BEA). He put in efforts to mobilise the researchers, academics

and executives to service social goals through their respective vocations.

Indeed, it was due to Ghafur Bhai’s inspiration, that I went on to serve BEA

as its General Secretary for three consecutive terms.

Dr Ghafur was a sincere well-wisher of the Centre for Policy Dialogue (CPD).

He was part of the initial set of authors when CPD in 1995 launched its

flagship programme titled “Independent Review of Bangladesh’s

Development” (IRBD). Over the last two decades and more, CPD did carry

forward that legacy with distinction.

Dr Ghafur was essentially a macro-economist with wide ranging interest. My

first encounter with his scholarship was through his works on public

expenditure and taxation. Ghafur Bhai led the pioneering research in

Bangladesh on informal cross-border trade. In later years, he worked on

flood-related issues. Even a cursory look at his works will make evident his

grasp over conceptual issues and the clarity with which he applied them in

empirical analysis. However, his volume of published works do not do justice

either to his talent or to his expertise.

At the end of the day, Ghafur Bhai was a pro-people thought leader, if I may

say, a public intellectual. While choosing my today’s lecture theme, I tried to

anticipate what would have concerned him at this juncture of Bangladesh’s

D. Bhattacharya: The Uncomfortable Truth 3

economic development. I can very well imagine Ghafur Bhai saying –

“Economic growth rate is pretty good, but how equitably the benefits are

being distributed?” Thus, as a way to pay homage to Dr Ghafur, I decided to

talk about the nature of the recent growth performance of our country.

2. Revisiting Bangladesh’s Recent Growth Performance

Global Perspective

It is by now well recognised that the Bangladesh economy has achieved

spectacular economic growth in the recent past. Indeed, the country can now

boast of a USD 275 billion worth of domestic economy (2017–18). The

robust economic growth rate has remarkably advanced the country in global

ranking—both in terms of size of the economy and per capita income (see

Table 1).

Table 1: Ranking of Bangladesh According to GDP/GNI and Per Capita

GDP/GNI

Source: Based on World Development Indicators (World Bank, n.d.-a: accessed on 21/10/2018).

BD Ranking

by

2000 2005 2010 2015 2016 2017 Closest Countries (2017)

Above Below

GDP in

current USD

49

(199)

56

(204)

59

(203)

46

(200)

44

(195)

43

(188)

Chile (41);

Finland (42)

Egypt (44);

Vietnam (45)

Per capita

GDP in

current USD

164

(199)

176

(204)

178

(203)

165

(200)

158

(195)

150

(188)

Ghana (148);

Pakistan

(149)

Zambia (151);

Kenya (152)

GNI in

current USD

46

(189)

54

(194)

55

(193)

44

(191)

44

(189)

42

(185)

Ireland (40);

Chile (41)

Finland (43),

Egypt (44)

GNI per

capita, Atlas

Method

(current

USD)

148

(184)

160

(192)

166

(191)

158

(189)

153

(188)

147

(184)

Cote d'Ivoire

(145); Ghana

(146)

Kenya (148);

Congo (149)

4 D. Bhattacharya: The Uncomfortable Truth

In terms of GDP size, the country got elevated from 49th position (among 199

countries) in 2000 to 43rd position (among 188 countries) in 2017. From the

vantage point of GNI size, the country moved up by four positions during the

comparable period. In terms of GDP per capita income measure,

Bangladesh’s progress had been no less discernible. The country progressed

by 14 ranks (from 164th place to 150th) between 2000 and 2017 as its per

capita GDP increased.

The list of countries that were overtaken by Bangladesh between 2000 and

2017– based on per capita GDP measure – is quite interesting (see Table 2).

The number of such countries was nine including Cambodia, Cameroon,

Haiti, Kenya, Laos, Mali, Myanmar, Uzbekistan and Zimbabwe. Laos;

however, resurpassed Bangladesh in 2006.

Table 2: Countries Surpassed by Bangladesh in Terms of GDP Per Capita

2000-05 2006-2010 2010-15 2015-2017

Haiti, Zimbabwe

and Laos (Laos

resurpassed

Bangladesh in

2006)

Mali Cambodia and

Myanmar

Cameroon, Kenya

and Uzbekistan

Source: Based on World Development Indicators (World Bank, n.d.-a: accessed on 21/10/2018).

Bangladesh’s economic growth performance has earned wide-ranging global

accolade. One may recall the reports of the Goldman Sachs (O’Neill, Wilson,

Purushothaman and Stupnytska, 2005) that included the country in the

group of Next-11. The Citigroup (Buiter, Rahbari, and Kupciuniene, 2011)

later made the country part of 11 Global Growth Generators (G3).

D. Bhattacharya: The Uncomfortable Truth 5

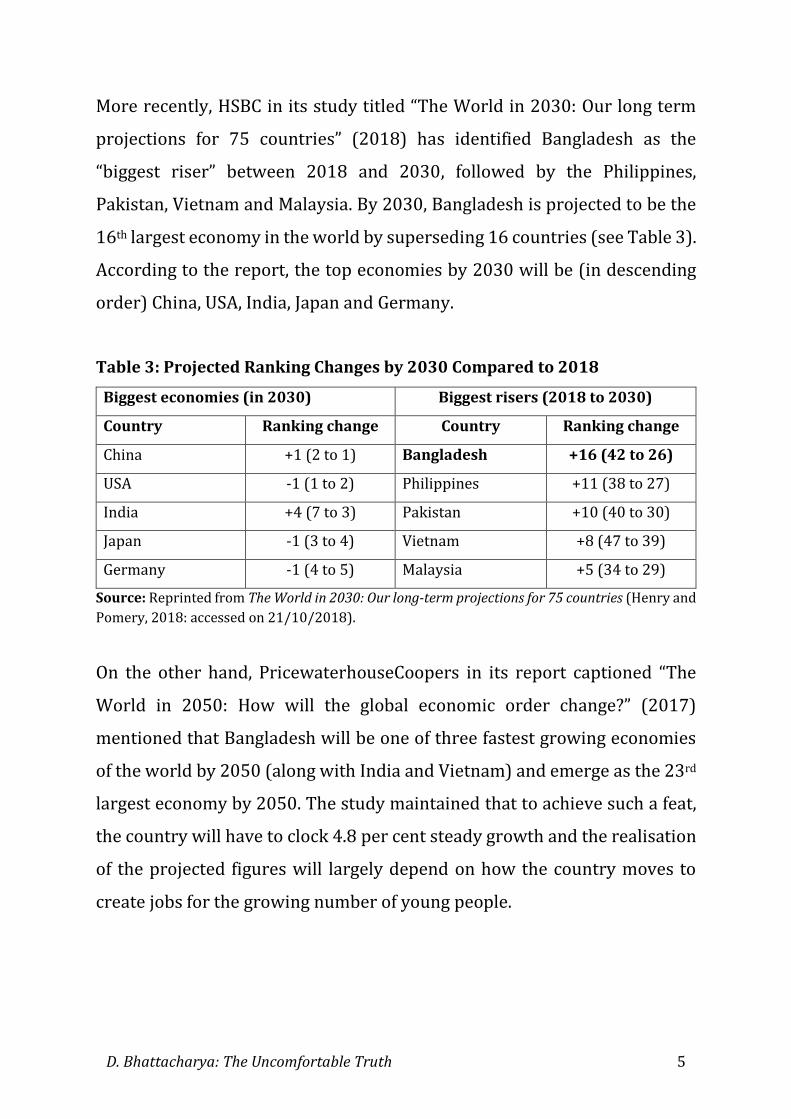

More recently, HSBC in its study titled “The World in 2030: Our long term

projections for 75 countries” (2018) has identified Bangladesh as the

“biggest riser” between 2018 and 2030, followed by the Philippines,

Pakistan, Vietnam and Malaysia. By 2030, Bangladesh is projected to be the

16th largest economy in the world by superseding 16 countries (see Table 3).

According to the report, the top economies by 2030 will be (in descending

order) China, USA, India, Japan and Germany.

Table 3: Projected Ranking Changes by 2030 Compared to 2018

Biggest economies (in 2030) Biggest risers (2018 to 2030)

Country Ranking change Country Ranking change

China +1 (2 to 1) Bangladesh +16 (42 to 26)

USA -1 (1 to 2) Philippines +11 (38 to 27)

India +4 (7 to 3) Pakistan +10 (40 to 30)

Japan -1 (3 to 4) Vietnam +8 (47 to 39)

Germany -1 (4 to 5) Malaysia +5 (34 to 29)

Source: Reprinted from The World in 2030: Our long-term projections for 75 countries (Henry and

Pomery, 2018: accessed on 21/10/2018).

On the other hand, PricewaterhouseCoopers in its report captioned “The

World in 2050: How will the global economic order change?” (2017)

mentioned that Bangladesh will be one of three fastest growing economies

of the world by 2050 (along with India and Vietnam) and emerge as the 23rd

largest economy by 2050. The study maintained that to achieve such a feat,

the country will have to clock 4.8 per cent steady growth and the realisation

of the projected figures will largely depend on how the country moves to

create jobs for the growing number of young people.

6 D. Bhattacharya: The Uncomfortable Truth

Growth Trends

The enthusiastic narratives regarding Bangladesh’s growth prospect,

emanating from global sources, are essentially based on statistics produced

by the national authorities, particularly by the Bangladesh Bureau of

Statistics (BBS). We can derive from the official data that during the last two

and a half decade (starting from 1990), Bangladesh has sequentially

enhanced its average growth rate of GDP and GNI every five years (see Table

4). Consequently, the observed trend got reflected in per capita GDP and per

capita GNI growth performance. As a result, per capita GDP and per capita

GNI experienced an almost five-fold increase between 1990 and 2017 (from

USD 298 to USD 1517 and from USD 310 to USD 1470 respectively).

Table 4: Average Growth Rates (1991–2017): GDP/GNI, GDP/GNI Per Capita

and GDP/GNI Growth Rates

1991-

95

1996-

00

2001-

05

2006-

10

2011-

15

2016-

17

GDP growth rate

(%)

4.53 4.83 5.09 6.07 6.32 7.20

GNI growth rate

(%)

4.71 4.84 5.34 6.79 6.00 6.14

Per capita GDP

growth rate (%)

1.55 5.12 3.67 9.44 9.89 11.94

Per capita GNI

growth rate (%)

1.27 4.97 4.85 8.06 8.84 11.15

GDP per capita

(USD)

294 394 436 618 988 1,438

GNI per capita

(USD)

320 394 464 656 1,016 1,400

Source: Based on World Development Indicators (World Bank, n.d.-a: accessed on 21/10/2018).

D. Bhattacharya: The Uncomfortable Truth 7

Double Transition

A direct upshot of this had been relocation of the country from low income

country to (low) middle income category where the cut off line (in 2014) was

a per capita GNI of USD 1045 (as per Atlas method) (see Figure 1).

Bangladesh crossed the lower middle income threshold in July 2015 based

on the GNI per capita of 2014.

The demonstrated growth performance also allowed Bangladesh (2018) to

recently fulfill the three eligibility criteria for graduation from the least

developed countries (LDC) group. The threshold figure for one of the three

criteria, had been per capita GNI of USD 1,230 (at the 2018 triennial review),

which Bangladesh crossed in 2016. If the Bangladesh economy does not

suffer any hiccups in the coming years, then the country will finally come out

of the LDC group in 2024.

Figure 1: Per Capita GDP and Per Capita GNI

Source: Based on World Development Indicators (World Bank, n.d.-a: accessed on 21/10/2018).

42

0

43

0

42

0

45

0

49

0

53

0

56

0

59

0

64

0

71

0

78

0 87

0

94

0

1,0

10

1,0

70

1,1

90

1,3

30

1,4

70

40

6

40

3

40

1

43

3

46

1

48

4

49

4

54

1

61

6

68

1

75

8

83

6

85

6 95

2

1,0

85

1,2

10

1,3

59

1,5

17

200

400

600

800

1,000

1,200

1,400

1,600

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Cu

rren

t U

SD

GNI per capita (Atlas method, USD) GDP per capita (USD)

LMIC threshold crossed

LDC threshold crossed

8 D. Bhattacharya: The Uncomfortable Truth

Sources of Growth

It would be interesting to explore what had been the sources of such

spectacular growth of the Bangladesh economy in the recent decades. It

transpires that over the period (1990–2018) incremental contribution of

agriculture has come down gradually with annual variations (see Table 5).

Table 5: Changing Configuration of Source of GDP Growth (in percentage

point)

Indicator FY90 FY95 FY00 FY05 FY10 FY15 FY16 FY17 FY18

Agriculture 0.64 0.78 1.79 0.49 1.07 0.53 0.43 0.44 0.59

Agriculture and

forestry

0.31 0.41 1.29 0.31 0.91 0.30 0.21 0.22 0.37

Industries 0.92 1.63 1.52 2.20 1.77 2.74 3.24 3.10 3.75

Manufacturing 0.78 0.93 0.71 1.27 1.08 1.93 2.26 2.21 2.80

Services 1.59 1.89 2.58 3.00 2.89 3.00 3.21 3.41 3.24

Wholesale and

retail trade

0.56 0.57 0.93 0.95 0.78 0.86 0.88 0.99 1.00

GDP growth

(%)

3.34 4.62 5.94 5.96 5.57 6.55 7.11 7.28 7.86

Source: Based on BBS (n.d. a), BBS (n.d. b) and Bangladesh Bank (2018).

In contrast, the role of industries and services have become more prominent

over time in terms of incremental contribution to GDP. Within these two

broad sectors, manufacturing and wholesale/retail trade have played an

increasingly stronger role in producing higher GDP growth.

Understandably, such changing configuration of sources of economic growth

had multifarious impacts on the Bangladesh economy, including in areas

such as employment and income generation, structural change and

competitiveness of the economy.

D. Bhattacharya: The Uncomfortable Truth 9

Structural Change

In view of the above, one would be tempted to ask whether the economy has

undergone any structural change during the last high growth period.

Between 1990–91 and 2017–18, the greatest increase in share of GDP was

expressed by manufacturing (from 12.2% to 21.9%) and largest decrease

was in the agriculture sector (from 28.7% to 13.7%) (see Table 6). Indeed,

Bangladesh is one of the rare developing countries that has avoided “pre-

mature deindustrialisation”—a phenomena currently afflicting many

African economies (Rodrik, 2015). Nonetheless, Bangladesh’s economy

continues to remain a service-sector dominated economy with the sector

accounting for more than half of the GDP. The single most important sub-

sector of the services continues to be wholesale and retail trade –

commanding more than a quarter of it.

Table 6: Changes in Sector-wise GDP Share (%)

Indicator FY90 FY95 FY00 FY05 FY10 FY15 FY16 FY17 FY18

Agriculture 28.71 25.01 24.61 21.36 17.54 15.35 14.73 14.14 13.66

Agriculture and

forestry

24.46 20.00 18.75 16.57 13.99 11.82 11.23 10.67 10.24

Industries 20.21 23.35 24.73 27.15 25.56 29.19 30.28 31.11 32.32

Manufacturing 12.18 14.56 14.82 15.83 16.42 19.34 20.17 20.86 21.93

Services 48.33 47.77 46.87 47.41 52.33 51.41 51.00 50.72 50.02

Wholesale and

retail trade

11.83 12.39 12.8 16.54 13.38 13.51 13.43 13.44 13.39

Total 100 100 100 100 100 100 100 100 100

Source: Based on BBS (n.d. a), BBS (n.d. b) and Bangladesh Bank (2018).

Yet, these inter-sectoral changes do not signify “structural transformation”

is happening in Bangladesh economy at a fast pace. As structural

10 D. Bhattacharya: The Uncomfortable Truth

transformation essentially entails relocation of labour and capital from

sectors with low productivity to high productivity, a recent study at CPD has

shown that during 1990–2015, the Bangladesh economy has experienced

“less growth in between sector productivity” (Moazzem and Arno, 2018).

Moreover, poor performance in export diversification, among others, is also

portrayed as a sign of lack of structural transformation.

Poverty Reduction

Robust economic growth did contribute to noticeable improvement in

poverty situation in Bangladesh during the recent decades. According to

successive HIES of the BBS, the share of population living under the upper

poverty line more than halved between 2000 (48.9%) and 2016 (24.3%)

(see Table 7). In terms of the lower poverty line, the corresponding figures

were more remarkable – the share of people living in extreme poverty

became almost one-third (34.3% in 2000 to 12.9% in 2016). It needs to be

mentioned that the decline in the share of poor under the upper poverty line

was more in the rural area in comparison to its urban counterpart, whereas

the opposite was true in case of lower poverty line. It appears that the share

Table 7: Poverty Rate (%) in Bangladesh by Residence

Year Upper Poverty Line Lower Poverty Line

National Rural Urban National Rural Urban

2000 48.9 52.3 35.2 34.3 37.9 20.0

2005 40.0 43.8 28.4 25.1 28.6 14.6

2010 31.5 35.2 21.3 17.6 21.1 7.7

2016 24.3 26.4 18.9 12.9 14.9 7.6

Source: Based on BBS, 2001a; BBS, 2006; BBS, 2011a and BBS, 2017a.

D. Bhattacharya: The Uncomfortable Truth 11

of poor are still higher in the rural areas (under both measures), but the

reduction of “hard core” rural poor had been faster (see Table 7).

However, it is now well evidenced that the rate of poverty reduction

experienced a slowdown in post-2005 period, notwithstanding the

acceleration of the GDP growth rate (see Table 8). During 2000–05 poverty

reduction rate was 1.8 per cent annually; in the subsequent two five-year

period (2005–10 and 2010–16), the corresponding figures were 1.7 per cent

and 1.2 per cent respectively. The observed slowdown in case of extreme

poverty reduction was even sharper. If during 2000–05, extreme poverty

reduction rate was 1.8 per cent per annum, the comparable figures for 2005–

10 and 2010–16 were 1.5 per cent and 0.8 per cent. In other words, the

growth elasticity of poverty has been falling since 2000. And such decline of

elasticity has been higher in case of extreme poverty. This decline cannot be

possibly explained by the reducing base of poverty incidence.

Table 8: GDP Growth and Poverty Reduction (in percentage point) Trends in

Bangladesh

Average annual 2000-05 2005-10 2010-16

GDP growth (%) 5.1 6.1 6.5

Poverty reduction (percentage point) 1.8 1.7 1.2

Extreme poverty reduction (percentage

point) 1.8 1.5 0.8

Source: Based on World Bank (n.d.-a), BBS (2001a), BBS (2006), BBS (2011) and BBS (2017a).

Note: Compounded annual growth rate (CAGR) was deployed to calculate average annual growth

of GDP.

Thus, within the country’s enviable economic growth performance, one can

notice that there are certain disquieting signals emanating from the

12 D. Bhattacharya: The Uncomfortable Truth

economy. I would like to reflect on these signals in the next part of the

lecture.

3. The Nature of Recent Economic Growth

While Bangladesh is being applauded by the global community for its

remarkable economic growth performance, the country has been lately

singled out for its inability to achieve inclusive growth. In its recently

published report on “The Commitment to Reducing Inequality Index 2018”,

Oxfam has put Bangladesh among the 10 worst performing countries as per

its CRI index. Bangladesh was ranked 148th among 157 countries based on

three criteria (i) spending in health, education and social protection, (ii)

progressivity of tax policy and (iii) labour rights and minimum wages.

No less alarming was the findings of the “World Ultra Wealth Report 2018”.

According to this report, Bangladesh was on the top 10 fastest growing Ultra

High Net Worth (UHNW) countries during the period 2012-2017. In other

words, individual with a net worth of US$ 30 million or more has grown

fastest in Bangladesh during the last five years in comparison to among other

countries in the world!

Regrettably, such a global reading of the nature of economic development in

Bangladesh is adequately corroborated by data and information obtained

from official sources of the country.

D. Bhattacharya: The Uncomfortable Truth 13

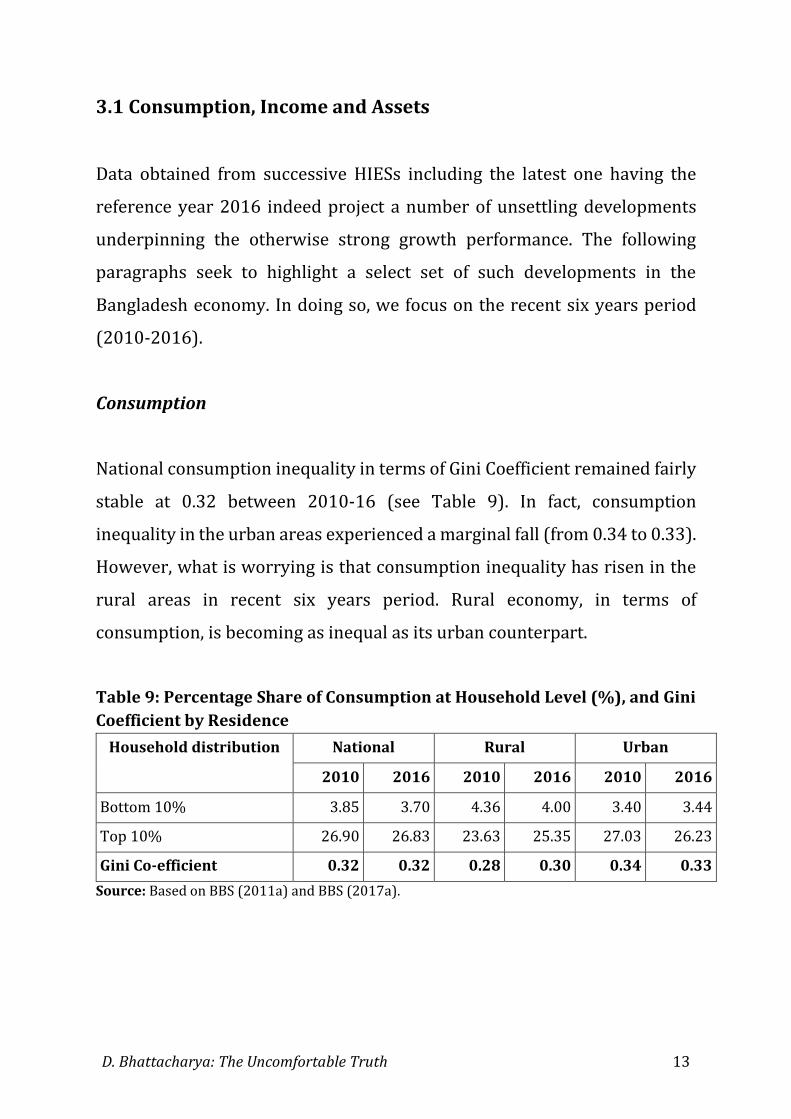

3.1 Consumption, Income and Assets

Data obtained from successive HIESs including the latest one having the

reference year 2016 indeed project a number of unsettling developments

underpinning the otherwise strong growth performance. The following

paragraphs seek to highlight a select set of such developments in the

Bangladesh economy. In doing so, we focus on the recent six years period

(2010-2016).

Consumption

National consumption inequality in terms of Gini Coefficient remained fairly

stable at 0.32 between 2010-16 (see Table 9). In fact, consumption

inequality in the urban areas experienced a marginal fall (from 0.34 to 0.33).

However, what is worrying is that consumption inequality has risen in the

rural areas in recent six years period. Rural economy, in terms of

consumption, is becoming as inequal as its urban counterpart.

Table 9: Percentage Share of Consumption at Household Level (%), and Gini

Coefficient by Residence

Household distribution National Rural Urban

2010 2016 2010 2016 2010 2016

Bottom 10% 3.85 3.70 4.36 4.00 3.40 3.44

Top 10% 26.90 26.83 23.63 25.35 27.03 26.23

Gini Co-efficient 0.32 0.32 0.28 0.30 0.34 0.33

Source: Based on BBS (2011a) and BBS (2017a).

14 D. Bhattacharya: The Uncomfortable Truth

Income

The HIES data show that income inequality in terms of Gini Coefficient has

increased along with increase in per capita national income (see Table 10).

Between 2010 and 2016, income inequality increased from 0.46 to 0.48. It is

to be noted that level of income inequality is higher than consumption

inequality in Bangladesh (0.48 and 0.32 respectively).

Table 10: Per Capita GNI and Income Gini Index

Year Per capita GNI (In current US $) Income Gini-Coefficient

2005 530 0.47

2010 780 0.46

2016 1,330 0.48

Source: Based on World Bank (n.d.-a), BBS (2006), BBS (2011a) and BBS (2017a).

A disaggregated look at the income distribution profile of households reveals

an alarming trend of income concentration (see Table 11). The acute

marginalisation of the bottom 5 per cent of households (in terms of income

level) between 2010 and 2016 is quite striking. This strata has lost out in

both urban and rural areas. The poorest 5 per cent population of Bangladesh

in 5 years (2010-16) lost out 2/3 of their share and now commands only a

minuscule 0.23 per cent of total income. Indeed, if one moves up the income

scale, we observe that not only the poorest section of the society, even the

lower middle class has experienced erosion of its income share. For example,

income share of bottom 40 per cent of the population went down as well

between 2010 and 2016 with the rural area experiencing such erosion more

than the urban area. On the other hand, the top 10 per cent, together with

the top 5 per cent households, enhanced their share of income between 2010

and 2016. And such increase in income concentration had been much higher

in the urban areas. The perceptible rise in income inequality in Bangladesh

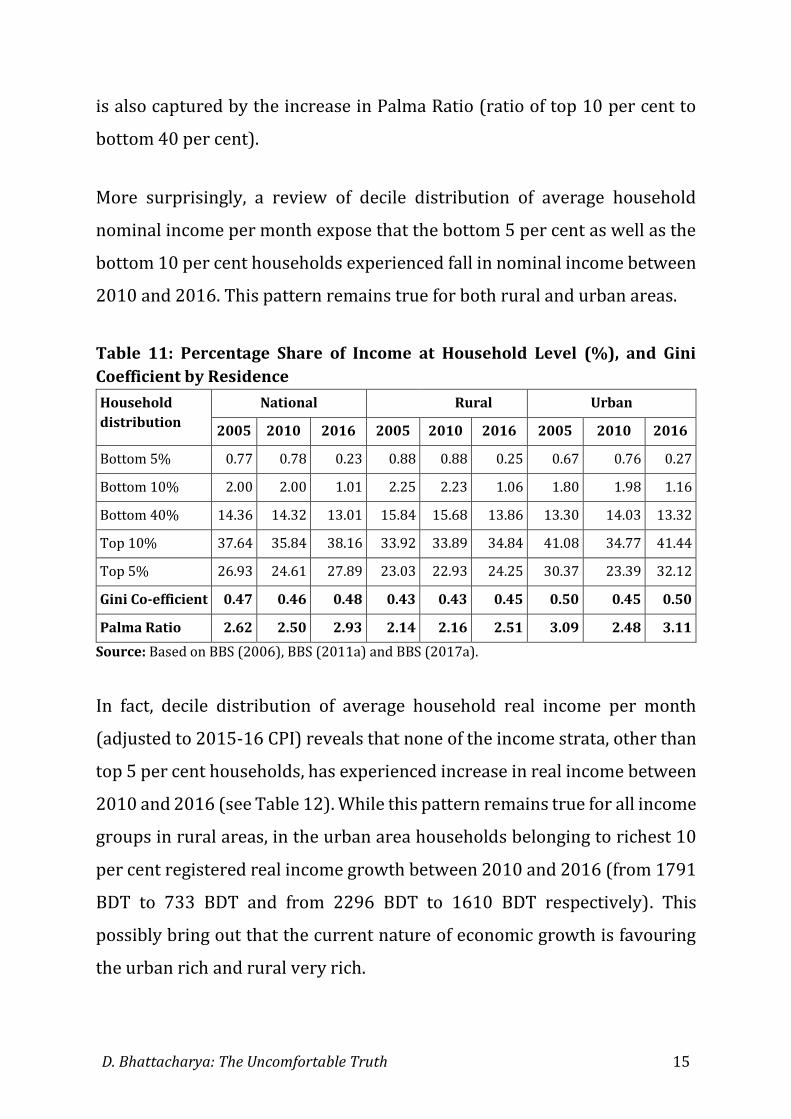

D. Bhattacharya: The Uncomfortable Truth 15

is also captured by the increase in Palma Ratio (ratio of top 10 per cent to

bottom 40 per cent).

More surprisingly, a review of decile distribution of average household

nominal income per month expose that the bottom 5 per cent as well as the

bottom 10 per cent households experienced fall in nominal income between

2010 and 2016. This pattern remains true for both rural and urban areas.

Table 11: Percentage Share of Income at Household Level (%), and Gini

Coefficient by Residence

Household

distribution

National Rural Urban

2005 2010 2016 2005 2010 2016 2005 2010 2016

Bottom 5% 0.77 0.78 0.23 0.88 0.88 0.25 0.67 0.76 0.27

Bottom 10% 2.00 2.00 1.01 2.25 2.23 1.06 1.80 1.98 1.16

Bottom 40% 14.36 14.32 13.01 15.84 15.68 13.86 13.30 14.03 13.32

Top 10% 37.64 35.84 38.16 33.92 33.89 34.84 41.08 34.77 41.44

Top 5% 26.93 24.61 27.89 23.03 22.93 24.25 30.37 23.39 32.12

Gini Co-efficient 0.47 0.46 0.48 0.43 0.43 0.45 0.50 0.45 0.50

Palma Ratio 2.62 2.50 2.93 2.14 2.16 2.51 3.09 2.48 3.11

Source: Based on BBS (2006), BBS (2011a) and BBS (2017a).

In fact, decile distribution of average household real income per month

(adjusted to 2015-16 CPI) reveals that none of the income strata, other than

top 5 per cent households, has experienced increase in real income between

2010 and 2016 (see Table 12). While this pattern remains true for all income

groups in rural areas, in the urban area households belonging to richest 10

per cent registered real income growth between 2010 and 2016 (from 1791

BDT to 733 BDT and from 2296 BDT to 1610 BDT respectively). This

possibly bring out that the current nature of economic growth is favouring

the urban rich and rural very rich.

Table 12: Average Household Real Income Per Month (adjusted to 2015-16 CPI)

HH Distribution National Rural Urban

2010 2016 % Change 2010 2016 % Change 2010 2016 % Change

Lower 5% 2,650 733 -72.3 2,466 668 -72.9 3,839 1,219 -68.3

Decile-1 3,397 1,610 -52.6 3,125 1,415 -54.7 5,000 2,618 -47.7

Decile-2 5,469 4,512 -17.5 4,946 4,006 -19.0 7,804 6,747 -13.5

Decile-3 6,964 6,442 -7.5 6,291 5,782 -8.1 9,975 9,432 -5.4

Decile-4 8,493 8,180 -3.7 7,608 7,304 -4.0 12,652 11,260 -11.0

Decile-5 10,209 9,934 -2.7 9,009 8,853 -1.7 15,935 13,336 -16.3

Decile-6 12,434 11,975 -3.7 10,719 10,616 -1.0 19,294 16,179 -16.1

Decile-7 15,389 14,542 -5.5 13,045 12,605 -3.4 23,486 18,842 -19.8

Decile-8 19,534 17,747 -9.1 16,113 15,730 -2.4 29,977 23,671 -21.0

Decile-9 27,076 23,662 -12.6 21,774 20,684 -5.0 40,609 30,034 -26.0

Decile-10 60,878 60,846 -0.1 47,485 46,522 -2.0 87,809 93,509 6.5

Top 5% 83,605 88,941 6.4 64,256 64,762 0.8 118,139 144,958 22.7

Source: Based on BBS (2011a) and BBS (2017a).

D. Bhattacharya: The Uncomfortable Truth 17

Assets

The HIES for 2016 is yet to release data on household level assets situation.

However, one can observe that asset concentration between 2005 and 2010

went up nationally with Gini Coefficient going up from 0.72 to 0.74 (see

Table 13). At a disaggregate level, the bottom 5 per cent households

demonstrates loss in asset share, whereas the top 5 per cent show noticeable

rise in the same. Between rural and urban areas, it appears, while the rural

poorest of the poor (bottom 10 per cent) more or less could hold on to their

low asset base, asset distribution in the urban areas became exceptionally

skewed. Taking note of the consumption and income inequality trends, one

can very well anticipate that the asset concentration has gone up further by

2016.

Table 13: Percentage Share of Wealth at Household Level (%), and Gini

Coefficient by Residence

Household

distribution

National Rural Urban

2005 2010 2005 2010 2005 2010

Bottom 5% 0.06 0.04 0.01 0.08 0.02 0.02

Bottom 10% 0.28 0.55 0.08 0.21 0.42 0.08

Top 10% 61.47 49.33 66.32 63.63 49.26 67.39

Top 5% 47.99 51.32 35.24 35.75 51.67 53.64

Gini Coefficient 0.72 0.74 0.63 0.62 0.78 0.79

Source: Based on unit level data from BBS (2006) and BBS (2011a).

The foregoing discussion suggests that Bangladesh economy – in terms of

consumption, income and assets – has become more unequal during the

recent decade, particularly between 2010-2016. Asset inequality increasing

at a faster pace than income inequality and income inequality increasing at

a faster pace than consumption inequality. These trends of growing

18 D. Bhattacharya: The Uncomfortable Truth

inequality have been largely driven by higher concentration of income in the

10 per cent of the population and greater concentration of assets in the top

5 per cent of the same. While the urban inequality is still higher than the

rural inequality, latter is gradually closing up with the former.

3.2 Employment Situation

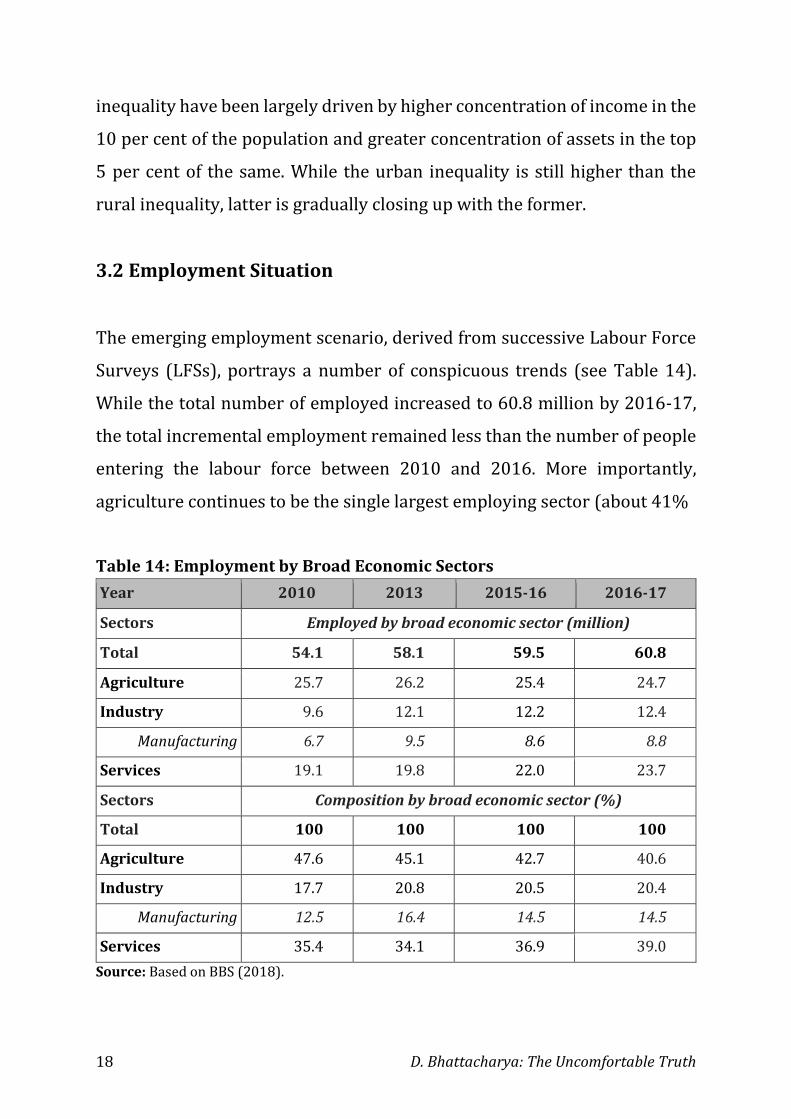

The emerging employment scenario, derived from successive Labour Force

Surveys (LFSs), portrays a number of conspicuous trends (see Table 14).

While the total number of employed increased to 60.8 million by 2016-17,

the total incremental employment remained less than the number of people

entering the labour force between 2010 and 2016. More importantly,

agriculture continues to be the single largest employing sector (about 41%

Table 14: Employment by Broad Economic Sectors

Year 2010 2013 2015-16 2016-17

Sectors Employed by broad economic sector (million)

Total 54.1 58.1 59.5 60.8

Agriculture 25.7 26.2 25.4 24.7

Industry 9.6 12.1 12.2 12.4

Manufacturing 6.7 9.5 8.6 8.8

Services 19.1 19.8 22.0 23.7

Sectors Composition by broad economic sector (%)

Total 100 100 100 100

Agriculture 47.6 45.1 42.7 40.6

Industry 17.7 20.8 20.5 20.4

Manufacturing 12.5 16.4 14.5 14.5

Services 35.4 34.1 36.9 39.0

Source: Based on BBS (2018).

D. Bhattacharya: The Uncomfortable Truth 19

of total employed population in 2016), notwithstanding its diminishing

share in GDP (less than 15% in 2016). Further, manufacturing sector

demonstrates a rather stagnating, if not declining employment situation. If

in 2013, manufacturing sector hosted 9.5 million jobs, in 2016-17 the

corresponding figure was 8.8 million. Manufacturing’s share in total

employment also experienced a decline from 16.4 per cent (2013) to 14.5

per cent (2016-17). This finding comes as a surprise in the backdrop of

increasing share of manufacturing in the GDP. In fact, one observes, that the

service sector is emerging as the foremost important sector for employment

generation – both in absolute and relative terms.

As one can suspect that a large part of these incremental jobs are located in

the informal sector where wages are low (often based on self-exploitation

driven self-employment) and working conditions are poor. The major

reason underwriting these patterns in the labour market relate to falling

employment elasticities in the manufacturing sector (-0.28 and -0.93

between 2013 to 2015-16 and 2015-16 to 2016-17 respectively), while

increase of the same in the service sector (0.58 and 1.20 between 2013 to

2015-16 and 2015-16 to 2016-17 respectively). Within the service sector,

majority of the additional jobs are created in the wholesale and retail trade

– pointing to informalisation of job market.

Youth Unemployment

The unemployment situation among the youth projects a perverse picture.

In 2016-17, about 10.6 per cent of the youth labour force (between 15 and

29 years) was unemployed. Indeed, the comparable figure in 2010 was 7.4

per cent. Not only upward trend in youth unemployment has been observed

20 D. Bhattacharya: The Uncomfortable Truth

between 2010 and 2016-17, such rate was significantly higher than the

national average unemployment figure.

More paradoxical is the fact that youth unemployment rate increases along

with the education level (see Table 15). In 2016-17 more than one-third of

the youth labour force with tertiary education (34.3%) remained

unemployed, whereas in 2010 the matching figure was less than 3 per cent!

In case of women, such rate was as high as 42.5 per cent. One wonders

whether this is a supply-side phenomenon (i.e. low quality of education

making the youth unemployable) or a demand-side phenomenon (i.e. where

the nature of economic growth creates less jobs for educated youth).

Table 15: Distribution of Youth Unemployment by Education Level (% of

total unemployed youth)

Year 2010 2013 2015-16 2016-17

No education – total 15.7 12.8 6.7 4.8

No education – male 13.4 5.1 6.1 2.3

No education – female 18.8 7.7 7.4 10.0

Primary – total 21.4 17.2 8.7 5.3

Primary – male 22.2 9.0 6.4 3.7

Primary – female 20.3 8.2 13.4 9.3

Secondary – total 49.0 34.7 10.7 8.7

Secondary – male 51.4 20.2 7.8 6.7

Secondary – female 47.4 14.5 17.6 11.7

Higher secondary – total 10.4 25.6 6.0 27.0

Higher secondary – male 10.3 12.4 6.1 22.7

Higher secondary – female 10.5 13.3 5.8 35.1

Tertiary – total 2.8 9.7 12.1 34.3

Tertiary – male 2.8 5.2 10.8 30.1

Tertiary – female 2.9 4.5 15.0 42.5

Total 7.4 8.1 8.7 10.6

Source: Based on BBS (2011b), BBS (2015), BBS (2017b) and BBS (2018).

D. Bhattacharya: The Uncomfortable Truth 21

Wages

The annual change (base 1969-70) in the general wage rate followed an

upward moving fluctuating trend (see Figure 2) till mid-2000. However,

since the introduction of the new base year (2010-11), the trend has

flattened out between 2011-12 and 2017-18. Between 2011-12 and 2014-

15, one observes decline of real wage rate index across sectors, while in the

last three years (2015-16, 2016-17 and 2017-18) one can notices a

stagnating trend.

Figure 2: Change in Real General Wage Rate Index (WRI) (%)

Source: Based on BBS (2017c).

Analysis of average real monthly income/wage (adjusted for 2016-17 CPI)

depicts that between 2013 to 2015-16, the largest drop was in the urban

areas (-6.8%), where women experienced much more loss of income (-

11.0%) than their male counterparts (-5.4%). However, between 2015-16

and 2017-18, negative change in real monthly income was more in the rural

areas. One may suggest that this has to do with declining profitability of the

crop sector.

0

2

4

6

8

10

12

14

16

18

20

Base: 1969-70 Base: 2010-11

22 D. Bhattacharya: The Uncomfortable Truth

3.3 Health Outcomes

Bangladesh is often appreciated for its success in attaining relatively high

human development outcomes, particularly in the areas of health and

education. However, a disaggregated look at the concerned indicators by

income or wealth status reveals the wide variations that remain concealed

within the national averages.

Among health related indicators, let us consider under-five mortality rate

and neo-natal mortality rate as well as prevalence of stunting and wasting

among children under five years. The tables presented in this section are

based on the latest sets of Bangladesh Demographic Health Survey (BDHS).

Under five mortality rate (deaths per 1000 live births) between 2011 and

2014 has declined nationally – from 53 to 46 (see Table 16). In fact, this

Table 16: Under- Five Mortality Rate and Neonatal Mortality Rate (deaths

per 1,000 live births) by Wealth Status

Indicator Value Year Wealth Status Mean

Absolute

deviation Lowest Second Middle Fourth Highest Total

Under

five

mortality

rate

Original

Value

2011 64 64 49 48 37 53 –

2014 53 63 47 37 30 46 –

Absolute

deviation

2011 11.0 11.0 4.0 5.0 16.0 – 9.4

2014 7.0 17.0 1.0 9.0 16.0 – 10.0

Neonatal

mortality

rate

Original

Value

2011 34 38 32 33 23 32 –

2014 35 35 34 23 14 28 –

Absolute

deviation

2011 2.0 6.0 0.0 1.0 9.0 – 3.6

2014 7.0 7.0 6.0 5.0 14.0 – 7.8

Source: Based on National Institute of Population Research and Training (NIPORT), Mitra and

Associates, and ICF International (2013) and National Institute of Population Research and

Training (NIPORT), Mitra and Associates, and ICF International (2016).

D. Bhattacharya: The Uncomfortable Truth 23

decline may be observed in all five wealth status group. However, the mean

absolute deviation of mortality rates by wealth status of household from

national averages have increased overtime (from 9.4 to 10.0). This implies

that households in Bangladesh, irrespective of their wealth status has

experienced improvement in child mortality rate, but the relatively well-off

families are improving at a faster rate – enhancing health-related inequality.

Similar trend may be observed in case of neonatal mortality (deaths per

1000 live births) (see Table 16). The national average declined during 2011-

14, from 32 to 28. However, there was a sharper rise (in comparison to under

five mortality rate) in mean absolute deviation of mortality rates by wealth

status of household from national average (from 3.6 to 7.8). In other words,

poorer families are losing relatively more new born children than the

wealthier families as the country moves forward.

One of the possible reasons of this differentiated health outcomes

concerning under five and neo-natal mortality rates by wealth status relates

to proportion of births attended by skilled health personnel. Here again, we

observe that the population of births attended by skilled health personnel

has increased nationally during 2011-14 (from 28.6% to 37.6%).

Nonetheless, population of births attended by skilled health personnel is

around five time higher among richest population (70.2%, 2014) than that

of among poorest population (14.9%, 2014). What is more disturbing is that

mean absolute deviation of the indicator from the national average has

increased over time.

In case of stunting among children under 5 years, between 2011 and 2014,

the national average did decline from 41.3 per cent to 36.1 per cent (see

24 D. Bhattacharya: The Uncomfortable Truth

Table 17). However, prevalence of stunting remains more 2.5 times higher

among the poorest 20 per cent of the population in comparison to the richest

20 per cent. More alarmingly the mean absolute deviation has increased

(from 7.6 to 8.2) between 2011 and 2014 disfavouring the poorer section of

the population.

Table 17: Prevalence of Stunting and Wasting among Children Under Five

Years of Age by Wealth Status

Indicator Value Year Wealth Status Mean

Absolute

deviation Lowest Second Middle Fourth Highest Total

Stunting Original

Value

2011 53.7 45.4 40.7 35.9 25.7 41.3 –

2014 49.2 42.2 35.9 31.0 19.4 36.1 –

Absolute

deviation

2011 12.4 4.1 0.6 5.4 15.6 – 7.6

2014 13.1 6.1 0.2 5.1 16.7 – 8.2

Wasting Original

Value

2011 17.5 16.2 17.7 13.6 12.1 15.6 –

2014 17.1 16.5 12.8 13.1 11.7 14.3 –

Absolute

deviation

2011 1.9 0.6 2.1 2.0 3.5 – 2.0

2014 2.8 2.2 1.5 1.2 2.6 – 2.1

Source: Based on National Institute of Population Research and Training (NIPORT), Mitra and

Associates, and ICF International (2013) and National Institute of Population Research and

Training (NIPORT), Mitra and Associates, and ICF International (2016).

Regarding wasting, we observe almost the same above mentioned trends,

although the differences among the richer and poorer sections are much less

in this instance (see Table 17).

3.4 Educational Attainment

Disparity in educational attainments becomes evident from early childhood

in Bangladesh. The Multiple Indicator Cluster Survey (MICS) 2012-13

D. Bhattacharya: The Uncomfortable Truth 25

reveals that percentage of children of age between 36-59 months attending

an organised childhood education varies across wealth status. For example,

if the concerned share is 11.7 per cent for the “poorest” strata, the

corresponding figure for the “richest” is 17.5 per cent.

Table 18: Enrolment of Children Aged 6-10 and Aged 11-15 Years by

Residence and Poverty Status, 2016

Year 2010 2016

Indicator Poverty

status

National Rural Urban National Rural Urban

Enrolment

of

children

aged 6-10

years

Original

Value

Poor 78.3 78.5 77.5 89.9 90.6 86.4

Non poor 89.0 87.9 91.7 94.3 94.7 92.9

National 84.8 83.8 87.9 93.5 93.9 92.2

Deviation

from

national

value

Poor 6.4 5.3 10.3 3.6 3.3 5.8

Non poor 4.3 4.1 3.8 0.8 0.8 0.7

Enrolment

of

children

aged 11-

15 years

Original

Value

Poor 70.2 72.3 60.8 74.8 76.4 66.7

Non poor 85.5 85.3 86.2 85.8 87.0 82.3

National 77.8 77.9 77.5 84.3 85.4 81.0

Deviation

from

national

value

Poor 7.6 5.7 16.7 9.5 9.4 14.3

Non poor 7.7 7.3 8.7 1.5 1.6 1.3

Source: Based on BBS (2011a) and BBS (2017b)

Similar differences may be also observed in case of enrolment of children

aged 6-10 years by residence and poverty status (see Table 18). School

enrolment of children (6-10 years) was higher among non-poor households

(94.3%, 2016) compared to the poor households (89.9, 2016). Incidentally,

divergence of enrolment rate (6-10 years) between poor and non-poor is

wider in the urban areas than in the rural. Thankfully, deviation of primary

26 D. Bhattacharya: The Uncomfortable Truth

school enrolment by poverty status from the national average slightly

decreased since 2010.

In case of enrollment of children aged 11-15 years, we observe that situation

of the urban poor households is the worst. In fact, mean deviation of this

indicator for children of the poor families nationally has increased between

2010 and 2016.

3.5 Regional Balance

Fruits of economic growth are not only being unevenly distributed among

different socio-economic groups, but also across different parts of

Bangladesh. Notwithstanding being a relatively small and compact country,

the issue of “East-West divide” of economic geography is being discussed

among the concerned quarters for sometime. Recent data (2016) from HIES

once again validates this claim of persisting regional imbalance in

development outcomes. For example, both general poverty rate and extreme

poverty rate are systematically lower in Dhaka, Sylhet and Chittagong (see

Table 19) in comparison to the same for Barisal, Khulna, Mymensingh,

Rajshahi and Rangpur. However, what is most disturbing is the fact, while all

over the country the poverty rates have declined between 2010 and 2016,

Rangpur experienced increase in both general poverty rate and extreme

poverty rates. The thought that comes to mind is: are we witnessing the re-

emergence of Monga?

D. Bhattacharya: The Uncomfortable Truth 27

Table 19: Poverty Rate (%) in Bangladesh by Division

Division Poverty Rate Extreme Poverty Rate

2010 2016 Rate of

Decline

2010 2016 Rate of

Decline

Barisal 39.4 26.5 12.9 26.7 14.5 12.2

Chittagong 26.2 18.4 7.8 13.1 8.7 4.4

Dhaka 30.5 16.0 14.5 15.6 7.2 8.4

Khulna 32.1 27.5 4.6 15.4 12.4 3

Mymensingh - 32.8 - - 17.6 -

Rajshahi 29.8 28.9 0.9 16.8 14.2 2.6

Rangpur 46.2 47.2 -1 27.7 30.5 -2.8

Sylhet 28.1 16.2 11.9 20.7 11.5 9.2

National 31.5 24.3 7.2 17.6 12.9 4.7

Source: Based on BBS (2011a) and BBS (2017a).

This apprehension is strengthened, among others, by comparative review of

administrative Division-wise figures on unemployment rate. Between 2010

and 2016, unemployment rate by Division declined, in Chittagong (5.9% to

3.5%), Dhaka (5.6% to 3.4%) and Sylhet (6.2% to 3.6); whereas it increased

in Barisal (4.6% to 5.4%), Khulna (3.5% to 4.1%) and Rajshahi (2.4% to

4.6%).

The Uncomfortable Truth

Thus, the “uncomfortable truth” of the recent development experience of our

country is very simple. The benefits of our recent economic growth had been

very unevenly distributed. This increasing disparity has accelerated in the

recent past according to the data for the period 2010-16. Manifestations of

this trend of disparity may be observed not only in case of consumption,

income and asset ownership, but also in the areas of employment, human

28 D. Bhattacharya: The Uncomfortable Truth

asset and regional development. In broad terms, it has favoured the richest

section of rural population and richer section of the urban population.

Indeed, the growing middle class of the country could not enhance its share

in the expanding economy.

Based on the foregoing analysis, it may be derived that youth

unemployment, informal sector jobs, wages for women, child mortality rates

of the poor households, school enrollment of the urban poor, and poverty-

stricken Rangpur region are some of the underbellies of our recent

development experience.

Indeed, CPD in its recent reports produced under the “Independent Review of

Bangladesh’s Development (IRBD)” programme has repeatedly highlighted

the dire picture of income inequality and wealth concentration. In its first

reading of the state of the economy for the fiscal year 2017-18, it has

mentioned that “while the importance of higher economic growth cannot be

undermined, the emphasis should be more on how to distribute the benefits

of growth across regions and marginalised communities” (CPD, 2018).

It is often said, a rising tide lifts all boats; but it can be also added that some

boats may not reach the harbor. Such a situation obviously begs the question

– why is this happening, while the stated public policy objective is “no one is

to be left behind”. In conclusion of the lecture, I would like to offer a couple

of observations in this regard – in my effort to consolidate the

understanding.

D. Bhattacharya: The Uncomfortable Truth 29

4. In Search of a Conclusion

In the recent past there has been a plethora of scholarly contributions

dealing with growth-inequality nexus. A significant part of it deals with

issues related to inequality among countries (Alvaredo, Chancel, Piketty et.

al., 2018; Schwab, 2018; WEF, 2017). There is an overwhelming agreement

that income convergence is taking place among countries in the midst of

rising Southern economies and persistent threat of secular stagnation in the

OECD countries (Milanovic, 2016; UNDESA, 2015).

There is also a general consensus that income inequality is increasing within

most of the countries including the developed ones. In this connection,

policymakers often fatalistically fall back on the much celebrated Kuznets

Curve; conveniently ignoring the recent exceptions, particularly in Latin

America. Some would, however, contend that this is “not a big deal”

(Vandemoortele, 2018).

In Latin America, since 2000, we have observed countries with both high

level (with Gini above 0.55) and low level (with Gini between 0.43 and 0.55)

of inequalities have experienced different levels of reduction. Figure 3

30 D. Bhattacharya: The Uncomfortable Truth

Figure 3: Latin American Countries: Initial Income Inequality and Reduction

Level (2000 to 2010)

Level of inequality

Level of reduction

Low Initial Inequality (Initial Income Gini coefficient between 0.43 and 0.55)

High Initial Inequality (Initial Income Gini coefficient between 0.55 and 1)

Lo

w

Re

du

ctio

n 1. Costa Rica

2. Panama 3. Argentina 4. Uruguay 5. the Dominican Republic

1. Guatemala 2. Colombia 3. Paraguay 4. Honduras

Hig

h

Re

du

ctio

n 1. Mexico

2. Venezuela 3. El Salvador 4. Peru

1. Brazil 2. Nicaragua 3. Bolivia 4. Ecuador 5. Chile

Source: Bogliacino and Rojas-Lozano (2017).

presents in four quadrants these countries. The countries with high initial

income inequality which have recorded high level of reduction include

Brazil, Nicaragua, Bolivia, Ecuador and Chile. Bangladesh being a country

with relatively low inequality (Gini being 0.48), may like to study

development experiences of countries in the third quadrant particularly that

of Peru and El Salvador.

There is also a venerable volume of literature focusing on the reasons

underpinning the recent rise of income inequality in a large number of

countries (Peters and Volwahsen, 2016; Dervis and Qureshi, 2016; WESS,

2012). These studies provide compelling evidence that growing inequality is

harmful for a country in many ways. This trend is harmful for economy,

environment, society and democracy (Wilkinson and Pickett, 2010; Stiglitz,

2012; Temple, 1999; Piketty, 2014; Dorling, 2017; Payne, 2017).

D. Bhattacharya: The Uncomfortable Truth 31

Without venturing into this evolving global discourse on the reasons behind

rising inequality within countries and their implications, let me highlight

three features of the Bangladesh scenario.

One of the critical reasons defining Bangladesh’s current nature of economic

growth relates to prevailing investment behavior of the private sector. As we

know, private sector investment as a share of GDP is stagnating around 23

per cent in the recent years. Does it mean that there is no investible

resources available? It is maintained that money siphoned out of the capital

market only during the bubble-burst of 2010-11 amounted to the tune of

USD 2,750 million (BDT 20,000 crores) (Byron and Rahman, 2011, based on

Report of the Khondaker Ibrahim Khaled Committee). Total amount of non-

performing loans reached a staggering number (as of June 2018) of USD

10,764 million (BDT 89,340 crores) which is about 4 per cent of GDP

(Bangladesh Bank, 2017; Uddin, 2018). Another 4 per cent of GDP (estimated

to be about USD 11,000 million in 2018) or more is illicitly flowing out of the

country annually. If all these resources got invested in the country in proper

ways, then we could have had a radically different gainful employment and

inequality situation.

The second issue concerns the nature of structural change we are witnessing

within Bangladesh economy. As has been mentioned earlier, the

manufacturing sector has been gradually increasing its share in the GDP. but

without corresponding rise is employment. However, the incremental share

of this manufacturing sector growth had taken place in its large and medium

scale component. While the large and medium scale industries enhanced its

share in GDP from 13.12 per cent in 2010 to 18.31 per cent in 2018, the

corresponding shares of the small scale industries were 3.30 per cent and

32 D. Bhattacharya: The Uncomfortable Truth

3.63 per cent. Inability to strengthen and expand the small scale industries

did have debilitating effects on the labour market situations.

On the other hand, the large and medium scale industries have increasingly

embraced improved technologies in their production processes so as to

enhance productivity and remain competitive in the (global) market. The

offshoot of this was decrease in employment elasticities of such investments,

implying less wage-based employment in the formal sector.

One is also tempted to raise a third aspect concerning the nature of

distribution of the benefits of recent economic growth of the country.

Evidence presented earlier suggest the aggravating skewed structure of

income distribution. The recent period is characterised by lack of political

competition in the country. A number of global reports have indicated

weakening of “voice” and oversight institutions in the country during this

period. World Bank’s Voice and Accountability Index for Bangladesh shows

a steep fall since 2010 (see Figure 4). One wonders whether enfeebling of

Figure 4: Voice and Accountability Index of Bangladesh (Estimate and

Ranking)

Source: Based on World Bank (n.d.-b)

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

0

10

20

30

40

50

60

Est

imat

e

Ran

k

Rank Estimate

D. Bhattacharya: The Uncomfortable Truth 33

the accountability mechanism has led to undermining economic governance

and, consequently, marginalisation of the disenfranchised stakeholders in

the distribution of benefits of development.

Today’s lecture was more a diagnostic one; it was not a prescriptive one

looking for new political settlements. However, if Dr Ghafur was around

today, he possibly would have said; “the first step in solving a problem is

recognising there is one”.

Thank you for your attention.

34 D. Bhattacharya: The Uncomfortable Truth

References

Alvaredo, F., Chancel, L., Piketty, T., Saez, E., and Zucman, G. (Eds.). (2018). World

Inequality Report 2018. Cambridge: Belknap Press of Harvard University

Press.

Bangladesh Bank (2017). Annual Report 2016-2017. Dhaka: Bangladesh Bank.

Retrieved from https://www.bb.org.bd/pub/annual/anreport/ar1617/

full_2016_2017.pdf

Bangladesh Bank. (2018). Monthly Economic Trends (Time Series data since 1972).

Dhaka: Bangladesh Bank. Retrieved from: https://www.bb.org.bd/pub/

monthly/econtrds/statisticaltable.xlsx

BBS. (2001a). Preliminary Report on Household Income and Expenditure Survey

2000. Dhaka: Bangladesh Bureau of Statistics (BBS).

BBS. (2001b). Labour Force Survey (LFS) 1999-2000. Dhaka: Bangladesh Bureau of

Statistics (BBS), Ministry of Planning, Government of Bangladesh.

BBS. (2006). Preliminary Report on Household Income and Expenditure Survey

2005. Dhaka: Bangladesh Bureau of Statistics (BBS).

BBS. (2007). Labour Force Survey (LFS) 2005-06. Dhaka: Bangladesh Bureau of

Statistics (BBS), Ministry of Planning, Government of Bangladesh.

BBS. (2011a). Preliminary Report on Household Income and Expenditure Survey

2010. Dhaka: Bangladesh Bureau of Statistics (BBS).

BBS. (2011b). Labour Force Survey (LFS) 2009-10. Dhaka: Bangladesh Bureau of

Statistics (BBS), Ministry of Planning, Government of Bangladesh.

BBS and UNICEF. (2014). Bangladesh-Multiple Indicator Cluster Survey 2012-2013.

Dhaka: Bangladesh Bureau of Statistics (BBS), Statistics and Informatics

Division, ministry of Planning, Government of the People’s Republic of

Bangladesh and United Nations International Children’s Emergency Fund

(UNICEF).

BBS. (2015). Labour Force Survey (LFS) Bangladesh 2013. Dhaka: Bangladesh

Bureau of Statistics (BBS), Ministry of Planning, Government of Bangladesh.

D. Bhattacharya: The Uncomfortable Truth 35

BBS. (2017a). Preliminary Report on Household Income and Expenditure Survey

2016. Dhaka: Bangladesh Bureau of Statistics (BBS).

BBS. (2017b). Quarterly Labour Force Survey (QLFS) 2015-16. Dhaka: Bangladesh

Bureau of Statistics (BBS), Ministry of Planning, Government of Bangladesh.

BBS. (2017c). Consumer Price Index (CPI), Inflation Rate and Wage Rate Index (WRI)

in Bangladesh. Dhaka: Bangladesh Bureau of Statistics (BBS), Ministry of

Planning, Government of Bangladesh.

BBS. (2018). Labour Force Survey (LFS) 2016-17. Dhaka: Bangladesh Bureau of

Statistics (BBS), Ministry of Planning, Government of Bangladesh.

BBS. (n.d.-a). Gross Domestic Product of Bangladesh at Constant Prices, 2014-

15 to 2017-18. Dhaka: Bangladesh Bureau of Statistics (BBS), Ministry of

Planning, Government of Bangladesh. Retrieved from: http://bbs.portal.

gov.bd/sites/default/files/files/bbs.portal.gov.bd/page/057b0f3b_a9e8_4

fde_b3a6_6daec3853586/F2_GDP_2017_18.pdf

BBS. (n.d.-b). Gross Domestic Product of Bangladesh at Constant Prices, 2010-

11 to 2014-15. Dhaka: Bangladesh Bureau of Statistics (BBS), Ministry of

Planning, Government of Bangladesh. Retrieved from:

http://203.112.218.65:8008/WebTestApplication/userfiles/Image/GDP/

GDP_2014-15_Final.pdf

Buiter, W., Rahbari, E. and Kupciuniene, D. (2011). The Global Growth Generators.

Global Economics View Global Growth Generators: Moving beyond ‘Emerging

Markets’ and ‘BRIC’, 21 February 2011, 62-73. New York: Citi Investment

Research and Analysis, Citigroup Global Markets Inc. Retrieved from:

https://www.eri.mn/download/smkncohc.

Byron, R. K. and Rahman, M. F. (2011, April 8). Tk 20,000cr swindled. The Daily

Star. Retrieved from https://www.thedailystar.net/news-detail-180918

CPD. (2018). Bangladesh Economy in FY2017-18. Interim Review of Macroeconomic

Performance. Dhaka: Centre for Policy Dialogue (CPD). Retrieved November

1, 2018, from https://cpd.org.bd/wp-content/uploads/2018/06/

Bangladesh-Economy-in-FY2017-18-Interim-Review-of-Macroeconomic-

Performance.pdf.

36 D. Bhattacharya: The Uncomfortable Truth

Dervis, K. and Qureshi, Z. (2016). Income Distribution within Countries: Rising

Inequality. Washington, D.C.: Global Economy and Development at

Brookings.

Dorling, D. (2017). The Equality Effect: Improving Life for Everyone. Oxford: New

Internationalist Publications Ltd.

Hawksworth, J., Clarry, R. and Audino, H. (2017). The World in 2050: The Long

View-How will the global economic order change by 2050? London:

PricewaterhouseCoopers (pwc).

Henry, J. and Pomery, J. (2018). The World in 2030: Our long term projection for 75

countries. London: HSBC Bank plc, Economics Global.

Kar, D. and Spanjers, J. (2015). Illicit Financial Flows from Developing Countries:

2003-2013. Washington, D.C: Global Financial Integrity. Retrieved from

https://www.gfintegrity.org/wp-content/uploads/2015/12/IFF-

Update_2015-Final-1.pdf

Lawson, M. and Martin, M. (2018). The Commitment to Reducing Inequality Index

2018: A global ranking of governments based on what they are doing to tackle

the gap between rich and poor. Cowley, Oxford: Development Finance

International and Oxfam Report.

Milanovic, B. (2016). Global Inequality. Cambridge: Harvard University Press.

Moazzem, K., and Arno, A. (2018). ‘Business as Usual’ Trend of Structural

Transformation: Can this Ensure Graduation with Momentum? (Policy Brief

No. 3). Dhaka: Centre for Policy Dialogue (CPD).

National Institute of Population Research and Training (NIPORT), Mitra and

Associates, and ICF International. (2013). Bangladesh Demographic and

Health Survey 2011. Dhaka, Bangladesh and Calverton, Maryland, USA:

NIPORT, Mitra and Associates, and ICF International.

National Institute of Population Research and Training (NIPORT), Mitra and

Associates, and ICF International. (2016). Bangladesh Demographic and

Health Survey 2014. Dhaka, Bangladesh, and Rockville, Maryland, USA:

NIPORT, Mitra and Associates, and ICF International.

O’Neill, J., Wilson, D., Purushothaman, R. and Stupnytska, A. (2005). How Solid are

the BRICs? (Global Economics Paper No: 134). New York: Goldman Sachs

Global Economics Group.

D. Bhattacharya: The Uncomfortable Truth 37

Payne, K. (2017). The Broken Ladder: How Inequality Affects the Way We Think,

Live, and Die. New York: Viking.

Peters, H. and Volwahsen, M. (2016). Rising Income Inequality: do not draw the

obvious conclusions. Germany: Deutsche Bank Research.

Piketty, T. (2014). Capital in the Twenty-First Century. Cambridge: Harvard

university Press.

Rodrik, D. (2015). Premature Deindustrialization. New Jersey: School of Social

Science, Institute for Advanced Study.

Schwab, K. (2018). The Global Competitiveness Report 2017-2018. Cologny: World

Economic Forum.

SDG Tracker: Bangladesh's Development Mirror. Dhaka: General Economics

Division, Planning Commission, Ministry of Planning, and a2i Programme,

Prime Minister’s Office, Government of Bangladesh. Retrieved from:

http://www.sdg.gov.bd/

Stiglitz, J. (2012). The Price of Inequality. London: Allen Lane.

Temple, J. (1999). The New Growth Evidence. Journal of Economic Literature 37

(1): 112–156.

Uddin, A. K. M. Z. (2018, September 11). Banks' toxic loans rise 20pc in six months.

The Daily Star. Retrieved from https://www.thedailystar.net/business/news/

bangladesh-bank-default-loans-rise-20pc-in-6-months-1632280

UNDESA. (2015). Income Convergence or Persistent Inequalities among Countries.

(Development Issues No. 5). United Nations Department of Economic and

Social Affairs (UNDESA)

Vandemoortele, J. (2018). From simple-minded MDGs to muddle-headed SDGs.

Development Studies Research. Retrieved from: https://

www.tandfonline.com/doi/full/10.1080/21665095.2018.1479647

WEF. (2017). The Global risks Report 2017. Geneva: World Economic Forum (WEF).

WESS. (2012). Inequality on the rise? An assessment of current available data on

income inequality, at global, international and national levels. (Background

document for the WESS 2013). New York: The World Economic and Social

Survey (WESS).

White, V., Imberg, M., Chesterfield, W. and Shaban, M. (2018). World Ultra Wealth

Report 2018. New York: WEALTH-X.

38 D. Bhattacharya: The Uncomfortable Truth

Wilkinson, R., and Pickett, K. (2010). The Spirit Level: Why Equality is Better for

Everyone. London: Penguin Books.

World Bank. (n.d.-a). World Development Indicators. Washington, D.C.: The World

Bank.

Accessed from: http://datatopics.worldbank.org/world-development-indicators/

World Bank. (n.d.-b). Worldwide Governance Indicators. Washington DC: World

Bank. Accessed from: http://info.worldbank.org/governance/wgi/#home

![BPL LIST-KOLKATA MUNICIPAL CORPORATION …ABDUL BORHAN ABDUL KADIR ABDUL MALEK ABDUL SOBAN ABDUL SOBHAN ABDUL AHAN KHAN ABDUL AJIJ ABDUL AJIJ] ABDUL GAFFAR MONDAL ABDUL HAMID KHAN](https://img.dokumen.tips/doc/110x75/5e6b7102b1682455b35c1d59/bpl-list-kolkata-municipal-corporation-abdul-borhan-abdul-kadir-abdul-malek-abdul.jpg)