Embed Size (px)

Citation preview

Options

1

Introduction to Corporate Finance

Prepared byYing PanTong Niu

Charlie GiurleoI.Murat Coskun

Options

2

Introduction

Basic concept - History - Current markets & Regulator - Characteristics & Terminology

Types of Options - Call options - Put options

Valuation - Payoff method - Binomial tree method

Strategies- Bullish strategy- Bearish strategy- Neutral strategy

Q&A & REWARDS!

Options

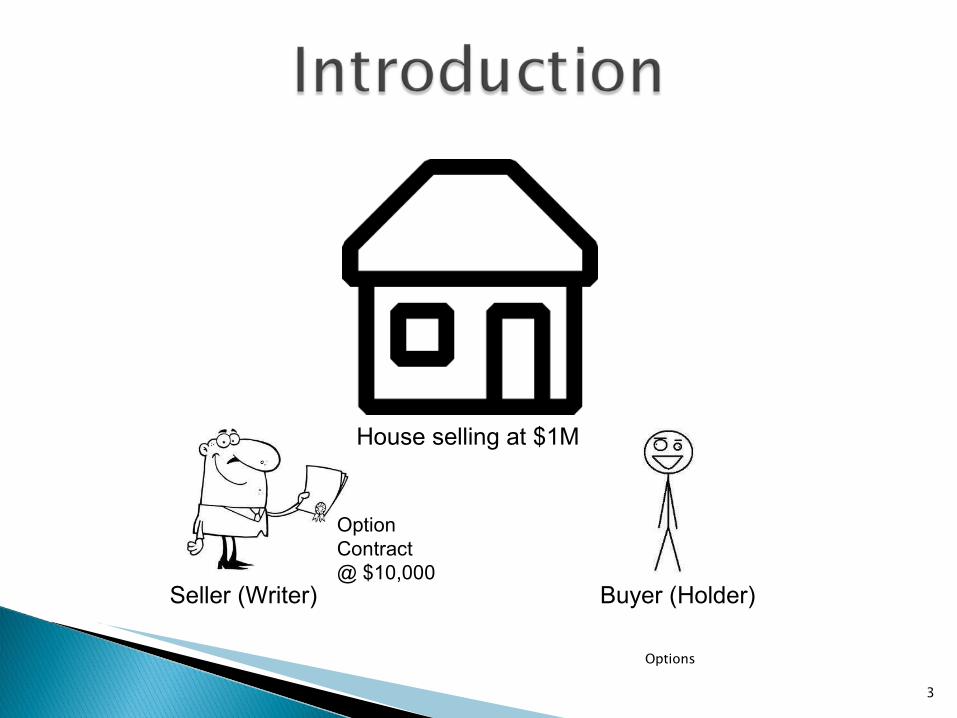

3

House selling at $1M

Option Contract@ $10,000

Seller (Writer) Buyer (Holder)

Options

4

House now selling at $2M ()

Seller (Writer) Buyer (Holder)

Scenario #1

Option Contract@ $10,000

$2,000,000$1,000,000 - $10,000 $990,000 (Profit)

Options

5

House now selling at $100K ()

Seller (Writer) Buyer (Holder)

Scenario #2

Option Contract@ $10,000

- $10,000 ($10,000) (Loss)

- Ancient Greek philosopher and mathematician – Thales of Miletus

- Purchased the Right to rent numerous olive presses before a predicted increase in olive harvest

- Fortunately, his prediction was right- Exercised his Right to rent out all presses!

HistoryHistory

Options

6

- Major markets over the world:

Current Markets & Current Markets & Regulator Regulator

•In Canada, options are traded on the Montreal Exchange and are cleared through the Canadian Derivatives Clearing Corp(CDCC)

•The CDCC stands between option buyers and option sellers (writers).

Options

7

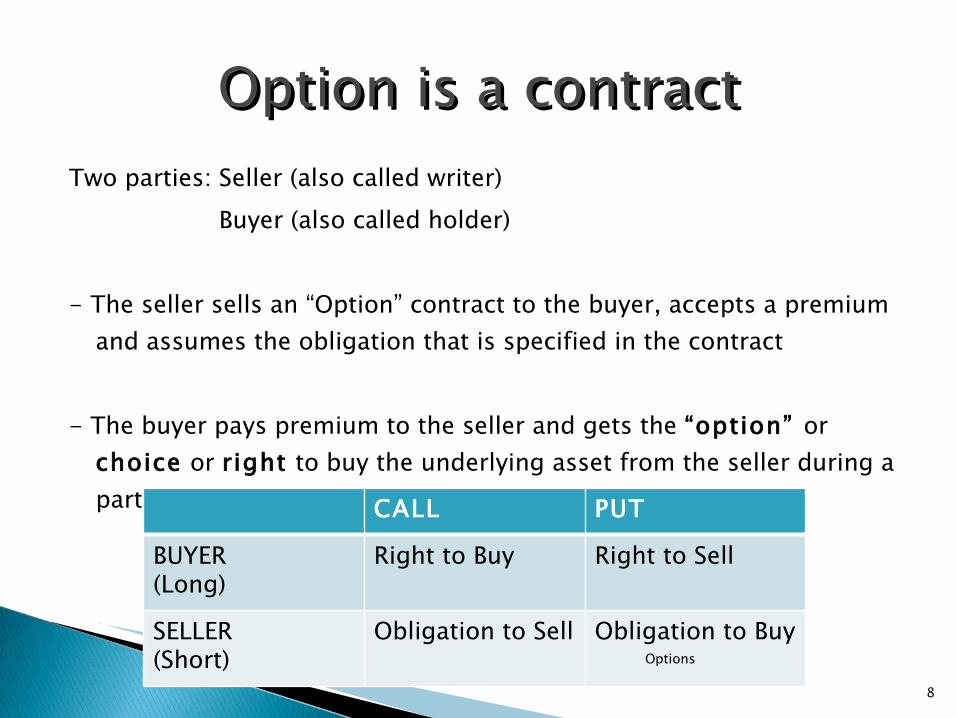

Two parties: Seller (also called writer) Buyer (also called holder)

- The seller sells an “Option” contract to the buyer, accepts a premium and assumes the obligation that is specified in the contract

- The buyer pays premium to the seller and gets the “option” or choice or right to buy the underlying asset from the seller during a particular period of time

Option is a contractOption is a contract

CALL PUT

BUYER(Long)

Right to Buy Right to Sell

SELLER(Short)

Obligation to Sell Obligation to BuyOptions

8

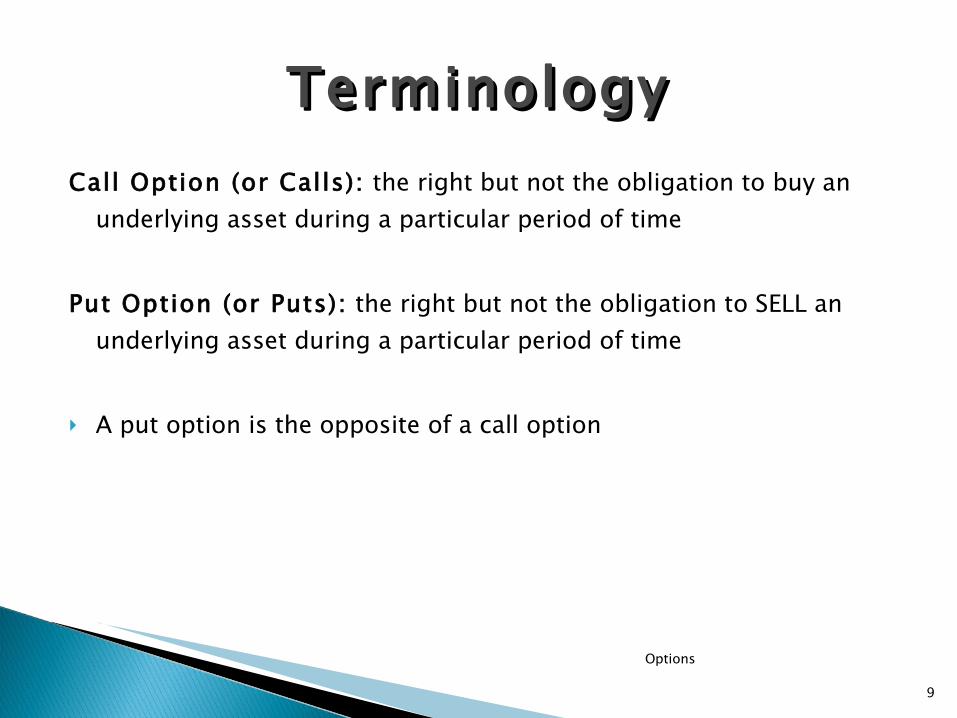

Call Option (or Calls): the right but not the obligation to buy an underlying asset during a particular period of time

Put Option (or Puts): the right but not the obligation to SELL an underlying asset during a particular period of time

A put option is the opposite of a call option

TerminologyTerminology

Options

9

Exercise the option: invoke the rights contracted

Exercising price (or striking price): the price at which the buyer can purchase or sell the underlying instrument

Expiration date: the date at which the rights to exercise the option cease to exist

Option premium: the price of an option

In-the-money, out-of-the-money: making a profit vs. not

TerminologyTerminology

Options

10

Trading Platform:- Listed: openly traded in exchange market- Over-the-counter: between two private parties

Exercise Types:- American: the right could be exercised any date before the

expiration date- European: the right could be exercised only on the day of

expiration date

Underlying assets :- Usual assets, common shares, commodities, rare metals,

interest rates, exchange rates, etc.

CharacteristicsCharacteristics

Options

11

Options

12

The buyer speculates the stock price will go up, then buy a call option by paying the option price (premium). If the stock price goes up during the expiration period, the buyer exercises the option and earns the profit. As illustrate in the table, the stock price goes up from $80 to $100, the call option buyer earns $11($20 minus $9 of option price ).

Buying a call from the Buying a call from the Buyer’s perspectiveBuyer’s perspective

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

80 100 July C 9 20 11

Options

13

Payoff from the buying a callPayoff from the buying a call

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

80 100 July C 9 20 11

Options

14

The seller will get the premium whenever he/she sells a call option. If the stock price does not go up by the expiration, the call buyer will not exercise the option and the seller can get the premium as a net profit.

If the stock price goes up and the buyer exercises the option, then the seller have to assume the obligation to sell the stock with the exercise price and bear a loss which equal is to the buyer’s net profit. In the example above, $11 is seller’s net loss and buyer’s net profit

Selling a call from theSelling a call from theSeller’s perspectiveSeller’s perspective

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

80 100 July C 9 20 11

Options

15

Payoff from writing a call.

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

80 100 July C 9 20 11

Options

16

The buyer speculates the stock price will go down, then buy a put option by paying the option price (premium). If the stock price goes down by the expiration, the buyer exercises the option and earns the profit. As illustrate in the table, the stock price goes down from $85 to $75, the call option buyer earns $10 minus $5 of option price and get $5 net profit.

Buying a put from the Buying a put from the buyer’s perspectivebuyer’s perspective

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

85 75 Aug P 5 10 5

Options

17

Payoff from buying a put.

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

85 75 Aug P 5 10 5

Options

18

The seller will get the premium whenever he/she sells a put option. If the stock price does not go down by the expiration, the put buyer will not exercise the option and the seller can get the premium as a net profit.

If the stock price goes down and the buyer exercises the option, then the seller have to assume the obligation to sell the stock with the exercise price and bear a loss which equal to the buyer’s net profit. In the example above, $5 is seller’s net loss and buyer’s net profit

Selling a put from the Selling a put from the seller’s perspectiveseller’s perspective

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

85 75 Aug P 5 10 5

Options

19

Payoff from writing a put.

Striking Price

Stock

Price

Expiration

Date

P/C Option Price

Option Value

Net Profit

85 75 Aug P 5 10 5

Options

20

Call option value= Stock value - PV of the exercise price

5 key variables:1) Current stock price (S0)

2) Exercise price of the option (E)

3) Time of expiration (t)

4) Risk free rate (Rf)

5) Variance of return on stock

C0=S0 -E/(1+Rf)t

Options

21

You would like to purchase a 1 year call option for RBC stock- the exercise price= $45 per share and the stock price is currently at $70 and the risk free rate=2% and you speculate that the stock will be between $60 and $80 in 1 year.

What is the cost of the option?

Options

22

.

t=0t=1

E= $45

S0 =70E=45Rf=2% Both speculated stock prices & t=1 are in the money, therefore:

discount E 1 yr

C0=S0 -E/(1+Rf)t = 70- (45/1.02)1= 25.88

Therefore call option = $25.88

S0 =70

Options

23

You would like to purchase a 1 year call option for RBC stock- the exercise price= $45 per share and the stock price is currently at $70

The risk free rate=2% and you speculate that the stock will be between $40 and $80 in 1 year.

What is the cost of the option?

Options

24

Call option calculation S0 =70, E=45, Rf=2% & t=1 therefore:

The option can finish out of the $ and be worth 0 at expiration or in the $ and be worth $35

When the stock finishes at $80, our risk-free asset pays $40, leaving us $40 short. Each option is worth $35 in this case, so we need $40/$35 = 1.14options to match the payoff on the stock.

Options

25

We must now invest $40 in a risk free asset and in 1.14call options

€

S0=1.14×C0+40

(1+Rf)

€

70=1.14×C0+40

(1.02)

€

C0 =$27.00

Options

26

For this case assume a 50% probability for both outcomes

Call option calculationS0 =70, E=45, Rf=2% & t=1 therefore:

Options

27

€

C0 =$17.501.02

=$17.16

Therefore value of call option is $17.16

Options

28

- Develops tailored to investor characteristics

- Multiple variables that matter in the strategy:- Investment Goals- Anticipation on the underlying asset movement- Risk Level

- Widely used for hedging (as an insurance tool)

- Numerous established strategies out there

Options

29

Options

30

Types:

- Bullish Strategies

- Bearish Strategies

- Neutral Strategies

Options

31

- Trader expects underlying asset price to go up - Assess: how high & time frame

- Most bullish strategy - Example: Simple Call Buying Strategy

- Moderate: target price for the bull run & utilize bull spreads to reduce cost

- Maximum profit is capped- Example: Bull Call Spread & Bull Put Spread

- Mildly bullish strategies: make money as long as the underlying stock price does not go down by the expiration date

- Example: Writing Out-of-the-Money Covered Calls

Options

32

- Trader expects underlying asset price to go down - Assess: how low & time frame

- Most bearish strategy - Example: Simple Put Buying Strategy

- Moderate: target price for the expected decline & utilize bear spreads to reduce cost

- Maximum profit is capped- Example: Bear Call Spread & Bear Put Spread

- Mildly bullish strategies: make money as long as the underlying stock price does not go up by the expiration date

Options

33

- Trader does not know what movement to expect for the underlying asset price

- Also called non-directional strategies: profit does not depend on underlying asset price going up or down

- Correct neutral strategy to employ depends on the expected volatility of the underlying stock price

- Examples:- Straddle: position in a call & a put at the same strike & expiration - Strangle: simultaneous buying or selling of out-of-the-money put & call with same expirations yet different strike prices - Butterfly: buy in-the-money and out-of-the-money call & sell two at the money calls or vice versa - Guts: sell in the money put and call

Options

34

Q & Q & AA

Options

35

a) the obligation to BUY an underlying asset during a particular period of time

b) the right to BUY an underlying asset during a particular period of time

c) the right to SELL an underlying asset during a particular period of time

d) the obligation to SELL an underlying asset during a particular period of time

A call option is:A call option is:

Options

36

a) 2 only b) 3 only c) both 1&4 d) both 2&3

What should a trader who believes that a stock's price will decrease do?

1) buy a call 2) buy a put 3) write a call 4) write a put

Options

37

a) American option b) European option c) Bermuda option d) all of these above

Which of the following option(s) could ONLY be exercised on the date of expiration?

Options

38

a) the market to go up in movement b) the long call to overlap the short call c) the underlying asset to go up in movement d) the prices of bovine animals to go up in

the near future

Which of the following best completes the below statement?

An option trader exercises a bullish strategy when he/she expects…

Options

39

References:TradeKing.com Covered Call Options Strategy. <http://www.youtube.com/watch?v=UT6Y4OZ_Ejc>OptionsPhysics.com Straddles and Strangles. <http://www.youtube.com/watch?v=HPHs7UsjBmY&NR=1>The Options Guide Options & Futures Trading Explained <http://www.theoptionsguide.com/>About.com <http://daytrading.about.com/b/2007/11/18/options-trading-basic-options-strategies.htm>OptionsTradingGuide.com <http://www.option-trading-guide.com/spreads.html>The Options Industry Council Strategies <http://www.optionseducation.org/strategy/default.jsp>Barrie, Scott (2001). The Complete Idiot's Guide to Options and Futures. Alpha Books. pp. 120–121.InvestorWords.com Index Options. < http://www.investorwords.com/2431/index_option.html >OIC< http://www.optionseducation.org/basics/leaps/default.jsp >Index Options. InvestorWords.com, March 18, 2011 Option (finance), Wikipedia, modified on 15 March 2011 at 23:34, < http://en.wikipedia.org/wiki/Option_(finance) > Options Basics: Types of options. Investopedia.com, March 18, 2011 < http://www.investopedia.com/university/options/option3.asp > Black, F. and Myron, S. The Pricing and Corporate Liabilities. Journal of Political Economy, 81, 637-659Cox, J. C., Ross, S.A. and Rubinstein, M. (1979). Option Pricing: A Simplified Approach. Journal of Financial Economics, 7, 229-263Dixit, A. K. and Pindyck, R.S.(1995). The Options Approach to Capital Investment. Harvard Business Review, 73, 105---115.Dale Jackson, BNN Producer 3:32 pm, E.T. February 17,2011 Canadian <http://www.bnn.ca/Blogs/2011/02/17/It-may-be-time-for-alternative-thinking.aspx> Call Options Trading for Beginners - Put and Call Options Explained <http://www.youtube.com/watch?v=q_z1Zx_BALo>Ross S.A., Westerfield R.W., Jordan B.D., Roberts G.S., (2010) Fundamentals of Corporate Finance, Seventh Canadian Edition. Canada: McGraw-Hill RyersonKaplan Schweser Faculty (2010). Chartered Financial Analyst Level 2, Book 5, Derivatives and portfolio management. La Crosse, WI, United States: Kaplan Berk J.,DeMarzo P.M.,Stangeland D.,(2010) Corporate Finance, Canadian Edition, Canada: Pearson Education Canada

Options

40

Backup SlidesBackup Slides

Options

41

Covered Call StrategyThree main steps:

(1) Purchase the Stock(2) Sell a Single Call Contract(3) Wait for Call to be Exercised or

Expired to Realize Profit

Risk: no protection if stock price goes down

Loss = Purchase Price of Stock – Price of Stock – Premium Received

Maximum Profit = Limited

Profit = Strike Price – Purchase Price of Stock + Premium Received

Options

42

Straddle StrategyMain steps:

(1) Buy both a call & a put at the same strike price with same expiration

(2) As the trade begins to move in one direction, trader sell the other

When: trader does not have a clear sense of which direction stock price will move

Goal: underlying stock moves far enough & winning leg of the position makes more money than the losing leg costs.

Options

43

Strangle StrategyMain steps:

(1) Buy both a call & a put at the same with same expiration, but different strike prices

(2) As the trade begins to move in one direction, trader sell the other

When: trader does not have a clear sense of which direction stock price will move, but believes the stock is highly volatile

Goal: underlying stock moves far enough & winning leg of the position makes more money than the losing leg costs.Limited Risk: cost of both options may be lost

Options

44

Call SpreadFour main steps:

(1) Purchase a single at money call contract(2) Sell a single in money call contract(3) Wait for the price to move above the

long call strike price plus the long call premium

(4) Exercise the long call to realize profit

Low Risk: limited to initial debit taken at entering the trade regardless of how far price moves down Maximum Risk = Initial Debit

Loss = Long Call Premium – Short Call Premium Maximum Profit = Short Call Strike Price – Long Call Strike Price – Initial Debit

Profit = Stock Price Upon Expiration – Long Call Strike Price – Initial Debit

Options

45

Put SpreadFour main steps:

(1) Purchase a single at money put contract(2) Sell a single in money put contract(3) Wait for the price to move above the short put

strike price(4) Let both puts expire worthless

Maximum Risk: Difference between long and short put strike prices – Initial Credit

Loss = Short Put Strike Price – Long Put Strike Price- Initial Credit

Maximum Profit = Initial Credit

Profit = Short Put Premium – Long Put Premium

Options

46

Payoff from buying a call.

Long callLong call

Options

47

A trader who believes that a stock's price will increase might buy the right to purchase the stock (a call option) rather than just purchase the stock itself. He would have no obligation to buy the stock, only the right to do so until the expiration date. If the stock price at expiration is above the exercise price by more than the premium (price) paid, he will profit. If the stock price at expiration is lower than the exercise price, he will let the call contract expire worthless, and only lose the amount of the premium. A trader might buy the option instead of shares, because for the same amount of money, he can control (leverage) a much larger number of shares

Options

48

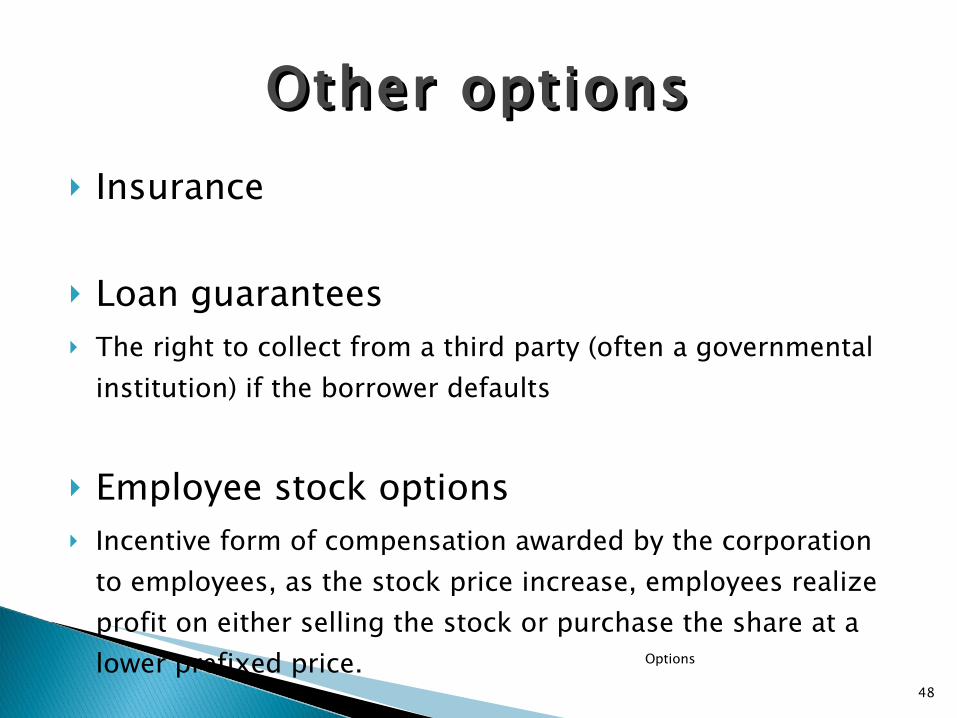

Insurance

Loan guarantees The right to collect from a third party (often a governmental

institution) if the borrower defaults

Employee stock options Incentive form of compensation awarded by the corporation

to employees, as the stock price increase, employees realize profit on either selling the stock or purchase the share at a lower prefixed price.

Other optionsOther options

Options

49

Other optionsOther options Real options An option with payoffs in real goods

Index options (stocks market index options) With an index as underlying security, the settlement is made

by cash payment if the option is exersiced.

LEAPS® (Long-Term Equity AnticiPation Securities® )

Options for investors who prepare to carry the position in long term of period.

Options

50

The call provision on the bond Held by the corporation, gives the corporation the right to

call back the bond at a fixed price for a fixed time period

Put bonds Gives the holder of the bond the right to force the issuer to

repurchase the bond at a fixed price for a fixed period of time

The overallotment options Gives the underwriters of an IPO the right to purchase

additional shares of stock of the firm

Other optionsOther options

- London engaged in Puts and Refusals (Calls) in 1690: - investors have the right to convert the bond into a common stock- issuers of the bond have the right to buy back the bond at a

specified price

- In 19th century of North America, Privileges were sold, which combine a call and a put on a selected share, expired usually within 3 months

Extra HistoryExtra History

Options

51

Options

52

http://www.slideshare.net/muratcoskun/options-presentation-introduction-to-corporate-finance