Embed Size (px)

Citation preview

Opportunities for Gender Inclusion via Fintech

Enrico Pini European Investment Bank

MAKING DIGITAL FINANCE

WORK FOR WOMEN

Elisabeth Ballreich

Principal Investment Officer

Women’s World Banking Asset Management

Between 2011 and 2017, 1.2 billion adults have obtained an account, including 600 million women

Today, 69% of adults

around the world have an account

Adults with an account (%), 2017 Source: Global World Bank Findex

Account ownership for women increased from 58% to 65%

But the 9% gender gap in developing economies remains unchanged

Adults with a mobile phone (%), 2017 Source: Callup World Poll 20917

3.4 billion women have

a mobile phone, incl.

61% of unbanked

women

Digital inclusion offers a potential solution for improving women’s financial inclusion

However, women face unique barriers to financial inclusion

Women tend to…

• be less literate

• have less time available

• be less mobile and spend

more time close to homes

Women face even more barriers to financial inclusion

Women typically…

• are less likely to have IDs

• lack trust and confidence

when it comes to formal

financial services

• work in the informal

sector and therefore have

irregular sources of income

Digital financial services can even exacerbate the gender gap

Research shows that women…

• are 14% less likely to own a

mobile phone than men

• exhibit steeper adoption

curves when it comes to

technology

• use phones less frequently

and intensively than men

Digital financial services need to be designed with women in mind to address

these barriers

How we design digital financial services to serve women

• Minimize barriers to account

opening with low or tiered KYC

policies

• Take the service to her

through instant account opening

in the field or door step banking

How we design digital financial services to serve women

• Bridge the emotional distance

by designing products with

relevant use cases and with

visuals and language that

speaks to her

• Build trust and a positive user

experience by training agents

on how to adequately serve

women customers

Ronald Everts - Opportunities for gender inclusion via Fintech - Sidi

Yasser El Jasouli

SCALING FOR IMPACT Since 2006, with a powerful social mission!

7 partners, 13 associates and consultants if required.

Core business financial inclusion, Digital Financial Services, ever more Mobile Information Services.

Automated credit scoring projects: Jordan, Uganda, Senegal

https://www.phbdevelopment.com/

PHB development

Where we work

PHB - Clients

1

7

Organisations Projects Time

Build Credit Risk scoring system using mobile money data and

financial data

Project funded by UNCDF

Credit scoring system for an emergency loans for

women

2019

2019

2019

Advisory on Credit Risk scoring

Project funded by UNCDF

Build a credit risk solution WISE Burundi MFI

Build Equity’s data warehouse and channel

performance KPI’s

– to monitor client acquisition and channel usage

Project funded by the Gates Foundation

Organisations Projects

2018

Time

2014-2017

Build a credit scoring solution for the Mobile lender

Ahli Microfinance Company

`Project funded by USAID

2018

Build consolidated credit risk and Business

Intelligence reporting at BNP group Level. 2018

Support the digitalization of

financial institutions

1. Digital

Transformation

Audit

2. Creation of

efficient data

collection systems

& consolidated

databases

4. Provide mobile

applications

(deposits, savings,

payments, loan

allocation)

3. Digitalization

and

automatization of

the credit scoring

process

5. Provide

analytical tools:

Loan portfolio

monitoring

Digital Action Group

We are member of: Current implementations of digital money

lending systems and m-payments/m-

deposits solutions:

Use case Jordan

Financed & facilitated by LENS & USAID.

AMC wants to introduce tablets for the Loan Officers with in the field credit scoring, digitize Loan Disbursements - Repayments (via the use of Mobile money.)

Management realizes that the organization faces fundamental challenges.

Business objectives: improve customer service.

Azesa is a proud

woman who took

up tailoring to

support herself

and her siblings

(11).

Rashad has been

managing his shop in

Bayader for over

20 years. 7 children

.

Application scoring : Information: CRB Information application

process Demographic Saving information Loan historical information Segmentation is used to

identify the group to which the customer belongs

New customers New customers with credit information

Use case Jordan, application scoring

Loan status

Description

Approved

The customer has a good credit rating

Need a visit

The field officer must visit the client and gather more

information

Loan refusal

The customer has a very poor credit rating

Call required

The field officer should call the client and survey them

further to gather more information on credit assessments

Business Requirements & understanding the data

Our credit-scoring approaches typically assess three characteristics:

–Identity: to reduce fraud

– Ability to repay: usually based on income and current debt load

– Willingness to repay: usually based on past credit

performance Hand & Henley (1997). “Statistical classification methods in consumer credit scoring: a review” Baer et al. (2013) “New credit-risk models for the unbanked”. Mckinsey.

Risk Criteria

# CreditScoringparameters

1 AgeoftheClient

2 MaritalStatus

3 NatureofBusiness/Employed

4 Gender

5 Product

6 Loanterm

7 CurrentLoanClassfication

8 encours

9 periodicite

10 AgewithBank

11 Loaneverbeeninbadclassification

12 NumberofLoansBorowed

13 sectoractivity

14 AverageacountCreditTurnover

15 AverageacountDebitTurnover

SocioDe

mograhic

Prod

uct

Loanhistory

Savinginfo

Exploratory analysis of

credit data

Gender impact in credit Scoring: Data

0

50

100

150

200

250

300

350

Count of Product

Type Rows Variable

Client identity 23.000 71

Savings 52.000 11

Loans 20.000 32

Urban Females aged 42 to 60 years are least at risk of default (< 3.5%)

Segment Default

Rate

All 4.13%

Male 4.56%

Female 3.57%

Urban Female 3,25%

Urban Male 3,63%

Rural Female 3.84%

Rural Male 5,26%

Identity : Default versus Gender-location- Age

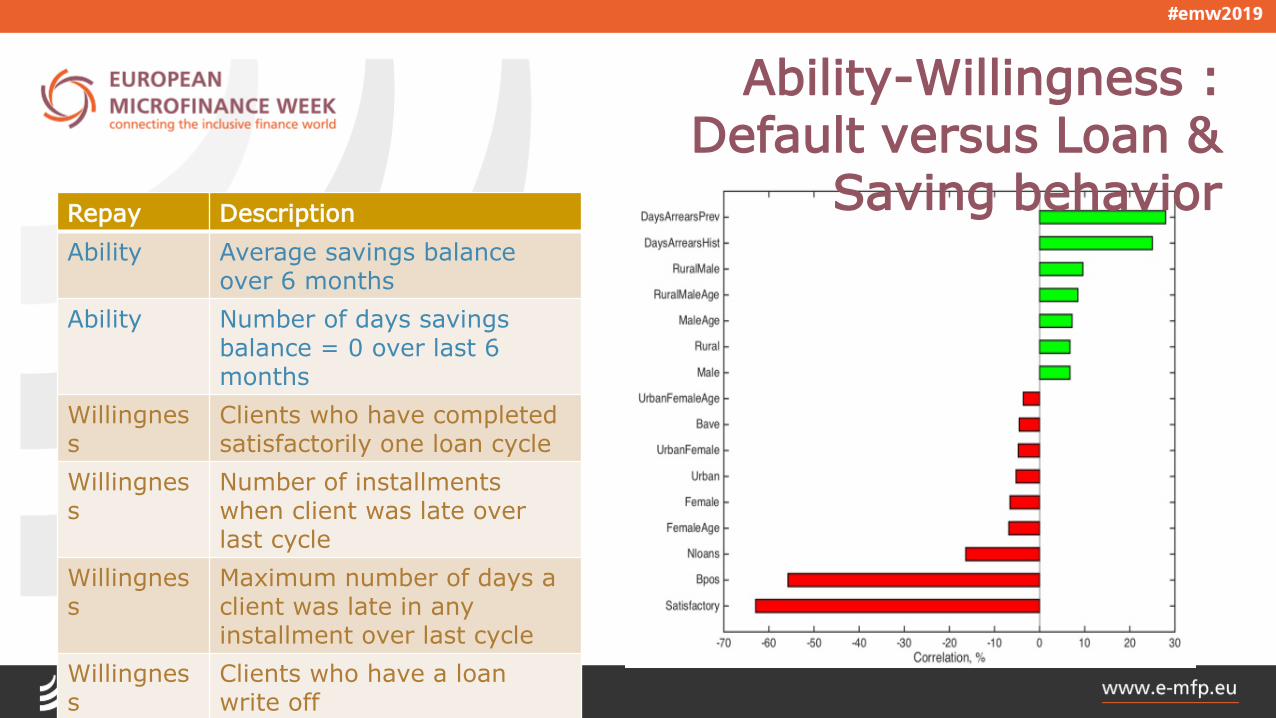

Repay Description

Ability Average savings balance over 6 months

Ability Number of days savings balance = 0 over last 6 months

Willingness

Clients who have completed satisfactorily one loan cycle

Willingness

Number of installments when client was late over last cycle

Willingness

Maximum number of days a client was late in any installment over last cycle

Willingness

Clients who have a loan write off

Ability-Willingness : Default versus Loan &

Saving behavior

Phone Call needed Loan Automatically Approved

Application Scoring

Lessons learned

Digitization must be incorporated into the business strategy of the MFI, have clear business drivers.

Digitization touches on all aspects of an organization: incremental introduction is a must!

Data analysis and Artificial Intelligence show how to combine social mission and economical viability:

Women are a desirable customer target group from both perspectives.

Opportunities for Gender Inclusion via Fintech

Bridget Dougherty

Program Head

BRAC International Microfinance

BRAC Global Footprint

Offices/Affiliates (3)

Netherlands

UK

USA

Operating countries (11)

Bangladesh

Afghanistan

Liberia

Myanmar

Nepal

Philippines

Rwanda

Sierra Leone

South Sudan

Tanzania

Uganda

Technical assistance

engagement (9)

Kenya

Philippines

Egypt

Rwanda

Pakistan

Tunisia

Uganda

Liberia

Lesotho

Country Clients Loan Out. Branches

Bangladesh 6 million $2.8 billion 2,272

Tanzania 198,683 $43.61m 151

Uganda 220,747 borrowers

69,273 savers $46.72m 163

Liberia 38,697 $5.07m 27

Sierra Leone 53,692 $6.93m 34

Myanmar 108,527 $21.44m 69

Rwanda (operation

started in July 2019)

934 borrowers

1,280 savers $.15m 3

At a Glance: BRAC Microfinance as of September 2019

BRAC INTERNATIONAL

MICROFINANCE MISSION

To provide a range of financial services responsibly to people at

the bottom of the pyramid.

We particularly focus on women living in poverty in rural and hard

to reach areas to create self-employment opportunities, build financial resilience, and harness women’s entrepreneurial spirit by empowering them economically.

Photo Credits: Matt Kertman, BRAC USA

“What would the advent of mobile money mean for microfinance generally and for our organization more specifically?”

“We realised quickly that our assumption—that what our clients want most is convenience—was wrong.” Bridging the Digital Gender

Divide in Financial Inclusion

LESSONS LEARNED

The switch to digital, especially for women who are particularly excluded, would not happen automatically.

Have to be deliberate and thoughtful about how to serve more women in poor and hard-to-reach areas, if we want technology to help to reduce the gender divide in financial inclusion.

THE IMPACT OF DISBURSING

MICROFINANCE LOANS WITH

MOBILE MONEY IN UGANDA

• 3,000 female microfinance clients from six branches in Kampala and Entebbe

- Is there demand from women clients for obtaining loans on a mobile money account?

- Does providing mobile money accounts, and the microfinance loan on a mobile money account, lead to more saving, business investment and profits for clients?

Conducted by Emma Riley, University of Oxford, Sept ’18

Locations of Participants

Stress gender lens

Add game story- hiding

loans in the household

https://novafrica.org/wp-

content/uploads/2019/05/

Hiding_loans_in_the_hou

sehold_using_mobile_mo

ney__Experimental_evid

ence_on_microenterprise

_investment_in_Uganda-

4.pdf

Over 700 successful disbursements with mobile money took place. However, there were initial and on-going difficulties

• Power cuts and unstable internet connections prevented the online platform being used; Network Failure

• The system involved a learning process during which disbursement with mobile money was slower than cash.

• Authorisation by multiple people was timely and delayed receipt of the mobile money loan

• Cross checking of correct sim numbers added to the timing

• If mobile disbursement failed the accountant had to make a second trip to the bank to withdraw cash or send clients home

DISBURSEMENTS WITH MOBILE MONEY

LESSONS LEARNED

Mobile Disbursement was most beneficial to women who

struggled with pressure to share money before the study.

Change Management: Don’t underestimate it

Mixed response to covering the related mobile charges

A stable internet connection is

needed

“The tax is a cost of using the

service. The benefits still outweigh the costs for me”

Women who receive their loan

on a mobile money account invest in 18%

more business assets. As a result

they have 15% higher profits (7% higher household

income)

“Saving on mobile money helps you to budget. When

you get hand cash you spend it.

When its on the mobile money

account you can withdraw only the money you need

and save the rest.”

Piloting Digital Agriculture Loan Starting date: February 2018

Objective: Understanding digital

credit risk scoring and mobile

money services for affordable

lending to smallholder farmers

99% of our clients are

women

93% of our staff are women

3 pilot loan cycles in East

Bago

Digital Agricredit for Smallholders in Myanmar

HCD Approach

Partners

Experian

IT vendor and Credit Scorer

Awhere

Crop suitability data provider from satellite data source

Ongo

Mobile money for loan disbursement and repayment.

L-IFT

Client enrolment and digital support for client.

Vendors

World Bank

Project coordinator, investor and platform owner, and policy advocacy

Telenor

MNO for Call Data Record (CDR) data provider for credit score

BRAC Myanmar Microfinance Co

Lending partner and operation lead

Daw Mya Khin has her member photo taken for registration

Trying to apply for a loan immediately after farmer orientation at

village meeting point

LESSONS LEARNED

Partnerships are key to unlocking the potential of technology, especially for women; But they can be challenging

Digital literacy is low, and lower for women - men have more phone ownership then women. Requires high touch as clients digital appetite is low

Digital credit scoring / decision making is complex as data is not mature and there is no SIM registration rules and no digital NRC (national registration card)

Need more flexible regulation for data sharing, that is supportive to the sector

Max $400

28% annual effective, RBM

3 months grace, 4th & 5th M

50% principle +interest

Less docs, Apply through

phone; Tech and human high

touch for decision

5 Months duration

BRAC has been announced the world’s number

1 NGO of 2019 by NGO Advisor, an independent

media organization based in Geneva.

BRAC retained the top spot for the fourth year in a row

in part due to its leadership of the Rohingya refugee

crisis, innovative new partnerships, and the continued

scale of its reach.

THANK

YOU

BETA SAVINGS PROPOSITION

A DIGITAL FINANCIAL SOLUTION FOR LOW INCOME MARKET WOMEN IN NIGERIA

BY

NJIDEKA NWABUEZE

ACCESS BANK & UN/DER BANKED WOMEN

Background

• Commercial bank with a fast-growing retail division • Sees financial inclusion as market development for growth • Expertise in technology, channels, managing outsourced sales team • National network of over 600 branches - potential for impact at

scale is significant • Opportunity to increase participation of women in customer base,

from less than 20% at baseline to 40% • Partnered with Women’s World Banking, EFInA, VISA and FSD

Africa.

OUR PARTNERS

BARRIERS TO WOMEN FINANCIAL INCLUSION

• Tend to be less literate and educated than their male counterparts

• Women are time poor and less mobile due to competing household and business priorities

• Less likely to have IDs or other legal documentation to open account

• Familiar with informal savings mechanisms but lack trust and confidence when it comes to formal financial services

• Women value Proximity and convenience – Accessibility- availability of their funds when they need the funds and Safety - to prevent misuse of the funds.

Overall women exhibit steeper adoption curves when it comes to technology

DEVELOPING A PROPOSITION FOR UN/DER BANKED WOMEN

• BETA Savings (“better” in Pidgin) is a simple savings account tailored for market women that offers maximum convenience to customers by delivering a low-cost banking service to their shops

• No forms, no signature, no ID required, no account references, no minimum balance

• No monthly fee, no deposit fee, no withdrawal fee (ATM/branch)

• Free starter pack with ATM card for instant account opening

BETA Savings is a simplesavings account tailored for low income market women

• The Customer’s Name • Customers Registered Mobile Phone

Number • Place of Birth • Date of Birth • Gender • Address • Next of Kins (Name and Phone number) • Initial deposit of N1,050 (This is fee for

the instant debit cards and VAT)

• Accounts are opened via phone in the field

ACCOUNT OPENING REQUIREMENTS

BETA OPERATING MODEL

ATM Branch

FAST ACCOUNT OPENING

Account opened in five minutes, from anywhere. BETA Friend captures data and photo through mobile app. Customer receives account number and mobile PIN via SMS. Customer receives starter pack with debit card, PIN mailer and info guide. EDUCATIONAL MARKETING

“Practical educational messages integrated in sales tool for BETA Friends, and in info guide in starter pack.

BETA Friend Market-based sales and service team. Promotes BETA & opens accounts. Collects deposits, handles withdrawals in the field.

Closa Agent

The success of this proposition is dependent on the success of the BETA friend who provides a friendly, trusted and dependable

service to customers

Brand Ambassadors; Face of the Bank, radiating trust, smartness and

friendly charisma

Collections: The primary collector, driving collections by providing the convenience the customer enjoys.

Service: Primary service channel, act as service providers thereby reducing traffic in the branch

Relationship officers: The main interface with the customers. Maintaining trust and accountability.

BETA FRIENDS - ROLE

BETA

Savings

Account

BETA

Target

Savings

Value

Added

Services

BETA

Kwik

Loan

• Transactional savings account

• Bridges distance between banks and market traders

• Over 900,000 customers

• Customers choose a target goal

• Save for 3, 6, or 12 months

• 300,000 investments booked

• Digital credit product. • Meet short-term needs

of market traders up to NGN 50,000 for a period of 30 days.

• 1,584 loans disbursed as of pilot completion

• Balance inquiry.

• Airtime purchase.

• Transfers. • 300,000 +

users

BETA SUITE OF PRODUCTS DEVELOPED TO MEET GROWING NEEDS OF MARKET TRADERS

RESULTS TILL DATE

• 321 branches, Over 1,300 BETA Friends • About 1 million accounts opened • 40% women • ₦8.5 billion deposit volume ($23.3million) • 45% have more than one transaction per month • 28.5% of account holders are previously unbanked CUSTOMER FEEDBACK BETA receives high rating from customers – it combines the convenience of informal systems with the security of saving with a bank. It is lower cost, pays interest, and offers 24/7 access to your money through the ATM/Agents.

“They’re collecting every day. I love it. It’s not every time [that] we’ll have time to go to the bank.” (Focus Group, Women, Balogun Oke-Arin)

Thank you