Embed Size (px)

Citation preview

Operational, Transitional and Exit Strategies for Closely-

Held and Entrepreneurial Business Owners

Robert Gabrielski, Esq., Moderator

1/17/2007

Joe Faire

Not Faire

Uma Faire

Well Faire

Boris & Natasha

Business Ownership and Transitions

Stefanie McNamara

Laize Faire Software

Organized as a C-Corporation Choose right entity for transition planning

Tax planning Management structure Ownership structure Possibility of providing incentive arrangements

Laize Faire may not have been organized as a C-corp today

Choosing an Entity

Corporation Centralized management Taxation on entity and shareholder level

S-Corporation Tax election as shareholder pass-through Subject to certain limitations

No more than 100 individual shareholders May only have common stock

Choosing an Entity – con’t

Limited Liability Company Pass-through taxation No personal liability for members Flexibility in structuring management; ownership

rights and distribution rights Partnership

Pass through taxation Personal liability for partners

Negotiating Exit Strategies (Cashing out)

Plan for exits in buy-sell agreement Provide liquidity of ownership interest Exits may be restricted but cannot completely

prohibit transfer Issues to consider in planning transition

Voluntary transfer restrictions Address and plan for involuntary transfers Structure different classes of ownership rights

(depends on type of entity)

Restrictions on Voluntary Exits

Right of First Refusal Must offer to other owners and/or company first on same

terms and conditions

Put/Call Rights Shareholder’s right to require other shareholders and/or

company to buy interest (Put) Company’s right to purchase interest (Call)

Tag/Drag Along Rights Right (Tag-Along) or requirement (Drag-Along) to

participation in sale of assets or ownership interest

Address Involuntary Exits

Death Disability Retirement Termination for Cause Lien placed on interest (i.e., bankruptcy) Valuation; terms of payment - may depend on

circumstance

Structuring Ownership Rights

Vehicle to facilitate transition Can have varied rights (i.e., voting or non) Can be equity, debt and/or combination Can be structured to:

maintain control obtain preferred return offer incentive compensation provide liquidation or any other preference

Executive CompensationCharles A. Bruder, Esq.

Executive Compensation

Planning Considerations

Attract new employees Retain existing “key employees” Provide employees with a greater sense of

involvement in the financial performance of

the company

Executive Compensation

Additional Considerations Succession planning issues Increased productivity/profitability

Financial targets Cash flow planning issues

Employment contracts – “golden handcuffs”

Executive Compensation - Equity

Outright grants of stock shares/LLC units Provides the employee with an ownership interest

in the company Permits the employee to share in the financial

success of the company Can utilize different classes of stock Shareholder dilution/transferability issues Current income taxation

Executive Compensation – Equity

Restricted Shares/LLC Units Addresses transferability issues May result in deferred income tax recognition by

the recipient Requires a written agreement between the

company and the employeeShareholders Agreement

Liquidity issuesBuy-back, claw back, employment termination

Executive Compensation – “Phantom Equity”

A bookkeeping entry that provides an “equity like” interest Value may be determined based upon an

underlying equity interest in the companyStock Appreciation Rights (“SARs”)

Can provide for dividends/distributions Does not provide the plan participant with an

ownership interest in the company Liquidity issues

Executive Compensation – Deferred Compensation

Current promise to pay compensation in the future Flexible structure – nonqualified arrangement Company stock/equity can be an “investment”

option Easily tied to company financial performance Administrative burdens/liquidity issues Code Section 409A Funding options

Executive Compensation – Other Equity Arrangements

Stock Options Non-qualified and incentive stock options

Qualified Defined Contribution Retirement Plans Investment options Matching contributions

Employee Stock Ownership Plans (“ESOPs”) Employee Stock Purchase Plans (“ESPPs”)

Executive Compensation - Planning Considerations

Who should benefit? What type of benefit should a participant

receive? What costs are involved to the sponsoring

company? Incentive compensation goals vs. succession

planning goals Income tax issues Cash flow maintenance

Tax Minimization

William J. McDevitt, CPA, CVA

What taxes are we trying to minimize?

Income tax Ongoing operations Sale of business

Estate / Gift tax Sales and Use Import / Export duties ALL OF THEM

Three Rules for Making Effective Business Decisions

Decisions should make sense short-term Decisions should position the business for

the best chance of long-term success Decisions should be tax-efficient

(See the three rules of tax planning)

Sale of a Business

What do sellers want?

Maximum selling price Minimize tax / taxable income

What do buyers want?

Lowest possible selling price Maximize current tax deductions*

* Public companies are generally more interested in maximizing EPS than minimizing taxes

Tax Rates

Federal Top Rate

Ordinary 35% Capital gains (long-term) 15%

Tax Rates

Top Rate

AMT 28% AMT – Capital gains (long-term) 15%

Tax Rates

State Top Rate

New Jersey 8.97%

Note: State taxes are not deductible when subject to AMT

What are you selling?

Stock / Partnership / Interest Asset Sale

Purchase Price Allocation

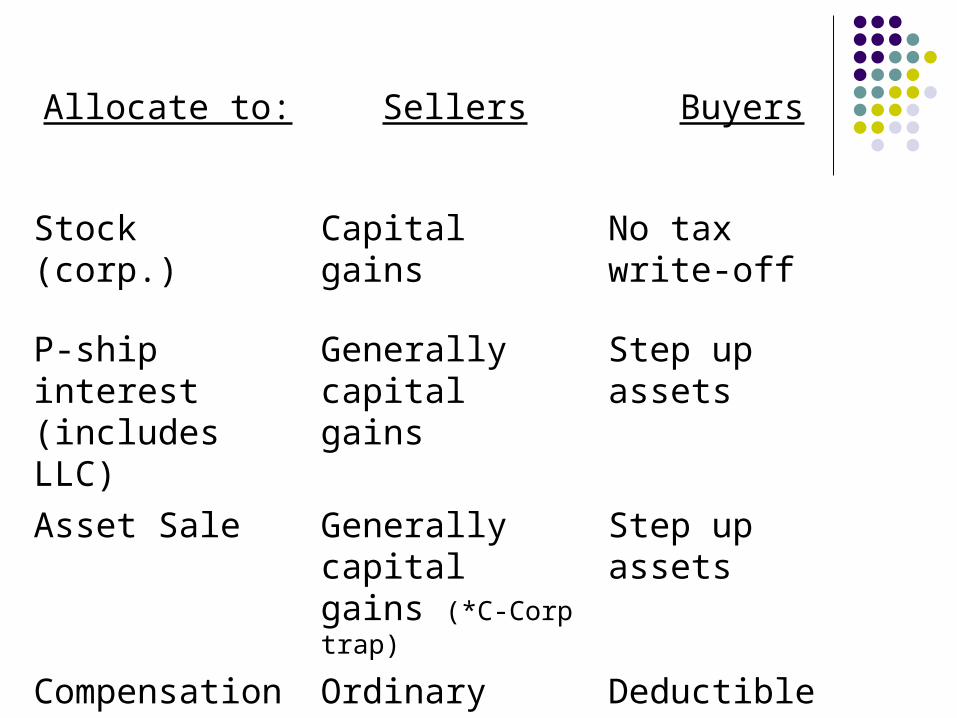

What is good for sellers may not be good for the buyer

Allocate to: Sellers Buyers

Stock (corp.) Capital gains No tax write-off

P-ship interest (includes LLC)

Generally capital gains

Step up assets

Asset Sale Generally capital gains (*C-Corp trap)

Step up assets

Compensation Ordinary plus FICA or SE

Deductible

Worst Case

C-Corp Asset SaleAssume selling price $92,000,000C-Corp tax (40%) – 36,800,000Proceeds to seller $ 55,200,000Individual tax (24%) – 13,248,000Net after tax to seller $ 41,952,000

Tax cost ≈ 55%

New Businesses

Generally should be Partnerships for tax reasons Corporate protection for legal reasons

“LLC”

Traps

Allocation of purchase price to: Ongoing consultation

Good for buyer

Bad for seller

Business Valuation Issues

Why do you value a business?

Buy/sell agreements Possible sale Estate/Gift Litigation

How do you value a business?

Depends on the purpose However basic, the concepts are the same

How do you value a house?

Comparables Correlate to subject house

With a business valuation, there is less reliable information available on the sales of other businesses

Case Study One

Cardboard box Every Monday the box generates $100 (except for

two weeks of summer) The box has followed this pattern for the last 50

years The box is expected to continue this path for the

next 50 years

What would you pay for the box?

Case Study Two

Cardboard box Every Monday the box requires a deposit of $100

(no summer vacation) The box has followed this pattern for the last three

years The expectation is that the box now contains the

next big thing in the industry

What would you pay for the box?

Discounts for Lack of Control and Lack of Marketability

If Boris is to get a 10% interest Subject to numerous restrictions

Transferability Voting Rights Etc.

Discounts for Lack of Control and Lack of Marketability

Then the value of the 10% is not $9.2 million (10% of $92 million)

It is worth less than $9.2 million

Financial Strategies for Business Owners

Patrick Sheridan

Where Are You Now?

The Business Cycle: Time

Survival Growth MaturityPlanned Transfer

No Plan

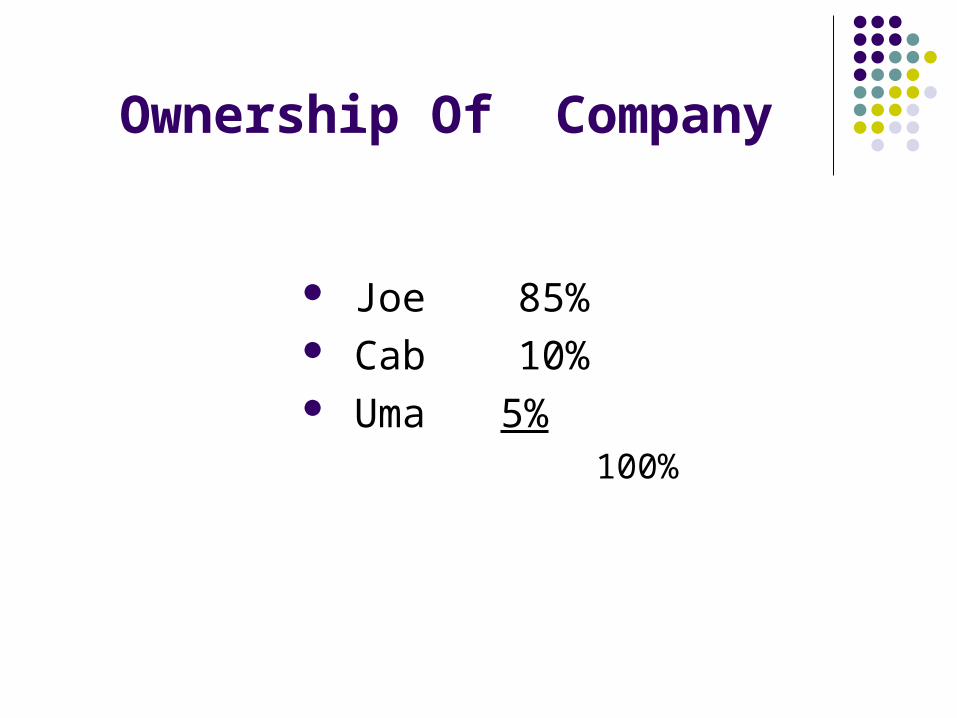

Ownership Of Company

Joe 85% Cab 10% Uma 5%

100%

What Could Get in the Way?

Owner (s) / Key Person (s)

Disability Death

Buy-Sell Agreement

Who are the potential buyers? If Joe sells company to Boris? After Joe dies who buys the company ?

10 yr Installment note $85,000,000 @ 6%

annual payment $11,000,000

Life Insurance policy for $85,000,000

annual premium $2,250,000

Salary Continuation

Agreement between company and employee covering retirement and death

Key Person - Equation

Management Talent / Capital = Return Money Rates

Protecting Your Company’s Assets Through Confidential,

Non-Compete and Invention Agreements

Patrick T. Collins, Esq.

Business Value/Employment Contracts

Do they exist? What are their terms? Are they enforceable?

The Basics

What is an employer’s protectable interest and how is that defined? Customer relationships Confidential business information Trade Secrets

To What Specific Information Have Courts Granted Protection?

Scientific data, chemical processes, manufacturing methods

Business information-marketing plans, pricing policies, financial information

Computer programs/data compilation Client lists, needs, preferences and/or

contacts

“Trade Secret” Status Will Not Be Provided To

The general skills/experience an employee acquires over time

Specialized skills, experience, contacts which an employee had prior to working for an employer

Factors In Determining Whether Information Is Proprietary1) The extent to which the information is known

outside of the owner’s business;2) The extent to which it is known by employees and

others involved in the owner’s business;3) The extent of measures taken by the owner to

guard the secrecy of the information;4) The value of the information to the owner and his

competitors;5) The amount of effort or money expended by the

owner in developing the information;6) The ease or difficulty with which the information

could be properly acquired or duplicated by others.

Missing Information

When did Boris sign the Agreement? Where was it signed? How long are the restrictions? What are the restrictions?

Geographic Customer Based

Blue Pencil States?

“Work-For-Hire” AgreementsThe General Rule:

Inventions belong to the inventor-the person who conceived, developed and perfected it

Exceptions:

Employees hired to invent Specific contractual arrangements

Employment for Purpose of Inventing

Definition: Employee who is hired for purpose of inventing and who succeeds in accomplishing task during employment must assign to employer all rights to the invention.

Invention must be developed during period of employment Express agreement on scope of employment should be

present Place where invention created generally not determinative

Shop Rights

Invention made by employee during working hours using employer’s materials and equipment provides employer with irrevocable but non-exclusive right to use of invention.

Employer does not obtain a shop right where idea was originated and fully developed by employee at home and not using material or labor of employer.

Shop right is personal and exclusive to employer. Cannot be assigned or transferred by employer to third party.

Written Agreements

Consideration (Employment/Continued Employment)

Permissible Scope- Generally Courts will not enforce agreements that

unreasonably obligate an employee to transfer ownership rights in each and every instance.

Typical Contract Language

The employee agrees to assign all inventions except those for which no equipment, supplies, facilities or trade secrets of employer was used and which was developed on employee’s own time unless (i) invention relates to business of employer or (ii) invention results from work performed for employer.

What Happens If Boris Leaves?

Why/How did Boris leave? Holdover invention agreement

- Generally must be limited to a reasonable time and to subject matter which employee worked on or had knowledge of during employment

Miscellaneous Issues

Successor/Assignability Liquidated Damages Forfeiture for Violation

The Corporate Opportunity Doctrine

1. A corporate opportunity is presented to an employee;

2. The company can undertake it financially;

3. It falls within the company’s normal business;

4. The company has an interest/expectancy in such opportunities.

Q & A

Thank you.Please fill out our seminar evaluation form.

![PRECEDENTIALSimran Dhillon, Esq. Max C. Kaufman, Esq. [ARGUED] Nancy Winkelman, Esq. Lawrence S. Krasner. Esq. Carolyn Engel Temin, Esq. Philadelphia County Office of District Attorney](https://img.dokumen.tips/doc/110x75/5f591458cf1cd86f902d709f/simran-dhillon-esq-max-c-kaufman-esq-argued-nancy-winkelman-esq-lawrence.jpg)