Embed Size (px)

Citation preview

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 1

Operational, Financial and Strategic Measures of Performance

Part A

Suggested References

When studying this topic you should refer to the following resources:

Primary Reference

Garrison, R.H., Noreen, E., and Brewer P. C., Managerial Accounting, 11th edition, Chapters 10,

16 and 17.

Supplementary References

Atkinson, A.A., Banker, R., Kaplan, R.S. and Young, D.W., Management Accounting, 4th edition,

2003, Chapter 9.

Brigham, Eugene F., and Houston, Joel F., Fundamentals of Financial Management, 9th edition,

1999, Chapter3.

Epstein, Marc and Wisner, Priscilla, “Using a Balanced Scorecard to Implement Sustainability”,

Environmental quality Management, Winter 2001 pp. 1-10.

Hansen, Don R., and Mowen, Maryanne M., Management Accounting (8th ed.), South Western

Publishing Co., Cincinnati, Ohio, 2007, Chapter 10 and Chapter 13.

Horngren, C.T., Datar S.M., and Foster, G., Ittner, C. and Rajan, M. Cost Accounting: A

Managerial Emphasis, 13th edition, 2008, Chapter 13.

Hurle, Mike, “Are You Balanced?”, A Plus, September 2005, pp. 29-32

Kimmel, P.D., Carlon, S., Loftus, J., Mladenovic, R., Kieso D.E., and Weygandt J.J., Accounting:

Building Business Skill, John Wiley and Sons, Ltd, Australia, 2003, Chapters 10 & 11.

Robinson, Thomas R., Munter, Paul, Grant, Julia, Financial Statement Analysis: A Global

Perspective, 2004

White, Gwendolen, “How to Report a Company’s Sustainability Activities”, Management

Accounting Quarterly, Fall 2005, pp. 36 – 43.

Bibliographic References

Kaplan, R.S. and D.P. Norton (1992). The Balanced Scorecard - Measures that Drive

Performance. Harvard Business Review, January-February, 71-79.

Kaplan, R.S. and D.P. Norton (1996a). The Balanced Scorecard: Translating Strategy into

Action. Harvard Business School Press, Boston.

Kaplan, R.S. and D.P. Norton (1996b). Using the Balanced Scorecard as a Strategic

Management System. Harvard Business Review, January-February, 71-79.

Kaplan, R.S. and D.P. Norton (1996c). Linking the Balanced Scorecard to Strategy. California

Management Review, Fall, 53-69.

Kaplan, R.S and D.P. Norton (2001a). Transforming the Balanced Scorecard from Performance

Measurement to Strategic Management: Part 1. Accounting Horizons, March, 87-104.

Kaplan, R.S and D.P. Norton (2001b). Transforming the Balanced Scorecard from Performance

Measurement to Strategic Management: Part 2. Accounting Horizons, June, 147-1

Section

9

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 2

Part B

Topic Learning Outcomes

On completion of this module, you should be able to:

i) Calculate financial, strategic and operational performance measures and understand the relationships between them.

ii) Describe the role of cash flow analysis in the evaluation of the organisation’s strategic and operational plan.

iii) Describe the interrelationships between shareholder wealth creation and performance measures aligned to that objective, including agency theory and its relationship to managerial incentive schemes

iv) Identify financial and non-financial measures of business profitability including cash flow measures.

Operational, financial and strategic measures of performance:

• Overall performance measures

• Financial measures

• Profitability

• Economic value added (EVA®)

• Cash flow

• Growth

• Financial and operating ratios

• Non-financial measures

• The balanced scorecard

• The performance pyramid

• Reporting and evaluating sustainability

• Agency theory and managerial incentive schemes

v) Describe measures of entity growth.

vi) List the main steps in translating strategies and plans into goals, recognising their interrelationships.

vii) List the limitations of benchmarking in facilitating organisational change.

viii) Describe the relationships between financial and operating ratios and be able to interpret trends over time and across time.

ix) Explain the key components of the balanced scorecard.

You may choose to complete this topic in a step-by-step way or skip ahead, depending on your

knowledge and assessment of your own competency in relation to the above Learning Outcomes.

Part C

Contents of this Section

9.1 Introduction ........................................................................................................................ 2 9.2 Overall performance measures ......................................................................................... 3 9.3 Financial measures............................................................................................................ 4 9.4 Profitability.......................................................................................................................... 4 9.5 Economic value added (EVA

®) .......................................................................................... 5

9.6 Cash flow ........................................................................................................................... 5 9.7 Growth.............................................................................................................................. 10 9.8 Financial and operating ratios .......................................................................................... 12 9.9 Non-financial measures ................................................................................................... 18 9.10 The balanced scorecard .................................................................................................. 19 9.11 The performance pyramid................................................................................................ 20 9.12 Reporting and evaluating sustainability............................................................................ 21 9.13 Agency theory and managerial incentive schemes.......................................................... 22

9.1 Introduction

In Section 8 we looked at designing and tailoring performance measures to suit the structure of

an organisation. In this section we look at applying performance measures to an organisation to

evaluate its financial, strategic and operational performance. First we consider the differences in

performance measures and how to calculate some of the main types. The links between different

types of measures are also examined. Secondly, cash flow analysis is presented, with a focus on

its relevance to strategic planning and operational planning. Shareholder valuation techniques,

such as EVA®, are shown to be consistent with shareholder value maximisation.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 3

In the last part we analyse ratios, both in isolation and in conjunction with other ratios.

9.2 Overall Performance Measures

9.2.1 Alignment with Strategic Goals

Most management accounting commentators agree that a mixture of financial and non-financial

measures is the appropriate methodology to judge business or business unit performance. This

is known as the Balanced Scorecard approach (BSC) (Kaplan & Norton 1992). The performance

measures should be aligned with the strategic goals of the organisation, which may be growth,

profitability or survival. Both financial and non-financial performance measures are very

important.

9.2.2 Comparisons and Benchmarking

In order to measure performance, there must be comparisons made:

• To the organisations past performance or budget;

• Between divisions of the organisation; and

• With the organisation’s competitors.

Benchmarking is a continuous and systematic process of evaluating the products, services and

work practices of an organisation against businesses that are considered to be the best

performers in the practice or industry (competitors). It is a continuous process that allows an

organisation to consider its financial and strategic position relative to world’s best practice.

The steps in benchmarking are as follows:

• identify the functions to be benchmarked;

• select benchmark partners;

• collect data and perform analysis to identify performance gaps;

• establish performance goals to narrow performance gap;

• implement plans.

Benchmarking provides the opportunity to compare performance across sites and between

companies to give an indication of current best practice. Potential sources for gathering data are:

• newspaper articles/ business magazines and journals;

• market research;

• inter-firm comparison reports (from government bodies);

• brokers/bankers or market analysts reports;

• exhibitions, trade fairs; and

• hiring of ex-employees.

Accurate and relevant information is often difficult to obtain, as it is likely to be closely guarded by

competitors, yet can be used as a comparative tool.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 4

9.3 Financial Measures

Financial measures of performance are covered under the following headings:

• Profitability (section 9.4)

• Economic value added (EVA™) (section 9.5)

• Cash flow (section 9.6)

• Growth (section 9.7)

• Financial and operating ratios (section 9.8).

9.4 Profitability

9.4.1 Return on Investment (ROI) and Residual Income (RI)

In section 8 individual divisions were evaluated using ROI and RI. These techniques can also be

applied to the organisation as a whole.

9.4.2 Return on Equity (ROE)

ROE measures the performance of the firm’s management in respect of their ability to invest

shareholder’s funds (equity). The usual calculation of ROE is:

Operating profit

Equity

Example: Assume two firms Company A and Company B with Operating Profit and Equity

balances of:

Company A Company B

Revenue $2,500,000 $9,600,000

Variable Expenses 1,880,000 6,560,000

Fixed Costs 300,000 2,400,000

Operating Profit 320,000 640,000

Total Assets 6,000,000 13,000,000

Total Liabilities 4,800,000 11,400,000

Equity 1,200,000 1,600,000

Company A has ROE of 26.67% ($320,000/$1,200,000) and Company B 40%

($640,000/$1,600,000). ROE would suggest Company B is more profitable but it is important to

consider the level of debt as this affects both the profit and the equity balances. The Du Pont

Formula, introduced by the Du Pont Company in the USA in the 1920s, can be used to further

decompose the ROE into its component parts. For more details, see Section 8.3.2 or any good

Finance Text, such as Brigham and Houston (1999), Chapter 3.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 5

9.5 Economic Value Added (EVA®

)1

EVA® has become widely used by profit-seeking organisations in recent years. The basic

calculation is as follows:

EVA® =

Net operating profit after tax

(NOPAT) –

[Total assets less current liabilities]

x

Weighted average cost of capital

The cost of capital is the required or minimum rate of return necessary to compensate the firm’s

capital contributors (equity investors and debt issuers) for the risk of the investment. Consider

the following example.

Information $

Sales 3,200,000

Operating expenses 2,000,000

Operating profit before tax 1,200,000

Income tax at 16% 192,000

Operating profit after tax 1,008,000

Total assets less current liabilities 10,000,000

Cost of capital 6%

The EVA® for this period is HK$408,000 because over this period, HK$408,000 of value has been

added to the company’s value. (The charge for the cost of capital was 6% of $10,000,000 or

$600,000). There are some differences in application of the EVA® number. Some commentators

use average capital over the period while others use beginning of the period capital.

It should be noted that there are more sophisticated EVA® models advocated by Stearns and

Stewart, the initial advocates of the method. However these models tend to be variations on the

basic calculations above, and also suffer from the major problem with the calculation i.e. the

numbers are based on accounting book values and do not necessarily reflect “true” economic

value.

9.6 Cash Flow

9.6.1 Overview

The management of cash flow is very important as cash balances must be maintained at a

sufficient level to ensure that enough cash is available to meet the organisation’s short-term cash

disbursement requirements and investment in idle cash balances is reduced to a minimum. The

organisation must be able to maintain inventories or pay for purchases (Just in Time); offer

competitive credit terms, and meet its short-term and long-term operating and financing costs as

they fall due. Failure to meet maturing liabilities on time makes the organisation technically

insolvent. Holding excess reserves of cash is also potentially dangerous as it can result in a loss

in profitability and it may increase the attractiveness of the organisation as a potential takeover.

1 EVA is a registered trademark of the Stern Stewart Corporation.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 6

9.6.2 Factors Affecting Cash Flows

Organisations experience irregular increases in their cash holdings due to external and internal

factors. External factors affecting cash inflows include sale of securities, such as ordinary shares,

preference shares, bonds and debentures or non-marketable debt contracts, including loans from

commercial banks. These cash flows tend to be irregular because there are usually large sums of

money involved. Other sources of cash arise from internal operations and occur on a more

regular basis. These usually comprise receipts from accounts receivable collections, cash sales

and sales of fixed assets. Decreases in cash arise from the payment of preference and ordinary

dividends, interest and principal repayments on debt, taxation liabilities; acquisition of fixed assets;

and purchases of raw materials and inventories for production.

If excess cash becomes temporarily available, the organisation purchases marketable securities

or where a cash deficit is forecast, a portion of the organisation’s marketable securities portfolio is

liquidated or short term borrowings can be made.

9.6.3 Reasons for Holding Cash

There are three reasons for holding cash: First to pay transactions arising in the ordinary course

of business. Secondly, for precautionary reasons as a buffer to satisfy potential cash needs.

Thirdly, for speculative purposes in order to take advantage of potential profit making situations.

9.6.4 Cash Flows and Performance

Managing the organisation’s cash flow involves simultaneous and interrelated decisions regarding

investments in current and non-current assets and the use of current liabilities. Cash flow

measures indicate the dividend or debt-paying ability of the firm, the ability of the firm to provide

for future growth opportunities and the general solvency of the firm.

a) Marginal Cash Flow

Marginal cash flow shows the net of the variable cash inflows generated by operations after

financing the variable working capital used by these operations. Marginal cash flow is the

difference between the margin of a product and the marginal working capital required to support

the sale of the product which includes trade debtors and inventory, less trade creditors required

for the next unit of product or service. It helps to indicate what is likely to happen to cash flow in

the future if these fundamental relationships are maintained. The marginal cash flow (MCF)

calculation is:

MCF = contribution margin - change in working capital where the change in working capital is an

increase in working capital.

b) Operating Cash Flow

Operating cash flow measures the cash generated from operations, less the cash invested to

fund operations and indicates whether the business’ ongoing ordinary operations are providing

cash towards paying interest, tax, dividends, etc. If operating cash flow is negative there is not

necessarily a problem. The business may be investing in fixed assets for future growth.

Operating cash outflows are funded by increased borrowings or equity.

The operating cash flow (OCF) calculation is:

OCF = EBIT - change in net operating assets

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 7

c) Net Cash Flow

Net cash flow is the real cash flow, the change in borrowings for the year. Depreciation and other

non-cash items are included in the determination of retained income and in the change in net

assets. Net cash flow is the operating cash flow less interest, tax, dividends and extraordinary

items (if applicable) and changes in equity, provision for tax and provision for dividend (if

applicable).

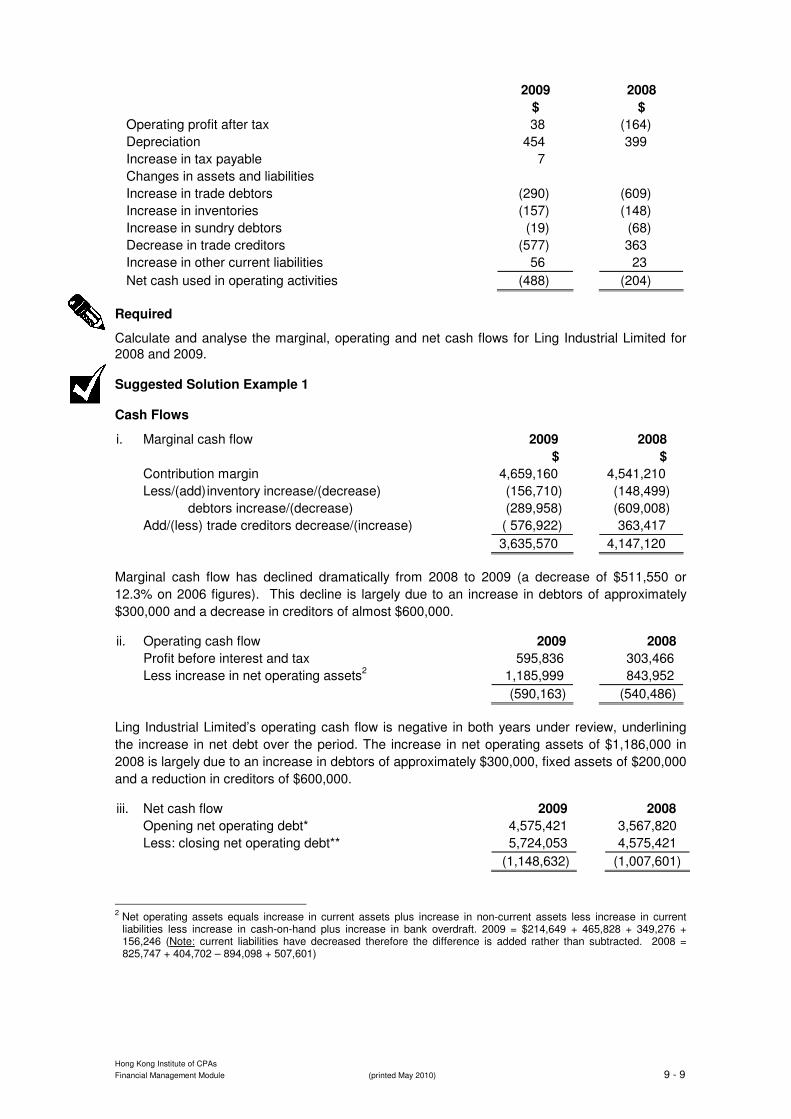

Example 1: Cash Flows

The following information relates to Ling Industrial Ltd.

Ling Industrial Limited: Balance Sheet as at 31 December 2009

Note 2009 2008 2007

$ $ $

Current assets

Accounts receivable 2,732,315 2,442,357 1,833,349

Inventory 1 1,412,935 1,256,225 1,107,726

Sundry debtors 189,700 170,540 102,300

4,334,950 3,869,122 3,043,375

Non-current assets

Fixed assets 4,599,772 4,385,123 3,980,421

Total assets 8,934,722 8,254,245 7,023,796

Current liabilities

Bank overdraft 2,224,053 2,075,421 1,567,820

Accounts payable 684,426 1,261,348 897,931

Other current liabilities 133,900 62,500 39,420

3,042,379 3,399,269 2,505,171

Non-current liabilities

Commercial bill 3,500,000 2,500,000 2,000,000

Total liabilities 6,542,379 5,899,269 4,505,171

Net assets 2,392,343 2,354,976 2,518,625

Shareholders equity

Share capital 1,000,000 1,000,000 1,000,000

Retained profits 1,392,343 1,354,976 1,518,625

2,392,343 2,354,976 2,518,625

Note 1: Inventory

Raw materials 320,649 298,851 270,511

WIP 274,943 173,752 120,344

Finished goods 817,343 783,622 716,871

1,412,935 1,256,225 1,107,726

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 8

Ling Industrial Limited: Profit and Loss Account for the year ended 31 December 2009

2009 2008

$ $

Sales 10,259,006 10,456,640

Cost of sales

Direct materials 3,276,495 3,439,624

Direct labour 1,919,093 2,051,656

Production o/heads variable 404,258 424,150

Production o/heads fixed 1,063,775 1,131,185

6,663,621 7,046,615

Gross profit 3,595,385 3,410,025

Overhead expenses

Admin salaries 838,572 881,010

Overhead expenses 2,160,977 2,225,549

2,999,549 3,106,559

Profit before interest and tax 595,836 303,466

Interest expense 551,429 467,115

Tax 7,040 -

Net profit after tax 37,367 (163,649)

Ling Industrial Limited: Statement of Cash Flows for the year ended 31 December 2009

Note 2009 $000

inflows (outflows)

2008 $000

inflows (outflows)

Cash flows from operating activities

Receipts from customers 9,950 9,779

Payments to suppliers and employees (9,887) (9,516)

Interest paid (551) (467)

Net cash used in operating activities 2 (488) (204)

Cash flows from investing activities

Payment for property, plant and equipment (669) (803)

Net cash used in investing activities (669) (803)

Cash flows from financing activities

Proceeds from borrowings 1,000 500

Net cash provided by financing activities 1,000 500

Net increase (decrease) in cash held (157) (507)

Cash at beginning of period (2,075) (1,568)

Cash at end of period (2,232) (2,075)

Note 2: Reconciliation of net cash used in operating activities to operating profit after tax

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 9

2009 2008

$ $

Operating profit after tax 38 (164)

Depreciation 454 399

Increase in tax payable 7

Changes in assets and liabilities

Increase in trade debtors (290) (609)

Increase in inventories (157) (148)

Increase in sundry debtors (19) (68)

Decrease in trade creditors (577) 363

Increase in other current liabilities 56 23

Net cash used in operating activities (488) (204)

Required

Calculate and analyse the marginal, operating and net cash flows for Ling Industrial Limited for 2008 and 2009.

Suggested Solution Example 1

Cash Flows

i. Marginal cash flow 2009 2008

$ $

Contribution margin 4,659,160 4,541,210

Less/(add) inventory increase/(decrease) (156,710) (148,499)

debtors increase/(decrease) (289,958) (609,008)

Add/(less) trade creditors decrease/(increase) ( 576,922) 363,417

3,635,570 4,147,120

Marginal cash flow has declined dramatically from 2008 to 2009 (a decrease of $511,550 or

12.3% on 2006 figures). This decline is largely due to an increase in debtors of approximately

$300,000 and a decrease in creditors of almost $600,000.

ii. Operating cash flow 2009 2008

Profit before interest and tax 595,836 303,466

Less increase in net operating assets2 1,185,999 843,952

(590,163) (540,486)

Ling Industrial Limited’s operating cash flow is negative in both years under review, underlining

the increase in net debt over the period. The increase in net operating assets of $1,186,000 in

2008 is largely due to an increase in debtors of approximately $300,000, fixed assets of $200,000

and a reduction in creditors of $600,000.

iii. Net cash flow 2009 2008

Opening net operating debt* 4,575,421 3,567,820

Less: closing net operating debt** 5,724,053 4,575,421

(1,148,632) (1,007,601)

2 Net operating assets equals increase in current assets plus increase in non-current assets less increase in current

liabilities less increase in cash-on-hand plus increase in bank overdraft. 2009 = $214,649 + 465,828 + 349,276 + 156,246 (Note: current liabilities have decreased therefore the difference is added rather than subtracted. 2008 = 825,747 + 404,702 – 894,098 + 507,601)

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 10

*Opening net debt 2009 2008

Total liabilities 5,899,269 4,505,171

less a/c payable 1,261,348 897,931

less other liabilities 62,500 39,420

net debt 4,575,421 3,567,820

**Closing net debt 2009 2008

Total liabilities 6,542,379 5,899,269

less a/c payable 684,426 1,261,348

less other liabilities 133,900 62,500

net debt 5,724,053 4,575,421

Net Cash Flow

The cash flow or change in net debt can also be calculated for 2009 as follows:

Net profit after tax for the year ended 31 December 2009 37,367

Less: Increase in net operating assets 1,185,999

Net cash outflow (1,148,632)

Net cash flow can be reconciled to operating cash flow in 2009 as follows:

Operating cash flow (590,163)

Less: interest (551,429)

Less: tax (7,040)

Net cash outflow (1,148,632)

9.7 Growth

9.7.1 Overview

Short term financial growth measures include percentage changes in: gross sales revenue, net

profit and earnings per share.

9.7.2 Percentage Change in Gross Sales Revenue

This is used to indicate growth at either the strategic level (i.e. organisation-wide) or at the

business unit (operational) level. Reasons for changes should be carefully scrutinised relying on

trends and comparisons with competitors.

9.7.3 Percentage Change in Net Profit

Net profit can also change for a number of reasons, including changes to cost structures,

changes to selling prices and external changes such as new accounting standards.

9.7.4 Percentage Change in Earnings Per Share

Brokers, analysts and other capital market participants frequently use EPS and EPS changes in

determining firm performance and growth prospects. The specific changes in EPS should be

determined because many “non-operating change type” factors influence changes in EPS such

as, non-payment of dividends, buying back ordinary shares, increasing debt level, and

acquisitions and divestitures of companies with different price-to-earnings ratios and/or different

capital structures.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 11

9.7.5 Sustainable Growth

Organisational growth is normally a strategic objective yet a firm must be able to fund its growth.

Future expansion requires the generation of funds sufficient to maintain the current or required

capital structure. The sustainable growth concept is used by businesses to manage the financial

performance of their organisation so that the longer-term growth requirements can be achieved.

The level of growth depends on such factors as market size, demand, and ability to deliver the

quantity of products/services necessary to achieve the desired growth rate.

Sustainable growth is measured by the relationship between retained income and opening

funding, as follows:

Retained income Sustainable growth % =

Opening equity x (1 - dividend payout ratio)

3

where dividend payout ratio is

Cash dividends Divided payout ratio =

Net profit

The sustainable growth rate highlights the level of growth capable of being funded from retained

income and existing debt. The measure helps management plan future expansion by highlighting

the fact that while growth opportunities are unlimited, the resources to fund growth are not.

Using the data from the previous example, we can calculate the sustainable growth rate for Ling

Industrial Limited for 2008 and 2009.

Sustainable growth = retained income/opening equity as follows:

2008 2009

$ $

Retained income (163,649) 37,367

Opening equity 2,518,625 2,354,976

=( 6.50%) = 1.58%

A negative ratio cannot be compared with a positive ratio value. The measure must be compared

to sales growth projections, after taking into account changes in the operating structure of the

business. Examples of changes in operating structure could be changes in the debt to equity

structure; changes in gross profit percentage; purchases or sales of fixed assets, etc.

3 When the entity pays no cash dividends for the period this calculation reduces to:

Retained income Sustainable growth % =

Opening equity

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 12

9.8 Financial and Operating Ratios

9.8.1 Financial Ratios

i) Liquidity Ratios – Short Term

The current ratio and quick ratio are used to assess liquidity and the formulae should be familiar.

The current ratio is calculated by dividing current assets by current liabilities. The quick ratio is

calculated by dividing current assets (except for inventory) by current liabilities. As they become

larger, these ratios indicate better liquidity but it is important to analyse trends, industry

comparisons and the mix of current assets. Consider the following simple example.

2009 2008 Trend

$ $ $

Inventory 5,800,000 1,000,000

Cash 100,000 1,000,000

Bank accepted bills 100,000 1,000,000

Total current assets 6,000,000 3,000,000

Current liabilities 3,000,000 3,000,000

Current ratio 2.00 1.00 Improving

Quick ratio 0.06 0.67 Worsening

The working capital turnover ratio is calculated by dividing sales by working capital. Working

capital is defined as total current assets less total current liabilities. Year-end, beginning-of-the-

year or average-for-the-year working capital numbers can be used. This ratio provides a number

that indicates the length of the firm’s operating cycle, i.e. the time from purchase of inventory to

receipt of cash from sale of that inventory. This can also be calculated by dividing 365 (days) by

the working capital turnover ratio. Consider the following example: Chang Ltd has the following

information for the past four years:

Year 2009 2008 2007 2006

Sales ($000) 3,500 2,800 1,950 1,500

Current assets ($000) 500 490 400 320

Current liabilities ($000) 200 200 190 150

Working capital (average working capital)

11.9 (3,500/295

4)

11.2 (2,800/250)

10.3 (1,950/190)

Working capital (ending working capital)

11.7 (3,500/300)

9.7 (2,800/290)

9.3 (1,950/210)

8.8 (1,500/170)

Days working capital turned over (ending working capital ratio)

31.1 days (365/11.7)

37.6 days (365/9.7)

39.3 days (365/9.3)

41.4 days (365/8.8)

4 (Opening balance + closing balance)/2 = (290+300)/2 = 295

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 13

The trend in these ratios is favourable, indicating that working capital is turning over more quickly

each year. The usual reason would be that sales are increasing at a faster rate than the

inventory, but other factors can increase this ratio. For instance, increases in creditors (ceteris

paribus) lower the denominator, increasing the working capital ratio and reducing the days

working capital turned over, yet this may also indicate liquidity problems for the firm (paying

creditors late).

ii) Liquidity Ratios – Long Term

The debt to total funds ratio total debt divided by total funds (total debt plus total equity). The

debt to equity ratio is calculated as total debt divided by total equity. Both ratios provide an

indication of the financial viability of an organisation, the lower the ratio, the better the financial

viability. Changes occur to the ratio when the financial structure of the entity is altered.

The long-term debt to equity ratio indicates the solvency for the long term. Future expectations

about a downturn in the economy, for example, might suggest that firms with high numbers for

this ratio will suffer solvency problems and/or incur higher interest rates.

The interest coverage ratio is calculated by dividing (net profit before income tax plus interest

expense) by interest expense. This ratio is called interest coverage because the resulting

number shows how many times the interest expense for a period is covered by the profit before

interest and tax. Higher coverage numbers are better. The number can change due to changes

in the debt structure and poor sales, increasing operating expenses, or both.

Non-current Assets to Equity:

A high level for this ratio might indicate that investment in non-current assets is too great. It

should be compared with industry averages or with a number of competitors. A lower ratio

suggests that some working capital is funded by equity, which is expected because a firm cannot

operate with non-current assets alone.

9.8.2 Operating Ratios

Net profit to net sales indicates the amount of net profit that one dollar of sales generates.

Gross profit to net sales indicates the ability of the organisation to cover other operating and

non-operating expenses. Factors affecting both these ratios include increased competition,

changes to sales revenue due to quantity and/or price changes.

9.8.3 Financial and Operating Ratio Relationships

Sales to accounts receivable is also called the debtors or accounts receivable turnover ratio

because it indicates the number of times that the amount of money equal to current debtors has

been received during the period. Low ratios can be due to inadequate credit collection policies

and procedures, bad debt write-offs, or credit terms for poor-paying customers. It is also possible

to calculate the average number of days that debtors have been outstanding by dividing 365

(days) by the accounts receivable turnover ratio. The ratios should be compared with prior

periods and industry averages. Industry averages are important because the nature of the

business will affect this ratio.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 14

9.8.4 Stock (Inventory) Ratios

The stock turnover ratio is calculated as cost of goods sold divided by average stock. The ratio

should be as high as possible. Possible reasons for changes include having too much or too little

stock in anticipation of a price rise or fall respectively.

The cost of sales to sales ratio indicates the number of dollars of cost of goods sold to each

dollar of sales revenue for the period. The lower the ratio the better. It can also be expressed as

days inventory held by dividing 365 days by the stock turnover ratio. A lowering trend is desirable.

Increasing days inventory held numbers usually indicates stock is becoming obsolete and is

becoming more difficult to sell. Take the following example.

XZY Ltd has the following information for the past six years:

2009 2008 2007 2006 2005 2004

Sales ($000’s) 7,800 7,900 8,000 5,000 2,500 1,000

Cost of sales ($000’s) 3,900 5,100 5,000 3,200 1,700 600

Average stock ($000’s) 1,600 2,100 2,000 1,200 600 150

Stock turnover (times)

Days Inventory held

2.4 (3,900/

1,600)

1525

2.4 (5,100/

2,100)

152

2.5 (5,000/

2,000)

146

2.7 (3,200/

1,200)

135

2.8 (1,700/

600)

130

4.0 (600/

150)

91

Both the declining turnover ratio and the days’ inventory held indicate that inventory is moving

more slowly. Further investigation would be needed to identify the specific cause. Additionally,

there may be other inter-related effects of lower inventory turnover. For example, there may be an

adverse effect on profitability.

5 = 365/2.4

To calculate the percentages in the table above we divide each number by the total sales for the company. E.g. the

gross profit percentage for Company C is: $200,000 / $800,000 x 100 = 25%.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 15

9.8.5 Trends

Analysing ratios over time can give valuable insights into a firm’s performance. Common size

analysis can be used to compare or benchmark financial performance against other firms within

the same industry; and to get a different picture about trends for one firm. Using this approach

each line item in the Profit and Loss Account (or Balance Sheet) is expressed as a percentage of

sales (or total assets).

Consider the following Profit and Loss Accounts and common size Profit and Loss Accounts for

three firms in the electronics industry6.

Company A Company B Company C

$(000’s) % $(000’s) % $(000’s) %

Sales 900.0 100.0% 600.0 100.00% 800.0 100.0%

Cost of sales 579.6 64.4% 319.8 53.3% 600.0 75.0%

Gross profit 320.4 35.6% 280.2 46.7% 200.0 25.0%

R & D 53.1 5.9% 48.0 8.0% 15.2 1.9%

Sales & admin. 162.0 18.0% 114.0 19.0% 79.2 9.9%

Other expenses 1.8 0.2% 9.6 1.6% 7.2 0.9%

Total expenses 216.9 24.1% 171.6 28.6% 101.6 12.7%

Profit before tax 103.5 11.5% 108.6 18.1% 98.4 12.3%

Income tax 16.5 1.8% 17.4 2.9% 15.7 2.0%

Net profit 87.0 9.7% 91.2 15.2% 82.7 10.3%

Company B has the highest gross and net profit percentages of the three companies indicating

better profitability. To see if these percentages are due to better efficiency, better strategy, some

other reason or a combination of these, further investigation is necessary. To establish a starting

point to answer these questions more fully, we could review the notes in the published financial

reports. Often, such reports can be obtained from the Internet in spreadsheet format so that

analyses can be carried out easily.

6 To calculate the percentages in the table we divide each number by the total sales for the company. E.g. the gross

profit percentage for Company C is: $200,000 / $800,000 x 100 = 25%.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 16

Common size analysis can also be used for within-company comparisons as shown in the table

below:

Zhou Company Inc

2007 2008 2009

Amount ($000’s)

% Amount ($000’s)

% Amount ($000’s)

%

Cash 45 0.88%7 115 1.94% 310 4.08%

Debtors 1,515 29.65% 1,700 28.66% 2,315 30.49%

Stock 1,655 32.38% 1,819 30.67% 2,267 29.85%

Other 145 2.84% 138 2.33% 141 1.86%

Total current assets 3,360 65.75% 3,772 63.60% 5,033 66.28%

Plant and equipment 1,600 31.31% 2,000 33.72% 2,400 31.60%

Other 150 2.94% 159 2.68% 161 2.12%

Total non-current assets 1,750 34.25% 2,159 36.40% 2,561 33.72%

Total assets 5,110 100.00% 5,931 100.00% 7,594 100.00%

Creditors 750 14.68% 1,265 21.33% 1,505 19.82%

Short-term loan 500 9.79% 420 7.08% 420 5.53%

Other 200 3.91% 210 3.54% 215 2.83%

Total current liabilities 1,450 28.38% 1,895 31.95% 2,140 28.18%

Long-term loan 1,000 19.57% 1,100 18.55% 1,300 17.12%

Total non-current liabilities 1,000 19.57% 1,100 18.55% 1,300 17.12%

Paid up capital 2,360 46.18% 2,560 43.16% 3,693 48.63%

Retained profits 300 5.87% 376 6.34% 461 6.07%

Total equity 2,660 52.05% 2,936 49.50% 4,154 54.70%

Total liabilities & equity 5,110 100.00% 5,931 100.00% 7,594 100.00%

The best way to start this analysis is to look at the trends in the subtotals and the totals. For

example, we see that non-current assets percentages have decreased from 2008 to 2009 and we

see that current assets percentages have increased. We would then look to the individual

accounts to determine the main reasons for this pattern. Cash has increased over the three-year

period, and debtors fell for the first year and then increased. A decline in accounts receivable

may be good news unless it has been caused by writing off bad debts or a decline in current-

period sales or some combination of these.

Stock also decreased slightly relative to total assets - good news as stock earns no return sitting

in a warehouse, yet some stock levels need to be maintained in order to satisfy customer

demand (unless the firm uses a JIT system and are very confident that our suppliers can deliver -

but this is not always the case, especially in Hong Kong). Other current assets have remained

relatively stable over the three-year period, while investment in non-current assets has decreased

relative to total assets from 2008 to 2009. This may be due to accounting or to real economic

reasons or both. Further investigation is required.

7 To calculate the common size balance sheet numbers we just divide each number by total assets. So, for example,

the percentage for plant and equipment for 2008 is 33.72% (2,000/5,931 × 100 = 33.72%).

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 17

The mix of how the assets are funded can be seen in the total liabilities and equity section. Total

debt (short and long-term debt) has fallen as a percentage of total assets, with some of this being

taken up by paid up capital. This means less of a future cash burden on the company because

paid up capital represents funding which does not attract a requirement to pay a regular cash

payment. This is because dividends are paid at the discretion of the directors. Debt, on the other

hand means the company must pay interest (and principal) each period regardless of how the

company is performing. Zhou Company also seems to be making much better use of its

accounts payable funding. Accounts payable is (usually), interest free so the longer the payment

can be deferred the better. However, relationships with suppliers are very important and they

must be nurtured and maintained at a good level so the company can carry out its operations and

satisfy its own customers. A balance needs to be achieved.

Index Analysis

We can also perform an index analysis when looking at trends. Index analysis expresses the

amounts of a particular profit and loss or balance sheet item as a percentage of the amounts of

that same item in the base year. The base year is selected by the analyst as the starting point for

the trend analysis. With index analysis we see how an item has changed over time relative to

itself. For example it may be seen from the index analysis below, that the cash balance in 2009

is 6.89 times the balance of cash in 2007 i.e. 310 / 45.

Index Analysis

2007 2008 2009

Amount (HK$000)

Index Amount (HK$000)

Index Amount (HK$000)

Index

Cash 45 1.00 115 2.56 310 6.89

Debtors 1,515 1.00 1,700 1.12 2,315 1.53

Stock 1,655 1.00 1,819 1.10 2,267 1.37

Other 145 1.00 138 0.95 141 0.97

Total current assets 3,360 1.00 3,772 1.12 5,033 1.50

Plant & equipment 1,600 1.00 2,000 1.25 2,400 1.50

Other 150 1.00 159 1.06 161 1.07

Total non-current assets 1,750 1.00 2,159 1.23 2,561 1.46

Total assets 5,110 1.00 5,931 1.16 7,594 1.49

Creditors 750 1.00 1,265 1.69 1,505 2.01

Short-term loan 500 1.00 420 0.84 420 0.84

Other 200 1.00 210 1.05 215 1.08

Total current liabilities 1,450 1.00 1,895 1.31 2,140 1.48

Long-term loan 1,000 1.00 1,100 1.10 1,300 1.30

Total non-current liabilities 1,000 1.00 1,100 1.10 1,300 1.30

Paid up capital 2,360 1.00 2,560 1.08 3,693 1.56

Retained profits 300 1.00 376 1.25 461 1.54

Total equity 2,660 1.00 2,936 1.10 4,154 1.56

Total liabilities & equity 5,110 1.00 5931 1.16 7,594 1.49

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 18

While the cash balance has increased significantly relative to itself over the three-year period, its

amount is not material when compared with total current assets. Of more interest are the index

changes for debtors and for stock. Based on the common size analysis percentages in the

previous table, the trends in these accounts did not appear to stand out (both remained at around

30% of total assets). The 2009 balance for debtors is about 1.5 times the balance in 2007 and

for stock it is about 1.4 times. Further analysis of debtors could include inspection of an aged trial

balance (if possible), to determine if the build up is due to an increase in cash collection times or

changes in credit sales over the period. The stock change is consistent with sales growth

explaining the change because stock would be expected to increase if sales and accounts

receivable are also increasing, yet other factors need to be considered. The increase in plant and

equipment seems to have been funded mainly from the increase in retained profits and paid up

capital (total equity).

Common size and index analysis complement one another yet the presentation of the information

in different ways makes certain relationships easier to see.

9.9 Non-financial Measures

9.9.1 Common Non-financial Measures

It is now commonly recognised that a balanced scorecard (BSC) should be used to measure

performance. The BSC requires the use of both financial and non-financial measures. Common

non-financial measures include:

• customer satisfaction;

• percentage of on-time deliveries;

• delivery response time;

• internal efficiency;

• cycle time;

• good output per employee;

• sales per employee;

• creativity;

• time for product to reach market from initial idea;

• time between new product and a competitor’s new product; and

• percentage of new products reaching the market before competitors’ products.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 19

Organisation’s Vision and Strategy

Learning and Growth Perspective

Employee Training Employee Satisfaction Strategic Investment Decisions

Internal Business Perspective

Production Flexibility % of Sales for New Products Product Quality After Sales Service

Financial Perspective

Return on Investment Operating Income Return on Equity Cash flow

Customer Perspective

Customer Satisfaction Surveys

Customer Retention Market Share New Customer Acquisition

9.10 The Balanced Scorecard

9.10.1 Description

“The BSC provides an organisation with a comprehensive framework that translates the

organisation's vision and strategy into a coherent set of performance measures” (Kaplan and

Norton, 1996a, p.24). Kaplan and Norton (1992) brought the BSC into prominence and it has

evolved from a performance measurement system to a core management system that is now

widely used across many sectors, including service, government, not for profit and for profit. The

performance measures in the BSC are organised under four perspectives: financial, customer,

internal business processes and learning and growth. Each perspective has a short term goal

with one or more critical success factors identified with that goal. The general BSC model is

illustrated in Figure One.

Figure 1: The Balanced Scorecard (Examples of Measures) Adapted from Kaplan and Norton (1992).

9.10.2 Benefits of the Balanced Scorecard

The balanced scorecard approach can lead to consensus on organisational priorities, clear

specification of goals, rigorous planning and improvement processes, alignment of strategic goals

with shorter term actions, clearer communication, team working and knowledge sharing and

clearer accountability for results.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 20

9.10.3 Potential Problems

Although the method may assist in highlighting organisational issues, it cannot always resolve

them easily. For example, some measures in the scorecard will conflict and difficult choices must

be made to resolve these issues (e.g. R & D investment versus short term profitability);

organisational culture may over-emphasise some measures and ignore others (e.g. an

organisation with a strong sales culture may ignore underlying profitability). Top management

commitment to the balanced scorecard approach is necessary for it to succeed. The BSC leads

to a better basis for managers’ performance bonuses. However, all performance measures are

open to manipulation by managers.

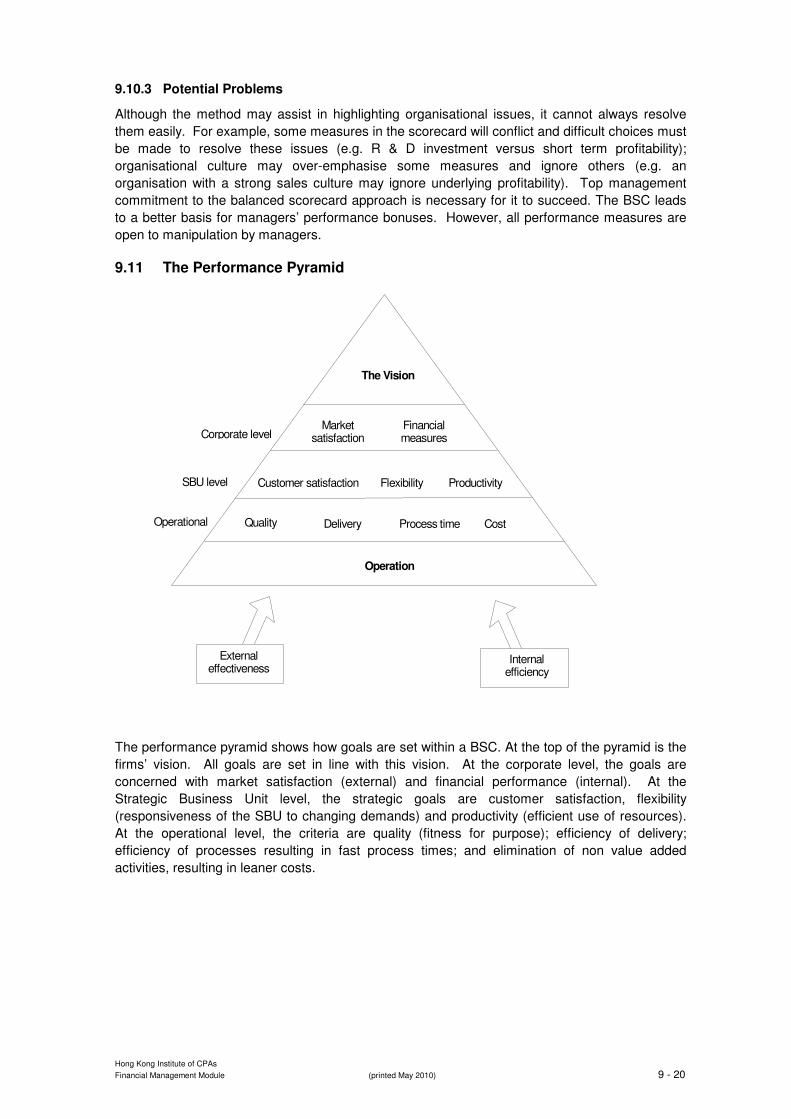

9.11 The Performance Pyramid

The performance pyramid shows how goals are set within a BSC. At the top of the pyramid is the

firms’ vision. All goals are set in line with this vision. At the corporate level, the goals are

concerned with market satisfaction (external) and financial performance (internal). At the

Strategic Business Unit level, the strategic goals are customer satisfaction, flexibility

(responsiveness of the SBU to changing demands) and productivity (efficient use of resources).

At the operational level, the criteria are quality (fitness for purpose); efficiency of delivery;

efficiency of processes resulting in fast process times; and elimination of non value added

activities, resulting in leaner costs.

Market satisfaction

Financial measures

Customer satisfaction Flexibility Productivity

Quality Delivery Process time Cost

The Vision

Operation

External effectiveness

Internal efficiency

Corporate level

SBU level

Operational

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 21

9.12 Reporting and Evaluating Sustainability

Many firms are recognising the benefits of operating in a sustainable manner. These benefits

include; keeping the environment clean, treating people with respect and operating profitably.

Firms that implement a BSC can extend this to monitor and measure their sustainability efforts

and link corporate sustainability objectives with appropriate corporate actions and performance

outcomes. When appropriate strategic measures are included in a firm’s BSC, sustainability can

be improved. For example toxic emissions are a lag measure of a firm’s process efficiency and

also a lead indicator of future environmental costs.

When choosing sustainability measures consideration should be given to ensuring the measures

are:

• quantifiable, either in absolute or percentage terms

• complete, in that the measure sums up in one number multiple measures of

performance e.g. profit is a summary measure of revenue generation and cost

control.

• Controllable, in that employees can influence improvement

Some firms choose to integrate sustainability measures into the existing perspective of the BSC.

Sustainability is typically included in the Internal business process perspective, however research

shows that sustainability measures can be incorporated into any of the four perspectives of the

BSC. Incorporation into an existing BSC can help to show the interrelationships between the

measures and other areas of the firm to fulfil corporate strategy. Other firms add a fifth

perspective to the BSC. By including social and environmental performance indicators that link

the other four perspectives the importance of social and environmental responsibilities is

highlighted as a corporate objective.

Benefits of firms including sustainability measures into a BSC include:

• Increased employee satisfaction

• Lower operational and administrative costs

• Improved productivity

• Enhanced image and reputation

• Increased market opportunities

• Improved shareholder relationships

• Share market premiums

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 22

9.13 Agency Theory and Managerial Incentive Schemes

An agency relationship exists whenever one party (the principal) hires another party (the agent) to

perform some service, and this service requires the principal to delegate some decision making

authority to the agent. Two types of principal-agent relationships arise in connection with

managerial incentive schemes. First, the organization’s owners or shareholders, acting as the

principal (usually through the board of directors), hire the chief executive group to be their agents

in managing the firm in their best interests. In the second principal - agent relationship, the firm’s

chief executive group acts as the principal and hires division managers as agents to manage sub-

units of the organization.

Agency theory assumes that all individuals - principals and agents - care not only about financial

compensation but also about such properties as attractive working conditions and flexibility in

hours worked. Managers are assumed to prefer leisure to hard or routine work, although for

some top management an aversion to work may not be a realistic assumption. Nevertheless, the

argument goes that agents require incentives to minimize the net costs of the divergence of

interests between them and the principal. Among other things, the agency model argues that if

top executives of the company are compensated only by straight salary, they may not be

motivated to take actions that increase the value of the firm to the shareholders. They may over-

consume in such areas as leisure, attractive working conditions, and company perquisites, or will

not spend enough time and effort to increase shareholder wealth.

If the firm’s owners knew what actions were optimal for the firm and could observe without cost

the actions of the top managers, they could direct the managers to implement these optimal

actions, with the threat of withholding compensation or dismissal if these actions were not carried

out. However, a dispersed group of owners will probably have inadequate information and will

find monitoring costly. Accordingly, the owners are unlikely either to know what the optimal

actions should be or to be able to direct and monitor the actions of the top executives. Therefore,

to encourage managers to take actions that are in the firm’s best interests, the owners may

introduce incentive compensation plans that enable the managers to share in the firm’s increased

wealth. These schemes can take a variety of forms, including merit raises, bonuses based on

reported performance, and various types of share ownership plans.

Executive incentive compensation bonus plans are designed to create a commonality of interest

between the owners (principal) and the executives (agents). However, some divergence of

interest will always exist between the principal and the agents. This is due to differences in risk

attitudes, the existence of private information (managers always know more about the firm than

shareholders), and limited or costly observability. The principal will usually attempt to limit this

divergence by establishing appropriate incentives for the agents, and by incurring monitoring

costs designed to limit actions that increase the agents’ welfare at the expense of the principal.

Annual audited financial statements are an excellent example of costly monitoring of managerial

behaviour.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 23

Part D

Practice Question 1 [30 Marks]

Financial information for Chang Inc is provided below for 2009 and 2010:

Chang Inc Corporation

Income Statement and Statement of Retained Earnings

For the Year Ended June 30, 2010

(in thousands)

Revenue:

Net sales $480,000

Other 36,000

Total revenue 516,000

Expenses:

Cost of goods sold 324,000

Selling and administrative 93,000

Depreciation 15,000

Interest 12,000

Total expenses 444,000

Income before income taxes 72,000

Income taxes (assumed 15%) 10,800

Net income 61,200

Less: Dividends 15,300

Net income added to retained earnings 45,900

Retained earnings, 1/7/2008 68,400

Retained earnings, 30/06/2009 $114,300

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 24

Chang Inc

Comparative Balance Sheets June 30, 2010 and 2009 ($ thousands)

Assets 2010 2009

Current assets:

Cash and marketable securities $28,700 $12,600

Net Receivables $28,800 $30,000

Inventories $39,000 $37,200

Other current assets $3,000 $1,800

Total current assets $99,500 $81,600

Investments $79,600 $68,400

Property, plant, and equipment:

Land $7,200 $7,200

Buildings and equipment $160,800 $148,800

Total property, plant, and equipment. $168,000 $156,000

Total assets $347,100 $306,000

Liabilities and Shareholders' Equity 2010 2009

Current liabilities:

Bank Overdraft $13,200 $14,400

Accounts payable $43,200 $42,600

Salaries payable $15,600 $16,200

Total current liabilities $72,000 $73,200

Long-term debt. $96,000 $102,600

Total liabilities $168,000 $175,800

Shareholders' equity:

Share capital $64,800 $61,800

Retained earnings $114,300 $68,400

Total shareholders' equity $179,100 $130,200

Total liabilities and shareholders' equity $347,100 $306,000

The following industry ratios apply:

1. Net profit as a percentage of sales 10% 2. Return on assets 15% 3. Return on equity 22% 4. Current ratio 1.7 5. Quick ratio .75 6. Debt-equity ratio 1.35 7. Interest coverage 6.75 8. Dividend payout ratio 35%

Required

a) Calculate the ratios listed below for Chang Inc for 2010:

1. Net profit as a percentage of sales.

2. Return on assets.

3. Return on equity.

4. Current ratio.

5. Quick ratio.

6. Debt-equity ratio.

7. Interest coverage.

8. Dividend payout ratio.

b) Analyse Chang Inc’s performance using two years of data where appropriate and the industry ratios provided.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 25

Suggested Solution

Practice Question 1 [30 Marks]

Timing (minutes) Part a) 30 minutes

b) 15 minutes

Total time spent on this question 45 minutes

a) The financial ratios are calculated as follows:

net profit 1. Net profit as a percentage of sales =

net sales

$61,200 =

$480,000 = 12.75%

net income before interest (net of taxes) 2. Return on assets =

average total assets

$61,200 + ($12,000 x .85) =

(347,100 + $306,000)/2 = 22% (rounded)

Operating Profit 3. Return on equity =

Equity

$61,200 =

($179,100 + $130,200)/2 = 40% rounded

current assets 4. (i) Current ratio (2010) =

current liabilities

$99,500 =

$72,000 = 1.38

current assets 4. (ii) Current ratio (2009) =

current liabilities

$81,600 =

$73,200 = 1.11

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 26

quick assets 5. (i) Quick ratio (2010) =

current liabilities

= $28,700 + $28,800

72,000

= 0.80 (rounded)

quick assets 5. (ii) Quick ratio (2009) =

current liabilities = $12,600 + $30,000

73,200

= 0.58 (rounded)

total liabilities* 6. (i) Debt/equity ratio 2010 =

total shareholders equity

$168,000 =

$179,100

= 0.94

total liabilities* 6. (ii) Debt/equity ratio 2009 =

total shareholders equity

$175,800 =

$130,200

= 1.35

operating income 7. Interest coverage =

interest expense

($72,000 + $12,000)* =

$12,000

= 7 times

*Income before taxes + Interest expense

cash dividends

8. Dividend payout ratio = net profit

= 15,300/61,200

= 25%

* Some literature uses total interest-bearing debt for these ratios. In that case, both

accounts payable and salaries payable would be excluded.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 27

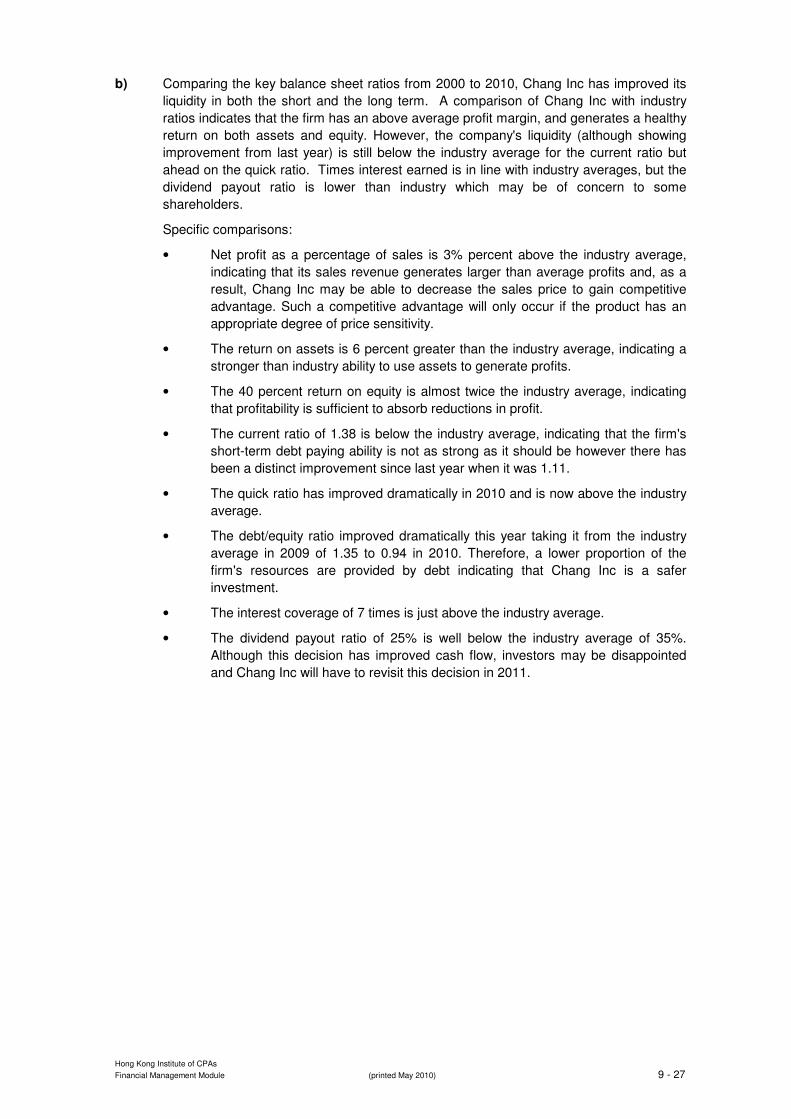

b) Comparing the key balance sheet ratios from 2000 to 2010, Chang Inc has improved its

liquidity in both the short and the long term. A comparison of Chang Inc with industry

ratios indicates that the firm has an above average profit margin, and generates a healthy

return on both assets and equity. However, the company's liquidity (although showing

improvement from last year) is still below the industry average for the current ratio but

ahead on the quick ratio. Times interest earned is in line with industry averages, but the

dividend payout ratio is lower than industry which may be of concern to some

shareholders.

Specific comparisons:

• Net profit as a percentage of sales is 3% percent above the industry average,

indicating that its sales revenue generates larger than average profits and, as a

result, Chang Inc may be able to decrease the sales price to gain competitive

advantage. Such a competitive advantage will only occur if the product has an

appropriate degree of price sensitivity.

• The return on assets is 6 percent greater than the industry average, indicating a

stronger than industry ability to use assets to generate profits.

• The 40 percent return on equity is almost twice the industry average, indicating

that profitability is sufficient to absorb reductions in profit.

• The current ratio of 1.38 is below the industry average, indicating that the firm's

short-term debt paying ability is not as strong as it should be however there has

been a distinct improvement since last year when it was 1.11.

• The quick ratio has improved dramatically in 2010 and is now above the industry

average.

• The debt/equity ratio improved dramatically this year taking it from the industry

average in 2009 of 1.35 to 0.94 in 2010. Therefore, a lower proportion of the

firm's resources are provided by debt indicating that Chang Inc is a safer

investment.

• The interest coverage of 7 times is just above the industry average.

• The dividend payout ratio of 25% is well below the industry average of 35%.

Although this decision has improved cash flow, investors may be disappointed

and Chang Inc will have to revisit this decision in 2011.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 28

Practice Question 2 [20 Marks]

Condensed financial data of Wong Manufacturing appear below:

WONG MANUFACTURING

Comparative Balance Sheets 30 June

2010 2009 (000s) (000s)

Cash $144,000 $70,000

Accounts receivable $170,000 $106,000

Inventories $240,000 $264,000

Prepaid expenses $38,000 $50,000

Investments $180,000 $150,000

Plant assets $620,000 $500,000

Accumulated depreciation ($130,000) ($120,000)

Total $1,262,000 $1,020,000

Liabilities and Shareholders' Equity

Accounts payable $186,000 $150,000

Accrued expenses payable $58,000 $48,000

Notes payable $260,000 $320,000

Ordinary shares $490,000 $340,000

Retained earnings $268,000 $162,000

Total $1,262,000 $1,020,000

WONG MANUFACTURING

Income Statement

for the year ended 30 June 2010 ($ 000s)

Sales $960,000

Less:

Cost of goods sold $580,000

Operating expenses (excluding depreciation) $120,000

Depreciation expense $34,000

Income taxes $30,000

Interest expense $36,000

Loss on sale of plant assets $6,000 806,000

Net income $154,000

Additional information:

1. New plant assets costing $170,000,000 were purchased for cash in 2010.

2. Old plant assets costing $50,000,000 were sold for $20,000,000 cash when book value

was $26,000,000.

3. Notes with a face value of $60,000,000 were converted into $60,000,000 of ordinary

shares.

4. A cash dividend of $48,000,000 was declared and paid during the year.

5. Accounts payable pertain to merchandise purchases.

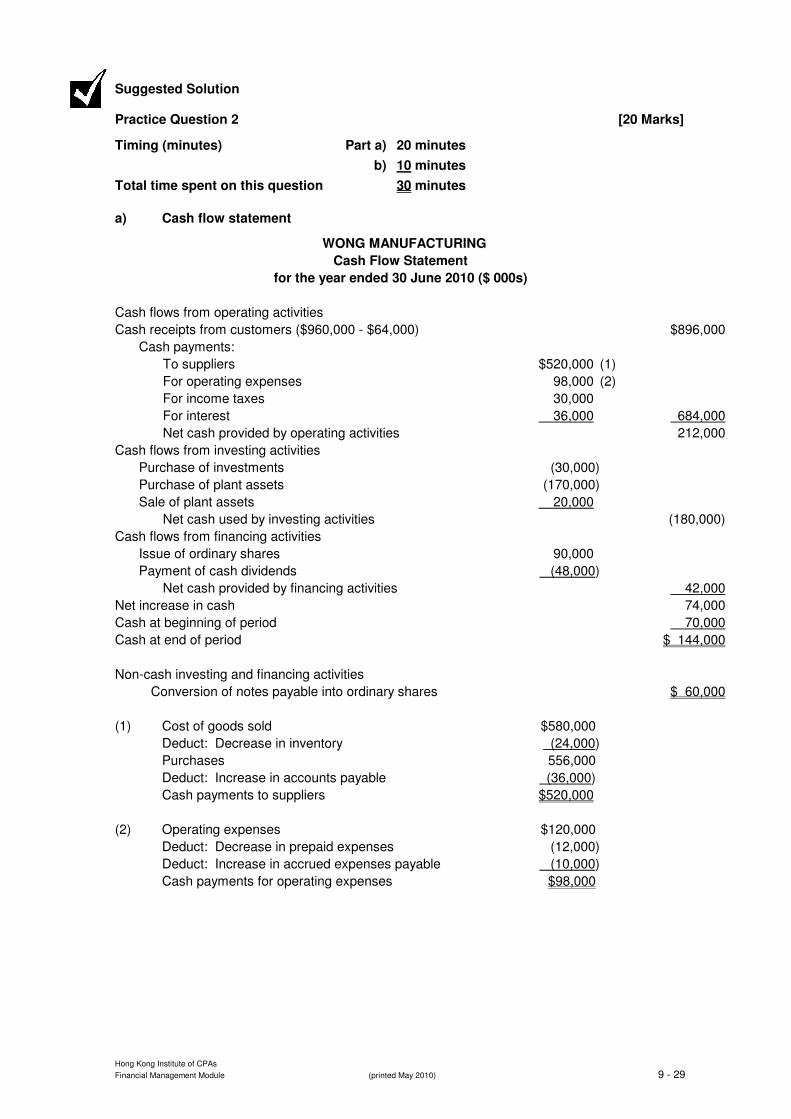

Required

a) Prepare a cash flow statement for the year ended 30 June 2010.

b) Reconcile operating profit to net cash from operating activities.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 29

Suggested Solution

Practice Question 2 [20 Marks]

Timing (minutes) Part a) 20 minutes

b) 10 minutes

Total time spent on this question 30 minutes

a) Cash flow statement

WONG MANUFACTURING

Cash Flow Statement

for the year ended 30 June 2010 ($ 000s)

Cash flows from operating activities

Cash receipts from customers ($960,000 - $64,000) $896,000

Cash payments:

To suppliers $520,000 (1)

For operating expenses 98,000 (2)

For income taxes 30,000

For interest 36,000 684,000

Net cash provided by operating activities 212,000

Cash flows from investing activities

Purchase of investments (30,000)

Purchase of plant assets (170,000)

Sale of plant assets 20,000

Net cash used by investing activities (180,000)

Cash flows from financing activities

Issue of ordinary shares 90,000

Payment of cash dividends (48,000)

Net cash provided by financing activities 42,000

Net increase in cash 74,000

Cash at beginning of period 70,000

Cash at end of period $ 144,000

Non-cash investing and financing activities

Conversion of notes payable into ordinary shares $ 60,000

(1) Cost of goods sold $580,000

Deduct: Decrease in inventory (24,000)

Purchases 556,000

Deduct: Increase in accounts payable (36,000)

Cash payments to suppliers $520,000

(2) Operating expenses $120,000

Deduct: Decrease in prepaid expenses (12,000)

Deduct: Increase in accrued expenses payable (10,000)

Cash payments for operating expenses $98,000

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 30

b) Reconciliation of net profit after tax with cash flows from operating activities

NOPAT $154,000

Non-cash items:

Depreciation $34,000

Loss on sale $6,000

Deferrals & Accruals:

Increase in accounts receivable (64,000)

Decrease in Inventory 24,000

Decrease in Prepaid expenses 12,000

Increase in Accounts Payable 36,000

Increase in Accrued expenses 10,000

Net cash from operating activities 212,000

Practice Question 3 [15 Marks]

The Balanced Scorecard (BSC) encourages firms to develop performance measures along four

perspectives. These are introduced above and are also discussed in detail in the readings.

Required:

a) Give a brief description of the four components of the balance scorecard.

b) Below is a list of performance measures for Ling Electronics Ltd. Produce a balanced

scorecard by placing these measures in the appropriate perspectives.

• Employee effectiveness

• Delivery time

• Number of new products

• Number of repairs under warranty

• Sales $

• Profit

• Throughput

• Return on Investment

• Sales to new customers

• Manufacturing cycle time

• Employee empowerment

• Customer satisfaction

• EVA™

• Employee turnover

• Number of new patents

• Customer retention

• Cost of scrap

• Lost sales

• Employee efficiency.

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 31

Suggested Solution

Practice Question 3 [15 Marks]

Timing (minutes) Part a) 7 minutes

b) 13 minutes

Total time spent on this question 20 minutes

a) The four components of the BSC include financial, customer, internal business process

and learning and growth. The financial perspective guides the firm on value creation for

stakeholders. The customer perspective ensures that the company understands how its

customers view the firm. In the internal business process perspective, the firm focuses

on improving efficiency across all aspects of the firms’ value chain. Finally the learning

and growth perspective focuses on three aspects: the efficiency and effectiveness of

employees; increasing information systems capabilities and product innovation.

b) Balanced Scorecard for Ling Electronics Limited.

Perspective Measures

Financial Sales $

Profit

Return on Investment

EVA™

Customer Lost sales

Sales to new customers

Customer retention

Customer satisfaction

Delivery time*

Number of repairs under warranty

Internal Business Process Throughput

Manufacturing cycle time

Cost of scrap

Learning and Growth Employee efficiency

Employee turnover

Employee empowerment

Employee effectiveness

Number of new patents

Number of new products

* Delivery time might also be classified as an Internal Business Process

Hong Kong Institute of CPAs

Financial Management Module (printed May 2010) 9 - 32

Part E

How do I know I have succeeded in this topic?

Can I:

Aft

er

wo

rkin

g th

rou

gh

th

is

Sectio

n

Aft

er

my W

ork

sh

op

Aft

er

talk

ing

to

my

Wo

rksh

op

Facili

tato

r

Aft

er

my e

xam

inatio

n

pre

para

tio

n

Sh

ou

ld I

do

mo

re r

esearc

h

Calculate financial, strategic and operational performance measures and understand the relationships between them.

Describe the role of cash flow analysis in the evaluation of the organisation’s strategic and operational plan.

Describe the interrelationships between shareholder wealth creation and performance measures aligned to that objective, including agency theory and its relationship to managerial incentive schemes.

Identify financial and non-financial measures of business profitability including cash flow measures.

Describe measures of entity growth.

List the main steps in translating strategies and plans into goals, recognising their interrelationships.

List the limitations of benchmarking in facilitating organisational change.

Describe the relationships between financial and operating ratios and be able to interpret trends over time and across time.

Explain the key components of the balanced scorecard.