Embed Size (px)

Citation preview

OPEN – C&HR – INFO 1-1OPEN – C&HR – INFO 1-1

UM Retirement PlanAnnual Valuation

Board of CuratorsJanuary 31, 2013

OPEN – C&HR – INFO 1-2

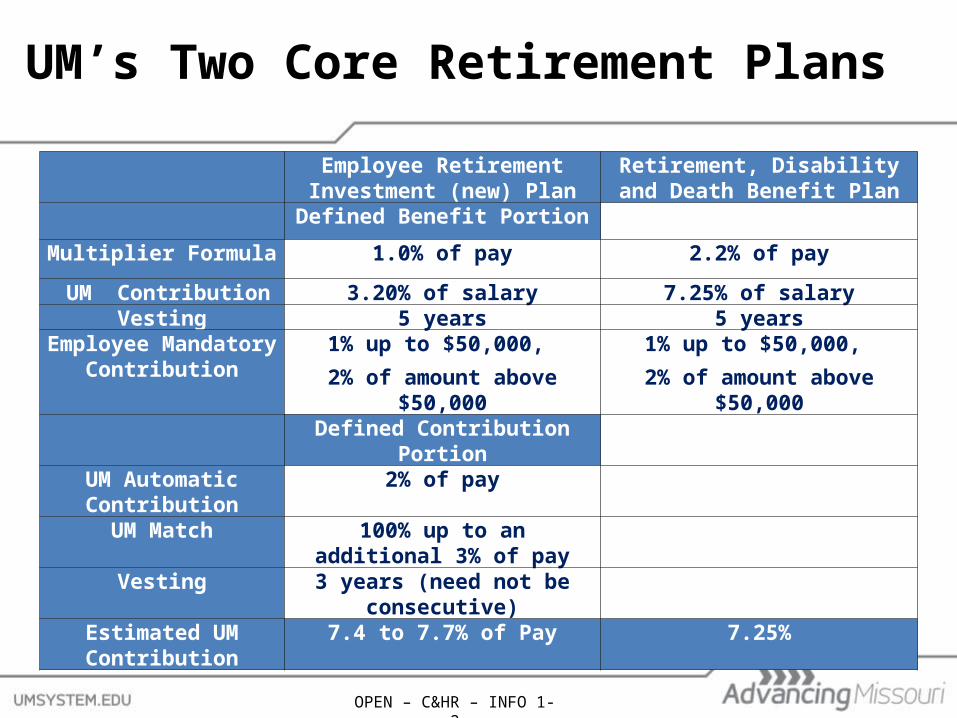

UM’s Two Core Retirement Plans

Employee Retirement Investment (new) Plan

Retirement, Disability and Death Benefit Plan

Defined Benefit Portion

Multiplier Formula 1.0% of pay 2.2% of pay

UM Contribution 3.20% of salary 7.25% of salaryVesting 5 years 5 years

Employee Mandatory Contribution

1% up to $50,000,

2% of amount above $50,000

1% up to $50,000,

2% of amount above $50,000Defined Contribution Portion

UM Automatic Contribution

2% of pay

UM Match 100% up to an additional 3% of pay

Vesting 3 years (need not be consecutive)

Estimated UM Contribution

7.4 to 7.7% of Pay 7.25%

OPEN – C&HR – INFO 1-3

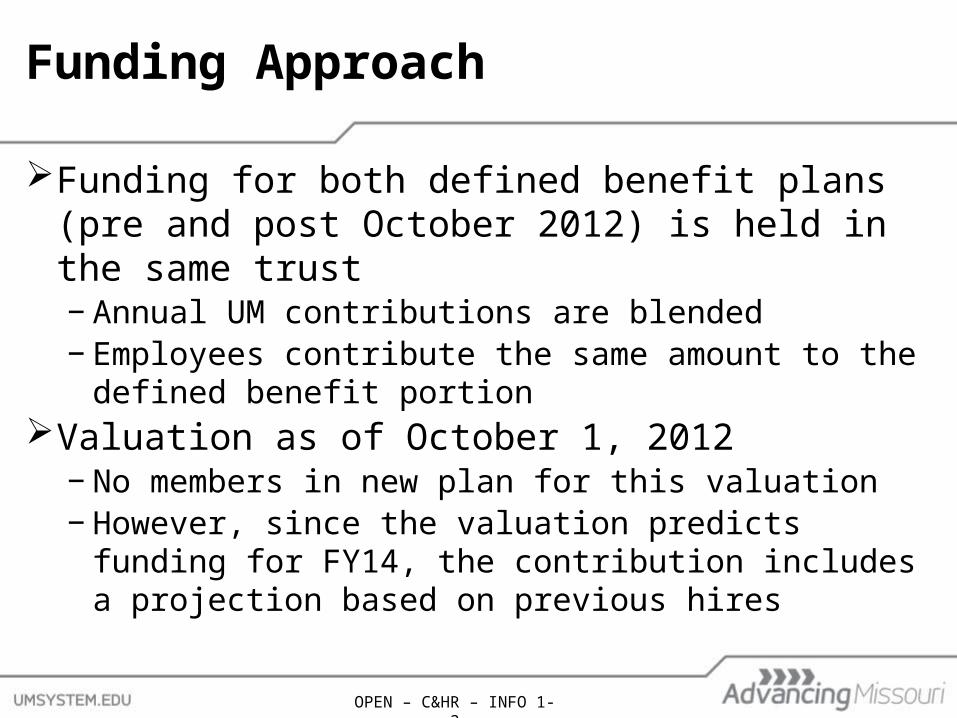

Funding Approach

Funding for both defined benefit plans (pre and post October 2012) is held in the same trust− Annual UM contributions are blended− Employees contribute the same amount to the

defined benefit portionValuation as of October 1, 2012

− No members in new plan for this valuation− However, since the valuation predicts funding for

FY14, the contribution includes a projection based on previous hires

OPEN – C&HR – INFO 1-4

Defined Benefit Annual Valuation Results

OPEN – C&HR – INFO 1-5

Annual Valuation Summary

Determine the annual contribution required to meet funding obligations

FY14 funding contribution is slightly less than originally predicted

Highest annual contribution in history of plan, due to extreme market downturn in 2008 and 2009

Note: Full report available on the UM benefits website

a

OPEN – C&HR – INFO 1-6

Actuarial Valuation Report

Howard Rog, Actuary, Segal Consultants

Annual valuation includes:− Present provisions of the plan− Characteristics of active, inactive and retired members− Actuarial assumptions and methods− Actuarial value of the Plan’s Trust assets

Determination of annual contribution

OPEN – C&HR – INFO 1-7

Characteristics of Active Members

Element 2011 2012

Academic and Administrative

Number 11,148 11,101

Average age 46.1 46.3

Average years of service 10.7 11.0

Average annual salary $71,541 $73,141

Clerical and Service

Number 7,279 7,098

Average age 44.5 44.8

Average years of service 9.9 10.1

Average annual salary $32,195 $32,986

OPEN – C&HR – INFO 1-8

Characteristics of Retired Members

Academic and Administrative

Clerical and Service

Number of retirees 4,103 2,621

Average age at retirement 63.5 62.3

Monthly benefits range from less than $100 to more than $5,000

48 retirees are age 95 or older

551 pensions began in 2012

OPEN – C&HR – INFO 1-9

Actuarial Valuation Report Assumptions

Assumptions (reviewed every 5 years): Investment ReturnActuarial Funding MethodAsset Valuation MethodSalary and Payroll Increases Retirement RatesMortality RatesWithdrawal RatesDisability RatesPresence and Age of Spouse

OPEN – C&HR – INFO 1-10

Development of Actuarial Value of Assets

Calculation of Unrecognized Return

Original Amount

Unrecognized Return

Year ended September 30, 2012 $141,201,927 $112,961,541

Year ended September 30, 2011 ($152,060,512) ($91,236,307)

Year ended September 30, 2010 $31,521,057 $12,608,423

Year ended September 30, 2009 ($183,169,581) ($36,633,916)

Year ended September 30, 2008 ($742,138,877) 0

Total Unrecognized Return ($2,300,259)

OPEN – C&HR – INFO 1-11

Changes Impacting Plan Contribution Requirements

Dollar Amounts

Percent of Payroll

Total cost as of October 1, 2011 $104,711,588 10.15%

Changes due to:

Change due to increased payroll $1,021,181 (0.04%)

Demographic changes ($188,141) (0.02%)

Loss/(gain) from actuarial experience and contributions

$20,529,665 1.96%

Total changes $21,362,705 1.90%

Total cost as of October 1, 2012 $126,074,293 12.05%

OPEN – C&HR – INFO 1-12

Determination of FY 14 DB Annual Contribution

Contribution Requirements % of Pay

Normal cost 6.75%

Total costs 11.62%

Employee contribution -1.27%Net employer DB contribution 10.35%

Note: Includes DB funding for both pre and post October 2012 members

OPEN – C&HR – INFO 1-13

Projected

UM Retirement Plans Contributions

% of Payroll Actual

OPEN – C&HR – INFO 1-14

Total Cost Projections for all Retirement Plans

(Defined Benefit and Defined Contribution)

OPEN – C&HR – INFO 1-15

FY14 Total Retirement Plan Costs

Contribution Requirements % of Pay

Total Defined Benefit (DB) costs 11.62%

Employee Contribution to DB -1.27%

Net Employer Contribution to DB 10.35%

Projected Employer Contribution to DC .47%

Total Employer Contribution to Plans* 10.82%*Estimated FY14 Employer Contribution = $119.2 million

OPEN – C&HR – INFO 1-16

Projected Use of Stabilization Fund

FY12 FY13 FY14 FY15 FY16 FY17

Gross Required Contribution 8.39% 10.16% 12.09% 12.30% 12.08% 11.96%

Projected Employee Contribution -1.23% -1.26% -1.27% -1.28% -1.29% -1.30%

Net Required Employer Contribution 7.16% 8.90% 10.82% 11.02% 10.79% 10.66%

Flat Rate – Retirement % 7.25% 8.25% 9.00% 9.75% 10.50% 11.25%

Excess (deficiency) of Flat Rate to Net Required Employer Contribution

0.09% -0.65% -1.82% -1.27% -.29% .59%

Stabilization Fund, Ending Balance (millions)

$ 67.6 $ 61.6 $ 42.2 $ 28.8 $ 26.1 $33.3