Embed Size (px)

Citation preview

Online Financial Intermediation

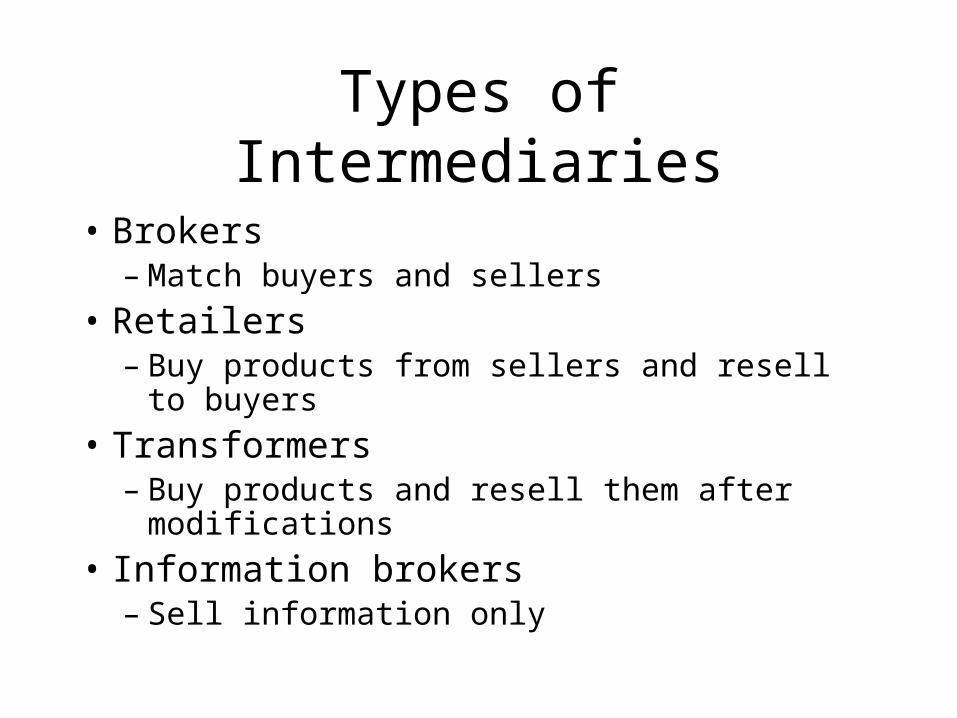

Types of Intermediaries

• Brokers– Match buyers and sellers

• Retailers– Buy products from sellers and resell to buyers

• Transformers– Buy products and resell them after modifications

• Information brokers– Sell information only

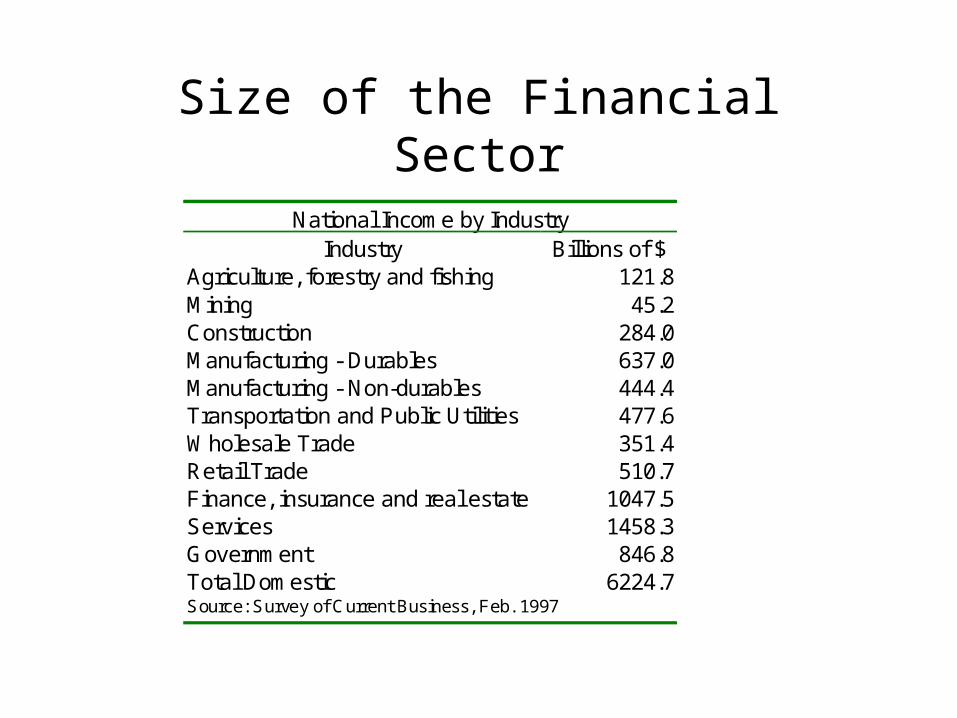

Size of the Financial Sector

National Income by IndustryIndustry Billions of $

Agriculture, forestry and fishing 121.8Mining 45.2Construction 284.0Manufacturing - Durables 637.0Manufacturing - Non-durables 444.4Transportation and Public Utilities 477.6Wholesale Trade 351.4Retail Trade 510.7Finance, insurance and real estate 1047.5Services 1458.3Government 846.8Total Domestic 6224.7Source: Survey of Current Business, Feb. 1997

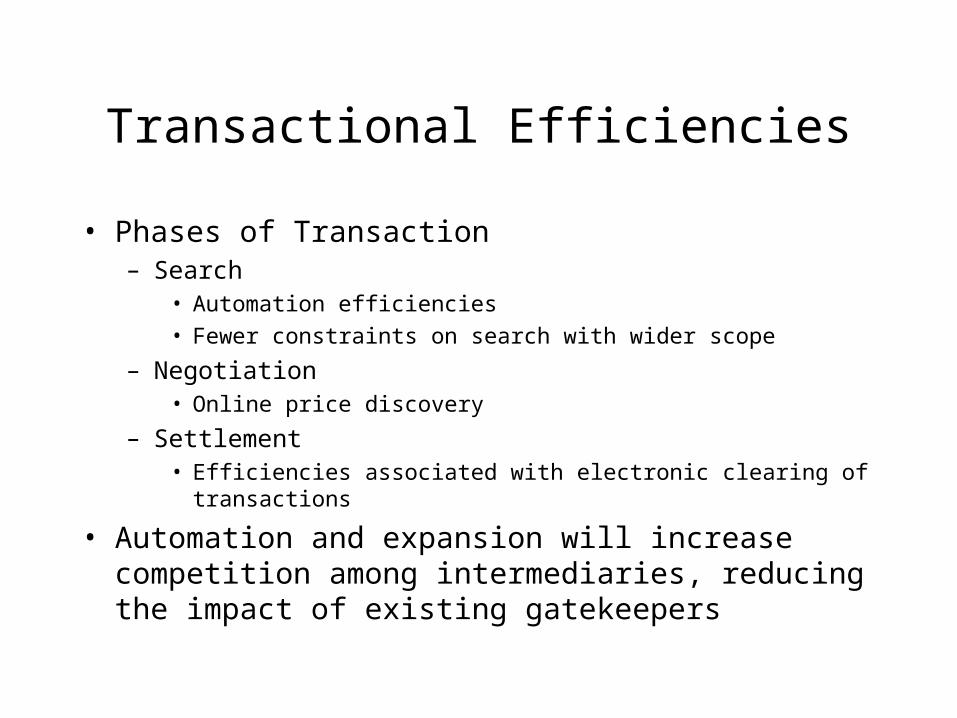

Transactional Efficiencies

• Phases of Transaction– Search

• Automation efficiencies

• Fewer constraints on search with wider scope

– Negotiation• Online price discovery

– Settlement• Efficiencies associated with electronic clearing of transactions

• Automation and expansion will increase competition among intermediaries, reducing the impact of existing gatekeepers

Value-Added Intermediation

• Transformation functions– Continuing role for intermediaries (such as banks) that allow

transformation of asset structures• Changes in maturity (short-term versus long-term borrowing and lending

activities)

• Volume transformation (aggregation of savings for provision of large loans)

• Information Brokerage– Importance of information in evaluation of risk and uncertainty

– Enhancements on the internet: EDGAR (Electronic Data Gathering, Analysis and Retrieval)

• Online database with all SEC filings and analysis of publicly available information

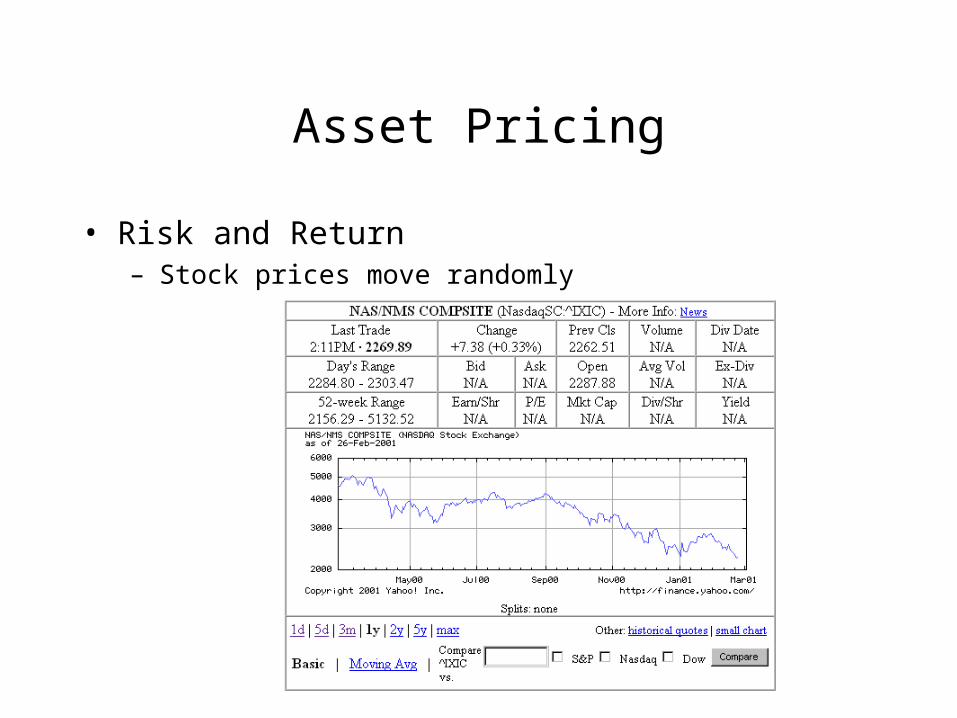

Asset Pricing

• Risk and Return– Stock prices move randomly

Asset Pricing

• Diversification and the law of large number– Model returns as a stochastic process

– N assets, j=1,2,…,N

– Simple model with AR(1) returns:

– Special case with =0: IID returns

10

1,,,0 2

1

ttj

xxj

t

jt

jt

jt

Asset Pricing

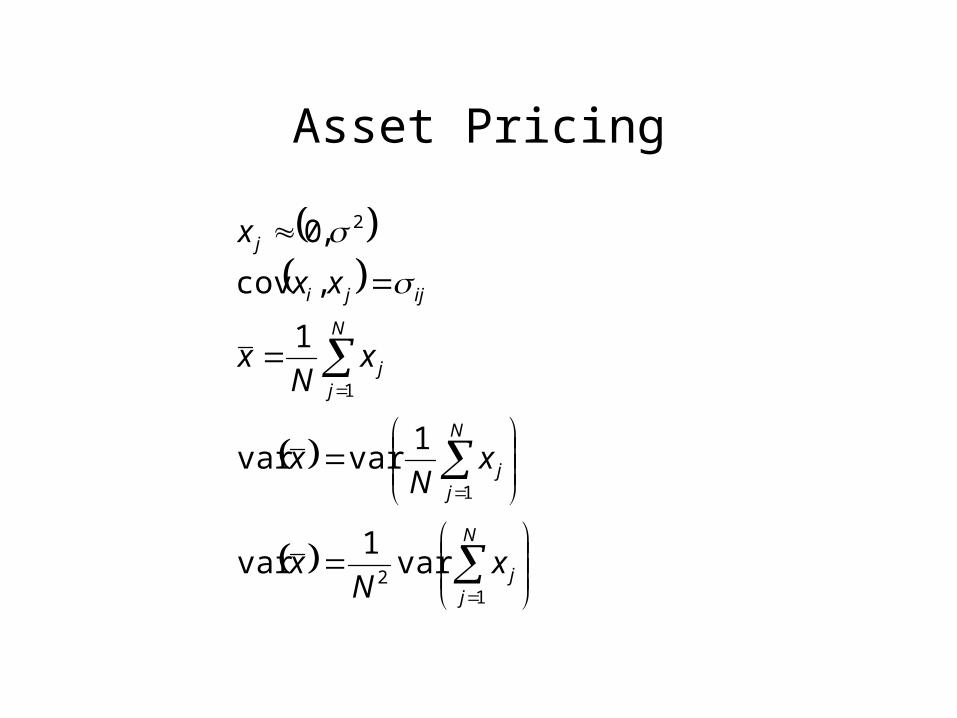

• Construct a portfolio consisting of 1/N shares of each stock– Payoff to the portfolio is the average return

– We measure the risk associated with the portfolio as simply the variance (or standard deviation of the returns).

• Risk of any given asset will be 2

• What is the risk of the average portfolio?

N

j

jt

N

j

jtt N

xN

r11

11

Asset Pricing

NN

N

N

VarN

xN

VarrVar

N

j

N

j

jt

N

j

jtt

2

2

2

1

22

12

1

1

1

1)(

Asset Pricing

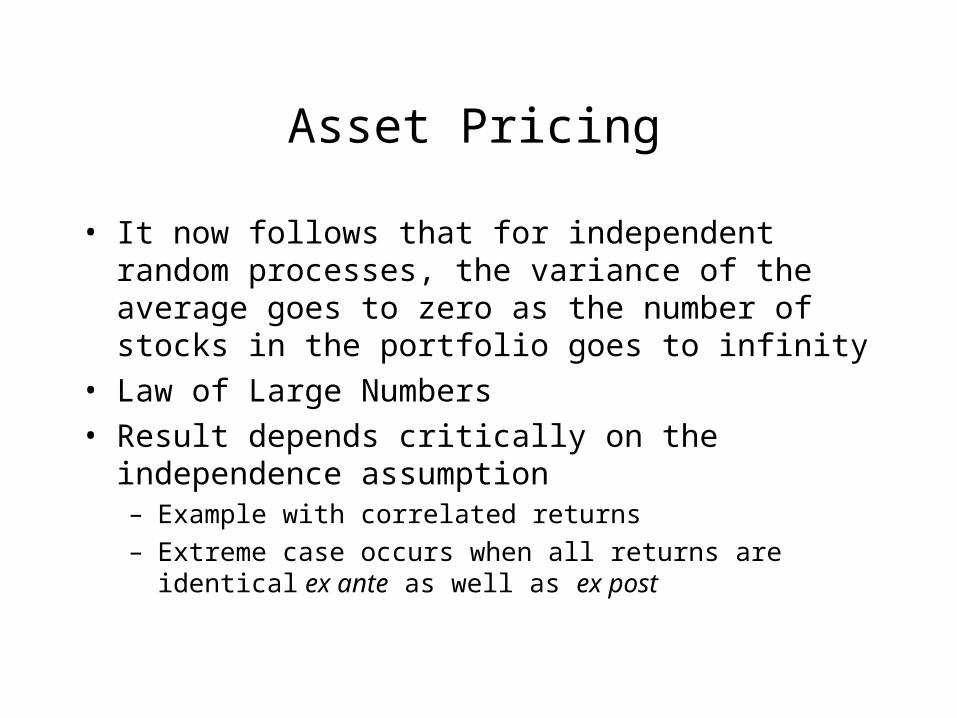

• It now follows that for independent random processes, the variance of the average goes to zero as the number of stocks in the portfolio goes to infinity

• Law of Large Numbers

• Result depends critically on the independence assumption– Example with correlated returns

– Extreme case occurs when all returns are identical ex ante as well as ex post

Asset Pricing

N

jj

N

jj

N

jj

ijji

j

xN

x

xN

x

xN

x

xx

x

12

1

1

2

var1

var

1varvar

1

,cov

,0

Asset Pricing

jiij

jiijj

NN

N

x

1

1

and

1

Let

var

,correlated are returns Because

N

1j

22

N

1j

2N

1j

Asset Pricing

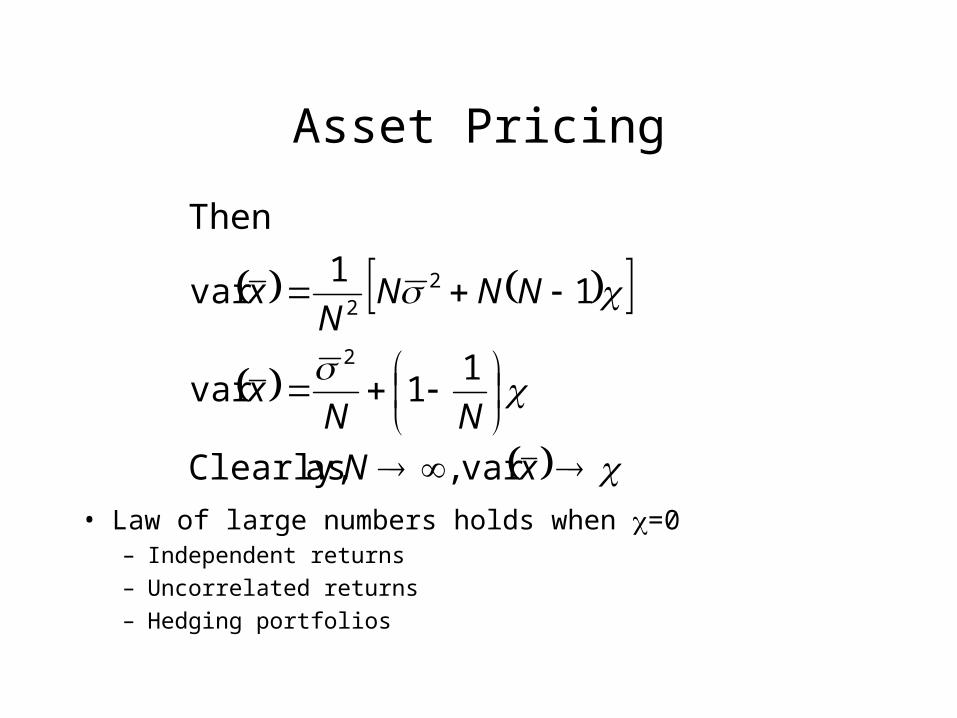

• Law of large numbers holds when =0– Independent returns

– Uncorrelated returns

– Hedging portfolios

xN

NNx

NNNN

x

var , as Clearly,

11var

11

var

Then

2

22

CAPM

• Capital Asset Pricing Model– Approximation assumption: returns are roughly normally

distributed

CAPM

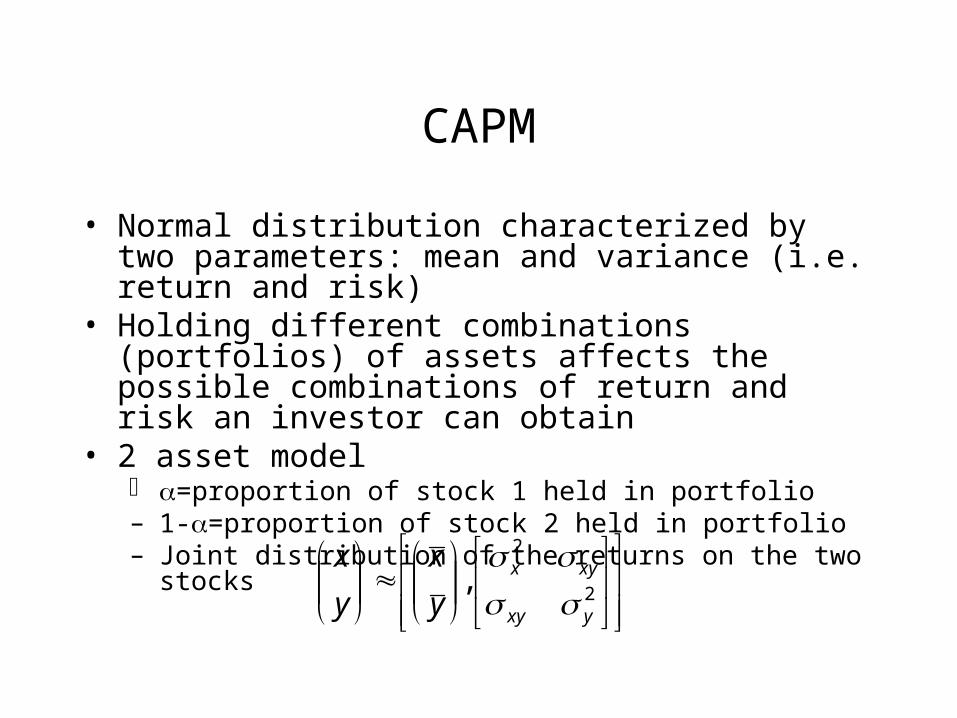

• Normal distribution characterized by two parameters: mean and variance (i.e. return and risk)

• Holding different combinations (portfolios) of assets affects the possible combinations of return and risk an investor can obtain

• 2 asset model =proportion of stock 1 held in portfolio– 1-=proportion of stock 2 held in portfolio– Joint distribution of the returns on the two stocks

2

2

,yxy

xyx

y

x

y

x

CAPM

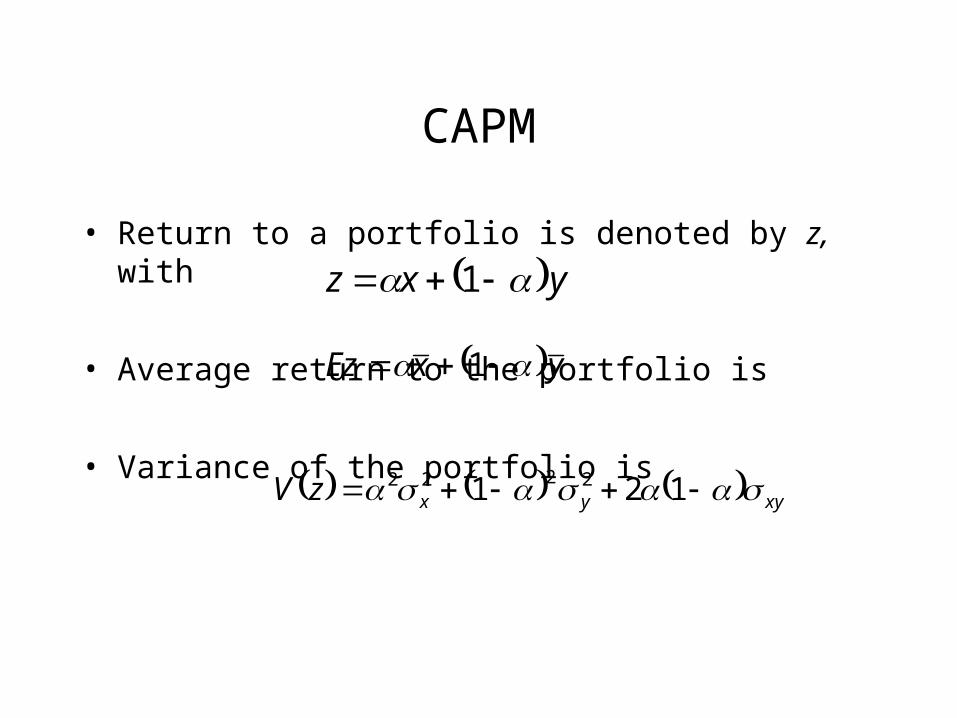

• Return to a portfolio is denoted by z, with

• Average return to the portfolio is

• Variance of the portfolio is

yxz 1

yxEz 1

xyyxzV 121 2222

CAPM

• We can derive the relationship between the mean of the portfolio and its variance by noting that

• Substituting for in the expression for the variance of the portfolio, we find

• To portfolio spreadsheet

yx

yz

2222

2

22 yyxyyxyx yx

yz

yx

yzzV

CAPM

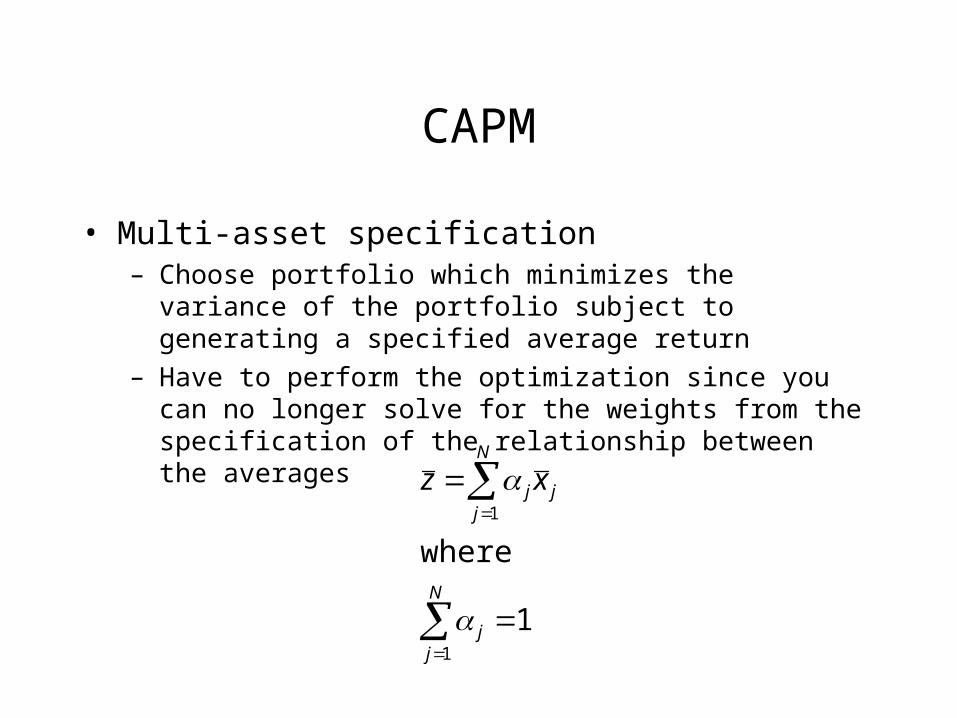

• Multi-asset specification– Choose portfolio which minimizes the variance of the portfolio

subject to generating a specified average return

– Have to perform the optimization since you can no longer solve for the weights from the specification of the relationship between the averages

N

jj

N

jjj xz

1

1

1

where

CAPM

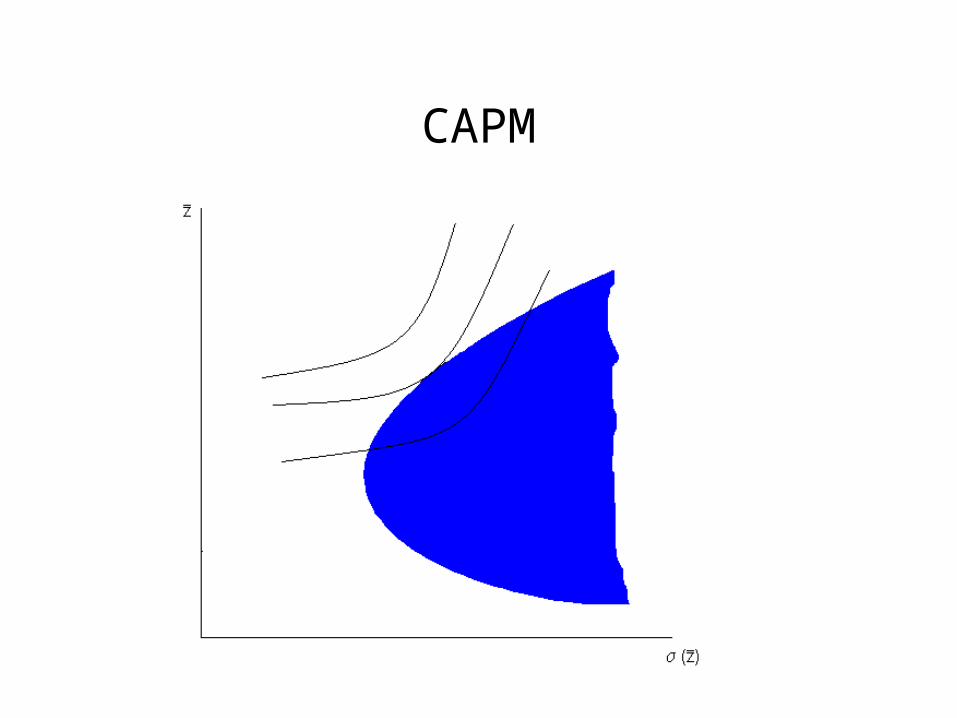

• As with the two asset case, yields a quadratic relationship between average return to the portfolio and its variance, which is called the mean-variance frontier– Frontier indicates possible combinations of risk and return

available to investors when they hold efficient portfolios (i.e. those that minimize the risk associated with getting a specific return

– Optimal portfolio choice can be determined by confronting investor preferences for risk versus return with possibilities

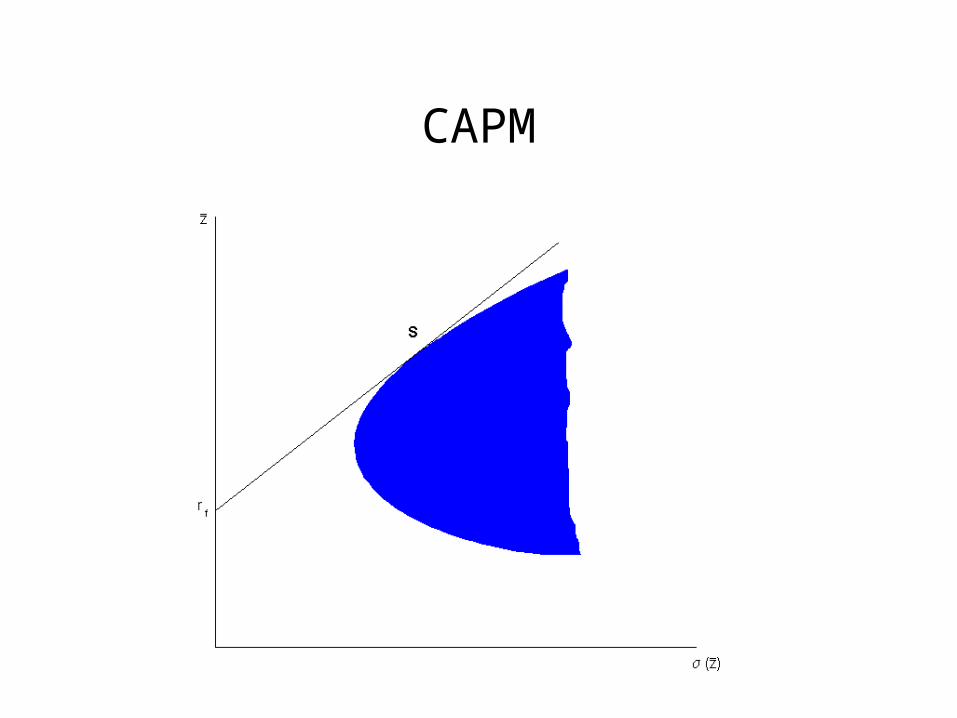

CAPM

CAPM

• Two fund theorem– Introduce possibility of borrowing or lending without risk

– Example: T-bills

– Let rf denote the risk-free rate of return

• Historically, around 1.5%

– The two fund theorem then states that there exists a portfolio of risky assets (which we will denote by S) such that all efficient combinations or risk and return (i.e. those which minimize risk for a given rate of return) can be obtained by putting some fraction of wealth in S while borrowing or lending at the risk-free rate. The portfolio S is called the market portfolio.

CAPM

CAPM

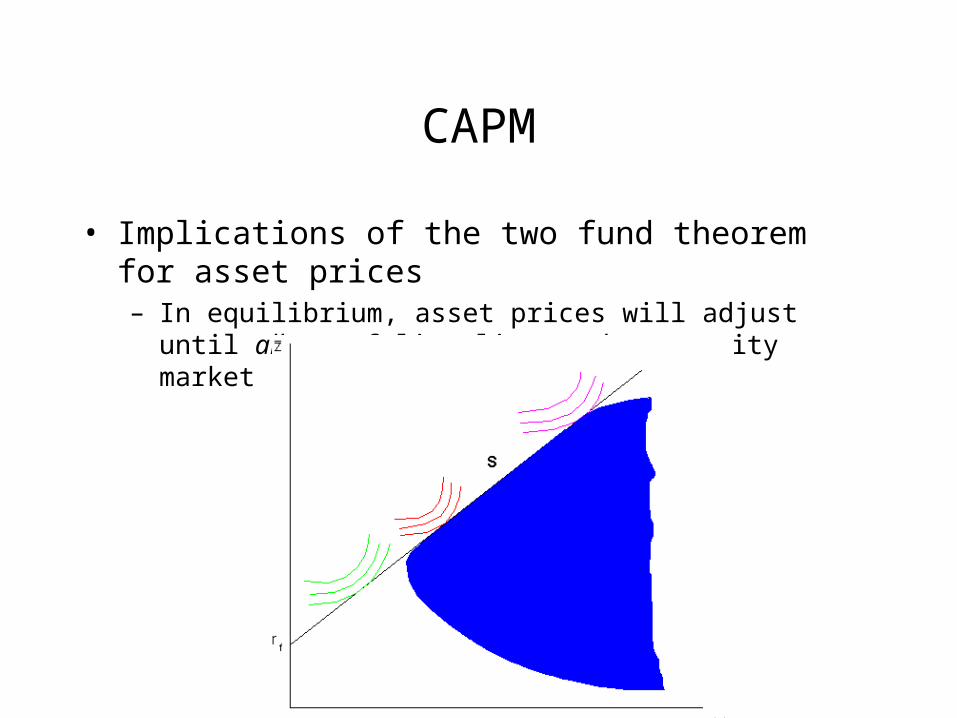

• Implications of the two fund theorem for asset prices– In equilibrium, asset prices will adjust until all portfolios lie on the

security market line

CAPM

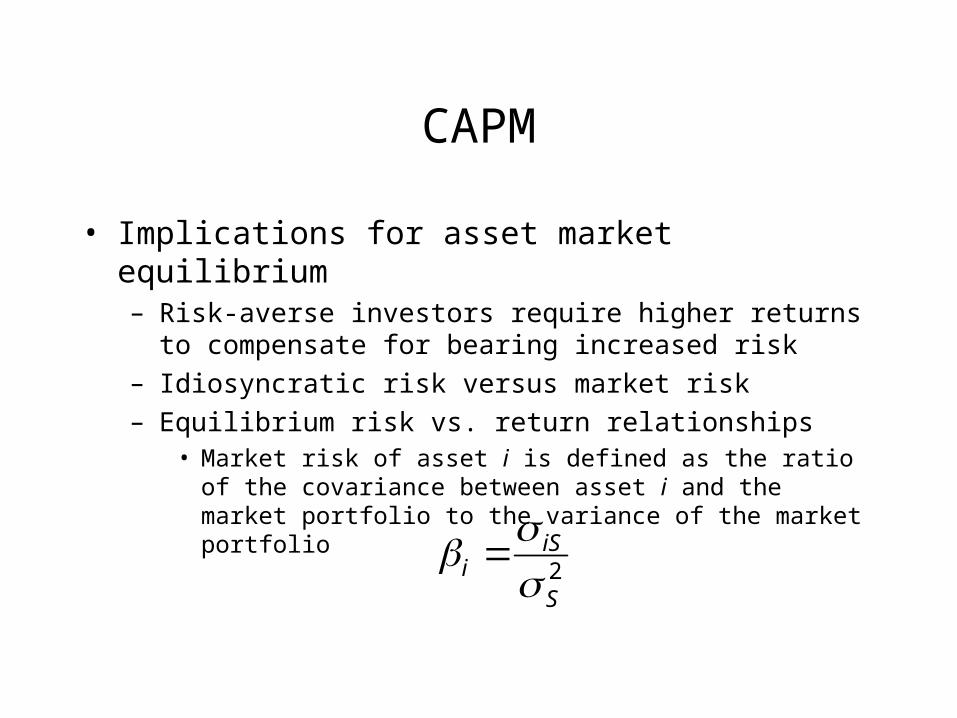

• Implications for asset market equilibrium– Risk-averse investors require higher returns to compensate for

bearing increased risk

– Idiosyncratic risk versus market risk

– Equilibrium risk vs. return relationships• Market risk of asset i is defined as the ratio of the covariance between

asset i and the market portfolio to the variance of the market portfolio

2S

iSi

CAPM

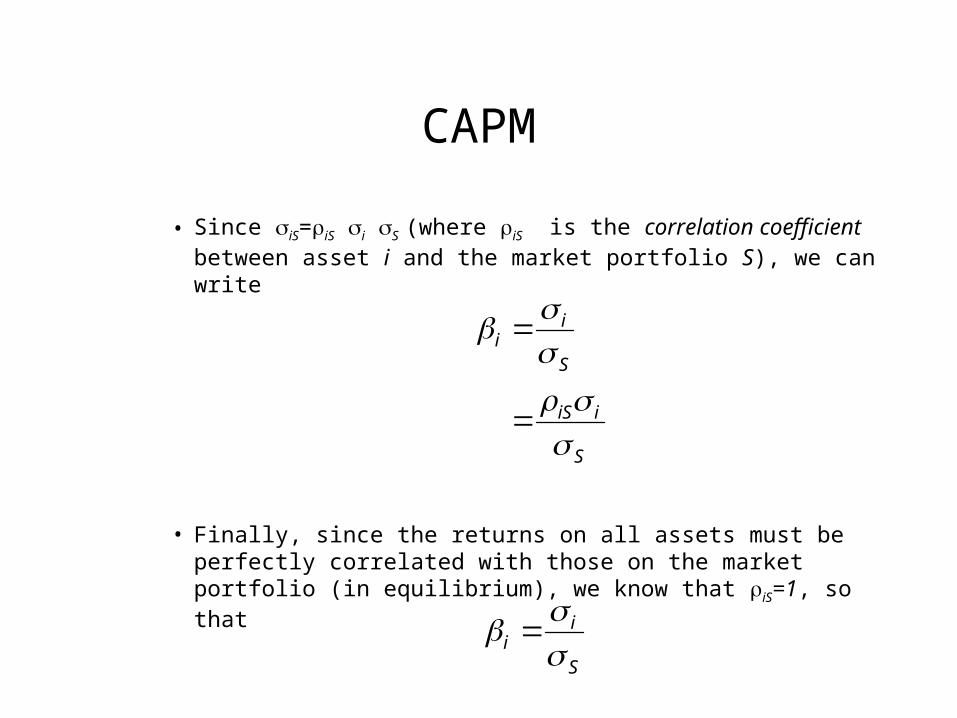

• Since iS=iS i S (where iS is the correlation coefficient between asset i and the market portfolio S), we can write

• Finally, since the returns on all assets must be perfectly correlated with those on the market portfolio (in equilibrium), we know that iS=1, so that

S

iiS

S

ii

S

ii

CAPM

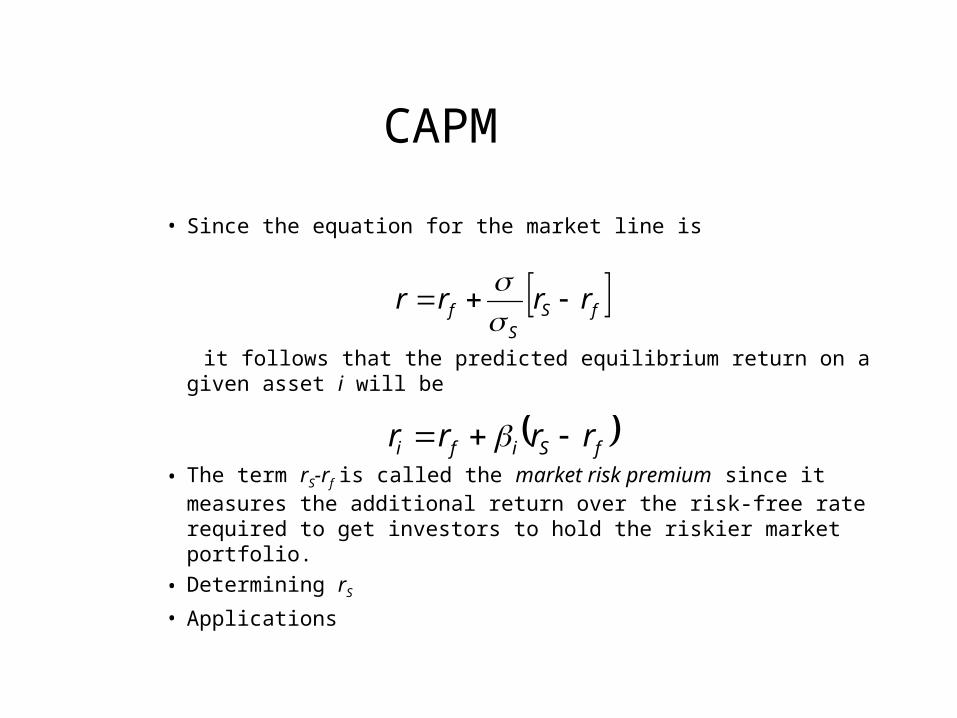

• Since the equation for the market line is

it follows that the predicted equilibrium return on a given asset i will be

• The term rS-rf is called the market risk premium since it measures the additional return over the risk-free rate required to get investors to hold the riskier market portfolio.

• Determining rS

• Applications

fSS

f rrrr

fSifi rrrr