Embed Size (px)

Citation preview

20 Novembre, 2010

On track to global carco

Q3 Results Review

October 28, 2011 Q3 2011 Results Review 2

CHIEF OPERATING

OFFICERS

BRAND LEADERS

INDUSTRIAL PROCESS LEADERS

CEO

Sergio

Marchionne

SUPPORT/ CORPORATE

LEADERS

EMEA Gianni Coda

NAFTA Sergio Marchionne

LATAM Cledorvino Belini

APAC Michael Manley

Parts & Service

(Mopar) Pietro Gorlier

Systems & Castings

(Comau & Teksid) Riccardo Tarantini

Components (Magneti Marelli)

Eugenio Razelli

Design Lorenzo Ramaciotti

Group Purchasing

Vilmar Fistarol

Quality Doug Betts

Product Portfolio

Management Mark Chernoby

Powertrain Coordinator

Bob Lee

Chief

Manufacturing

Officer Stefan Ketter

Chief Technology

Officer Harald Wester

Business Development

Alfredo Altavilla

Chief Human

Resource Officer

Linda Knoll

Chief

Financial

Officer

Richard Palmer

Jeep Michael Manley

Fiat Olivier François

Chief

Marketing Officer

Olivier François

Commercial Vehicles

Lorenzo Sistino

Alfa

Romeo

Abarth

Maserati Harald Wester

Lancia

Chrysler Saad Chehab

Dodge Reid Bigland

Fiat Services

& Holdings

Alessandro Baldi

A global company, one leadership team

Group financials

Autos & LCVs

Luxury & performance brands

Magneti Marelli

Fiat Powertrain

Outlook

1

2

3

4

5

6

October 28, 2011 Q3 2011 Results Review 4

Europe 28%

North America

47%

Mercosur 17%

RoW 8%

1

Europe 57%

North America 3%

Mercosur 32% RoW

8%

Q3 REVENUES BY GEOGRAPHY

Looking at Fiat from a different perspective Better geographical diversification

FY REVENUES BY GEOGRAPHY

Europe 60%

North America

3%

RoW 9%

Mercosur 28%

North America

47% Europe 30%

Mercosur 17%

RoW 6%

* Assuming 12 months of Chrysler

October 28, 2011 Q3 2011 Results Review 5

8.4

17.6

Q3 „11 Q3 „10

Net profit (€mn)

Net industrial debt

(€bn)

Liquidity (€bn)

• Increase mainly reflects seasonal working capital absorption in addition to payments to UST & Canada for purchase of interests in Chrysler (€0.5bn), and non-cash items (€0.3bn)

• Capex for the quarter amounted to €1.6bn

Trading profit (€mn)

Trading margin

• Chrysler contributing €556mn, two-thirds of Group‟s trading profit

• Ex Chrysler at €295mn, a 15% year-over-year improvement

• Total available liquidity, inclusive of undrawn credit facilities, €12.8bn for Fiat ex Chrysler and €8.0bn for Chrysler

• Increase over prior quarter also reflects closing of Fiat‟s new €1.95bn revolving credit facility, of which €1.75bn already available and undrawn at quarter-end

• September-end position includes early reimbursement of a €1.0bn credit facility and proceeds from €1.5bn bond issuances in July

Note: Q3 ‟10 figures provided herein exclude businesses transferred to Fiat Industrial under demerger

• Chrysler: 6.0%

• FGA: 2.0%

• Ferrari: 14.7%

• Maserati: 5.6%

• Components & Production Systems: 3.1%

• Fiat ex Chrysler: 3.3%

Q3 „10

256

851

Q3 „11

Q3 „10

3.0%

4.8%

Q3 „11

73

112

Q3 „11 Q3 „10

5.8

Sep 30 „11 Jun 30 „11

3.4

1

Q3 „11 highlights Strong operating performance for Chrysler & Components, resilience elsewhere

• Ex €138mn loss on mark-to-market of two Fiat stock-option related equity swaps and €57mn in net unusual charges, Group achieved a net profit of ~€300mn and Fiat ex Chrysler at break-even

• Chrysler net profit of €322mn

1.0

Jun 30 „11

20.2 20.8

Sep 30 „11

19.2 18.1

Cash & Mktable Securities

Undrawn available committed credit lines

Net revenues (€bn)

• Chrysler contribution of €9.3bn, consolidated for the first full quarter

• Fiat ex Chrysler at €8.8bn, up 4.4% on the back of growth in Luxury Brands and Components businesses

2.7

October 28, 2011 Q3 2011 Results Review 6

• Continued firm grip on costs and production levels

Tight management of production systems maintaining output levels in line with sales trend

Temporary layoffs as major source of operating flexibility at plants while minimizing social impact

Global dealer inventory down ~3% at FGA, US dealer stock down ~12% in the quarter

World Class Manufacturing delivered €120+mn for Fiat & Chrysler combined

Savings to-date in excess of €350mn in aggregate, fully on track with FY targets

Full leverage of purchasing power proceeding apace (€52+bn direct materials APV expected for FY „11 when considering also Fiat Industrial)

Fiat ex-Chrysler net purchasing savings in sight of ~€80mn FY target (€50mn Sep YTD)

Chrysler net purchasing performance substantially break-even in the quarter and for Sep YTD

• New 4-year national labor contract with UAW for Chrysler ratified on Oct 26

• Successful refinancing of Fiat‟s bank & capital market maturities due in 2011-12

Bond issuances for an aggregate amount of €1.5bn

Close of syndication of committed revolving credit facility for €1.95bn

• Simplification of share capital structure

• FY 2011 guidance for Group trading profit firmed up to more than €2.1bn, all remaining targets confirmed

1 Q3 „11 highlights (cont‟d)

October 28, 2011 Q3 2011 Results Review 7

Revenues (€mn)

15,958

(1,237)

Automobiles Components & Production

Systems

Eliminations & Others

Q3 „11

Trading profit (€mn)

Fiat Group Automobiles

• Revenues of €6.5bn, in line with prior year (+0.6% at constant exchange

rates). A more favorable sales mix, resulting from higher volumes of LCVs,

and contribution from distribution of Jeep in Europe offset by contraction in

passenger car volumes

• Trading profit of €128mn (€130mn in Q3 „10) driven by industrial

efficiencies and improvement in mix offsetting decline in volumes

Luxury & Performance brands

• Revenues for Ferrari up 17.7% , Maserati +6.0%

• Trading profit slightly improved at Ferrari despite higher R&D spending for

new products

• Maserati doubling trading profit to €8mn

Components & Production Systems (Magneti Marelli, Fiat Powertrain, Teksid, Comau)

• Revenues for Magneti Marelli +7.1%, Production Systems +46%, Teksid

+16% while Fiat Powertrain slightly down (-1%)

• Nearly doubled trading profit at Magneti Marelli together with

improvements at Teksid & Comau more than compensating for reduction at

Fiat Powertrain

Magneti Marelli 1,374

Fiat Powertrain 1,002

Teksid 229

Comau 371

769 (6)

Automobiles Components & Production

Systems

Eliminations & Others

Q3 „11

Magneti Marelli 43

Fiat Powertrain 29

Teksid 12

Comau 4

FGA 6,520

Chrysler 9,284

Ferrari 525

Maserati 142

FGA 128

Chrysler 556

Ferrari 77

Maserati 8

7.5%

12.8%

Chrysler Group LLC

• Revenues of €9.3bn resulting from a 15% worldwide shipments increase to

469k vehicles

• Trading profit at €556mn with continued positive trend in volume, mix and

price from new vehicle launches, with trading margin benefiting also from a

low amortization charge for R&D, as current spending relates to products

still in development

17,552 2,831

851 88

1 Q3 „11 Revenues and trading profit by business

October 28, 2011 Q3 2011 Results Review 8

1 From trading profit to net result Q3 „11

(€mn; IFRS) Q3 „11

Fiat w/Chrysler Q3 „11

Chrysler

Q3 Fiat

2011 2010

Trading profit 851 556 295 256

Unusual items, net (57) 3 (60) (2)

Operating income 794 559 235 254

Financial charges, net (543) (209) (334) (27)

Investment income, net 31 6 25 14

Pre-tax result 282 356 (74) 241

Taxes (170) (34) (136) (168)

Net result 112 322 (210) 73

• “Unusual items, net” includes €63mn in restructuring charges related to Fiat Group Automobiles

• “Financial charges, net” includes loss of €138mn in the mark-to-market value of two stock option-related equity swaps (€58mn gain for Q3 „10)

October 28, 2011 Q3 2011 Results Review 9

1 From trading profit to net result Sep YTD ‟11

• “Unusual items net” relates to:

Unusual income totaled €2,025 million, of which €2,017 million related to the fair value re-measurement of the 30% ownership interest held in Chrysler prior to the acquisition of control and of the right to receive an additional 5% ownership interest following achievement by Chrysler of the third Performance Event

Unusual expense totaled €1,024 million, of which €804 million ex-Chrysler (including €562 million in non-cash charges) largely attributable to the impact on Fiat‟s businesses of the strategic realignment with Chrysler‟s manufacturing and commercial activities, further accelerated following the increase of Fiat‟s ownership interest, and to one-off charges mainly related to the realignment of certain minor activities of the Group

Chrysler‟s June-September 2011 operating profit of €486 million includes €220 million in unusual expenses recognized at the date of acquisition of control in relation to an upward revaluation or “step up” of its inventories associated with the recognition of assets acquired and liabilities assumed at fair value. Due to rapid inventory turnover, in June this amount was fully written off (recognized as a one-off non-cash charge)

• “Financial charges, net” includes loss of €115mn in the mark-to-market value of two stock option-related equity swaps (€26mn gain for Sep YTD „10)

(€mn; IFRS) Sep YTD „11

Fiat w/Chrysler

Sep YTD „11 Chrysler

(Jun-Sep)

Sep YTD Fiat

2011 2010

Trading profit 1,627 706 921 793

Unusual items, net 1,001 (220) 1,221 (25)

Operating income 2,628 486 2,142 768

Financial charges, net (911) (279) (632) (355)

Investment income, net 79 6 73 93

Pre-tax result 1,796 213 1,583 506

Taxes (410) (34) (376) (437)

Net result 1,386 179 1,207 69

October 28, 2011 Q3 2011 Results Review 10

(€mn; IFRS) Q3 „11

Fiat w/Chrysler

Chrysler Q3 Fiat

2011 2010

Net Industrial (Debt)/Cash beginning of period (3,407) (2,428) (979) (4,544)

Purchase of UST and Canada additional stake in CG (1) (490) - (490) -

Adj. Net Industrial (Debt) / Cash beginning of period (3,897) (2,428) (1,469) (4,544)

Net Income 112 322 (210) 73

D&A 1,023 460 563 559

Change in Funds & Others 91 (56) 147 8

Cash Flow from Op. Activities bef. Chg. in W.C. 1,226 726 500 640

Change in Working Capital (1,430) (640) (790) (297)

Cash Flow from Operating Activities (204) 86 (290) 343

Tangible & Intangible Capex (1,562) (720) (842) (609)

Cash Flow from Operating Activities net of Capex (1,766) (634) (1,132) (266)

Change in Investments, Scope & Others (22) 254 (276) 95

Net Industrial Cash Flow (1,788) (380) (1,408) (171)

Capital Increase / Share Repurchases / Dividends (1) (2) 1 42

FX Translation Effect (86) (78) (8) (19)

Change in Net Industrial Debt (1,875) (460) (1,415) (148)

Net Industrial (Debt)/Cash end of period (5,772) (2,888) (2,884) (4,692)

• Payments of €0.5bn to UST & Canada for purchase of interests in Chrysler

• Negative working capital mainly driven by trade payable reduction due to seasonal low production levels, with Q3 „10 impacted by non-recurring cash receipts

• Increased Capex progressing broadly in line with FY guidance

• €0.3bn negative non-cash impact from derivatives valuations and FX translation

• Reduced dealer inventory levels

(1) Including Equity Recapture Agreement

1 Cash flow Q3 „11

October 28, 2011 Q3 2011 Results Review 11

1 Successfully refinanced 2011-12 maturities Fiat ex Chrysler

• Three over subscribed new bond issuances in first 9 months of the year

Five-year €1bn bond in April (6.375% coupon)

Bond issuances with aggregate value of €1.5bn in July

Three-year €0.9bn tranche (6.125% yield)

Seven-year €0.6bn tranche (7.375% yield)

1.1

1.5

1.0

2.2

1.5

1.0 1.0

0.6

0.0 0.0

0.5

1.0

1.5

2.0

2.5

Q4

2011

2012 2013 2014 2015 2016 2017 2018 > 2018

•Committed and signed €1.75bn Revolving Credit Facility (RCF) in July

•Syndication phase launched in early September and closed for €1.95bn in October

Three-year facility with 18 key relationship banks replacing a 3-year €1bn revolving credit facility originally signed in February 2009

•Facility fully undrawn at quarter-end and intended for general corporate purposes and working capital needs

•Size of new RCF equal to ~100% of bank maturities outstanding at Sep 30th 2011 and due through end of 2012

Mostly self-liquidating position related to dealer floor-plan financing in Brazil and capital leases

Bonds issued in 2011

(Principal only)

October 28, 2011 Q3 2011 Results Review 12

Note: Numbers may not add due to rounding

1 Debt maturity schedule (€bn)

1) Excluding fair value of Bonds, including interest accruals

Outstanding Sept. 30, „11

Fiat SpA (ex Chrysler)

Next 12 M

3M 2011

2012 2013 2014 2015 Beyond

4.6 Bank Debt 1.7 0.7 1.3 1.1 0.5 0.5 0.5

10.2 Capital Market (1) 2.7 1.4 1.6 1.0 2.2 1.5 2.6

1.4 Other Debt 0.9 0.9 0.1 0.1 0.0 0.1 0.2

16.1 Total Cash Maturities 5.2 2.9 2.9 2.2 2.7 2.1 3.3

11.1 Cash & Mktable Securities

1.8 Undrawn committed credit lines

12.8 Total Available Liquidity

3.1 Sale of Receivables (IFRS de-recognition compliant)

2.2 of which receivables sold to financial services JVs (FGA Capital)

Outstanding Sept. 30, „11

Chrysler Next 12 M

3M 2011

2012 2013 2014 2015 Beyond

2.6 Bank Debt 0.1 0.0 0.1 0.1 0.0 0.1 2.3

2.4 Capital Market (1) 0.1 0.1 0.0 0.0 0.0 0.0 2.3

4.9 Other Debt 0.1 0.0 0.2 0.2 0.3 0.3 3.9

9.9 Total Cash Maturities 0.3 0.1 0.3 0.3 0.3 0.4 8.5

7.0 Cash & Mktable Securities

1.0 Undrawn committed credit lines

8.0 Total Available Liquidity

October 28, 2011 Q3 2011 Results Review 13

1 Simplification of share capital structure Summary of the proposed transaction

Conversion of Fiat Preference and Savings into Ordinary (not interconditional between classes)

Preference shareholders will receive 0.850 Ordinary shares for each Preference share owned

Savings shareholders will receive 0.875 Ordinary shares for each Savings share owned

Description

Fiat EGM

Special EGM of Preference shareholders

Special EGM of Savings shareholders

Required approvals

EGMs to be held at the time of the annual shareholder meeting for the approval of 2011 financials, indicatively scheduled for early April 2012

Timing

Transaction triggers withdrawal rights for absent, abstaining and dissenting Preference and Savings shareholders

The right consists in the cash-out option at a price equal to 6 months average price prior to the publication of the notice of call of the EGM, indicatively expected by end of February 2012

Withdrawal rights

(“Diritto di recesso”)

If declared, special dividends accrued to Preference and Savings with respect to the 2011 financial year will be unaffected

Dividends

Max withdrawal rights condition: the conversion will not be completed if entitled special shareholders exercise the withdrawal right for an amount higher than €56mn for Preference and €44mn for Savings (€100mn in total, divided for each class according to the respective number of shares outstanding)

Other conditions

Simplification of capital structure: from three classes of shares that differ in voting and economic rights to one single share class

Simplification of governance: same voting and capital rights for all shareholders

Exchange at a premium for a more liquid stock for special shareholders

EPS accretive

Rationale / Benefits

October 28, 2011 Q3 2011 Results Review 14

1 Simplification of share capital structure Summary timetable

Oct Nov Dec Jan Feb Mar Apr May Sep

2011

BoD resolution and

announcement (Oct 27)

Jun

2012

Publication of the notice of call of EGMs

Fiat AGM, EGM and special EGMs of Preference and Savings

Entitled special shareholders can exercise withdrawal rights

Max withdrawal condition tested – if condition is met, conversion becomes unconditional

By end of February

Early April

Note: the Company will, within 180 days, cash-out withdrawn shares from the exercise of withdrawal rights

October 28, 2011 Q3 2011 Results Review 15

2

3.1 3.1

~13.6 0.4 0.4

~1.8

Q3 '10 Q3 '11 FY '11E

EU27 + EFTA

LATIN AMERICA

1.06 1.12

~4.2

0.27 0.31

~1.2

Q3 '10 Q3 '11 FY '11E

Autos & LCVs Quarterly industry volumes & outlook (mn units)

NORTH AMERICA

US

Industry volumes up 7% in Q3 2011 vs. prior year

Truck segments up 13% vs. a year ago (comprised 55% of industry)

Passenger car market flat

FY industry expected up ~9% over 2010

Canada

Continued robust industry in Q3, flat vs. prior year

FY market demand expected up ~2% vs. a year ago

3.1 3.3

~12.8

Q3 '10 Q3 '11 FY '11E

US

0.4 0.4

~1.6

Q3 '10 Q3 '11 FY '11E

CANADA

~5.4

1.43 1.33

In particular:

Brazilian market holding up well notwithstanding a particularly strong quarter a year ago (+1.8% to 889k units in Q3 2011, +6.7% to 2,528k units for 9 months into the year)

Flattish passenger car market and continued strong growth in LCVs (+14.8% vs. prior year) in Q3

Brazilian overall market projected to ~3.5mn units for FY 2011

Passenger cars up ~2% and robust growth for LCVs (up ~13%)

0.38 0.36

~1.7

0.04 0.04

~0.2

Q3 '10 Q3 '11 FY '11E

Passenger cars

EU27+EFTA industry up 1.7% or 52k units in Q3 driven by strong performance in Germany (+11.6%); continuing shift in demand towards higher segments, Germany & France in particular

Continued weakness in Italian market, down 6.1% to 355k units in the quarter

LCVs

Sustained growth pattern for LCVs in Q3 across all EU countries (+5.6% overall), with exception of Italy (-2.2%) & France (-4.5%); minor markets up 11.5% in aggregate

FY 2011E for Europe unchanged vs. prior forecast

Passenger car industry expected down ~1.5% vs. a year ago with slightly improved outlook for France countering persisting weakness in Italy (demand now seen down ~10-12% from 2010 levels)

LCVs up ~8% with mixed trend across major markets (Germany driving the increase while decline in France & UK and Italy now projected down ~3%)

EUROPE

Passenger cars LCVs Passenger cars LCVs

October 28, 2011 Q3 2011 Results Review 16

MARKET SHARE

(%)

2010 2011 2009

2 Autos & LCVs US & Canada – Business dynamics in Q3 „11

8.0

9.6

11.4

11.3

12.8

14.5

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

US

September marking the 18th-consecutive month of year-over-year sales gains

Q3 share at 11.4%, up 180 bps vs. a year ago and 340 bps compared to a low/point of 8.0% in Q3 2009

Six consecutive quarterly year-over-year share gains

Retail sales (excluding fleet) increased 41%

Retail of retail market share* increased to 10.2%, up 250 bps

Fleet mix at 26%, down from 34%

Steady increase in market share primarily resulting from momentum of 16 new and significantly refreshed products

All-new Jeep Grand Cherokee, new Chrysler 200 and Dodge Durango continue to boost sales

Canada

Share steadily increased from 2009 lows

Q3 share at 14.5%, up 170 bps from a year ago

Retail sales (excluding fleet) increased 10%

Retail of retail market share* increased to 13.4%, up 160 bps

Key performers: Jeep Wrangler (+52%), Jeep Compass (+35%), Jeep Grand Cherokee (+31%) & Ram Pickup (+9%)

*Company calculation; retail sales (excluding fleet) versus industry retail sales (excluding fleet)

October 28, 2011 Q3 2011 Results Review 17

2010 2011

2 Autos & LCVs US sales – Key vehicle contributors

Q1 Q2 Q3

+64%

+196%

Q1 Q2 Q3

+19% +13%

Q1 Q2 Q3

New

New

Q1 Q2 Q3

New

New 15k

8k 23k

10k

Q1 Q2 Q3

+64%

+112%

+38%

+63%

+52%

New

16k

New

26k

October 28, 2011 Q3 2011 Results Review 18

Autos & LCVs EU+EFTA – Passenger car business dynamics in Q3 „11

2

•Sales of 202k units in the quarter

•Q3 share at 6.5%, 60 bps lower than a year ago due to unfavorable segment & geographic mix

Italy: share gain of 50 bps unable to counter decline of aggregate share in Rest of Europe

Europe ex Italy: 3.5%, down 50 bps

Combined A- & B-segment down 310 bps from 33.6% in Q3 „10 resulting in almost 40 bps loss in FGA share

•Share performance impacted by initial contribution of Lancia Ypsilon & Fiat Freemont, and continued strength of Alfa Romeo Giulietta despite discontinuation of 5 models (Punto Classic in particular)

*Including Jeep & Chrysler

MARKET SHARE*

(%)

• Reversed trend in year-over-year change in quarterly market share

• First quarterly year-over-year share gain since Q1 2010 notwithstanding a negative 260 bps impact of phased-out models in the quarter

Strong performance of Jeep (more than 3x 2010 level) contributing 60 bps to share

Initial contribution to share improvement from Lancia New Ypsilon & Fiat Freemont (14k units in Q3)

Italy*

(market share and y-o-y change in market share)

30.6

29.4 28.8

29.3 30.0 29.9

Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11

-350 bps

-300 bps -230 bps

-60 bps

EU27+EFTA

7.5 7.8 8.1

8.4

7.1 6.5

31.7 31.8 32.4 32.9

29.4 29.9

2007 2008 2010 2009 2011 2006

+50 bps

-410 bps

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q4 Q2 Q3 Q1 Q3 Q4 Q3 Q1 Q2

October 28, 2011 Q3 2011 Results Review 19

Autos & LCVs EU27+EFTA – Q3 „11 sales highlights by brand

2

• Share at 4.6%, or 90 bps lower than a year ago

The most impacted brand for unfavorable segment & geographic mix

• Strong performance of recently launched Freemont

More than 18k orders taken to date

FY 2011 target confirmed at 20k+units

AWD version with 6-speed automatic transmission to round out product offering in Q4

• Brand share stable at 0.9%

Sales at 27k units in the quarter

• Robust sales of Giulietta (+29%) on first full quarter comparison

Best-in-class C-Segment player in all main EU countries

~15k orders (~120k since launch in May 2010)

~17k shipments in Q3 (64k Sep YTD), on track with FY target of 90-100k units

• Sep YTD total sales up 32.1% (20 bps share gain), exceeding 105k units

• Share doubled vs. a year ago to 0.2% on the back of new and redesigned vehicles launched in 2011

• Total sales up 135% to ~7k units (over 17k Jeeps sold at Sep YTD)

Grand Cherokee +126%

Strong performance of Compass (14x last year level)

Wrangler up 59%

• Q3 product actions

Full availability of 2WD for Compass (40% of mix)

New diesel engines delivering significant improvement in CO2

• Share up 10 bps to 0.7% albeit with weak Italian market

• Performance of New Ypsilon in line with FY 2011 target of 45-50k shipments

More than 25k orders taken to date

• Further new product intros (Thema & Voyager) available in market starting early November

October 28, 2011 Q3 2011 Results Review 20

Autos & LCVs New Panda: the “magic box” since the „80s

2

• International press event in December 2011

• Preview at dealerships in January 2012

• Available in all European markets from February and later in more than 40 countries outside Europe

• FY 2012 target of ~230k Pandas including Panda Classic as entry-level model

DESIGN EVOLUTION

Compact size (3.65m in length)

Seamless window design

Split 3D headlamps

SAFETY

Best-in-class among reference competitors

VERSATILITY & FUNCTIONALITY

Slim seats for improved roominess

Improved boot size

Integrated navigation system

TECHNOLOGY & PERFORMANCE

The widest powertrain offering in segment

Highly fuel-efficient powertrains with TwinAir covering 65-85hp range (99g/km CO2 emissions)

CNG application available on TwinAir engine

Start&Stop

Traction Plus for improved 4x2 traction in difficult conditions

Available also in 4x4 version, the best off-road vehicle in A-segment

FUN

A nippy car, easy and fun-to-drive

A colorful collection of interior trims

October 28, 2011 Q3 2011 Results Review 21

• Fiat Professional outperformed European market recording 30 bps share gain despite unfavorable market mix

Italy: 100 bps share gain driven by strong performance of small vans and car derived vehicles

EU-ex Italy: sales up 12.8% corresponding to 50 bps gain in market share on the back of New Ducato and Doblò

• Brand sales in Europe up 8.4% to 47.7k units with volume gains in almost all markets, in particular Germany, Spain & The Netherlands

MARKET SHARE*

(%)

10.611.8 12.1 12.1 11.6 11.9

45.443.3 42.5

39.941.4

42.4

*Due to unavailability of data from Italy since Jan 2011, figures reported for 2011 for that

country are an extrapolation. As there are no current market figures, possibility of a margin of error for EU totals exists

EU27+EFTA

2007 2008 2010 2009

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q4 Q2 Q3 Q1 Q3

2011

Q4 Q3 Q1

2006

Q2

Autos & LCVs EU27+EFTA – LCV business dynamics in Q3 „11

2

• Latest product introduction rounding out Fiat Professional product offerings, the most up-to-date and complete of any EU producer

• First OEM-produced drop side vehicle ensuring higher quality and reliability to customers

Payload up to 1T, a unique offer in its segment

Lower consumption/emissions levels than a pick-up, more competitive price and compact dimensions than large van-derived

October 28, 2011 Q3 2011 Results Review 22

Update on labor relations US & Italy

2

• Continued operating flexibility at plants

Sustained alignment of production systems with market demand through use of flexibility tools such as temporary layoffs, agency contract adjustments and overtime, as required

• New investments in Italy announced

Mirafiori: Confirmed intention to install most updated version of one of three main architectures on which various nameplates for various brands will be produced, starting with a Jeep SUV in 2013

Pratola Serra: new 1.8L 4-cyl. engine to be developed for Alfa Romeo

• Continued commitment to transform Italian industrial infrastructures allowing sustainable international competition

Exit from Confindustria (confederation of Italian businesses) as of Jan 1, 2012 allowing direct negotiation with Unions and correct application of contracts already signed at Pomigliano, Mirafiori and Grugliasco plants, thus securing optimized operating flexibility

• Termination of car production at Termini Imerese plant at end of 2011

• New plant and product investments

$4.5bn in investments

2,100 new entry-level jobs

• Gains for new hires

Highest max hourly rate increases to $19.28 by end of contract

No cap on new hires

• Simplified and transparent profit sharing formula

Based on 85% of worldwide Modified Operating Profit

• No additional cost for traditional employee defined benefit pension plans

New hire pension plan changed to a defined contribution plan; Legal Services Plan eliminated after 2013

• Maintained overall labor cost competitiveness with foreign transplants

~$51/hour all-in

• Ratification, performance, and quality / WCM bonuses

Ratification bonus of $3,500, 50% delayed until a financial milestone achieved

Performance and quality bonuses total $4,000 over contract period with 100% upside potential

New 4-year national labor agreement with UAW, maintaining Chrysler cost competitiveness and linking variable compensation directly to Company performance and product quality

October 28, 2011 Q3 2011 Results Review 23

Autos & LCVs Latin America – Business dynamics in Q3 „11

2

Fiat market leader for 39 consecutive quarters with share in line with FY expectations, maintaining price discipline in an increasingly competitive market

Passenger car share impacted by delay in customs clearance of Siena units from Argentina

Gap over nearest competitor of 140 bps (over 700 bps in LCVs)

Inventory levels at Sep-end in line with Q2 exit

Dealer stock at 24-days of supply

Market continuing to grow robustly over prior year (+32.2% in Q3)

Significant share gain in both passenger cars (+170 bps to 11.6%) & LCVs (+270 bps to 12.9%)

Continued strong performance of best selling products

Brazil: strong share in A/B segment, flat year-over-year at 28.0% with Novo Uno 39 bps higher than a year ago (40k shipments in the quarter)

Argentina: overall share up 190 bps to 11.9% on the back of robust performance in A/B & pick-up segments

Share gain of 200 bps to 15.1% in A/B segment with Novo Uno growing significantly quarter by quarter since market intro (+76% vs. Q1 2011)

Consolidating segment leadership of Strada (50% share, up 800 bps in Q3) with Double Cab version driving the increase (50% mix)

Successful launch of Fiat 500 & Freemont in September with very good initial reception

Both models imported from Mexico benefiting from FTA

Cost base for Fiat 500 now particularly competitive compared to model previously imported from Europe

Novo Palio commercially available in November

(presented on Oct 4th in Turkey)

26.2 26.3 24.4 24.5 23.7

21.9

10.5 10.4 10.7 10.1 10.0 11.9

MARKET SHARE (PASSENGER CARS & LCVS; %)

2007 2008 2010 2009

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q3 Q1 Q2 Q4 Q2

2011

Q3 Q4

2006

Q1 Q3

October 28, 2011 Q3 2011 Results Review 24

Flex/ Gas 1.0L

Flex 1.0-2.0L

Flex >2.0L

Gas 1.0-2.0L

Gas >2.0L

LCVs Trucks

7%

37%

11%

41%

18%

48%

25%

4%

34%

0%

30%

55%

13%

43%

Autos & LCVs Update on “Brazil Maior” tax regime

2

New Government tax measures increased IPI rates (Federal VAT) on imported vehicles by 30 p.p.

New IPI rates to enter into force in Dec 2011 (expiring year-end 2012)

Local production in Brazil and automotive imports from Mercosul & Mexico not be affected by new tax measures upon certain conditions

Minimum local content representing 65% of total net revenues of each company

Minimum of 0.5% of revenues invested in local R&D

Local manufacturing consisting of at least 6 out of 11 activities (i.e. assembling, painting, engine and transmission assembling…)

Before

After

Local

production

(tax exempted)

76%

Import

(tax

exempted) 14%

Imported

under new

taxation 10%

Under new tax regime, market weight of tax exempted imported vehicles expected to slightly increase from current levels

Prices for vehicles imported from non-Mexico & Mercosul countries expected to reflect tax increase

October 28, 2011 Q3 2011 Results Review 25

On sale in North American markets since early 2011

Produced in Mexico, now distributed through 123 dealers in US (increasing to 130+ by year-end 2011)

~30k shipments at Sep YTD

Run-rate target of 45-50k units annually

Fiat 500 & Fiat 500C already available in market, Abarth version on sale from 2012

Named candidate for “2012 North America Car of the Year”

Named “Top Safety Pick for 2011”

Launched in Brazil in September 2011

1.5k orders in just one month

FY 2011 target of ~8k units

An iconic, successful and multi-awarded product in Europe

A leading position in A-segment

More than 770k shipments since launch in 2007 (~440k outside of Italy)

~32k shipments in Q3 (~130k at Sep YTD)

On sale in China since Sep 2011

Imported from Mexico

Peak annual target of ~8k units

Autos & LCVs Fiat 500 around the world

2

October 28, 2011 Q3 2011 Results Review 26

3 Luxury & performance brands – Ferrari Quarterly margin sequentially improving in 2011

Shipments by region (%)

USA 31.3%

European Top-5 32.6%

China, Hong Kong & Taiwan

10.3%

Japan 3.2%

Others 22.5%

• Top-line of €525mn, up 17.7%

1,588 shipments, up 13.6% on the back of strong sales performance of 12-cylinder models, the new FF in particular

North America remaining #1 market (+1% vs. a year ago)

China, Hong Kong & Taiwan up 49% to 164 shipments

Notable performance in Germany (+93%), France (+54%) & Switzerland (+43%)

• Trading profit at €77mn, 14.7% margin

Trading profit holding up (+€1mn vs. a year ago) despite higher R&D spending for new products

Margin improvement of 80 bps from Q2 2011

FF (available in market since June)

458 Spider

(first ever mid-rear engine 8-cylinder, unveiled at Frankfurt Motor Show, sales starting November 2011)

October 28, 2011 Q3 2011 Results Review 27

Luxury & performance brands – Maserati Paving the way for the future

Shipments by region (%)

USA 38.9%

European Top-5 19.5%

China, Hong Kong & Taiwan

19.2%

Japan 4.5%

Others 17.0%

Brand new SUV Concept (Kubang)

(the first ever SUV in brand‟s history presented at Frankfurt Motor Show)

• Revenues up 6.0% to €142mn

1,459 shipments, up 6.7%

North America up 16%

China, Hong Kong & Taiwan up 2.4x last year levels

• Trading profit of €8mn, doubling over a year ago

Margin at 5.6%, a 260 bps improvement over Q3 ‟10

3

October 28, 2011 Q3 2011 Results Review 28

4

• Revenues up 7.1% to €1.4bn on the back of strong performance of Lighting and Electronic Systems

Growth across regions with Brazil, North America and China driving the increase

Improvement in Europe driven by Lighting (particularly to German customers) and LCVs

Sales to third-party customers remaining above 55%

• Trading profit at €43mn, margin at 3.1%

Increased sales volumes and manufacturing efficiencies more than offset cost pressures from higher materials prices

Margin up 130 bps vs. a year ago

Operational update

• Additional orders for €265mn taken in the quarter

Main contracts relating to German and French customers in Lighting and Electronic Systems

• JV established with Chinese automotive components maker Wanxiang Qianchao for production of shock absorbers

Electronic Systems

Powertrain

Exhaust Systems Suspension Systems

Plastic C. and M. Shock Absorbers

After Market

Magneti Marelli FY profitability target in sight

32%16%

12%40%

High-Tech business lines accounting for 60% of revenues

387

228

143

443

226

167

Automotive Lighting Powertrain Electronics

Q3 '10 Q3 '11

+14.5%

-(0.9)%

+16.8%

Revenues trend by business line (€mn)

October 28, 2011 Q3 2011 Results Review 29

• Start of production of 2.0 MultiJet for Ducato family in the quarter

A 115hp diesel engine embedding leading edge technology of MultiJet II to replace previous entry-level Euro4 100hp 2.2L

Reduced consumption and increased capacity at equal GVW

• CO2 emissions of just 169 g/km, 13% less than equivalent version with previous engine application

• Announced investment for a new gas engine for Alfa Romeo to reconnect the brand to its historical roots

A 1.8L 4-cyl direct injection turbo engine made entirely of aluminum with max output of 300hp, designed for both transversal and longitudinal applications

• Highly fuel efficient, compliant with future emissions standards in both Europe & US

Most advanced technological engine with features at the very best in its category and characteristic of Alfa Romeo engines

Start of production at Pratola Serra plant (Italy) beginning in early 2013

5 Fiat Powertrain Technology always to the forefront

• Revenues at €1.0bn, substantially in line with last year

Engines down 5.1% vs. prior year to 532k units

• Gas engines: volumes up +2% in Latin America more than offset by decline of Fire applications in Europe (-28%)

• Diesel engines: volumes holding up (+5%) driven by applications on Giulietta & LCVs

Transmissions in line with previous year at 526k units

• Trading profit at €29mn or €16mn less than a year ago mainly due to lower volumes and higher raw material cost

Margin at 2.9%

October 28, 2011 Q3 2011 Results Review 30

Revenues in excess of €58bn

Trading profit in excess of €2.1bn (revised from ~€2.1bn)

Net profit at ~€1.7bn

Capital expenditure of ~€5.5bn

Net industrial debt between ~€5.0 and ~5.5bn

Total available liquidity expected greater than €18bn

Outlook 6

APPENDIX

October 28, 2011 Q3 2011 Results Review 32

Q3 „11 Reported revenues & trading profit

Q3 „11 Q3 ‟10

Cons. Industrial Financial Cons. Industrial Financial

Revenues 17,552 17,481 98 8,444 8,390 71

of which

Automobiles 15,958 15,880 98 7,090 7,033 71

FGA 6,520 6,447 91 6,550 6,497 66

Chrysler 9,284 9,284 0 - - -

Ferrari 525 520 7 446 442 5

Maserati 142 142 0 134 134 0

Components 2,831 2,831 0 2,634 2,634 0

Others & Elim. (1,237) (1,230) 0 (1,280) (1,277) 0

Trading profit 851 829 22 256 238 18

of which

Automobiles 769 747 22 210 192 18

FGA 128 108 20 130 113 17

Chrysler 556 556 0 - - -

Ferrari 77 75 2 76 75 1

Maserati 8 8 0 4 4 0

Components 88 88 0 78 78 0

Others & Elim. (6) (6) 0 (32) (32) 0

(€mn)

October 28, 2011 Q3 2011 Results Review 33

Q3 „11 - Chrysler Net income reconciliation (from IFRS to US GAAP)

1) Under IFRS, development costs for vehicle project production are capitalized as intangible assets if the development costs can be measured reliably and the economic feasibility of the product support the view that the development expenditure will generate future economic benefits. Capitalized development costs include all direct and indirect costs that could be directly attributable to the development process. These costs are subsequently amortized to expense on a straight-line basis from the start of production over the estimated production cycle. Under US GAAP, with the exception of certain software development costs, development costs are expensed as incurred in accordance with ASC 730, Research and Development Costs

Three Months ended September 30, 2011

Four Months ended September 30, 2011

Euros USD Euros USD

Chrysler Net Income (Loss) - IFRS €

322 $

453 €

179 $

252

Reconciling Items:

Capitalization of development costs1)

(147)

(208)

(180)

(253)

Other

(25)

(33)

185

260

(172)

(241)

5

7

Chrysler Net Income - US GAAP €

150 $

212 €

184 $

259

October 28, 2011 Q3 2011 Results Review 34

Q3 „11 - Chrysler Net debt reconciliation (from IFRS to US GAAP)

September 30, 2011

Euros USD

Chrysler Net Debt - IFRS € 2,888 $ 3,899

Unamortized purchase accounting adjustments1) (563) (759)

Classification and other differences:

Accrued interest (202) (273)

Other 1 1

(201) (272)

Net Industrial Debt - US GAAP € 2,124 $ 2,868

1) In connection with the transaction, all financial liabilities were re-measured to their fair value as of the first date of consolidation. The unamortized balance primarily relates to the fair value adjustment on the VEBA Trust Note

October 28, 2011 Q3 2011 Results Review 35

Chrysler Group LLC Net revenues & trading profit

8,542

9,284

Q3 '10 Pro-forma Q3' 11

340

556

Q3 '10 Pro-forma Q3 '11

380

433407

382

485

514

469

Q1 '10 Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11

Vehicle Shipments (000)

• Net revenues up 8.8% (19% in US$ terms) driven primarily by increased demand for Chrysler Group‟s 16 all-new or significantly refreshed cars and trucks launched in 2010

• Revenue increase driven by 15% year-over-year increase in vehicle shipments and improved pricing and mix

• Shipments seasonally decreased from Q2 „11 due to model-year changeover

• Trading profit benefitted from increased shipments and improved pricing and mix, partially offset by increased advertising of new products and slightly higher industrial costs

October 28, 2011 Q3 2011 Results Review 36

Chrysler Group LLC Trading profit variance & margin

• Unadjusted volumes increased by 62k units on continued success of new and refreshed products

• Mix and net price improved primarily due to 2011 model year vehicle launches and increased US retail penetration

• Industrial costs primarily impacted by higher commodity and transportation costs, partially offset by lower depreciation & amortization

• SG&A primarily reflects increased advertising expenditures

(€mn)

340

556237

119

(15)

(95)(30)

Q3 '10

Pro-forma

Volume Mix & Net

Price

Industrial

Costs

SG&A Other Q3 '11*

4.0%

6.0%

October 28, 2011 Q3 2011 Results Review 37

123 132

151 152

55 66

74 87

15

4

17

Q3 '10 Q3 '11

301 331

50

58 18

18 34

45 4

17

Q3 '10 Q3 '11

U.S.

Canada

Mexico

Int‟l

Units (000s)

407 407

469

+30

+8

-0-

+11

2011 +/- 2010

+9

+11

+13

+15

2011 +/- 2010

+1

+15%

Contract Mfg +13 Contract Mfg +13

469

Chrysler Group LLC Q3 worldwide vehicle shipments

October 28, 2011 Q3 2011 Results Review 38

114 160

147

164

57

68 83

93

11

Q3 '10 Q3 '11

293

369

55

61

18

19

35

47

Q3 '10 Q3 '11

U.S.

Canada

Mexico

Int‟l

401 401

496 496

+76

+6

+1

+12

2011 +/- 2010

+46

+11

+11

+10

2011 +/- 2010

+17

+24%

Note – Excludes contract manufactured vehicles, primarily for Fiat (17k in Q3 2011 and 4k in Q3 2010)

Units (000s)

Chrysler Group LLC Q3 worldwide vehicle sales

October 28, 2011 Q3 2011 Results Review 39

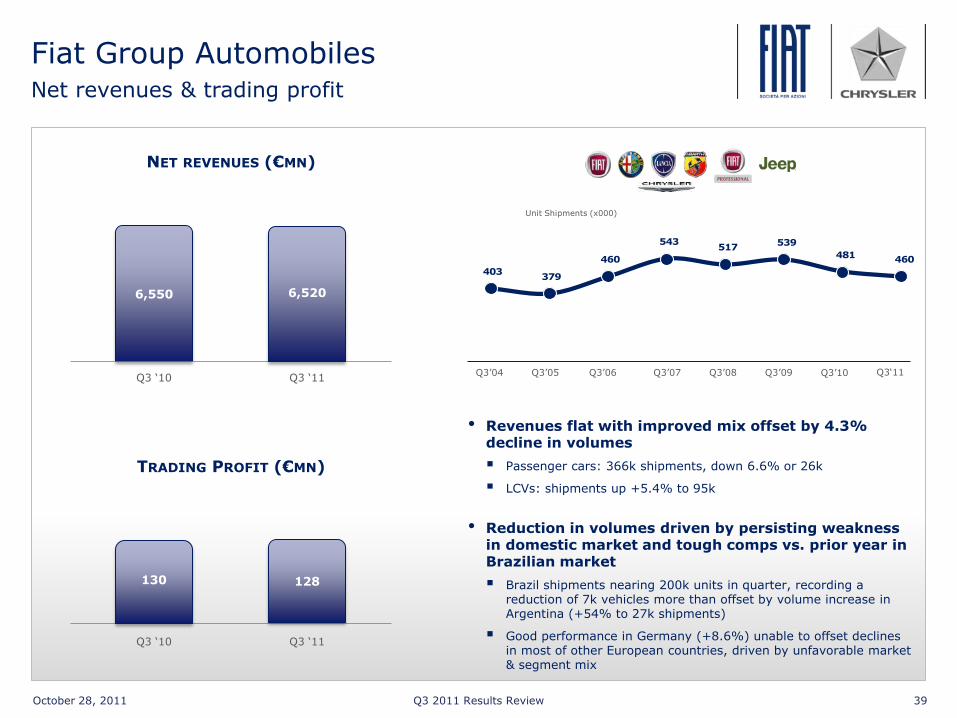

403 379

460

543 517

539

481 460

Q3‟04 Q3‟05 Q3‟06 Q3‟07 Q3‟08 Q3‟09 Q3‟10

Unit Shipments (x000)

NET REVENUES (€MN)

TRADING PROFIT (€MN)

6,550

Q3 „11 Q3 „10

Q3 „10 Q3 „11

130

6,520

128

Q3„11

Fiat Group Automobiles Net revenues & trading profit

• Revenues flat with improved mix offset by 4.3% decline in volumes

Passenger cars: 366k shipments, down 6.6% or 26k

LCVs: shipments up +5.4% to 95k

• Reduction in volumes driven by persisting weakness in domestic market and tough comps vs. prior year in Brazilian market

Brazil shipments nearing 200k units in quarter, recording a reduction of 7k vehicles more than offset by volume increase in Argentina (+54% to 27k shipments)

Good performance in Germany (+8.6%) unable to offset declines in most of other European countries, driven by unfavorable market & segment mix

October 28, 2011 Q3 2011 Results Review 40

Fiat Group Automobiles Trading profit variance & margin

(€mn)

Q3 ‟10 Volume Price & Mix

Purchasing Net

Production Cost

Absorp.

SG&A R&D Q3 „11 Other

• Excluding 5k Jeeps increase, overall shipments down ~26k units

• Improved mix from LCVs & first full quarter of sales for Fiat Freemont & New Lancia Ypsilon partially offset by competitive pressure on existing products in EU

• Purchasing & WCM efficiencies on track to FY target

• R&D spending in line with cadence of new products

• SG&A driven by higher advertising due to launches in EU

• Other mainly relates to FX translation

(28)

130 2

128

2.0% 2.0%

10

14

(23)

18

5

October 28, 2011 Q3 2011 Results Review 41

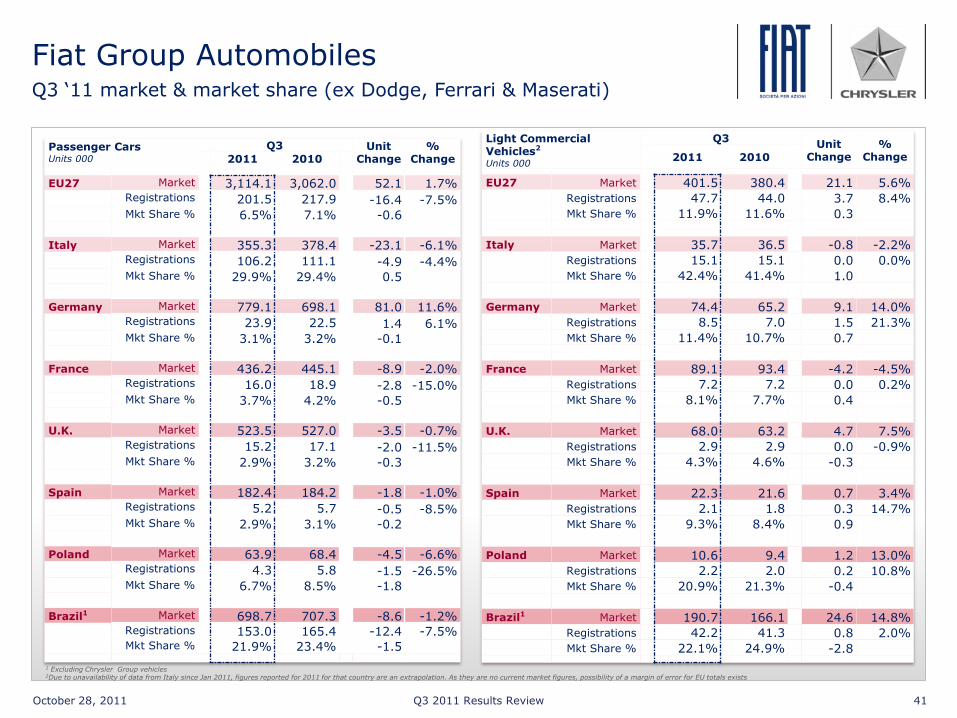

1 Excluding Chrysler Group vehicles 2Due to unavailability of data from Italy since Jan 2011, figures reported for 2011 for that country are an extrapolation. As they are no current market figures, possibility of a margin of error for EU totals exists

Fiat Group Automobiles Q3 „11 market & market share (ex Dodge, Ferrari & Maserati)

Passenger Cars Units 000

Q3 Unit Change

% Change 2011 2010

EU27 Market 3,114.1 3,062.0 52.1 1.7%

Registrations 201.5 217.9 -16.4 -7.5%

Mkt Share % 6.5% 7.1% -0.6

Italy Market 355.3 378.4 -23.1 -6.1%

Registrations 106.2 111.1 -4.9 -4.4%

Mkt Share % 29.9% 29.4% 0.5

Germany Market 779.1 698.1 81.0 11.6%

Registrations 23.9 22.5 1.4 6.1%

Mkt Share % 3.1% 3.2% -0.1

France Market 436.2 445.1 -8.9 -2.0%

Registrations 16.0 18.9 -2.8 -15.0%

Mkt Share % 3.7% 4.2% -0.5

U.K. Market 523.5 527.0 -3.5 -0.7%

Registrations 15.2 17.1 -2.0 -11.5%

Mkt Share % 2.9% 3.2% -0.3

Spain Market 182.4 184.2 -1.8 -1.0%

Registrations 5.2 5.7 -0.5 -8.5%

Mkt Share % 2.9% 3.1% -0.2

Poland Market 63.9 68.4 -4.5 -6.6%

Registrations 4.3 5.8 -1.5 -26.5%

Mkt Share % 6.7% 8.5% -1.8

Brazil1 Market 698.7 707.3 -8.6 -1.2%

Registrations 153.0 165.4 -12.4 -7.5%

Mkt Share % 21.9% 23.4% -1.5

Light Commercial Vehicles2 Units 000

Q3 Unit

Change %

Change 2011 2010

EU27 Market 401.5 380.4 21.1 5.6%

Registrations 47.7 44.0 3.7 8.4%

Mkt Share % 11.9% 11.6% 0.3

Italy Market 35.7 36.5 -0.8 -2.2%

Registrations 15.1 15.1 0.0 0.0%

Mkt Share % 42.4% 41.4% 1.0

Germany Market 74.4 65.2 9.1 14.0%

Registrations 8.5 7.0 1.5 21.3%

Mkt Share % 11.4% 10.7% 0.7

France Market 89.1 93.4 -4.2 -4.5%

Registrations 7.2 7.2 0.0 0.2%

Mkt Share % 8.1% 7.7% 0.4

U.K. Market 68.0 63.2 4.7 7.5%

Registrations 2.9 2.9 0.0 -0.9%

Mkt Share % 4.3% 4.6% -0.3

Spain Market 22.3 21.6 0.7 3.4%

Registrations 2.1 1.8 0.3 14.7%

Mkt Share % 9.3% 8.4% 0.9

Poland Market 10.6 9.4 1.2 13.0%

Registrations 2.2 2.0 0.2 10.8%

Mkt Share % 20.9% 21.3% -0.4

Brazil1 Market 190.7 166.1 24.6 14.8%

Registrations 42.2 41.3 0.8 2.0%

Mkt Share % 22.1% 24.9% -2.8

October 28, 2011 Q3 2011 Results Review 42

Fiat Group Automobiles Sep YTD 2011 market & market share (ex Dodge, Ferrari & Maserati)

1 Excluding Chrysler Group vehicles 2Due to unavailability of data from Italy since Jan 2011, figures reported for 2011 for that country are an extrapolation. As they are no current market figures, possibility of a margin of error for EU totals exists

Passenger Cars Units 000

YTD Sep Unit Change

% Change 2011 2010

EU27 Market 10,462.7 10,547.2 -84.5 -0.8%

Registrations 742.5 835.7 -93.2 -11.2%

Mkt Share % 7.1% 7.9% -0.8

Italy Market 1,369.5 1,543.8 -174.2 -11.3%

Registrations 406.8 474.4 -67.6 -14.2%

Mkt Share % 29.7% 30.7% -1.0

Germany Market 2,401.7 2,166.9 234.9 10.8%

Registrations 78.2 72.5 5.7 7.9%

Mkt Share % 3.3% 3.3% 0.0

France Market 1,661.3 1,657.5 3.8 0.2%

Registrations 62.1 69.5 -7.3 -10.6%

Mkt Share % 3.7% 4.2% -0.5

U.K. Market 1,553.1 1,635.7 -82.6 -5.0%

Registrations 46.1 52.8 -6.6 -12.6%

Mkt Share % 3.0% 3.2% -0.2

Spain Market 623.9 787.2 -163.3 -20.7%

Registrations 19.5 26.1 -6.6 -25.2%

Mkt Share % 3.1% 3.3% -0.2

Poland Market 202.6 215.5 -12.9 -6.0%

Registrations 15.1 19.2 -4.1 -21.4%

Mkt Share % 7.4% 8.9% -1.5

Brazil1 Market 2,002.4 1,915.1 87.3 4.6%

Registrations 442.9 441.7 1.1 0.3%

Mkt Share % 22.1% 23.1% -1.0

Light Commercial Vehicles2 Units 000

YTD Sep Unit

Change %

Change 2011 2010

EU27 Market 1,335.2 1,235.6 99.6 8.1%

Registrations 174.9 161.0 13.9 8.6%

Mkt Share % 13.1% 13.0% 0.1

Italy Market 137.4 138.2 -0.7 -0.5%

Registrations 62.1 61.7 0.4 0.7%

Mkt Share % 45.2% 44.6% 0.6

Germany Market 230.4 198.7 31.7 15.9%

Registrations 29.7 22.7 7.0 31.1%

Mkt Share % 12.9% 11.4% 1.5

France Market 318.3 312.0 6.2 2.0%

Registrations 30.0 27.9 2.1 7.7%

Mkt Share % 9.4% 8.9% 0.5

U.K. Market 204.1 175.1 29.0 16.6%

Registrations 7.9 6.9 1.0 14.0%

Mkt Share % 3.9% 4.0% -0.1

Spain Market 78.8 86.9 -8.1 -9.3%

Registrations 7.3 7.4 -0.2 -2.2%

Mkt Share % 9.2% 8.6% 0.6

Poland Market 31.3 27.9 3.3 11.9%

Registrations 6.3 6.3 0.0 0.7%

Mkt Share % 20.2% 22.4% -2.2

Brazil1 Market 525.4 454.5 70.9 15.6%

Registrations 119.3 106.9 12.3 11.5%

Mkt Share % 22.7% 23.5% -0.8

October 28, 2011 Q3 2011 Results Review 43

204 197

112104

127

115

39

44

Q3 '10 Q3 '11

(3.4)%

(7.0)%

(9.4)%

14.8%

357383

377 331

279289

74 84

H1 '10 H1 '11

Brazil

Italy

EU27 ex

Italy

RoW

- (4.3)%

7.4%

(12.2)%

3.5%

1,087 481

460

560 580

489 435

406404

113129

Sep YTD '10 Sep YTD '11

3.5%

(11.0)%

(0.5)%

(1.3)%

13.9%

1,568 1,087

* Incl. shipments w/buyback, Chrysler Group shipments in Europe, ex JVs and Ferrari & Maserati

13.5%

1,547

Fiat Group Automobiles Worldwide unit shipments by region, Cars & LCVs (unit/000)*

Brazil

Italy

EU27 ex Italy

RoW

October 28, 2011 Q3 2011 Results Review 44

90 95

272026

341 306

28

27

Q3 '10 Q3 '11

194 218

11357

53

784 726

5177

H1 '10 H1 '11

- (4.3)%

1,087 481

460

284 313

3197779

1,125 1,032

79104

YTD Sep '10 YTD Sep '11

(1.3)%

1,568 1,087 1,547

12.5%

(6.2)%

(7.4)%

51.1%

13x

5.4%

(9.8)%

(3.5)%

26.7%

3.5x

10.2%

2.5%

(8.3)%

31.6%

6.3x

Fiat Group Automobiles Worldwide unit shipments by brand, Cars & LCVs (unit/000)*

* Incl. shipments w/buyback, Chrysler Group shipments in Europe, ex JVs and Ferrari & Maserati

October 28, 2011 Q3 2011 Results Review 45

521521

468527

556612

556 592 600665

542

402465

582 541 582 543 583506 515 549 591

483

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Production & Purchases

(„000 units)

2006

509530

469502

569600

537571

591631

532

463

525

630

557565

580

545500

517527

562 484

485516

460

520

541

579

543

571

564

645

517

428

465

591

539556 532

554

481514 519

568

460

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Registrations Shipments

Registrations & Shipments

Fiat Group Automobiles Worldwide production volumes, shipments & registrations

2007 2008 2009 2010 2011

October 28, 2011 Q3 2011 Results Review 46

Fiat Group Automobiles Inventory trend by quarter

• Total inventory flat compared to previous quarter

• Company inventory slightly increasing due to stock in transit from Argentina to Brazil (delay in customs clearance)

Months of Supply (as per average of latest 3 months)

Company Inventory

Dealer Inventory

2008

2.5

1.4

1.92.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2009 2010 2011

October 28, 2011 Q3 2011 Results Review 47

Components Teksid & Comau

197

Q3 „10 Q3 2011

229

Q3 „10 Q3 2011

12

Q3 „10 Q3 2011

254

371

Q3 „10 Q3 2011

• Revenues up 16.2%

Cast Iron up 14.6% driven by positive performance in Mercosur, NAFTA & Europe

• Trading profit up 33.3% primarily on volume increases

• Revenues up 46%

All business lines up with Body Welding and Powertrain Systems and activities in China making a significant contribution

• Trading profit of €4mn, attributable to Body Welding operations and activities in China

• Order intake of €256mn for the quarter, up 5.3% vs. a year ago

4

-0- 9

October 28, 2011 Q3 2011 Results Review 48

Fiat ex Chrysler Net debt breakdown (€bn)

Note: Numbers may not add due to rounding

June 30, „11

Sept 30, „11

Cons. Ind. Fin. Cons. Ind. Fin.

16.4 13.4 3.1 Gross Debt* 17.0 13.9 3.1

(0.4) (0.4) - Derivatives M-to-M, Net (0.1) (0.1) -

(12.2) (12.0) (0.2) Cash & Mktable Securities (11.1) (10.9) (0.2)

3.8 1.0 2.9 Net Debt 5.8 2.9

2.9

* Net of intersegment receivables

October 28, 2011 Q3 2011 Results Review 49

Fiat ex Chrysler Gross debt (€bn)

Note: Numbers may not add due to rounding

Outstanding June 30, „11

Outstanding Sept 30, „11

15.7 Cash Maturities 16.1

5.5 Bank Debt 4.6 8.8 Capital Market (1) 10.2 1.4 Other Debt 1.4

0.7 Securitization and Sale of Receivables (on

book) 0.7

0.0 ABS / Securitization 0.0 0.0 Warehouse Facilities 0.0 0.7 Sale of Receivables 0.7

0.1 Adjust. for Hedge Accounting on Fin.

Payables 0.2

16.4 Gross Debt 17.0

(12.2) Cash & Mktable Securities (11.1)

(0.4) Derivatives Fair Value (0.1)

3.8 Net Debt 5.8

0.0 Undrawn committed credit lines 1.8

(1) Excluding fair value of Bonds, including interest accruals

October 28, 2011 Q3 2011 Results Review 50

Chrysler Gross debt (€bn)

Note: Numbers may not add due to rounding

Outstanding Jun 30, „11

Outstanding Sep 30, „11

9.4 Cash Maturities (1) 9.9

2.5 Bank Debt 2.6

2.2 Capital Market 2.4

4.7 Other Debt 4.9

0.1 Securitization and Sale of Receivables

(on book) 0.0

0.1 ABS / Securitization 0.0

9.5 Gross Debt 9.9

(7.0) Cash & Mktable Securities (7.0)

(0.0) Derivatives Fair Value (0.0)

2.4 Net Debt 2.9

0.9 Undrawn committed credit lines 1.0

(1) Including accrued Interest

October 28, 2011 Q3 2011 Results Review 51

Financial charges breakdown Q3 „11 vs. Q3 „10

Average Outstanding

(€bn)

Rate/Spread

(%)

Net Charges (€mn)

2010 2011 Chg

Net Industrial Debt Q3 2011 (2.3) 5.8% (33) +18

Net Industrial Debt Q3 ‟10 (4.5) 4.5% (51)

“Cost of Carry” Q3 2011 (11.4) 3.5% (100) -65

“Cost of Carry” Q3 ‟10 (1) (6.7) 2.0% (35)

Equity Swap (related to stock option plans) 58 (138) -196

IAS 19 (interest cost on pension & OPEB) (12) (10) +2

Others

(indirect Taxes on banking transactions, fees, FX, interest cost on long-term provisions, discount of certain receivables...)

13 (53) -66

NET FINANCIAL CHARGES (Fiat) (27) (334) -307

Chrysler Group - (209) -209

NET FINANCIAL CHARGES (Fiat w/ Chrysler) (27) (543) -516

(1) Net of cash deposited by Fiat Industrial

October 28, 2011 Q3 2011 Results Review 52

Safe Harbor Statement

Cer ta i n i n fo rmat i on i n c l uded i n t h i s

p resen ta t i on , i n c l ud i ng , w i t hou t l im i ta t i on ,

any f o recas t s i n c l uded here i n , i s f o rwa rd

l ook i ng and i s sub j ec t t o impor tan t r i sks and

uncer t a i n t i es t ha t cou l d cause ac tua l resu l t s

t o d i f f e r ma te r i a l l y . The Group ‟ s bus i nesses

i nc l ude i t s au tomot i ve , au tomot i ve- re l a t ed and

o ther sec t o rs , and i t s ou t l ook i s p redominan t l y

based on i t s i n t e rp re ta t i on o f what i t

cons i de rs t o be the key economi c f a c t o r s

a f f ec t i ng these bus i nesses . Fo rward - l ook i ng

s t a t emen t s w i th rega rd t o t he Group ' s

bus i nesses i nvo l ve a number o f impor tan t

fa c t o r s t ha t a re sub j ec t t o change , i n c l ud i ng ,

bu t no t l im i t ed t o: t he many i n t e r re l a t ed

fa c to r s t ha t a f f ec t consumer con f i dence and

wor l dw ide demand fo r au tomot i ve and

au tomot i ve - re l a t ed p roduc t s ; governmen ta l

p rog rams; genera l economi c cond i t i ons i n each

o f t he Group ' s marke t s ; l eg i s l a t i on ,

pa r t i cu l a r l y t ha t re l a t i ng t o au tomot i ve-

re l a t ed i s sues , t he env i ronmen t , t rade and

commerce and i n f ra s t ru c tu re deve l opmen t ;

a c t i ons o f compet i t o r s i n t he va r i ous

i ndus t r i es i n wh i ch the Group competes ;

produc t i on d i f f i cu l t i e s , i n c l ud i ng capac i ty and

supp l y cons t ra i n t s and excess i nven to ry

l eve l s ; l abo r re l a t i ons ; i n t e res t ra t es and

cu r rency exchange ra t es ; po l i t i ca l and c i v i l

un res t ; ea r thquakes and o ther r i sks and

uncer t a i n t i es . Any o f the assumpt i ons

under l y i ng t h i s p resen ta t i on o r any o f the

c i r cumstances o r da ta men t i oned i n t h i s

p resen ta t i on may change . Any f o rward - l ook i ng

s t a t emen t s con ta i ned i n t h i s p resen ta t i on

speak on l y a s o f t he da te o f t h i s p resen ta t i on .

F i a t does assume and exp ress l y d i s c l a ims any

ob l i ga t i on t o upda te t hese f o rward - l ook i ng

s t a t emen t s . F i a t does no t a ssume and

express l y d i s c l a ims any l i ab i l i t y i n connec t i on

w i th any i naccu rac i es i n any o f t hese f o rward -

l ook i ng s ta t emen t s o r i n connec t i on w i t h any

u se by any th i rd par t y o f su ch f o rward - l ook i ng

s ta temen t s . Th i s p resen ta t i on does no t

rep resen t i nves tmen t adv i ce o r a

recommenda t i on f o r t he pu rchase o r sa l e o f

f i nanc i a l p roduc t s and/o r o f any k i nd o f

f i nanc i a l se rv i ces . F i na l l y , t h i s p resen ta t i on

does no t rep resen t an i nves tmen t so l i c i t a t i on

i n I t a l y , pu rsuan t t o Sec t i on 1 , l e t t e r ( t ) o f

Leg i s l a t i ve Dec ree no . 58 o f Februa ry 24 ,

1998 , a s amended, nor does i t r ep resen t a

s im i l a r so l i c i t a t i on a s con temp la ted by the

l aws i n any other count ry or s ta te .

October 28, 2011 Q3 2011 Results Review 53

Contacts

Marco Auriemma +39-011-006-3290 Vice President

Alexandra Deschner +39-011-006-2308

Paolo Mosole +39-011-006-1064

Sara Nicola +39-011-006-2572

Maristella Borotto +39-011-006-2709

fax: +39-011-006-3796

email: [email protected]

website: www.fiatspa.com