Embed Size (px)

Citation preview

On the Determinants of Corporate Social

Responsibility: International Evidence

on the Financial Industry

Hsiang-Lin ChihHsiang-Hsuan Chih

Tzu-Yin Chen

ABSTRACT. This article sets out to undertake a thor-

ough, point-by-point examination of the theory postu-

lated by Campbell (2007), in which an attempt is made to

specify the conditions under which corporations may or

may not act in socially responsible ways. In order to ensure

the overall reliability of our study, and to attempt to pro-

vide a new understanding of, and greater insights into,

whether corporate social responsibility (CSR) is affected

by financial and institutional variables, we empirically

investigate a total of 520 financial firms in 34 countries,

between the years 2003 and 2005. Our empirical findings

are: (i) firms with larger size are more CSR minded, and

the financial performance and CSR are not related; (ii)

firms would actually act in more socially responsible ways

to enhance their competitive advantages when the market

competitiveness is more intense; (iii) financial firms in

countries with stronger levels of legal enforcement tend to

engage in more CSR activities; however, interestingly and

rather strikingly, those firms in countries with stronger

shareholder rights tend to engage in less CSR activities; and

(iv) self-regulation within the financial industry has a sig-

nificantly positive effect on CSR, with firms being found

to act in more socially responsible ways in those countries

which have more cooperative employer–employee rela-

tions, higher quality management schools, and a better

macroeconomic environment.

KEY WORDS: corporate social responsibility (CSR),

Dow Jones Sustainability Index, institutional theory,

investor protection, legal enforcement

Introduction

In light of the accounting scandal at Enron, the recent

Wall Street’s crisis and the Madoff scandal, consid-

erable commentary has begun to attribute such fraud

to what is now being referred to as ‘‘a decay in

business morality’’ (New York Times, 2002) and to

interpret ‘‘we don’t just need a financial bailout; we

need an ethical bailout. We need to re-establish the

core balance between our markets, ethics, and reg-

ulations’’ (New York Times, 2008).1 Such criticism

goes some way explaining why leading speakers on

public opinion, among consumers, investors, and

commerce, in general, have begun to advocate a duty

of enterprise leaders not to gear their businesses to-

ward the pursuit of pure profit at the expense of

fulfilling their obligations to their employees, to the

environment, and to society as a whole.2

Hsiang-Lin Chih is the Chairperson and Professor of Depart-

ment of Banking and Cooperative Management at National

Taipei University, Taiwan. His current research focuses on

corporate social responsibility, corporate governance, and

financial institutions management. His writings have

appeared in Journal of Quantitative and Financial

Analysis, Journal of Banking and Finance, Corporate

Governance: An International Review, Journal of

Business Ethics, Academia Economic Papers and in

other journals. He received his Ph.D. from the National

Taiwan University in 1998.

Hsiang-Hsuan Chih is currently the Associate Professor of

Department of Finance in National Dong Hwa University in

Taiwan. Her current research focuses on corporate finance,

behavioral finance and corporate governance. Her recent

publications include Journal of Management, Review of

Securities and Futures Markets, and Review of

Financial Risk Management. She received her Ph.D.

degree from National Central University in 2003.

Tzu-Yin Chen is a research assistant for the Department of

Banking and Cooperative Management at National Taipei

University, Taiwan. Her research focuses on corporate social

responsibility and financial institutions management. She

received her master degree from the Department of

Cooperative Economics, College of Business, National

Taipei University, Taiwan.

Journal of Business Ethics (2010) 93:115–135 � Springer 2009DOI 10.1007/s10551-009-0186-x

Although extensive research has already been

undertaken in this particular area, the related studies

have typically tended to focus on the relationship

existing between corporate social responsibility

(CSR) and financial performance (Coombs and

Gilley, 2005; Griffin and Mahon, 1997; Hillman and

Keim, 2001; McWilliams and Siegel, 2000, 2001;

Pava and Krausz, 1996; Roberts and Dowling, 2002;

Rowley and Berman, 2000; Simpson and Kohers,

2002; Waddock and Graves, 1997; Walsh et al.,

2003). As such, little theoretical attention has thus far

been placed on trying to gain a better understanding

of whether or not, and if so why, corporations act in

socially responsible ways (Campbell, 2007).3

Margolis and Walsh (2003) have shown them-

selves to be highly critical of the extant literature for

its tendency to ignore several factors, other than

corporate financial performance, which may well

affect CSR; and indeed, there are now growing calls

among other researchers (for example, Walsh et al.,

2003) for much more serious theoretical inquiry into

this issue. A prime example of such calls is provided

by the study of Campbell (2007), which offers an

institutional theory on CSR comprising a series of

propositions specifying the conditions under which

corporations are more (or less) likely to behave in

socially responsible ways.

The conditions proposed by Campbell include

the general financial condition of the firm, the health

of the economy, the level of competition faced by a

corporation (see also Shleifer, 2004), and certain

institutional factors, including public and/or private

regulations, the presence of non-governmental and

other independent organizations, institutionalized

norms, associative behavior among corporations, and

organized dialog between corporations and their

stakeholders.

The primary aim of this article is to empirically

investigate whether or not, and if so why, corpora-

tions will tend to act in socially responsible ways. In an

attempt to ensure the overall reliability of our study,

we employ cross-country data so as to provide a firm

understanding of, and greater insights into, whether

CSR is affected by firm- and country-level variables.

Furthermore, our study also attempts to investigate

the determinants of socially responsible corporate

behavior from various global dimensions, including

firm-specific financial characteristics, regulations,

institutions, and macroeconomic conditions.

In order to effectively measure the degree of CSR

across firms and countries, we take as our CSR

firms, constituent companies of the Dow Jones

Sustainability World Index (DJSI World), an index

which is compiled as a result of cooperation between

the Dow Jones Indexes, STOXX Limited, and the

SAM.4 In order to qualify for inclusion in the DJSI

World Index, companies must be in the top 10% of

the largest 2,500 companies in the Dow Jones World

Index, in terms of three socially responsible dimen-

sions: economic, environmental, and social.

The economic dimension comprises four criteria:

corporate governance, risk and crisis management,

codes of conduct/compliance/corruption and bribery,

and industry-specific criteria. The environmental

dimension comprises three criteria: environmental

performance (eco-efficiency), environmental report-

ing, and industry-specific criteria. The social dimen-

sion comprises six criteria: human capital development,

talent attraction and retention, labor practice indicators,

corporate citizenship/philanthropy, social reporting,

and industry-specific criteria.5

The financial firms extracted from these 2,500

companies listed on the Dow Jones World Index are

classified into two groups: the CSR Group, which

includes the financial firms that are listed in the DJSI

World, and the non-CSR Group, which includes

those firms that are not listed in the DJSI World.6

The remainder of this article is organized as

follows. An explanation of the Campbell (2007)

propositions specifying the determinants of CSR is

provided in ‘‘Determinants of CSR section,’’ along

with the selection of the appropriate measures to

proxy for these determinants. An explanation on the

empirical models used in this study is provided in

‘‘Econometric model’’ section, followed in ‘‘Data and

descriptive statistics’’ section, by a summary of the

data and the descriptive statistics. A discussion of the

empirical results is undertaken in ‘‘Empirical results’’

section, with ‘‘Conclusions’’ section presenting the

conclusions drawn from this study.

Determinants of CSR

Campbell (2007) offers a comprehensive institutional

theory on CSR comprising a series of propositions

specifying the conditions under which corporations

are likely to behave in socially responsible ways. The

116 Hsiang-Lin Chih et al.

focus of this section, based on Campbell (2007), is

placed on providing an explanation of the determi-

nants of CSR and proposing appropriate measures to

proxy for these determinants in our empirical study.

Financial performance and economic environment

Campbell (2007) proposes that since firms that are less

profitable have fewer resources to spare for socially

responsible activities than those firms that are more

profitable, ‘‘Corporations will be less likely to act in

socially responsible ways where they are currently

experiencing relatively weak financial performance’’

(Waddock and Graves, 1997). It therefore follows

that firm’s profitability is expected to be positively

related to their level of CSR; thus, we use return on

assets (ROA), obtained from the Compustat Global

Vantage database, to measure the profitability among

our cross-country sample of firms. Firm size is also

used as a control variable, since larger firms are subject

to closer scrutiny by the public, thereby raising the

likelihood of such firms acting in more socially

responsible ways (Dierkes and Coppock, 1978;

Fombrun and Shanley, 1990; Trotman and Bradley,

1981).

As to the economic environment, Campbell

(2007) argues that ‘‘Corporations will be less likely

to act in socially responsible ways where they are

operating in a relatively unhealthy economic envi-

ronment where the possibility for near-term profit-

ability is limited.’’ An example of this would be

circumstances of high inflation, low productivity

growth, and weak consumer confidence, a situation

in which it would seem relatively difficult for firms

to achieve healthy near-term profits; under such

circumstances, firms would arguably be less likely to

behave in socially responsible ways (Campbell,

2007). We therefore adopt the Inflation Rate (INF),

the Industrial Production Index (IPI), and the

Consumer Confidence Index (CCI) as the economic

environment variables for our sample countries.

The INF is taken from the World Development

Index; the IPI, which is obtained from the International

Financial Statistics, represents the state of production

within the industrial sector at a given period of time,

as compared to a reference point in time, with a

higher score indicating greater production within the

industrial sector; the CCI is taken from ACNielsen,

which undertakes regular surveys on consumer

confidence for local markets, with a higher score

indicating stronger consumer confidence.

Competition

‘‘Corporations will be less likely to act in socially

responsible ways if there is either too much, or

too little competition; that is, the relationship

between competition and socially responsible cor-

porate behavior will be curvilinear’’ (Campbell,

2007). Campbell’s proposition here is that in cir-

cumstances where there is extremely intensive competi-

tion, corporations are likely to act in socially irresponsible

ways to save money, since their profit margins will already

be sufficiently narrow as to put shareholder value at risk

(Campbell, 2007; Shleifer, 2004).

However, at the other extreme, in situations

where competition is virtually non-existent, a cor-

poration may also have little interest in using

philanthropic measures to enhance its ‘‘competitive

advantage’’ (Porter and Kramer, 2002) or to improve

its long-term financial performance, since its stake-

holders (for example, its customers and suppliers)

have very few alternatives (Campbell, 2007).

In order to estimate the extent of competitiveness

and to indicate the structure of the banking systems

across our sample countries, we obtain the com-

petitiveness measure, H-statistics – taken directly

from Chih and Cheng (2008) in which the Panzar

and Rosse (1987) and Claessens and Laeven (2004)

methodologies are applied – to estimate the degree

of competitiveness across the banking systems of 61

countries, with a higher value indicating greater

competitiveness.

Legal environment

Campbell (2007) suggests that ‘‘Corporations will be

more likely to act in socially responsible ways if there

are strong and well-enforced state regulations in

place to ensure such behavior, particularly if the

process by which these regulations and enforcement

capacities were developed was based upon negotia-

tion and consensus building among corporations,

government and the other relevant stakeholders.’’

According to Leuz et al. (2003), legal systems can

117On the Determinants of Corporate Social Responsibility

protect outside investors by conferring on them the

right to discipline insiders (for example, to replace

managers), and also through the enforcement of

contracts designed to limit the private control ben-

efits of insiders.

As a result, legal systems, which effectively protect

outside investors, reduce the incentives for insiders

to act in irresponsible ways, such as engaging in the

manipulation or obfuscation of a firm’s earnings to

conceal their own rent-seeking behavior. We

therefore use the Shareholder Rights and Legal

Enforcement indices as proxies for the legal envi-

ronment across our sample countries. The former

index, which is based on La Porta et al. (1998), is an

aggregate measure of (minority) Shareholder Rights,

comprising (i) the country allows shareholders to

mail their proxy vote to the firm, (ii) shareholders

are not required to deposit their shares prior to the

general shareholders’ meeting, (iii) cumulative vot-

ing or proportional representation of minorities in

the board of directors is allowed, (iv) an oppressed

minorities mechanism is in place, (v) the minimum

percentage of share capital that entitles a shareholder

to call for an extraordinary shareholders’ meeting is

less than or equal to 10%, or (vi) shareholders have

preemptive rights that can be waived only by a

shareholders’ vote. The index ranges from 0 to 6,

with a higher score indicating higher Shareholder

Rights. The latter index, also adopted by La Porta

et al. (1998), measures the mean score across three

legal variables for each country, comprising: (i) the

efficiency of the judicial system; (ii) an assessment of

the rule of law; and (iii) the corruption index. All

three variables range from 0 to 10, with a higher

score indicating a better legal enforcement.

We also consider the origin of the legal system of

each country, comprising English, French, German,

or Scandinavian legal origins, essentially because our

results may suffer from endogeneity bias if CSR,

Shareholder Rights and Legal Enforcement are

simultaneously determined. We address this concern

by regarding the legal origins of the countries as legal

environment variables, since a country’s legal origin

can be considered as predetermined and exogenous

(Leuz et al., 2003). La Porta et al. (1998) reported

that the strongest measures for the legal protection of

investors were generally found in English common

law countries, while German and Scandinavian civil

law countries provided medium-level protection,

and French civil law countries demonstrated the

weakest levels of protection.

Private regulation and the presence of independent

organizations

Campbell (2007) further proposes that ‘‘Corpora-

tions will be more likely to act in socially responsible

ways if there is a system of well organized and

effective industrial self-regulation in place to ensure

such behavior, particularly if it is based upon the

perceived threat of state intervention or broader

industrial crisis, and if the state provides support for

this form of industrial governance’’ and also, that

‘‘Corporations will be more likely to act in socially

responsible ways if there are private, independent

organizations, including NGOs, social movement

organizations, institutional investors, and the press,

in their environment, who monitor their behavior

and, when necessary, mobilize to change it.’’

In order to identify appropriate measures to proxy

for industrial self-regulation or the presence of

independent organizations, we consider two kinds of

principles, the Equator and Wolfsberg’s principles.

The Equator Principles were developed as a result of

cooperation between 59 financial institutions and

the International Finance Corporation (IFC) of the

World Bank Group, while the Wolfsberg Principles

were developed by the Wolfsberg Group, an asso-

ciation of 12 global banks, in conjunction with

Transparency International. An important criterion

in the adoption of these principles is that if a financial

firm adopts either the Equator or the Wolfsberg

Principles, it will be required to act in socially

responsible ways and to engage in sound environ-

mental management practices.7,8

Business education environment

Campbell (2007) notes that ‘‘Corporations will be

more likely to act in socially responsible ways if they

operate in an environment where normative calls for

such behavior are institutionalized, for example, in

important business publications, business school

curricula, and other educational venues in which

corporate managers participate.’’ In order to measure

the soundness of the business educational environ-

118 Hsiang-Lin Chih et al.

ment across countries, we use the Quality of Man-

agement Schools Index, taken from the Global

Competitiveness Report of the World Economic For-

um, with a higher score indicating a higher quality

management school.

Employer–employee relations

Campbell (2007) also suggests that ‘‘Corporations will

be more likely to act in socially responsible ways if

they belong to trade or employers associations, but

only if these associations are organized in ways that

promote socially responsible behavior’’ and that

‘‘Corporations will be more likely to act in socially

responsible ways if they are engaged in institutional-

ized dialog with unions, employees, community

groups, investors and other stakeholders.’’ In order

to test these propositions, we use the Cooperation

in Labor–Employer Relations Index, which is also

taken from the Global Competitiveness Report, as an

explanatory variable in our regression models. The

scores range from 1 to 7, with a higher score

indicating higher cooperative employer–employee

relations.

Econometric model

In this section, we test the extent to which financial

characteristics and institutional variables have an

impact on the likelihood of firms engaging in CSR.

We first of all classify the financial firms from the

largest 2,500 companies included in the Dow Jones

World Index into two groups, the CSR Group,

which includes the financial firms listed on the DJSI

World, and the non-CSR Group, which includes

those firms that are not listed on the DJSI World.

Equation 1 then tests the relationship between CSR

and its determinants, as follows:

CSRi;j;t ¼ a0 þ a1ROAi;j;t þ a2TAi;j;t þ a3Hj

þ a4H2j þ a5LAWj þ a6QMSj;t

þ a7CLERj;t þ a8REGj;t þ a9INFj;t

þ a10IPIj;t þ a11CCIj þ ei;j;t; ð1Þ

where CSRi,j,t is a dummy variable for sample firm

i of country j at year t, which takes the value of 1

if the firm belongs to the CSR Group and 0 if the

firm belongs to the non-CSR Group9; ROAi,j,t

the return on assets for sample firm i of country j

at year t; TAi,j,t the total assets for sample firm i of

country j at year t; and Hj the H-statistics (obtained

from Chih and Cheng, 2008), which measure the

degree of competitiveness in the financial industry

of country j, with a higher value indicating greater

competitiveness.10 LAWj comprises three kinds of

law variables for country j, the legal origin, the

Shareholder Rights index and the Legal Enforcement

index. The legal origin for country j, which is

taken from La Porta et al. (1998), is a set of dum-

mies (French, German, and Scandinavian, with

English as the omitted dummy). The Shareholder

Rights index for country j, which is also taken

from La Porta et al. (1998), ranges from 0 to 6,

with a higher score indicating enhanced share-

holder rights. The Legal Enforcement index for

country j, which was again used by La Porta et al.

(1998), ranges from 0 to 10, with a higher score

indicating better legal enforcement.

QMSj,t, the Quality Of Management Schools for

country j at year t, which ranges from 1 to 7, is taken

from the Global Competitiveness Report of the World

Economic Forum, with a higher score indicating a

higher quality management school; ‘‘cooperative

employer–employee relations’’ for country j at year t

(CLERj,t), ranging from 1 to 7, is the Cooperation in

Labor–Employer Relations Index taken from the

Global Competitiveness Report, with a higher score

indicating better cooperative employer–employee

relations.11 REGi comprises two types of industry

self-regulatory measures for firm i, ‘‘Equator Princi-

ples’’ and ‘‘Wolfsberg Principles,’’ which are dummy

valuables taking the value of 1 if the firm adopts either

Equator or Wolfsberg Principles, and 0 if the firm

does not adopt either of these principles; the INF for

country j at year t (INFj,t) is taken from the World

Development Index of the World Bank.

IPIj,t, the Industrial Production Index for country

j at year t, is taken from the International Financial

Statistics of the International Monetary Fund, with a

higher score indicating greater production within the

industrial sector. CCIj, the Consumer Confidence

Index for country j, is taken from ACNielsen, with a

higher score indicating stronger consumerconfidence.

ei,j,t is the error term at year t.

119On the Determinants of Corporate Social Responsibility

Data and descriptive statistics

Data sources

We begin by searching through the sample countries

for the names of the financial firms included in the

largest 2,500 companies listed on the Dow Jones

World Index and on the DJSI World. The former is

provided by the Dow Jones Company, while the

latter is provided by the Dow Jones Indices,

STOXX Limited and the SAM Group.12

The constituents that appear in the DJSI World

index are classified as ‘‘CSR firms,’’ while those

appearing in the Dow Jones World, but not in the DJSI

World index, are referred to as ‘‘non-CSR’’ firms. We

screen the Compustat Global Vantage database for

these firms to obtain the required financial data cov-

ering the years 2003–2005. Our search, based upon

these criteria, provided a final sample of 520 financial

firms in 34 countries for the period under examination,

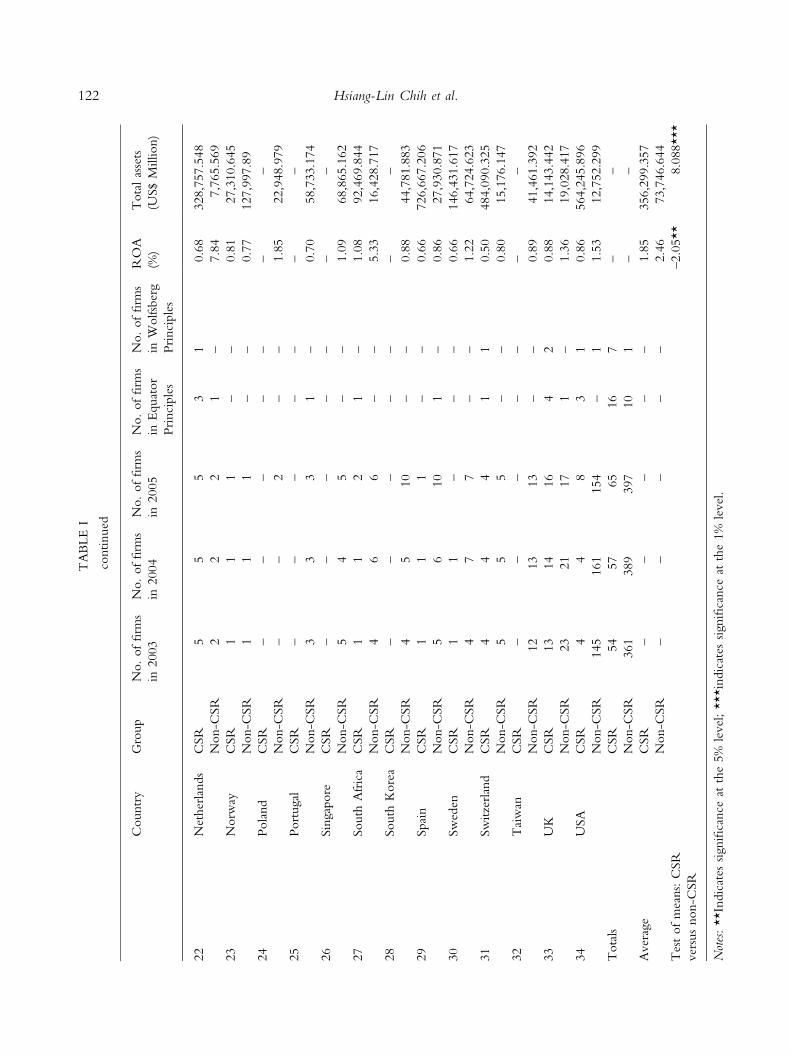

giving a total of 1,323 firm years (Table I).

Descriptive statistics

As shown in Table I, the respective numbers of CSR

and non-CSR financial firms in our sample are 176

(54 + 57 + 65) and 1,141 (361 + 389 + 397). The

first column shows the names of the 34 sample

countries, while the third to fifth columns report the

number of sample firms included in the DJSI World

index for each country and for each of the sample

years. In 2005, for example, the countries with the

highest number of financial firms in the DJSI World

index were the UK (16), the US (8), and Australia (7),

while 19 sample countries had no financial firms in the

index.13 The last two columns in Table I present the

average profitability (ROA) and asset size of the CSR

and non-CSR financial firms for each country; based

upon the test of the means, before taking other insti-

tutional factors into account, CSR-minded financial

firms are found to be larger in size (t = 8.088) and

have poorer financial performance (t = -2.051).

Details on the basic H-statistics, Quality of Man-

agement Schools, and cooperation in employer–em-

ployee relations are presented in Table II. The highest

H-statistics are found in Taiwan (0.961), Hong Kong

(0.938), and the Netherlands (0.880); conversely, the

three countries with the lowest H-statistics are Spain

TA

BLE

I

Des

crip

tive

stat

istics

of

CSR

and

firm

-spec

ific

var

iable

sof

finan

cial

firm

sac

ross

34

countr

ies

Countr

yG

roup

No.

of

firm

s

in2003

No.

of

firm

s

in2004

No.

of

firm

s

in2005

No.

of

firm

s

inE

quat

or

Pri

nci

ple

s

No.

of

firm

s

inW

olfsb

erg

Pri

nci

ple

s

RO

A

(%)

Tota

las

sets

(US$

Million)

1A

ust

ralia

CSR

67

71

–4.5

414,1

62.3

69

Non-C

SR

12

14

14

––

3.3

09,1

01.4

24

2A

ust

ria

CSR

––

––

––

–

Non-C

SR

22

3–

–0.5

4136,6

42.3

17

3B

elgiu

mC

SR

11

11

–4.9

924,7

06.9

73

Non-C

SR

–2

2–

–6.7

77,5

83.6

25

4B

razi

lC

SR

21

11

–2.1

852,2

42.2

4

Non-C

SR

–1

21

–2.1

65,0

804.3

07

5C

anad

aC

SR

22

21

–0.5

5295,5

43.2

79

Non-C

SR

15

16

17

3–

1.1

080,8

96.6

08

120 Hsiang-Lin Chih et al.

TA

BLE

I

continued

Countr

yG

roup

No.

of

firm

s

in2003

No.

of

firm

s

in2004

No.

of

firm

s

in2005

No.

of

firm

s

inE

quat

or

Pri

nci

ple

s

No.

of

firm

s

inW

olfsb

erg

Pri

nci

ple

s

RO

A

(%)

Tota

las

sets

(US$

Million)

6C

hile

CSR

––

––

––

–

Non-C

SR

31

1–

–3.8

611,2

81.0

22

7C

ypru

sC

SR

––

––

––

–

Non-C

SR

1–

–0.5

926,2

63.7

53

8C

zech

Rep

ublic

CSR

––

––

––

–

Non-C

SR

1–

–1.7

920,9

10.4

00

9D

emar

kC

SR

––

––

––

–

Non-C

SR

33

4–

–1.0

620,5

18.1

44

10

Fin

land

CSR

––

––

––

–

Non-C

SR

11

2–

–1.6

640,1

92.0

83

11

Fra

nce

CSR

23

4–

–1.1

2253,9

68.3

32

Non-C

SR

97

7–

–0.5

6135,0

57.9

57

12

Ger

man

yC

SR

44

5–

10.3

3651,7

31.8

29

Non-C

SR

55

5–

–0.6

0108623.2

76

13

Gre

ece

CSR

––

––

––

–

Non-C

SR

44

5–

–0.8

444,5

14.1

90

14

Hong

Kong

CSR

––

––

––

–

Non-C

SR

10

11

11

––

4.5

014,5

32.7

55

15

Hungar

yC

SR

––

––

––

–

Non-C

SR

1–

–

16

Indones

iaC

SR

––

––

––

–

Non-C

SR

21

1–

–2.1

518,0

37.3

17

17

Irel

and

CSR

––

––

––

–

Non-C

SR

33

3–

–0.9

162,7

40.0

18

18

Ital

yC

SR

23

3–

–0.6

0194,9

78.7

29

Non-C

SR

13

12

12

1–

0.6

156,7

79.0

36

19

Japan

CSR

55

5–

–0.5

755,2

11.5

40

Non-C

SR

60

66

66

1–

0.4

036,2

13.4

18

20

Mal

aysia

CSR

––

––

––

–

Non-C

SR

44

3–

–1.2

222,0

37.4

09

21

Mex

ico

CSR

––

––

––

–

Non-C

SR

22

3–

–2.7

512,5

78.0

68

121On the Determinants of Corporate Social Responsibility

TA

BLE

I

continued

Countr

yG

roup

No.

of

firm

s

in2003

No.

of

firm

s

in2004

No.

of

firm

s

in2005

No.

of

firm

s

inE

quat

or

Pri

nci

ple

s

No.

of

firm

s

inW

olfsb

erg

Pri

nci

ple

s

RO

A

(%)

Tota

las

sets

(US$

Million)

22

Net

her

lands

CSR

55

53

10.6

8328,7

57.5

48

Non-C

SR

22

21

–7.8

47,7

65.5

69

23

Norw

ayC

SR

11

1–

–0.8

127,3

10.6

45

Non-C

SR

11

1–

–0.7

7127,9

97.8

9

24

Pola

nd

CSR

––

––

––

–

Non-C

SR

––

2–

–1.8

522,9

48.9

79

25

Port

ugal

CSR

––

––

––

–

Non-C

SR

33

31

–0.7

058,7

33.1

74

26

Sin

gap

ore

CSR

––

––

––

–

Non-C

SR

54

5–

–1.0

968,8

65.1

62

27

South

Afr

ica

CSR

11

21

–1.0

892,4

69.8

44

Non-C

SR

46

6–

–5.3

316,4

28.7

17

28

South

Kore

aC

SR

––

––

––

–

Non-C

SR

45

10

––

0.8

844,7

81.8

83

29

Spai

nC

SR

11

1–

–0.6

6726,6

67.2

06

Non-C

SR

56

10

1–

0.8

627,9

30.8

71

30

Sw

eden

CSR

11

––

–0.6

6146,4

31.6

17

Non-C

SR

47

7–

–1.2

264,7

24.6

23

31

Sw

itze

rlan

dC

SR

44

41

10.5

0484,0

90.3

25

Non-C

SR

55

5–

–0.8

015,1

76.1

47

32

Tai

wan

CSR

––

––

––

–

Non-C

SR

12

13

13

––

0.8

941,4

61.3

92

33

UK

CSR

13

14

16

42

0.8

814,1

43.4

42

Non-C

SR

23

21

17

1–

1.3

619,0

28.4

17

34

USA

CSR

44

83

10.8

6564,2

45.8

96

Non-C

SR

145

161

154

–1

1.5

312,7

52.2

99

Tota

lsC

SR

54

57

65

16

7–

–

Non-C

SR

361

389

397

10

1–

–

Aver

age

CSR

––

––

–1.8

5356,2

99.3

57

Non-C

SR

––

––

–2.4

673,7

46.6

44

Tes

tof

mea

ns:

CSR

ver

sus

non-C

SR

–2.0

5**

8.0

88***

Not

es:

**In

dic

ates

signifi

cance

atth

e5%

level

;***in

dic

ates

signifi

cance

atth

e1%

level

.

122 Hsiang-Lin Chih et al.

TABLE II

Descriptive statistics of the institutional variables across 34 countries

Country H-statisticsa Quality of management

schoolsb (average, 2003–2005)

Cooperation in labor–employer

relationsc (average, 2003–2005)

1 Australia 0.60 6.22 3.27

2 Austria 0.52 5.42 5.77

3 Belgium 0.54 5.98 2.79

4 Brazil 0.68 4.06 3.33

5 Canada 0.39 8.52 3.34

6 Chile 0.32 6.58 4.42

7 Cyprus – 2.86 3.69

8 Czech Republic 0.54 4.46 4.00

9 Demark 0.30 6.29 7.49

10 Finland 0.41 6.59 4.78

11 France 0.42 7.03 2.41

12 Germany 0.67 6.29 3.79

13 Greece 0.41 3.19 3.18

14 Hong Kong 0.94 4.17 6.80

15 Hungary 0.36 4.27 3.85

16 Indonesia 0.59 3.41 3.08

17 Ireland 0.28 4.85 3.57

18 Italy 0.62 3.77 2.74

19 Japan 0.24 3.28 6.35

20 Malaysia 0.86 3.98 6.15

21 Mexico 0.61 4.09 3.82

22 Netherlands 0.88 6.59 6.16

23 Norway 0.34 6.06 5.66

24 Poland 0.71 4.00 3.46

25 Portugal 0.78 4.95 3.57

26 Singapore 0.49 6.28 8.63

27 South Africa 0.48 5.99 2.76

28 South Korea 0.61 3.45 2.56

29 Spain 0.02 6.82 3.79

30 Sweden 0.21 7.72 6.11

31 Switzerland 0.59 7.36 7.02

32 Taiwan 0.96 4.94 5.79

33 UK 0.54 7.81 5.42

34 USA 0.57 8.34 4.39

Average 0.53 5.46 4.53

SD 0.22 1.60 1.61

Notes: aThe H-statistics are taken from Chih and Cheng (2008), with a higher value indicating a more competitive

financial environment.b‘‘Quality of Management Schools’’ scores, ranging from 1 to 7, are taken from the Global Competitiveness Report of the

World Economic Forum, with a higher score indicating a higher quality of management school; we normalize the scores

across management schools, per country per year, using the mean divided by the standard deviation, and thus the

normalized scores range from 2.86 to 8.52.c‘‘Cooperation in Labor Employer Relations’’ scores, ranging from 1 to 7, are also taken from the Global Competitiveness

Report, with a higher score indicating better cooperative relations; we normalize the scores across firms, per country per

year, using the mean divided by the standard deviation, and thus the normalized scores range from 2.41 to 8.63.

123On the Determinants of Corporate Social Responsibility

(0.019), Sweden (0.211), and Japan (0.240), suggesting

lower competitiveness levels in the financial industries

of these countries. The top three countries with the

highest quality of management schools are Canada

(8.524), the US (8.342), and the UK (7.810), while

those countries which demonstrate the most cooper-

ative employer–employee relations are Singapore

(8.625), Denmark (7.494), and Switzerland (7.023).

As shown in Table III, along with Switzerland, the

two Scandinavian countries of Norway and Denmark

clearly have the highest scores on investor protection

among all countries, followed by other European

countries, including the UK, Germany, France, and

the Netherlands, as well as the US and Canada.

Norway and Denmark also have the highest con-

sumer confidence levels. In contrast, Latin American

and some Asian countries have weaker scores for

investor protection and higher INFs.

Empirical results

The results of the estimations on the determinants of

CSR are provided in Table IV, which presents eight

model specifications each with a different combi-

nation of explanatory variables. The first four model

specifications consider the Equator Principles, while

the subsequent four specifications take into account

the Wolfsberg Principles. We add the square terms

of the H-statistics into specification (B), (D), (F), and

(H) to investigate whether the relationship between

competition and socially responsible corporate

behavior is curvilinear.

As shown in Table IV, the coefficients of ROA

are overwhelmingly positive and significant, indi-

cating that financial firms achieving better financial

performance will act in more socially responsible

ways, consistent with Campbell (2007); total assets

are also found to have a positive correlation with

CSR, indicating that larger firms, which are natu-

rally subject to closer scrutiny by the public, will act

in more socially responsible ways.

The results for the remaining explanatory variables

are also interesting. First, the H-statistic coefficients

are significantly positive, while the H-statistics2 coef-

ficients are significantly negative, which, consistent

with Campbell (2007), implies that firms will be less

likely to act in socially responsible ways if there is

either too much, or too little, competition.

Second, financial firms in countries with French

and German legal origins are more CSR minded,

while those firms in countries with stronger legal

enforcement levels engage in more CSR activities.

However, interestingly, and rather strikingly, the

coefficients of Shareholder Rights are overwhelm-

ingly negative and significant, which suggests that

financial firms in countries with stronger Share-

holder Rights will tend to be geared toward share-

holders’ welfare at the expense of fulfilling their

obligations to other stakeholders.

Third, significantly positive coefficients are found

for the Quality of Management Schools Index (QMS)

and the Cooperation in Labor–Employer Relations

Index (CLER) in some of the specifications, which

suggests that financial firms will act in more socially

responsible ways in countries with better quality

management schools and where there are more

cooperative employer–employee relations; this is again

consistent with the findings of Campbell (2007). Those

firms in countries with well-organized and effective

private regulations, as well as the presence of inde-

pendent organizations, will tend to be more CSR-

minded, consistent with Campbell (2007), since the

coefficients of both the Equator and Wolfsberg Prin-

ciples are significantly positive across all specifications.

Finally, the coefficients of the INF are signifi-

cantly negative in specification (A), while the coef-

ficients of the CCI are all significantly positive –

with the exception of specification (H) – which

implies that financial firms in countries with higher

consumer confidence levels and lower INFs will act

in more socially responsible ways, again providing

support for the Campbell (2007) propositions.

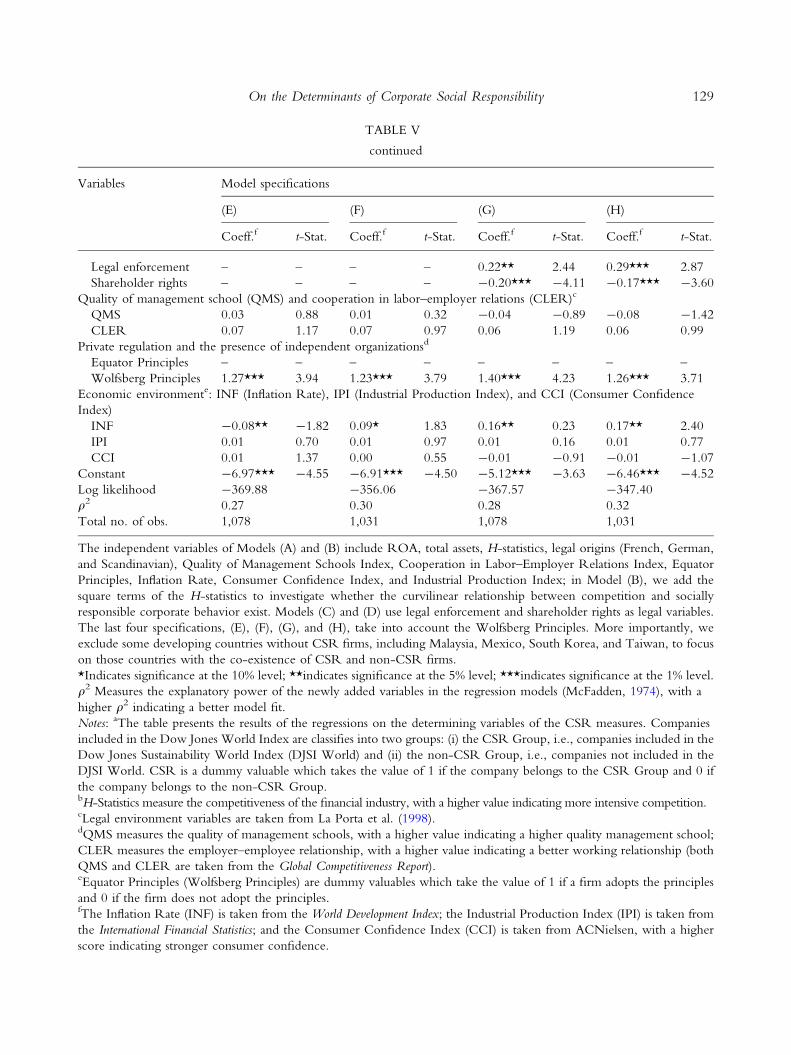

However, in order for the robustness check, two

additional settings are taken into account. First, since

most of the competitive markets are in the devel-

oping countries, such as Malaysia, Mexico, South

Korea, and Taiwan (as shown in Table II), and none

of them have CSR companies (as shown in Table I),

which is the possible shortcomings of the DJSI-

biased selection procedure as shown in ‘‘Notes’’ no.

13, it is worthwhile to focus on those countries with

the co-existence of CSR and non-CSR firms, and

check if the results are consistent with those in

Table IV. We exclude developing countries without

CSR firms, including Malaysia, Mexico, South

Korea, and Taiwan, and we find, as shown in

Table V, most of the empirical results are the same as

124 Hsiang-Lin Chih et al.

TABLE III

Descriptive statistics of the legal and macroeconomic variables across 34 Countries

Country Legal

origina

Legal

enforcementbShareholder

rightscInflationd (%) IPIe

(2000 = 100)

CCIf

1 Australia Eng 9.51 4 3.34 – 117

2 Austria Ger 9.36 2 1.84 111.74 –

3 Belgium Fr 9.44 – 2.12 102.80 100

4 Brazil Fr 6.13 3 2.50 – 93

5 Canada Eng 9.75 5 3.14 99.87 110

6 Chile Fr 6.52 5 5.89 – 102

7 Cyprus – – – – 110.70 –

8 Czech Republic – – – 0.05 134.04 97

9 Demark Sc 10.00 2 2.04 102.69 119

10 Finland Sc 10.00 3 0.86 106.78 99

11 France Fr 8.68 3 1.53 101.29 77

12 Germany Ger 9.05 1 0.52 102.74 89

13 Greece Fr 6.82 2 2.39 99.66 87

14 Hong Kong Eng 8.91 5 3.40 – 106

15 Hungary – – – 2.47 129.95 90

16 Indonesia Fr 2.87 2 8.18 – 104

17 Ireland Eng 8.36 4 2.73 124.95 112

18 Italy Fr 5.74 1 2.70 96.23 89

19 Japan Ger 9.17 4 2.26 99.18 76

20 Malaysia Eng 7.72 4 4.75 120.17 114

21 Mexico Fr 5.37 1 7.13 99.53 98

22 Netherlands Fr 10.00 2 1.86 101.38 96

23 Norway Sc 10.00 4 4.46 96.45 120

24 Poland – – – 1.64 129.94 103

25 Portugal Fr 7.19 3 2.67 100.97 60

26 Singapore Eng 8.93 4 1.83 – 103

27 South Africa Eng 6.45 5 5.01 – 102

28 South Korea Ger 5.55 2 5.63 124.97 62

29 Spain Fr 7.14 4 4.15 101.31 101

30 Sweden Sc 10.00 3 1.38 106.03 93

31 Switzerland Ger 10.00 2 0.65 97.94 98

32 Taiwan Ger 7.37 2 1.40 115.34 80

33 UK Eng 9.22 5 2.48 96.21 99

34 USA Eng 9.54 5 2.41 100.25 103

Average 8.16 3.07 2.89 107.86 96.84

SD 1.83 1.44 1.86 11.72 14.43

Notes: aDetails on the legal origins, indicated by English (Eng), French (Fr), German (Ger) or Scandinavian (Sc), are taken from La Porta

et al. (1998).bThe Legal Enforcement Index, as used in La Porta et al. (1998), ranges from 0 to 10, with a higher score indicating a better legal

enforcement.cThe Shareholder Rights Index, ranging from 0 to 6, is also taken from La Porta et al. (1998), with a higher score indicating enhanced

shareholder rights.dInflation Rates are taken from the World Development Index of the World Bank.eThe Industry Product Index (IPI) is taken from the International Financial Statistics, with a higher score indicating greater production

levels within the industrial sector.fThe Consumer Confidence Index (CCI) is obtained from ACNielsen, with a higher score indicating stronger consumer confidence.

125On the Determinants of Corporate Social Responsibility

TABLE IV

Determinants of corporate social responsibility

Variables Model specifications

(A) (B) (C) (D)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Financial performance

ROA 0.03** 2.40 0.04*** 2.82 0.03** 2.18 0.04** 2.48

Total assets 0.26*** 6.53 0.27*** 6.54 0.25*** 6.37 0.26*** 6.47

Competitiona

H-statistics 0.13 0.59 5.03*** 4.50 -0.03 -0.13 3.09** 2.19

H-statistics2 – – -4.75*** -4.84 – – -3.04** -2.49

Legal environmentb

French 0.82*** 4.45 1.16*** 5.90 – – – –

German 0.66*** 2.91 0.93*** 4.10 – – – –

Scandinavian -0.06 -0.18 0.10 0.30 – – – –

Legal enforcement – – – – 0.12 1.57 0.11 1.37

Shareholder rights – – – – -0.22*** -4.24 -0.24*** -4.53

Quality of management school (QMS) and cooperation in labor–employer relations (CLER)c

QMS 0.07** 1.97 0.06* 1.67 0.05 1.32 0.03 0.83

CLER 0.04 0.78 0.10** 2.03 0.00 0.03 0.04 0.84

Private regulation and the presence of independent organizationsd

Equator Principles 0.57*** 3.20 0.56*** 3.11 0.62*** 3.45 0.62*** 3.40

Wolfsberg Principles – – – – – – – –

Economic environmente: INF (Inflation Rate), IPI (Industrial Production Index), and CCI (Consumer Confidence

Index)

INF -0.08* -1.78 -0.04 -0.80 0.01 0.12 0.02 0.41

IPI 0.00 0.18 -0.00 -0.11 -0.00 -0.35 -0.00 -0.35

CCI 0.03*** 3.81 0.03*** 4.13 0.01** 2.09 0.01* 1.75

Constant -7.49*** -5.67 -9.11*** -6.89 -5.18*** -4.73 -5.74*** -5.01

Log likelihood -380.23 -372.00 -380.19 -376.63

q2 0.27 0.28 0.27 0.27

Total no. of obs. 1,149 1,149 1,149 1,149

Variables Model specifications

(E) (F) (G) (H)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Financial performance

ROA 0.03** 2.28 0.04*** 2.72 0.03** 2.05 0.03** 2.36

Total assets 0.26*** 6.49 0.26*** 6.54 0.25*** 6.39 0.25*** 6.52

Competitiona

H-statistics 0.17 0.78 5.65*** 5.63 0.08 0.36 4.12*** 3.39

H-statistics2 – – -5.24*** -5.77 – – -3.84*** -3.58

Legal environmentb

French 0.80*** 4.22 1.13*** 5.63 – – – –

German 0.58** 2.49 0.87*** 3.71 – – – –

Scandinavian -0.05 -0.18 0.13 0.42 – – – –

126 Hsiang-Lin Chih et al.

TABLE IV

continued

Variables Model specifications

(E) (F) (G) (H)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Legal enforcement – – – – 0.14* 1.77 0.14* 1.71

Shareholder rights – – – – -0.22*** -4.08 -0.24*** –4.39

Quality of management school (QMS) and cooperation in labor–employer relations (CLER)c

QMS 0.06* 1.82 0.05 1.47 0.04 1.18 0.02 0.51

CLER 0.02 0.36 0.08* 1.69 -0.03 -0.60 0.02 0.38

Private regulation and the presence of independent organizationsd

Equator Principles – – – – – – – –

Wolfsberg Principles 1.18*** 3.96 1.25*** 3.96 1.28*** 4.25 1.39*** 4.11

Economic environmente: INF (Inflation Rate), IPI (Industrial Production Index), and CCI (Consumer Confidence

Index)

INF -0.08* -1.82 -0.04 -0.84 0.01 0.23 0.03 0.57

IPI 0.01 0.70 0.00 0.46 0.00 0.16 0.00 0.25

CCI 0.03*** 3.56 0.03*** 3.91 0.01** 1.97 0.01 1.51

Constant -7.54*** -5.72 -9.33** -7.00 -5.50*** -5.16 -6.35*** -5.68

Log likelihood -377.86 -368.71 -376.96 -372.09

q2 0.27 0.29 0.27 0.28

Total no. of obs. 1,149 1,149 1,149 1,149

The independent variables of Models (A) and (B) include ROA, total assets, H-statistics, legal origins (French, German,

and Scandinavian), Quality of Management Schools Index, Cooperation in Labor–Employer Relations Index, Equator

Principles, Inflation Rate, Consumer Confidence Index, and Industrial Production Index; in Model (B), we add the

square terms of the H-statistics to investigate whether the curvilinear relationship between competition and socially

responsible corporate behavior exist. Models (C) and (D) use legal enforcement and shareholder rights as legal variables.

The last four specifications, (E), (F), (G), and (H), take into account the Wolfsberg Principles.

*Indicates significance at the 10% level; **indicates significance at the 5% level; ***indicates significance at the 1% level.

q2 Measures the explanatory power of the newly added variables in the regression models (McFadden, 1974), with a

higher q2 indicating a better model fit.

Notes: aThe table presents the results of the regressions on the determining variables of the CSR measures. Companies

included in the Dow Jones World Index are classified into two groups: (i) the CSR Group, i.e., companies included in the

Dow Jones Sustainability World Index (DJSI World) and (ii) the non-CSR Group, i.e., companies not included in the

DJSI World. CSR is a dummy valuable which takes the value of 1 if the company belongs to the CSR Group and 0 if

the company belongs to the non-CSR Group.bH-Statistics measure the competitiveness of the financial industry, with a higher value indicating more intensive com-

petition.cLegal environment variables are taken from La Porta et al. (1998).dQMS measures the quality of management schools, with a higher value indicating a higher quality management school;

CLER measures the employer–employee relationship, with a higher value indicating a better working relationship (both

QMS and CLER are taken from the Global Competitiveness Report).eEquator Principles (Wolfsberg Principles) are dummy valuables which take the value of 1 if a firm adopts the principles

and 0 if the firm does not adopt the principles.fThe Inflation Rate (INF) is taken from the World Development Index; the Industrial Production Index (IPI) is taken from

the International Financial Statistics; and the Consumer Confidence Index (CCI) is taken from ACNielsen, with a higher

score indicating stronger consumer confidence.

127On the Determinants of Corporate Social Responsibility

TABLE V

Determinants of corporate social responsibility: controlling the possible shortcomings of the DJSI-biased selection pro-

cedure

Variables Model specifications

(A) (B) (C) (D)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Financial performance

ROA 0.02 1.26 0.02 1.09 0.01 0.81 0.02 1.06

Total assets 0.25*** 6.10 0.26*** 6.13 0.24*** 5.98 0.26*** 6.30

Competitiona

H-statistics 1.13*** 3.90 1.19*** 3.83 0.68** 2.21 0.74** 2.24

H-statistics2 – – 0.40*** 3.26 – – 0.50*** 3.82

Legal environmentb

French 0.63*** 3.06 0.39* 1.81 – – – –

German 1.03*** 4.59 0.67*** 2.69 – – – –

Scandinavian 0.19 0.60 0.34 0.67 – – – –

Legal enforcement – – – – 0.19** 2.28 0.27*** 2.78

Shareholder rights – – – – -0.20*** -4.38 -0.18*** -3.80

Quality of management school (QMS) and cooperation in labor–employer relations (CLER)c

QMS 0.04 0.96 0.01 0.35 -0.04 -0.75 -0.07 -1.30

CLER 0.09 1.62 0.09 1.40 0.09* 1.77 0.09 1.50

Private regulation and the presence of independent organizationsd

Equator Principles 0.56*** 3.09 0.51*** 2.80 0.58*** 3.13 0.46** 2.50

Wolfsberg Principles – – – – – – – –

Economic environmente: INF (Inflation Rate), IPI (Industrial Production Index), and CCI (Consumer Confidence

Index)

INF 0.13** 2.48 0.10** 2.11 0.16*** 2.68 0.17*** 2.61

IPI 0.00 0.41 0.01 0.74 0.00 0.33 0.01 0.57

CCI 0.01 1.56 0.00 0.76 -0.01 -0.71 -0.01 -0.90

Constant -7.11*** -4.72 -7.06*** -4.66 -5.12*** -3.66 -6.44*** -4.48

Log likelihood -372.78 -359.19 -372.25 -351.48

q2 0.27 0.29 0.27 0.31

Total no. of obs. 1,078 1,031 1,078 1,031

Variables Model specifications

(E) (F) (G) (H)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Financial performance

ROA 0.02 1.74 0.02 1.00 0.01 0.68 0.02 0.90

Total assets 0.24*** 6.06 0.25*** 6.05 0.23*** 5.92 0.25*** 6.22

Competitiona

H-statistics 1.23*** 4.46 1.27*** 4.25 0.84*** 2.94 0.88*** 2.84

H-statistics2 – – 0.42*** 3.38 – – 0.51*** 3.81

Legal environmentb

French 0.61*** 2.88 0.36 1.63 – – – –

German 0.96*** 4.12 0.60** 2.34 – – – –

Scandinavian 0.24 0.75 0.44 0.88 – – – –

128 Hsiang-Lin Chih et al.

TABLE V

continued

Variables Model specifications

(E) (F) (G) (H)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Legal enforcement – – – – 0.22** 2.44 0.29*** 2.87

Shareholder rights – – – – -0.20*** -4.11 -0.17*** -3.60

Quality of management school (QMS) and cooperation in labor–employer relations (CLER)c

QMS 0.03 0.88 0.01 0.32 -0.04 -0.89 -0.08 -1.42

CLER 0.07 1.17 0.07 0.97 0.06 1.19 0.06 0.99

Private regulation and the presence of independent organizationsd

Equator Principles – – – – – – – –

Wolfsberg Principles 1.27*** 3.94 1.23*** 3.79 1.40*** 4.23 1.26*** 3.71

Economic environmente: INF (Inflation Rate), IPI (Industrial Production Index), and CCI (Consumer Confidence

Index)

INF -0.08** -1.82 0.09* 1.83 0.16** 0.23 0.17** 2.40

IPI 0.01 0.70 0.01 0.97 0.01 0.16 0.01 0.77

CCI 0.01 1.37 0.00 0.55 -0.01 -0.91 -0.01 -1.07

Constant -6.97*** -4.55 -6.91*** -4.50 -5.12*** -3.63 -6.46*** -4.52

Log likelihood -369.88 -356.06 -367.57 -347.40

q2 0.27 0.30 0.28 0.32

Total no. of obs. 1,078 1,031 1,078 1,031

The independent variables of Models (A) and (B) include ROA, total assets, H-statistics, legal origins (French, German,

and Scandinavian), Quality of Management Schools Index, Cooperation in Labor–Employer Relations Index, Equator

Principles, Inflation Rate, Consumer Confidence Index, and Industrial Production Index; in Model (B), we add the

square terms of the H-statistics to investigate whether the curvilinear relationship between competition and socially

responsible corporate behavior exist. Models (C) and (D) use legal enforcement and shareholder rights as legal variables.

The last four specifications, (E), (F), (G), and (H), take into account the Wolfsberg Principles. More importantly, we

exclude some developing countries without CSR firms, including Malaysia, Mexico, South Korea, and Taiwan, to focus

on those countries with the co-existence of CSR and non-CSR firms.

*Indicates significance at the 10% level; **indicates significance at the 5% level; ***indicates significance at the 1% level.

q2 Measures the explanatory power of the newly added variables in the regression models (McFadden, 1974), with a

higher q2 indicating a better model fit.

Notes: aThe table presents the results of the regressions on the determining variables of the CSR measures. Companies

included in the Dow Jones World Index are classifies into two groups: (i) the CSR Group, i.e., companies included in the

Dow Jones Sustainability World Index (DJSI World) and (ii) the non-CSR Group, i.e., companies not included in the

DJSI World. CSR is a dummy valuable which takes the value of 1 if the company belongs to the CSR Group and 0 if

the company belongs to the non-CSR Group.bH-Statistics measure the competitiveness of the financial industry, with a higher value indicating more intensive competition.cLegal environment variables are taken from La Porta et al. (1998).dQMS measures the quality of management schools, with a higher value indicating a higher quality management school;

CLER measures the employer–employee relationship, with a higher value indicating a better working relationship (both

QMS and CLER are taken from the Global Competitiveness Report).eEquator Principles (Wolfsberg Principles) are dummy valuables which take the value of 1 if a firm adopts the principles

and 0 if the firm does not adopt the principles.fThe Inflation Rate (INF) is taken from the World Development Index; the Industrial Production Index (IPI) is taken from

the International Financial Statistics; and the Consumer Confidence Index (CCI) is taken from ACNielsen, with a higher

score indicating stronger consumer confidence.

129On the Determinants of Corporate Social Responsibility

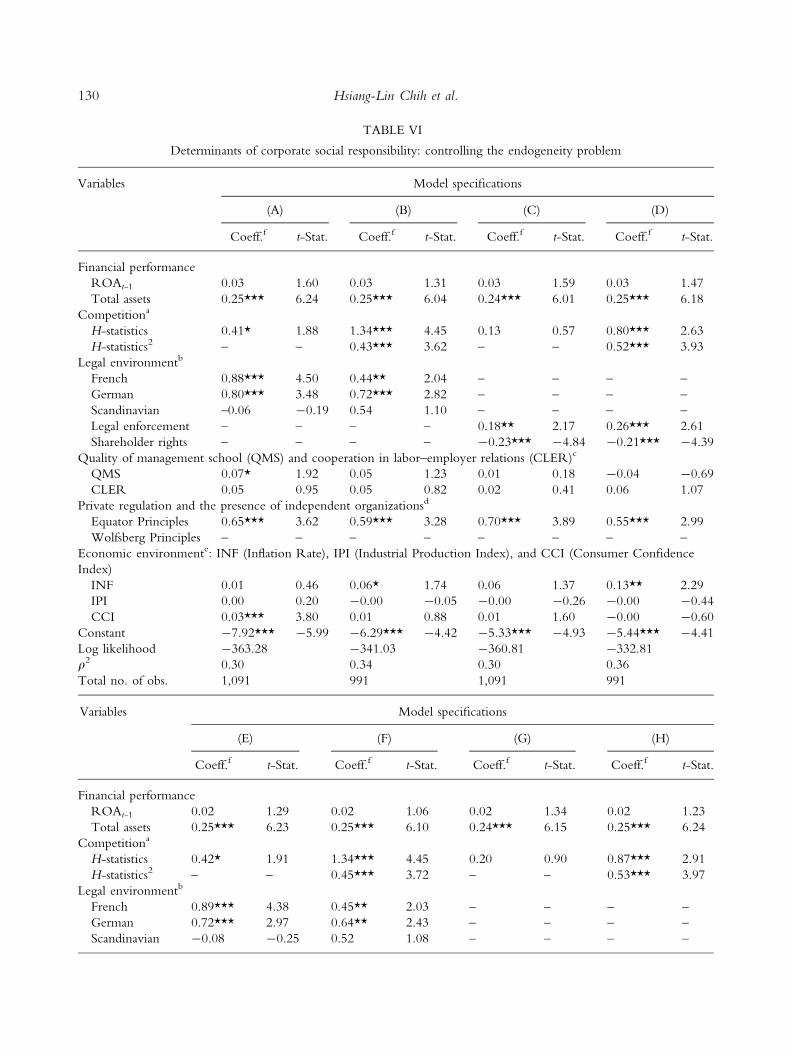

TABLE VI

Determinants of corporate social responsibility: controlling the endogeneity problem

Variables Model specifications

(A) (B) (C) (D)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Financial performance

ROAt-1 0.03 1.60 0.03 1.31 0.03 1.59 0.03 1.47

Total assets 0.25*** 6.24 0.25*** 6.04 0.24*** 6.01 0.25*** 6.18

Competitiona

H-statistics 0.41* 1.88 1.34*** 4.45 0.13 0.57 0.80*** 2.63

H-statistics2 – – 0.43*** 3.62 – – 0.52*** 3.93

Legal environmentb

French 0.88*** 4.50 0.44** 2.04 – – – –

German 0.80*** 3.48 0.72*** 2.82 – – – –

Scandinavian –0.06 -0.19 0.54 1.10 – – – –

Legal enforcement – – – – 0.18** 2.17 0.26*** 2.61

Shareholder rights – – – – -0.23*** -4.84 -0.21*** -4.39

Quality of management school (QMS) and cooperation in labor–employer relations (CLER)c

QMS 0.07* 1.92 0.05 1.23 0.01 0.18 -0.04 -0.69

CLER 0.05 0.95 0.05 0.82 0.02 0.41 0.06 1.07

Private regulation and the presence of independent organizationsd

Equator Principles 0.65*** 3.62 0.59*** 3.28 0.70*** 3.89 0.55*** 2.99

Wolfsberg Principles – – – – – – – –

Economic environmente: INF (Inflation Rate), IPI (Industrial Production Index), and CCI (Consumer Confidence

Index)

INF 0.01 0.46 0.06* 1.74 0.06 1.37 0.13** 2.29

IPI 0.00 0.20 -0.00 -0.05 -0.00 -0.26 -0.00 -0.44

CCI 0.03*** 3.80 0.01 0.88 0.01 1.60 -0.00 -0.60

Constant -7.92*** -5.99 -6.29*** -4.42 -5.33*** -4.93 -5.44*** -4.41

Log likelihood -363.28 -341.03 -360.81 -332.81

q2 0.30 0.34 0.30 0.36

Total no. of obs. 1,091 991 1,091 991

Variables Model specifications

(E) (F) (G) (H)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Financial performance

ROAt-1 0.02 1.29 0.02 1.06 0.02 1.34 0.02 1.23

Total assets 0.25*** 6.23 0.25*** 6.10 0.24*** 6.15 0.25*** 6.24

Competitiona

H-statistics 0.42* 1.91 1.34*** 4.45 0.20 0.90 0.87*** 2.91

H-statistics2 – – 0.45*** 3.72 – – 0.53*** 3.97

Legal environmentb

French 0.89*** 4.38 0.45** 2.03 – – – –

German 0.72*** 2.97 0.64** 2.43 – – – –

Scandinavian -0.08 -0.25 0.52 1.08 – – – –

130 Hsiang-Lin Chih et al.

TABLE VI

continued

Variables Model specifications

(E) (F) (G) (H)

Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat. Coeff.f t-Stat.

Legal enforcement – – – – 0.18** 2.12 0.27*** 2.59

Shareholder rights – – – – -0.23*** -4.57 -0.20*** -4.18

Quality of management school (QMS) and cooperation in labor–employer relations (CLER)c

QMS 0.07* 1.91 0.05 1.27 0.01 0.17 -0.04 -0.70

CLER 0.03 0.56 0.03 0.48 -0.01 -0.24 0.03 0.57

Private regulation and the presence of independent organizationsd

Equator Principles – – – – – – – –

Wolfsberg Principles 1.17*** 3.87 1.07*** 3.53 1.25*** 4.13 1.06*** 3.45

Economic environmente: INF (Inflation Rate), IPI (Industrial Production Index), and CCI (Consumer Confidence

Index)

INF 0.00 0.14 0.05 1.35 0.05 1.09 0.12** 2.02

IPI 0.00 0.66 0.00 0.40 0.00 0.28 -0.00 -0.04

CCI 0.03*** 3.64 0.01 0.87 0.01 1.61 -0.00 -0.63

Constant -8.01*** -5.99 -6.54*** -4.53 -5.67*** -5.32 –5.72*** -4.71

Log likelihood -362.55 -340.67 -360.00 -331.87

q2 0.30 0.34 0.31 0.36

Total no. of obs. 1,091 991 1,091 991

The independent variables of Models (A) and (B) include ROA, total assets, H-statistics, legal origins (French, German,

and Scandinavian), Quality of Management Schools Index, Cooperation in Labor-Employer Relations Index, Equator

Principles, Inflation Rate, Consumer Confidence Index, and Industrial Production Index; in Model (B), we add the

square terms of the H-statistics to investigate whether the curvilinear relationship between competition and socially

responsible corporate behavior exist. Models (C) and (D) use legal enforcement and shareholder rights as legal variables.

The last four specifications, (E), (F), (G), and (H), take into account the Wolfsberg Principles. Other things being equal,

the lagged ROA (ROAt-1) is used as the independent variable to prevent from the possible endogeneity problem.

*Indicates significance at the 10% level; **indicates significance at the 5% level; ***indicates significance at the 1% level.

q2 Measures the explanatory power of the newly added variables in the regression models (McFadden, 1974), with a

higher q2 indicating a better model fit.

Notes: aThe table presents the results of the regressions on the determining variables of the CSR measures. Companies

included in the Dow Jones World Index are classifies into two groups: (i) the CSR Group, i.e., companies included in the

Dow Jones Sustainability World Index (DJSI World) and (ii) the non-CSR Group, i.e., companies not included in the

DJSI World. CSR is a dummy valuable which takes the value of 1 if the company belongs to the CSR Group and 0 if

the company belongs to the non-CSR Group.bH-Statistics measure the competitiveness of the financial industry, with a higher value indicating more intensive com-

petition.cLegal Environment variables are taken from La Porta et al. (1998).dQMS measures the quality of management schools, with a higher value indicating a higher quality management school;

CLER measures the employer–employee relationship, with a higher value indicating a better working relationship (both

QMS and CLER are taken from the Global Competitiveness Report).eEquator Principles (Wolfsberg Principles) are dummy valuables which take the value of 1 if a firm adopts the principles

and 0 if the firm does not adopt the principles.fThe Inflation Rate (INF) is taken from the World Development Index; the Industrial Production Index (IPI) is taken from

the International Financial Statistics; and the Consumer Confidence Index (CCI) is taken from ACNielsen, with a higher

score indicating stronger consumer confidence.

131On the Determinants of Corporate Social Responsibility

those in Table IV, but the coefficients of H-statistic2

turn out to be significantly positive. It indicates that

the financial firms would actually act in more socially

responsible ways to enhance their competitive advan-

tages when the market competitiveness is extremely

intense, after we control the possible shortcomings of

the DJSI-biased selection procedure. Therefore, the

curvilinear relationship between competition and

socially responsible corporate behavior, proposed by

Campbell (2007), is actually not supported.14

Second, we use the lagged ROA (ROAt–1) as the

independent variable in the probit regression, to

prevent from the endogeneity problem. As shown in

Table VI, most of the empirical results are found the

same as those in Table IV, except that the coefficients

of the lagged ROA turn out to be insignificant

and those of H-statistics2 are significantly positive.

The former result implies that the link between

the corporate financial performance and CSR is

insignificant; the latter result implies that the financial

firms would actually act in more socially responsible

ways to enhance their competitive advantages when

the market competitiveness is extremely intense, and

the curvilinear relationship between competition and

socially responsible corporate behavior, proposed by

Campbell (2007), is again not supported.

Conclusions

Our empirical findings are as follows. First, financial

firms with larger size will be more CSR-minded,

and the link between the corporate financial per-

formance and CSR is insignificant. Second, financial

firms would actually act in more socially responsible

ways to enhance their competitive advantages when

the market competitiveness is more intense. There-

fore, the curvilinear relationship between competi-

tion and socially responsible corporate behavior,

proposed by Campbell (2007), is actually not sup-

ported.

Third, financial firms in countries with stronger

legal enforcement measures engage in more CSR

activities, but interestingly and rather strikingly,

those firms in countries with stronger investor rights

engage in less CSR activities. These findings, in fact,

may induce a more complete understanding of the

impact of shareholders rights. Since La Porta et al.

(1997) find that countries with poor investor

protections have smaller and narrower capital mar-

kets, many related studies have typically tended to

focus on the positive impact of the shareholder

rights. La Porta et al. (2002), for example, find that

stronger minority shareholder rights should be

associated with lower dividend payouts. Leuz et al.

(2003) find that the legal protection of outside

investors is a key determinant of the quality of

financial information communicated by insiders to

outsiders and find that earnings management decreases

in stronger legal protection countries. Shen and

Chih (2005) also find that stronger shareholder rights

and greater transparency in accounting disclosure

can reduce banks’ incentives to manage earnings. In

our article, however, stronger shareholder rights are

found to have the negative impact on the incentives

of firms to engage in CSR activities, since financial

firms in countries with stronger shareholder rights

may tend to be geared toward shareholders’ welfare

at the expense of fulfilling their obligations to other

stakeholders.

Fourth, self-regulation in the financial industry

has a significantly positive effect on CSR. Therefore,

a financial firm, which adopts either the Equator or

Wolfsberg Principles, will be an attractive invest-

ment for socially responsible investors, since it will

be effectively required to act in socially responsible

ways and to engage in sound environmental man-

agement practices, according to our findings. This is

of vital importance in driving interest and invest-

ments in CSR to the mutual benefit of financial

firms and investors. Finally, we also conclude that

financial firms in countries with more cooperative

employer–employee relations, higher quality man-

agement schools and a better macroeconomic envi-

ronment will be more CSR minded.

Acknowledgments

The authors gratefully acknowledge the financial support

granted from the project NSC-96-2416-H-305-005-

MY3 by the National Science Foundation in Taiwan.

Notes

1 See Norris (2002) and Friedman (2008).2 A formal definition of ‘‘CSR’’ emerged from an

international meeting of the World Business Council

132 Hsiang-Lin Chih et al.

for Sustainable Development (WBCSD) which was

organized and attended by 60 leading speakers on pub-

lic opinion from inside and outside of the business

world. This formal definition states that: ‘‘CSR is the

continuing commitment by business to behave ethically

and to contribute to economic development while

improving the quality of life of the workforce and their

families as well as of the local community and society at

large’’ (WBCSD Stakeholder Dialog on CSR, Nether-

lands, 6–8 September 1998).3 McWilliams et al. (2006) develop an excellent

framework for consideration of the strategic implica-

tions of CSR, and then go on to propose an agenda for

additional theoretical and empirical research into CSR.4 The DJSI Series, which was first published in Sep-

tember 1999, comprises five general benchmark indexes:

the DJSI World Index, the Dow Jones STOXX Sustain-

ability Index, the Dow Jones Euro STOXX Sustainabil-

ity Index, the Dow Jones Sustainability North America

Index, and the Dow Jones Sustainability United States

Index, each of which, respectively, represents the overall

indices of CSR companies in the global, European, Eu-

rozone, North American and United States markets.

According to the DJSI website, these indices provide as-

set managers with reliable and objective benchmarks for

the management of their sustainability portfolios. A total

of 60 DJSI licenses are currently held by asset managers

in 15 countries around the world for the management of

a variety of financial products, including active and pas-

sive funds, certificates and segregated accounts; these

licensees currently manage a total of over US$5 billion

based in the DJSI. Since the aim of this article is to

investigate the determinants of CSR on a global scale,

we therefore select the DJSI World as our benchmark,

as opposed to the remaining four DJSI Indexes.5 See the Dow Jones Sustainability World Indices

Guide, version 9.1, January 2008.6 McWilliams and Siegel (2000) and Chih et al.

(2008) use a similar approach to classify firms into

socially responsible and socially irresponsible groups.

We choose the financial industry mainly because, as a

result of its large market capitalization, it represents one

of the major industries, and also because firms of the

same industry share more common features, thus help-

ing to avoid confounding effects in the investigation of

the CSR determinants. Furthermore, Griffin and Ma-

hon (1997) also noted in their investigation of the

CSR/CFP relationship that: ‘‘…the internal and exter-

nal pressures in a given industry…are expected to be

the same within the industry’’ and ‘‘multi-industry stud-

ies serve to confound this particular relationship.’’

7 For a number of years, banks working in the pro-

ject financing sector had been seeking ways to develop

a common and coherent set of environmental and social

policies/guidelines that could be applied globally and

across all industry sectors. In October 2002, a small

number of banks convened in London, together with

the World Bank Group’s IFC, to discuss these issues.

The banks in attendance jointly decided to try to devel-

op a banking industry framework for addressing the

environmental and social risks involved in project

financing. This led to the drafting of the first set of

Equator Principles by these banks, which were then

launched in Washington, DC on 4 June 2003. As of

March 2008, a total of 59 institutions had adopted these

principles. The Equator Principles Financial Institutions

(EPFIs) have consequently adopted these principles to

ensure that the financed projects are developed in a

manner which is socially responsible and which reflects

sound environmental management practices. By doing

so, negative impacts on project-affected ecosystems and

communities should be avoided where possible, and if

these impacts are unavoidable, they should be reduced,

mitigated and/or appropriately compensated for (Equa-

tor Principles, July 2006). Refer also to: www.equator-

principles.com.8 The Wolfsberg Group is an association comprising

of twelve global banks which aims to develop financial

services industry standards, and related products, for

Know Your Customer, Anti-Money Laundering and

Counter Terrorist Financing policies. The group came

together in 2000, at Chateau Wolfsberg in Switzerland,

in the company of Transparency International, to pub-

lish the Wolfsberg Anti-Money Laundering Principles

for Private Banking (revised in May 2002). The group

then published a Statement on the Financing of Terror-

ism in January 2002, and also released the Wolfsberg

Anti-Money Laundering Principles for Correspondent

Banking in November 2002 and the Wolfsberg State-

ment on Monitoring Screening and Searching in Sep-

tember 2003. In 2004, the group focused on the

development of a due diligence model for financial

institutions. In June 2006, the group published two sets

of guidelines: Guidance on a Risk-based Approach for

Managing Money Laundering Risks and AML Guid-

ance for Mutual Funds and Other Pooled Investment

Vehicles. In early 2007, the group issued its Statement

against Corruption, in close association with Transpar-

ency International and the Basle Institute on Gover-

nance. Refer also to: www.wolfsberg-principles.com.9 Since CSRi,j,t is a discrete dependent variable, we

estimate the probit model in this article.

133On the Determinants of Corporate Social Responsibility

10 Following Panzar and Rosse (1987) and Claessens and

Laeven (2004), we estimate the following reduced-form

revenue equation on pooled samples for each country:

lnðPitÞ ¼ a þ b1 lnðW1;itÞ þ b2 lnðW2;itÞþ b3 lnðW3;itÞ þ c1 lnðY1;itÞþ c2 lnðY2;itÞ þ c3 lnðY3;itÞ þ dD þ eit;

where Pit is the ratio of gross interest revenue to

total assets (proxy for output price of loans), W1,it is

the ratio of interest expenses to total deposits and

money market funding (proxy for input price of

deposits), W2,it is the ratio of personnel expense to

total assets (proxy for input price of labor), and W3,it

is the ratio of other operating and administrative

expense to total assets (proxy for input price of

equipment/fixed capital). The subscript i denotes

bank i, and the subscript t denotes year t. We

include several control variables at the individual

bank level. Specifically, Y1,it is the ratio of equity to

total assets, Y2,it is the ratio of net loans to total

assets, and Y3,it is the logarithm of total assets (to

control for potential size effects). We also use dum-

my variables (D) for the years 1994 through 2003

(we drop the year dummy for the year 1993) to

control for the fixed effects of calendar years; for

simplicity, these results are not reported in the

tables. The H-statistic equals b1 + b2 + b3.11 We normalize QMS by dividing its mean by its

standard deviation across management schools per coun-

try per year, and also normalize CLER by dividing its

mean by its standard deviation across firms per country

per year.12 Refer to the two websites: www.djindexes.com and

www.sustainability-indexes.com.13 It should be noted that in most of the emerging finan-

cial markets, there are no CSR firms whatsoever, which

implies that CSR firms are highly concentrated within the

developed countries. For example, although Taiwan has as

many as 13 financial firms listed on the Dow Jones World

Index, none of these is included in the DJSI World. Al-

though this may well reflect the fact that developed coun-

tries have much greater concern for CSR, it may also be

simply due to the fact that companies in the developed

countries are better known to DJSI analysts.14 In fact, in Table IV, we have excluded some coun-

tries without CSR firms, including Chile, Cyprus,

Czech Republic, Indonesia, Poland, Singapore, and

South Africa, since some legal or macroeconomic vari-

ables of these countries are not available. For example,

there are no IPI data for Chile, Indonesia, Singapore,

and South Africa, and no legal variables for Cyprus,

Czech Republic, and Poland.

References

Campbell, J. L.: 2007, ‘Why Would Corporations Behave

in Socially Responsible Ways? An Institutional Theory

of Corporate Social Responsibility’, Academy of

Management Review 32(3), 946–967.

Chih, H.-L. and R.-K. Cheng: 2008, ‘Banking

Competition, Profitability Persistence and Access to

Finance: Some International Evidence’, Working