Embed Size (px)

Citation preview

Page 1 of 26

ON GPIS LETTERHEAD

07th

May 2015

To

Mr.G.K.Dwivedi,

Joint Secretary to the Government of India

Ministry Of Home Affairs Government of India

Foreigners Division (FCRA Wing)

NDCC – II Building, (Opposite Jantar Mantar)

Jai Singh Road, Connaught Place,

New Delhi – 110 011

Dear Sir

Sub: Response to your show cause notice under Section 14 of Foreign Contribution

(Regulation) Act, 2010 – F.No.II/21022/58(0047)/2013-FCRA(MU) dated 09

April, 2015 received by us on 13 April 2015.

1. A copy of the show cause notice is enclosed as Annexure 1.

2. We do hereby object your proposal to cancel our registration under section 14 of the

Foreign Contribution (Regulation) Act (FCRA) on the following grounds.

3. At the outset we wish to bring to your kind attention our following preliminary objections:

3.1 These preliminary submissions are without prejudice to our request, dated 16th

April,

2015, and reiterated on 21st April, 2015, that you provide us with copies of all reports

, including the report entitled "MHA Inspection of Greenpeace India Society dated

4th

March 2015,” which has been shared extensively with the media but not so far

provided to us. Principles of natural justice demand that, prior to being required to

respond to the show cause notice, we have the right to know the basis and nature of

the charges against us, and to have sight of all relevant documents in your

possession, whether inculpatory or exculpatory, so that we may answer the charges,

and their basis, against us. Upon expeditious receipt of the relevant documents in

your possession, we reserve the right to reply in further detail with regard to that

information, and to address any issues raised therein.

3.2 Though your show cause notice (SCN) and order under section 13 (Order) dated 9

April 2015 suspending our registration and freezing our bank accounts were received

by us only on 13 April 2015, the banks had apparently been informed earlier and the

freeze had been applied by the banks from 9 April 2015 itself. Information about the

Page 2 of 26

freeze was also available in the press on 9 April 2015. It is not clear as to how SCN

and Order dated 9 April 2015 were available to banks for action and reached the

press for reporting on the same day while we ourselves got to know of it only later

with the hard copies reaching us on 13 April 2015. Equity and principles of natural

justice demand that the noticee be first or at least simultaneously be made aware of

the SCN/Order. That the information reached the press earlier can only be viewed as

an indicator to generate negative publicity and destroy the morale of the various

stake holders of our organisation not behoving a statutory authority.

3.3 In fact a sum of € 1,48,068 (Rs.1 crore approximately) transferred by Stitching

Greenpeace International on 23 March 2015 was not credited by the bank to our

account although your SCN and Order under section 13 are dated 9 April 2015 only.

In response to our specific query vide our letter dated 8 April 2015 the Deputy

Secretary Mr.Mahendra Kumar has informed us by his letter dated 23 April 2015 that

“The question of credit of foreign contribution transferred by Stitching Greenpeace

Council, Amsterdam on 23 March, 2015 would be considered after the FCRA

designated bank account is regularised”. FCRA designated account was frozen only

on 9 April 2015 and the legal authority under which the credit of 148068 € was

frozen more than two weeks earlier has to be clarified by you. Please note that this

violates the order of the Delhi High Court in WP (C) 5749/2014.

3.4 There are some grounds in the SCN and Order which were not raised in your onsite

inspection report dated 27 November 2014 (Inspection Report) but these grounds

have been relied on in the SCN and also in the Order under section 13. Therefore

with respect to these grounds though no explanations have been sought from us they

have nevertheless been relied on by you for your action of freezing our bank account

and suspending our registration under section 13.

3.5 We had responded to your Inspection Report in detail by our letter dated 20

December 2014. In both the SCN and Order you have not dealt with our response at

all. Both the SCN and Order are non-speaking as it is not clear as to why our

response was not acceptable to you. Any statutory SCN and Order have to be

speaking for themselves. In the absence of a speaking order we are constrained to

repeat our response to the Inspection Report in many cases.

3.6 Both your SCN and Order are not specific. To illustrate your observation in

paragraph 5 below just lists the bank accounts with no specific information on the

transfers/amounts. You have not given breakup of Rs.47,80,147/- (paragraph 9

below) said to have been transferred by us to Greenpeace Environment Trust

(GPET). Administrative expenses (paragraph 7) are quantified without any

basis/breakup. This makes any response from us impossible.

In the case of administrative expenses the basis for the quantification of the figures of

administrative expenses at Rs.6,07,43,232 and Rs.8,22,43,335 (paragraph 7 below)

Page 3 of 26

has not been provided by you inspite of our specific request in our response to your

Inspection Report. Without providing a breakup and therefore without an opportunity

for us to respond you have initiated action under sections 13 and 14.

3.7 FCRA, 1976 has been repealed. FCRA, 2010 and Foreign Contribution (Regulation)

Rules, 2011 were notified on 29 April 2011 only. Some of your questions pertain to

transactions relating to the period prior to 29 April 2011 and in some of these cases

you seek to apply FCRA, 2010 or Rules, 2011 to such transactions which are

incorrect under law. We had objected in our response to your Inspection Report to

your application of 50% ceiling on administrative expenses for the period prior to 29

April 2011 and you have dropped that issue. However you are invoking section 8 (1)

(a) of FCRA, 2010 to payments (paragraph 8.1 below) made in FY 2008-09 and

2009-10.

3.8 There is also lack of application of mind for your action under sections 13 and 14 as

even the obvious mistakes/failures to consider the issues holistically (paragraphs

6.1.3, 6.2 and 8.3 below) in your Inspection Report are persisted with and relied on.

Further petty amounts which are immaterial and where the disclosures have been

erring on the right side - for example paragraphs 6.3.2, 6.4, 6.5 etc., below on Bibit

gateway are treated as violation of section 33.

4. We have reproduced the grounds relied on by you in italics followed by our response in

paragraphs 5 to 13 below.

5. Has first transferred Foreign Contribution received in the FCRA designated bank account

to the FCRA utilisation account and from there to five other undeclared utilisation bank

accounts as mentioned below without informing authority concerned in violation of Rule 9

(1) (e) of Foreign Contribution (Regulation) Rules, 2011;

S.

No.

Account No. Credited from A/c Debit A/c No.

1. 005103000000888 (IDBI Bank),

FCRA designated Bank Account

Foreign Donors like

Greenpeace International,

Greenpeace Netherlands,

Climate Works Foundation

005103000004169

002284100000616

0022840000002052

2. 0022840000002052

Yes Bank

FCRA utilisation Bank Account

005103000000888 (Foreign

contribution account)

005103000004169

002284100000616

015694600000011

1. 005103000004169 (IDBI Bank,

Chennai)

005103000000888 (Foreign

Contribution account)

002284100000616

0022840000002052

002284100000616,

002283800005431,

015694600000011,

005103000000408

(Greenpeace

Environment Trust)

Page 4 of 26

2. 002284100000616

(Yes Bank)

005103000000888 (Foreign

Contribution account)

005103000004169

0022840000002052

002283800005431

005103000004169

625401068671

3. 00283800005431

(Yes Bank)

005103000004169 002284100000616

015694600000011

4. 015694600000011

(Yes Bank)

005103000004169

0022840000002052

002283800005431

625401068671 (ICICI Bank)

625401068671

(ICICI Bank)

5. 625401068671

(ICICI Bank)

015694600000011

(Yes Bank)

015694600000011

(Yes Bank)

As per the provisions of Section 17 (1) of the Act, foreign contribution will be received in a

single account only through such one of the branches of a bank as specified in the

application for grant of certificate and no funds other than foreign contribution shall be

received or deposited in such account. The Act provides for opening of one or more

accounts in one or more banks for utilisation of the foreign contribution received and in all

such cases, as per Rules 9 (1) (e) of FC(R) Rules, 2011 intimation on plain paper shall

have to be furnished to Ministry of Home Affairs within 15 days of the opening of the

account;

Whereas, it has also been found that multiple transfers were made to multiple other

accounts including inter account transfers from the utilisation account without any

intimation or permission of Ministry of Home Affairs, which is a violation of Section 17(1)

of FCRA, 2010 read with Rule 9(1) (e) of FC(R) Rules, 2011;

5.1 The FCRA designated account is with IDBI Bank (account no. 0888) and the

utilisation account is with Yes Bank (account no.2052). All the foreign grants

received have been credited into the designated account with IDBI Bank (account

no.0888) and any credit in 2052 is out of 0888 only. Identifiable non FCRA (local)

funds have never been credited into these two accounts.

FCRA and Foreign Contribution (Regulation) Rules, 2011 (Rules) were notified on

29 April 2011 only. The utilisation account was operational only on 12 December

2011 as intimated to you vide our letter dated 13 December 2011 (Annexure 2).

Therefore a few transfers have been made after FCRA 2010 came into effect from

0888 to 616 with Yes Bank which are also on account of reimbursement.

5.2 There can be no objection from you to interse transfers between local accounts i.e.,

accounts other than 0888 and 2052.

Page 5 of 26

5.3 There has been no transfer by us to Greenpeace Environment Trust (GPET). Any

entries with respect to GPET appearing in our bank statement are errors committed

by banks and subsequently rectified by them. Please see paragraph 9.2 below.

5.4 Substantial portion of the donations are from local sources with foreign grants

constituting only around 35% (for the period 2010-11 to date) of the total donations

received by us. Many a time the advances for expenses will be made out of the local

account and on settlement of bills allocation will be made between the FC and the

local component based on the programme. When an individual draws advance for

expenditure he will incur expenditure out of the advance both towards FC and local

project. Therefore allocation is essential and unavoidable. The transfers were towards

reimbursement of expenditure initially met in the local account.

The exact amount was transferred from 2052 once the expenditure was booked

in FCRA books and after reconciling the inter account dues from FCRA to

Local account in the books of account of both. In some months when such

reconciliation got delayed, an approximate amount in round sum was transferred

first and after the reconciliation the balance amount was transferred from FC account

to LC. Hence all transfers are towards reimbursement only. Consequently there is no

violation of rule 9 (1) (e) as the transfers from 2052 are against FC expenses

incurred.

All transfers are backed by actual FC expenditure declared in the FC returns and

audited FC statements. No portion of the FC grant has been used for local

expenditure. Further every debit, credit and expenditure can be tracked and identified

as per the requirements of FCRA. Your Inspection Report and SCN do not question

the authenticity and genuineness of any of our expenses/payments.

Mere allocation of expenditure in this fashion cannot be construed as a violation of

section 17(1) of FCRA or rule 9 (1) (e) of FCR Rules.

5.5 It is clarified that where the expenditure is identifiable at the point of incurrence, the

payment is always made out of account 888 or 2052 only. Online payment facility is

not available in account 888 which was an impediment in its usage. Further foreign

grants have never been used for local projects.

5.6 There is no transfer to account no 68671 with ICICI Bank and in the case of account

no.5431 (Yes Bank) the transfer for the period 10 April 2011 to 30 September 2014

is Rs.70,000/- only. However both these accounts are also frozen. Even Rs.70,000/-

is on account of reimbursement.

5.7 Such transfers to local accounts was also for ease of operation as we are a large all

India environmental organisation engaged in 3 to 4 major environmental campaigns

across many locations in India deploying over 300 employees and consultants who

had to travel extensively. Local donations accounted for about 60 to 65% of the total

income of GPIS and there were always adequate funds in the local bank accounts.

Page 6 of 26

Hence we have no need or occasion to beef up these local accounts with funds

transfer from FCRA bank accounts.

5.8 Given the nature of our programme and entity level compliance requirements, it is

practically impossible to demarcate transactions of FCRA and local donations

without any procedural overlap as the organisation as a whole is one legal entity and

its accounts have to be maintained as such. To illustrate, statutory payments like

income tax deducted at source (TDS), provident fund, profession tax etc., have to be

remitted in a consolidated manner for the entity as a whole. Ultimately in our case

every FC transaction and FC payment can be tracked and identified which is the

main purpose of demarcation between FC and LC. Hence this cannot be viewed as an

intentional, serious violation of FCRA 2010 warranting cancellation/suspension

action under Section 13 and 14.

6. Whereas the association has under-reported and repeatedly mentioned incorrect amount of

Foreign contribution received, as mentioned below, in violation of Section 33 of FCRA,

2010, the most glaring example being Foreign Contribution opening balance for 2008-09,

which was reported as Nil in the auditor’s certificate but was actually Rs.6,60,31,783/-.

Greenpeace India Society subsequently admitted the same and claimed it to be a

typographical error, which is not tenable. Some other violations are:

6.1 General Response

6.1.1 FCRA 2010 came into effect only from 29 April 2011. Without prejudice, your

questions relating to the earlier years when FCRA, 1976 was in force are also

dealt with in this paragraph.

You have stated that our explanation that the difference in opening balance in

the auditor certificate of Rs.6,60,31,783/- is due to a typographical error is “not

tenable”. However we wish to point out that in your own remarks column in

paragraph 6.2 below the foreign contribution has been shown as Rs.20,89,661/-

instead of the correct figure of Rs.2,08,96,661/- shown by you under the head

receipts. Though this error was noted by us in your Inspection Report we chose

not to point it out as such human errors do occur. Further you have stated

(paragraph 6.2) that there is variation in interest between the disclosure in FC3

(Rs.51,31,704/-) and receipt and payment account (Rs.51,13,704/-). This is

factually incorrect as the figure is the same at Rs.51,13,704/- as already pointed

out in our response to your Inspection Report. However mistakes in the

inspection report persist even in the SCN which is the basis for your action

under section 14.

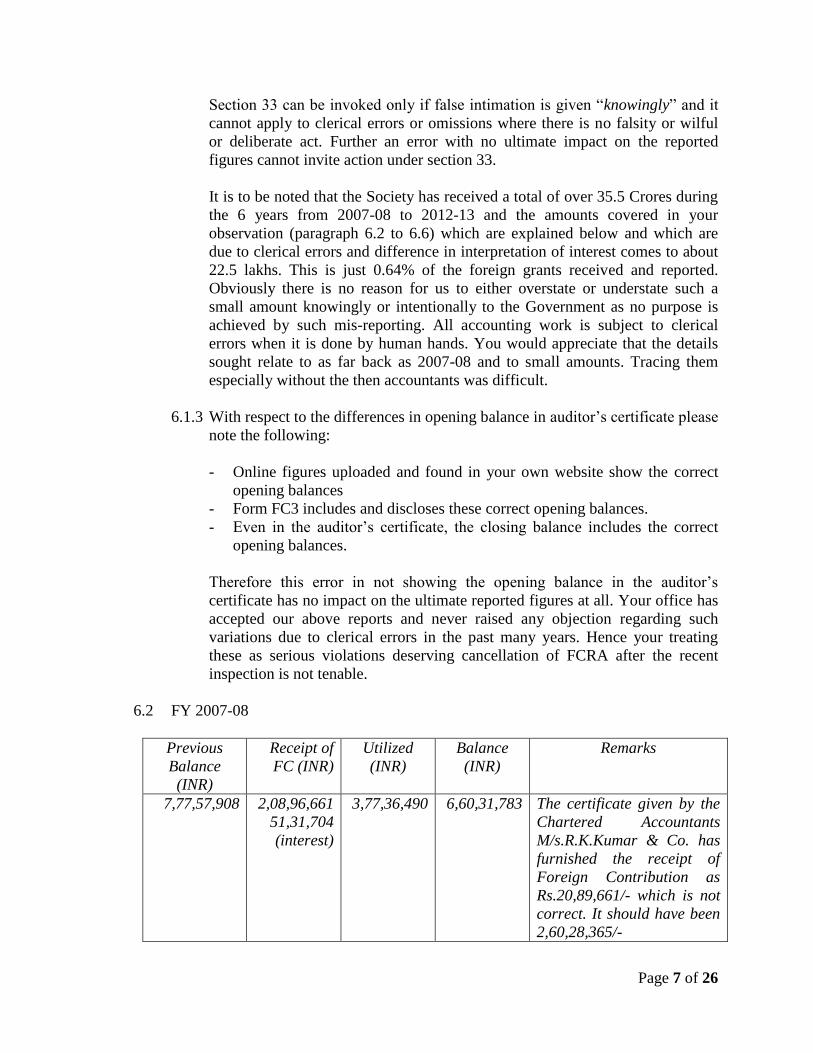

6.1.2 Section 33 applies to “any person, subject to this Act, who knowingly, (a) gives

false intimation under sub-section (c) of section 9 or section 18”…...

Page 7 of 26

Section 33 can be invoked only if false intimation is given “knowingly” and it

cannot apply to clerical errors or omissions where there is no falsity or wilful

or deliberate act. Further an error with no ultimate impact on the reported

figures cannot invite action under section 33.

It is to be noted that the Society has received a total of over 35.5 Crores during

the 6 years from 2007-08 to 2012-13 and the amounts covered in your

observation (paragraph 6.2 to 6.6) which are explained below and which are

due to clerical errors and difference in interpretation of interest comes to about

22.5 lakhs. This is just 0.64% of the foreign grants received and reported.

Obviously there is no reason for us to either overstate or understate such a

small amount knowingly or intentionally to the Government as no purpose is

achieved by such mis-reporting. All accounting work is subject to clerical

errors when it is done by human hands. You would appreciate that the details

sought relate to as far back as 2007-08 and to small amounts. Tracing them

especially without the then accountants was difficult.

6.1.3 With respect to the differences in opening balance in auditor’s certificate please

note the following:

- Online figures uploaded and found in your own website show the correct

opening balances

- Form FC3 includes and discloses these correct opening balances.

- Even in the auditor’s certificate, the closing balance includes the correct

opening balances.

Therefore this error in not showing the opening balance in the auditor’s

certificate has no impact on the ultimate reported figures at all. Your office has

accepted our above reports and never raised any objection regarding such

variations due to clerical errors in the past many years. Hence your treating

these as serious violations deserving cancellation of FCRA after the recent

inspection is not tenable.

6.2 FY 2007-08

Previous

Balance

(INR)

Receipt of

FC (INR)

Utilized

(INR)

Balance

(INR)

Remarks

7,77,57,908 2,08,96,661

51,31,704

(interest)

3,77,36,490 6,60,31,783 The certificate given by the

Chartered Accountants

M/s.R.K.Kumar & Co. has

furnished the receipt of

Foreign Contribution as

Rs.20,89,661/- which is not

correct. It should have been

2,60,28,365/-

Page 8 of 26

The association has shown

interest in FC-3 Statement

as Rs.51,31,704/-, whereas,

it has been shown in Receipt

& Payment account as

Rs.51,13,704/- leaving

behind a difference of

Rs.18000/-

Response :

The correct figure of interest is Rs.51,13,704/- and not as shown by you of

Rs.51,31,704/- in the remarks. Therefore there is no difference of Rs.18,000/- as

pointed out by you. Rs.51,13,704/- is shown in both FC-3 and Receipts and

Payments account for the F.Y. 2007-2008. However, the C.A. Certificate does not

include interest received of Rs.51,13,704/- hence actual FC receipt Rs.2,60,10,365/-

(including interest) is only shown.

The copy of the FC-3 and Receipts and payments are attached at Annexures 3 and 4

wherein interest shown is Rs.51,13,704/- only. Hence there is no difference between

FC-3 and Receipts and Payments Account. In your remarks you state that the foreign

contribution shown by the auditors is Rs.20,89,661/- but the actual figure shown by

them is Rs.2,08,96,661/-

6.3 FY 2008-09

Previous

Balance

(INR)

Receipt of

FC (INR)

Utilized

(INR)

Balance

(INR)

Remarks

6,60,31,783 3,00,59,377

37,98,937

(Interest)

5,69,93,513 4,28,96,584 The certificate given by the

Chartered Accountants

M/s.R.K.Kumar & Co.

reflects the opening balance

as ‘Nil’ and Receipt of

‘Foreign Contribution’ is

Rs.3,00,59,377/-, which is not

correct As per FC-6 return,

the receipt of foreign

contribution is

Rs.3,00,59,377/- whereas the

Receipt & Payment Accounts

shows that the association

has received Rs.2,97,06,047/-

Page 9 of 26

leaving behind a different of

R3,53,330/-

Response :

6.3.1 Opening balance stated as NIL for the years from 2008-09 in the auditor

certificate seems to be due to a typographical error. However the closing

balance of F.Y. 2008-09 and subsequent years till 2011-12 is correctly

shown after considering the opening balances. In the year 2012-13, the

opening balance has been mentioned correctly. FC Receipt Rs.30059377/-

shown in auditor’s certificate does not include interest of Rs.3798937/-.

6.3.2 Monies were being collected online through an international gateway of

Greenpeace International called Bibit. Bibit offers online gateway on

recurring basis for monthly collections and this facility of online recurring

collection from individual donors was not available in India at the time. As

Bibit could not transfer money to India under the arrangement Greenpeace

International remitted (for lack of option) to the FC bank account of the

Society monies which included Rs.3,53,331/- from Indian citizens which are

to be classified as local grant. As Rs.3,53,331/- was credited by the

gateway/GPI to the FC bank account it has been transferred by us to our

local bank account. FC 3 included Rs.3,53,331/- as a receipt as per the gross

credits in the FC bank account but in the receipt and payment account

Rs.3,53,331/- was not included as a foreign grant receipt. Hence the

difference.

6.4 FY – 2009-10

Previous

Balance

(INR)

Receipt of

FC (INR)

Utilized

(INR)

Balance

(INR)

Remarks

4,28,96,584 6,70,10,297

26,23,043

(Interest)

8,70,63,873 2,54,66,051 The certificate given by the

Chartered Accountants

M/s.R.K.Kumar& Co. reflects

the opening balance as ‘Nil’

which is not correct. As per

the FC-6 Returns, the

association has received

Rs.6,70,10,297/- but, as per

Receipt & Payment Accounts,

the association has

Rs.6,59,58,502/- leaving a

difference of Rs.10,51,795/-.

Response :

Page 10 of 26

Opening balance stated in the audit certificate as NIL for the year 2009-10, seems to

be due to a typographical error. However in the year 2012-13, the opening balance

was correct. Further the closing balance of F.Y. 2009-10 is shown after considering

the opening balance which shows that its omission in the opening balance cannot be

treated as a violation of section 33 as it has no impact whatsoever.

Please note that Rs.10,51,795/- represents receipt through Bibit international gateway

as explained in paragraph 6.3 above. However Rs.5,53,412/- is shown as other

income in receipts and payment account. Therefore the difference is Rs.4,98,383/-

from Indian citizens credited to the designated account by gateway/GPI as explained

in paragraph 6.3 above and transferred to our local bank account.

6.5 FY 2010-11

Previous

Balance

(INR)

Receipt of

FC (INR)

Utilized

(INR)

Balance

(INR)

Remarks

2,54,66,051 2,52,19,703

6,45,966

(interest)

7,70,69,833 42,61,887 The certificate given by the

Chartered Accountants

M/s.R.K.Kumar& Co.

reflects the opening balance

as ‘Nil’ which is not correct.

The association has

mentioned as Foreign

Contribution received in

FC-6 return as

Rs.5,52,19,703/-, whereas,

they have mentioned in

Receipt & Payment

Accounts as Foreign

Contribution received

Rs.5,45,39,253/-, which

leaves a difference of

Rs.6,80,450/-

Response :

Opening balance stated in the audit certificate as NIL for the year 2010-11 seems to

be due to a typographical error. However in the year 2012-13, the opening balance

was correct. Further the closing balance of F.Y. 2010-11 is shown after considering

the opening balance.

Please note that Rs.6, 80,450/- represents receipt through Bibit international gateway

as explained in paragraph 6.3 above.

Page 11 of 26

Of Rs.6,80,450/-,

- Rs.438340/- is shown as “Other Income” in Receipts and payments and also

shown in FC –3

- Rs.172110/- is shown as “Other Income” in Receipts and payments of F.Y 2009-

10 on accrual basis but shown in FC-3 for the F.Y. 2010-11.

- Rs.70,000/- received in FCRA designated Bank A/c and transferred to Greenpeace

India Society Local bank A/c

6.6 FY 2011-12

Previous

Balance

(INR)

Receipt of

FC (INR)

Utilized

(INR)

Balance

(INR)

Remarks

42,61,887 6,74,22,334

10,47,191

(interest)

6,97,23,208 30,08,204 The certificate given by the

Chartered Accountants

M/s.R.K.Kumar& Co.

reflects the opening balance

as ‘Nil’ which is not correct.

The Receipt & Payment

Accounts shows the receipt

of Foreign Contribution of

Rs.6,72,54,834/- (excluding

interest). whereas, it has

been shown in FC-6 Return

as Rs.6,74,22,334/-. There is

a difference of Rs.1,67,500/-

in the figure mentioned in

the Receipt & Payment

account and FC-6

Statements.

Response :

Opening balance stated in the audit certificate as NIL for the year 2011-12 seems to

be due to a typographical error. However in the year 2012-13, the opening balance

was correct. Further the closing balance of F.Y. 2011-12 is shown after considering

the opening balance.

Page 12 of 26

Please note that Rs.1, 67,500/- represents receipt through Bibit international gateway

as explained in paragraph 6.3 above. Of Rs.1,67,500/-, Rs.131510/- is shown as

“Other Income” in Receipts and payments and also shown in FC –3

- Rs.35990/- is shown as “Other Income” in Receipts and payments of F.Y 2010-11

on accrual basis but shown in FC-3 for the F.Y. 2011-12.

7. Whereas the association has incurred more than 50% of the Foreign Contribution on

administrative expenditure during financial year 2011-12 and 2012-13 without obtaining

the prior approval of the Central Government in violation of Section 8 (1)(b) of FCRA,

2010, which is also substantiated by the notice/orders issued by the income Tax

Department and subsequent payment of Rs.62.12 lakhs by the Greenpeace India Society to

the income Tax Department.

S.No. Financial Year Foreign Contribution

Received (Rs.)

Administrative

Expenditure (Rs.)

1. 2011-12 6,84,69,525 6,07,43,232

2. 2012-13 10,14,72,417 8,22,43,335

Section 8(1) (b) of FCRA, 2010 stipulates that administrative expenses shall not exceed

50% of the foreign contribution received in a financial year and any expenditure of

administrative nature in excess of 50% shall be defrayed only after prior approval of the

Central Government.

7.1 You have neither given the breakup nor the basis for determining the administrative

expenses at Rs.6.07 crores (31 March 2012) and Rs.8.22 crores (31 March 2013). We

had infact asked for this information to be given to us even in our response to your

Inspection Report but there has been no response from you. Without providing us an

opportunity to explain you have invoked section 13 and section 14 which is not

legally sustainable.

7.2 Our administrative expenses do not constitute more than 50% of the foreign

contribution receipt during the year. A tabular analysis of the expenses incurred for

the years 31 March 2013 and 31 March 2012 is given below.

7.2.1 Year ended 31 March 2013

Programme Salaries Consultancy,

Training

Travel

and

Accomm

odation

Commu

nications

Office

Maintena

nce

Finance

& Legal

Total

Expenses

% to

Total

Exp.

Climate &

Energy

13553411

1868383

4513725

151796

816186

76062

20979563

23

Sustainable

Agriculture

3116538

35295

594255

10207

109077

1258

3866630

4

Page 13 of 26

Oceans 658075 10056 210186 0 31673 12 910002 1

Non Violent

Direct Action

2870903

0

177791

549 27098 8595 3084936

3

Media &

Communicati

ons

7138359 6000 331577 82488 1051 6947 7566422

9

Public

Engagement 7473640 1401133 402019 15636 46957 12189 9351574

10

Public

Awareness

Campaign &

Fundraising 20321883 6804215 2493010 0 832 2039 29621979

32

Organisation

Support 12939533 130000 162257 0 5110 3472559 16709459

18

Grand Total 68072342 10255082 8884820 260676 1037984 3579661 92090565 100

7.2.2 Year ended 31 March 2012

Programme Salaries Consultancy,

Training

Travel

and

Accomm

odation

Commu

nications

Office

Maintena

nce

Finance

& Legal

Total

Expenses

% to

Total

Exp

Climate &

Energy 10215594 1039976 3631401 106463 3260847 160 18254441

27

Sustainable

Agriculture 1347715 14050 798866 34728 222563 0 2417922

4

Oceans 1090865 1100 608968 23980 93520 772 1819205 3

Non Violent

Direct Action

1520012 10000 414016 15580 258968 0 2218576

3

Media &

Communicati

ons 3475593 0 88548 125044 9003 0 3698188

5

Public

Engagement 1695378 0 64878 37194 4970 0 1802420

3

Public

Awareness

Campaign &

Fundraising 21447220 4903877 2082103 30821 177575 0 28641596

43

Organisation

Support 6026297 0 182334 39373 2123364 17274 8388642

12

Grand Total 46818674 5969003 7871114 413183 6150810 18206 67240990 100

7.2.3 In the income and expenditure account the expenses are classified based on

natural account heads and that classification cannot be the basis for reaching

adverse conclusion on the nature of expenses. Please note that programmewise

classification of expenses is drawn from and based on our books of account

Page 14 of 26

only. In fact the table for the year ended 31 March 2012 is reproduced even in

the income tax assessment order for that year.

7.2.4 Without prejudice even if the organisation support is taken to be administrative

in nature the percentage of such expenses to the foreign contribution received

will be 16% (31 March 2013) and 12% (31 March 2012) only.

7.3 It is clear from Rule 5 of FCRA Rules 2011 that salaries paid to programmatic staff

and those involved in research, training and the related expenses cannot be treated as

administrative expenses. Further only salary, wages and travel of the executive

committee and human resources department are treated as administrative expenses. It

is not clear if you have applied the rule.

7.4 Our Society is not engaged in direct delivery of materials/services like in hospitals,

schools and disaster relief work. We are engaged in environmental protection work

which involves research studies, campaign, advocacy and lobbying for environment

friendly policy formulations necessitating engagement of staff and third party

consultants who are highly qualified and experienced specialists in environmental

issues. Our programme involves extensive travel and working proactively with the

Governments of India and States. Salary, consultancy fees and travel expenses of

such staff and consultants engaged in programmatic work are to be excluded from

the administration expenses as per Rule 5 above.

7.5 It may also be noted that no donor will accept administrative expenditure of between

81% and 88% of their total grants as computed in your table.

7.6 We have not accepted the contentions of the income tax department in FY 31 March

2011 on overheads. This contention was a mere generalised opinion without any

basis, evidence and details. This has been challenged by us in appeal before

commissioner of Income Tax (Appeals) who has heard us on the matter. The CIT

(Appeals) has sought a response from the assessing officer on our rebuttal of the

Assessing Officer’s contentions sometime in September/October 2014. As the

Assessing Officer has not yet responded to the CIT (Appeals), even after seven

months, the appeal is still pending before the CIT(A).

7.7 Payment of Rs.62.11 lakhs being 25% of tax demand is made because the income tax

department does not stay the entire tax demand during the pendency of appeal. The

maximum stay is of 50% of the tax demand normally. We were therefore constrained

to pay 50% of the tax demand eventually even during the pendency of appeal.

Therefore your reliance on our tax payment where the order is under appeal is

misplaced and incorrect. This amount will have to be refunded by the income tax

department with interest if our appeal is upheld.

FCRA being an independent enactment you ought to have exercised your mind on

the facts of our case as per the provisions of FCRA instead of relying on income tax

assessment orders under appeal.

Page 15 of 26

8. Whereas the association has funded legal costs, not only for seeking bail, but also for filing

writ petitions of an association Indian NGO activists of the association some of which

were: Greenpeace India Society incurred an expenditure of Rs.25,000/- in Financial Year

2008-09 and Rs.55,000/- in Financial Year 2009-10 for securing bail bonds and payment

of legal fee without any previous consent of the donor, in contravention of Section 8 (1) (a)

of FCRA, 2010, which envisages that Foreign Contribution should be utilised only for the

purpose for which it has been received. Moreover, this activity does not fall within the

ambit of the aims and objectives of the association;

8.1 The transactions relate to FY 2008-09 and FY 2009-10 when FCRA, 2010 was not in

force. As pointed out elsewhere in this response FCRA 2010 and the Rules

thereunder were notified on 29 April 2011 only. Therefore section 8 (1) (a) of FCRA,

2010 is irrelevant with respect to these transactions.

8.2 When our staff or volunteers who take part in any campaign or related Non Violent

Direct Action to highlight environmental violations and draw public attention get

arrested, we advance money as bail bonds to secure their release on bail as per

directions of the Courts. These bonds are released and returned to us when the cases

are disposed of by the courts. Hence these payments are not to be classified as

“expenditure” but are more in the nature of security deposits. Moreover, they are

incurred for the purpose of achieving the organisational objectives and are well

within the ambit of the aims and objectives of the Society. The grants given by the

donor are for supporting all our environmental programmes and administrative

expenditure and hence no specific consent of the donor is required for each

expenditure. This outgo is not in contravention of section 8 (1) (a) as it is a natural

concomitant to our programme. However, without prejudice to our above stand, in

view of your observation we had in our response to our Inspection Report attached a

letter from the donor, Greenpeace International, giving their specific approval for this

and other such observations of yours calling for donor’s specific sanction for some

types of expenditure which has not been considered by you before initiating action

under section 13 and 14. This letter is again attached in Annexure 5.

8.3 The total outflow is Rs.55000/- only and not Rs.80000/- as stated in your

observation. We had pointed this out in our response to your Inspection Report also.

Rs.25,000/- as at the end of FY 2008-09 is included in the closing balance of

Rs.55,000/- in FY 2009-10. Therefore total outflow foreign + local is Rs.55,000/-

only. The table given below is self-explanatory. Of the total outflow of Rs.55,000/-,

Rs. 30000/- is incurred out of local funds and not out of foreign grants.

The details of the bail bonds obtained, those released after dismissal of the cases and

the bonds pending release are given below. The case against the 6 activists for whom

Rs. 5000 each was paid from FCRA towards Bail bonds shown below has also been

dismissed and we have received Rs.30,000/- plus interest but we are unable to

deposit due to your freeze of our bank accounts.

Page 16 of 26

GREENPEACE INDIA SOCIETY - DETAILS OF SURETY BOND

Particulars

FY 2008-09

Total

FY 2009-10

Total

Foreign

Source

Local

Funds

Foreign

Source

Local

Funds

Opening Balance as on 1-4-2008

(Bidhan Chandra Singh) 10000 0 10000 10000 0 10000

Opening Balance as on 1-4-2009

(Kolaghat Axn Surety) 0 0 0

15000 15000

Jai krishna-HO-staff-surety bond at

hyd 0 0 0 5,000 0 5000

Md.Sadiquiddin Khan-volunteer-

surety bond at hyd 0 0 0 5,000 0 5000

Leonard Francis F-volunteer-surety

bond at hyd 0 0 0 5,000 0 5000

S.Ve.Eshwaran-Volunteer-surety

bond at hyd 0 0 0 5,000 0 5000

Calyanaramon-Volunteer-surety

bond at hyd 0 0 0 5,000 0 5000

Konda Venkateswarlu-Hyd staff-

surety bond at hyd 0 0 0 5,000 0 5000

Kolaghat Axn surety 0 15000 15000 0 0 0

Total 10000 15000 25000 40000 15000 55000

9. Whereas the association has admitted before the Income Tax Department and as proved

through the bank account scrutiny during inspection that in the financial year 2010-11,

Greenpeace India Society paid Rs.8,05,027/- to the employees of Greenpeace Environment

Trust (GET), which is a separate Trust with a different PAN number in violation of Section

7 of the FCRA, which prohibits transfer of Foreign Contribution from an FCRA registered

NGO to a non-FCRA registered NGO without the prior approval of the Central

Government. It has been found that Greenpeace Environment Trust account

No.005103000000408 in IDBI Bank received Rs.47,80,147/- from Greenpeace India

Society Bank account No,005103000004169 from 3rd

January, 2013 to 5th

November, 2013

in violation of Section 7 of FCRA 2010;

9.1 No payment has been made by us to GPET’s employees. In fact GPET has no

employees. Therefore the question of us paying the employees of GPET does not

arise. This is a factually incorrect statement in the income tax assessment order

without any basis. No admission to this effect has been made by us before the

assessing officer (AO). Rs.8,05,027/- represents expenses on travel incurred and paid

by us in respect of our employees. In fact the Assessing Officer has been given

Page 17 of 26

employeewise and purposewise breakup with amounts and dates for Rs.8,05,027/-

This aspect of the assessment order is also under appeal before CIT (Appeals).

You ought to have given us an opportunity and sought our clarification before

relying on this for issue of SCN and Order. This was not raised in your Inspection

Report.

9.2 We do not know how you arrived at the figure of Rs.47,80,147/- transferred from

GPIS account no. IDBI 4169 to GPET account no. IDBI 408 both of which are local

accounts.

If you provide us with the breakup – date, amount etc., we will explain them.

We have not made any transfer on our own from GPIS to GPET. Further both the

accounts 4169 and 408 are local accounts. Therefore without prejudice transfers from

4169 to 408 cannot be objected to by you as being violative of FCRA.

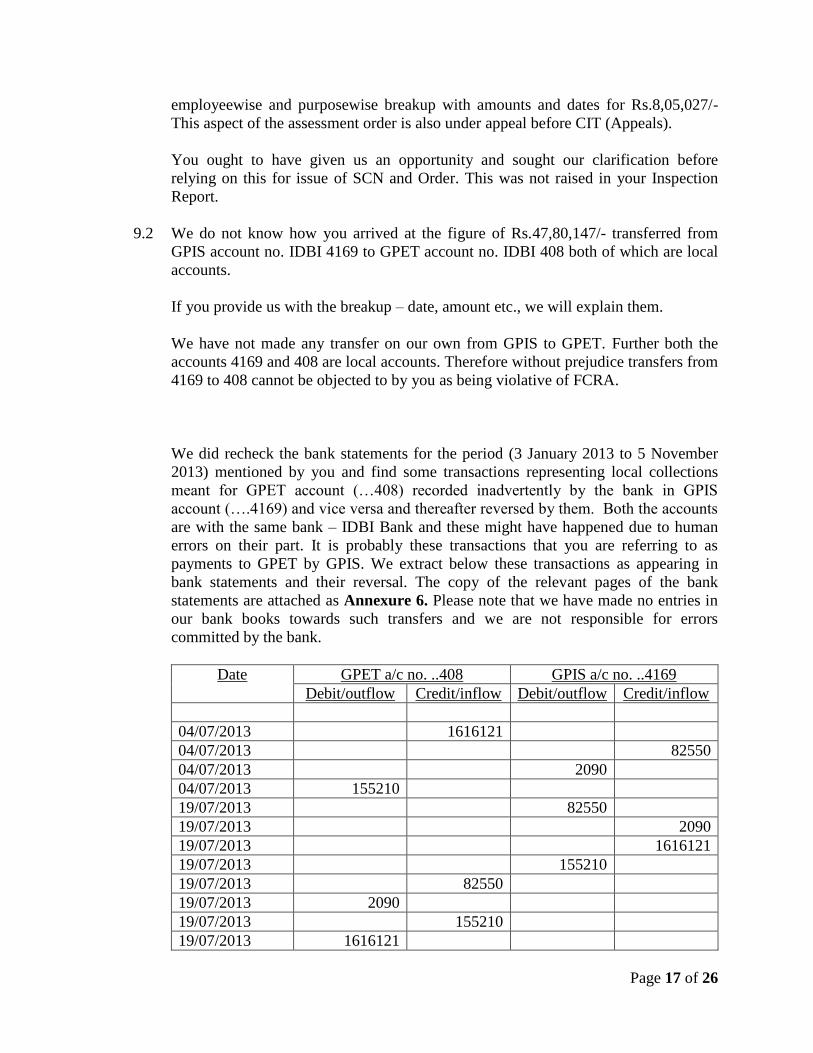

We did recheck the bank statements for the period (3 January 2013 to 5 November

2013) mentioned by you and find some transactions representing local collections

meant for GPET account (…408) recorded inadvertently by the bank in GPIS

account (….4169) and vice versa and thereafter reversed by them. Both the accounts

are with the same bank – IDBI Bank and these might have happened due to human

errors on their part. It is probably these transactions that you are referring to as

payments to GPET by GPIS. We extract below these transactions as appearing in

bank statements and their reversal. The copy of the relevant pages of the bank

statements are attached as Annexure 6. Please note that we have made no entries in

our bank books towards such transfers and we are not responsible for errors

committed by the bank.

Date GPET a/c no. ..408 GPIS a/c no. ..4169

Debit/outflow Credit/inflow Debit/outflow Credit/inflow

04/07/2013 1616121

04/07/2013 82550

04/07/2013 2090

04/07/2013 155210

19/07/2013 82550

19/07/2013 2090

19/07/2013 1616121

19/07/2013 155210

19/07/2013 82550

19/07/2013 2090

19/07/2013 155210

19/07/2013 1616121

Page 18 of 26

In the case of the following transactions in GPET a/c no. ..408 the name of GPIS was

shown inadvertently by the bank in the description column for the initial debit and its

reversal on return. In the subsequent debit on 10 October 2013 the correct name of

GPET only appears. A copy of this statement is also enclosed as Annexure 7.

Date Debit Credit

09-10-2013 200000

09-10-2013 200000

10-10-2013 200000

10. Whereas the association has wilfully suppressed and not disclosed the payment of salary

@ Euro 56,951.16 per annum by Greenpeace International to Greg Muttitt, a foreign

Greenpeace activist, who worked on secondment with Greenpeace India Society in India

for 5 ½ months from 15th

September 2013 to 28 February 2014. He was an important part

of Greenpeace India Society strategy-making and implementation, monitoring of

Greenpeace India Society fund distribution and guiding the planning of protests. He was

paid directly by and his contract signed by Greenpeace International in violation of

Section 33 of FCRA, 2010 by not reporting the details thereof in the returns filed to the

Government;

10.1 Section 2(1) (h) defines foreign contribution as below :-

“2. (1) In this Act, unless the context otherwise requires,—

(h) “foreign contribution” means the donation, delivery or transfer made by

any foreign source,—

(i) of any article, not being an article given to a person as a gift for

his personal use, if the market value, in India, of such article, on

the date of such gift, is not more than such sum as may be specified

from time to time, by the Central Government by the rules made by

it in this behalf;

(ii) of any currency, whether Indian or foreign;

Page 19 of 26

(iii) of any security as defined in clause (h) of section 2 of the

Securities Contracts (Regulation) Act, 1956 (42 of 1956) and

includes any foreign security as defined in clause (o) of section 2 of

the Foreign Exchange Management Act, 1999 (42 of 1999).

10.2 Section 2(h) of Foreign Exchange Management Act (FEMA) read with section 2(2)

of FCRA defines currency.

For the terms ‘security’ and ‘foreign security’, section 2 (1) (h) (iii) of FCRA relies

on FEMA and Securities Contracts (Regulation) Act (SCRA). The term foreign

security is defined in section 2 (o) of FEMA and the term security is defined in

section 2 (h) of SCRA.

10.2.1 FEMA

“Definitions.

2. In this Act, unless the context otherwise requires,—

(h) “currency” includes all currency notes, postal notes, postal

orders, money orders, cheques, drafts, travellers cheques, letters

of credit, bills of exchange and promissory notes, credit cards or

such other similar instruments, as may be notified by the

Reserve Bank;

(o) “foreign security” means any security, in the form of shares,

stocks, bonds, debentures or any other instrument denominated

or expressed in foreign currency and includes securities

expressed in foreign currency, but where redemption or any

form of return such as interest or dividends is payable in Indian

currency;

(za) “security” means shares, stocks, bonds and debentures,

Government securities as defined in the Public Debt Act, 1944

(18 of 1944), savings certificates to which the Government

Savings Certificates Act, 1959 (46 of 1959) applies, deposit

receipts in respect of deposits of securities and units of the Unit

Trust of India established under sub-section (1) of section 3 of

the Unit Trust of India Act, 1963 (52 of 1963) or of any mutual

fund and includes certificates of title to securities, but does not

include bills of exchange or promissory notes other than

Government promissory notes or any other instruments which

may be notified by the Reserve Bank as security for the purposes

of this Act;”

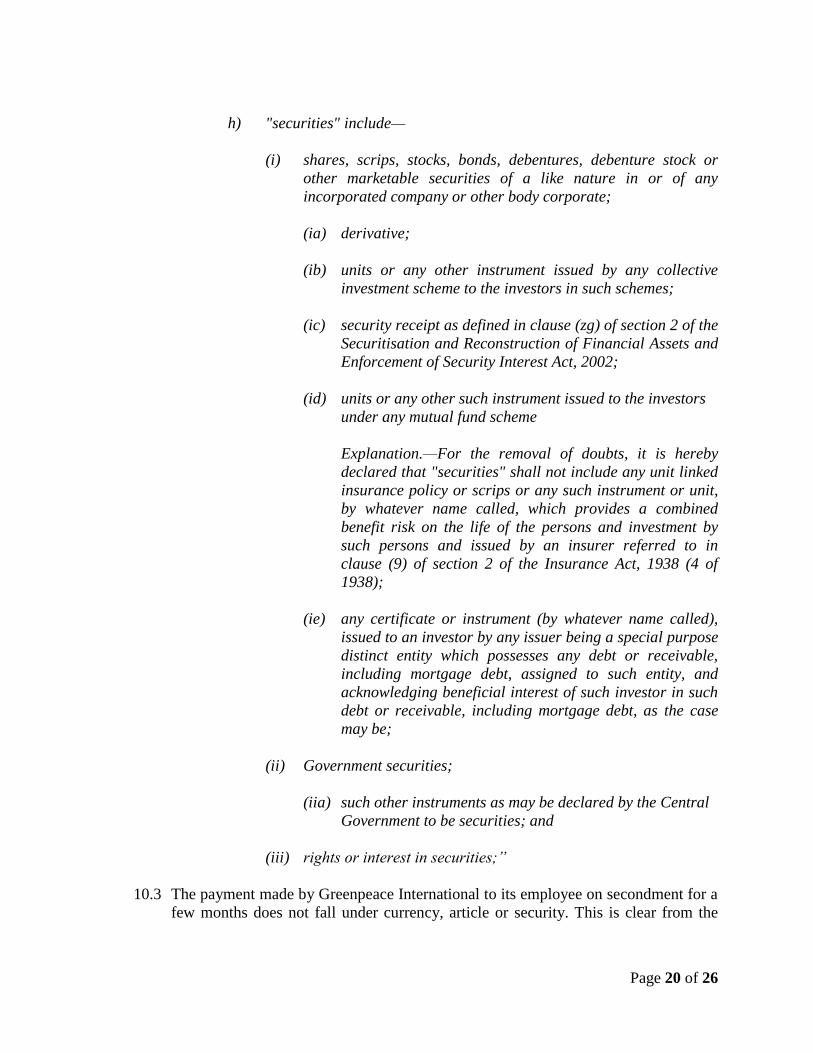

10.2.2 SCRA

Page 20 of 26

h) "securities" include—

(i) shares, scrips, stocks, bonds, debentures, debenture stock or

other marketable securities of a like nature in or of any

incorporated company or other body corporate;

(ia) derivative;

(ib) units or any other instrument issued by any collective

investment scheme to the investors in such schemes;

(ic) security receipt as defined in clause (zg) of section 2 of the

Securitisation and Reconstruction of Financial Assets and

Enforcement of Security Interest Act, 2002;

(id) units or any other such instrument issued to the investors

under any mutual fund scheme

Explanation.—For the removal of doubts, it is hereby

declared that "securities" shall not include any unit linked

insurance policy or scrips or any such instrument or unit,

by whatever name called, which provides a combined

benefit risk on the life of the persons and investment by

such persons and issued by an insurer referred to in

clause (9) of section 2 of the Insurance Act, 1938 (4 of

1938);

(ie) any certificate or instrument (by whatever name called),

issued to an investor by any issuer being a special purpose

distinct entity which possesses any debt or receivable,

including mortgage debt, assigned to such entity, and

acknowledging beneficial interest of such investor in such

debt or receivable, including mortgage debt, as the case

may be;

(ii) Government securities;

(iia) such other instruments as may be declared by the Central

Government to be securities; and

(iii) rights or interest in securities;”

10.3 The payment made by Greenpeace International to its employee on secondment for a

few months does not fall under currency, article or security. This is clear from the

Page 21 of 26

definition reproduced above. Therefore it does not attract section 2(1) (h) and no

reporting requirements are attracted under FCRA.

FCRA does not cover invisibles or benefits accruing to an entity from actions of a

foreign source. If this were to be so even evaluations or review of the programmes

carried out by foreign donors will have to be costed notionally and accounted as

foreign contribution. This is not contemplated at all under FCRA 2010.

10.4 FCRA as the definition under section 2(1) (h) shows covers only tangibles.

The definition under section 2(1) (h) is not an inclusive one. It uses the word

“means” which implies that the definition is limited to currency, article and security

only. The definition cannot be stretched to include the payment by Greenpeace

International to its employee. If the definition is stretched in this manner even

notional interest foregone by a foreign donor in giving grants have to be costed and

accounted as foreign contribution.

10.5 This issue was not raised in your Inspection Report. We should have been given an

opportunity to explain before your relying on this for issue of SCN and Order.

11. Whereas it has also been found that the association has shifted its functioning and

activities from the registered address, New No.47 (Old No.22), 2nd

Cross Street, Ellai

Amman Colony, Chennai – 600 086 (Tamilnadu) to an unreported address at 60,

Wellington Street, Richmond Town, Bengaluru – 560 025 (Karnataka) without

approval/intimation of this Ministry, in violation of the Undertaking & Declaration given

by the association in its application for registration under Rule 9(1) (a) of Foreign

Contribution (Regulation) Rules, 2011.

The registered office of the society as per the FCRA database is New No.47 (Old No.22),

2nd

Cross Street, Ellai Amman Colony, Chennai – 600 086 (Tamilnadu). But, this office is

for name sake only and is used for storing old records. All its activities are being carried

out from 60, Wellington Street, Richmond Town, Bengaluru – 560 025 (Karnataka). The

Annual Report of the society for 2013 shows this Bengaluru address and does not show its

registered Chennai office address. All the vouchers and correspondence of the society also

show its Bengaluru address. At the time of inspection, website of the association,

www.greenpeace.org.in, also did not show the address of its registered Chennai office.

This in effect means that for all practical purposes Greenpeace India Society is functioning

from its Bengaluru office. However, no intimation for the same has been furnished to this

Ministry. Hence, this non-intimation of an important change is a violation of the

Declaration and Undertaking given by the association at the time of seeking registration

under FCRA.

Page 22 of 26

Our Society is registered as a Society under the Tamilnadu Societies Registration Act,

1975 with its registered office address at Chennai which is a clause in its Memorandum of

Association. Hence it cannot change its registered office to another State. Like most

companies and all other organisations in India we have offices in many cities for carrying

out our environmental protection programmes and the office at Bangalore is also a hub for

many such programmes. This does not in any way amount to change of our registered

office or a violation of the declaration given in the application for permanent registration.

The address of the Registered office is shown in the extract of the Balance Sheet as on 31

Dec 2013 appearing in page no 101 of the Annual Report. Vouchers and correspondence

will bear the address where the payment is made or is generated from. Therefore that

cannot be the determinant.

Further your inspection was carried out in our registered office at Chennai only. The extent

of operation that an organisation should have in a location is a matter to be decided by the

organisation.

We had explained the above in our response to your Inspection Report but you have

repeated the same in the SCN and Order without dealing with our response in any manner.

12. Whereas the association has also replaced 50% or more of the executive committee

members without obtaining prior approval of the Central Government which is a violation

of the undertaking & declaration given by the association in its application for registration

under Rule 9 (1) (a) of Foreign Contribution (Regulation) Rules, 2011.

The Undertaking given and Declaration made by Greenpeace India Society in its

application for registration under FCRA, that at any point of time any such change that

causes the replacement of 50% or more of such Members of the Executive

Committee/Governing Council of the association, intimation would be given to Ministry of

Home Affairs within thirty days of such change in accordance with the Undertaking &

Declaration given by the association in its application for registration or prior permission,

as the case may be. Further, as per the Undertaking and Declaration, the association

should not accept any foreign contribution except with prior permission till the permission

to replace the office bearer(s) has been granted by Ministry of Home Affairs, which is in

violation of the Undertaking & Declaration given by the association in its application for

registration under Rule 9 (1) (a) of Foreign Contribution (Regulation) Rules, 2011;

12.1 The undertaking given in the Application for permanent registration under FCRA

2010 states:

Page 23 of 26

(ii) to obtain prior permission for change of Members of the Executive Committee

/Governing Council, if, at any point of time, such change causes replacement of 50%

or more of such Members as were mentioned in the application

no.______________________ dated_____________ for registration under the

Foreign Contribution(Regulation)Act, 2010 (42 of 2010) and undertake further not

to accept any foreign contribution except with prior permission till the permission to

replace the office-bearer(s) has been granted.

This undertaking is broadly in line with that given under FCRA 1976.

It is not every change in the executive council that attracts this undertaking. The

undertaking is attracted only if 50% change happens at “any point of time”.

Cumulative changes over a ten year time frame happening especially due to

retirement, death, induction of new members, non-election etc., cannot be considered

to determine if the 50% rule is violated.

12.2 As per Article 5 (3) forming part of the Memorandum of Association (MoA), of the

Society the minimum number of members of the Executive Committee (EC) which

is the Governing body of the Society is 4 and maximum number is 7. Article 5 (2)

provides : “EC Members shall be elected by a majority vote of the Members at the

Annual General Body Meeting for two-year terms and they shall be eligible for re-

election.”

12.3 Details of the 4 members of the EC mentioned in the Application for permanent

registration in 2005 and subsequent changes in the composition of the EC are shown

in Annexure 8. It can be seen that two more members were elected and added to the

EC in the AGM in Aug 06 (Sl. Nos. 5 & 6) taking the total strength of EC to 6.

Subsequent changes are gradual by way of election of new members in place of those

retiring on completion of their tenure of two years or those who resign from

membership for any reason. It can be seen that one member of the 4 mentioned in the

above Application (Sl.No1) resigned in Jan 07 and another member (Sl. No2) did not

offer for re-election on completion of his term in Aug 07 and thus retired. In their

places two members (Sl Nos.7 & 8) were elected in the AGM held on Aug 07.

The third member mentioned in the Application (Sl No. 4) retired by not offering for

re-election on completion of his term in Aug 08 and in his place a new member (Sl

No.9) was elected in that AGM.

In the AGM held on Aug 08 an additional member (Sl. No. 10) was elected to the EC

taking its strength to 7 which is the maximum permissible under the MoA.

The 4th

member mentioned in the Application for permanent registration (Sl No. 3)

retired by not offering for re-election in the AGM held on Aug 10 and in her place a

new member (Sl. No. 11) was elected in the AGM.

Page 24 of 26

12.4 Thus, it can be seen that there was no change in the membership or the composition

of the Executive Committee amounting to 50% of the number of members mentioned

in the Application for permanent registration at any point of time as per our

undertaking in that application and the changes were gradual over the period of 5

years after grant of permanent registration and effected by the democratic process as

per Article 5 (2) of the Rules and Regulations mentioned above. Such gradual

changes happening over a period of time in the composition of governing council is a

normal process in any democratic organisation, be it a company or a Government

body or a charitable organisation. It cannot be the intention of any law to bring such

changes occurring over a long period within the ambit of the undertaking. Hence

there has been no contravention of the undertaking and declaration given in the

Application for permanent registration.

12.5 Moreover, we have furnished the above details of changes in the membership of the

Society to your office in reply to Question No. 25 of your Questionnaire vide our

letter dated 28 Sep 2012 sent by Speed Post Ack.

12.6 Without prejudice the following points are relevant :-

12.6.1 The declaration is neither referred to in FCRA nor the Rules. Therefore

there is no legal backup for this declaration.

12.6.2 Further organisations registered under FCRA before the form was amended

would not have given this undertaking making it discriminatory.

12.6.3 With the introduction of renewal of registration every five years (proviso to

section 11(1) of FCRA) the entire declaration is redundant as in any case

you look into all aspects before renewal.

12.6.4 Declaration was possibly to prevent wholesale takeover of organisations

enjoying FCRA registration without due diligence by MHA of the new EC

members. Where the change is gradual over many years due to election,

death, resignation etc., applying this declaration is incorrect and does not

subserve the purposes for which it was introduced.

13. And whereas, the Central Government having regard to the information and evidence in its

possession is satisfied that the acceptance of foreign contribution by the said Association,

Greenpeace India Society, New No.47 (old No.22), 2nd

cross Street, Ellai Amman colony,

Gopalapuram, Chennai – 600086, Tamilnadu, has prejudicially affected the public

interest in violation of Section 12(4)(f)(iii) and has prejudicially affected the economic

interest of the State in violation of Section 12(4)(f)(ii) of FCRA, 2010, which violates

conditions of grant of Certificate of registration;

13.1 Sections 12(4) (f) (ii) and (iii) read as below :

Page 25 of 26

“12. Grant of certificate of registration

(4) The following shall be the conditions for the purposes of sub-section (3),

namely:-

(f) the acceptance of foreign contribution by the person referred to in

sub-section (1) is not likely to affect prejudicially –

(i) The security, strategic, scientific or economic interest of the

State; or

(ii) The public interest; or”

13.2 There is no violation of section 12(4) (f) (ii) and (iii) of FCRA 2010. These sections

come into play only if the actions affect prejudicially the security, strategic, scientific

or economic interest of the state and the public interest. All our activities further

public interest and promote the economic, strategic, security and scientific interest of

the state. It is not clear from your SCN/Order as to how these interests are affected

adversely by our activities. Protection of environment, interest of the tribals, forestry

and wildlife and offering alternative policies cannot be considered to be against the

interest of the country/public/state in any manner.

13.3 Holding and advocating views which are contrary to the economic, agricultural,

industrial and financial policies pursued by the Government of the day at a given

point in time cannot be considered as against public interest. As noted in the recent

decisions of the Evironment Ministry and Coal Ministry in relation to coal mining

and the Mahan Forest, heeding the views of civil society organisations and public

opinion generated by people’s movements can lead governments to change policies

and that is the essence of democracy. Greenpeace India Society is as much Indian

and committed to the development of India as the rest of India and the Government

are. Civil society organisations are entitled to disagree with the policies of the

Government of India. Such disagreement cannot, per se be construed as detrimental

to national interest. As the Delhi High Court has stated:

“Non-Governmental Organizations often take positions, which are contrary to the

policies formulated by the Government of the day. That by itself, in my view,

cannot be used to portray, petitioner’s action as being detrimental to national

interest. The government is free to execute its policies as it has the mandate of the

people behind it, notwithstanding a different point of view of Non-Governmental

Organizations, such as the petitioner.”

13.3 Your SCN does not bring out any violation of section 12 (4) (f) (ii) and (iii) of

FCRA. We have furnished detailed explanations with respect to each of your grounds

in the SCN. There are no violations of FCRA brought out in the SCN when read with

our reply. In any case it is not clear as to how the security, strategic, scientific or

economic interest of the country or the public interest is affected by any of the

grounds relied on by you in the SCN.

Page 26 of 26

Under the circumstances explained above we request you drop further proceedings, remove the

suspension of our certificate of registration under FCRA, defreeze all our bank accounts and

refrain from cancelling our certificate under section 14. We request you to give us an opportunity

for personal hearing in case you decide to proceed further.

We have also separately represented to the Secretary, Ministry of Home Affairs in response to

your Order dated 9 April 2015 under section 13 suspending our registration under FCRA.

For Greenpeace India Society

Samit Aich

Executive Director.