Embed Size (px)

Citation preview

FTL_ACTIVE 5339732.4

OMNIBUS GRANTOR TRUST RULES

Debra L. Boje, Esq.Gunster, Yoakley & Stewart, P.A.401 E. Jackson Street, Suite 2500

Tampa, Florida 33602

FTL_ACTIVE 5339732.4 1

I. WHY IS IT IMPORTANT TO KNOW IF A TRUST IS A GRANTOR TRUST?

A. Classification of Trusts for Federal Income Tax Purposes: Subchapter J of the Internal Revenue Code of 1986, as amended, (“Code or “I.R.C.”) governs the taxation of estates, trusts, beneficiaries, and decedents. There are two basic types of trusts for federal income tax purposes: “grantor trusts” (which this outline addresses) that are governed by Subpart E of Subchapter J (§§ 673 – 679) and all other trusts that are governed by Subpart A-D of Subchapter J. It is important to determine the type of trust to determine who is the taxpayer for purposes of reporting “income, deductions, and credits” for federal income tax purposes.

B. What Is a Grantor Trust?

1. A grantor trust is a trust in which the grantor (as defined below) retainscertain rights or powers over the trust that cause all or part of the trust’s income, deductions, and credits to be taxed or imputed directly to the grantor (as opposed to the trust or its beneficiaries). The separate existence of the trust is disregarded for federal income tax purposes, but not necessarily for federal gift or estate tax purposes.

The term “grantor trust” is not used in either the Code or the Treasury Regulations.

2. During the settlor’s lifetime a revocable trust is almost always a grantor trust because the settlor retains the right to revoke or amend the trust. I.R.C. § 676(a). The analysis of whether a trust is a grantor trust usually is only necessary if and when the trust becomes irrevocable.

3. A trust that is not a grantor trust generally is recognized as a separate taxable entity and is taxed under the normal rules of Subchapter J, Subparts A–D. (I.R.C. §§ 641 – 668; I.R.C. § 671; Treas. Regs. § 1.671-2(d). A trust that is treated as a separate entity reports its own income and deductions. The trust pays income tax on its taxable income; however, in determining its taxable income, the trust is entitled to a deduction for amounts actually distributed or required to be distributed to beneficiaries. The distributions carry out “distributable net income” or “DNI” proportionately to the distributions the beneficiaries receive. The beneficiaries in turn must include the taxable portion of the distribution in their own taxable income.

FTL_ACTIVE 5339732.4 2

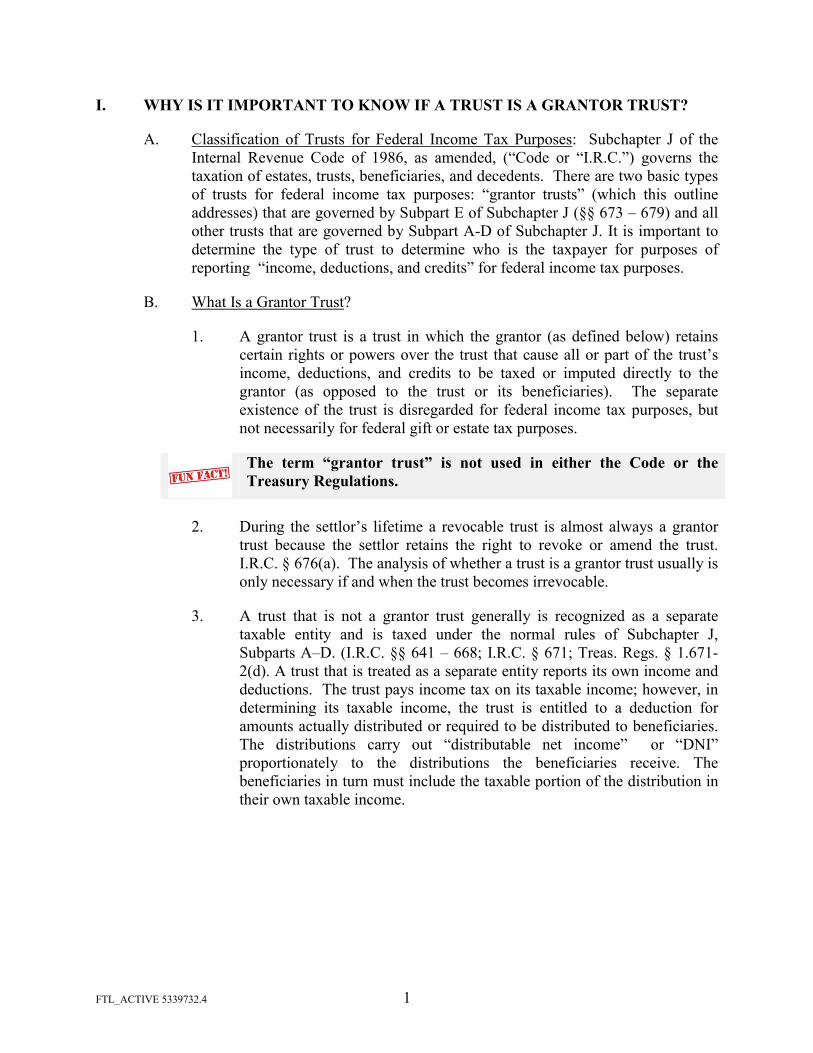

C. The Evolution of the Grantor Trust Rules

1. Before the Tax Reform Act of 1986, the graduated tax brackets of individuals and trusts were the same. Thus, high-bracket taxpayers (grantors) saw the opportunity to use trusts to shift income to lower tax bracket taxpayers (i.e., trusts), thus running the brackets on income. Not wanting to lose control over the trust assets, the trusts were drafted to allow the grantors to retain various rights and powers over the trust’sassets.

2. To combat abuse, the “grantor trust rules” were enacted. Although the roots of the rules first took hold in the Internal Revenue Code of 1954, traces of the rules can be found as far back as the Revenue Act of 1924. Today, the grantor trust rules are found in §§ 671 through 679 (Subchapter J, Subpart E) of the Code.

3. The Tax Reform Act of 1986 adjusted the income tax brackets for trusts tograduate much quicker than individual income tax brackets, thus reducing the appeal to create a trust to “run the brackets.”

FEDERAL INCOME TAX RATES

TRUSTS UNMARRIED INDIVIDUALIncome Rate Income Rate

$0 to $2,600 10% $0 - $9,700 10%$2,601 - $9,300 $260 plus 24%

over $2,600$9,701 - $39,475 $970 plus 12% over

$9,700$9,301 - $12,750 $1,868 plus 35%

over $9,300$39,476 - $84,200 $4,543 plus 22% over

$39,475$12,751 or more $3,075.50 plus

37% over $12,750

$160,726 - $204,100 $32,748.50 plus 32% over $160,725

$204,101 - $510,300 $46,628.50 plus 35% over $204,100

$510,301 or more $153,798.50 plus 37% over $510,300

4. Despite the adjustment to the tax brackets for trusts the grantor trust rules still remain an important factor to consider when drafting or administering a trust.

II. OVERVIEW OF THE GRANTOR TRUST RULES

A. Key Terms

1. Who is the grantor? To determine who is a grantor it is necessary to look at Treas. Regs. § 1.671-2(e).

FTL_ACTIVE 5339732.4 3

a. A grantor includes any person to the extent the person eithercreates a trust, or directly or indirectly makes a gratuitous transfer of property to a trust.

(i) If a person creates or funds a trust on behalf of another person, both persons are treated as a grantor of such trust.

(ii) The term “property” includes cash.

(iii) A person who funds a trust with an amount that is directly reimbursed to such person within a reasonable period of time and who makes no other transfers to the trust that constitute gratuitous transfers is not treated as an owner of any portion of the trust. The person, however, is considered to be a grantor of the trust.

b. Corporations or partnership as grantor.

(i) If a gratuitous transfer is made by a partnership or corporation to a trust for a business purpose of the partnership or corporation, the partnership or corporation will generally be treated as the grantor of the trust. Treas. Regs. § 1.671-2(e)(4).

(ii) If a gratuitous transfer is made by a partnership or corporation to a trust not for a business purpose of the partnership or corporation, but for the personal purposes of one or more of the partners or shareholders, the partner or shareholder will be treated as the grantor of the trust. Treas. Regs. § 1.671-2(e)(4).

c. Trust to trust transfers.

(a) If a trust makes a gratuitous transfer of property to another trust, the grantor of the transferor trust generally will be treated as the grantor of the transferee trust. The trustee is not treated as the grantor. Treas. Regs. § 1.671-2(e)(5).

(b) If one exercises a general power of appointment over a trust fund in favor of a second trust, he or shewill be deemed the grantor of the second trust, even if the grantor of the first trust is treated as its owner under the grantor trust rules. Id.

FTL_ACTIVE 5339732.4 4

d. Involuntary grantor.

Trusts occasionally are created with funds belonging to one who does not have the legal capacity to create a trust. The IRS tends to view the individual receiving the benefit of the trust as the grantor. Rev. Rul. 83-25, 1983-1 C.B. 116.

When reciprocal trusts are created, a settlor may be re-characterized as the grantor of the trust that he or she did not create. Krause v. Commissioner, 497 F.2d 1109 (6th Cir. 1974).

2. What is a gratuitous transfer?

a. A gratuitous transfer is any transfer other than a transfer for fair market value.

(i) It is irrelevant whether the transfer constitutes a gift for gift tax purposes (i.e., there does not need to be a completed gift). Treas. Regs. § 1.671-2(e)(2)(i).

(ii) A transfer will not be considered made for fair marketvalue just because the transferor recognizes gain on the transfer. Treas. Regs. § 1.671-2(e)(2)(ii).

(iii) A transfer is for fair market value only to the extent of the value of property received from the trust, services rendered by the trust, or the right to use the property of the trust.

(a) An interest in the trust is not property received from the trust. Treas. Regs. § 1.671-2(e)(2)(ii).

(b) Rents, royalties, interest, and compensation paid to a trust can be transfers for fair market value if the payment reflects an arm’s length price.

3. What is income?

Treas. Regs. § 1.671-2(b) provides that unless specifically limited, income for purposes of Subpart E (the grantor trust rules) refers to “income” determined for tax purposes and not to income determined for fiduciary accounting purposes. If income for fiduciary accounting purposes is intended, the term “ordinary income” is used.

The definition of income under the grantor trust provisions is an exception to the general rules. For the rest of Subchapter J the term “income” (unless modified by the terms “gross,” “taxable,” or “distributable net”) means fiduciary accounting income as determined

FTL_ACTIVE 5339732.4 5

under state law. I.R.C. § 643(b).

4. Who is a nonadverse party?

A nonadverse party is anyone who is not an adverse party. I.R.C. § 672(b); Treas. Regs. § 1.672(b)-1.

5. Who is an adverse party?

a. Any person having a beneficial interest in the trust (including a power of appointment over the trust) is an adverse party,

(i) No attribution rules apply (not deemed to own due to family ownership).

(ii) Mere fiduciary relationship and right to fees does not create beneficial interest in the trustee. Treas. Regs. § 1.672(a)-1(a); Duffy v. United States, 487 F.2d 282 (6th Cir. 1973), cert. denied, 416 U.S. 938 (1974).

b. Whose interest is substantial.

(i) Low standard: substantial if “value in relation to the total value of the property subject to the power is not insignificant.” Treas. Regs. § 1.672(a)-1(a).

(ii) The interest does not have to be vested in order to be substantial. The interest can be contingent. Treas. Regs. § 1.672(a)-1(c).

c. Whose interest would be adversely affected by the exercise or nonexercise of the power held by the grantor or a nonadverse party.

(i) One’s interest is adverse to the exercise or nonexercise of the grantor’s or nonadverse party’s power only if, and to the extent that, such exercise or nonexercise will affect the amount of income or principal received by the party. Treas. Regs. § 1.672(a)-1(b).

(ii) Generally, an interest of a remainderman is only adverse as to the exercise of a power over principal. Treas. Regs. § 1.672(a)-1(d). The interest of an income beneficiary would be adverse as to a power over income and may be adverse as to a power over principal if the power over principal could alter the income interest. Treas. Regs. § 1.672(a)-1(c).

FTL_ACTIVE 5339732.4 6

6. Who is a related or subordinate party? Any nonadverse party who is:

a. The grantor’s spouse (if living with the grantor);

b. The grantor’s mother, father, issue, brother, or sister (includes half-bloods);

c. Employees of the grantor (not attorneys and accountants) (Bennett v. Commissioner, 79 T.C. 470 (1982); I.R.C. § 672(c)(2); Rev. Rul. 66-160, 1966-1 C.B. 164); and

d. A corporation or employee of a corporation in which the stock holdings of the grantor and the trust are significant from the viewpoint of voting control or a subordinate employee of a corporation in which the grantor is an executive.

7. What is the spousal unity rule?

a. The grantor is deemed to hold any power or interest held by:

(i) Any individual who was the spouse of the grantor at the time of the creation of such power or interest or

(ii) Any individual who became the spouse of the grantor after the creation of such power or interest, but only with respect to periods after such individual became the spouse of the grantor. I.R.C. § 672(e)(1).

b. An individual who is legally separated from his spouse under a divorce decree (or other separate maintenance order) “shall not be considered as married.” I.R.C. § 672(e)(2) (emphasis added).

c. The extent to which a subsequent divorce cuts off the spousal unity rule as to that prior spouse is not clear. I.R.C. § 672(e)(2) does not say that § 672(e)(1) no longer applies following a divorce; it merely says the persons are not considered as married.

d. “Curiously, § 672(e) does not indicate whether spousal unity ends when the marriage does, § 672(e)(1)(B) making it clear only that marriage when the interest or power was created is not required if they subsequently get married. In addition, § 682 overrides the special unity rule following a divorce or legal separation, but only to the extent the spouse is entitled to income from the trust, and not otherwise. Thus, it does not turn off grantor trust status attributable to powers . . . And it might not apply with respect to discretionary income or capital gains that are allocable to corpus and are not distributed currently to the spouse [citing Treas. Regs. § 1.682(a)-1(a)(1)(i)] . . . [Section] 7701(a)(17) limits the definition of

FTL_ACTIVE 5339732.4 7

husband and wife as including a former spouse only for specified purposes. Arguably the failure to include § 672(e) in that list is indicative of an intent that former spouses not be subject to § 672(e). If that was true, however, query why Congress made it explicit that §§ 674(c) and 675(3) (last sentences) are applicable only ‘for periods during which an individual is the spouse of the grantor’ but no specific provision otherwise establishes that a §672(e) or § 677(a) capital gain problem can be divorced.” CASNER & PENNELL, ESTATE PLANNING (8th ed) §5.11.1 n. 36.

B. What Powers or Rights Cause a Trust to be a Grantor Trust?

1. Code §§ Sections 673-677 specify the following five circumstances under which the grantor will be treated as the owner and taxed on all or part of the income of the trust:

a. If the grantor has retained a reversionary interest under I.R.C. § 673;

b. If the grantor or a non-adverse party has certain powers over the beneficial interests in the trust under I.R.C. § 674;

c. If certain administrative powers over the trust exist under which the grantor can or does benefit under I.R.C. § 675;

d. If the grantor or a non-adverse party has a power to revoke the trust or return the corpus to the grantor under I.R.C. § 676; or

e. If the grantor or a non-adverse party has the power to distribute income to or for the benefit of the grantor or the grantor’s spouse under I.R.C. § 677.

Treas. Regs. § 1.671-1(a).

2. I.R.C. § 678 sets forth circumstances in which persons other than the grantor will be treated as a substantial owner.

3. I.R.C. § 679 sets forth special rules when a foreign trust having one or more U.S. beneficiaries may be treated as a grantor trust.

A person who creates a trust but makes no gratuitous transfer to the trust is not treated as the owner of any portion of the trust for purposes of applying the grantor trust rules (Note: this will keep the trustee who creates a trust for decanting purposes from becoming the grantor).

FTL_ACTIVE 5339732.4 8

C. Tax Consequences of Being a Grantor Trust.

When the grantor or (another person) is treated as the owner of any portion of a trust under I.R.C. §§ 671-679, the grantor (or other person) must include all items of income, deductions, and credits that are attributable to that portion of the trust in which the grantor is deemed the owner in computing his or her own taxable income on his or her income tax return.

If the grantor is treated as owning all of part of the trust for purposes of reporting income,the grantor also will be treated as owning the same portion of the trust for purposes of reporting deductions and credits. Thus, throughout this outline if the grantor is required to report all or part of the income, assume that the grantor also will report deductions and credits related to that portion.

D. What “Portion” of the Trust Treated as a Grantor Trust Is So Taxed?

1. The grantor may be taxed as the owner of all or “any portion of the trust.”

2. A portion may consist of specific trust property, an undivided fractional interest, an interest represented by a dollar amount (pecuniary share), only ordinary income, or only income allocated to corpus. Treas. Regs. §1.671-3.

3. A grantor who owns only a portion of the trust includes in his or her tax computation the income, deductions, and credits allocable to the portion of the trust the grantor is deemed to own. Treas. Regs. § 1.671-3(a).

PLANNING POINTER: If the intent is to create a grantor trust, it is generally desirable to ensure that the grantor is treated as the owner of the entire trust.

E. Certain Types of Trusts Excluded.

The grantor trust rules do not apply to pooled income funds, charitable remainder annuity trusts, and charitable remainder unitrusts, as defined in I.R.C. §§ 642(c)(5) and 664(d), merely because the grantor retains the right to income and principal payments from a pooled income fund or charitable remainder trust. Treas. Regs. § 1.671-1(d).

F. Application of Other Code Provisions.

Just because a grantor may not be subject to tax under the grantor trust rules does not mean he or she will not be taxed on the trust income under other tax principles. Examples: Assignment of income doctrine (Treas. Regs. § 1.671-1(c)); transfers-leasebacks (Treas. Regs. § 1.671-1(c)); discharge of legal

FTL_ACTIVE 5339732.4 9

obligations (Treas. Regs. § 1.671-1(c)); nonexempt employee deferred compensation plans (Prop. Treas. Regs. § 1.671-1(g)).

III. BROAD OVERVIEW OF THE POWERS AND/OR RIGHTS THAT CAUSE GRANTOR TRUST STATUS

A. Reversionary Interest — I.R.C. § 673

1. If the grantor retains a reversionary interest in the income or principal of a trust with a value (at the time of the transfer to the trust) that is worth 5%or more of the value of the trust, the grantor is taxed as the owner of the portion of the trust equal to the reversionary interest.

2. Example: P creates a trust for the benefit of C. The trust provides for income and principal distributions to C for life. Upon C’s death any property remaining in the trust reverts to P if P is living, or if not, to P’s estate. P has a reversionary interest. Assuming that interest is worth at least 5% of the value of the trust, the trust is a grantor trust.

3. The actuarial rules under I.R.C. § 2031 are used to value the reversionaryinterest and the tables under I.R.C. § 7520 apply. The tables are based on the prevailing interest rates in effect for the month of the transfer using the federal mid-term interest rate.

4. I.R.C. 673(b) carves out an exception for grantor trust treatment for conventional I.R.C. § 2503(c) minor trusts if the grantor (or grantor’s spouse) merely has a reversionary interest by reason of the fact that the trust would revert back to him or her in the event the minor dies before the age of 21 without the child exercising his or her general power of appointment.

5. For estate tax purposes, I.R.C. § 2037 provides that the gross estate shall include the value of all property that the decedent transfers during lifetime in which the decedent retains a reversionary interest worth more than 5% of the total value of the property on the date of the decedent’s death. Thus, if avoidance of inclusion for estate tax is desired, then for planning purposes creation of a grantor trust under I.R.C. § 673 is not recommended.

This provision was put into the Code in response to the Supreme Court’s decision in Clifford v Helvering 309 U.S. 331 (1940).

B. Power to Control Beneficial Enjoyment – I.R.C. § 674.

1. A grantor is treated as the owner of a trust and taxed on its income if the grantor or a non-adverse party (or both) has the power to affect the

FTL_ACTIVE 5339732.4 10

beneficial enjoyment of the trust corpus or income without the approval or consent of an adverse party.

2. Example: P is the grantor of a trust. P only retains the right to “sprinkle” the trust’s income among the beneficiaries. P will be treated as the owner of the trust income.

3. A power held by the grantor to add beneficiaries to a trust also will cause the grantor to be treated as the owner unless the power is limited to only after-born or after-adopted children. I.R.C. § 674(b)(5)

4. The “power” does not have to be held directly by the grantor. The power can be held by a non-adverse party.

5. There are an number of important exceptions to the general rule that apply and are set forth in I.R.C. § 674(b), (c) and (d). These exceptions are extremely detailed and beyond the scope of this outline.

a. I.R.C. § 674(b) sets forth exceptions for powers that can be held by anyone including the grantor.

b. I.R.C. § 674(c) sets forth exceptions for powers that can be held by an independent trustee.

c. I.R.C. § 674(d) sets forth exceptions for powers that can be held if limited by a standard.

PLANNING POINTER: An I.R.C. § 674 power can be created by including a limited or special power of appointment in the trust. The grantor merely has to have the power. It is not required that the grantor have the capacity to presently exercise the power.

C. Administrative Powers - I.R.C. § 675.

1. A grantor is treated as the owner of the trust if the grantor or any non-adverse person (or both) possesses certain administrative rights that are primarily for the grantor’s benefit, rather than for the benefit of the beneficiaries, or are exercisable in a nonfiduciary capacity.

2. I.R.C. § 675 provides for four categories of prohibited administrative powers.

FTL_ACTIVE 5339732.4 11

a. Power to deal with trust property for less than adequate consideration.

b. Power to borrow trust assets without adequate interest or security;

PLANNING POINTER: The power to borrow without adequate interest could create gift and estate tax consequences if exercised and inadequate interest issues also could be triggered under I.R.C. § 7872. In addition, unless the grantor borrows the entire corpus, it is unclear what portion of the trust the grantor will be treated as owning.

PLANNING POINTER: If the grantor wants to retain the power to borrow, but does not want the trust to be a grantor trust then the trust document specifically should prohibit the trustee from making loans to any person without adequate interest and security and the trustee should not be the grantor or related or subordinate to the grantor.

c. Actual borrowing of trust assets (without adequate interest or security) without repayment during the tax year (this includes indirect borrowing by the grantor or the grantor’s spouse (e.g., loan to an entity in which the grantor holds an interest)).

d. Certain administrative powers exercisable in a nonfiduciary capacity by the grantor or a nonadverse party without the approval or consent of a person in a fiduciary capacity (this includes powers to vote stock or other securities of a corporation in which the holdings of the grantor and the trust are significant from the viewpoint of voting control, to control investments of the trust funds, or to substitute property of an equivalent value).

(i) Fiduciary capacity defined.

(a) When a trustee holds any power, such power is presumed to be held in a fiduciary capacity unless it can be shown by clear and convincing evidence that the power is not exercisable primarily in the interest of the trust beneficiaries. Treas. Regs. § 1.675-1(b)(4).

(b) If a power is not exercisable by a person as trustee, the determination of whether the power is exercisable in a fiduciary or nonfiduciary capacity depends on all the terms of the trust and the circumstances surrounding its creation and administration.

FTL_ACTIVE 5339732.4 12

(ii) Power of Substitution - This power is discussed in more detail below as it is one of the more common powers used to create grantor trust status.

D. Power to Revoke - I.R.C. § 676.

1. The grantor will be treated as the owner of any part of a trust to which the grantor (the grantor’s spouse) or any non-adverse party has the power to revest title to trust assets in the grantor.

2. A traditional revocable trust is the most common example.

3. The power to revest title includes the power to revoke, terminate, alter, amend, or appoint. Treas. Regs. § 1.676(a)-1.

4. A power to revoke does not create a grantor trust under I.R.C. § 676 if the power of revocation can only be exercised after a time period that is so long that, if the power to revoke had been a reversionary interest, ownership of that interest would not cause the trust to become a grantor trust pursuant to I.R.C. § 673 (i.e., the reversionary interest would not be valued at more than 5% of the trust assets). I.R.C. § 676(b).

PLANNING POINTER: Although the trend in most states is to treat a trust as revocable unless stated otherwise in the trust document, the drafter should specify whether the trust is amendable or revocable. It is also recommended that the trust provide the manner in which the power may be exercised (e.g., in writing delivered to the trustee during the settlor’s lifetime).

By default, a Florida trust created after July 1, 2017, is revocable by the settlor unless the trust expressly states otherwise. Fla.Stat. § 736.0602(1).

E. Income for the Benefit of the Grantor - I.R.C. § 677.

1. The grantor will be treated as the owner of any portion of a trust if the income from the trust is or may, in the discretion of the grantor, the grantor’s spouse, or a non-adverse person without the consent of an adverse party, be:

(i) Distributed to the grantor or the grantor’s spouse;

(ii) Accumulated for future distributions to the grantor or the grantor’s spouse; or

(iii) Applied to the payment of insurance policies on the life of the grantor or the grantor’s spouse.

FTL_ACTIVE 5339732.4 13

2. If the consent of an adverse party is required to make the distribution to (or for the benefit of) the grantor or the grantor’s spouse this provision does not apply.

3. If only the income portion of the trust can be accumulated then the grantor will be taxed only on the ordinary income items and the trust will be taxed on capital gains. Treas. Regs. § 1.677(a)-1(e) and (g). If the capital gain items can be held or accumulated for future distributions then capital gains also will be taxed to the grantor. Treas. Regs. § 1.677(a)-1(f) and (g).

4. Grantor trust treatment will not result merely because income of the trust can be used to provide for the support or maintenance of a beneficiary (other than the grantor’s spouse) that the grantor has a legal obligation to support. Rather, grantor trust treatment only will be triggered if income is actually used for the beneficiary’s support or maintenance. I.R.C. § 677(b). NOTE: if the spouse is a potential discretionary beneficiary of the trust this will cause the trust to be a grantor trust under I.R.C. § 677.

PLANNING POINTER: If intentionally trying to create a grantor trust it is not recommended not to rely on income distributions to the grantor’s spouse as the spouse could die before the grantor.

5. Impact of divorce – it is unclear whether divorce after the creation of the trust will cause the trust to lose grantor trust status. The spousal unity rule in I.R.C. § 672(e) provides that the test is administered at the time the interest is created.

F. Persons Other Than Grantor Treated As Owner – I.R.C. § 678.

1. A person other than the grantor of a trust will be treated as owning the trust assets if that person holds one or more of the following powers:

(i) The unilateral right to withdraw the trust corpus or income;

(ii) Retention of a grantor trust-type of power (under I.R.C. §§ 673-677) over the assets after having released a power to withdraw trust corpus or income; or

FTL_ACTIVE 5339732.4 14

(iii) The actual use of trust income to discharge the holder’s legal support obligation.

2. Crummey powers can cause a beneficiary to be treated as an owner of a portion of the trust.

a. A Crummey power is a power that generally permits the beneficiary to demand annually the lesser of the annual gift tax exclusion amount (which for the year 2019 is $15,000) or the amount of the gifts made to the trust.

b. The portion of the trust that is taxable to the beneficiary as the owner can be difficult to determine. This is especially the case if the power is allowed to lapse (which is often the case) or the contributions to the trust exceed the demand power.

3. If the grantor holds a power over the trust assets that would cause the grantor to be treated as the owner of all or part of the trust income and at the same time a beneficiary holds a power that otherwise would cause the beneficiary to be treated as the owner of the same income then the beneficiary’s power is disregarded and the grantor is treated as the owner and taxed on the trust income. I.R.C. § 678(b).

If the grantor is treated as owning only the principal (capital gains), then the beneficiary can be treated as being the owner of the income of the trust.

G. Foreign Trust with U.S. Beneficiaries — I.R.C. § 679.

1. I.R.C. § 679 treats the U.S. grantor of a foreign trust that has one or more U.S. beneficiaries as the owner of the trust’s assets under the grantor trust rules. Unlike the other grantor trust rules, I.R.C. § 679 applies regardless of the terms of the trust and regardless of any powers or interest the U.S. grantor or any other person may have with respect to the trust income or corpus.

2. The discussion of foreign trusts is beyond the scope of this outline.

IV. COMMON POWERS USED TO CREATE A GRANTOR TRUST.

A. Powers Generally Used to Create a Grantor Trust.

1. Power to add charitable beneficiaries under I.R.C. § 674(b)(5) [see Treas. Regs. § 1.674(d)-2; example 1].

a. Must apply to all trust property if the trust is to be entirely a grantor trust

FTL_ACTIVE 5339732.4 15

b. The grantor should not be given this power because the retained power will cause the transfer to be an incomplete gift and could cause the trust assets to be included in the grantor’s estate under I.R.C. §§ 2036 and 2038. If the power is given to the trustee this may cause the trustee to breach the trustee’s fiduciary duties if the power is exercised. It may be preferable to give the power to a nontrustee who is non-adverse (consider a trust protector);

2. Power to make loans to the grantor without adequate security under I.R.C. § 675(2)

a. Make sure the loan bears adequate interest to avoid trust assets from being included in the grantor’s estate under I.R.C. §§ 2036 and 2038.

b. As an added precaution in lieu of allowing loans to the grantor allow loans to the grantor’s spouse. The spousal unity rule would treat the power as if it were held by the grantor. NOTE: there is no spousal unity rule for estate tax purposes.

3. Power of Substitution under I.R.C. § 675(4)(C).

a. The property substituted must be of equal value.

b. The power must be held in a nonfiduciary capacity, thus the power should not be held by the trustee nor should the trustee’s approval or consent be required.

c. Contrary: to I.R.C. § 675(4), which says the administrative power (which includes the power of substitution) can be held “by any person.” Treas. Regs. § 1.675-1(b)(4) refers to powers of administration held in a nonficuciary capacity “by any non-adverse party.” Thus, it is recommend that a beneficiary not hold the power.

d. Revenue Ruling 2008-22 provides support for the position that the grantor’s nonfiduciary power of substitution will not trigger inclusion under I.R.C. §§ 2036 and 2038 if the trustee has the duty under local law or the trust instrument to ensure that the property substituted is of equal value and the grantor does not have the power to swap property that shifts the benefits of the beneficiaries.

PLANNING POINTER: In an abundance of caution,consideration should be given to granting the substitution power to the grantor’s spouse if the spouse is not a beneficiary of the trust. As noted above, the spousal unity rule would treat the power as if it were held by the grantor. Because there is no spousal unity rule

FTL_ACTIVE 5339732.4 16

for estate tax purposes this should eliminate any I.R.C. §§ 2036 and 2038 inclusion concerns.

PLANNING POINTER: This power has the benefit of allowing the grantor to reaquire highly appreciated assets from the trust in order to receive a stepped-up basis on death.

4. Power to use income to pay premiums on insurance on the life of the grantor or the grantor’s spouse under I.R.C. § 677(a)(3)

a. Caution: Priv. Ltr. Rul. 8839008 putting into question whether the trust income actually must be used on life insurance premiums.

B. The foregoing powers are the most common powers used to cause a trust to be a grantor trust for income tax purposes. Nonetheless, there is still some risk that even these powers may cause the trust to be included in the grantor’s estate for federal estate tax purposes. Caution also should be given if using the spouse to create a grantor trust because a divorce or death of the spouse could terminate the grantor trust status.

PLANNING POINTER: If grantor trust status is desired, it is recommended that the drafter state in the document the settlor’s intention to treat the trust as a grantor trust.

V. Tax Implications.

A. Gift Tax Effects of Grantor’s Payment of Income Tax on Trust Income.

Revenue Ruling 2004-64, 2004-2 C.B. 7 held that the grantor’s payment of income taxes attributable to the grantor trust is not treated as a gift to the trust beneficiaries.

B. Tax Reimbursement Clauses.

1. A tax reimbursement clause gives the trustee the authority to reimburse the grantor for taxes paid (or to pay the tax liability directly) on trust income.

2. Discretionary reimbursements. Revenue Ruling 2004-64, 2004-2 C.B. 7 provides that a trustee’s discretionary power to reimburse the grantor for income taxes paid will not cause inclusion in the grantor’s estate provided:

a. The grantor may not act as trustee (the trustee should not be related or subordinate to the grantor);

b. The grantor may not have the power to remove and replace the trustee with related and subordinate parties;

FTL_ACTIVE 5339732.4 17

c. State law cannot subject the trust assets to the claims of the grantor’s creditors because of the power to reimburse; and

Fla.Stat. § 736.0505(1)(c) provides that “the assets of an irrevocable trust may not be subject to the claims of an existing or subsequent creditor or assignee of the settlor, in whole or in part, solely because of the existence of a discretionary power granted to the trustee by the terms of the trust, or any other provision of law, to pay directly to the taxing authorities or to reimburse the settlor for any tax on trust income or principal which is payable by the settlor under the law imposing such tax.”

d. There is no implied understanding to exercise the power to reimburse (the burden of proof is on the taxpayer to show there are no pre-existing arrangements or understanding with the trustee to pay the taxes).

PLANNING POINTER – It generally is advisable to include a discretionary tax reimbursement clause in a trust that is intended to be a grantor trust. Nonetheless, there should be no prearranged understanding that the grantor will be reimbursed. Moreover, the trustee probably should not make regular reimbursement distributions to the grantor.

3. The grantor’s payment of the income taxes attributable to the inclusion of the trust income in his or her taxable income does not constitute a gift to the trust beneficiaries since it is the grantor, not the trust, that is liable for the taxes. Rev. Rul. 2004-64, 2004-27 I.R.B. 7.

a. Neither mandatory nor discretionary reimbursement provisions (under the trust instrument or local law) alter the rule. Id.

4. Mandatory reimbursements: if the trust instrument or local law demands that the grantor be reimbursed for the payment of the income taxes attributable to the inclusion of the trust income in his or her taxable income then under I.R.C. § 2036(a)(1), the full value of the trust will be included in the grantor’s gross estate since the grantor has retained the right to have trust income expended in discharge of his or her legal obligations. Id.

The effective tax rate is not 100%, so why should the entire value of the trust be included?

FTL_ACTIVE 5339732.4 18

C. Tax Reporting Methods.

1. Every trust having for the taxable year any taxable income, or having gross income of $600 or over, regardless of amount of taxable income is required to file a return reporting the income. I.R.C. § 6012(a)(4).

2. Treas. Regs. § 1.671-4 sets forth three alternative methods that can be used for reporting purposes: the traditional method and two alternative methods.

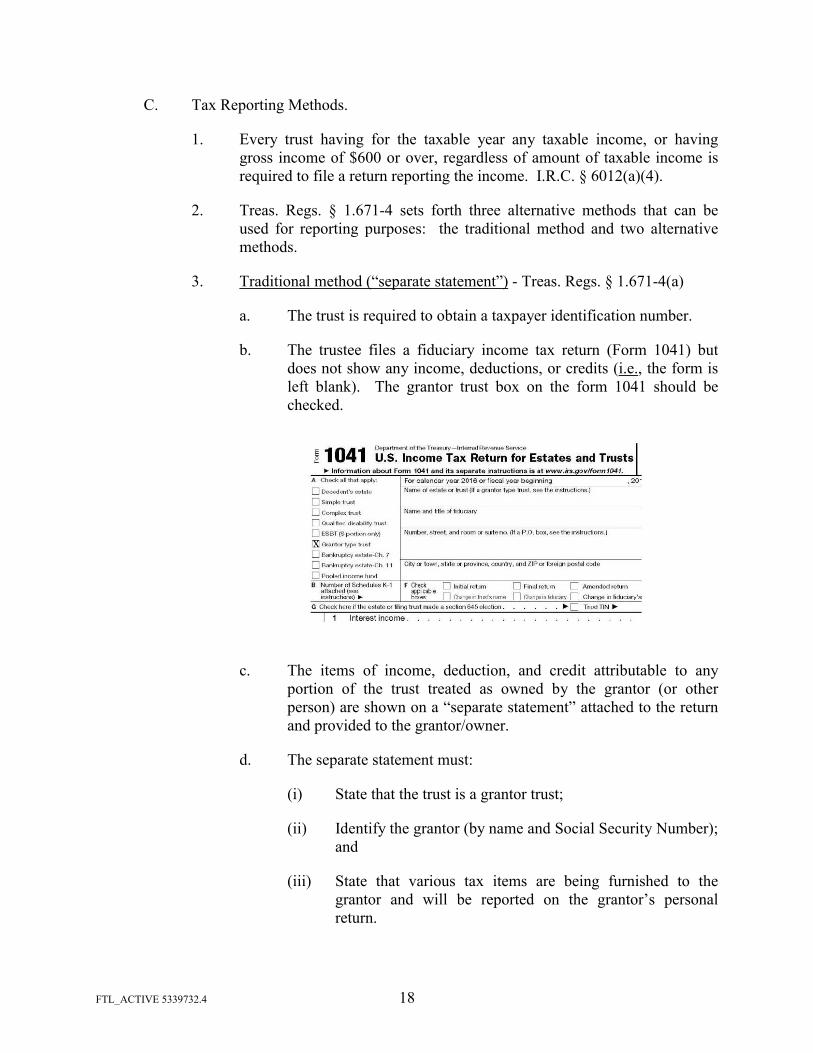

3. Traditional method (“separate statement”) - Treas. Regs. § 1.671-4(a)

a. The trust is required to obtain a taxpayer identification number.

b. The trustee files a fiduciary income tax return (Form 1041) but does not show any income, deductions, or credits (i.e., the form is left blank). The grantor trust box on the form 1041 should be checked.

c. The items of income, deduction, and credit attributable to any portion of the trust treated as owned by the grantor (or other person) are shown on a “separate statement” attached to the return and provided to the grantor/owner.

d. The separate statement must:

(i) State that the trust is a grantor trust;

(ii) Identify the grantor (by name and Social Security Number); and

(iii) State that various tax items are being furnished to the grantor and will be reported on the grantor’s personal return.

FTL_ACTIVE 5339732.4 19

e. Any grantor trust may use the traditional method.

f. Certain types of grantors trusts, such as Qualified Subchapter S trusts and trusts with situs outside the U.S., must use the traditional method.

4. First Alternative Method (“Single grantor method”).

a. The trustee is not required to file any type of return with the Internal Revenue Service. Treas. Regs. § 1.671-4(b)(2)(ii)(B). Nonetheless, the trustee must obtain a Form W-9 from the grantor (or other person) treated as the owner verifying the owner’s taxpayer identification number.

b. The trustee must furnish the name and taxpayer identification number (e.g., Social Security Number) of the grantor (or other person) treated as the owner, and the address of the trust to all “payors” during the tax year. Treas. Regs. § 1.671-4(b)(2)(i)(A).

c. The term “payor” means any person who is required by any provision of the Internal Revenue Code and the regulations thereunder to make any type of information return (including Form 1099 or Schedule K-1) with respect to the trust for the taxable year, including persons who make payments to the trust or who collect (or otherwise act as middlemen with respect to) payments on behalf of the trust. Treas. Regs. § 1.671-4(b)(4).

d. Unless the grantor (or other person) treated as the owner of the trust is the trustee or a co-trustee of the trust, the trustee must furnish the grantor (or other person) treated as the owner a statement that:

(i) Shows all items of income, deduction, and credit of the trust for the taxable year;

(ii) Identifies the payor of each item of income;

(iii) Provides the grantor or other person treated as the owner of the trust with the information necessary to take the items into account in computing the grantor’s or other person’s taxable income; and

(iv) Informs the grantor or other person treated as the owner of the trust that the items of income, deduction, and credit and other information shown on the statement must be included in computing the taxable income and credits of the grantor or other person on the income tax return of the grantor or other person. Treas. Regs. § 1.671-4(b)(2)(ii)(A).

FTL_ACTIVE 5339732.4 20

e. This method is allowed only when the trust is treated as owned by one grantor or one other person. This method is most frequently used in the revocable trust context.

5. Second Alternative Method (“single/multi grantor method”).

a. The trustee must furnish the name, taxpayer identification number, and address of the trust to all payors during the tax year. Treas. Regs. § 1.671-4(b)(2)(i)(B).

b. The trustee must file with the IRS the appropriate Forms 1099, reporting the income or gross proceeds paid to the trust during the taxable year, and showing the trust as the payor and the grantor or other person treated as the owner of the trust as the payee. Treas. Regs. § 1.671-4(b)(2)(iii)(A).

c. The trustee also needs to furnish a summary and transmittal of informational returns (Form 1096).

d. Unless the grantor (or other person) treated as the owner of the trust is the trustee or a co-trustee of the trust, the trustee must furnish the grantor with a statement that:

(i) Shows all items of income, deduction, and credit of the trust for the taxable year;

(ii) Provides the grantor or other person treated as the owner of the trust with the information necessary to take the items into account in computing the grantor’s or other person’s taxable income; and

(iii) Informs the grantor or other person treated as the owner of the trust that the items of income, deduction, and credit and other information shown on the statement must be included in computing the taxable income and credits of the grantor or other person on the income tax return of the grantor or other person. Treas. Regs. § 1.671-4(b)(2)(iii)(B).

e. The second alternative method can be used if there is a single owner/grantor or multiple owners/grantors.

D. Loss of Grantor Trust Status.

1. The trust will cease to be a grantor’s trust the moment the grantor’s powers are eliminated. The trust then will become a separate taxpayer for income tax purposes.

FTL_ACTIVE 5339732.4 21

2. During grantor’s lifetime.

a. Loss of status will be treated as a transfer by the grantor of the trust assets to the trust, in exchange for any consideration given by the trust to the grantor. Treas. Regs. § 1.1001-2(c) Ex. 5; Rev. Rul. 77-402 1977-2 C.B. 222; Madorin v. Commissioner, 84 T.C. 667 (1985).

b. Deemed a gratuitous transfer for income tax (not gift tax) purposes.

c. Trust takes a I.R.C. § 1015 basis in the assets obtained from the grantor.

d. No realization of gain or loss (exception if trust holds encumbered assets and the debt exceeds the basis of the assets).

3. At grantor’s death.

a. IRS rulings suggest that the death of the grantor is a non-recognition event for income tax purposes. See Madorin v. Commissioner, 84 T.C. 667 (1985); Rev. Rul. 85-13 1985-1 C.B. 184.

b. There is no basis step-up if the assets are not included in the grantor’s gross estate. CCA 200937028.

E. Toggling Grantor Trust Status

1. Most grantor trust powers can be drafted so that the grantor or other person holding the power can release it at any time, thereby terminating the grantor trust status.

PLANNING POINTER – For simplicity consider releasing the power as of midnight on December 31st.

PLANNING POINTER – Include a provision that gives an independent third party the power to re-grant a released power back to the grantor (or other person) to retrigger grantor trust status.

2. To avoid potential breach of fiduciary claims, the ability to release the power should be given to a third party who is acting in a nonfiduciary capacity (i.e., not to the trustee, a trust protector, or special trustee). The third party should be a non-adverse party to avoid the possible argument that the right to release the power is tantamount to the right to consent to its exercise.

FTL_ACTIVE 5339732.4 22

3. Reasons to toggle off.

a. The estate planning “pros” of shifting appreciation out of grantor’s estate generally no longer outweigh the “cons” of the grantor having to pay the trust income tax (in light of the increased applicable exclusion amount, the pros for avoiding estate taxes generally no longer outweigh the burden of paying the income tax).

b. The trust is going to sell highly appreciated long-term capital gain property and the grantor does not want to pay the capital gains taxes.

c. Changes in the law.

4. Retriggering grantor trust status.

a. The person who has the power to toggle grantor trust status off cannot be the same person with the power to toggle grantor trust status back on. Likewise, the power should not be given to the grantor.

(i) Example: Grantor G has the right to reacquire trust assets by substituting assets of equivalent value. G also has the power to release such right. G cannot also hold the right to reinstate the power. The power must be held by someone other than G; otherwise, G’s release of such power would likely be disregarded.

b. The IRS has suggested that a state law trust modification may be another means of retriggering grantor trust status. IRS Priv. Ltr. Rul. 2008-48-017 (Nov. 18, 2008).

c. Tax consequences – see above “Loss of Grantor Trust Status.”

VI. Special Needs Trust Classification.

A. Third-Party Special Needs Trusts.

1. Tax Status. Generally a third-party special needs trust is not a grantor trust. The trust is treated as a separate taxpayer and will have its own taxpayer identification number.

2. Income taxable to beneficiary. Only if distributions are made to or for the benefit of the beneficiary will trust income (referred to as distributable net income or “DNI”) be carried to the beneficiary. The trust will report the DNI on a Schedule K-1 that is provided to the beneficiary. The

FTL_ACTIVE 5339732.4 23

beneficiary in turn will be required to report the income shown on the Schedule K-1 on the beneficiary’s own tax return.

3. Income taxable to trust. The trust will be taxed on income that is not carried out to the beneficiary.

B. First-Party Special Needs Trust.

1. Tax Status. Generally a first-party special needs trust is a grantor trust for income tax purposes.

2. In Private Letter Ruling 20060025, the IRS held that a first-party (d)(4)(A) special needs trust was a grantor trust with respect to the beneficiary under I.R.C. § 677(a)(1) and (2), since the income of the trust was to be used or accumulated for the benefit of the grantor-beneficiary in the discretion of the trustee who was not an adverse party.

PLANNING POINTER - Although the trust could use the taxpayer’s Social Security Number, consideration should be given to having the trust obtain its own taxpayer identification number to separately associate the income earned by the trust assets with income that may be earned separately by the beneficiary. See Second Alternative Method above.

PLANNING POINTER – Including a tax reimbursement provision that allows the trust to pay the income tax is advisable.

3. Generally a first-party special needs trust is included in the beneficiary’s gross estate under I.R.C. § 2036. Priv. Ltr. Rul. 9437034

VII. Planning Opportunities.

A. Exclusion for Gain on Sale of Residence.

1. In planning for long-term care (“LTC”), assets may be transferred into an irrevocable trust in order to minimize the applicant’s countable resourcesand to qualify the applicant for Medicaid benefits. Generally, the Medicaid applicant retains at least some right to withdraw income from the trust, but no right to withdraw trust principal. A common asset that is transferred to the trust is the individual’s home. Although the trust is generally drafted in a manner that allows the settlor/applicant to live in the home for the rest of his or her lifetime, what happens if the home has to be sold?

2. As general rule, a taxpayer is allowed to exclude the first $250,000 ($500,000 in the case of married couples) of gain from the sale of his or

FTL_ACTIVE 5339732.4 24

her home from income tax. A trust that is recognized as a separate taxpaying entity is not eligible for this exclusion.

3. Thus, to avoid loss of the exemption for gain on the sale of a personal residence, the trust should be drafted to ensure that it is a grantor trust.

B. Taking Advantage of Lower Tax Rates.

1. As referenced above, it often is desirable for trust income to be reportable by the individual rather than the trust, due to the lower individual tax brackets.

2. To capture these lower rates, consider whether a third-party special needs trust could be drafted to qualify as a grantor trust. Generally, this is accomplished by drafting what is referred to as an “intentionally defective grantor trust.”

C. Deductibility of Trustee Fees and Attorney’s Fees.

1. The 2017 Tax Cuts and Jobs Act added I.R.C. § 67(g), which suspends all “miscellaneous itemized deductions” previously allowed to individual taxpayers by I.R.C. § 67(a) for the tax years 2018-2025. This suspension includes guardian, trustee, and attorneys fees.

2. IRS Notice 2018-61 clarified that the removal of miscellaneous itemized deductions does not affect the deductibility of payments described in I.R.C. § 67(e)(1), which deals with trust administration costs. Nonetheless, I.R.C. § 67(e) applies only to estates and nongrantor trusts. Therefore, absent further clarification from the IRS, it appears that grantor trusts would be subject to I.R.C. § 67(g), and trustee fees and attorneys would not be deductible for the tax years 2018-2025.

3. If a trust has the ability to toggle off grantor trust status, consider whether to trigger non-grantor trust status to take advantage of deductions.

D. Be Careful Not To Include Powers That Would Cause the Assets To Be Deemed Available For Eligibility Purposes.

1. A third-party special needs trust that contains a Crummey power could cause the asset to be considered “available” resources.

2. Moreover, the failure to exercise a Crummey power could convert a third-party special needs trust into a first-party special needs trust, thereby mandating inclusion of the payback provisions.

E. A first-party special needs trust.

FTL_ACTIVE 5339732.4 25

1. A (d)(4)(A) trust by its very nature will, in all likelihood, be a grantor trust under I.R.C. § 673 or § 677.

2. To ensure grantor trust status, consider adding the power to substitute under I.R.C. § 675(4)(C).