Embed Size (px)

Citation preview

IEA 2019. All rights reserved.

Oil 2019 – Analysis and Forecasts to 2024

Neil Atkinson, Olivier Lejeune

Oslo, 26 March 2019

IEA

2IEA 2019. All rights reserved.

Supply

3IEA 2019. All rights reserved.

US expansion is 70% of global growth. Gains in Brazil, Iraq, Norway, the UAE and Guyana.

Main declines in Iran and Venezuela.

US leads the way in global supply growth

Change in total oil supply 2018-24

US

Brazil

Iraq

Norway

UAE

Guyana

Iran

Venezuela

-2

-1

0

1

2

3

4

5

mb

/d

4IEA 2019. All rights reserved.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

mb

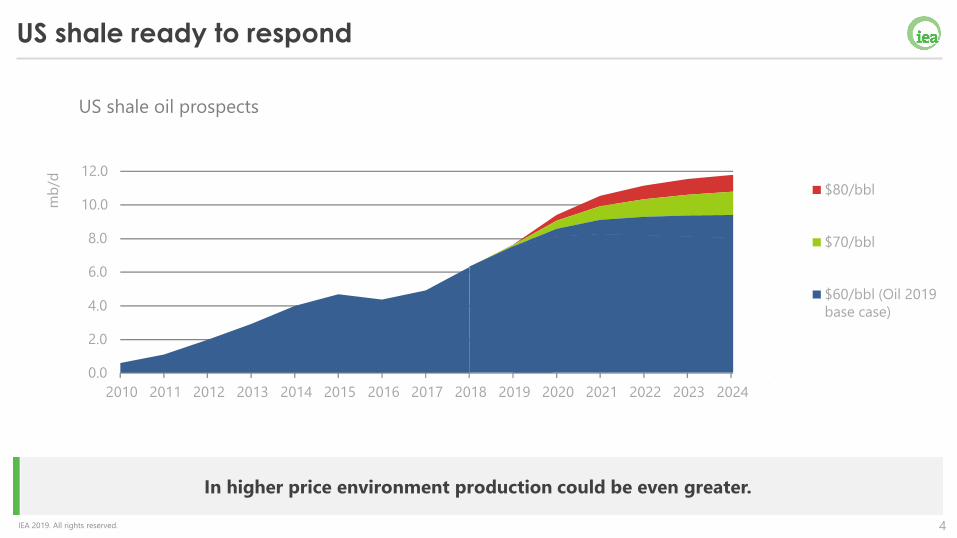

/dUS shale ready to respond

In higher price environment production could be even greater.

$80/bbl

$70/bbl

$60/bbl (Oil 2019

base case)

US shale oil prospects

5IEA 2019. All rights reserved.

US crude export capacity no longer a constraint

Enough pipelines planned to match Saudi exports, even if not all of them will be built.

* Based on pipelines currently under construction or in final development stage.

0,0

2,0

4,0

6,0

8,0

10,0

2018 2019 2020 2021 2022 2023 2024

mb/d WithAdditionalPipelinesProposed

US CrudeExportCapacity

2018 SaudiCrudeExports

2018RussianCrudeExports

6IEA 2019. All rights reserved.

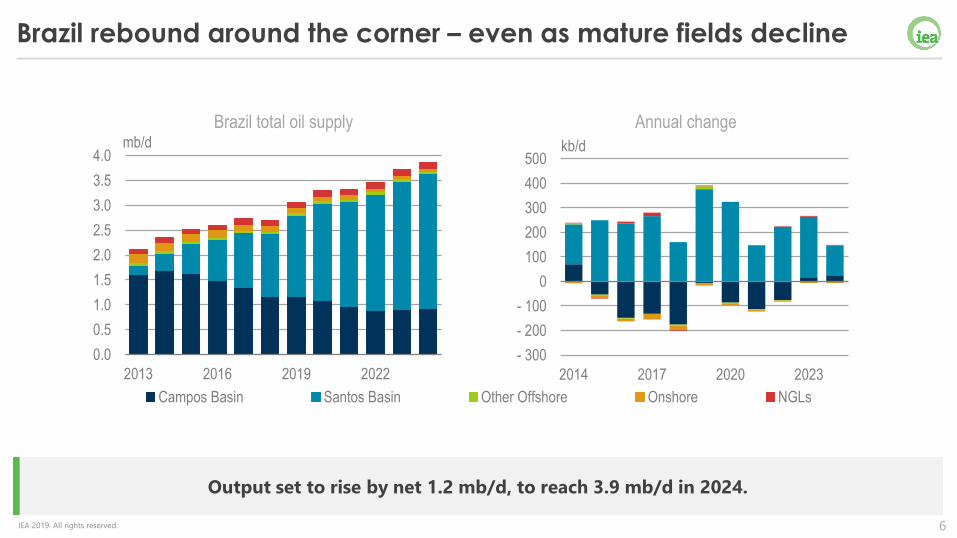

Brazil rebound around the corner – even as mature fields decline

Output set to rise by net 1.2 mb/d, to reach 3.9 mb/d in 2024.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2013 2016 2019 2022

mb/d

Campos Basin Santos Basin Other Offshore Onshore NGLs

- 300

- 200

- 100

0

100

200

300

400

500

2014 2017 2020 2023

kb/d

Brazil total oil supply Annual change

7IEA 2019. All rights reserved.

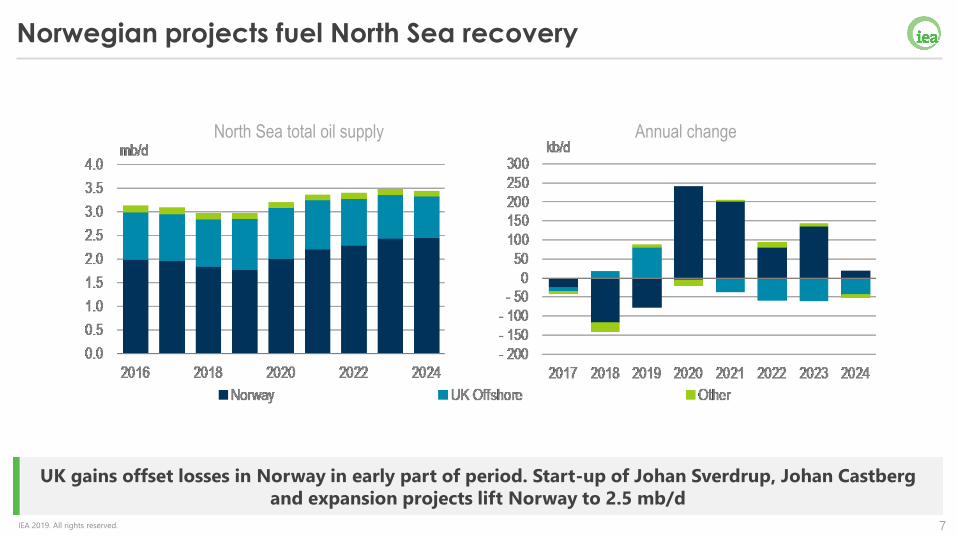

Norwegian projects fuel North Sea recovery

UK gains offset losses in Norway in early part of period. Start-up of Johan Sverdrup, Johan Castberg

and expansion projects lift Norway to 2.5 mb/d

North Sea total oil supply Annual change

8IEA 2019. All rights reserved.

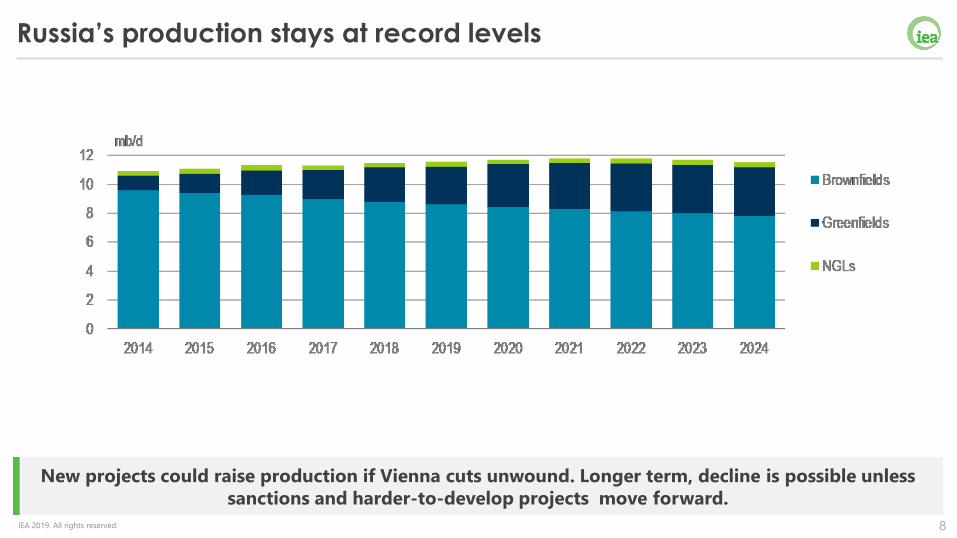

Russia’s production stays at record levels

New projects could raise production if Vienna cuts unwound. Longer term, decline is possible unless

sanctions and harder-to-develop projects move forward.

9IEA 2019. All rights reserved.

Canada’s growth eases back

Infrastructure bottlenecks led to mandatory production cuts in 2019. New projects stall.

Canada total oil supply Annual change

10IEA 2019. All rights reserved.

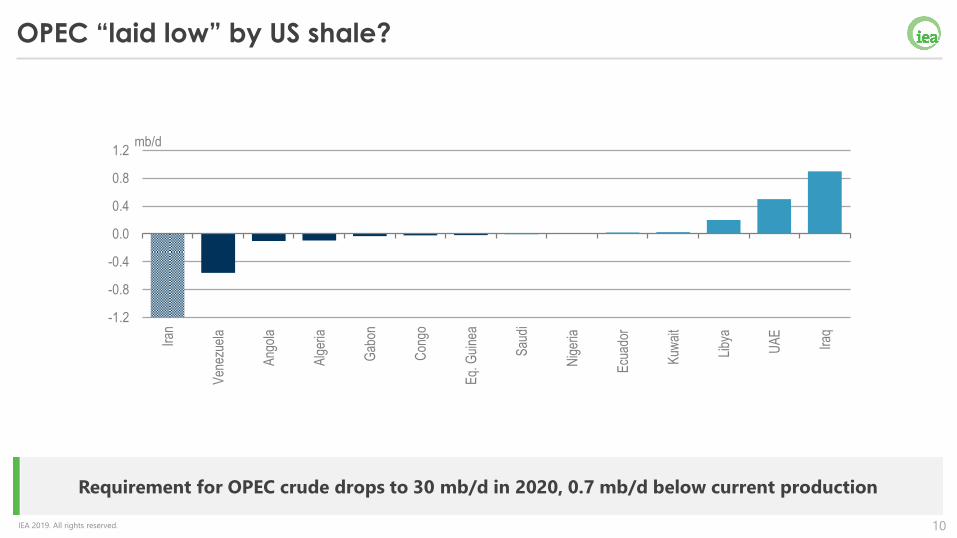

OPEC “laid low” by US shale?

Requirement for OPEC crude drops to 30 mb/d in 2020, 0.7 mb/d below current production

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

Iran

Ven

ezue

la

Ang

ola

Alg

eria

Gab

on

Con

go

Eq.

Gui

nea

Sau

di

Nig

eria

Ecu

ador

Kuw

ait

Liby

a

UA

E

Iraq

mb/d

11IEA 2019. All rights reserved.

Demand

12IEA 2019. All rights reserved.

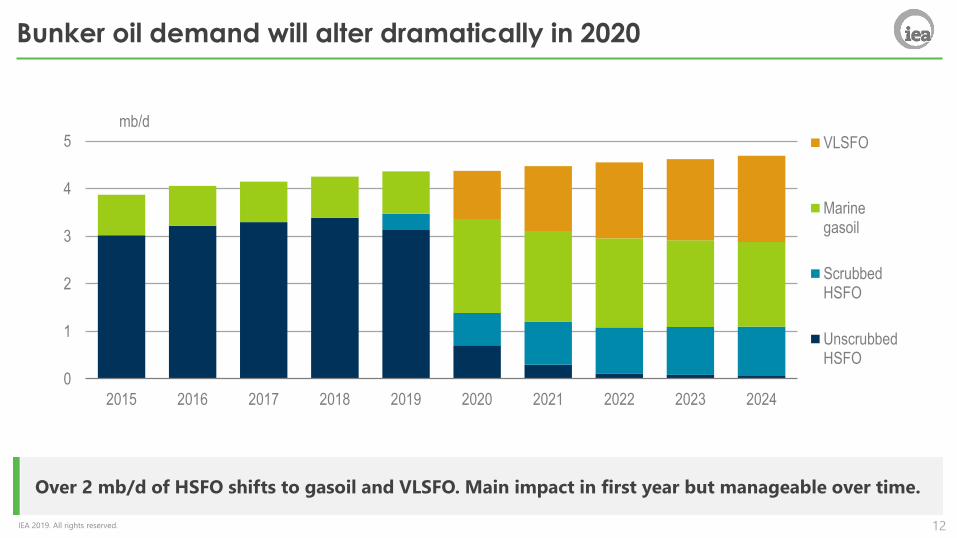

Bunker oil demand will alter dramatically in 2020

Over 2 mb/d of HSFO shifts to gasoil and VLSFO. Main impact in first year but manageable over time.

0

1

2

3

4

5

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

mb/d

VLSFO

Marinegasoil

ScrubbedHSFO

UnscrubbedHSFO

13IEA 2019. All rights reserved.

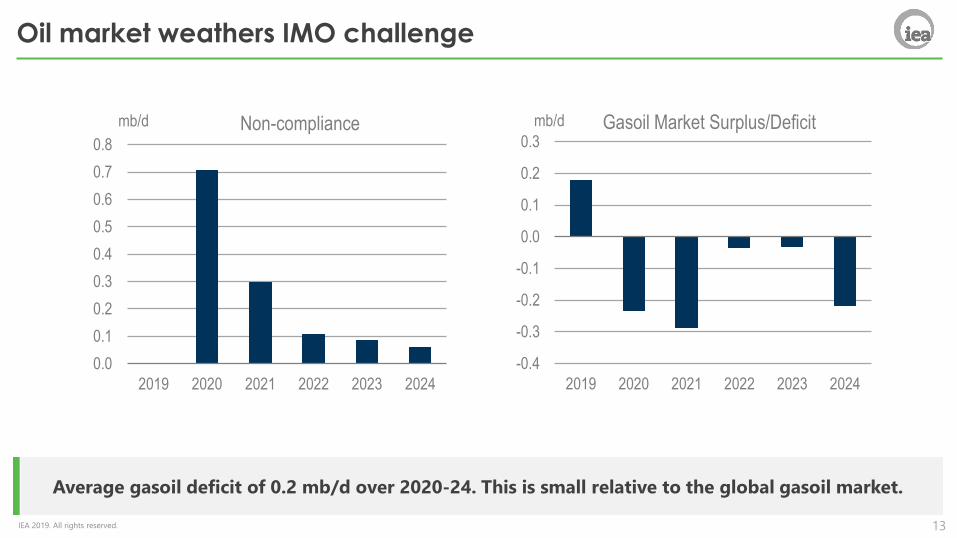

Oil market weathers IMO challenge

Average gasoil deficit of 0.2 mb/d over 2020-24. This is small relative to the global gasoil market.

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2019 2020 2021 2022 2023 2024

mb/d Non-compliance

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

2019 2020 2021 2022 2023 2024

mb/d Gasoil Market Surplus/Deficit

14IEA 2019. All rights reserved.

Scrubber installations rise rapidly in 2019-20

But investments slow markedly in 2021 as gasoil availability rises.

0

1 000

2 000

3 000

4 000

5 000

6 000

2019 2020 2021 2022 2023 2024

Vessels with scrubbers Forecast scrubber installations by vessel category Other

LPG

Cruise

Containerships

BulkCarriers

OilTankers

15IEA 2019. All rights reserved.

Bunker demand growth to slow

Bunker demand falls in 2020 following IMO rule implementation and slows to 1.9% p.a. after

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2000 2005 2010 2015 2020

mb/d Global bunker fuel demand

OECD Non-OECD Forecast

-10%

-5%

0%

5%

10%

15%

20%

2005 2008 2011 2014 2017 2020 2023

%/year Global bunker fuel demand growth

Historic Forecast

16IEA 2019. All rights reserved.

Marine gasoil takes rising share of global market

Inland gasoil/diesel demand growth slows. Marine sector accounts for 56% of growth in gasoil demand.

0

5

10

15

20

25

30

35

2000 2004 2008 2012 2016 2020 2024

mb/d Global gasoil/diesel demand

Inland gasoil Marine gasoil

-4%

-2%

0%

2%

4%

6%

2004 2008 2012 2016 2020 2024

%/year Inland gasoil/diesel demand growth

Historic Forecast

17IEA 2019. All rights reserved.

Some HSFO finds its way in the power sector

Middle East power sector demand grows, mainly in Saudi Arabia

0

50

100

150

200

250

300

350

400

450

500

2020 2021 2022 2023 2024

kb/d

Saudi Arabia Other Middle east Asia Other

Incremental fuel oil demand (changes vs. 2019)

18IEA 2019. All rights reserved.

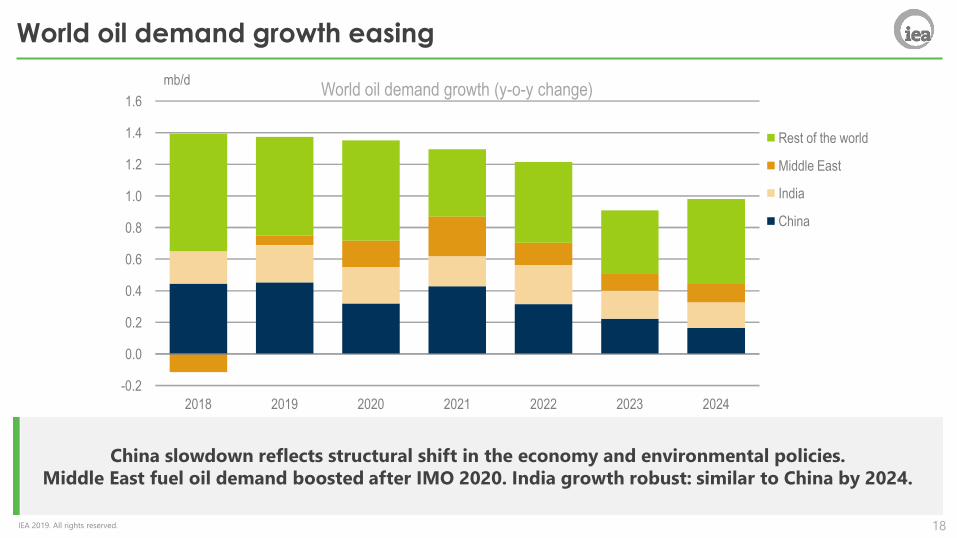

World oil demand growth easing

China slowdown reflects structural shift in the economy and environmental policies.

Middle East fuel oil demand boosted after IMO 2020. India growth robust: similar to China by 2024.

World oil demand growth (y-o-y change)

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2018 2019 2020 2021 2022 2023 2024

mb/d

Rest of the world

Middle East

India

China

19IEA 2019. All rights reserved.

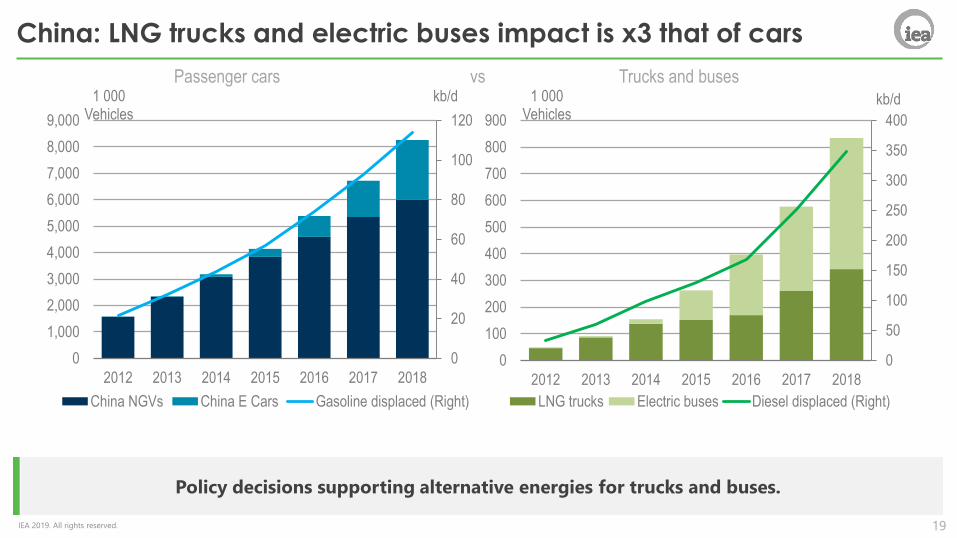

China: LNG trucks and electric buses impact is x3 that of cars

Policy decisions supporting alternative energies for trucks and buses.

0

20

40

60

80

100

120

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2012 2013 2014 2015 2016 2017 2018

kb/d1 000 Vehicles

China NGVs China E Cars Gasoline displaced (Right)

0

50

100

150

200

250

300

350

400

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016 2017 2018

kb/d1 000 Vehicles

LNG trucks Electric buses Diesel displaced (Right)

Passenger cars vs Trucks and buses

20IEA 2019. All rights reserved.

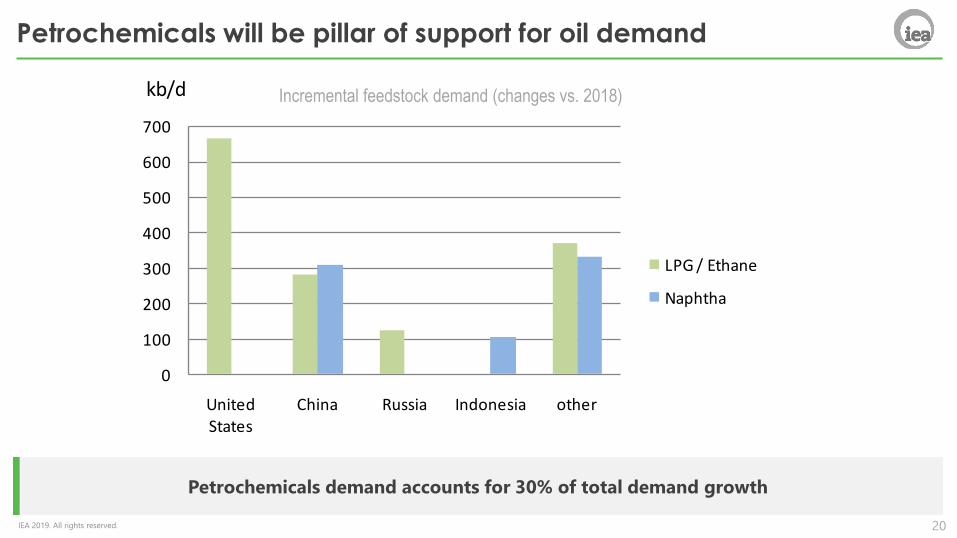

Petrochemicals will be pillar of support for oil demand

Petrochemicals demand accounts for 30% of total demand growth

0

100

200

300

400

500

600

700

United States

China Russia Indonesia other

kb/d

LPG / Ethane

Naphtha

Incremental feedstock demand (changes vs. 2018)

21IEA 2019. All rights reserved.

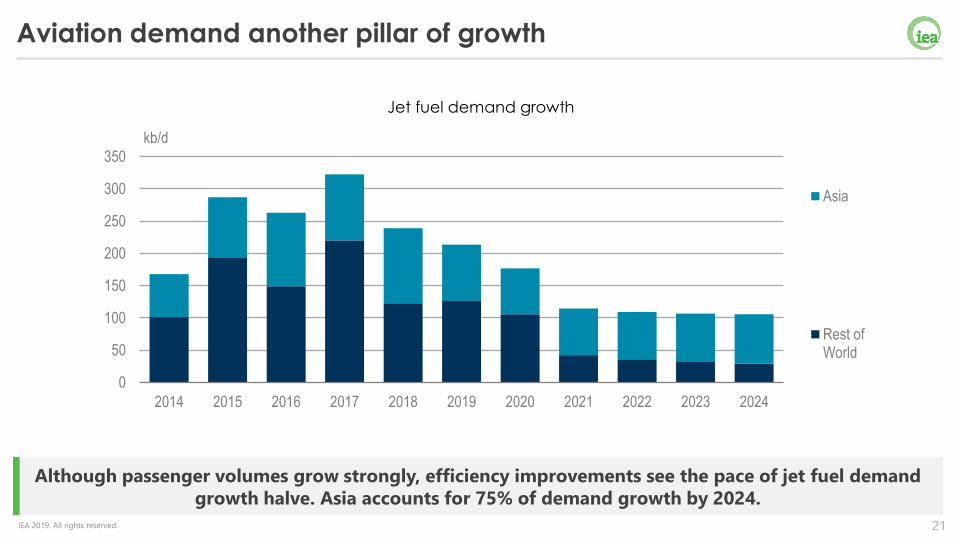

Although passenger volumes grow strongly, efficiency improvements see the pace of jet fuel demand

growth halve. Asia accounts for 75% of demand growth by 2024.

Jet fuel demand growth

0

50

100

150

200

250

300

350

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

kb/d

Asia

Rest ofWorld

Aviation demand another pillar of growth

22IEA 2019. All rights reserved.

Refining & Trade

23IEA 2019. All rights reserved.

Downstream capacity additions challenge refiners

Global capacity growth to 2024 far exceeds refined products demand growth.

China

Other Asia

Middle East

Other

0

2

4

6

8

10

Capacity additions Demand growth Implied excess

capacity

Capacity closures

in 2013-18

mb/d

Demand for

refined products

24IEA 2019. All rights reserved.

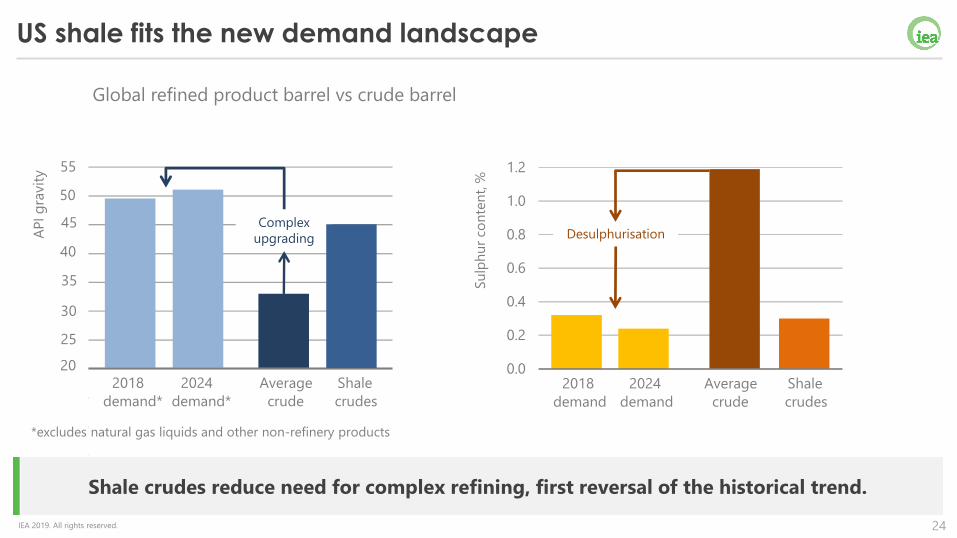

Shale crudes reduce need for complex refining, first reversal of the historical trend.

US shale fits the new demand landscape

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2018

demand

2024

demand

Average

crude

Shale

crudes

Su

lph

ur

con

ten

t, %

20

25

30

35

40

45

50

55

2024

demand*

Average

crude

Shale

crudes

AP

Ig

ravit

y

2018

demand*

Complex

upgrading Desulphurisation

*excludes natural gas liquids and other non-refinery products

Global refined product barrel vs crude barrel

25IEA 2019. All rights reserved.

US gross exports overtake Russia, close in on Saudi Arabia

US is net oil exporter in 2021 after 75 years of import dependency. US exports add to market flexibility.

-8

-6

-4

-2

0

2

4

6

8

10

2012 2014 2016 2018 2020 2022 2024

mb/d US net oil balance

Saudi gross exports

Russia gross exports

US gross exports

US net seaborne trade

26IEA 2019. All rights reserved.

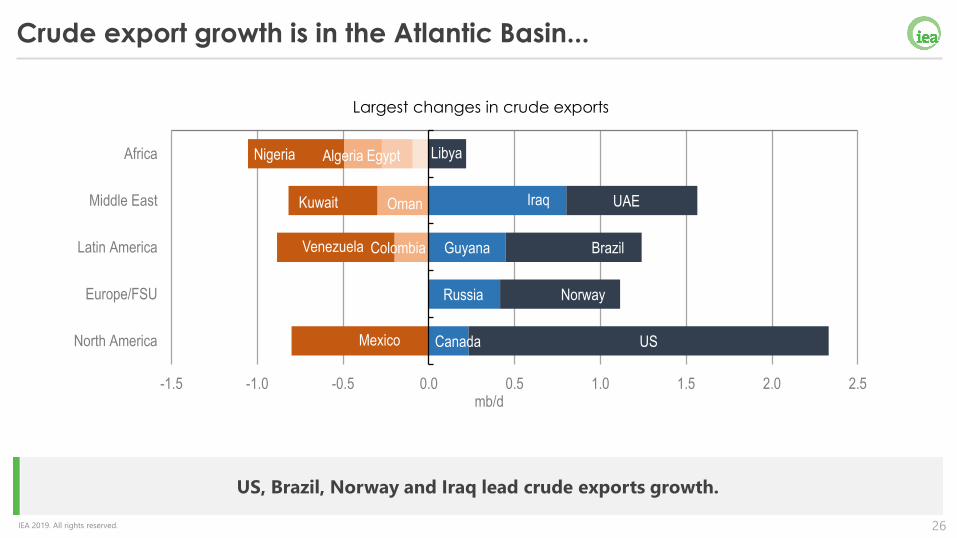

US, Brazil, Norway and Iraq lead crude exports growth.

Crude export growth is in the Atlantic Basin...

Algeria

Oman

Nigeria

Kuwait

Venezuela

Mexico

Egypt

UAE

Colombia

Russia

Canada

Guyana

Libya

Iraq

Brazil

Norway

US

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

Africa

Middle East

Latin America

Europe/FSU

North America

mb/d

Largest changes in crude exports

27IEA 2019. All rights reserved.

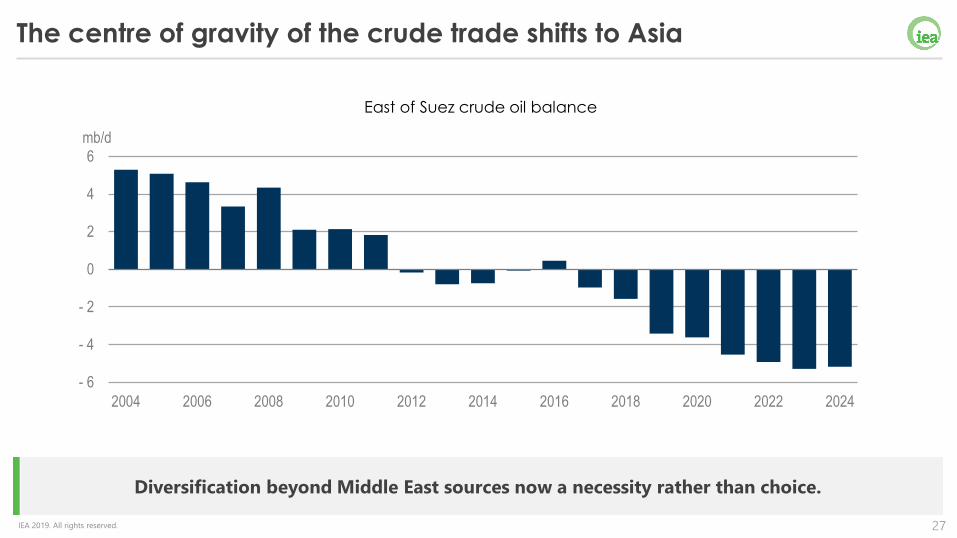

Diversification beyond Middle East sources now a necessity rather than choice.

The centre of gravity of the crude trade shifts to Asia

- 6

- 4

- 2

0

2

4

6

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

mb/d

East of Suez crude oil balance

28IEA 2019. All rights reserved.

Conclusions

• The United States to provide 70% of the increase in global oil supply over next five years, with Iraq, Brazil, Norway & Guyana other major contributors

• Global oil demand growth to slow modestly, but still average 1.2 mb/d, with petrochemicals a key driver

• While there may be teething problems, refiners & shippers are relatively well

prepared to implement the new IMO bunker fuel regulations

• The 2nd wave of the US shale revolution is coming – it will shake-up international oil & gas trade flows, with profound implications for the geopolitics of energy

• Up to and beyond 2024: oil industry must do more to cut its carbon footprint, e.g. flaring & methane leakages, and use of CCUS, EOR, hydrogen & renewables.

29IEA 2019. All rights reserved.

www.iea.orgIEA