Embed Size (px)

Citation preview

OHLONE COMMUNITY COLLEGE DISTRICT

COUNTY OF ALAMEDA

FREMONT, CALIFORNIA

FINANCIAL STATEMENTS

WITH SUPPLEMENTAL INFORMATION

FOR THE YEAR ENDED JUNE 30, 2010

AND

INDEPENDENT AUDITOR'S REPORT

OHLONE COMMUNITY COLLEGE DISTRICT

FINANCIAL STATEMENTSWITH SUPPLEMENTAL INFORMATION

For the Year Ended June 30, 2010

TABLE OF CONTENTS

Page

Introduction:

Organization 1

Objectives of the Audit 2

Independent Auditor's Report 3-4

Management's Discussion and Analysis 5-16

Basic Financial Statements:

Statement of Net Assets 17

Discretely Presented Component Unit - Ohlone CollegeFoundation - Statement of Net Assets 18

Statement of Revenues, Expenses and Change in Net Assets 19

Discretely Presented Component Unit - Ohlone CollegeFoundation - Statement of Revenues, Expenses andChange in Net Assets 20

Statement of Cash Flows 21

Discretely Presented Component Unit - Ohlone CollegeFoundation - Statement of Cash Flows 22

Statement of Fiduciary Net Assets 23

Notes to Financial Statements 24-49

Required Supplementary Information:

Schedule of Other Postemployment Benefits (OPEB) Funding Progress 50

Supplemental Information:

Independent Auditor's Report on Supplemental Information 51-52

Combining Statement of Net Assets by Fund 53-54

Combining Statement of Revenues, Expenses and Change inNet Assets by Fund 55-56

OHLONE COMMUNITY COLLEGE DISTRICT

FINANCIAL STATEMENTSWITH SUPPLEMENTAL INFORMATION

For the Year Ended June 30, 2010

TABLE OF CONTENTS(Continued)

Page

Supplemental Information: (Continued)

Schedule of Expenditures of Federal Awards 57-58

Schedule of State Financial Awards 59

Schedule of Workload Measures for State General Apportionment 60

Reconciliation of Annual Financial and Budget Report (CCFS-311)with Audited Financial Statements 61

Notes to Supplemental Information 62

Independent Auditor's Report on State Compliance Requirements 63-64

Independent Auditor's Report on Internal Control over FinancialReporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 65-66

Independent Auditor's Report on Compliance with RequirementsApplicable to Each Major Program and Internal Control overCompliance in Accordance with OMB Circular A-133 67-68

Findings and Recommendations:

Schedule of Audit Findings and Questioned Costs 69

Summary of Findings and Recommendations 70-71

Summary Schedule of Prior Audit Findings 72

OHLONE COMMUNITY COLLEGE DISTRICT

ORGANIZATION

June 30, 2010

Ohlone Community College District (the "District") was established on July 1, 1966, andis comprised of an area approximating 534 acres in Fremont and 80 acres in Newark. Therewas no change in the boundaries of the District during the current year.

The Board of Trustees and District Administration for the fiscal year endedJune 30, 2010, were comprised of the following members:

BOARD OF TRUSTEES

Members Office Term Expires

Rich Watters Chair December 2010

Nick Nardolillo Vice Chair December 2012

John Weed Member December 2010

Garrett Yee Member December 2010

Bill McMillin Member December 2010

Greg Bonaccorsi Member December 2012

Teresa Cox Member December 2012

Kevin Feliciano Student May 2011

DISTRICT ADMINISTRATION

Gari Browning, Ph.D.President/Superintendent

James Wright, Ph.D.Vice President of Academic Affairs/

Deputy Superintendent

Michael CalegariVice President Administrative Services

Ron Travenick, Ed D.Vice President Student Development

OHLONE COMMUNITY COLLEGE DISTRICT

OBJECTIVES OF THE AUDIT

Year Ended June 30, 2010

The single audit of Ohlone Community College District (the "District") had the followingobjectives:

• To determine the fairness of presentation of the District's basis financialstatements in accordance with accounting principles generally accepted in theUnited States of America.

• To evaluate the adequacy of the systems and provisions affecting compliancewith applicable federal and California laws and regulations with which,noncompliance would have a material effect on the District's financial statementsand the allowability of program expenditures for federal and California financialassistance programs.

• To evaluate the adequacy of the internal control structure sufficient to meet therequirements of auditing standards generally accepted in the United States ofAmerica, for the purpose of formulating an opinion on the basic financialstatements taken as a whole and sufficient to ensure compliance with federaland state regulations.

• To determine whether financial and financially related reports to state andfederal agencies are fairly present.

• To recommend appropriate actions to correct any noted areas where internalcontrol compliance with applicable federal and California laws and regulationscould be improved.

5

OHLONE COMMUNITY COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010 In accordance with the Governmental Accounting Standard’s Board (GASB) Codification Section (Cod. Sec.) 2200.101, “Basic Financial Statements and Management’s Discussion and Analysis for State and Local Governments,” Ohlone Community College District (OCCD) prepares the financial statements in accordance with this standard. OCCD adopted the BTA reporting model as recommended by the California Community College Chancellors Office. In compliance with GASB Cod. Sec. 2100.138, the Ohlone College Foundation, which qualifies as a component unit is discretely presented.

Overview of the Financial Statements As required by accounting principles, the annual report consists of three basic financial statements that provide information on OCCD as a whole: the Statement of Net Assets; the Statement of Revenues, Expenses and Change in Net Assets; and the Statement of Cash Flows. The information provided on the statements that follow includes all funds, with the exception of the Student Association and Agency funds, shown on page 23 and the Foundation, shown on pages 18, 20 and 22. Each statement will be discussed separately. Under the BTA model of financial reporting, a single entity-wide statement is required to report financial activity for all funds of the District. Since the District is made up of many different funds with a variety of purposes, the following information is provided to help with the understanding of the financial statements. The supplemental section of the audited financial statements provides a reconciliation of the typical fund-type format with the BTA-type presentation.

Budget Highlights For the two years prior to 2009-10 the District had growth rates that exceed what was actually funded by almost double. Both 07-08 and 08-09 were funded at 1.2% even though the District could have grown by much more. While growth was modestly funded, overall apportionment had a deficit applied mid-year of 1.68% and 1.48% respectively. 2009-10 received a workload reduction of 3.39% at a time when State Colleges and Universities were restricting access and high unemployment persisted. Other funding sources such as international tuition provided some relief from the reduced state funding. In order to mitigate the imposed deficit, the District continues a selective hiring freeze, offered a Supplemental Employee Retirement Program and the employee groups all took 5 days of furlough. To add to the situation, the state instituted additional revenue deferrals for the months of February, March and April that added to the already established June amount which moved cash payments into the next fiscal year creating a cash flow challenge.

6

Financial Highlights The District Measure A General Obligation Bond that was passed in 2002 for

$150 million is coming to a close. Since the bond was passed, multiple projects have been completed on the Fremont Campus and the Newark Center was completed on time, ready for classes in January of 2008. The Student Support Center (SSC) was substantially complete June 15. With the completion of the SSC on the Fremont Campus, only a few safety projects remain. The enrollment continues to be strong. With the workload reduction of 3.39%, careful enrollment management strategies have been utilized to ensure that students can continue to register for the classes they need without excessive unfunded FTES. The stabilization reserve along with other cost cutting strategies noted above allowed the District to mitigate the effects of the current economic and housing down turn. There has been a strong effort on the part of the District to collect past due balances and provide some flexibility to students in handling the increasing cost of education. These measures have decreased the student receivable at a time when the state has increased revenue deferrals helping to mitigate the negative effect on cash flow.

Attendance Highlights • Although the District was eligible for a 3.68% growth rate in 2002-03, the State

could support only 40% of that rate for a funded growth rate of 1.48% in 2003-04. In order to manage its enrollment to maximize growth funding, the District schedules its summer programs so that summer enrollment could count toward either fiscal year. Therefore, enrollment that was not fully funded by the State, in the 2002-03 fiscal year was reported in the 2003-04 fiscal year.

• The growth target for 2003-04 was 2.8%, but with the system wide base

adjustment the District experienced only a .89 increase in FTES. The District has a large percentage of part time students and is working to increase the number of full time students.

• There was a 4.4% growth rate available for 2004-05 but the District experienced

an actual decline of 330 FTES. In order to ensure that the District could restore base funding the decision was made to report 880 Summer FTES in the 2005-06 fiscal year. The decline was due to a 45% increase in tuition, general economic trends and an overall decline in high school graduation rates.

• With the assistance of the 880 FTES from summer 2004-05 and 880 from 2005-

06 the District was able to restore FTES to the base level and even reported a modest amount of growth. The growth was taken from summer ’06 leaving only 20 for 2006-07.

7

• The growth trend from 2005-06 continued into 2006-07. The growth available was 4.24% but the District was only able capture 1.87% of what was available. And again the District chose to use the majority of summer to achieve that growth.

• The funded growth rate of 1.21% was achieved for 2007-08. • The rate for 2008-09 of 1.20% was achieved. The 2009-10 fiscal has a 3.39%

workload reduction as a part of the Final State Budget. • In 2009-10 the system experienced a workload reduction of 3.39%, even though

with the recession and high unemployment numbers the college could have grown.

Full Time Equivalent Students (FTES) Trends

0100020003000400050006000700080009000

'02-03

'03-04

'04-05

'05-06

'06-07

'07-08

'08-09

09-10

FTES

Actual

Reported

8

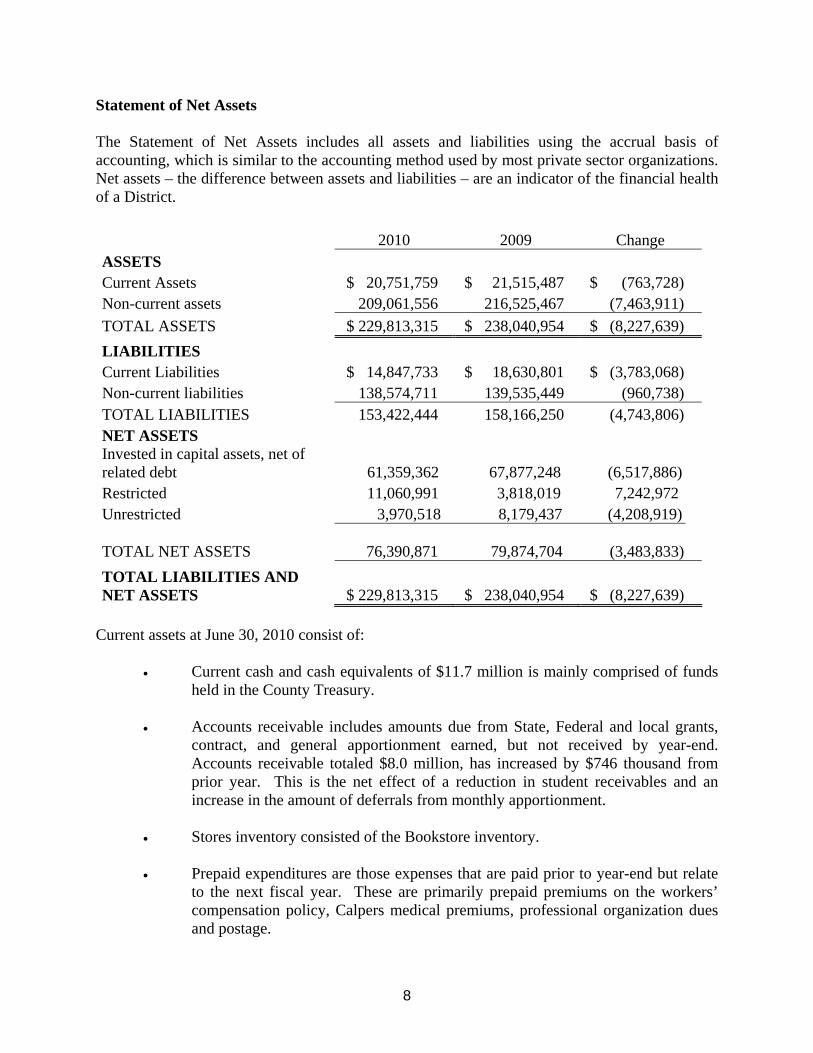

Statement of Net Assets The Statement of Net Assets includes all assets and liabilities using the accrual basis of accounting, which is similar to the accounting method used by most private sector organizations. Net assets – the difference between assets and liabilities – are an indicator of the financial health of a District. 2010 2009 Change ASSETS Current Assets $ 20,751,759 $ 21,515,487 $ (763,728) Non-current assets 209,061,556 216,525,467 (7,463,911) TOTAL ASSETS $ 229,813,315 $ 238,040,954 $ (8,227,639) LIABILITIES Current Liabilities $ 14,847,733 $ 18,630,801 $ (3,783,068) Non-current liabilities 138,574,711 139,535,449 (960,738) TOTAL LIABILITIES 153,422,444 158,166,250 (4,743,806) NET ASSETS Invested in capital assets, net of related debt 61,359,362 67,877,248 (6,517,886)Restricted 11,060,991 3,818,019 7,242,972 Unrestricted 3,970,518 8,179,437 (4,208,919)

TOTAL NET ASSETS 76,390,871

79,874,704 (3,483,833) TOTAL LIABILITIES AND NET ASSETS $ 229,813,315 $ 238,040,954 $ (8,227,639)

Current assets at June 30, 2010 consist of:

• Current cash and cash equivalents of $11.7 million is mainly comprised of funds held in the County Treasury.

• Accounts receivable includes amounts due from State, Federal and local grants,

contract, and general apportionment earned, but not received by year-end. Accounts receivable totaled $8.0 million, has increased by $746 thousand from prior year. This is the net effect of a reduction in student receivables and an increase in the amount of deferrals from monthly apportionment.

• Stores inventory consisted of the Bookstore inventory.

• Prepaid expenditures are those expenses that are paid prior to year-end but relate

to the next fiscal year. These are primarily prepaid premiums on the workers’ compensation policy, Calpers medical premiums, professional organization dues and postage.

9

Non-current Assets

• Restricted cash and cash equivalents consist of amounts relating to Capital Projects and cash in the Bond Redemption Fund. The Bond Redemption Fund is where taxes are set aside to repay the bond holders of the Districts General Obligation Bonds.

• Net Capital Assets are reported at the historical cost of land, buildings and equipment less accumulated depreciation, where applicable. There was a $2.6 million net decrease which is attributable to depreciation and the reduction in restricted cash as the Measure A Bond comes to completion.

Current liabilities consist of:

• Accounts payable are mainly amounts due to vendors ($1.5 million), which is a $1.4 million decrease over last year due primarily the slow down of construction projects as Measure A comes to a close.

• Deferred revenue relates to federal, state and local program funds received but not yet earned as of the end of the fiscal year. Most grants are earned when expended. Also included are the deferrals on enrollment fees for the summer and fall 2010 terms. This was down by $722 thousand primarily due to the reduction in summer courses.

• Accrued payroll and benefits represents the amount held for the payment to employees that work 10 months but elect to have their salary spread over a 12 month period.

• Interest Payable at $4.9 million comparable to last year and represents payments due to bond holders.

• Other Accrued Liabilities represents obligations of the District that are estimates and had not yet been invoiced. It is at $3.2 million, comparable to the prior year.

• The Long-term Liabilities due within one year is the amount due to the bond holders of the District's Measure A Bond. These payments are made from the voter approved tax assessments from Fremont and Newark property taxes. The original amount issued was $40 million. A second issuance of $110 million was completed 05-06. The amount due next fiscal year is $1.6 million which is the same as in the prior year

10

Non-current liabilities are:

• Non-current liabilities represent debt potentially owed in future years. The major component is the long-term portion (due in more than one year) of the Measure A Bond. The remaining balances are $26.0 million on the $40 million issuance and $105.9 million on the $110 million issuance will be paid over 22 and 26 years respectively. Subsequent to year end the $26 million was refinanced to reduce the interest payable by the tax payers.

Net Assets: Analysis of the District’s Financial Position Net assets, the difference between the District’s assets and liabilities, are an indicator of the District’s financial position. Net assets are reported in three components: unrestricted; restricted comprised of expendable and nonexpendable; and invested in capital assets, net of related debt. Invested in capital, net of related debt is $61.3 million. Restricted expendable include amounts legally restricted for payment of scholarships, other capital projects and debt service ($11.1 million) primarily related to debt service. Unrestricted Net Assets ($4.0 million) represent resources with no external restrictions. This category includes $2.8 million from the Bookstore. These funds may also carry designations from the Board of Trustees for contingencies, stabilization and other special purposes. Unrestricted Net Assets represent 5.3% of Total Net Assets.

Net Assets

Invested in capital, 80.2%

Expendible14.5%

Unrestricted 5.3%

11

The Statement of Revenues, Expenses and Change in Net Assets The Statement of Revenues, Expenses and Change in Net Assets presents the operating activity of the District, as well as the non-operating revenues and expenses. State general apportionment funds, while budgeted as operations, are considered non-operating revenues according to generally accepted accounting principles. 2010 2009 Change Total Operating Revenue $ 21,791,333 $ 21,210,172 $ 581,161 Total Operating Expenses 66,651,109 66,514,015 137,094 Operating income (loss) (44,859,776) (45,303,843) 444,067 Net non-operating revenue (expenses) 33,429,616 36,565,034 (3,135,418) Gain(loss) before capital revenue (11,430,160) (8,738,809) (2,691,351) Capital revenues 7,946,327 7,874,856 71,471 Increase(decrease) in net assets (3,483,833) (863,953) (2,619,880) Net Assets - Beginning of the year 79,874,704 84,482,320 (4,607,616) P/Y adjustment to the beginning Balance (3,743,663) (3,743,663) Net-Assets - End of the year $ 76,390,871 $ 79,874,704 $ (3,483,833)

Changes in operating revenue:

• Net tuition and fees is made up of enrollment fees and scholarship, discounts and allowances - the Board of Governor’s fee waivers. Enrollment fees are set by the state legislature for all community colleges. These fees are up by 9.1% due to the net of growth in our international programs and a reduction in the work load measures. The full impact of the reduction will be recognized in 2010-11. While Fall and Spring courses were reduced the biggest impact was to summer 2010 and that revenue will be reported in the 2010-11 fiscal year as required by the Budget and Account Manual.

• Overall grants increased from $11.9 million in 2008-09 to $12.6 million in 2009-

10 as a result of Work Force Investment grants focused on assisting the displaced automotive workers that lost their jobs when the NUMII plant was closed.

• The Bookstore saw a $712K reduction in activity as a result of the reduced FTES

and a change in inventory valuation.

12

Changes in non-operating revenues:

• State apportionments were $26.7 million in 2008-09 down to $25.2 in 2009-10. State apportionment represents total general apportionment earned less regular enrollment fees and less property taxes. State apportionment was down by $1.4 million. The reduction was the result of a 3.39% workload reduction that resulted in fewer full time equivalent students (FTES) being funded by the state.

• Local property taxes decreased in 2009-10 by $394 thousand. This is the result of the second wave of re-assessments. Changes in property tax revenue results in a corresponding increase/decrease in the District’s state apportionment revenue.

• State apportionment related to capital is down by $350 thousand as a result of the removal of scheduled maintenance from the state budget for the second year in a row.

• Other Revenue is relatively flat primarily due to an increase in our Community Education offerings and facility rentals while lottery and interest earnings both decreased.

Total Revenues for the Year Ended 2010 2009 Change Net tuition and fees $ 7,053,293 $ 6,463,802 $ 589,491 State apportionment non-capital 25,273,414 26,675,198 (1,401,784) Local property taxes 12,903,548 13,297,791 (394,243) Grants 12,671,467 11,967,983 703,484 Auxiliary enterprise (Bookstore) 2,066,573 2,778,387 (711,814) State apportionment capital 207,138 558,126 (350,988) Property taxes capital 7,739,189 7,316,730 422,459 Other 3,228,962 3,213,999 14,963 $ 71,143,584 $ 72,272,016 $ (1,128,432)

13

REVENUE

Changes in Operating Expenses

• In 2009-10 there was a reduction of $2.6 million resulting from the effects of a hiring freeze, a Supplemental Employee Retirement Program (SERP), a severance incentive and mandatory furloughs taken by all units.

• Benefits increased due primarily to increases in the cost of Health Care.

• The reduction is supplies is the direct result of cost savings plans and an early purchasing cut off that were implemented to assist with the closing the funding gap.

• Depreciation is increasing as the Bond Projects are completed and brought on as Fixed Assets.

• Financial aid to students was up by 32.3% in 2008-09 and up again in 2009-10 by another 48.8%. This increase is due to the influx of Federal Funds to specifically the PELL program.

Net Tuition

10%

Grants18%

Apportionment35%

Other5%

State Apportionment Capital

11%

Taxes18%

Bookstore3%

Capital11%

14

Operating Expenditures for the Year Ended 2010 2009 Change Academic and classified salaries $ 36,567,624 $ 39,155,223 $ (2,587,599) Employee benefits 7,997,209 7,492,918 504,291 Supplies and other operating expenses 10,336,945 11,071,425 (734,480) Depreciation 5,965,295 4,906,262 1,059,033 Student financial aid 5,784,036 3,888,187 1,895,849 $ 66,651,109 $ 66,514,015 $ 137,094

EXPENSES

Salaries54%

Benefits12%

Depreciation9%

Operating Expneses16%

Financial Aid9%

The Statement of Cash Flows The Statement of Cash Flows provides information about cash receipts and cash payments during the fiscal year. This statement also helps users assess the district’s ability to generate net cash flow, its ability to meet its obligations as they come due, and its need for external financing. 2010 2009 Change Net Cash provided (used) by: Operating activities $ (45,197,792) $ (44,197,098) $ (1,000,694) Non-capital financing activities 39,007,205 39,973,937 (966,732) Capital and related financing activities (511,937) (16,221,800) 15,709,863 Investment activities 172,643 24,748,804 (24,576,161) Net increase (decrease) in cash (6,529,881) 4,303,843 (10,833,724) Cash - beginning of the year 30,048,735 25,744,892 4,303,843 Cash - end of the year $ 23,518,854 $ 30,048,735 $ (6,529,881)

15

• The primary cash receipts from operating activities consist of student fees, grants and contracts. The primary cash outlays include payment of wages, benefits, supplies, contracts and Financial Aid to students. Net Cash used increased 2.26% as a result of the net effect of all of these activities with a decrease in state funding for categoricals and an increase in Aid to students showing the largest swings.

• General apportionment is the primary source of non-capital financing. The two main components of general apportionment are state apportionment and property taxes. The 2.24% decrease reflects the effects of the added deferrals.

• The main capital financing activities are for the purchases and upgrades of capital assets (land, building, and equipment). The District has fully issued all $150 million in bond funds approved by the voters. In 2008-09 the Student Support Building was the last of the major projects to come on line. The net change in 2009-10 reflects the smaller number of projects being completed as the Measure A Bond projects come to a close.

• Cash from investing activities is related to the sale of investments. The District cashed in a guaranteed investment contract in August 2008. In 2009-10 these funds continue to be drawn down to pay for construction costs but are accounted for in the cash section. The only investing activity come from interest earned on what remains of the bond proceeds.

Economic Outlook The State is still facing a structural deficit due in part to continued borrowing, a downward trend in property tax revenue and reduced income tax receipts as a result of an ongoing economic slow-down. At this writing a state budget is imminent but there are significant gaps in the information related to the implementation of the pending Budget Act. Enrollment Challenges and Opportunities The information at this point indicates that the State Budget will include some growth that would lessen the workload reduction of 3.39% that occurred in 2009-10. The specifics of the growth are not known at this point so none is included in the District’s final budget. The VP of Academic Affairs and the Academic Deans worked to reduce the course offerings in the previous year while maintaining the core mission. This strategy positioned the college well to remain stable if necessary or to take advantage of growth possibilities in the spring and subsequent summer 2011.

16

Overall Financial Picture The budget saving activities of 2009-10 provided a solid ground to move forward in 2010-11. There were significant savings from the continuing hiring freeze, Supplemental Employee Retiree Program (SERP), severance incentives and an early purchasing cut off. As part of the 2010-11 budget process:

• Categoricals were asked to cut back to the 2009-10 funding level, reducing the General Fund amount needed to assist the programs

• Employee groups agreed to an additional 6 furlough days • Budget managers reviewed their budgets for additional savings • Software was explored to assist with some of the workload pressure

As of this writing the state budget is not final, therefore revenue is projected to be at about the same level as 2009-10. Even with all of the savings from the prior year activities, and the concessions that are already in place, fixed costs increased leaving the District to cover an anticipated $618,054 deficit. Once there is a final budget the extent of the deficit will be analyzed. Until then, the rainy day reserve will be utilized to cover this shortfall. Even though the financial outlook for this funding year is less than optimistic, Ohlone has positioned itself well for the inevitability of down cycles. With frugal cash management, the Board approved rainy day reserve, and the support of all District employees, the college will be able to continue to provide excellent educational opportunities even in this down cycle.

OHLONE COMMUNITY COLLEGE DISTRICT

STATEMENT OF NET ASSETS

June 30, 2010

ASSETS

Current assets:Cash and cash equivalents $ 11,703,095Accounts receivable, net 8,010,792Stores inventories 505,725Prepaid expenditures 532,147

Total current assets 20,751,759

Noncurrent assets:Restricted cash and cash equivalents 11,815,759Capital assets, net 197,245,797

Total noncurrent assets 209,061,556

Total assets $ 229,813,315

LIABILITIES

Current liabilities:Accounts payable $ 1,483,283Deferred revenue 2,977,977Accrued payroll and benefits 1,731,294Interest payable 4,900,572Other accrued liabilities 572,188Long-term liabilities due within one year 2,294,432Deferred bond premium, current portion 186,021

Total current liabilities 14,145,767

Noncurrent liabilities:Long-term liabilities, net of current portion 135,711,263Deferred bond premium, long-term portion 3,565,414

Total noncurrent liabilities 139,276,677

Total liabilities 153,422,444

Commitments and contingencies

NET ASSETS

Invested in capital assets, net of related debt 61,359,362Restricted:

Expendable:Scholarships and loans 15,395Capital projects 6,319,269Debt services 1,252,407Other special purposes 3,473,920

Unrestricted 3,970,518

Total net assets 76,390,871

Total liabilities and net assets $ 229,813,315

The accompanying notes are an integralpart of these financial statements.

17

OHLONE COMMUNITY COLLEGE DISTRICT

DISCRETELY PRESENTED COMPONENT UNIT - OHLONE COLLEGE FOUNDATION

(A Nonprofit Organization)

STATEMENT OF NET ASSETS

June 30, 2010

ASSETS

Current assets:Cash and cash equivalents $ 921,959Accounts receivable 38,517Other assets 14,640Prepaid expenses 1,500

Total current assets 976,616

Noncurrent assets:Investments 2,185,669Assets held in trust 832,320

Total noncurrent assets 3,017,989

Total assets $ 3,994,605

LIABILITIES

Current liabilities:Accounts payable $ 104,707Liability to beneficiaries due within one year 67,258

Total current liabilities 171,965

Noncurrent liabilities:Liability to beneficiaries 387,665

Total liabilities 559,630

Commitments and contingencies

NET ASSETS

Restricted:Restricted by donors 1,218,707Permanent endowments 1,882,500

Unrestricted 333,768

Total net assets 3,434,975

Total liabilities and net assets $ 3,994,605

The accompanying notes are an integralpart of these financial statements.

18

OHLONE COMMUNITY COLLEGE DISTRICT

STATEMENT OF REVENUES, EXPENSES AND CHANGE IN NET ASSETS

For the Year Ended June 30, 2010

Operating revenues:Tuition and fees (gross) $ 8,211,270Less: scholarship discounts and allowances (1,157,977)

Net tuition and fees 7,053,293

Grants and contracts/gifts, non-capital:Federal 7,361,512State 4,203,113Local 1,106,842

Auxiliary enterprise sales and charges 2,066,573

Total operating revenues 21,791,333

Operating expenses:Academic and classified salaries 38,353,199Employee benefits 7,997,209Supplies, materials, and other operating expenses

and services 10,336,945Depreciation 5,965,295Student financial aid and scholarships 5,784,036

Total operating expenses 68,436,684

Loss from operations (46,645,351)

Non-operating revenues (expenses):State apportionment, non-capital 25,273,414Local property taxes 12,903,548State taxes and other revenues 1,351,420Investment income, noncapital 110,136Investment income, capital 144,763Interest expense on capital asset-related debt, net (6,169,520)Net loss on disposal of building and equipment (21,213)Other non-operating revenues 1,622,643

Total non-operating revenues 35,215,191

Loss before capital revenues (11,430,160)

Capital revenues:State apportionment 207,138Local property taxes and revenues 7,739,189

Total capital revenues 7,946,327

Change in net assets (3,483,833)

Net assets, July 1, 2009 79,874,704

Net assets, June 30, 2010 $ 76,390,871

The accompanying notes are an integralpart of these financial statements.

19

OHLONE COMMUNITY COLLEGE DISTRICT

DISCRETELY PRESENTED COMPONENT -OHLONE COLLEGE FOUNDATION

(A Nonprofit Organization)

STATEMENT OF REVENUES, EXPENSES AND CHANGE IN NET ASSETS

For the Year Ended June 30, 2010

Temporarily Permanently Unrestricted Restricted Restricted Total

Revenues and support:Revenues:

Private donations, grants andbequests $ 44,658 $ 808,420 $ 20,000 $ 873,078

Program management income 10,817 10,817Change in value of split-interest

agreements 20,264 20,264Investment income 10,879 114,888 125,767Operating transfers (57,731) (477,269) 535,000

Total revenues 8,623 466,303 555,000 1,029,926

Support:Events 129,110 129,110In-kind contributions 504,865 504,865

Total support 633,975 633,975

Net assets released from restrictionsand transfers 750,635 (750,635)

Total revenues and support 1,393,233 (284,332) 555,000 1,663,901

Expenses:Program services:

College program support 791,626 791,626Scholarships 130,825 130,825

Total program services 922,451 922,451

Support services:Events 164,971 164,971Fundraising 245,965 245,965Contract services 56,241 56,241

Total support services 467,177 467,177

Total expenses 1,389,628 1,389,628

Change in net assets 3,605 (284,332) 555,000 274,273

Net assets, beginning of year 330,163 1,503,039 1,327,500 3,160,702

Net assets, end of year $ 333,768 $ 1,218,707 $ 1,882,500 $ 3,434,975

The accompanying notes are an integralpart of these financial statements.

20

OHLONE COMMUNITY COLLEGE DISTRICT

STATEMENT OF CASH FLOWS

For the Year Ended June 30, 2010

Cash flows from operating activities:Tuition and fees $ 7,789,685Federal grants and contracts 7,126,224State grants and contracts 4,203,113Local grants and contracts 962,107Payments to suppliers for goods and services (16,327,260)Payment to/on behalf of employees (46,777,606)Payment to/on behalf of students (5,786,432)Auxiliary enterprises sales and charges 1,826,802

Net cash used in operating activities (46,983,367)

Cash flows from noncapital financing activities:State appropriations and receipts 24,193,933State taxes and other revenue 291,611Property taxes 12,903,549Other receipts 1,618,112

Net cash provided by noncapital financing activities 39,007,205

Cash flows from capital and related financing activities:State appropriations for capital purposes 691,308Purchase of capital assets (1,321,479)Loss on disposal, capital assets (21,213)Principal paid on capital debt (1,300,000)Interest paid on capital debt (4,514,167)Local property taxes and other revenues for capital purposes 7,739,189

Net cash provided by capital and related financing activities 1,273,638

Cash flows provided by investing activities:Investment income 172,643

Change in cash and cash equivalents (6,702,524)

Cash and cash equivalents - beginning of year 30,048,735

Cash and cash equivalents - end of year $ 23,518,854

Reconciliation of loss from operations to net cash used inoperating activities:

Loss from operations $ (46,645,351)Adjustments to reconcile loss from operations to net cash

used in operating activities:Depreciation expense 5,965,295Changes in assets and liabilities:

Accounts receivable (202,886)Inventory and prepaids (131,674)Accounts payable (7,846,950)Deferred revenue 366,018Compensated absences 854,580Retiree health benefits 657,601

Net cash used in operating activities $ (46,983,367)

The accompanying notes are an integralpart of these financial statements.

21

OHLONE COMMUNITY COLLEGE DISTRICT

DISCRETELY PRESENTED COMPONENT UNIT - OHLONE COLLEGE FOUNDATION

(A Nonprofit Organization)

STATEMENT OF CASH FLOWS

For the Year Ended June 30, 2010

Cash flows from operating activities:Received from private donors $ 974,274Received from other sources 16,018Payments to suppliers for goods and services (116,455)Payments for distribution to District (613,143)Payment to/on behalf of students (65,525)

Net cash provided by operating activities 195,169

Cash flows from investing activities:Net cash used in investment activities (580,554)

Change in cash and cash equivalents (385,385)

Cash and cash equivalents - beginning of year 1,307,344

Cash and cash equivalents - end of year $ 921,959

Reconciliation of change in net assets to net cashprovided by operating activities:

Increase in net assets $ 274,273Adjustments to reconcile increase in net assets to

net cash provided by operating activities:Change in value of split-interest agreements (20,264)Donation of property and equipment (14,640)Interest and dividends on investments (111,423)Change in assets and liabilities:

Accounts receivable (6,262)Prepaid expense (1,500)Accounts payable 80,620Deferred revenue (5,635)

Net cash provided by operating activities $ 195,169

The accompanying notes are an integralpart of these financial statements.

22

OHLONE COMMUNITY COLLEGE DISTRICT

STATEMENT OF FIDUCIARY NET ASSETS

June 30, 2010

AssociatedStudents of

Ohlone College

ASSETS

Cash and cash equivalents $ 725,062Accounts receivable 78,535

Total assets $ 803,597

LIABILITIES

Accounts payable $ 24,509Deferred revenue 36,713Amounts held in trust for others 742,375

Total liabilities $ 803,597

The accompanying notes are an integralpart of these financial statements.

23

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Reporting Entity

Ohlone Community College District (the "District"), formerly known as Fremont-NewarkCommunity College District, was established July 1, 1966 with the founding of OhloneCollege. The District operates a main campus in the city of Fremont and a satellite inNewark.

The District has reviewed criteria to determine whether other entities with activities thatbenefit the District should be included within its financial reporting entity. The decisionto include potential component units in the reporting entity was made by applying thecriteria set forth in generally accepted accounting principles (GAAP) and GASB Cod.Sec. 2100.101 as amended by GASB Cod. Sec. 2100.138. The District, based on itsevaluation of this criteria, identified the Ohlone College Foundation (the "Foundation") asa component unit.

The Foundation was established as a legally separate, not-for-profit corporation tosupport the District and its students. It contributes to various scholarship funds for thebenefit of District students and also contributes directly to the District. The fundscontributed directly by the Foundation to the District are significant to the District'sfinancial statements. Therefore, the District has classified the Foundation as acomponent unit that will be discretely presented in the District's annual financialstatements. The District provides in-kind contributions to the Foundation in the form ofsalaries, facility use, equipment, supplies and utilities. The value of these in-kindcontributions for the year ended June 30, 2010 was estimated to be $504,865.

Complete financial statements for the Foundation may be obtained from the DistrictOffice at 43600 Mission Boulevard, Fremont, California.

Basis of Presentation - Financial Statements

GASB released Cod. Sec. 2200.101, "Basic Financial Statements and Management'sDiscussion and Analysis for State and Local Governments" in June 1999, whichestablished a new reporting format for annual financial statements. In November 1999,GASB released Cod. Sec. C05.101, "Basic Financial Statements and Management'sDiscussion and Analysis for Public Colleges and Universities," which applies the newreporting standards of GASB Cod. Sec. 2200.190 - .191 to public colleges anduniversities. The GASB then amended those statements in June 2001 with the issuanceof GASB Cod. Sec. 2200 and 2300. The District adopted and applied these newstandards beginning in 2001-02 as required. In May 2002, the GASB released Cod.Sec. 2100.142, "Determining Whether Certain Organizations Are Component Units,"which amends GASB Cod. Sec. 2100.119 - .140, to provide guidance for determiningand reporting whether certain organizations are component units. The District adoptedand applied this standard for the 2003-04 fiscal year as required. The District nowfollows the financial statement presentation required by the aforementioned provisions.This presentation provides a comprehensive, entity-wide perspective of the District'sassets, cash flows, and replaces the fund-group perspective previously required.

24

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Basis of Accounting

For financial reporting purposes, the District is considered a special-purposegovernment engaged only in business-type activities. Under this model, the District'sfinancial statements provide a comprehensive one-line look at its financial activities.Accordingly, the District's financial statements have been presented using the economicresources measurement focus and the accrual basis of accounting. All significant intra-agency transactions have been eliminated.

In addition to the District's business-type activities, the District maintains fiduciary funds.These funds account for assets held by the District in a trustee capacity or as an agenton behalf of others. Fiduciary funds are accounted for using the economic resourcesmeasurement focus. The District reports the following fiduciary funds:

Agency Funds – This fund includes the Associated Students and the Other AgencyFunds:

Associated Students Fund – The Associated Students Fund accounts for thefunds of the Associated Students. The amounts reported for student body fundsrepresent the combined totals of all accounts for the various student body clubsand activities within the District.

The Foundation's financial statements are prepared on the accrual basis of accounting.Recognition of contributions is dependent upon whether the contribution is restricted orunrestricted. Net assets are classified on the Statement of Net Assets as unrestricted,temporarily restricted or permanently restricted net assets based on the absence orexistence of donor-imposed restrictions.

The District has the option to apply all Financial Accounting Standards Board (FASB)pronouncements issued after November 30, 1989, unless FASB conflicts with GASB.The District has elected to not apply FASB pronouncements issued after that date.

Cash and Cash Equivalents

For the purposes of the financial statements, cash equivalents are defined as financialinstruments with an original maturity of three months or less. Funds invested in theAlameda County Treasury are considered cash equivalents.

Restricted Cash, Cash Equivalents and Investments

Cash that is externally restricted to make debt service payments, maintain sinking orreserve funds, or to purchase or construct capital or other noncurrent assets, isclassified as non current assets in the statement of net assets.

25

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Fair Value of Investments

The District records its investment in Alameda County Treasury at fair value. Changesin fair value are reported as revenue in the statement of revenues, expenses andchange in net assets. The fair value of investments, including the Alameda CountyTreasury external investment pool, at June 30, 2010 approximated their carrying value.Foundation investments in debt and equity securities are carried at market value.Realized gains and losses and unrealized appreciation (depreciation) of thoseinvestments are reflected in the statement of revenues, expenses and change in netassets.

Accounts Receivable

Accounts receivable consist of tuition and fee charges to students and auxiliaryenterprise services provided to students, faculty and staff, the majority of each residingin the State of California. Accounts receivable also include amounts due from theFederal Government, State and Local Governments, or private sources, in connectionwith reimbursements of allowable expenditures made pursuant to the District's grantsand contracts.

Contributions

Contributions receivable consist of unconditional promises to give. Unconditionalpromises to give that are expected to be collected within one year are recorded at netrealizable value. An allowance for uncollectible contributions receivable is establishedbased upon estimated losses related to specific amounts and is recorded through aprovision for bad debt which is charged to expense. Unconditional promises to give thatare expected to be collected with future years are recorded at the present value of theirestimated future cash flows. As of June 30, 2010, the Foundation has applied adiscount rate of 7% to its charitable remainder trusts expected to be received in futureyears greater than one year. At June 30, 2010, an allowance for uncollectiblecontributions is not considered necessary and has not been recorded.

Assets Held in Trust and Liability to Beneficiary

Charitable remainder trust assets include the estimated fair value of various irrevocablecharitable trusts in which the Foundation is both the trustee and secondary beneficiary.The net present values of these assets were determined using investment returnsconsistent with the composition of the asset portfolios, life expectancies, and relevantdiscount rate. Irrevocable charitable trusts whose use by the Foundation is limited dueto donor-imposed restrictions increase restricted net assets.

Liability to beneficiaries represents the present value of the liability due to primarybeneficiaries of the irrevocable charitable remainder trusts for which the Foundation isboth trustee and secondary beneficiary. On an annual basis, the Foundation reviews itsactuarial assumptions and the need to revalue the liability for future distributions to thedesignated beneficiaries based upon any changes in the actuarial assumptions. Thepresent value of the estimated future payments is calculated using a discount rate of5.0% and applicable life expectancy tables.

26

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Inventory

Inventories are stated at cost, determined using the retail inventory method.

Capital Assets

Capital assets are recorded at the date of acquisition, or fair market value at the date ofdonation in the case of gifts. For equipment, the District's capitalization policy includesall items with a unit cost of $5,000 or more, and estimated useful life of greater than oneyear. Renovations to buildings, infrastructure, and land improvements that significantlyincrease the value or extend the useful life of the structure are capitalized. Routinerepairs and maintenance are charged to operating expense in the year in which theexpense was incurred.

Depreciation is computed using the straight-line method over the estimated useful livesof the assets, generally 50 years for buildings, 20 years for land improvements, 8 yearsfor vehicles, and 5 – 10 years for machinery and equipment.

The District evaluates capital assets for financial impairment as events or changes incircumstances indicate that the carrying amounts of such assets may not be fullyrecoverable.

Compensated Absences

Compensated absences costs are accrued when earned by employees. Accumulatedunpaid employee vacation benefits are recognized at year end as liabilities of theDistrict.

Accumulated Sick Leave

Sick leave benefits are not recognized as liabilities of the District. The District's policy isto record sick leave as an operating expenditure or expense in the period taken sincesuch benefits do not vest nor is payment probable; however, unused sick leave is addedto the creditable service period for calculation of retirement benefits for certain STRSand PERS employees, when the employee retires.

Deferred Revenue

Revenue from federal, state and local special projects and programs is recognized whenqualified expenditures have been incurred. Funds received but not earned are recordedas deferred revenue until earned.

27

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Net Assets

The District's net assets are classified as follows:

Invested in capital assets, net of related debt: This represents the District's totalinvestment in capital assets, net of associated outstanding debt obligations related tothose capital assets. To the extent debt has been incurred but not yet expended forcapital assets, such amounts are not included as a component invested in capitalassets, net of related debt.

Restricted net assets: Restricted expendable net assets include resources in which theDistrict is legally or contractually obligated to spend in accordance with restrictionsimposed by external third parties. Nonexpendable restricted net assets consist ofendowment and similar type funds in which donors or other outside sources havestipulated, as a condition of the gift instrument, that the principal is to be maintainedinviolate and in perpetuity, and invested for the purpose of producing present and futureincome, which may either be expended or added to principal.

Unrestricted net assets: Unrestricted net assets represent resources derived fromstudent tuition and fees, State apportionments, and sales and services of educationaldepartments and auxiliary enterprises. These resources are used for transactionsrelating to the educational and general operations of the District, and may be used at thediscretion of the governing board to meet current expenses for any purpose.

When an expense is incurred that can be paid using either restricted or unrestrictedresources, the District's policy is to first apply the expense toward unrestrictedresources, and then towards restricted resources.

The Foundation's net assets are classified as follows:

Unrestricted: Unrestricted net assets consist of all resources of the Foundation, whichhave not been specifically restricted by a donor.

Temporarily restricted: Temporarily restricted net assets consist of cash and otherassets received with donor stipulations that limit the use of the donated assets. When astipulated time restriction ends or purpose restriction is accomplished, temporarilyrestricted net assets are reclassified to unrestricted net assets and reported in theStatement of Revenue, Expense, and Change in Net Assets as net assets releasedfrom restriction.

Permanently restricted: Permanently restricted net assets are nonexpendable net assetsconsisting of endowment and similar type funds in which the donor has stipulated ascondition of the gift, that the principal be maintained in perpetuity.

The Foundation's endowment currently consists of 36 individual funds established forthe purpose of supporting education at the District. The endowment includes donor-restricted endowment funds. Net assets associated with endowment funds areclassified and reported based on the existence or absence of donor-imposedrestrictions.

28

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Net Assets (Continued)

The Board of Directors of the Foundation has interpreted UPMIFA as requiring thepreservation of the fair value of the original gift as of the gift date of the donor-restrictedendowment funds absent explicit donor stipulations to the contrary. As a result of thisinterpretation, the Foundation classifies as permanently restricted net assets (a) theoriginal value of the gifts donated to the permanent endowment, (b) the original value ofsubsequent gifts to the permanent endowment, and (c) accumulations to the permanentendowment made in accordance with the direction of the applicable donor giftinstrument at the time the accumulation is added to the fund. The remaining portion ofthe donor-restricted endowment fund that is not classified in permanently restricted netassets is classified as temporarily restricted net assets until those amounts areappropriated for expenditure by the organization in a manner consistent with thestandard prudence prescribed by UPMIFA.

The Foundation follows the Foundation's adopted investment and spending policies forendowment assets that attempt to provide a predictable stream of funding to programssupported by its endowments while seeking to maintain purchasing power of theendowment assets. Endowment assets include those assets of donor-restricted fundsthat the Foundation must hold in perpetuity or for a donor-specific period(s) as well asboard-designated funds.

The investment objective is to optimize earnings on all invested funds, while maintainingthe preservation of capital. Risk will be minimized by investing in high quality fixedincome instruments. To the extent that corporate obligations are purchased, thosepurchases will be diversified in terms of issuer and industry sector.

State Apportionments

Certain current year apportionments from the state are based on various financial andstatistical information of the previous year. Prior year corrections due to therecalculation in February 2010 will be recorded in the year computed by the state.

On-Behalf Payments

GASB Cod Sec. 2300.120 requires that direct on-behalf payments for benefits andsalaries made by one entity to a third party recipient for the employees of another,legally separate entity be recognized as revenue and expenditures by the employergovernment. The State of California makes direct on-behalf payments for retirementbenefits to the State Teachers and Public Employees Retirement Systems on behalf ofall Community Colleges in California. However, a fiscal advisory issued by the CaliforniaDepartment of Education instructed districts not to record revenue and expenditures forthese on-behalf payments. These payments consist of state general fund contributionsto CalSTRS in the amount of $298,751 (2.017%) of salaries subject to CalSTRS). Hadthis amount been reflected in the District's financial statements, both revenues andexpenditures would have increased by $298,751.

29

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Classification of Revenue

The District has classified its revenues as either operating or nonoperating revenues.Certain significant revenue streams relied upon for operations are recorded asnonoperating revenues, as defined by GASB Cod. Sec. C05.101 including stateappropriations, local property taxes, and investment income. Nearly all the District'sexpenses are from exchange transactions. Revenues and expenses are classifiedaccording to the following criteria:

Operating revenues: Operating revenues include activities that have the characteristicsof exchange transactions, such as (1) student tuition and fees, net of scholarshipdiscounts and allowances, (2) sales and services of auxiliary enterprises, (3) mostfederal, state and local grants and contracts and federal appropriations, and (4) intereston institutional student loans.

Nonoperating revenues: Nonoperating revenues include activities that have thecharacteristics of nonexchange transactions, such as gifts and contributions, and otherrevenue sources described in GASB Cod. Sec. C05.101, such as state appropriationsand investment income.

Scholarship Discounts and Allowances

Student tuition and fee revenue are reported net of scholarship discounts andallowances in the statement of revenues, expenses and change in net assets.Scholarship discounts and allowances represent the difference between stated chargesfor goods and services provided by the District and the amount that is paid by studentsand/or third parties making payments on the students' behalf. Certain governmentalgrants, such as Board of Governor's Grants (BOGG) and other federal, state ornongovernmental programs, are recorded as operating revenues in the District'sfinancial statements. To the extent that revenues from such programs are used tosatisfy tuition and fees and other student charges, the District has recorded ascholarship discount and allowance.

Estimates

The preparation of financial statements in conformity with accounting principlesgenerally accepted in the United States of America requires management to makeestimates and assumptions. These estimates and assumptions affect the reportedamounts of assets and liabilities and disclosure of contingent assets and liabilities at thedate of the financial statements and the reported amounts of revenues and expendituresduring the reporting period. Accordingly, actual results may differ from those estimates.

30

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

New Financial Accounting Pronouncements

The Hierarchy of Generally Accepted Accounting Principles for State and LocalGovernments

In March 2009, the GASB issued Governmental Accounting Standards BoardCodification Section (GASB Cod. Sec.) 1000, The Hierarchy of Generally AcceptedAccounting Principles for State and Local Governments (GASB Cod. Sec. 1000). ThisStatement is intended to incorporate the hierarchy of generally accepted accountingprinciples (GAAP) for state and local governments into the Governmental AccountingStandard's Board (GASB) authoritative literature. The "GAAP hierarchy" consists of thesources of accounting principles used in the preparation of financial statements of stateand local governmental entities that are presented in conformity with GAAP, and theframework for selecting those principles. The adoption of this update did not have amaterial impact on the District's net assets, change in net assets and cash flows.

Codification of Accounting and Financial Reporting Guidance Contained in the AICPAStatements on Auditing Standards

In March 2009, the GASB issued GASB Cod. Sec. 2250, Codification of Accounting andFinancial Reporting Guidance Contained in the AICPA Statements on AuditingStandards (GASB Cod. Sec. 2250). The objective of this Statement is to incorporateinto the GASB authoritative literature certain accounting and financial reporting guidancepresented in the American Institute of Certified Public Accountants' Statement onAuditing Standards. This Statement addresses three issues not included in theauthoritative literature that establishes accounting principles – related party transactions,going concern considerations, and subsequent events. The presentation of principlesused in the preparation of financial statements is more appropriately included inaccounting and financial reporting standards rather than in the auditing literature. ThisStatement does not establish new accounting standards but rather incorporates theexisting guidance (to the extent appropriate in a governmental environment) in theGASB standards. The adoption of this Statement did not have a material impact on theDistrict's net assets, change in net assets and cash flows.

31

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

2. CASH, CASH EQUIVALENTS AND INVESTMENTS

Cash, cash equivalents and investments at June 30, 2010, consisted of the following:

Agency District Foundation Funds

Pooled Funds:Cash in County Treasury $ 20,021,273

Deposits:Cash on hand and in banks 3,497,581 $ 921,959 $ 725,062

Total cash, cash equivalents 23,518,854 921,959 725,062

Less: restricted cash and cash equivalents:

Cash held by Fiscal Agents 11,685,759Cash held in trust 130,000

Total restricted cash and cashequivalents 11,815,759

Net cash and cash equivalents $ 11,703,095 $ 921,959 $ 725,062

Investments $ - $ 3,017,989 $ -

Pooled Funds

As provided for by in Education Code, Section 41001, a significant portion of theDistrict's cash balances is deposited with the County Treasurer for the purpose ofincreasing interest earnings through County investment activities. Interest earned onsuch pooled cash balances is allocated proportionately to all funds in the pool.

Because the District's deposits are maintained in a recognized pooled investment fundunder the care of a third party and the District's share of the pool does not consist ofspecific, identifiable investment securities owned by the District, no disclosure of theindividual deposits and investments or related custodial credit risk classifications isrequired.

In accordance with applicable State laws, the Alameda County Treasurer may invest inderivative securities. However, at June 30, 2010, the Alameda County Treasurer hasindicated that the Treasurer's pooled investment fund contained no derivatives or otherinvestments with similar risk profiles.

Deposits

The California Government Code requires California banks and savings and loanassociations to secure the District's deposits by pledging government securities ascollateral. The market value of pledged securities must equal 110 percent of anagency's deposits. California law also allows financial institutions to secure an agency'sdeposits by pledging first trust deed mortgage notes having a value of 150 percent of anagency's total deposits and collateral is considered to be held in the name of the District.All cash held by financial institutions is entirely insured or collateralized.

32

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

2. CASH, CASH EQUIVALENTS AND INVESTMENTS (Continued)

Under provision of the District's policy, and in accordance with Sections 53601 and53602 of the California Government Code, the District may invest in the following typesof investments:

• Securities of the U.S. Government, or its agencies• Small Business Administration Loans• Negotiable Certificates of Deposit• Bankers' Acceptances• Commercial Paper• Local Agency Investment Fund (State Pool) Deposits• Passbook Savings Account Demand Deposits• Repurchase Agreements

Cash balances held in banks are insured up to $250,000 by the Federal DepositoryInsurance Corporation (FDIC). At June 30, 2010, the carrying amount of the District'scash on hand and in banks (including certificates of deposit) was $3,497,581 and thebank balance was $4,428,320. The bank balance amount insured by the FDIC was$500,000, with the remaining balance fully collateralized.

At June 30, 2010, the carrying amount of the Foundation's cash on hand and in bankswas $921,959 and the bank balance was $921,959. The bank balance amount insuredby the FDIC was $250,000, with the remaining balance fully collateralized.

At June 30, 2010, the carrying amount of the Agency Fund's cash on hand and in bankswas $725,062 and the bank balance was $744,548. The bank balance amount insuredby the FDIC was $250,000, with the remaining balance fully collateralized.

33

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

2. CASH, CASH EQUIVALENTS AND INVESTMENTS (Continued)

Investments Authorized by the District's and Foundation's Investment Policies

The table below identifies the investment types authorized for the District by theCalifornia Government Code Section 53601. This table also identifies certain provisionsof the California Government Code that address interest rate risk, credit risk andconcentration of credit risk.

Maximum MaximumMaximum Percentage Investment in

Authorized Investment Type Maturity of Portfolio One Issuer

Local Agency Bonds or Notes 5 years None NoneU.S. Treasury Obligations 5 years None NoneU.S. Agency Securities 5 years None NoneBankers Acceptances 180 days 40% 30%Commercial Paper 270 days 25% 10%Negotiable Certificates of Deposit 5 years 30% NoneRepurchase Agreements 1 year None NoneReverse Repurchase Agreements 92 days 20% NoneMedium-Term Notes 5 years 30% NoneMutual Funds N/A 20% 10%Mortgage Pass through Securities 5 years 20% NoneJoint Power Agreements 5 years 20% NoneCounty Pooled Investment Funds N/A None NoneLocal Agency Investment Funds (LAIF) N/A None None

The table below identifies the investment types authorized by the Foundation'sinvestment policy. The Foundation's investment policy does not contain any specificprovisions intended to limit the Foundation's exposure to interest rate risk, credit risk andconcentration of credit risk.

Maximum MaximumAuthorized Maximum Minimum Percentage Investment in

Investment Type Maturity Rating (1) of Portfolio One Issuer

Common Stock N/A N/A 5% NonePreferred Stock N/A N/A 5% NoneU.S. Treasury Obligations N/A N/A 15% NoneU.S. Agency Securities N/A N/A 15% NoneFixed Income Investments N/A N/A 15% NoneMutual Funds N/A N/A N/A None

(1) U.S. Treasury securities and other fixed investments that carry an "investment grade" rating by Standardand Poor's or Moody's rating service. The finance committee may periodically grant the investmentmanager discretion to invest up to 15% of the portfolio in below investment grade fixed incomeinvestments.

Derivative Investments

The District and Foundation did not directly enter into any derivative investments.

34

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

2. CASH, CASH EQUIVALENTS AND INVESTMENTS (Continued)

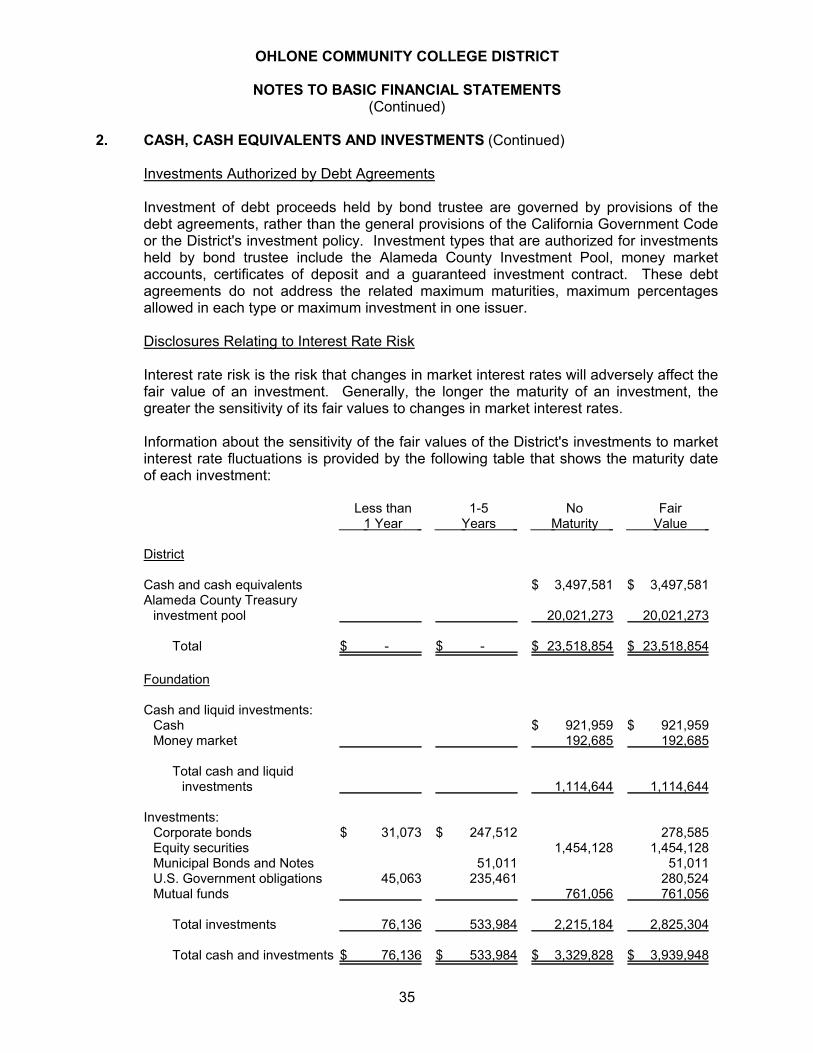

Investments Authorized by Debt Agreements

Investment of debt proceeds held by bond trustee are governed by provisions of thedebt agreements, rather than the general provisions of the California Government Codeor the District's investment policy. Investment types that are authorized for investmentsheld by bond trustee include the Alameda County Investment Pool, money marketaccounts, certificates of deposit and a guaranteed investment contract. These debtagreements do not address the related maximum maturities, maximum percentagesallowed in each type or maximum investment in one issuer.

Disclosures Relating to Interest Rate Risk

Interest rate risk is the risk that changes in market interest rates will adversely affect thefair value of an investment. Generally, the longer the maturity of an investment, thegreater the sensitivity of its fair values to changes in market interest rates.

Information about the sensitivity of the fair values of the District's investments to marketinterest rate fluctuations is provided by the following table that shows the maturity dateof each investment:

Less than 1-5 No Fair 1 Year Years Maturity Value

District

Cash and cash equivalents $ 3,497,581 $ 3,497,581Alameda County Treasury

investment pool 20,021,273 20,021,273

Total $ - $ - $ 23,518,854 $ 23,518,854

Foundation

Cash and liquid investments:Cash $ 921,959 $ 921,959Money market 192,685 192,685

Total cash and liquidinvestments 1,114,644 1,114,644

Investments:Corporate bonds $ 31,073 $ 247,512 278,585Equity securities 1,454,128 1,454,128Municipal Bonds and Notes 51,011 51,011U.S. Government obligations 45,063 235,461 280,524Mutual funds 761,056 761,056

Total investments 76,136 533,984 2,215,184 2,825,304

Total cash and investments $ 76,136 $ 533,984 $ 3,329,828 $ 3,939,948

35

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

2. CASH, CASH EQUIVALENTS AND INVESTMENTS (Continued)

Disclosures Relating to Credit Risk

Generally, credit risk is the risk that an issuer of an investment will not fulfill its obligationto the holder of the investment. This is measured by the assignment of a rating by anationally recognized statistical rating organization. The County Treasury investmentpool does not have a rating provided by a nationally recognized statistical ratingorganization.

Presented below is the minimum rating required by (where applicable) the CaliforniaGovernment Code, or debt agreements, and the actual rating as of year end for eachinvestment type.

Fair Investment Moody's Value

District

Alameda County Treasuryinvestment pool N/A $ 20,021,273

Cash and cash equivalents N/A 3,497,581

Total District cash and investments $ 23,518,854

Foundation

Cash and liquid investments:Cash N/A $ 921,959Money markets N/A 192,685

Total cash and liquid investments 1,114,644

Investments:Corporate bonds and mutual funds Aa2 134,331Corporate bonds and mutual funds Aa3 10,431Corporate bonds and mutual funds A2 124,175Corporate bonds and mutual funds B3 9,648Corporate bonds and mutual funds Not Rated 761,056Municipal bonds and notes AA3 51,011Equity securities Not Rated 1,454,128U.S. Government obligations Aaa 280,524

Total investments 2,825,304

Total Foundation cash and investments $ 3,939,948

36

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

2. CASH, CASH EQUIVALENTS AND INVESTMENTS (Continued)

Fair Value Measurements

The following presents information about the Foundation's assets and liabilitiesmeasured at fair value on a recurring basis as of June 30, 2010, and indicates the fairvalue hierarchy of the valuation techniques utilized by the Foundation to determine suchfair value based on the hierarchy:

Level 1 - Quoted market prices or identical instruments traded in active exchangemarkets.

Level 2 - Significant other observable inputs such as quoted prices for identical orsimilar instruments in markets that are not active, and model-based valuationtechniques for which all significant assumptions are observable or can be corroboratedby observable market data.

Level 3 - Significant unobservable inputs that reflect a reporting entity's ownassumptions about the methods that market participants would use in pricing an assetor liability.

The Foundation is required or permitted to record the following assets at fair value on arecurring basis:

Description Fair Value Level 1 Level 2 Level 3

Investment securities:Equity securities $ 1,454,128 $ 1,454,128Corporate bonds 278,585 $ 278,585Municipal bonds and

notes 51,011 51,011U.S. Government

obligations 280,524 280,524Mutual funds 761,056 761,056

$ 2,825,304 $ 1,454,128 $ 1,371,176 $ -

The fair value of investment securities classified as Level 1 equals quoted marketprices. Certain investments were classified as Level 2 as comparable investmentsecurities were used to determine fair value measurements.

The Foundation had no non-recurring assets and no liabilities at June 30, 2010, whichwere required to be disclosed using the fair value hierarchy.

Concentration of Credit Risk

The investment policies of the District and Foundation contain no limitations on theamount that can be invested in any one issuer beyond that stipulated by the CaliforniaEducation Code. There are no investments in any one issuer that represent 5% or moreof total County Office investments.

37

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

2. CASH, CASH EQUIVALENTS AND INVESTMENTS (Continued)

Custodial Credit Risk

Custodial credit risk for deposits is the risk that, in the event of the failure of a depositoryfinancial institution, a government will not be able to recover its deposits or will not beable to recover collateral securities that are in the possession of an outside party. TheCalifornia Education Code and the District's and Foundation's investment policies do notcontain legal or policy requirements that would limit the exposure to custodial credit riskfor deposits, other than the following provision for deposits: The California GovernmentCode requires that a financial institution secure deposits that are made by state or localgovernmental units by pledging securities in an undivided collateral pool held by adepository regulated under state law (unless so waived by the governmental unit). Themarket value of the pledged securities in the collateral pool must equal at least 110% ofthe total amounts deposited by the public agencies.

The Foundation did not hold any deposits with financial institutions in excess of federaldepository insurance limits held in uncollateralized accounts.

The custodial credit risk for investments is the risk that, in the event of the failure of thecounterparty (e.g., broker-dealer) to a transaction, a governmental entity will not be ableto recover the value of its investment or collateral securities that are in the possession ofanother party. The Foundation's investment policy does not contain legal or policyrequirements that would limit the exposure to custodial credit risk for investments. Withrespect to investments, custodial credit risk generally applies only to direct investmentsin marketable securities. Custodial credit risk does not apply to a governmental entity'sindirect investment in securities through the use of mutual funds.

Foreign Currency Risk

The current Foundation investment policy does not address foreign currency risk, whichis the risk that changes in exchange rates will adversely affect the fair value of aninvestment or a deposit. The Foundation does not have any deposits or investments inforeign currency.

3. ACCOUNTS RECEIVABLE

Accounts receivable at June 30, 2010 are summarized as follows:

Primary Institution Foundation

Federal $ 823,943State 6,638,672Local and other, net of allowance 548,177 $ 38,517

Totals $ 8,010,792 $ 38,517

The allowance for doubtful accounts of $536,568 is maintained at an amount whichmanagement considers sufficient to fully reserve and provide for the possibleuncollectibility of other receivable balances.

38

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

4. CAPITAL ASSETS

Capital asset activity consists of the following:

Balance BalanceJuly 1, June 30,

2009 Additions Deductions 2010

Non-depreciable:Land $ 36,116,441 $ 36,116,441Construction work in progress 4,574,560 $ 1,762,916 $ 153,977 6,183,499

Depreciable:Buildings and improvements 173,150,312 52,550 173,202,862Donated Equipment 129,716 129,716Machinery and equipment 19,500,381 1,354,681 88,708 20,766,354Bookstore equipment 407,475 264,797 672,272

Total 233,749,169 3,564,660 242,685 237,071,144

Less accumulated depreciation:Building and improvements 23,326,608 2,160,019 25,486,627Machinery and equipment 10,385,510 3,719,496 67,491 14,037,515Bookstore equipment 215,425 85,780 301,205

Total 33,927,543 5,965,295 67,491 39,825,347

Capital assets, net $ 199,821,626 $ (2,400,635) $ 175,194 $ 197,245,797

5. DEFERRED REVENUE AND DEFERRED SUPPORT

Deferred revenue for the District consisted of the following:

Deferred federal and state revenue $ 310,000Deferred local revenue 3,639Deferred student fees 492,116Deferred tuition and other student enrollment fees 2,172,222

Total deferred revenue $ 2,977,977

6. SPLIT-INTEREST AGREEMENTS

The Foundation's split-interest agreements with donors consist of irrevocable charitableremainder unitrusts, where the Foundation serves as both trustee and beneficiary.Assets invested under these trusts and payments made to beneficiaries are based onthe terms of the trust agreements. As of June 30, 2010, assets held in trust underunitrust agreements total $832,320 and the associated liability to beneficiaries of$454,923 is recorded in the statement of net assets.

39

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

7. LONG-TERM LIABILITIES

Changes in Long-Term Liabilities

A schedule of changes in general long-term liabilities for the year ended June 30, 2010is shown below:

Balance BalanceJuly 1, June 30, Due Within Non-

2009 Additions Deductions 2010 One Year Current

Compensated absences $ 1,197,864 $ 132,908 $ 116,813 $ 1,213,959 $ 309,268 $ 904,691Post-employment health

benefits 857,072 725,666 880,772 701,966 701,966General obligation bonds 133,305,000 1,300,000 132,005,000 1,605,000 130,400,000Bond premiums 3,937,456 186,021 3,751,435 186,021 3,565,414SERP liability 1,900,820 115,245 1,785,575 380,164 1,405,411Accreted interest 2,012,976 286,219 2,299,195 2,299,195

$ 141,320,981 $ 3,045,613 $ 2,598,851 $ 141,757,130 $ 2,480,453 $ 139,276,677

General Obligation Bonds

In June 2002 and August 2005, the District issued general obligation bonds totaling$150,000,000. These bonds were issued to finance the acquisition, construction andmodernization of property and facilities.

A summary of activity for general obligation bonds during the year ended June 30, 2010is as follows:

Amount Bonds BondsDate of Interest of Original Outstanding Redeemed Outstanding

Issue Rate Issue July 1, 2009 During Year June 30, 2010

2002 3.00 - 5.375% $ 40,000,000 $ 27,190,000 $ 1,100,000 $ 26,090,0002006 3.00 - 5.375% 110,000,000 106,115,000 200,000 105,915,000

$ 150,000,000 $ 133,305,000 $ 1,300,000 $ 132,005,000

The annual requirements to amortize general obligation bonds outstanding as ofJune 30, 2010 are as follows:

Year Ending June 30, Principal Interest Total

2011 $ 1,605,000 $ 6,047,838 $ 7,652,8382012 1,935,000 5,985,325 7,920,3252013 2,310,000 5,892,000 8,202,0002014 2,285,497 6,158,228 8,443,7252015 2,579,814 6,296,286 8,876,100

2016-2020 15,164,689 33,601,857 48,766,5462021-2025 34,920,000 23,192,903 58,112,9032026-2030 71,205,000 13,269,250 84,474,250

$ 132,005,000 $ 100,443,687 $ 232,448,687

40

OHLONE COMMUNITY COLLEGE DISTRICT

NOTES TO BASIC FINANCIAL STATEMENTS(Continued)

7. LONG-TERM LIABILITIES (Continued)

SERP Liability

During 2010, the District provided the option of a Supplemental Employee RetirementPlan ("SERP") to the District employees. As of June 30, 2010, there were 31 employeesin the Plan. Employees under the SERP will receive monthly annuity benefits. TheDistrict is obligated to pay annual installments for the calculated benefits for employeesunder the SERP and for the administration of the plan.

The annual requirements to amortize the SERP liability outstanding as of June 30, 2010are as follows:

Year Ending June 30,

2011 $ 380,1642012 380,1642013 380,1642014 380,1642015 264,919

$ 1,785,575

8. PROPERTY TAXES

All property taxes are levied and collected by the Tax Assessor of the County ofAlameda and paid upon collection to the various taxing entities including the District.Secured taxes are levied on July 1 and are due in two installments on November 1 andFebruary 1, and become delinquent on December 10 and April 10, respectively. Thelien date for secured and unsecured property taxes is March 1 of the preceding fiscalyear.

9. FUNCTIONAL EXPENSES

For the year ended June 30, 2010, operating expenses are charged by function asfollows:

StudentFinancial

Foundation Salaries Benefits Services Depreciation Aid Total

Instructional activities $ 19,699,396 $ 2,433,008 $ 1,233,699 $ 23,366,103Instructional support 2,624,343 541,253 288,320 3,453,916Student services 6,057,122 1,551,764 864,425 8,473,311Plant operations and

maintenance 1,933,970 805,040 1,820,606 4,559,616Institutional support 5,007,940 1,974,761 3,118,415 10,101,116Community services and

economic development 1,732,705 368,179 1,094,700 3,195,584Ancillary and auxiliary

services 1,218,141 321,636 1,916,780 3,456,557Student aid 79,582 1,568 $ 5,784,036 5,865,186Depreciation expense $ 5,965,295 5,965,295

$ 38,353,199 $ 7,997,209 $ 10,336,945 $ 5,965,295 $ 5,784,036 $ 68,436,684

41

OHLONE COMMUNITY COLLEGE DISTRICT