Embed Size (px)

Citation preview

Office of the District Audit Officer, State Audit, Kakinada.

The Draft Audit Report on the accounts of Municipal Council, Samalkot for the year

2015-2016 is submitted herewith for kind approval duly enclosing the following documents.

1. Annual Account for the year 2015-2016.

2. Audit Report for the year 2014-2015.

3. Draft Special Letter.

AAO Dist. Audit Officer

WORK DONE STATEMENT

Sl.No.

Name of the Auditor Subjects allotted for Audit Signature

1. B. Rama Krishna, AAO Works Audit, Verification ofAnnual Account and overall

supervision on the work doneby auditors.

2. G. Satyanarayana, S.A. General Contingencies,Advances & Deposits,

Work/pay Bill recoveries & theirpayment, Vr. Adj. Regr, MDR &

Town Planning Receipt3. RVT Kumar, SA. Public Health & Engineering

Contingencies, Provident FundA/c, D & O Trades

4. K. Deepak, SA. All Cash Books/Pass Books,Out Sourcing Salaries alongwith EPF & ESI payments,

Treasury salaries w.r.t. TBR5.6.

Ch. Ramesh, SA &Smt K. Sireesha

Chitta, MR, DD’s & ChequesReceipt Regr., Petty Cash

Book, Library Cess Receipt &Payment & PT/WT/VLT ChallanRegrs, Vr. Tracing in cash book

etc.,

GOVERNMENT OF ANDHRA PRADESHSTATE AUDIT DEPARTMENT

From ToSri L. Peeroji, M.Com., The Commissioner,District Audit Officer, Municipal Council,State Audit, Samalkot.Kakinada.

Lr.S.A.No. 92/ 2016-17/ dt:_12.5.17__________

Sir,

Sub :- Audit – Audit Report on the accounts of Samalkot Municipality for the year 2015-2016 – Issued – Reg.

*** I forward here with the audit report on the accounts of Samalkot Municipality for the

year 2015-2016 in duplicate with reference to Rule 60(d) of Schedule – II to the A.P.

Municipalities Act, 1965 and to request that one copy of the Audit Report may be returned to

Asst. Audit Officer, State Audit (T1), Kakinada together with the replies in triplicate duly

approved by the Council within 3 months from the date of receipt of the Audit Report as

required in G.O.Rt.No.876 M.A., Dept., dt.13.11.1967.

Yours faithfully,Sd /- L.Peeroji

DISTRICT AUDIT OFFICER,STATE AUDIT, KAKINADA.

Encl :- Audit Report in duplicate.Copy to the Accountant General, A.P., Hyderabad.Copy submitted to the Regional Deputy Director of State Audit, Zone-II, Eluru.

GOVERNMENT OF ANDHRA PRADESHSTATE AUDIT DEPARTMENT

From ToSri L. Peeroji, M.Com., Sri K.T. SudhakarDistrict Audit Officer, Commissioner,State Audit, Municipal Council,Kakinada. SAMALKOT

Spl. Lr. S.A.No. 86, dt: 04-07-2017

Sir,

I have the honor to invite your attention to paragraphs

35, 36, 39, 41, 42, 46, 47, 48, 51, 53, 54, 60, 61, 101, 102 (Extracts Enclosed) of audit report

on the accounts of Municipal Council, Samalkot, E.G.Dist, for the year 2015-2016 and to

state that unless the defects pointed out in are recorded and the facts reported to this office

within four months from the date of receipt of this letter. Action will be taken under sub-rule 4

of rule 9 as rules issued in G.O.Ms.No.130 Fin&P (FW-Admn-II) Department dated 8-9-2000

under section 16 by Andhra Pradesh State Audit Act.

Yours faithfully, Sd /- L.Peeroji

District Audit Officer, State Audit, Kakinada.

AUDIT REPORT ON THE ACCOUNTS OF MUNICIPAL COUNCIL, SAMALKOT FOR THEYEAR 2015-2016

Name of the Auditor :- Sri B. Rama Krishna. Asst. Audit Officer

Time taken for audit :- 11.07.2016, 16.7.2016,18.07.2016 to 23.07.2016,

16.01.2017 to 21.01.2017, 23.01.2017 to 25.01.2017,

27.01.2017 to 28.01.2017 &30.01.2017.

The office of the Chairman was held by the following persons during the period under

audit.

Sl. No. Name of the SpecialOfficer/Chairman

Period

1 Smt M. Padmavathi 01.04.2015 to 31.03.2016

The office of the Commissioner was held by the following person during the year

under audit.

Sl. No Name of the Commissioner Period

1 Sri K. T. Sudhakar 01-04-2015 to 31-03-2016

1. GENERAL FINANCIAL REVIEW:

The receipts and payments during the year were shown in the Receipts & Paymentsstatement together with the opening and closing balances. The opening balance in the cashbook was in agreement with the closing balance of the previous year. The consolidatedannual account (MGF + CPF + PEF) was showing the closing balance of Rs.11,92,21,600.68on 31-3-2016. The monthly abstracts and yearly abstract are arrived at and noted in thecash books at the time of audit.

1(a) FINANCIAL POSITION

The resources of ULBs consist of grants and assistance from the Government of India

(GOI) and the State Government under various schemes and own revenue generated

through various tax and non-tax collections. The tax revenue mainly accrued from property

tax. Non-tax revenue comes from water charges, encroachment fees, developmental

charges, building fee, etc. The financial position of the ULB has been analysed with

reference to the figures provided in the budget as follows. Further during the year under

audit, as the subsidiary registers were not produced, the actual receipts in respect of

revenue were taken based on the annual account figures.

Rs.

Sl. No Head of account Budgetestimates

Actual Difference

1 Property tax 2,26,40,662.00 2,22,91,248.00 -3,49,414.002 Vacant land tax 10,00,000.00 2,46,593.00 -7,53,407.003 Entertainment tax 20,00,000.00 0.00 -20,00,000.004 Adv. Tax 2,25,000.00 84,883.00 -1,40,117.005 Water fees 55,00,000.00 58,85,931.00 3,85,931.006 D&O trades licence

fee5,00,000.00 5,89,125.00 89,125.00

7 Surcharge on StampDuty

1,20,00,000.00 88,27,218.00 -31,72,782.00

8 Magisterial Fines 1,00,000.00 0.00 -1,00,000.009 Int. on Arrears of Tax

Revenue85,00,000.00 Details not

available---

10 Sundry Receipts(PTC)

4,00,000.00 1,34,415.00 -2,65,585.00

11 Birth and Deathregister extract fee

1,00,000.00 2,11,350.00 1,11,350.00

12 Road Maint. Grant 1,50,00,000.00 0.00 1,50,00,000.0013 Misc. Receipt (TS) 3,00,000.00 3,85,393.00 85,393.0014 Law Charges 35,000.00 0.00 -35,000.0015 JB Grant 1,85,000.00 1,85,000.00 0.0016 OAP Grant 6,30,00,000.00 6,99,32,729.00 69,32,729.0017 Road Cutting Charges 1,00,000.00 0.00 -1,00,000.0018 Water Harvesting Pits 2,00,000.00 0.00 -2,00,000.0019 NFBS Grant 2,00,000.00 0.00 -2,00,000.0020 School Fees 2,000.00 0.00 2,000.0021 Market Leases 10,76,000.00 10,26,000.00 -50,000.0022 Shop Room Rents 27,50,000.00 34,12,826.00 6,62,826.0023 Kabela Fees 95,000.00 4,050.00 -90,950.0024 Avenues 16,900.00 7,484.00 -9,416.0025 Fishery 7,500.00 0.00 -7,500.0026 PH Misc. Receipt 1,05,000.00 88,180.00 -16,820.0027 Education Tax 25,59,930.00 Details not

available---

28 Tap Estimate Charges 1,00,000.00 17,811.00 -82,189.0029 Tap Security Deposits 1,50,000.00 43,480.00 -1,06,520.0030 Tap Repair Charges 1,00,000.00 7,350.00 -92,650.0031 Tap Donations 0.00 2,26,656.00 2,26,656.0032 Building Licence Fees 4,00,000.00 5,63,446.00 1,63,446.0033 Conversion Fees 2,00,000.00 0.00 -2,00,000.0034 Development Charges 1,50,000.00 2,09,291.00 59,291.0035 Compounding Fees 2,00,000.00 34,864.00 -1,65,136.0036 Building Material

Charges1,50,000.00 1,87,927.00 37,927.00

37 Town Planning Misc.Receipts

1,00,000.00 2.00.000.00 1,00,000.00

38 Enc. Fees 1,30,000.00 1,11,650.00 -,18,350.0039 Lay out Fees 1,00,000.00 46,360.00 -53,640.0040 Water Supply Tanker

Charges0.00 80,488.00 80,488.00

1( b) TAX REVENUE RAISED BY THE MUNICIPAL COUNCIL:-

The tax revenue consists of property tax, water tax and advertisement tax etc. Taxon property is the main source which constituted the bulk of revenue receipts of MunicipalCouncil during the year. An analysis of tax revenue for the current year and the precedingtwo years is given below.

Sl.No.

Nature of Tax

Collection Increase/Decrease

w.r.t.previous

year

2013-14Rs

2014-15Rs

2015-16Rs

1 Property tax1,36,93,407.0

0

1,75,93,233.0

0

2,22,91,248.0

0Increased

2 Advertisement tax 1,48,815.00 2,61,670.00 84,883.00Decrease

d3 Vacant land tax 2,76,197.00 1,78,644.00 2,46,593.00 Increased4 Water Tax 47,24,280.00 51,88,583.00 58,85,931.00 Increased

5 Entertainment tax 0.00 10,65,772.00 0.00Decrease

d

1(c) NON-TAX REVENUE OF THE MUNICIPAL COUNCIL:-

Building rents, leases of markets, slaughter houses, D& O Licence fees etc., form thenon-tax revenue and constituted …… percentage of revenue of the municipal council. Ananalysis of the non-tax revenue under some principal heads for the year and during thepreceding 2 years is given here under.

Sl.No.

Item ofrevenue

Collection Increase/Decreasewith ref. to

previous years2013-14 2014-15 2015-16

1Leases of markets

7,83,870.00 8.25.981.00 10,26,000.00 Increase

2Slaughter house

66,500.00 68,100.00 4,050.00 Decrease

3License fees (D&O)

5,14,301.00 5,56,625.00 5,89,425.00 Increase

4Building license fee

4,00,632.00 6,56,975.00 7,72,737.00 Increase

5Shop Room rents

19,60,330.00 24,96,013.00 34,12,886.00 Increase

6 Others 55,735.00 23,904.00 7,484.00 Decrease

7D & O License

fees5,14,301.00 5,56,625.00 5,89,425.00 Increase

8Encroachment

fee63,450.00 1,38,000.00 1,11,650.00 Decrease

1 (d) REVENUE RECEIPTS AND ITS ANALYSIS:-

The source of revenue receipts during the year was through (1) revenue raised by theMunicipal Council (2) receipts from the state government towards share of entertainment tax,and surcharge on stamp duty etc (3) Grant-in-aid received from the Government. Ananalysis of receipts under the above heads during the year along with corresponding figuresfor the preceding 2 years is given below.

Item of revenueRECEIPTS

2013-14 2014-15 2015-16

1.Revenue raised by Municipal Councila) Tax Revenue 1,41,18,419.00 2,32,22,130.00 2,85,08,655.00b) Non-tax revenue leases, fees and rents etc

38,44,488.00 45,40,219.00 65,13,597.00

Total: 1,79,62,907.00 2,77,62,349.00 3,50,22,252.002. Receipts from Govt.

a) Entertainment tax 0.00 10,65,772.00 0.00b) Surcharge on SD 33,71,316.00 72,16,014.00 88,97,126.00c) 13th Fin. Grant ---- 3,05,60,074.00 ----d) 14th Fin. Grant --- --- 1,39,30,736.00Total 3371316.00 3,88,41,860.00 2,28,27,862.00

1 (e) DETAILS OF THE CLOSING BALANCES AS PER RECEIPTS AND PAYMENTS

STATEMENT IN ANNUAL ACCOUNT AS ON 31-3-2016:

SL.NO DETAILS MGF CPF PEF

TOTAL

1

Cash in

Hand 5,90,426.00 0.00 0.00

5,90,426.00

2

Cash at

Bank 7,54,39,973.57

4,29,02,408.1

1

2,88,793.0

0

11,86,31,174.6

8

3

Cheque in

Hand 0.00 0.00 0.00

0.00

TOTAL 7,60,30,399.57

4,29,02,408.1

1

2,88,793.0

0

11,92,21,600.6

8

DETAILS OF THE CLOSING BALANCES AS PER CASH BOOKS IN ULB AS ON 31-3-2016:

Cash Cheque in

hand

Treasury/Bank

C.B as per the General Fundscash book (001)

3,22,164.00 0.00 4,33,64,954.00

C.B as per the General Fundscash book (002)

2,41,766.000.00

91,26,869.00

C.B as per the 13th Finance cashbook (003)

0.000.00

2,40,75,568.00

Library Cess 13,249.00 0.00 0.00

Development Charges 5,192.00 0.00 7,36,590.00

RWHS 8,055.00 0.00 9,01,999.00

Total 5,90,426.00 0.00 *****

****** Closing balances of other cash books separate Statement enclosed

SEPARTAE STATEMENT ENCLOSED

OB'S, RECEIPT, EXPENDITURE & CB'S OF MGF/CPF/PEF'S OF SAMALKOT MUNICIPALITY FOR THE YEAR 2015-2016

SL.NO. NAME OF THESCHEME BANK A/c No. OB

RECEIPT PAYMENTSCB

INTEREST GRANT/OTHER EXP. BC

CAPITAL PROJECT FUND

1 Slum Dev. AB, PDP 23798 1696.00 68.00 0.00 0.00 0.00 1764.00

2 TPRO Salary AB,SMLKT 73160 76899.50 3112.00 0.00 0.00 68.00 79943.50

3 Parks & Play Grounds AB, PDP 779 3454.00 140.00 0.00 0.00 0.00 3594.00

4 Office Building AB, PDP 22647 90406.00 3661.00 0.00 0.00 0.00 94067.00

5 NFBS AB, PDP 229 6742.00 273.00 0.00 0.00 0.00 7015.00

6 JB & SS SBH,SMLKT 83643 -85000.00 0.00 94790.00 0.00 300.00 9490.00

7 MSB AB,SMLKT 99492 79947.00 3236.00 0.00 0.00 0.00 83183.00

8 USEP AB,SMLKT 16830 709.00 28.00 0.00 0.00 0.00 737.00

9 Census AB,SMLKT 18893 83368.00 5020.00 29450.00 0.00 0.00 117838.00

10 NPG AB, PDP 2777 6462697.00 231324.00 0.00 2024321.00 0.00 4669700.00

11 12th Fin. AB, PDP 760 5238.00 212.00 0.00 0.00 0.00 5450.00

12 ASG BOI, SMLKT 12857 146685.00 5853.00 0.00 13759.00 0.00 138779.00

13 BC Census BOI, SMLKT 5109 18236.00 737.00 0.00 0.00 0.00 18973.00

14 ILCS SBH, SMLKT 3623 6485182.00 263325.00 0.00 0.00 0.00 6748507.00

15 School Facilities SBH, SMLKT 99253 8790.00 356.00 0.00 0.00 0.00 9146.00

16SJSRY (Prog. & Maint.) SBI, SMLKT 21468 10776.00 0.00 0.00 0.00 630.00 10146.00

17 13th Fin. SBI, PDP 203003 29810565.00 0.00 0.00 5734997.00 0.00 24075568.00 Dif. With ERP Rs. 3,04,456/-

18 SPL. NPG SBI, SMLKT 25713 159113.83 6456.00 0.00 0.00 0.00 165569.83

19 MP LADS SBI, SMLKT 72333 120863.47 5935.00 675000.00 51809.00 0.00 749989.47

20 COM. TOILETS SBI, SMLKT 25917 4812.00 195.00 0.00 0.00 0.00 5007.00

21 OAP SBI, SMLKT 26353 17196.00 15013.3764453712

64472826 69.00 13026.37

22 PENSION GRANT SBI, PDP 21571 166712.00 0.00 0.00 0.00 630.00 166082.00

23 PAVALA VADDI SBI, SMLKT 95882 173261.00 7000.00 0.00 0.00 0.00 180261.00

24 CDP SBI, PDP 844812022 3873592.00 0.00 550750.00 1218622.00 0.00 3205720.00

25 SJSRY (CS) SBI, SMLKT 21162 7320.00 0.00 0.00 0.00 630.00 6690.00

26 NFBS (TRY.) SBI, PDP 844812012 0.00 0.00 0.00 0.00 0.00 0.00

27 Election Grant SBH, SMLKT 56164 4623.00 143.00 0.00 0.00 0.00 4766.00 Dif., Rs. 45/- in OB & CB

28 ICE Activities SBH, SMLKT 545614 0.00 0.00 2071826.00 44730.00 452.00 2026644.00 NEW

29 SCAP SBH, SMLKT 267640 0.00 0.00 40500.00 40000.00 250.00 250.00 NEW

CPF TOTAL 47733883.80 552087.37 67916028.00 73601064 3029.00 42597906.17

MUNICIPAL GENERAL FUND

1 001 SBI, PDP 8448120001 51716676.00 0.00 19888255.00 27917813.00 0.00 43687118.00 Dif. With ERP Rs. 1,50,434/- (ST)

2 002 SBI, PDP 8448120002 6927054.00 0.00 31742136 29300555.00 0.00 9368635.00 Dif. With ERP Rs. 7,92,765/- (ST)

3 PF STAFF SBI, SMLKT 160643 3847325.00 160115.00 977504.00 719378.00 0.00 4265566.00

4 TEACHING PF SBI, SMLKT 49444 99733.57 4029.00 0.00 0.00 0.00 103762.57

5 BPS/BRS SBI, SMLKT 21106 858750.00 0.00 0.00 0.00 630.00 858120.00

6 RWHS SBI, SMLKT 470602 595131.00 25723.00 282257.00 0.00 1112.00 901999.00 Dif. Rs. 2085/- (Reconcilation)

7 DEV. CHARGES SBI, SMLKT 467317 511638.00 22015.00 204099.00 0.00 1162.00 736590.00 Dif. Rs. 2085/- (Reconcilation)

8 STAFF RECOVERIES SBI,PDP 84332 -52374.00 0.00 3997561.00 3722030.00 859.00 222298.00 Dif. Rs.5524/- i.e., -227822/-

9 WATER USER CHARGESSBH, SMLKT 47248 472500.00 0.00 0.00 0.00 600.00 471900.00

10 PROPERTY TAX A/cSBH, SMLKT 34241 0.00 1055.00 198992.00 0.00 1055.00 198992.00

11 Lib. CessDUMMY A/c 2202010 28844.00 0.00 0.00 0.00 0.00 28844.00 Dummy A/c created by Accountant

12 Service Tax PayableSBH, SMLKT 6831024 0.00 0.00 927077.00 927077.00 0.00 0.00 NEW

13 EPF Online PaymentSBH, SMLKT 2943427 0.00 1.00 693032.00 693033.00 0.00 0.00 NEW

14 14th Fin. SBI, PDP 8448120004 0.00 0.00 13930736.00 0.00 0.00 13930736.00 NEW

15 BDC ON LINE HDFC,PDP 7151 164120.00 0.00 116500.00 0.00 0.00 280620.00 NEW

MGF TOTAL 65169397.57 212938.00 72958149.00 63279886.00 5418.00 75055180.57

PRIMARY EDUCATION FUND

1 Ele. Edn. Funds SBI, PDP 46986 289423.00 0.00 0.00 0.00 630.00 288793.00 OB Dif. Rs. 630/- Rs. 288793/-

PEF TOTAL 289423.00 0.00 0.00 0.00 630.00 288793.00

2 )COMPLAINCE OF AUDIT OBJECTIONS BY THE COMMISSIONER:-

The No. of objections pending at the beginning of the year, the No. of auditobjections added during the year, the no. of audit objections settled during the year andbalance, left at the close of the year along with the amount involved is given here under.

DetailsNo. of

objectionsAmount

Involved (in Lakhs)1972-73 to 2014-2015 1335 1723.17During the Year 2015-2016 114 114.09Total 1449 1837.26Settled during the year 0 0.00No. of Objections outstanding 1449 1837.26

According to the orders issued in G.O.Ms.No.874 M.A. Dept., dt.13.11.1967, the

audit reports and replies shall be placed before the Mpl. Council, and the replies submitted to

the Govt. through the Director of State Audit with a copy of the resolution approving the

replies for consideration of waiver of the objections. The records of the Mpl. Council do not

reveal the observance of these orders. The progress in the settlement of the audit objections

during the year 2015-2016 was poor. The Commissioner may take much interest in

rectifying the defects and in settling down the objections.

Code No.13) (A) Huge differences in Opening Balances (MGF) – Reasons not explained to

Audit :

On verification of annual account for the year 2015-16 there are hugevariations in different heads while adopting the previous year closing balances and openingbalances for this year. The differences are as follows.

Account Code

AccountHead

2014-15 CB 2015-16 OB Difference Remarks

3101001 RevenueTransfers

42,11,10,465.07

50,42,47,461.57

8,31,36,996.50

Reasons forenhancement not known.

3501002 Contractors 91,472.00 0.00 -91,472.00 Continuedfrom 31.3.14through MJ

3501003 Expenses 18,33,697.00 0.00 -18,33,697.00 Continuedfrom 09-10

=49,000.0010-11 =

12,62,020.0011-12 =

4,62,975.0012-13 =

58,752.0013-14 =

950.00 Total=

18,33,697.00

3501105 GPFPayable

7,39,361.00 0.00 -7,39,361.00 Transferredto 3502001

3502001 GPF 11,77,959.00 19,17,320.00 7,39,361.00 Transferredfrom 3502001

3503001 LibraryCess

Current

-3,48,243.00 0.00 -3,48,243.00 Reasons notknown

4501001 Cash inHand

15,91,558.00 8,67,982.00 -7,23,576.00 Reasons notknown

4501002 Cash inTransit

86,832.00 0.00 -86,832.00 Reasons notknown

4501051 Cheque inHand

3,07,435.00 0.00 -3,07,435.00 Reasons notknown

4502118 LibraryCess

(DummyA/c)

3,26,944.00 0.00 -3,26,944.00 Reasons notknown

4601002 Conveyance Advance

3,992.00 0.00 -3,992.00 Reasons notknown

4601003 ComputerAdvance

1,00,000.00 0.00 -1,00,000.00 Reasons notknown

4601006 Misc. 7,80,862.00 0.00 -7,80,862.00 Reasons not

Advances known

4601007 PayAdvance

60,000.00 0.00 -60,000.00 Reasons notknown

4601009 MarriageAdvance

25,000.00 0.00 -25,000.00 Reasons notknown

4602000 EPF Loans 12,02,586.00 0.00 -12,02,586.00 Reasons notknown

4603000 Loans toothers

1,552.00 0.00 -1,552.00 Reasons notknown

4604003 Advance toExp.

10,73,000.00 0.00 -10,73,000.00 Reasons notknown

4608011 OtherCurrentAssets

-10,000.00 0.00 10,000.00 Reasons notknown

3) (b) Huge differences in Opening Balances (CPF) – Reasons not explained toAudit :

On verification of annual account for the year 2015-16 there are hugevariations in different heads while adopting the previous year closing balances and openingbalances for this year. The differences are as follows.

AccountCode

AccountHead

2014-15 CB 2015-16 OB Difference Remarks

3101001 RevenueTransfers

7,72,108.94 6,90,89,510.24 -81,63,598.70

Reasons forDECREASEnot known.

3501003 Expenses 12,85,410.00 0.00 -12,85,410.00

Reasons forDECREASEnot known.

4601006 Misc.Advances

-10,000.00 0.00 10,000.00 Reasons notknown

3 C) Huge differences in Opening Balances (PEF) – Reasons not explained toAudit :

On verification of annual account for the year 2015-16 there are hugevariations in different heads while adopting the previous year closing balances and openingbalances for this year. The differences are as follows.

AccountCode

AccountHead

2014-15 CB 2015-16 OB Difference Remarks

3101001 RevenueTransfers

5,45,437.00 2,88,793.00 -2,56,644.00 Reasons forDECREASEnot known.

3502008 TDS fromEmployees

46,360.00 0.00 -46,360.00 Reasons notknown

4702051 Inter FundTransfer

3,02,374.00 0.00 -3,02,374.00 Reasons notknown

Code.No 1 4 )DIFFERENCES BETWEEN ULB RECORDS & ANNUAL A/C IN RESPECT OFCLOSING BALANCES – NEEDS RECTIFICATION.

Audit reveals that the following are the differences between the ULB records &Annual A/c in respect of Closing Balances in various accounts. The same shall be rectifiedimmediately.

A. Municipal General Fund

ItemName of the

A/c

Amountshown in

ULB Records

Amountshown in

Annual A/cDif.

1. Cheque in Hand

01 2,58,000.00 0.00 2,58,000.00

3.Treasury/ Bank Balances

001 4,33,64,954.00 4,35,15,388.00 1,50,434.00

002 91,26,869.00 99,19,634.00 7,92,765.00

Dummy A/c 0.00 28,844.00 28,844.00

StaffRecoveries 2,22,298.00 2,27,822.00 5,524.00

The reasons for the above differences between ULB records & Annual A/c in respect oftreasury/bank balances are not explained in Audit by the authorities. But, audit revealsthat the authorities are not reconcile the figures between cashbook & passbook. Thetreasury balance shown in the annual account must be the treasury balance shown incash book. But, the accountants are showing the balance available in treasury passbook as treasury balance in Annual Account. This is irregular. The same shall be

rectified.

B.Capital Project Fund

ItemName of the

A/cAmount shown

in ULBAmount shownin Annual A/c

Dif. With reasons

1. BankBalances

13 th Fin. 2,40,75,568.00 2,43,80,024.00 3,04,456.00

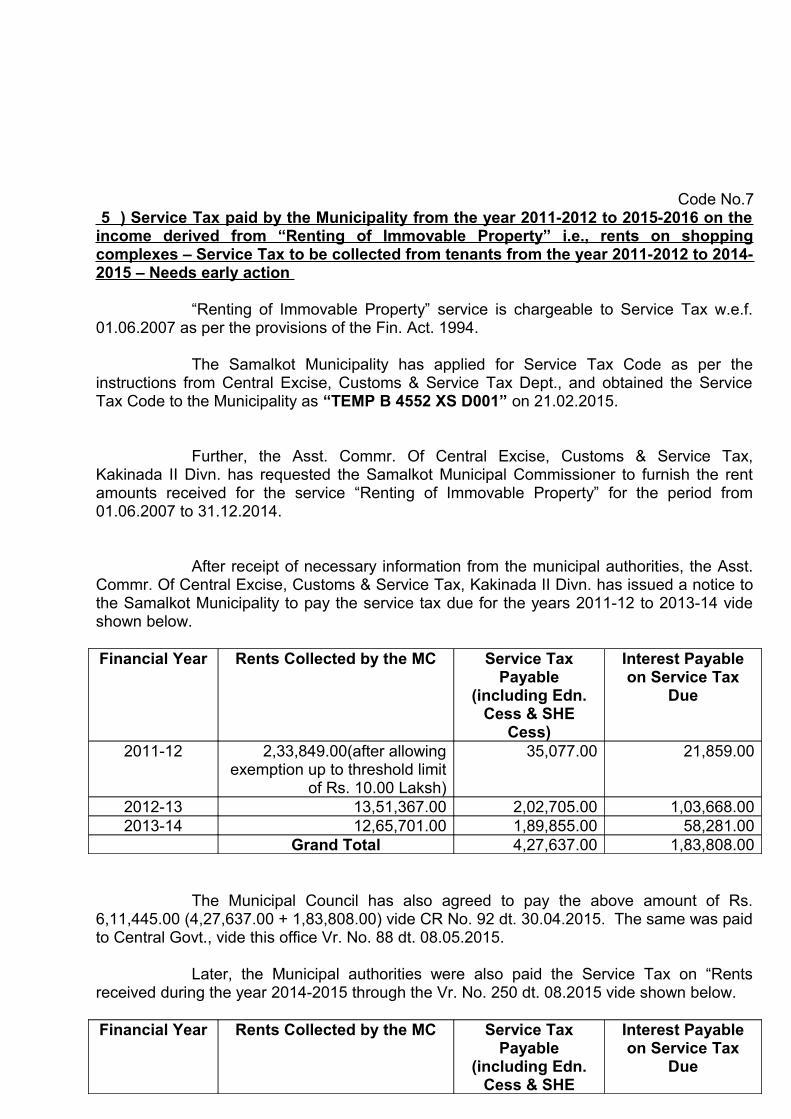

Code No.7 5 ) Service Tax paid by the Municipality from the year 2011-2012 to 2015-2016 on theincome derived from “Renting of Immovable Property” i.e., rents on shoppingcomplexes – Service Tax to be collected from tenants from the year 2011-2012 to 2014-2015 – Needs early action

“Renting of Immovable Property” service is chargeable to Service Tax w.e.f.01.06.2007 as per the provisions of the Fin. Act. 1994.

The Samalkot Municipality has applied for Service Tax Code as per theinstructions from Central Excise, Customs & Service Tax Dept., and obtained the ServiceTax Code to the Municipality as “TEMP B 4552 XS D001” on 21.02.2015.

Further, the Asst. Commr. Of Central Excise, Customs & Service Tax,Kakinada II Divn. has requested the Samalkot Municipal Commissioner to furnish the rentamounts received for the service “Renting of Immovable Property” for the period from01.06.2007 to 31.12.2014.

After receipt of necessary information from the municipal authorities, the Asst.Commr. Of Central Excise, Customs & Service Tax, Kakinada II Divn. has issued a notice tothe Samalkot Municipality to pay the service tax due for the years 2011-12 to 2013-14 videshown below.

Financial Year Rents Collected by the MC Service TaxPayable

(including Edn.Cess & SHE

Cess)

Interest Payableon Service Tax

Due

2011-12 2,33,849.00(after allowingexemption up to threshold limit

of Rs. 10.00 Laksh)

35,077.00 21,859.00

2012-13 13,51,367.00 2,02,705.00 1,03,668.002013-14 12,65,701.00 1,89,855.00 58,281.00

Grand Total 4,27,637.00 1,83,808.00

The Municipal Council has also agreed to pay the above amount of Rs.6,11,445.00 (4,27,637.00 + 1,83,808.00) vide CR No. 92 dt. 30.04.2015. The same was paidto Central Govt., vide this office Vr. No. 88 dt. 08.05.2015.

Later, the Municipal authorities were also paid the Service Tax on “Rentsreceived during the year 2014-2015 through the Vr. No. 250 dt. 08.2015 vide shown below.

Financial Year Rents Collected by the MC Service TaxPayable

(including Edn.Cess & SHE

Interest Payableon Service Tax

Due

Cess)2014-2015 8,49,686.00 1,05,021.00 0.00

Audit reveals that the municipal authorities were not recovered the service taxon rents from the tenants during the above years i.e., from 2011-2012 to 2014-2015. Due toavoiding legal complications the MC has paid the entire amount from his own funds. TheMunicipal Authorities are collecting rents along with service tax From the year 2015-2016.The receipt & payment particulars of Service Tax for the year 2015-2016 are as follows.

Financial Year Service Tax collected by theMC along with Shop Rents

Service Tax Paid(including Edn.

Cess & SHECess)

Vr. No. & Date

2015-2016 2,94,701.00 99,876.00 440/11.15 (4/15 to9/15)

75,203.00 576/02.16 (10/15 to1/16)

35,532.00 629/03.16 (2/2016)79,251.00 /06.16 (3/16)

Grant Total 2,89,862.00

Hence, the municipal authorities are here by instructed to recoup the amountsalready paid to Central Govt. towards Service Tax for the years 2011-12 to 2014-2015 fromthe tenants of shops and made good to municipal funds.

6 )Assessment of Service Charges on Railway Properties in Samalkot town – NeedsSpeed up of Collection process Rs. 15,31,812.00

Hon’ble Supreme Court has delivered a Judgement in Civil Appeal No. 9458, 9457,9464, 9465 all four of the year 2003 and No. 6706 of 2004 on 19.11.2009, in the matter ofpayment of service charges payable by Union of India and its sub-ordinate departments toMunicipal Corporations, in the case filed by Rajkot Municipal Corporation against Union ofIndia and others.

The Operating Part of the Judgement is as follows.

“ The Union of India and its departments will pay services provided by theappellant Municipal Corporations. The Service Charges shall be paid at 75 %,50 % and 33 1/3 % respectively of the property tax levied on private owners,depending upon whether Union of India or its department is utilizing the fullservices or partial services or nil services.“

Necessary instructions were also issued by the State Govt., vide Govt. Memo. No.170/TC.1/2001-1 MA, dt. 11.05.2010 for collection of service charges from Central Govt.Properties. Further, vide Govt. Memo. No. 14245/F2/2013-4 MA dt. 21.08.2013 Govt. statedthat there is no ambiguity on payment of 1/3rd of the demand by the railways even after theSupreme Court Orders. Therefore, there is no reason not to collect the same and the samemay be collected with arrears without prejudice to the claims of the respective parties.

Audit reveals that the Samalkot Municipal authorities are initially assessed theservice charges in respect of Samalkot Railway properties as follows.

Service Charges @ 75 % Service Charges @ 50 % Service Charges @ 33 %No. ofAssets

Amount No. ofAssets

Amount No. ofAssets

Amount

0 0 22 20,714.00 127 87,120.00

Later, the same were revised as follows.

Service Charges @ 75 % Service Charges @ 50 % Service Charges @ 33 %No. ofAssets

Amount No. ofAssets

Amount No. ofAssets

Amount

0 0 22 21,287.00 153 1,06,364.00

The Mpl. Commissioner is also addressed to A.D.E.N., South Central Railwayfor payment of service charges payable by Railway Authorities for a tune of Rs. 1,27,651/-per half year from April, 2010 onwards vide Lr. Roc. No. 571/2013-A2 dt. 09.07.2014. TheAssessment wise details were also sent as enclosures.

The Sr. Divisional Engineer (North), S.C. Railway, Vijayawada replied thatMunicipal Commissioner vide Lr. No. 417//I/2/Vol.Vii/Works dt. 01.08.2014. He has informedthat the process of payment of Service Charges to the Samalkot Municipality will be taken upas soon as the detailed guidelines are received from their Head Quarters office.

Further, the Municipal Commissioner has requested the A.D.E.N., SouthCentral Railway, Samalkot vide his Lr. Roc. No. 571/2013-A2 dt. 20.06.2015 to pay theservice charges immediately for the period from 4/2010. Surprisingly, the Commissioner hasasked the Railway Authorities to pay the service charges Rs. 1,07,834/- i.e., (Rs. 20,714/- +Rs. 87,120/-) instead of Rs. 1,27,651/- i.e., (Rs. 21,287/- + Rs. 1,06,364/-) as mentionedearlier. The same shall be rectified immediately.

Till date, the railway authorities are also not paid the service charges to themunicipality.

Hence, the authorities may address again to railway authorities for payment ofservice charges to municipality duly stating the following demand and made good to Mpl.General Funds.

Rs. 1,27,651/- per half year x 12 No. of Half Years = Rs. 15,31,812.00 (2010-11- to2015-16)

Code.No 97 ) Cash Book & Pass Book reconciliation is done in respect of PD A/cs. 001, 002 &003 – Defects noticed – Needs rectification.

Audit reveals that the cash books maintenance in Samalkot Municipality w.r.t.PD A/cs operated in the Sub-Treasury, Peddapuram it is known that the reconciliationprocess is doing now.

On verification of monthly reconciliations it is noticed the following defects. Thetypes of defects are at a glance as follows.

1.While taking the receipt, the remittances were posted in another a/c of thisMunicipality (or) another Municipality.

2.While booking the expenditure, the expenditure was posted in another a/c of thisMunicipality (or) another Municipality.

3.The other Municipal Receipt/Expenditure was taken in the Samalkot MC.

The details are as follows.

001 AccountDefect Needs Rectification

The Municipal Authorities are here byinstructed to address the treasury

authorities to rectify the defect throughAlteration Memo in Form T.A. IX

1. In the month of 7/2015 a Cheque i.e., No. 5111/28.07.2015 was issued for Rs. 34,019.00 from “002” A/c for payment of work bill recoveries to the concerned heads.

But, the expenditure was booked in the same Municipality in “001” A/c by mistake.

2. In the Month of 8/2015 a Cheque i.e., No. 5123/04.08.2015 was issued for Rs. 2,65,874.00 from “002” A/c for payment of EPF amount.

But, the expenditure was booked in the same Municipality in “001” A/c by mistake.

002 Account

Defect Needs Rectification

1. In the month of 7/2015 a Cheque i.e., No. 5111/28.07.2015 was issued for Rs. 34,019.00 from“002” A/c for payment of work bill recoveries to the

concerned heads.

But, the expenditure was booked in the same Municipality in “001” A/c by mistake.

The Municipal Authorities are here by instructed to address thetreasury authorities to rectify the defect through Alteration Memo in Form T.A. IX

2. In the Month of 8/2015 a Cheque i.e., No. 5123/04.08.2015 was issued for Rs. 2,65,874.00 from “002” A/c for payment of EPF amount.

But, the expenditure was booked in the same Municipality in “001” A/c by mistake.

3. In the month of 8/2015 an amount of Rs.35,902.00 adjusted to “002” A/c on 10.08.2015 videCh. No. 2205. But, the same was not deposited bythis Municipality.

Code. No 98) A Review on Journal Entries passed during the year

Journal Book shall be the book of original entry for recording all transactionsother than those involving cash and/or bank. A non-cash/bank transaction is first recorded inthe Journal Book by dividing into its debit and credit aspects, from which a posting is done inthe relevant ledger account.

A) JE’s not passed for demand fixation of receipt heads i.e., for PT/VLT/Advt.Tax/Water Tax/Markets/Shop Room Leases/Enc. Fees/D&O Licence Fees –Leads decrease in the receivables to the institution

Revenue Income is “Gross” inflow of receivables (which includes recoverablelike taxes, fees, lease amounts etc.,). In accrual basis of accounting, revenue incomes are

reflected in the accounts in the period in which they accrue. Accrual basis of accountingsystem could be followed for most of the income sources.

Pre-requisites for recognition of revenue on accrual basis:

Revenue Income

Is the incomeascertainable?

If the answer is “YES”

If the answer is “NO”

Is the data is accurate?Demand Notices served toall the Assesses?

Accrual Basis of Accounting

Cash Basis of Accounting

During the year the demand entries are not passed in Journal Book for thefollowing heads.

AccountCode

AccountHead

Demand raisedfor the current

year

Remarks

110-01-01 Property Tax 0.00

For these heads the income isascertainable & data is accurateand demand notices served to allassesses. Hence, these incomeheads are recognized on accrualbasis of accounting. Hence, theDemand entries to be passed by

the accountant.

110-01-02Vacant Land Tax

0.00

110-11-11 Advt. Tax 0.00110-02-02 Water Tax 0.00130-10-01 Market Sale 0.00130-10-15 Shop Rents 0.00140-11-01 D & O Trades 0.00

140-11-04Slaughter House License Fee

0.00

140-11-06 Enc. Fee 0.00

Format of Receivables:: OB + Fresh Demand(by JE) – Collection = CB

Audit reveals that due to non-passing of demand entries, the receivables of theSamalkot Municipality are decreased un-necessarily.

The details are as follows:-

Account

Code

AccountHead

Sub-Head

Receivables

OBDemandRaised

CB changeddue to

passing ofwrong JE

43110Receivablesof PT & VLT

Property Tax2,90,76,541.0

00.00

Vacant Land Tax

60,77,314.00 0.00

Total (A)3,51,53,855.0

00.00

43119Receivablesof other Taxes

Advt. Tax 3,51,270.00 0.00

Total (B) 3,51,270.00 0.0043130 Receivables Water Supply 1,86,43,524.0

for Fees & user charges

Receivables 00.00

Others 3,68,736.00 0.00Market Sale 11,01,000.00 0.00D & O Trades 4,69,000.00 0.00Slaughter House LicenseFee

83,000.00 0.00

Enc. Fee 1,76,000.00 0.00Building Permit Fee

4,68,000.00 0.00

Dev. Charges 1,84,000.00 0.00Other TP Receipt

2,36,000.00 0.00

Mutation Fees 98,000.00 0.00

Road cutting &restoration charges

6,63,000.00 0.00

Forms & Pass Books

80,000.00 0.00

Scrap 19,000.00 0.00

Old News Papers

2,000.00 0.00

Total ( C) 2,25,91,260 0.00

43140Receivablesfrom Shop Rents

Shop Rents 43,39,321.00 0.00

Total (D) 43,39,321.00 0.00

Total (A+B+C+D) 6,24,35,706.00

0.00

The authorities are hereby instructed to pass necessary demand entriesimmediately to show the correct amount of receivables of the institution.

B) The procedure in accounts manual for accounting of collections against demandnot followed – Collections made under each head were not posted against demand –But, the receivables reduced un-necessarily through passing JE’s - Resultsdecrease in receivables at the end of year – Needs Rectification.

- The procedure for accounting of collections is described below:

a) Recording of tax collections: Based on summary of daily collectionreceived from the various collecting centers, the accounts departmentshall pass the following entry:

Account Code Account Head Debit Credit

450-10-01/02 Cash/ Bank A/c 0.00

431-80-01Receivable control Accounts -Property Tax etc.,

0.00

b) The summary of daily collection does not provide the details in respect of the yearwise head wise collections made in respect of property and other taxes. Hence, thetotal amount collected should be credited to “Receivables Control Accounts – PropertyTaxes etc.,) A/c. The collection made shall be segregated into year wise, head wisecollection on a monthly basis.

c) Recording of break-up of collections: A summary statement of year wise/head wiseCollection of Property & other taxes shall be prepared and sent to the AccountsDepartment to record the details of collection. Interest on delayed payment may becharged to the taxpayer in accordance with relevant provisions. Interest shall berecognized as income only on collection.

d) To record the break-up of collections into year wise recovery, tax received inadvance and to record the interest income the accounts department shall pass thefollowing entry.

Account Code Account Head Debit Credit

431-80-01Receivable control Accounts -Property Tax etc.,

0.00

431-10-81Receivables of Property Taxes (year…..)

0.00

431-10-82Receivables of Property Taxes (year…..)

0.00

350-41-01Advance Collection of Revenues – Property Tax

0.00

171-80-01 Other Interests – Receivables 0.00140-20-05 Penalties & Fines 0.00

Audit reveals that the above procedure is not followed while accounting thetax/fees/rents etc.,

Instead of following the above procedure, at the end of year the accountanthas passed a journal entry vide JE No. MJ – 6146260/2015-2016 dt, 31.03.2016regarding DCB entry. The reason for passing the JE is also not explained in audit.Without adjusting the real collections under each head they are simply passing theabove JE. The same is hereby described as follows.

DCB as per made in ERP Journal Entries

Account Code

AccountHead

Sub-Head

Receivables

Demand(Arrear)

Reducedthrough

passing JE’s

Balance(Arrear)

43110Receivablesof PT & VLT

Property Tax

2,90,76,541.00 2,02,57,541.0088,19,000.00

Vacant Land Tax

60,77,314.00 27,63,314.00 33,14,000.00

Total (A) 3,51,53,855.00 2,30,20,855.00 1,21,33,000.00

43119Receivablesof other Taxes

Advt. Tax 3,51,270.00 2,30,270.00 1,21,000.00

Total (B) 3,51,270.00 2,30,270.00 1,21,000.0043130 Receivables

for Fees & user

Water Supply Receivables

1,86,43,524.001,22,98,524.00 63,45,000.00

chargesOthers 3,68,736.00 3,68,736.00 0.00Market Sale 11,01,000.00 11,01,000.00 0.00D & O Trades

4,69,000.00 4,69,000.00 0.00

Slaughter House License Fee

83,000.00 83,000.00 0.00

Enc. Fee 1,76,000.00 1,76,000.00 0.00Building Permit Fee

4,68,000.00 4,68,000.00 0.00

Dev. Charges

1,84,000.00 1,84,000.00 0.00

Other TP Receipt

2,36,000.00 2,36,000.00 0.00

Mutation Fees

98,000.00 98,000.00 0.00

Road cutting & restoration charges

6,63,000.00 6,63,000.00

0.00

Forms & Pass Books

80,000.00 80,000.00 0.00

Scrap 19,000.00 19,000.00 0.00

Old News Papers

2,000.00 2,000.00 0.00

Total ( C) 2,25,91,260 1,62,46,260.00 63,45,000.00

43140Receivablesfrom Shop Rents

Shop Rents 43,39,321.00 39,80,321.00 3,59,000.00

Total (D) 43,39,321.00 39,80,321.00 3,59,000.00

Total(A+B+C+D)

6,24,35,706.00 4,34,77,706.00 1,89,58,000.00

DCB As per the demand registers of the ULB

Account Code

Account

HeadSub-Head

Receivables

Demand(Arrear+Curren

t)

Collections(Arrear+Curren

t)

Balance(Arrear+Curren

t)

43110Receivables of PT &

VLT

Property Tax

Demand Regrs.Not written up

by the Mpl.Authorities

2,22,87,955.00 Balance detailsnot available in

MunicipalityVacant Land Tax

2,49,886.00

Total (A)

43119Receivables of other Taxes

Advt. Tax 3,05,997.00 79,181.00 2,26,816.00

Total (B)43130 Receivable

s for Fees & user

Water Supply Receivable

Demand Regrs.Not written up

by the Mpl.

58,85,931.00 Balance detailsnot available in

Municipality

charges s AuthoritiesMarket Sale

10,76,000.00 8,00,000.00 2,76,000.00

D & O Trades

5,25,125.00 5,25,125.00 0.00

Slaughter House License Fee

14,050.00 4,050.00 10,000.00

Enc. Fee 1.19.950.00 1,00,050.00 19.900.00

Total(C)

43140

Receivables from Shop Rents

Shop Rents

45,67,716.00 2946670.00 16,21,046.00

Total (D)

Total(A+B+C+D

)(Due to lake of information regarding the arrear demand of PT,VLT, WT the arrear balances of PT,VLT & WT not included in the above figure.

As seen from the above 2 DCB’s the difference in receivables of the institutionis as follows. The same shall be rectified immediately duly passing the necessary JournalEntries.

Receivables as on 31.03.2016 as per ERP (only Arrears shown) 1,89,58,000.00

Receivables as on 31.03.2016 as per ULB DCB Not finalisedlake of

DemandRegisters.

Difference ---

C) Cash balance adjustment entry passed through JE – Bank balances increased –Circumstances for passing the JE not explained to Audit.

Audit objections were raised regarding the differences between ERP & ULBrecords in respect of Cash in Hand in previous years.

The accountant has passed JE vide JE No. 6142756/2015-2016 dt02.04.2015 for clearing the difference in cash in hand and adjusted the difference amount tothe following accounts.

Sl. No. Details of Account Amount in Rs.

1 SBI, Peddapuram 001 (4502105) 2,43,873.00

2 SBI, Peddapuram 002 (4502106) 5,95,265.00

3 SBI, Library Cess (4502118) (Dummy Account)

28,844.00

Total 8,67,982.00

The basis for transferring the amounts to the above accounts is notexplained in audit. Hence, the authorities hereby instructed to explain the reasons withdetails for transferring the cash in hand amount to the above bank accounts to auditimmediately.

D) The real collections towards different taxes & fees are changed due to additions& deletions made through JE’s – Reasons for passing the JE’s are not explainedto Audit

During the year 2015-2016 the following amounts are received under differentheads towards taxes & fees as per Receipts & Payments statement. But, these amountswere changed due to passing of some JE’s by the Accountant. The reasons for additions &deletions to the concerned heads are not explained in audit.

Account

Code

Account

Head

RealReceipt(R &C)

Additionsvide

JournalEntry

Deletions vide

JournalEntry

FinalAmount

Shown asIncome

JE No. Remarks

1100101

Property Tax

2,22,91,248

0 64,55,955

MJ-6146260/15-16dt.31.03.2016

Reasonsnotknownfordeletion

0 3,293 1,58,32,000

MJ-5997354/15-16dt.31.03.2016

VLTtransferred to VLThead

1100102

VacantLandTax

2,46,593 3,293 0 MJ-6146260/15-16dt.31.03.2016

VLTamountreceivedfrom PThead

1,25,114.00

0 3,75,000 MJ-6146260/15-16dt.31.03.2016

Reasonsnotknownforaddition

1100201

WaterTax

58,85,931 1,44,069 0 60,30,000 MJ-6146260/15-16dt.31.03.2016

Reasonsnotknownforaddition

1101105

Advt.Tax

39,823 84,43,177 0 84,83,000 MJ-6146260/15-16dt.31.03.2016

Reasonsnotknownforaddition

130101 Shop 36,42,287 0 6,91,287 29,51,000 MJ- Reasons

5 Rents 6146260/15-16dt.31.03.2016

notknownfordeletion

Hence, the authorities are hereby instructed to explain the reasons to audit foradditions & deletions made to above heads.

E) Advances payable by the employees added /deleted through JE’s – Reasons notexplained to Audit:

During the year 2015-2016 the following amounts are given to loans &advances to the employees under different heads as per Receipts & Payments statement.But, these amounts were changed due to passing of some JE’s by the Accountant. Thereasons for additions & deletions to the concerned heads are not explained in audit.

AccountCode

AccountHead

RealExp.

(R &C)

Additions vide

JournalEntry

LoanRecovery vide

JournalEntry

FinalBalanc

eShownas Due

JE No.Remark

s

4601002(MGF)

Conveyance Adv.

60,000 51,750 1,08,750 3000 MJ-6146177/15-16dt.31.03.2016

Reasonsfor Additionof Rs. 51,750/- not known

4601006(MGF)

Other Adv. 0 3,08,400 0 3,08,400

MJ-6146177/15-16dt.31.03.2016

Reasonsfor Additionof Rs. 3,08,400/- not known

4601007(MGF)

MarriageAdv.

80,000 62,366 42,244 1,00,122

MJ-6146177/15-16dt.31.03.2016

Reasonsfor Additionof Rs. 62,366/- not known

4604003(MGF)

Adv. ForExp.

2,08,000

1,03,000 1,85,000 1,26,000

MJ-6146177/15-16dt.31.03.2016

Reasonsfor Additionof Rs. 1,03,000/- not known

46011000 (CPF)

Loans toOthers

14,543 0.00 14543.00

0.00 CJ-6146178/15-16dt.31.03.2016

Reasonsfor Deletionof Rs. 14,543/- not known

F) Adjustment of Work Bill Recoveries through JE’s – Reasons not explained toAudit:

During the year 2015-2016 the following amounts are Work Bill Recoveries & theirpayments under different heads as per Receipts & Payments statement. But, these amountswere changed due to passing of some JE’s by the Accountant. The reasons for additions &deletions to the concerned heads are not explained in audit.

Account

Code

AccountHead

RealReceipt(R &C)& OB

Additions vide

JournalEntry

Exp. videJournalEntry/Real Exp.

FinalBalanc

eShownas Due

JE No. &Date

Remarks

3502003

(MGF)

GIS 8,61,48750,967

11,713 09,24,167

0.00 MJ-6146189/15-16dt.31.03.2016

Reasons forAdditionof Rs.11,713/-notknown

3502008

(MGF)

TDS fromemployees

03,55,619

0 3,55,6190

0.00 MJ-6146189/15-16dt.31.03.2016

Reasons forDeletionof Rs.3,55,619/- notknown

3502015

(MGF)

LabourCess

0.00 12,66012,660

1,7865,1012,707

15,726 MJ-6146189/15-16dt.31.03.2016

Reasons forDeletionof Rs.5,101/-notknown

3502025

(MGF)

TDS fromContractor

s

4,65,4692,68,312

5,582 2,70,7294,20,798

47,836 MJ-6146189/15-16dt.31.03.2016

Reasons forDeletionof Rs.2,70,729/- notknown

3502052

(MGF)

VAT 8,99,6761,93,893

0 1,78,0708,34,363

81,136 MJ-6146189/15-16dt.31.03.2016

Reasons forDeletionof Rs.1,78,070/- notknown

3502053

(MGF)

CST/GST 06,211

0 6,2110

0.00 MJ-6146189/15-16dt.31.03.2016

Reasons forDeletionof Rs.6,211/-notknown

3502054

(MGF)

ServiceTax

026,008

9,01,069 09,27,077

0.00 MJ-6146189/15-16dt.31.03.2016

Reasons forAdditionof Rs.9,01,069/- notknown

3502056

(MGF)

Seignorage

2,01,2266,549

3,064 3,7961,80,651

26,392 MJ-6146189/15-16dt.31.03.2016

Reasons forAdditionof Rs.3,064/-notknown

3503001

(MGF)

Lib. CessCurrent

5,54,74612,660

0

0 12,66012,660

58976,798

4,64,699

0.00 MJ-6146189/15-16dt.31.03.2016

Reasons forDeletionof Rs.589/- notknown

3117006

(CPF)

OAP 69932729 11660

15,531 069946894

13,026 CJ-6146203/15-16dt.31.03.2016

Reasons forAdditionof Rs.15,531/-notknown

3502008

(CPF)

TDS fromemployees

073,525

0 73,5250

0.00 CJ-6146203/15-16dt.31.03.2016

Reasons forDeletionof Rs.73,525/-notknown

3502015

(CPF)

LabourCess

57,3190

2,862 43,70050

16,431

0.00 CJ-6146203/15-16dt.31.03.2016

Reasons forAdditionof Rs.2,862/-notknown

3502024

(CPF)

OtherEmp.

Deductions

01,100

0 1,100 0.00 CJ-6146203/15-16dt.31.03.2016

Reasons forDeletionof Rs.1,110/-notknown

3502025

(CPF)

TDS fromContractor

s

74,8683,01,086

0 1,2732,97,163

77,518

0.00 CJ-6146203/15-16

Reasons forDeletion

dt.31.03.2016

of Rs.2,97,163/- notknown

3502052 (CPF)

VAT 2,65,10216,636

0 2,3241,06,578

0.00 CJ-6146203/15-16dt.31.03.2016

Reasons forDeletionof Rs.2,324/-notknown

3502056

(CPF)

Seignorage

1,00,7798,860

0 3,0611,06,578

0.00 CJ-6146203/15-16dt.31.03.2016

Reasons forDeletionof Rs.3,061/-notknown

3502058 (CPF)

Otherrecoveries

fromcontractor

s

56,0461,64,065

42,283 042,283

1,64,065

--- ---

3503001

(CPF)

Lib. CessCurrent

010,681

1,41750

10,6811,467

0.00 CJ-6146203/15-16dt.31.03.2016

Reasons forDeletionof Rs.10,681/-notknown

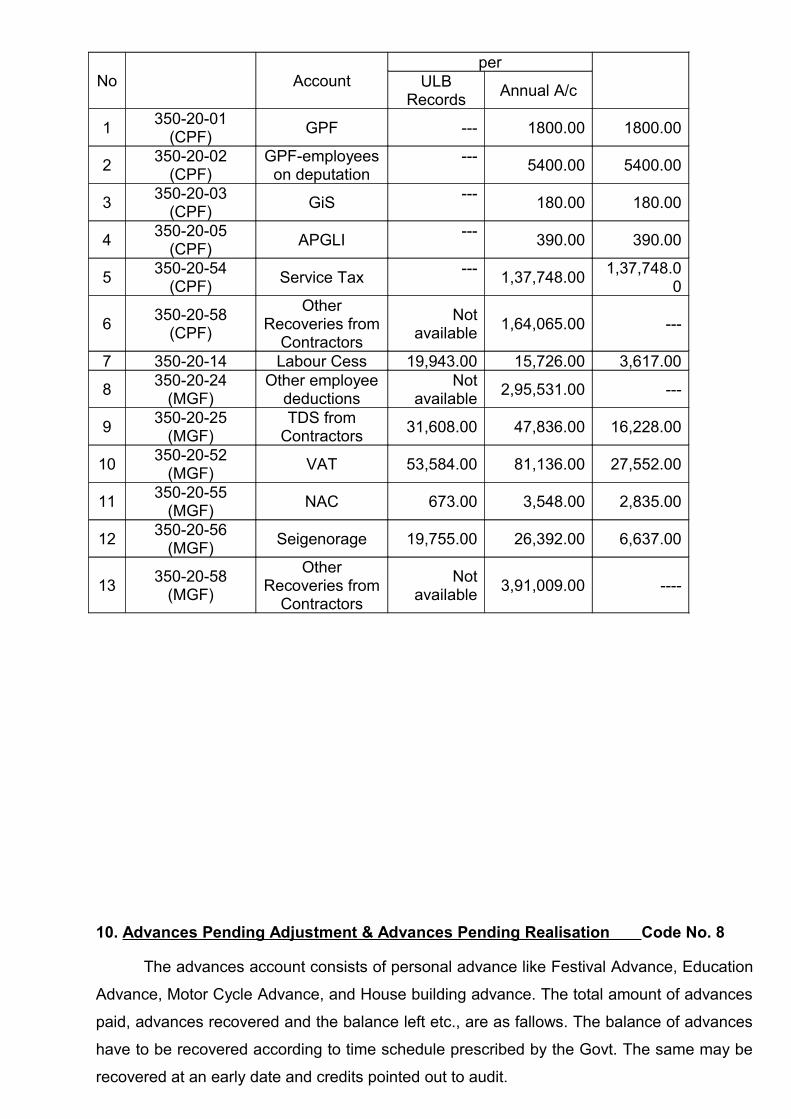

Code.No 1 9 ) Huge differences between the figures in ULB Records & Annual A/c in respect ofrecoveries payable – Needs Rectification.

Audit reveals that the authorities are promptly remitting all the recoveries everymonth to the concerned heads & departments. By mistake some of the deductions are notremitted. They are petty & shown below. But, as seen from the annual account under thehead of “350-20” i.e., Recoveries Payable showed huge balances pending remittance. Thisis not correct. The same shall be rectified duly re-examining the receipt & payments undereach head. The differences are as follows.

Sl. Account Code Head of Recoveries Payable as Difference

No Accountper

ULBRecords

Annual A/c

1350-20-01

(CPF)GPF --- 1800.00 1800.00

2350-20-02

(CPF)GPF-employees

on deputation---

5400.00 5400.00

3350-20-03

(CPF)GiS

---180.00 180.00

4350-20-05

(CPF)APGLI

---390.00 390.00

5350-20-54

(CPF)Service Tax

---1,37,748.00

1,37,748.00

6350-20-58

(CPF)

OtherRecoveries from

Contractors

Notavailable

1,64,065.00 ---

7 350-20-14 Labour Cess 19,943.00 15,726.00 3,617.00

8350-20-24

(MGF)Other employee

deductionsNot

available2,95,531.00 ---

9350-20-25

(MGF)TDS from

Contractors31,608.00 47,836.00 16,228.00

10350-20-52

(MGF)VAT 53,584.00 81,136.00 27,552.00

11350-20-55

(MGF)NAC 673.00 3,548.00 2,835.00

12350-20-56

(MGF)Seigenorage 19,755.00 26,392.00 6,637.00

13350-20-58

(MGF)

OtherRecoveries from

Contractors

Notavailable

3,91,009.00 ----

10. Advances Pending Adjustment & Advances Pending Realisation Code No. 8

The advances account consists of personal advance like Festival Advance, Education

Advance, Motor Cycle Advance, and House building advance. The total amount of advances

paid, advances recovered and the balance left etc., are as fallows. The balance of advances

have to be recovered according to time schedule prescribed by the Govt. The same may be

recovered at an early date and credits pointed out to audit.

Sl.No

Nature ofAdvance

DEMAND COLLECTION BALANCE

Arrear Current Total Arrear Current Total Arrear Current Total

1Festival Adv

4000 0 4000 0 0 0 4000 0 4000

2 MCA 291213 60000 351213 50600 0 50600 240613 60000 300613

3Marriage Adv

96916 80000 176916 27266 12128 39394 69650 67872 137522

4Sivarathri work Adv

100000 100000 200000 100000 0 100000 0 100000 100000

5All Advances

114100 108000 222100 100000 105000 205000 14100 3000 17100

Total 606229 348000 954229 277866 117128 394994 328363 230872 559235

Code No.9

11 ) MGF Receipt - Tender Deposits, EMD’s, Shop Deposits etc., were shown under

the head of other income i.e., Lapsed Deposits 180-11-02 – Irregular – Needs

Rectification.

As per Para No. 5.74 of AP Municipal Accounts Manual, Deposits not claimed

within 3 years from the date it is due for payment, shall be considered as lapsed and shall

not be repaid to the party. At the end of each accounting year, the respective sections shall

prepare a list of such lapsed deposits. To recognize the income, on obtaining the approval of

the authorities, the accounts section shall pass the necessary journal entries. But, this

process was not done in the year 2015-2016.

However, during the year the Other Income i.e., Lapsed Deposits under the

head “180-11-02” is shown in the Receipt & Payments as Rs. 21,83,592.00.

Audit reveals that the amount shown under the head of “180-11-02” during the

year is the receipt towards Tender Deposits, EMD’s & Shop Deposits amount etc., The

Shop Deposits, EMD.s & Tender Deposits are Capital Receipt. But, they are shown as

Revenue Receipt. This is irregular. The same shall be transferred to the heads noted against

each. The details are as follows.

Sl. No. Details Amount Head to be transferred1 Shop Deposits 17,48,217.00 340-20-012 EMD’s & Tender

Deposits4,35,075.00

340-10-01

Grand Total 21,83,592.00

Hence, the authorities are here by instructed to transfer the entire amount to

concerned heads immediately.

Code No.9

12 ) MGF Receipt – Rental Deposits under the head of 340-20-01 shown less than the

actual receipt – Irregular – Needs Rectification.

On verification of the subsidiary registers like Deposit Register it is noticed that an amount of Rs. 20,77,678.00 is received during the year 2015-16 towards Shop Deposits.

But, as seen from the annual account for the year 2015-16 the receipt towards Rental Deposits under the head of 340-20-01 is shown as Rs. 1,00,000.00. This is irregular.

While entering the receipt figures in ERP the same were entered in different headsas Revenue Receipt erroneously. The same shall be transferred to the head 340-20-01 immediately.

Name of the Receipt Transfer from Transfer to AmountOpening Balance 50,500.00

Rental Deposits

Receipt under the head 1,00,000.00130-10-15 340-20-01 2,29,461.00

180-11-02 340-20-01 17,48,217.00Grand Total 21,28,422.00

Code No.9

13) MGF Receipt – Earnest Money Deposits under the head of 340-10-01 shown less

than the actual receipt – Irregular – Needs Rectification.

On verification of the subsidiary registers like Deposit Register it is noticed that an amount of Rs. 7,73,918.00 is received during the year 2015-16 towards EMD’s.

But, as seen from the annual account for the year 2015-16 the receipt towards EMD’s under the head of 340-10-01 is shown as Rs. 3,36,168.00. This is irregular.

While entering the receipt figures in ERP the same were entered in different headsas Revenue Receipt erroneously. The same shall be transferred to the head 340-20-01 immediately.

Name of the Receipt Transfer from Transfer to AmountOpening Balance 3,02,884.00

EMD’s

Receipt under the head 3,36,168.00340-20-02 340-10-01 2,675.00

180-11-02 340-10-01 4,35,075.00Grand Total 10,76,802.00

Code – 9

14) MGF Receipt – Receipt towards Shop Deposits are posted under the head “130-10-

15” i.e., Rents from Shopping Complexes – Irregular - Needs rectification.

Audit reveals that the receipt towards Rents on shopping complexes during the year isRs. 34,12,826.00.

But, as seen from the Receipt & Payment statement, the receipt towards Rents onshopping complexes showed under the head of “130-10-15” is Rs. 36,42,287.00

Hence, the following amounts i.e., Shop Deposits etc. are shown under this head bymistake, the same shall be transferred to concerned head immediately duly passing theJournal entries.

Name of the Receipt Transfer from Transfer to AmountRents from Shopping

ComplexesReceipt under the head 36,42,287.00

130-10-15 340-20-01 (-) 2,29,461.00Grand Total 34,12,826.00

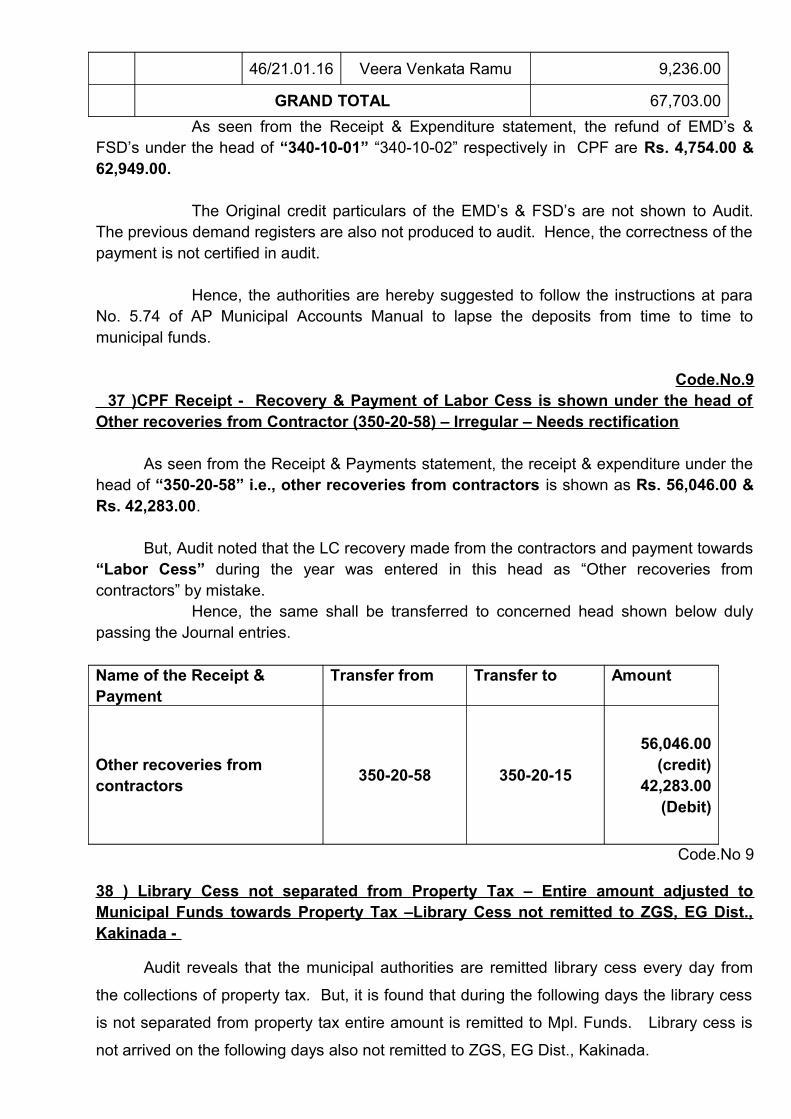

Code.No.9 15 )MGF Receipt - Recovery & Payment of Labor Cess is shown under the head ofOther recoveries from Contractor (350-20-58) – Irregular – Needs rectification.

As seen from the Receipt & Payments statement, the receipt & expenditureunder the head of “350-20-58” i.e., other recoveries from contractors is shown as Rs.1,66,035.00 & Rs. 1,64,572.00.

But, Audit noted that the LC recovery made from the contractors and paymenttowards “Labour Cess” during the year was entered in this head as “Other recoveries fromcontractors” by mistake.

Hence, the same shall be transferred to concerned head shown below dulypassing the Journal entries.

Name of the Receipt &Payment

Transfer from Transfer to Amount

Other recoveries from contractors

350-20-58 350-20-15

1,66,035.00(credit)

1,64,572.00(Debit)

Code.No.9 16 )MGF Payments – Payment towards Commissioner’s vehicle Hire Charges –Shown in the head of A/c of 230-40-02 instead of 220-40-02 – Irregular – Needsrectification

As seen from the Receipt & Payments statement, the expenditure taken under thehead of “230-40-02” i.e., Hire Charges to Vehicles is shown as Rs. 3,98,724.00

But, Audit noted that the payments made towards Commissioner’s vehicle hirecharges were entered in this head as “Hire Charges to Vehicles” by mistake.

Audit also reveals that the Commissioner’s vehicle hire charges to be enteredin the head of A/c of “220-40-02”

Hence, the same shall be transferred to concerned head shown below dulypassing the Journal entries.

Name of the Payment Transfer from Transfer to Amount

Hire Charges to Vehicles 230-40-02 220-40-02 3,98,724.00

Grand Total 3,98,724.00

Code.No.9 17 )MGF Exp. – Amount is shown under the head of Prior period item “OtherExpenses” (280-80-00) – Irregular – Needs rectification

As seen from the Receipt & Payments statement, the expenditure taken under thehead of “280-80-00” i.e., Prior period item “Other Expenses” is shown as Rs. 3,87,196.00

As per para No. 6.89 & 6.90 of AP Municipal Accounts Manual, Prior period items aregenerally infrequent in nature and can be distinguished from changes in accountingestimates. Accounting estimates by their nature are approximations that may needs revisionas additional information becomes known.

The nature and amount of prior period items should be separately disclosed in thestatement of Profit & Loss in a manner that their impact on the current profit or loss can beperceived.

But, Audit noted that School Sweeper salaries, School Rents, Park WatchmanSalaries, TPBO & AE salaries, Election Deposit Refunds & Penalties to Income Tax Dept.,are entered in this head as Prior period item “Other Expenses” by mistake.

Hence, the same shall be transferred to concerned heads shown below duly passing

the Journal entries.

Name of the Receipt Transfer from Transfer to Amount RemarksPrior period item

“Other Expenses”280-80-00 210-10 1,37,852.00 Stipend to AE

210-10 86,513.00Stipend to

TPBO

210-10 3,960.00Park Watcher

Salary210-10 82,773.00 School

Sweeper

Wages

350-20-25 71,078.00Default

payment to ITDept.,

340-20 2,500.00Refund of Ele.

Deposits

220-10 1,600.00School

Building Rent--- 900.00 Misc.

Grand Total 3,87,196.00

18) Demand Registers for Property Tax, Vacant Land Tax & Water Tax not written up and produced to Audit- Irregular.

Audit reveals that the demand registers of Property Tax, VLT & Water Tax arenot written up and produced to audit for the year 2015-16. The authorities stated thateverything is available in online. Hence, they are not preparing the demand registersmanually. But, the CDMA, AP has issued instructions for continuation of maintenance ofmanual records even though the demand, collections are made available on online. Theauthorities are not adhered the instructions of the CDMA.

E.Suvidha is closed during the year 2015-2016 and ERP module is now runningfor collection of taxes. But, the data available in E.Suvidha are not transferred to ERPmodule. The authorities are also not taken the data from E.Suvidha before closing themodule. Now, the authorities are not certifying the exact demand of Property Tax, VLT,Water Tax. Simply, they are stated that data is not available in ERP.

The Bills issue register is also not maintained. Hence, it is not possible to verifythe exact demand in respect of Property tax, VLT & Water Tax.

The Audit is now confines only to the collection of taxes. The data for demand inrespect of PT, VLT & Water Tad etc., are not available in office for verification.

Further, the collections towards PT, VLT & Water Tax are not split up to arrear ¤t. Up to the previous year the authorities are noted the arrear collection figures in aregister. During the year the same system is dis-continued. They have stated that the wardwise collection particulars for the year 2015-2016 on available in on line.

The present position of the revenue sections is that they are collecting the taxeswithout knowing the manual demand for both current & arrear. They are totally depending onon line. This is irregular. Hence, the authorities are hereby suggested and maintain themanual registers also even the transactions are made in on line.

Code.No 11

19 ) ARREAR COLLECTIONS DURING THE YEAR IN RESPECT OF TAXES/FEES &RENTS – ADR’S NOT PREPARED – COLLECTIONS NOT POSTED – BALANCES NOT

ARRIVED - AUDIT NOT DONE IN RESPECT OF ARREAR DEMAND, COLLECTION &BALANCES

During the year the following arrear collections in respect of the followingtaxes/fees & rents. Sl.No

Account Code

Head of AccountArrear Collections

REMARKS

1 110-01-01 Property TaxData not

available inthe

Municipality

For these heads ADR’s not prepared. Due to this reason the Arrear Demand, Collection & Balances are not verified & certified in audit.

2 110-01-02 Vacant Land Tax3 110-02-02 Direct Water Tax5 140-11-01 D &O Trades6 140-11-06 Encroachment Fee7 130-10-01 Market 0.00 For these heads ADR prepared.

Due to this reason the Arrear Demand, Collection & Balances are verified & certified in audit.

8 110-11-50 Advt. Tax 48,611.009 130-10-07 Shop Rents 7,30,233.00

Grand Total 7,78,844.00

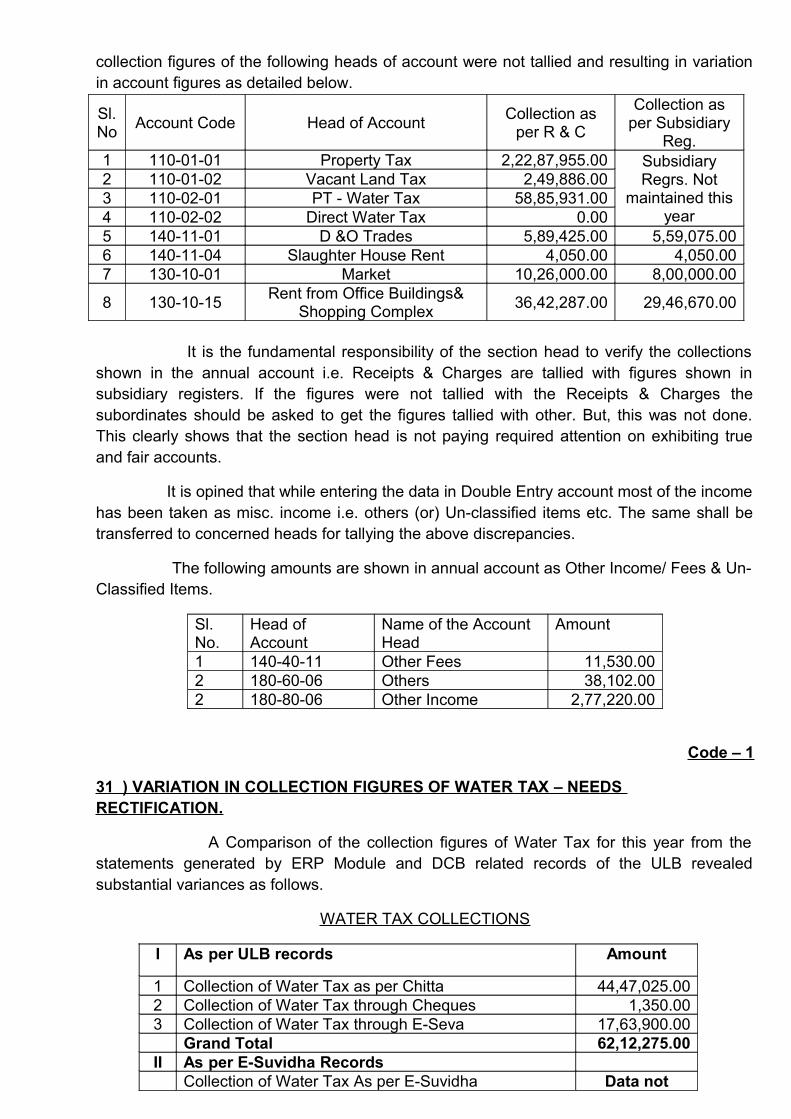

It is the fundamental responsibility of the section head to verify the collections shown in the annual account i.e. Receipts & Charges are tallied with figures shown in subsidiary registers.

If the figures were not tallied with the Receipts & Charges the subordinates shouldbe asked to get the figures tallied with other. But, this was not done. This clearly shows thatthe section heads are not paying required attention on exhibiting true and fair accounts.Necessary steps may take to follow these instructions as per AP Municipal Accounts Manualby all the section heads.

a)Recording of tax collections: Based on summary of daily collection received fromthe various collecting centres, the Revenue Officer shall prepare Form GEN-12 andsent to the accounts department for passing necessary entries:

b)The summary of daily collection i.e., Form Gen-12 does not provide the details inrespect of the year wise head wise collections made in respect of property and othertaxes. Hence, the total amount collected should be segregated into year wise, headwise collection on a monthly basis and prepare the Form P & OT - 3.

c)Recording of break-up of collections: After preparation of summary statement ofyear wise/head wise Collection of Property & other taxes i.e., Form P & OT – 3, thesame shall be sent to the Accounts Department to record the details of collection.Interest on delayed payment may be charged to the taxpayer in accordance withrelevant provisions. Interest shall be recognized as income only on collection.

d)To record the break-up of collections into year wise recovery, tax received inadvance and to record the interest income the accounts department shall pass thefollowing entry.

Code.No 9 20 ) Huge Arrears of Taxes/Fees/Rents etc,., pending receipt as per annual account -Provisions for doubtful recoveries not made as per AP Municipal Accounts Manualnorms – All the balances are shown as receivables - Irregular. As per para No. 5.27 of AP Municipal Accounts Manual every municipality makenecessary provisions in annual account in respect of property tax demand outstandingbeyond 2 years on the following norms:

i) Outstanding for more than 2 years, but not exceeding 3 years : 25%ii) Outstanding for more than 3 years, but not exceeding 4 years : 50%iii) Outstanding for more than 4 years, but, not exceeding 5 years: 75%iv) Outstanding for more than 5 years : 100%

As per para No. 5.34 & 5.81 of AP Municipal Accounts Manual every

municipality make necessary provisions in annual account in respect of Water tax & RentalIncome demand outstanding beyond 2 years on the following norms:

i) Outstanding for more than 2 years, but not exceeding 3 years : 50%ii) Outstanding for more than 3 years : 100%

The arrears pending collection on 31.03.2016 are as follows.

Sl.No

AccountCode

Head of Account Arrears DUE REMARKS

1 431-10-01Property Tax Receivables

88,19,000.00Year wise split up not available in MC. ADR’s not prepared & available in Revenue section.

2 431-10-02Vacant Land Tax Receivables

33,14,000.00

Year wise split up not available in MC. Only arrear collections were entered in a register for knowing the collection of arrears. Arrear Demand details are also not available.

3 431-19-03Other Taxes Receivables

1,21,000.00Year wise split up not available in MC. Arrear Demand details are also not available.

5 431-30-01Water Supply Receivables

63,45,000.00Year wise split up not available in MC. Arrear Demand details are also not available.

6 431-40-01 Rent Receivables 3,59,000.00

The amount relates to 7 years i.e.,from 2007-2008 to 2013-14. But, provisions not provided in annual account as per the accounts manual.

But, as seen from the Balance Sheet & Income & Expenditure Statement there is noprovisions are made against the doubt full recoveries under head of “270” in respect of Taxes& Leases. Hence, the authorities are hereby instructed to made necessary provisionsagainst doubt full recoveries.

The provision made in the form of debit at the end of the year only for accountingpurpose and it should neither be considered as reduction in demand not be treated as writtenoff.

Code.No 4

21 ) ILCS Grant received – Kept in Banks – Non-utilization of the Grant – Irregular.

Audit revels that the Samalkot Municipality had received the grant towards ILCS in the

year 2010-2011 for helping the public for constructing the toilets. The same was deposited in

SBI, Samalkot in A/c. No. 10938524662. The particulars are as follows.

Details Rs. Rs.

Grant received on 22.04.2010 20,00,000.00Grant received on 25.05.2010 34,00,000.00

Total 54,00,000.00Interest received

2010-2011 1,37,550.002011-2012 2,19,461.002012-2013 2,33,121.002013-2014 2,42,001.002014-2015 2,53,049.002015-2016 2,63,325.00

Total 13,48,507.00Balance available on 31.03.2016 67,48,507.00

As seen from the above it is known that during the 4 years a single rupee is notexpensed by the Municipality towards construction of toilets. Interest accumulated for Rs.13,48,507.00 till date.

The authorities are here by instructed to utilize the grant received towards ILCSwithout lapse the same to the GOVT. in future.

Code No.4

22 ) AMOUNTS KEPT IDLE - UNSPENT BALANCES NOT REMITTED:

The CDMA Hyderabad vide circular No Roc No PD A/c /CDMA/2012 Dt:13.10.12

issued instructions to all the Municipal Commissioners in the state to close all the non-

operative accounts and FDRs which were opened without any orders of the higher

authorities and transfer the available balances to the PD A/c No “001”and after transferring

those amounts separate cash book and other necessary record shall be maintained for

reconciliation and issue of UCs. The ULBs shall maintain a Master Cash Book for the Head

wise and scheme wise transactions etc., and before the transfer and closing of accounts, it

shall be informed to the Municipal Council for recording in the Minutes.

During the course of audit, it was observed that this Municpality has opened following

saving bank accounts without any permission from the competent authority for depositing of

funds received for implementation of the schemes sanctioned by the GOI and GOAP. The

said scheme funds were kept idle with banks. No transactions were done during the year

under audit. The Executive Authority would need to take immediate action to remit the

unspent balance amounts which were kept idle with the banks, to the heads concerned and

the result may be intimated to audit.

Sl.No

Name of the Scheme Name of theBank

A/c.No.

Amount in Rskept idle.

1Slum Devlopment

AB,Peddapuram

23798 1,764.00

2Parks & Paly Grounds

AB,Peddapuram

779 3,594.00

3BRS A/c

AB,Peddapuram

22647 94,067.00

4NFBS

AB,Peddapuram

229 7,015.00

5 Cyclone Grant AB, Samalkot 16830 737.006 CENSUS AB, Samalkot 18893 1,17,838.007 Maint. Of internal roads BOI, Samalkot 5109 18,973.008 School Fecilities SBI, Samalkot 99253 9,146.009 SJSRY SBI, Samalkot 21468 10,146.0010 Community Toilets SBI, Samalkot 25917 5,007.0011 Pension Grant SBI, Samalkot 31571 1,66,082.0012

12th FinanceAB,

Peddapuram760 5,450.00

13 SJSRY (CS) SBI, Samalkot 21162 6,690.0014 Pavala Vaddi SBI, Samalkot 95882 1,80,261.94

Code.No 1

23 ) VARIATION IN COLLECTION FIGURES OF PROPERTY TAX – NEEDS RECTIFICATION.

A Comparison of the collection figures of Property Tax for this year from thestatements generated by ERP Module and DCB related records of the ULB revealedsubstantial variances as follows.

PROPERTY TAX COLLECTIONS

I As per ULB records Amount(Rs.)

1 Collection of Property Tax as per Chitta (PT + LC) 92,18,998.002 Collection of Property Tax through Cheques (PT + LC) 63,91,240.003 Collection of Property Tax through E-Seva 28,14,143.004 35% share of PT from APIIC 48,68,159.00

Grand Total 2,32,92,540.00II As per E-Suvidha Records

1

Collection of Property Tax As per E-Suvidha (Including the penalty amount of Rs. -––––––––––––)both in I & II HYS)

EMASSclosed datanot saved.Details notavailable

III As per DCB furnished by the Municipal authorities 0.00IV As per the R & C in Double Entry Account 2,22,87,955.00

Hence the authorities are here by instructed to update the Property Tax collections inthe Online system in order to avoid variation in collection figures of Property Tax from theStatements generated ERP data base and DCB register of the ULB’s.

To reconcile both the systems of data i.e. manual system/ on line system ERP and take necessary steps and ensure that only single system of maintenance is primarily relied upon with other system only used to fulfil the bare and essential requirements.

Code.No 9

24) PROPERTY TAX – JOURNAL ENTRIES NOT PASSED BY THE ACCOUNTSSECTION FOR CURRENT YEAR DEMAND – NEEDS ACTION.

It is normal practice for the ULB to include the arrears of the tax dues whileissuing the fresh demand. Entries in respect of the arrears would have already beenrecorded in the earlier years. So, income should be recognized only in respect of thecurrent year property tax demand.

As per manual records of the Samalkot Municipality the demand in respect ofProperty Tax for the year 2015-16 is as follows.

Sl.No

Details AmountRs.

1 1st + 2nd Half Year Demand Not Available

As per Para No. 5.17 of AP Municipal Accounts Manual the account section maypass the journal entries for property tax receivables after receipt of the demand particularsfrom the revenue section before accounting for the collection.

But, journal entries are not passed by the account section for current year demand.

Hence, action may be taken to pass the journal entry as per Para No. 5.17 of APMunicipal Accounts Manual for raising the current demand of Property Tax.

Code.No 9 25 ) Collection of Property Tax through E-Seva Kendras – Remittance of PropertyTax to the Municipality through the AD, E-Seva, Kakinada after deducting the LibraryCess/Transaction Charges/Service Tax there on – Net amount was taken as receiptunder the head of Property Tax by the Municipal Authorities – Irregular.

Audit reveals that the collection of property tax by E-Seva Kendras in the Municipalarea is returned back to the Municipality from the AD, E-Seva, Kakinada byFortnightly/Monthly through DD’s.

While sending the Property Tax collections the AD, E-Seva, Kakinada have made thefollowing deductions.

1.LIBRARY CESS: Directly sent the same to the ZGS, Kakinada.2. Transaction Charges: Rs. 5/- per transaction at their end.3.Service Tax on Transaction Charges: Rs. 12.36% /14% / 14.5 % to Govt.,

After deducting the above amounts, the AD, E-Seva, Kakinada has sent the DD for“Net Amount” to the concerned municipality. The same was also adjusted to treasury passbook in “002” A/c towards property tax collection made by E-Seva’s on behalf of MC. TheMunicipal authorities while entering the same in their cash book the “Net Amount” sent by theAD, E-Seva, is taken. This is not correct.

For example, the total property tax collected by the E-Seva on behlalf of MC Samalkotis Rs. 23,25,393.00 and the property tax received by the Municipality after deductions duringthe year is Rs. 21,74,774.00 shown below for ready reference.

Sl. Period PT Deductions Total Net amount

No

collectedby E-Seva

deductions

received byMC

LC

TransactionCharges @Rs5/-

ST @12.36%,14%,14.5 %

11/3/15 to 31/03/15

4,22,959 21410 1995 247 23652 3.99.307.00

21/4/15 to 30/04/15

1,32,978 6245 995 123 7363 1,25,615.00

31/5/15 to 31/05/15

29,116 1461 300 37 1798 27,318.00

41/6/15 to 30/06/15

2,74,284 16560 2425 340 19325 2,54,959.00

5 1/7/15 to 31/7/15 2,81,731 15923 3915 548 20386 2,61,345.00

6 1/8/15 to 31/8/15 1,55,555 8325 1755 246 10326 1,45,229.00

71/9/15 to 30/09/15

1,37,205 6220 935 131 7286 1,29,919.00

81/10/15 to31/10/15

56,604 2858 590 83 3531 53,073.00

91/11/15 to 15/11/15

35,070 1874 320 45 2239 32,831.00

1015/11/15 to 30/11/15

96,058 5608 1370 199 7177 88,881.00

111/12/15 to 31/12/15

7,03,833 40374 6255 907 47536 6,56,297.00

TOTAL 23,25,393 15061921,74,774.0

0

The following DD is adjusted during the year 2016-2017.

11/1/16 to 31/01/16

2,34,350 0 2425 352 2777 2,31,573.00

21/2/16 to 29/02/16

2,69,595 0 1680 244 1924 2,67,671.00

31/3/16 to 31/03/16

4,07,764 0 2260 328 2588 4,05,176.00

9,11,709.00

7289 9,04,420.00

Hence, it is suggested that while making the entry towards collection of PT from E-

Seva in cash books, the entire collection made by the E-Seva shall be shown as total receipt

towards PT and the deductions done by the AD, Eseva may be shown as expenditure i.e.,

remittance of LC & Collection charges etc., through BOOK ADJUSTMENT.

Unless the following this procedure the total amount collected towards property tax by

E-Seva and how much amount remitted by the E-Seva authorities towards Library Cess and

how much amount deducted by the E-Seva authorities towards collection charges & Service

Tax there on are not reflected in the Municipal Account.

Code.No. 9

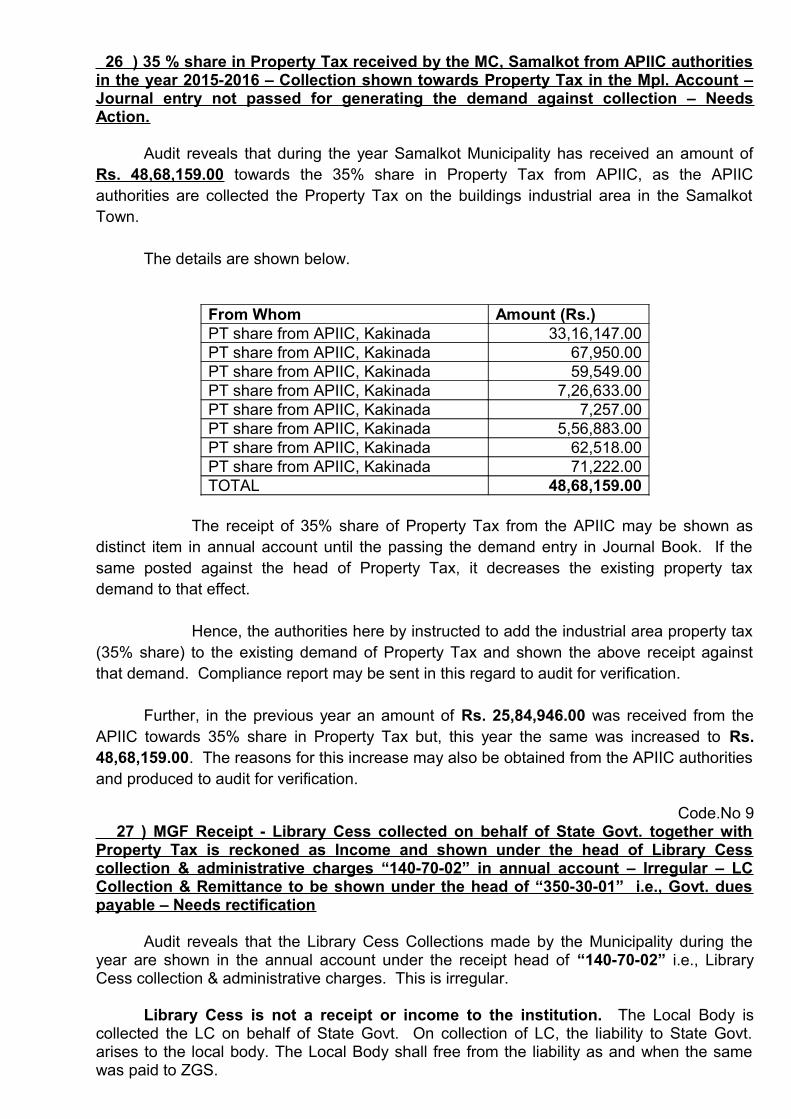

26 ) 35 % share in Property Tax received by the MC, Samalkot from APIIC authoritiesin the year 2015-2016 – Collection shown towards Property Tax in the Mpl. Account –Journal entry not passed for generating the demand against collection – NeedsAction.

Audit reveals that during the year Samalkot Municipality has received an amount ofRs. 48,68,159.00 towards the 35% share in Property Tax from APIIC, as the APIICauthorities are collected the Property Tax on the buildings industrial area in the SamalkotTown.

The details are shown below.

From Whom Amount (Rs.)PT share from APIIC, Kakinada 33,16,147.00PT share from APIIC, Kakinada 67,950.00PT share from APIIC, Kakinada 59,549.00PT share from APIIC, Kakinada 7,26,633.00PT share from APIIC, Kakinada 7,257.00PT share from APIIC, Kakinada 5,56,883.00PT share from APIIC, Kakinada 62,518.00PT share from APIIC, Kakinada 71,222.00TOTAL 48,68,159.00

The receipt of 35% share of Property Tax from the APIIC may be shown asdistinct item in annual account until the passing the demand entry in Journal Book. If thesame posted against the head of Property Tax, it decreases the existing property taxdemand to that effect.

Hence, the authorities here by instructed to add the industrial area property tax(35% share) to the existing demand of Property Tax and shown the above receipt againstthat demand. Compliance report may be sent in this regard to audit for verification.

Further, in the previous year an amount of Rs. 25,84,946.00 was received from theAPIIC towards 35% share in Property Tax but, this year the same was increased to Rs.48,68,159.00. The reasons for this increase may also be obtained from the APIIC authoritiesand produced to audit for verification.

Code.No 9 27 ) MGF Receipt - Library Cess collected on behalf of State Govt. together withProperty Tax is reckoned as Income and shown under the head of Library Cesscollection & administrative charges “140-70-02” in annual account – Irregular – LCCollection & Remittance to be shown under the head of “350-30-01” i.e., Govt. duespayable – Needs rectification

Audit reveals that the Library Cess Collections made by the Municipality during theyear are shown in the annual account under the receipt head of “140-70-02” i.e., LibraryCess collection & administrative charges. This is irregular.

Library Cess is not a receipt or income to the institution. The Local Body iscollected the LC on behalf of State Govt. On collection of LC, the liability to State Govt.arises to the local body. The Local Body shall free from the liability as and when the samewas paid to ZGS.

As per the instructions of the AP Municipal Accounts Manual under the head of TaxRevenue i.e., in respect of Property Tax at Para 5.14 it was stated that the collections to bemade on behalf of State Govt., i.e., Library Cess and included in the property tax demandshall be reckoned together with Property tax demand and credited to Control Account called“State Govt. Levies in Taxes – Control A/c under the head of “431-91-00”.

The liability on behalf of the State Govt. shall be recognized on collection based onthe receipt of summary statement of the year under Property Tax. After recognition theliability for recording the same, the Accounts Department shall transfer the amount from thehead of A/c “431-91-00” to “350-30-01” through the Journal entries.

On receipt of the payment order the remittance on behalf of the State Govt. should berecorded duly debiting the head of “350-30-01”. But, the procedure is not done by theAccountant.

As per the ULB records the details of collection of LC & remittance of LC during theyear in the MC are as follows.