Embed Size (px)

Citation preview

October 31, 2017

IPO Review

ICICI Securities Ltd | Retail Equity Research

New India Assurance (NIA) is the largest general insurance company in

India in terms of net worth, domestic GDPI, PAT and branch count as on

FY17. As of FY17, it had issued 27.1 million policies across all product

segments. This is the highest among all general insurance companies in

India. NIA offers a comprehensive and well-diversified range of products,

including motor, health, crop/weather, fire, personal accident, marine,

engineering insurance, through multiple distribution channels.

As of June 30, 2017, NIA had 68,389 agents, 16 corporate agents, 25

bancassurance partners and 2452 offices in India. It also has a presence

across 28 other countries through a number of international branches,

agency offices and subsidiaries. Net worth (excluding fair value change

account) increased from | 9605 crore in FY13 to | 12596 crore in FY17.

The company commands robust financial position with solvency ratio as

of 2.27x (June 2017) compared to IRDAI requirement of 1.50x.

Key business aspects

Market leadership and established brand

NIA has been operating for almost a century since incorporation in 1919

and has been the largest Indian general insurance company in terms of

domestic GDPI as of FY17. Despite significant competition, NIA

maintained a leadership position with 15% market share of GDPI (FY17).

Given established brand, business reputation, large & diversified product

portfolio and multi-channel distribution network, NIA is well positioned to

capitalise on growth potential in Indian general insurance industry.

Longstanding global footprint, successful international operations

NIA has a presence in 28 international jurisdictions including the UK,

Japan and Australia. In addition, the company’s global operations are

spread across Asia Pacific, Middle East, Africa and the Caribbean. In FY17,

gross written premium (GWP) from international operations was at

| 3164.0 crore contributing ~14.2% of total GWP. NIA intends to further

expand its international presence through new regions based on existing

market knowledge, underwriting expertise and risk management.

Multi-channel distribution network but combined ratio remains high

NIA has expansive multi-channel distribution network including 68,389

individual agents, 16 corporate agents, 25 bancassurance partners and

2452 offices in India. In FY17, agent (individual and corporate agents),

brokers, and bancassurance partners contributed 42.01%, 25.75%, and

1.15%, respectively, of GDPI in India. Company reported weak combined

ratio of 119.7% in FY17 and has remained consistently above 115%.

Concerns

Catastrophic events could have material adverse effect on operations

Inability to bring down high combined ratios in future

Significant business is generated from relatively few regions

Regulation of motor insurance; changes in demand for motor vehicles

Additional risks associated with international operations

Priced at 64x P/E & 4.3x P/B (post issue FY17 PAT, NW) on higher band

At the IPO upper price band of | 800, the stock is available at a P/B

multiple of 4.3x FY17 (post issue) networth excluding fair value change.

Post issue market capitalisation is at ~| 64000 crore at the upper band.

Being slightly expensive with high combined ratios, we believe one

should subscribe only from a longer term view and not for the purpose of

accruing listing gains.

The New India Assurance Co Ltd

Price band | 770-800

Rating matrix

Rating: Subscribe only for long term

Issue Details*

Issue Opens 1-Nov-17

Issue Closes 3-Nov-16

Issue Size (| Crore) 9107-9467

Price Band (|) 770-800

No of Shares on Offer (crore) 12.0

QIB (%) 50

Non-Institutional (%) 15

Retail (%) 35

Minimum lot size (No. of shares) 18

*Retail & Employee discount: | 30/-per share

Objects of the Issue

The object of the issue is to utilize the net proceeds from fresh issue

of 2.4 crore shares towards meeting future capital requirements. And

further, to achieve benefits of listing equity shares on stock

exchanges and sell up to 9.6 crore equity shares by the selling

shareholders.

1997-98 2001-04 2006

HUL acquires 23% stake. Mitsubishi Corporation and

Shareholding Pattern Pre-Issue Post-Issue

Promoter & promoter group 100.0% 85.4%

Public 0.0% 14.6%

Financial Summary

| Crore FY14 FY15 FY16 FY17

Premiums earned - Net 10994 13354 15215 17675

Income from Investments 1286 1488 1527 1656

Claims Incurred (net) 9462 11262 13234 16300

PAT 805 1377 930 840

Valuation Summary (at | 800; upper price band)

(x) FY14 FY15 FY16 Pre Post

P/E 19.3 11.3 16.6 76.2 78.5

P/BV 1.5 1.4 1.3 5.0 4.3

FY17*

Research Analyst

Kajal Gandhi

Vasant Lohiya

Vishal Narnolia

*Factoring bonus shares issued in August 2017 and fresh issue

Page 2 ICICI Securities Ltd | Retail Equity Research

Company Background

New India Assurance (NIA) is the largest general insurance company in

India in terms of net worth, domestic gross direct premium, PAT and

number of branches as on FY17. The company has been in operation for

almost a century.

The issue involves 12 crore share on offer totalling |9600 crore. Around

2.4 crore shares are fresh issue raising |1920 crore and balance funds will

flow to the government.

As of FY17, it had issued 27.1 million policies across all product segments

which is the highest among all general insurance companies in India.

NIA’s insurance products can be broadly categorized into the following

product verticals: fire insurance; marine insurance, motor insurance, crop

insurance, health insurance and other insurance products. Between FY13

and FY17, despite increasing competition from private players, NIA has

maintained market leadership in the general insurance industry in India

and were leaders in all segments except crop insurance (source: Crisil

report). In FY17, the gross direct premium from fire, engineering, aviation,

liability, marine, motor and health insurance represented a market share

of 19.1%, 21.9%, 29.6%, 18.2%, 21.0%, 15.1% and 18.4%, respectively,

of total gross direct premium in these segments in India.

Exhibit 1: Product-wise breakup of NIA

(| crore)

Product Segment GWP % of total GWP % of total GWP % of total

Fire Insurance 3302.4 19% 3463.7 18% 3563 15%

Marine Insurance 877.2 5% 742.9 4% 714 3%

Motor Insurance 6555.7 39% 7652.5 40% 9016 39%

Crop Insurance 66.7 0% 52.3 0% 1250 5%

Health Insurance 4017.7 24% 4961.3 26% 6085 26%

Other Insurance 2166.9 13% 2354.4 12% 2602 11%

Total 16986.6 100% 19227.0 100% 23230 100%

FY15 FY16 FY17

Source: RHP, ICICIdirect.com Research

The company has developed an expansive multi-channel distribution

network that includes individual and corporate agents, brokers,

bancassurance partners and other intermediaries, as well as direct sales

and sales through online channels. As of Q1FY18, its distribution network

in India included 68,389 individual agents and 16 corporate agents,

bancassurance arrangements with 25 banks in India, and a large number

of OEM and automotive dealer arrangements through its agent and

broker network.

Further, the company has developed a pan-India branch network. As of

Q1FY18, it had 2452 offices in India across 29 states, seven union

territories and across 28 other countries globally through a number of

international branches, agency offices and subsidiaries. It also partners

with the GoI and state governments for implementation of various

government schemes including health insurance and policies for

underprivileged customer segments.

In FY15, FY16 and FY17, NIA’s gross written premium was | 16987 crore,

| 19227 crore and | 23230 crore, respectively. Gross written premium has

increased at a CAGR of 15.2% from | 13200 crore in FY13 to | 23230

crore in FY17. In FY16 and FY17, the company paid dividends (including

dividend distribution tax) of | 360 crore and | 302 crore, respectively,

while for FY17 it has declared dividend payments (including dividend

distribution tax) of | 373 crore.

Page 3 ICICI Securities Ltd | Retail Equity Research

The key highlight is that the company has funded its operations for more

than 40 years without any external capital infusion. The net worth

(excluding fair value change account) increased from | 9605 crore as of

FY13 to | 12596 crore as of FY17. The total net worth (including fair value

change account) increased from | 25470 crore as of FY13 to | 36298 crore

as of FY17. The company commands a robust financial position with a

solvency ratio as of FY17 of 2.22x, vs. the IRDAI requirement of 1.50x.

NIA has been rated A-(Excellent) by AM Best Company since 2007 and

has been rated AAA/Stable by Crisil since 2014.

Details of product portfolio

Fire insurance: The fire insurance portfolio includes fire and special perils

insurance, business interruption insurance, and large risk package

insurance policies.

Marine Insurance: The marine insurance business includes marine cargo

insurance, hull and machinery insurance and offshore oil and energy

insurance products.

Motor Insurance: The motor insurance portfolio includes liability only

(third party) policies and comprehensive motor (third party and own

damage) policies.

Crop Insurance: The crop insurance products include Pradhan Mantri

Fasal Bima Yojana farmers package insurance, weather based crop

insurance, unified package insurance schemes and horticulture/

plantation insurance.

Health Insurance: Health insurance products include individual health

products such as mediclaim, floater and premier mediclaim products;

corporate (group) health insurance products; and personal accident

products and schemes implemented for the GoI such as the Rashtriya

Swasthya Bima Yojana, PMSBY and PMJDY.

Other Insurance: The company has a broad range of general insurance

products under this category, including the following: liability insurance;

engineering insurance; aviation insurance; nuclear insurance; fidelity

guarantee and burglary insurance; householder insurance; insurance

specific commercial insurance such as banker‘s indemnity and

shopkeepers insurance; money insurance; travel insurance; and social

insurance products.

Page 4 ICICI Securities Ltd | Retail Equity Research

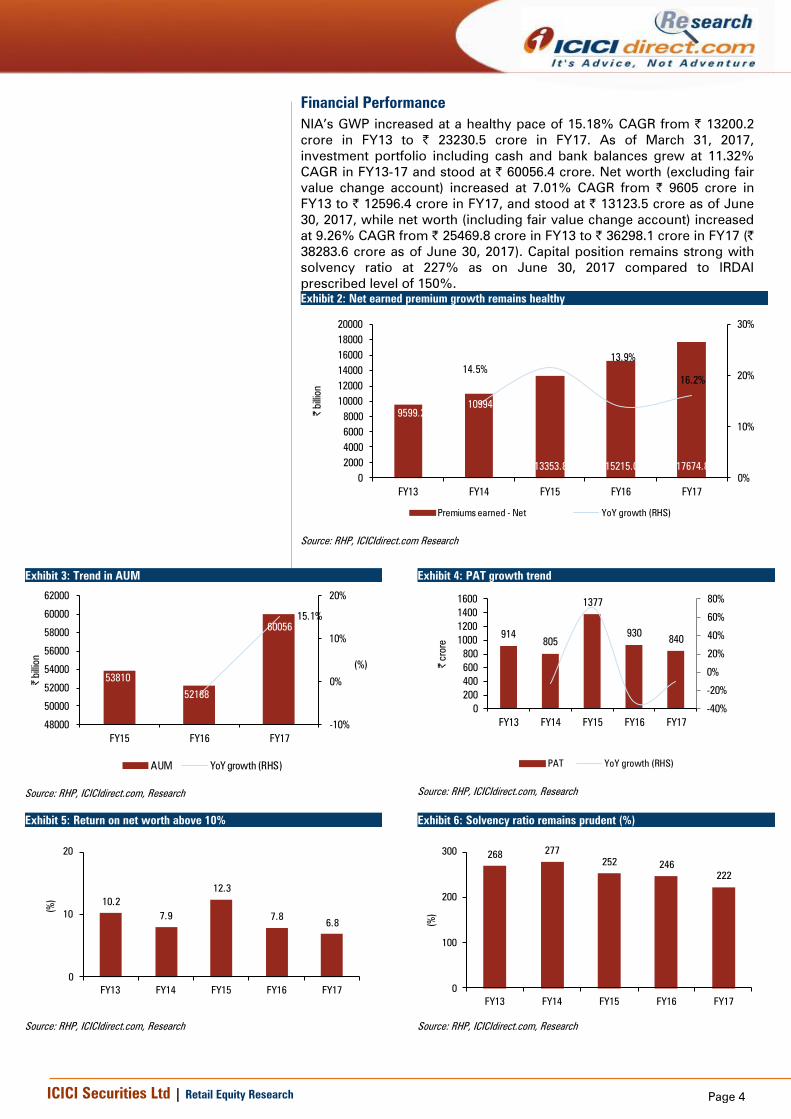

Financial Performance

NIA’s GWP increased at a healthy pace of 15.18% CAGR from | 13200.2

crore in FY13 to | 23230.5 crore in FY17. As of March 31, 2017,

investment portfolio including cash and bank balances grew at 11.32%

CAGR in FY13-17 and stood at | 60056.4 crore. Net worth (excluding fair

value change account) increased at 7.01% CAGR from | 9605 crore in

FY13 to | 12596.4 crore in FY17, and stood at | 13123.5 crore as of June

30, 2017, while net worth (including fair value change account) increased

at 9.26% CAGR from | 25469.8 crore in FY13 to | 36298.1 crore in FY17 (|

38283.6 crore as of June 30, 2017). Capital position remains strong with

solvency ratio at 227% as on June 30, 2017 compared to IRDAI

prescribed level of 150%.

Exhibit 2: Net earned premium growth remains healthy

9599.2

10994.1

13353.8 15215.0 17674.8

14.5%

21.5%

13.9%

16.2%

0%

10%

20%

30%

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

FY13 FY14 FY15 FY16 FY17

| b

illion

Premiums earned - Net YoY growth (RHS)

Source: RHP, ICICIdirect.com Research

Exhibit 3: Trend in AUM

53810

52188

60056

-3.0%

15.1%

-10%

0%

10%

20%

48000

50000

52000

54000

56000

58000

60000

62000

FY15 FY16 FY17

(%)

| b

illion

AUM YoY growth (RHS)

Source: RHP, ICICIdirect.com, Research

Exhibit 4: PAT growth trend

914

805

1377

930840

-40%

-20%

0%

20%

40%

60%

80%

0

200

400

600

800

1000

1200

1400

1600

FY13 FY14 FY15 FY16 FY17

| c

rore

PAT YoY growth (RHS)

Source: RHP, ICICIdirect.com, Research

Exhibit 5: Return on net worth above 10%

10.2

7.9

12.3

7.86.8

0

10

20

FY13 FY14 FY15 FY16 FY17

(%

)

Source: RHP, ICICIdirect.com, Research

Exhibit 6: Solvency ratio remains prudent (%)

268277

252246

222

0

100

200

300

FY13 FY14 FY15 FY16 FY17

(%

)

Source: RHP, ICICIdirect.com, Research

Page 5 ICICI Securities Ltd | Retail Equity Research

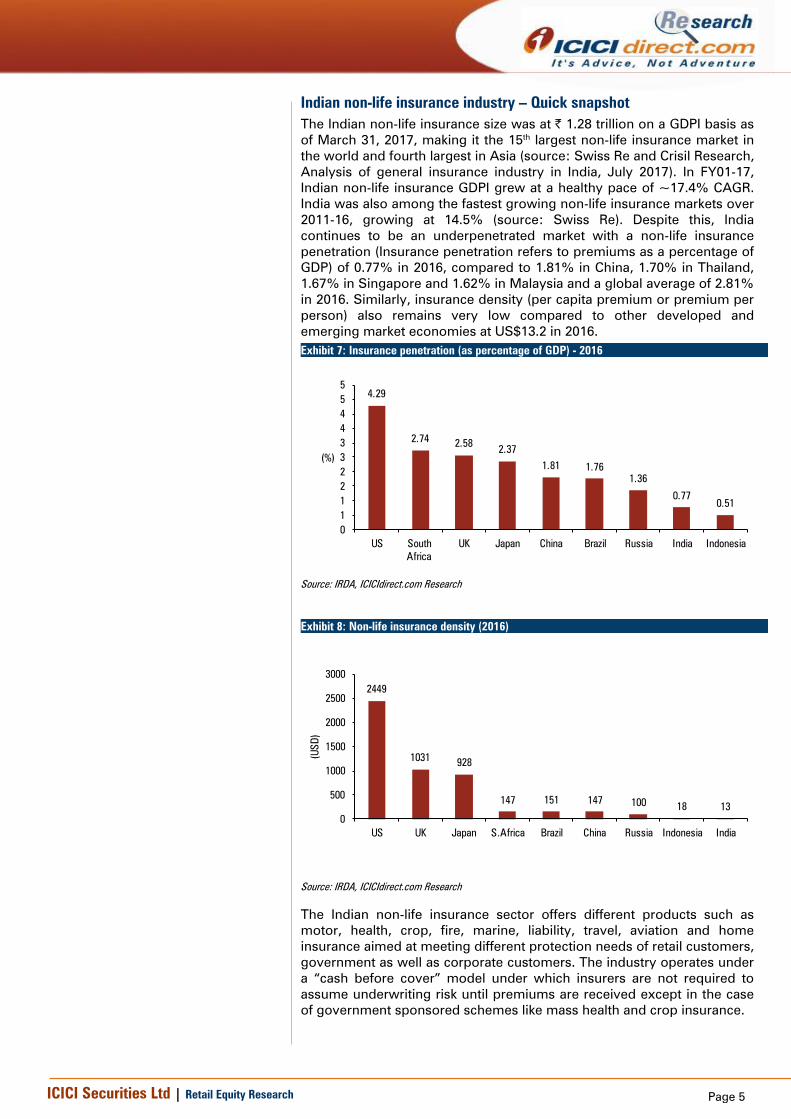

Indian non-life insurance industry – Quick snapshot

The Indian non-life insurance size was at | 1.28 trillion on a GDPI basis as

of March 31, 2017, making it the 15th largest non-life insurance market in

the world and fourth largest in Asia (source: Swiss Re and Crisil Research,

Analysis of general insurance industry in India, July 2017). In FY01-17,

Indian non-life insurance GDPI grew at a healthy pace of ~17.4% CAGR.

India was also among the fastest growing non-life insurance markets over

2011-16, growing at 14.5% (source: Swiss Re). Despite this, India

continues to be an underpenetrated market with a non-life insurance

penetration (Insurance penetration refers to premiums as a percentage of

GDP) of 0.77% in 2016, compared to 1.81% in China, 1.70% in Thailand,

1.67% in Singapore and 1.62% in Malaysia and a global average of 2.81%

in 2016. Similarly, insurance density (per capita premium or premium per

person) also remains very low compared to other developed and

emerging market economies at US$13.2 in 2016.

Exhibit 7: Insurance penetration (as percentage of GDP) - 2016

4.29

2.742.58

2.37

1.81 1.76

1.36

0.77

0.51

0

1

1

2

2

3

3

4

4

5

5

US South

Africa

UK Japan China Brazil Russia India Indonesia

(%)

Source: IRDA, ICICIdirect.com Research

Exhibit 8: Non-life insurance density (2016)

2449

1031928

147 151 147 10018 13

0

500

1000

1500

2000

2500

3000

US UK Japan S.Africa Brazil China Russia Indonesia India

(U

SD

)

Source: IRDA, ICICIdirect.com Research

The Indian non-life insurance sector offers different products such as

motor, health, crop, fire, marine, liability, travel, aviation and home

insurance aimed at meeting different protection needs of retail customers,

government as well as corporate customers. The industry operates under

a “cash before cover” model under which insurers are not required to

assume underwriting risk until premiums are received except in the case

of government sponsored schemes like mass health and crop insurance.

Page 6 ICICI Securities Ltd | Retail Equity Research

The Indian non-life insurance sector has significant growth potential

because of its under-penetration and low insurance density compared to

other economies. According to Crisil Research, GDPI for non-life insurers

are projected to grow at 15-20% CAGR in FY17-22. India’s large working

population, rising affluence, rapid urbanisation and rising awareness of

risk with higher disposable incomes is expected to continue to propel the

growth of the non-life insurance industry in India. In addition, improving

economic growth, emergence of new risks such as cyber frauds and a

strong regulatory focus on improving insurance coverage are expected to

be the key catalysts among others for this growth.

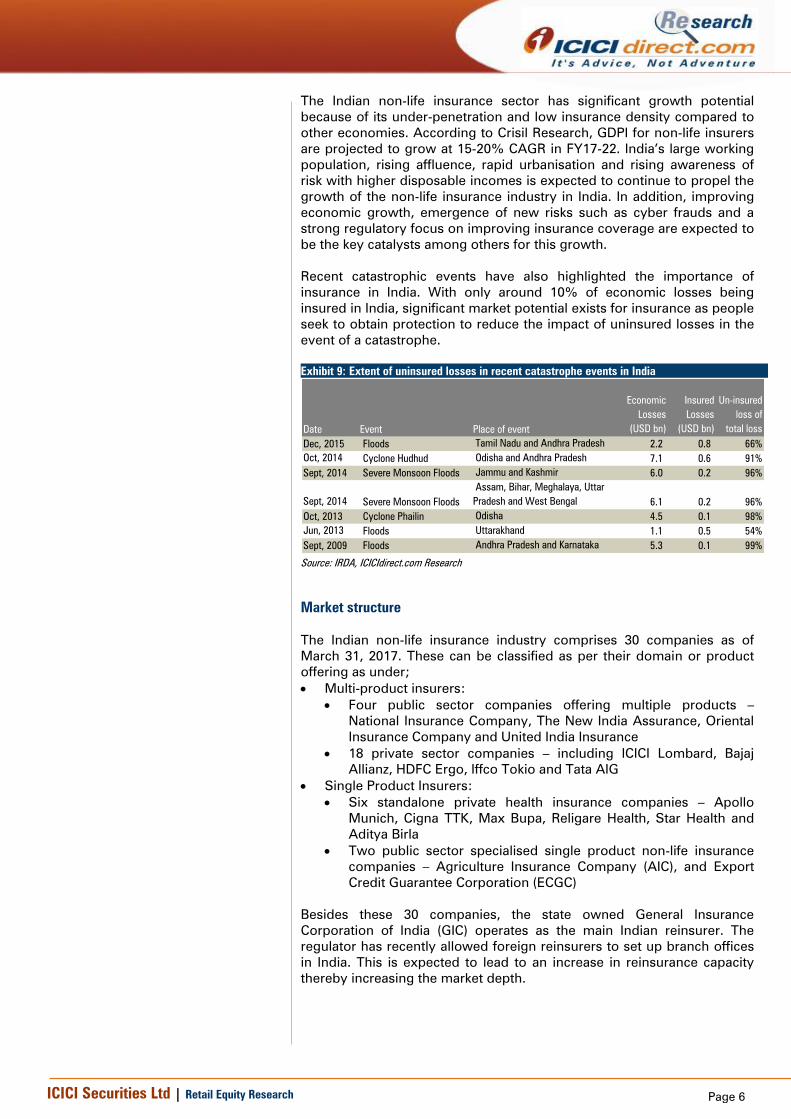

Recent catastrophic events have also highlighted the importance of

insurance in India. With only around 10% of economic losses being

insured in India, significant market potential exists for insurance as people

seek to obtain protection to reduce the impact of uninsured losses in the

event of a catastrophe.

Exhibit 9: Extent of uninsured losses in recent catastrophe events in India

Date Event Place of event

Economic

Losses

(USD bn)

Insured

Losses

(USD bn)

Un-insured

loss of

total loss

Dec, 2015 Floods Tamil Nadu and Andhra Pradesh 2.2 0.8 66%

Oct, 2014 Cyclone Hudhud Odisha and Andhra Pradesh 7.1 0.6 91%

Sept, 2014 Severe Monsoon Floods Jammu and Kashmir 6.0 0.2 96%

Sept, 2014 Severe Monsoon Floods

Assam, Bihar, Meghalaya, Uttar

Pradesh and West Bengal 6.1 0.2 96%

Oct, 2013 Cyclone Phailin Odisha 4.5 0.1 98%

Jun, 2013 Floods Uttarakhand 1.1 0.5 54%

Sept, 2009 Floods Andhra Pradesh and Karnataka 5.3 0.1 99%

Source: IRDA, ICICIdirect.com Research

Market structure

The Indian non-life insurance industry comprises 30 companies as of

March 31, 2017. These can be classified as per their domain or product

offering as under;

Multi-product insurers:

Four public sector companies offering multiple products –

National Insurance Company, The New India Assurance, Oriental

Insurance Company and United India Insurance

18 private sector companies – including ICICI Lombard, Bajaj

Allianz, HDFC Ergo, Iffco Tokio and Tata AIG

Single Product Insurers:

Six standalone private health insurance companies – Apollo

Munich, Cigna TTK, Max Bupa, Religare Health, Star Health and

Aditya Birla

Two public sector specialised single product non-life insurance

companies – Agriculture Insurance Company (AIC), and Export

Credit Guarantee Corporation (ECGC)

Besides these 30 companies, the state owned General Insurance

Corporation of India (GIC) operates as the main Indian reinsurer. The

regulator has recently allowed foreign reinsurers to set up branch offices

in India. This is expected to lead to an increase in reinsurance capacity

thereby increasing the market depth.

Page 7 ICICI Securities Ltd | Retail Equity Research

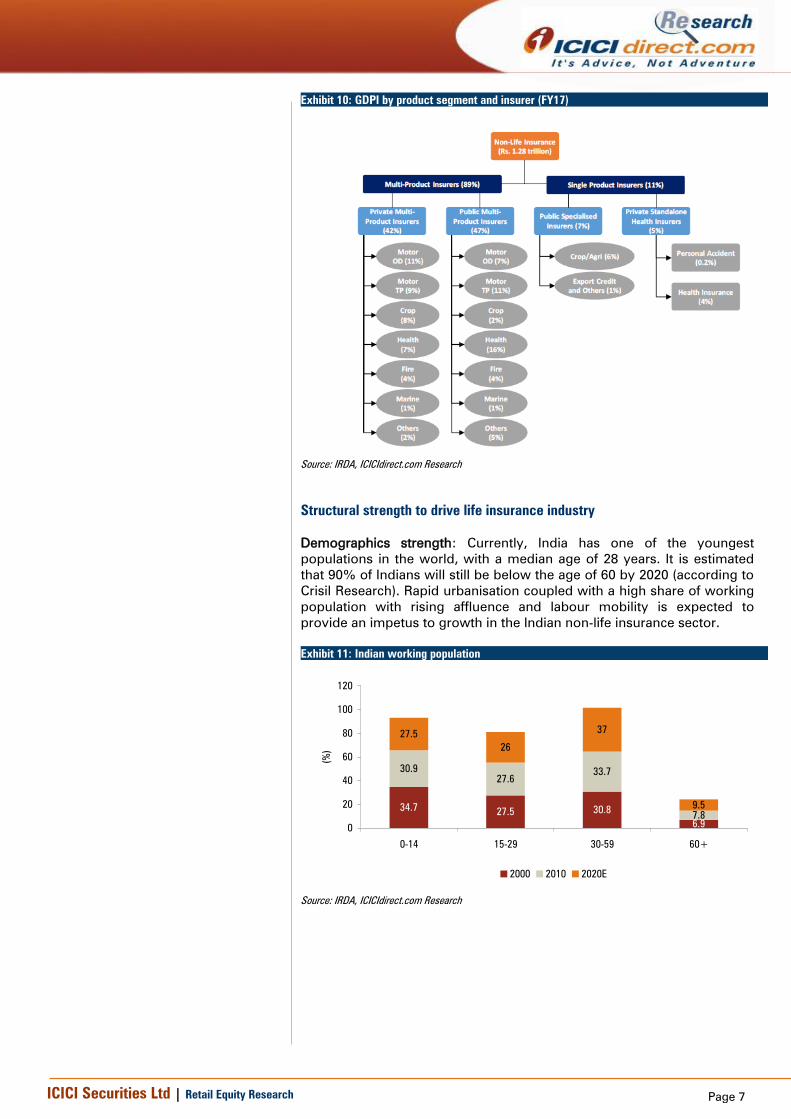

Exhibit 10: GDPI by product segment and insurer (FY17)

Source: IRDA, ICICIdirect.com Research

Structural strength to drive life insurance industry

Demographics strength: Currently, India has one of the youngest

populations in the world, with a median age of 28 years. It is estimated

that 90% of Indians will still be below the age of 60 by 2020 (according to

Crisil Research). Rapid urbanisation coupled with a high share of working

population with rising affluence and labour mobility is expected to

provide an impetus to growth in the Indian non-life insurance sector.

Exhibit 11: Indian working population

34.727.5 30.8

6.9

30.9

27.6

33.7

7.8

27.5

26

37

9.5

0

20

40

60

80

100

120

0-14 15-29 30-59 60+

(%

)

2000 2010 2020E

Source: IRDA, ICICIdirect.com Research

Page 8 ICICI Securities Ltd | Retail Equity Research

Exhibit 12: Urban proportion of total population (2016)

94.1

8681.8

74.1

65.3

56.2 54.5

33.1

0

10

20

30

40

50

60

70

80

90

100

Japan Brazil US Russia S.Africa China Indonesia India

(U

SD

)

Source: IRDA, ICICIdirect.com Research

Recent product innovations: Non-life insurers have been continuously

innovating with new product offerings and services in response to market

needs. In FY17, 165 products were cumulatively introduced across

insurers, compared with 101 products in FY16. Products launched include

long term health insurance, long term two wheeler insurance, cyber

liability, crop insurance through PMFBY and railway accident insurance.

Add-on products such as engine protect, road assistance, zero

depreciation, return to invoice have also been introduced in recent times

to offer additional services to the customers.

Improved penetration in motor insurance to boost growth: In India, motor

insurance forms the largest pie in the Indian non-life insurance sector

contributing ~40% of industry GDPI in FY17. Among segments, own

damage motor insurance forms ~19% of industry GDPI, while third party

motor insurance forms ~21% of industry GDPI in FY17. Despite being

more advanced than other forms of non-life insurance, motor insurance in

India continues to be underpenetrated relative to global levels. As per

Crisil Research estimates, only 60% of cars, older than three years, are

insured in India against the global benchmark of 90%. In two wheelers,

only ~25% are insured in India against global benchmark of over 90%.

Exhibit 13: Projected growth rates for individual segments in motor insurance

Source: IRDA, ICICIdirect.com Research

Increased commission rates for comprehensive auto insurance policies

and third party insurance have been adopted aiming to improve renewal

rates. Improving adoption of telematics is expected to improve own

damage motor insurance performance. Passage of Motor Vehicles

(Amendment) Bill 2016, a legislation that is currently being evaluated by

the Indian Parliament is expected to bring in long term changes in the

industry.

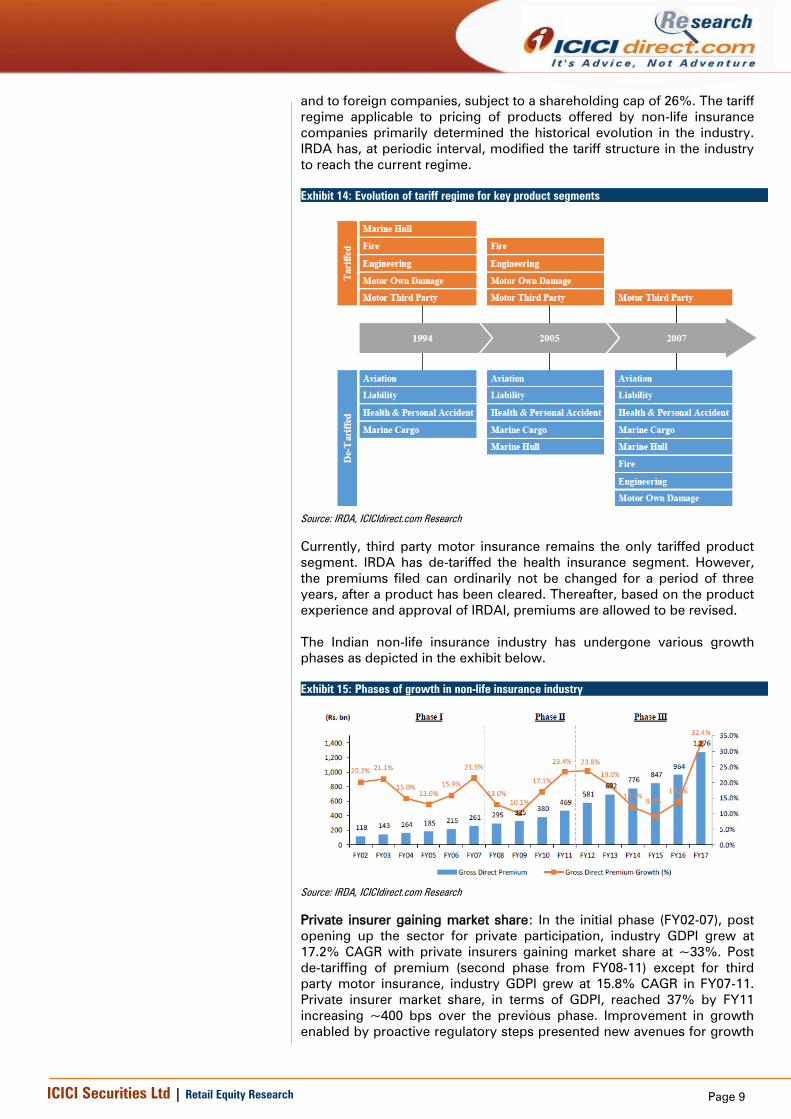

Historical evolution of Indian non-life insurance industry

The Indian non-life insurance sector has experienced three phases of

growth since FY02, when the sector was opened to private companies,

Page 9 ICICI Securities Ltd | Retail Equity Research

and to foreign companies, subject to a shareholding cap of 26%. The tariff

regime applicable to pricing of products offered by non-life insurance

companies primarily determined the historical evolution in the industry.

IRDA has, at periodic interval, modified the tariff structure in the industry

to reach the current regime.

Exhibit 14: Evolution of tariff regime for key product segments

Source: IRDA, ICICIdirect.com Research

Currently, third party motor insurance remains the only tariffed product

segment. IRDA has de-tariffed the health insurance segment. However,

the premiums filed can ordinarily not be changed for a period of three

years, after a product has been cleared. Thereafter, based on the product

experience and approval of IRDAI, premiums are allowed to be revised.

The Indian non-life insurance industry has undergone various growth

phases as depicted in the exhibit below.

Exhibit 15: Phases of growth in non-life insurance industry

Source: IRDA, ICICIdirect.com Research

Private insurer gaining market share: In the initial phase (FY02-07), post

opening up the sector for private participation, industry GDPI grew at

17.2% CAGR with private insurers gaining market share at ~33%. Post

de-tariffing of premium (second phase from FY08-11) except for third

party motor insurance, industry GDPI grew at 15.8% CAGR in FY07-11.

Private insurer market share, in terms of GDPI, reached 37% by FY11

increasing ~400 bps over the previous phase. Improvement in growth

enabled by proactive regulatory steps presented new avenues for growth

Page 10 ICICI Securities Ltd | Retail Equity Research

and eased restrictions on existing product lines. Industry GDPI grew at

18.1% CAGR in FY11-17. Since inception, the private multi-product sector

has grown significantly and currently accounts for ~42% (46.7%

including private standalone health insurers) of GDPI of non-life insurance

industry in FY17. Market share growth was driven by superior customer

service and claims settlement.

Exhibit 16: Market share of private insurer on the rise (GDPI basis)

36.1 36.7 35.6 36.1 37.3 39.3 40.0 40.3 40.0 42.1

58.4 56.9 55.7 54.8 53.9 52.1 51.3 51.7 51.0 46.8

0

20

40

60

80

100

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

(%

)

Private Multi-Product Insurers Public Multi-Product Insurers

Private Standalone Health Insurers Specialised Insurers

Source: IRDA, ICICIdirect.com Research

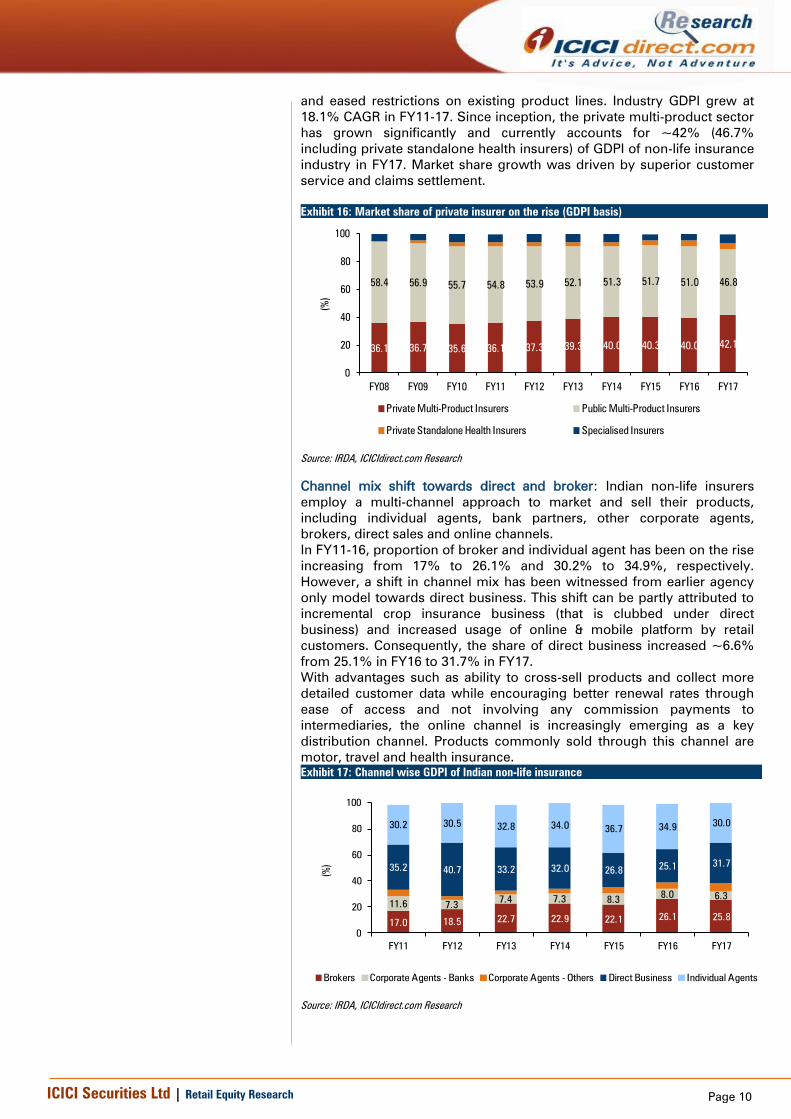

Channel mix shift towards direct and broker: Indian non-life insurers

employ a multi-channel approach to market and sell their products,

including individual agents, bank partners, other corporate agents,

brokers, direct sales and online channels.

In FY11-16, proportion of broker and individual agent has been on the rise

increasing from 17% to 26.1% and 30.2% to 34.9%, respectively.

However, a shift in channel mix has been witnessed from earlier agency

only model towards direct business. This shift can be partly attributed to

incremental crop insurance business (that is clubbed under direct

business) and increased usage of online & mobile platform by retail

customers. Consequently, the share of direct business increased ~6.6%

from 25.1% in FY16 to 31.7% in FY17.

With advantages such as ability to cross-sell products and collect more

detailed customer data while encouraging better renewal rates through

ease of access and not involving any commission payments to

intermediaries, the online channel is increasingly emerging as a key

distribution channel. Products commonly sold through this channel are

motor, travel and health insurance.

Exhibit 17: Channel wise GDPI of Indian non-life insurance

17.0 18.522.7 22.9 22.1 26.1 25.8

11.6 7.37.4 7.3 8.3

8.0 6.3

35.2 40.7 33.2 32.0 26.825.1

31.7

30.2 30.532.8 34.0

36.7 34.930.0

0

20

40

60

80

100

FY11 FY12 FY13 FY14 FY15 FY16 FY17

(%)

Brokers Corporate Agents - Banks Corporate Agents - Others Direct Business Individual Agents

Source: IRDA, ICICIdirect.com Research

Page 11 ICICI Securities Ltd | Retail Equity Research

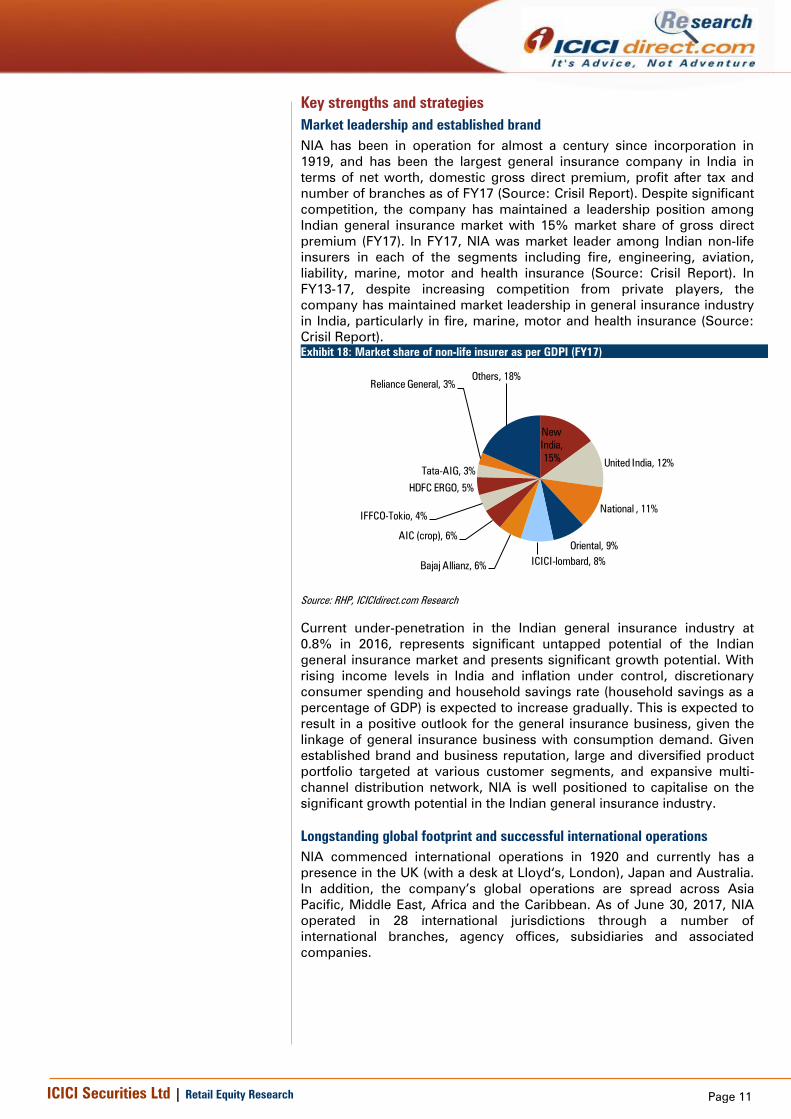

Key strengths and strategies

Market leadership and established brand

NIA has been in operation for almost a century since incorporation in

1919, and has been the largest general insurance company in India in

terms of net worth, domestic gross direct premium, profit after tax and

number of branches as of FY17 (Source: Crisil Report). Despite significant

competition, the company has maintained a leadership position among

Indian general insurance market with 15% market share of gross direct

premium (FY17). In FY17, NIA was market leader among Indian non-life

insurers in each of the segments including fire, engineering, aviation,

liability, marine, motor and health insurance (Source: Crisil Report). In

FY13-17, despite increasing competition from private players, the

company has maintained market leadership in general insurance industry

in India, particularly in fire, marine, motor and health insurance (Source:

Crisil Report).

Exhibit 18: Market share of non-life insurer as per GDPI (FY17)

New

India,

15%United India, 12%

National , 11%

Oriental, 9%

ICICI-lombard, 8%Bajaj Allianz, 6%

AIC (crop), 6%

IFFCO-Tokio, 4%

HDFC ERGO, 5%

Tata-AIG, 3%

Reliance General, 3%

Others, 18%

Source: RHP, ICICIdirect.com Research

Current under-penetration in the Indian general insurance industry at

0.8% in 2016, represents significant untapped potential of the Indian

general insurance market and presents significant growth potential. With

rising income levels in India and inflation under control, discretionary

consumer spending and household savings rate (household savings as a

percentage of GDP) is expected to increase gradually. This is expected to

result in a positive outlook for the general insurance business, given the

linkage of general insurance business with consumption demand. Given

established brand and business reputation, large and diversified product

portfolio targeted at various customer segments, and expansive multi-

channel distribution network, NIA is well positioned to capitalise on the

significant growth potential in the Indian general insurance industry.

Longstanding global footprint and successful international operations

NIA commenced international operations in 1920 and currently has a

presence in the UK (with a desk at Lloyd‘s, London), Japan and Australia.

In addition, the company’s global operations are spread across Asia

Pacific, Middle East, Africa and the Caribbean. As of June 30, 2017, NIA

operated in 28 international jurisdictions through a number of

international branches, agency offices, subsidiaries and associated

companies.

Page 12 ICICI Securities Ltd | Retail Equity Research

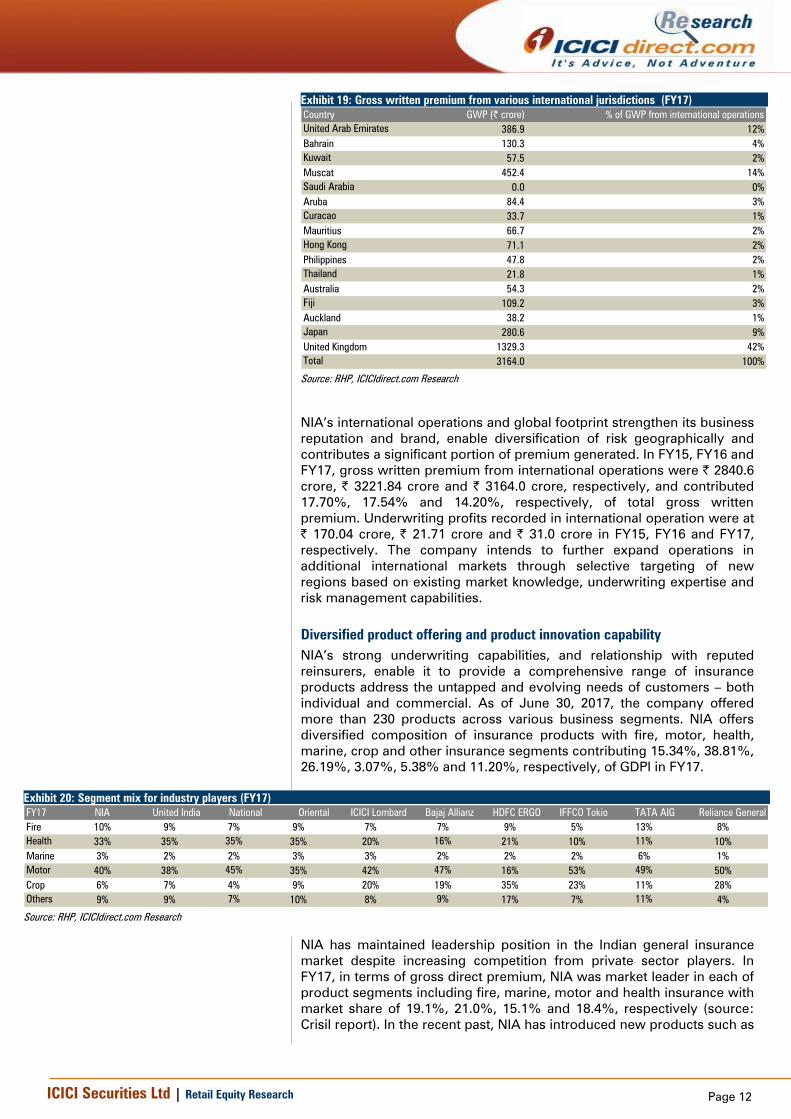

Exhibit 19: Gross written premium from various international jurisdictions (FY17)

Country GWP (| crore) % of GWP from international operations

United Arab Emirates 386.9 12%

Bahrain 130.3 4%

Kuwait 57.5 2%

Muscat 452.4 14%

Saudi Arabia 0.0 0%

Aruba 84.4 3%

Curacao 33.7 1%

Mauritius 66.7 2%

Hong Kong 71.1 2%

Philippines 47.8 2%

Thailand 21.8 1%

Australia 54.3 2%

Fiji 109.2 3%

Auckland 38.2 1%

Japan 280.6 9%

United Kingdom 1329.3 42%

Total 3164.0 100%

Source: RHP, ICICIdirect.com Research

NIA’s international operations and global footprint strengthen its business

reputation and brand, enable diversification of risk geographically and

contributes a significant portion of premium generated. In FY15, FY16 and

FY17, gross written premium from international operations were | 2840.6

crore, | 3221.84 crore and | 3164.0 crore, respectively, and contributed

17.70%, 17.54% and 14.20%, respectively, of total gross written

premium. Underwriting profits recorded in international operation were at

| 170.04 crore, | 21.71 crore and | 31.0 crore in FY15, FY16 and FY17,

respectively. The company intends to further expand operations in

additional international markets through selective targeting of new

regions based on existing market knowledge, underwriting expertise and

risk management capabilities.

Diversified product offering and product innovation capability

NIA’s strong underwriting capabilities, and relationship with reputed

reinsurers, enable it to provide a comprehensive range of insurance

products address the untapped and evolving needs of customers – both

individual and commercial. As of June 30, 2017, the company offered

more than 230 products across various business segments. NIA offers

diversified composition of insurance products with fire, motor, health,

marine, crop and other insurance segments contributing 15.34%, 38.81%,

26.19%, 3.07%, 5.38% and 11.20%, respectively, of GDPI in FY17.

Exhibit 20: Segment mix for industry players (FY17)

FY17 NIA United India National Oriental ICICI Lombard Bajaj Allianz HDFC ERGO IFFCO Tokio TATA AIG Reliance General

Fire 10% 9% 7% 9% 7% 7% 9% 5% 13% 8%

Health 33% 35% 35% 35% 20% 16% 21% 10% 11% 10%

Marine 3% 2% 2% 3% 3% 2% 2% 2% 6% 1%

Motor 40% 38% 45% 35% 42% 47% 16% 53% 49% 50%

Crop 6% 7% 4% 9% 20% 19% 35% 23% 11% 28%

Others 9% 9% 7% 10% 8% 9% 17% 7% 11% 4%

Source: RHP, ICICIdirect.com Research

NIA has maintained leadership position in the Indian general insurance

market despite increasing competition from private sector players. In

FY17, in terms of gross direct premium, NIA was market leader in each of

product segments including fire, marine, motor and health insurance with

market share of 19.1%, 21.0%, 15.1% and 18.4%, respectively (source:

Crisil report). In the recent past, NIA has introduced new products such as

Page 13 ICICI Securities Ltd | Retail Equity Research

personal accident cover for 41.2 crore individuals with RuPay cards,

nuclear operator liability insurance, cellular network policies to operators,

bonded warehouse insurance for warehouse owners and customised

insurance solutions for various large risk projects across India. Continued

focus on product innovation will enable further to appropriately respond

to market demands and maintain market leadership in a rapidly growing

and changing general insurance market in India.

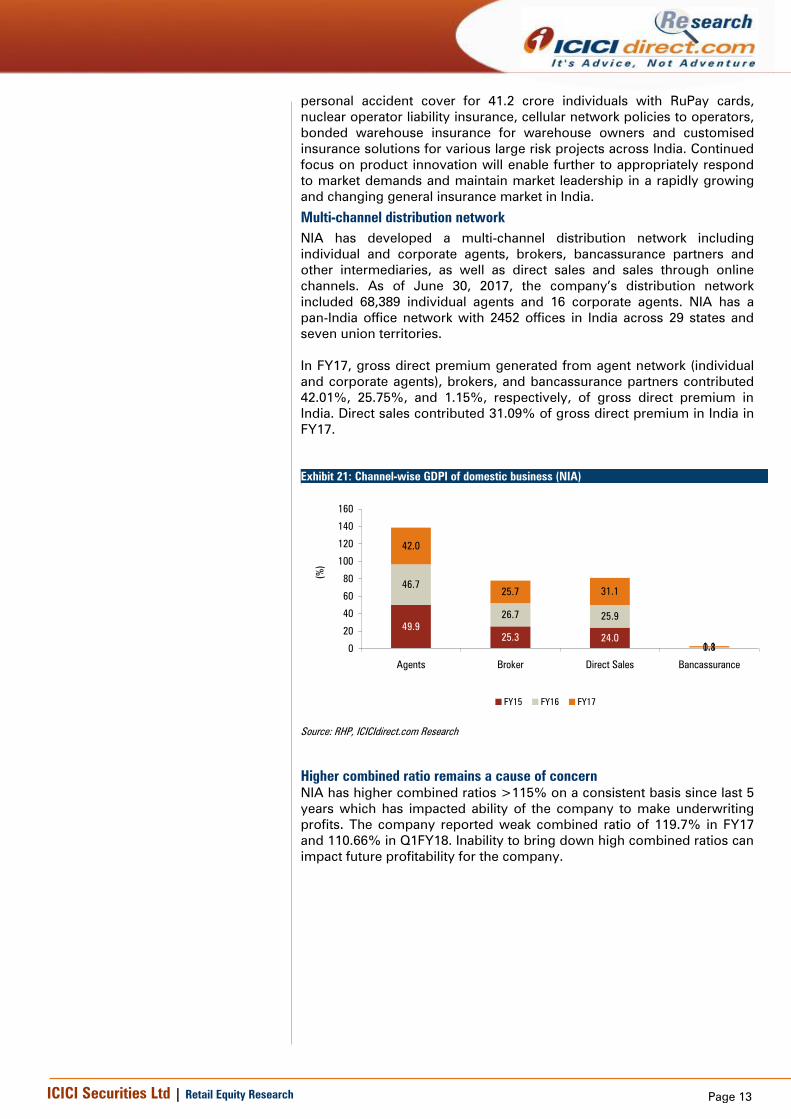

Multi-channel distribution network

NIA has developed a multi-channel distribution network including

individual and corporate agents, brokers, bancassurance partners and

other intermediaries, as well as direct sales and sales through online

channels. As of June 30, 2017, the company’s distribution network

included 68,389 individual agents and 16 corporate agents. NIA has a

pan-India office network with 2452 offices in India across 29 states and

seven union territories.

In FY17, gross direct premium generated from agent network (individual

and corporate agents), brokers, and bancassurance partners contributed

42.01%, 25.75%, and 1.15%, respectively, of gross direct premium in

India. Direct sales contributed 31.09% of gross direct premium in India in

FY17.

Exhibit 21: Channel-wise GDPI of domestic business (NIA) es

49.9

25.3 24.0

0.8

46.7

26.7 25.9

0.8

42.0

25.7 31.1

1.10

20

40

60

80

100

120

140

160

Agents Broker Direct Sales Bancassurance

(%

)

FY15 FY16 FY17

Source: RHP, ICICIdirect.com Research

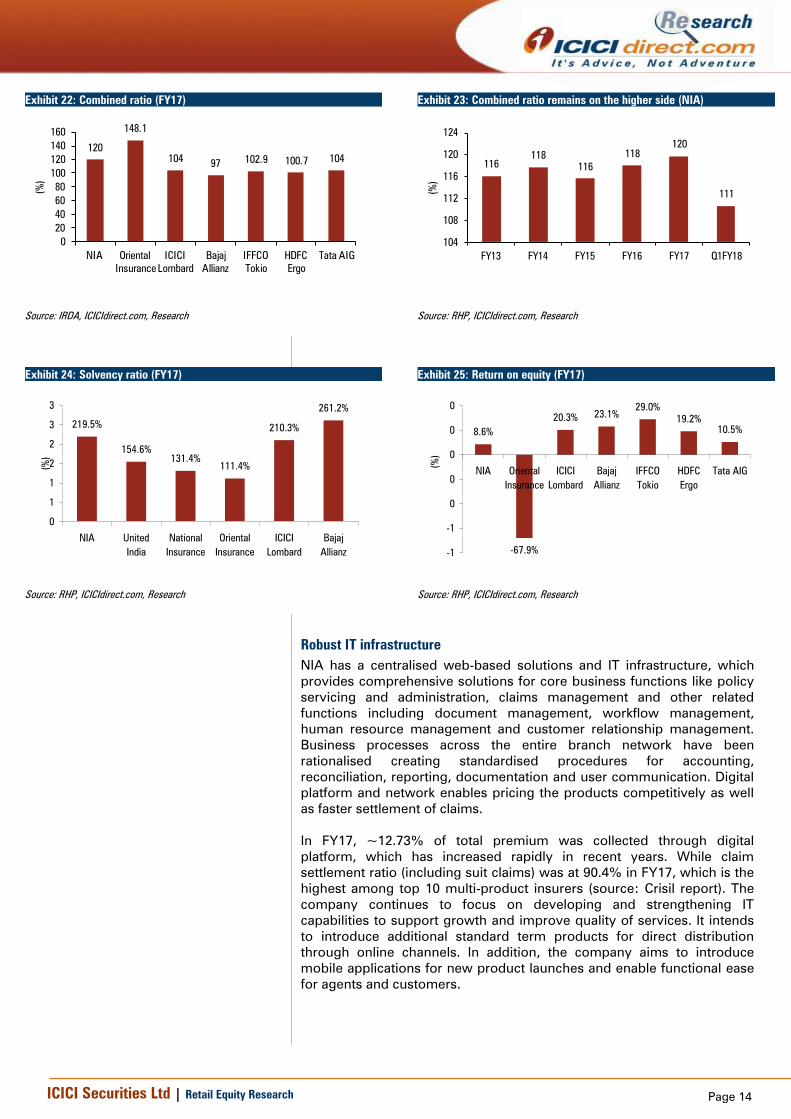

Higher combined ratio remains a cause of concern

NIA has higher combined ratios >115% on a consistent basis since last 5

years which has impacted ability of the company to make underwriting

profits. The company reported weak combined ratio of 119.7% in FY17

and 110.66% in Q1FY18. Inability to bring down high combined ratios can

impact future profitability for the company.

Page 14 ICICI Securities Ltd | Retail Equity Research

Exhibit 22: Combined ratio (FY17)

120

148.1

10497

102.9 100.7 104

0

20

40

60

80

100

120

140

160

NIA Oriental

Insurance

ICICI

Lombard

Bajaj

Allianz

IFFCO

Tokio

HDFC

Ergo

Tata AIG

(%

)

Source: IRDA, ICICIdirect.com, Research

Exhibit 23: Combined ratio remains on the higher side (NIA)

116

118

116

118

120

111

104

108

112

116

120

124

FY13 FY14 FY15 FY16 FY17 Q1FY18

(%

)

Source: RHP, ICICIdirect.com, Research

Exhibit 24: Solvency ratio (FY17)

219.5%

154.6%

131.4%

111.4%

210.3%

261.2%

0

1

1

2

2

3

3

NIA United

India

National

Insurance

Oriental

Insurance

ICICI

Lombard

Bajaj

Allianz

(%

)

Source: RHP, ICICIdirect.com, Research

Exhibit 25: Return on equity (FY17)

8.6%

-67.9%

20.3%23.1%

29.0%

19.2%

10.5%

-1

-1

0

0

0

0

0

NIA Oriental

Insurance

ICICI

Lombard

Bajaj

Allianz

IFFCO

Tokio

HDFC

Ergo

Tata AIG

(%

)

Source: RHP, ICICIdirect.com, Research

Robust IT infrastructure

NIA has a centralised web-based solutions and IT infrastructure, which

provides comprehensive solutions for core business functions like policy

servicing and administration, claims management and other related

functions including document management, workflow management,

human resource management and customer relationship management.

Business processes across the entire branch network have been

rationalised creating standardised procedures for accounting,

reconciliation, reporting, documentation and user communication. Digital

platform and network enables pricing the products competitively as well

as faster settlement of claims.

In FY17, ~12.73% of total premium was collected through digital

platform, which has increased rapidly in recent years. While claim

settlement ratio (including suit claims) was at 90.4% in FY17, which is the

highest among top 10 multi-product insurers (source: Crisil report). The

company continues to focus on developing and strengthening IT

capabilities to support growth and improve quality of services. It intends

to introduce additional standard term products for direct distribution

through online channels. In addition, the company aims to introduce

mobile applications for new product launches and enable functional ease

for agents and customers.

Page 15 ICICI Securities Ltd | Retail Equity Research

Key risks and concerns

Catastrophic events may have material adverse effect on operations

NIA has a wide range of insurance products including products that cover

losses from unpredictable events such as hurricanes, storms, monsoons,

earthquakes, fires, industrial explosions, floods, riots, terrorism, etc.

There can be no assurance that the company has been or will in future be

able to effectively cover large losses arising out of these catastrophic

events. In case the company incurs one or more large catastrophic losses,

its ability to write future business may be adversely impacted if the

company is unable to replenish its capital.

Dependence on select insurance products for premium & profitability

In FY17, the fire, motor and health insurance segments contributed

12.1%, 41.1% and 27.9% respectively, of NIA’s gross direct premium.

Any constraint in selling these products due to future regulatory changes

restricting or limiting the sale or marketing of these products, changes in

customer preference could have a material adverse effect on business

operations.

Inability to bring down high combined ratios in future

High combined ratios >115% on a consistent basis since last 5 years

impact ability of the company to make underwriting profits. Company

reported weak combined ratio of 119.7% even in FY17 and 110.66% in

Q1FY18. Inability to bring down high combined ratios can impact future

profitability for the company.

Significant portion of business is generated from relatively few regions

Maharashtra and Tamil Nadu accounted for 44.74% of NIA’s domestic

gross direct premium in FY17. Thus, it is susceptible to economic and

other trends and developments, including adverse weather conditions, in

these areas. Given NIA’s, geographic concentrations, any catastrophic

event in such locations may significantly increase catastrophic

reinsurance premiums.

Regulation of motor insurance; changes in demand for motor vehicles

In FY15, FY16 and FY17, NIA derived 38.59%, 39.80% and 38.81%

respectively, of its gross written premium from motor vehicle insurance

products. This has largely been driven by the continued growth in

demand for motor vehicles. Such growth in demand may not sustain in

the future. Further, under the Motors Vehicles Act, 1988, as amended,

there is a requirement for every person who uses (except passengers) or

causes or allows any other person to use a motor vehicle in public, to

purchase motor vehicle third-party liability insurance. If there is any

change in this requirement, the demand for third-party motor insurance

may decline, which could have an adverse effect on company’s business

as this product line contributed to 19.6% of its gross premium in FY17.

Additional risks associated with international operations

In FY15, FY16 and FY17, gross written premium from NIA’s international

operations was | 2840 crore, | 3222 crore and | 3164 crore, respectively,

and contributed 17.7%, 17.54% and 14.2%, respectively, of its ‘s gross

written premium in such periods. This business is subjects to various

risks, including currency risk, risks associated with political instability,

catastrophic risk affecting business underwritten abroad, changing market

conditions around the globe, economic downturn, which could result in

financial market disruption, and risk of compliance with local laws, any of

which could cause a material and adverse effect on NIA’s business and

prospects.

Page 16 ICICI Securities Ltd | Retail Equity Research

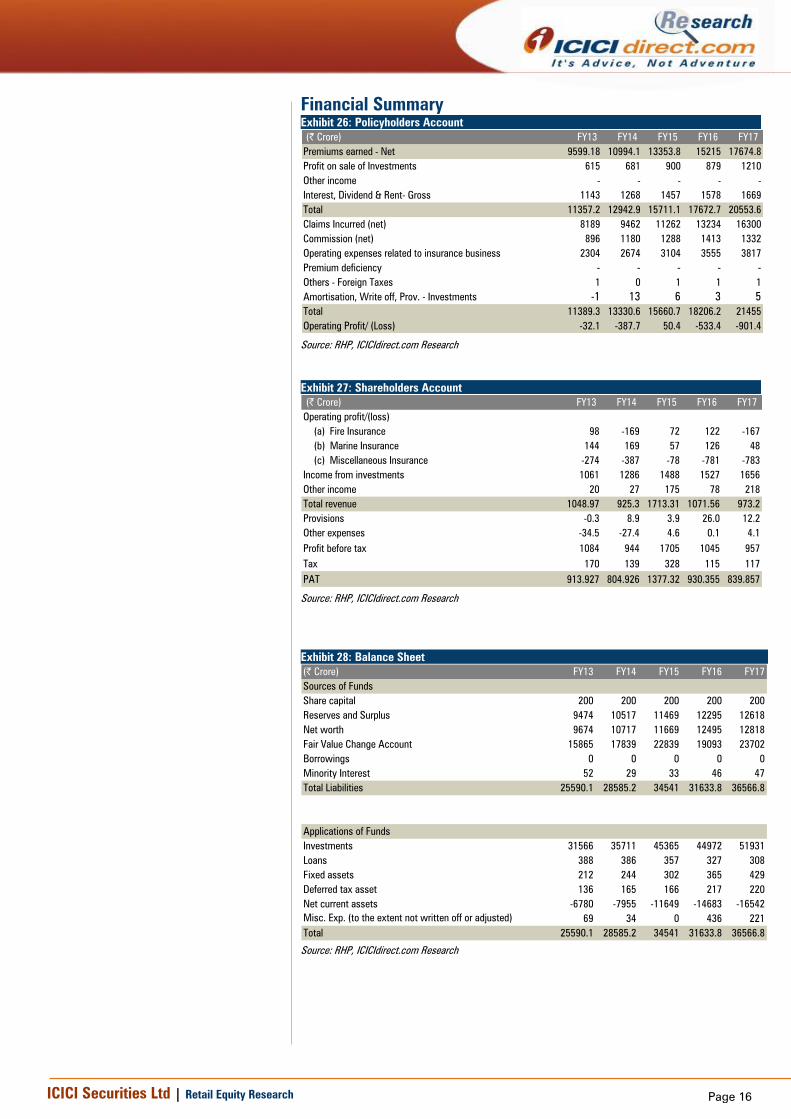

Financial Summary

Exhibit 26: Policyholders Account

(| Crore) FY13 FY14 FY15 FY16 FY17

Premiums earned - Net 9599.18 10994.1 13353.8 15215 17674.8

Profit on sale of Investments 615 681 900 879 1210

Other income - - - - -

Interest, Dividend & Rent- Gross 1143 1268 1457 1578 1669

Total 11357.2 12942.9 15711.1 17672.7 20553.6

Claims Incurred (net) 8189 9462 11262 13234 16300

Commission (net) 896 1180 1288 1413 1332

Operating expenses related to insurance business 2304 2674 3104 3555 3817

Premium deficiency - - - - -

Others - Foreign Taxes 1 0 1 1 1

Amortisation, Write off, Prov. - Investments -1 13 6 3 5

Total 11389.3 13330.6 15660.7 18206.2 21455

Operating Profit/ (Loss) -32.1 -387.7 50.4 -533.4 -901.4

Source: RHP, ICICIdirect.com Research

Exhibit 27: Shareholders Account

(| Crore) FY13 FY14 FY15 FY16 FY17

Operating profit/(loss)

(a) Fire Insurance 98 -169 72 122 -167

(b) Marine Insurance 144 169 57 126 48

(c) Miscellaneous Insurance -274 -387 -78 -781 -783

Income from investments 1061 1286 1488 1527 1656

Other income 20 27 175 78 218

Total revenue 1048.97 925.3 1713.31 1071.56 973.2

Provisions -0.3 8.9 3.9 26.0 12.2

Other expenses -34.5 -27.4 4.6 0.1 4.1

Profit before tax 1084 944 1705 1045 957

Tax 170 139 328 115 117

PAT 913.927 804.926 1377.32 930.355 839.857

Source: RHP, ICICIdirect.com Research

Exhibit 28: Balance Sheet

(| Crore) FY13 FY14 FY15 FY16 FY17

Sources of Funds

Share capital 200 200 200 200 200

Reserves and Surplus 9474 10517 11469 12295 12618

Net worth 9674 10717 11669 12495 12818

Fair Value Change Account 15865 17839 22839 19093 23702

Borrowings 0 0 0 0 0

Minority Interest 52 29 33 46 47

Total Liabilities 25590.1 28585.2 34541 31633.8 36566.8

Applications of Funds

Investments 31566 35711 45365 44972 51931

Loans 388 386 357 327 308

Fixed assets 212 244 302 365 429

Deferred tax asset 136 165 166 217 220

Net current assets -6780 -7955 -11649 -14683 -16542

Misc. Exp. (to the extent not written off or adjusted) 69 34 0 436 221

Total 25590.1 28585.2 34541 31633.8 36566.8

Source: RHP, ICICIdirect.com Research

Page 17 ICICI Securities Ltd | Retail Equity Research

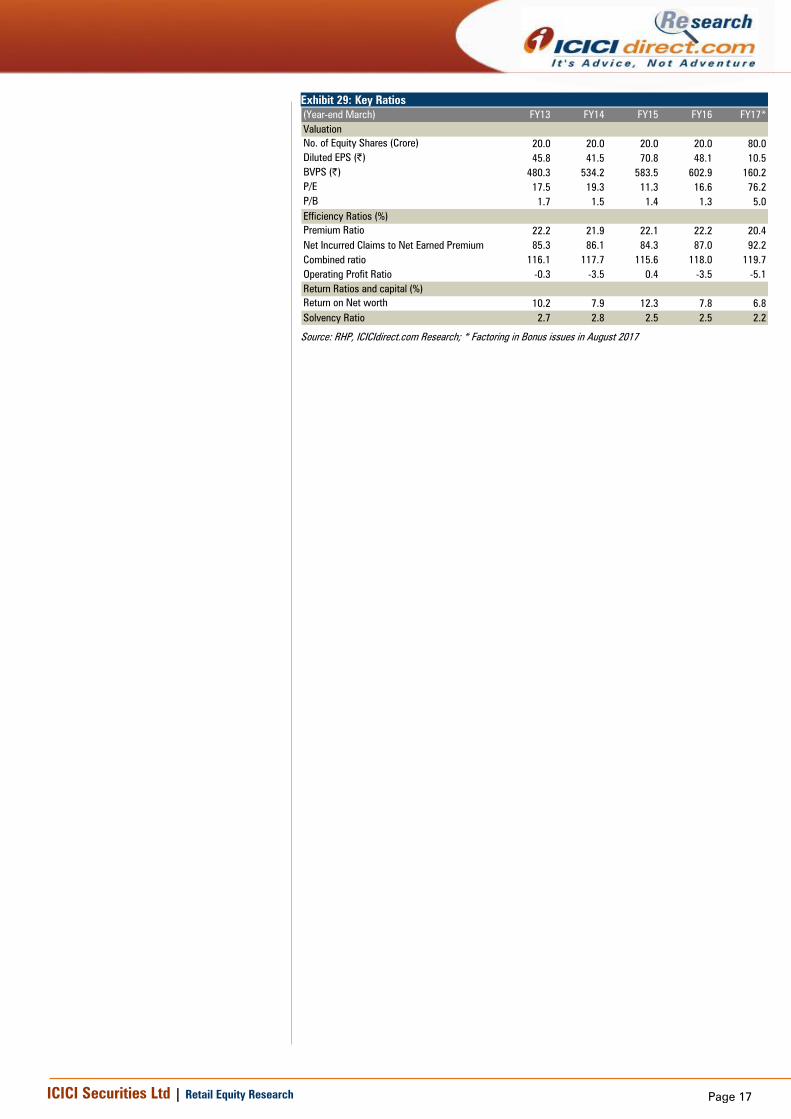

Exhibit 29: Key Ratios

(Year-end March) FY13 FY14 FY15 FY16 FY17*

Valuation

No. of Equity Shares (Crore) 20.0 20.0 20.0 20.0 80.0

Diluted EPS (|) 45.8 41.5 70.8 48.1 10.5

BVPS (|) 480.3 534.2 583.5 602.9 160.2

P/E 17.5 19.3 11.3 16.6 76.2

P/B 1.7 1.5 1.4 1.3 5.0

Efficiency Ratios (%)Expense of Management to Net Written

Premium Ratio 22.2 21.9 22.1 22.2 20.4

Net Incurred Claims to Net Earned Premium 85.3 86.1 84.3 87.0 92.2

Combined ratio 116.1 117.7 115.6 118.0 119.7

Operating Profit Ratio -0.3 -3.5 0.4 -3.5 -5.1

Return Ratios and capital (%)

Return on Net worth 10.2 7.9 12.3 7.8 6.8

Solvency Ratio 2.7 2.8 2.5 2.5 2.2

Source: RHP, ICICIdirect.com Research; * Factoring in Bonus issues in August 2017

Page 18 ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its

stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold

and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts'

valuation for a stock.

Subscribe: Apply for the IPO

Avoid: Do not apply for the IPO

Subscribe only for long term: Apply for the IPO only from a long term investment perspective

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

Page 19 ICICI Securities Ltd | Retail Equity Research

ANALYST CERTIFICATION

We /I, Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research

report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s)

or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA Research Analysts of this report have not received any compensation from the companies mentioned in the report in the

preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

![Khenyei v. New India Assurance Co. Ltd. & Ors]](https://img.dokumen.tips/doc/110x75/577cb5581a28aba7118d0ee1/khenyei-v-new-india-assurance-co-ltd-ors.jpg)