Embed Size (px)

Citation preview

Leadership in life insurance

October 2014

22

Industry overview and outlook

Performance update

Our strategy

Agenda

3

Agenda

3

Industry overview and outlook

Performance update

Our strategy

Total premium (` bn)

Penetration (as a % to

GDP)

New business premium1

(` bn)

Number of players

Insurance density (`)

FY2014

24

454

3,141

2,479

FY2002

12

116

501

2.1%

460

28.7%

26.1%

Source: IRDA, Public disclosures, Life insurance council, Company

estimates

India life insurance growth story

Asset under

management (` bn)

20,0692,30424.3%

1. Retail weighted premium

FY2008

18

527

2,014

1,680

8,477

-2.4%

7.7%

15.4%

4

4.0% 2.8%

Source: UN Population division‘s release: ‘World Population Prospects-

The 2012 Revision’

Fuelled by favourable demographics..

Increase in target population with rising income levels

Population of age > 25 years (in mn)

5

613

755

888

-

100

200

300

400

500

600

700

800

900

1,000

2010 2020E 2030E

..High household savings

Source: RBI, CSO

*Company estimates6

2.98 3.44 4.31 5.38

7.60 8.56

10.26

14.23 14.95 17.08

2.47 3.13

4.38

5.80

5.71

7.75

7.74

6.32

7.17

8.19

0

5

10

15

20

25

30

2001-02 2003-04 2005-06 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Rs t

rillio

n

Physical savings Financial saving

Financial year 2002 2004 2006 2008 2009 2010 2011 2012 2013 2014

Financial savings

/ GDP10.5% 11.0% 11.9% 11.6% 10.1% 12.0% 9.9% 7.0% 7.1% 7.2%

Household

savings / GDP23.2% 23.2% 23.5% 22.4% 23.6% 25.2% 23.1% 22.8% 21.9% 22.3%*

13.4%

14.3%

22.0%

21.0%

26.2%

20.0%

21.3%

17.3%

0%

20%

40%

60%

80%

100%

FY2002 FY2004 FY2006 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014

Provident / Pension Fund / Claims on Govt Shares / Debentures / MFS

Life Insurance Fund Currency & Deposits

Share of life insurance in financial savings

14.4%17.0%

Source: RBI

7

Distribution of financial assets

Insurance market size

Significant opportunity at current savings rate

Household savings

Insurance

FY

2008

1.70

Gross financial

savings

Nominal GDP

FY

2020E*

4.62

58.84

27.16

262.65

FY

2002

0.41

23.48

15%

CAGR

49.87

5.45

2.86

11.18

7.72

FY

2014

2.00

113.55

25.27*

11.74

27%

CAGR

13%

CAGR

13%

CAGR

18%

CAGR

3%

CAGR

15%

CAGR

15%

CAGR

7%

CAGR

Amounts in ` trillion

15%

CAGR

15%

CAGR

15%

CAGR

Source: RBI, CSO

*Company estimates8

Industry: New business premium1

1. Retail weighted new business premium

Source : IRDA, Life insurance council

Rs

bn

9

Growth FY2010 FY2011 FY2012 FY2013 FY2014 H1-FY2015

Private 7.1% -20.0% -23.9% 1.9% -3.4% 8.8%

LIC 29.3% 4.3% 11.2% -4.1% -3.4% -21.4%

Industry 16.7% -8.5% -4.8% -1.9% -3.4% -10.5%

52.3%

45.7%

36.5%38.0%

38.0%

43.7%

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

350

FY2010 FY2011 FY2012 FY2013 FY2014 H1-FY2015

LIC Private Private market share

Channel mix1

Industry

1. Individual new business premium basis

Source: IRDA, Public disclosures

Private players

10

79% 79% 78% 78% 77%

13% 15% 16% 16% 16%

8% 6% 6% 6% 7%

FY2011 FY2012 FY2013 FY2014 Q1-FY2015

Agency Banca Others

47%44%

40% 40%37%

33% 39%43% 44%

45%

20%17% 17% 16% 18%

FY2011 FY2012 FY2013 FY2014 Q1-FY2015

Agency Banca Others

Product mix1

Industry Private players

1. New business premium basis

Source: IRDA, Life insurance council 11

58%

85%90%

93% 92%

42%

15%10%

7% 8%

FY2011 FY2012 FY2013 FY2014 Q1-FY2015

Traditional ULIP

31%

59%

65%71% 72%

69%

41%

35%29% 28%

FY 2011 FY 2012 FY 2013 FY 2014 Q1-FY2015

Traditional ULIP

Agenda

Industry overview and outlook

Performance update

Our strategy

12

Retail new business premium 34.20

Retail renewal premium

Group premium

Total premium

RWRP

34.32

80.55 81.00

20.63 8.97

135.38 124.29

33.10 32.53

FY2014FY2013` bn

Premium summary

13

14.35

32.18

4.67

51.20

13.57

H1-FY2014

18.45

37.34

5.55

61.34

17.48

H1-FY2015

Key parameters

Profit after tax

Solvency ratio (%)

Assets under management

APE

New Business Profit (NBP)1

35.32 34.44

5.29 4.27

14.96 15.67

396 372

741.64 805.97

14.95

2.15

7.51

395

739.76

18.56

2.02

7.81

357

907.26

FY2014FY2013` bn H1-FY2014 H1-FY2015

1. Traditional Embedded Value basis, on medium term expense targets,

post-tax basis

15

Agenda

15

Industry overview and outlook

Performance update

Our strategy

Key strategic objective

Enhance market leadership

Provide superior value proposition to customers

Strengthen multichannel distribution architecture

Improve cost efficiency

Improve persistency and control surrenders

Target superior risk adjusted fund performance

16

Robust risk management and control framework

Consistent leadership1

1

3

4

5

2

FY2006 FY2012

6

FY2013

1. Retail weighted received premium (RWRP) basis

17

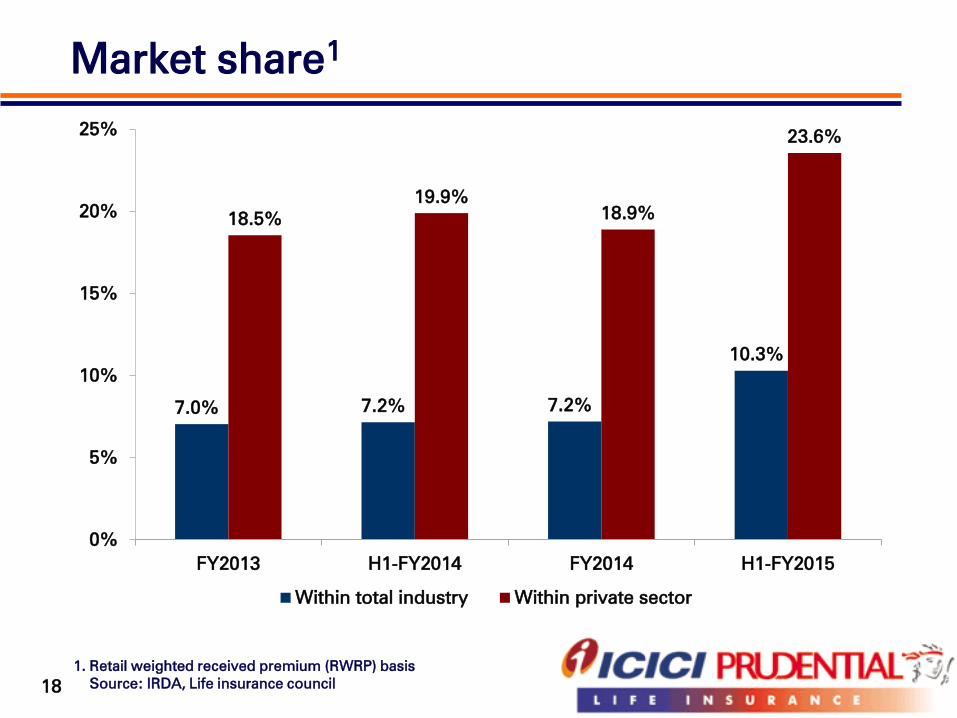

FY2002 FY2010 FY2014 H1-FY2015

Market share1

18

1. Retail weighted received premium (RWRP) basis

Source: IRDA, Life insurance council

7.0% 7.2% 7.2%

10.3%

18.5%

19.9%

18.9%

23.6%

0%

5%

10%

15%

20%

25%

FY2013 H1-FY2014 FY2014 H1-FY2015

Within total industry Within private sector

Product mix1

1. Retail weighted received premium (RWRP) basis

19

45.5%40.50%

33.5%

18.2%

54.5%59.5%

66.5%

81.8%

0%

20%

40%

60%

80%

100%

FY2013 H1-FY2014 FY2014 H1-FY2015

Traditional Ulip

Distribution mix1

20

1. Retail weighted received premium (RWRP) basis

35.4%

28.5% 29.0%

22.4%

44.9%53.7% 54.6%

61.8%

13.1% 11.1% 9.6% 7.0%

6.5% 6.7% 6.8% 8.8%

0%

50%

100%

FY2013 H1-FY2014 FY2014 H1-FY2015

Agency Banca CABR Others

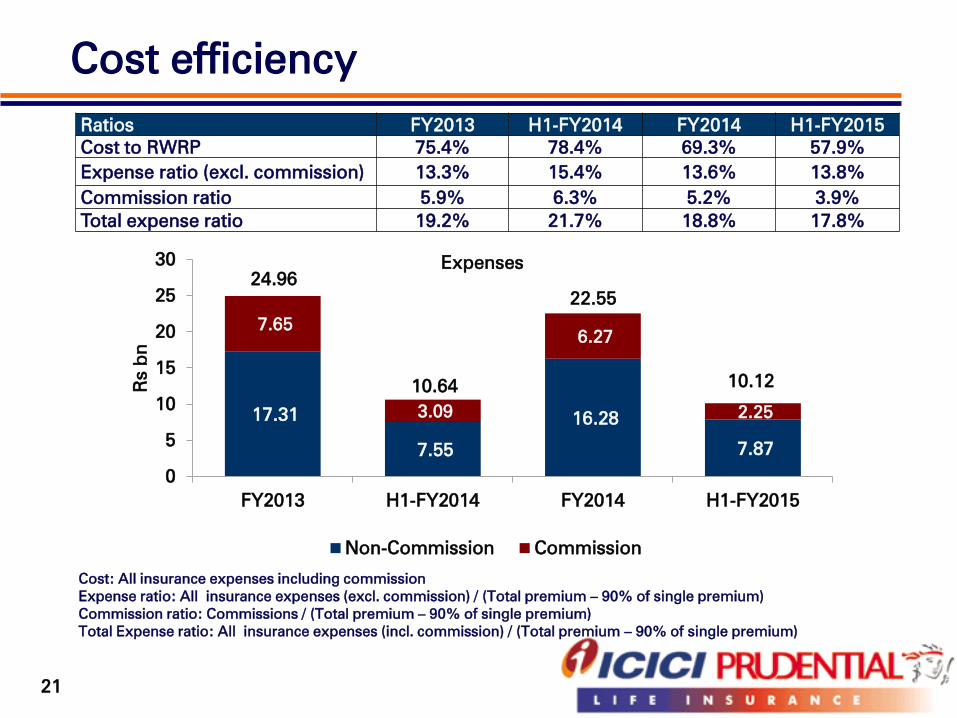

Cost efficiency

Cost: All insurance expenses including commission

Expense ratio: All insurance expenses (excl. commission) / (Total premium – 90% of single premium)

Commission ratio: Commissions / (Total premium – 90% of single premium)

Total Expense ratio: All insurance expenses (incl. commission) / (Total premium – 90% of single premium)

21

Ratios FY2013 H1-FY2014 FY2014 H1-FY2015

Cost to RWRP 75.4% 78.4% 69.3% 57.9%

Expense ratio (excl. commission) 13.3% 15.4% 13.6% 13.8%

Commission ratio 5.9% 6.3% 5.2% 3.9%

Total expense ratio 19.2% 21.7% 18.8% 17.8%

22.55

24.96

10.1210.64

17.31

7.55

16.28

7.87

7.65

3.09

6.27

2.25

0

5

10

15

20

25

30

FY2013 H1-FY2014 FY2014 H1-FY2015

Rs b

n

Expenses

Non-Commission Commission

Customer retention

13th

month persistency

1. Average monthly retail surrenders

Surrenders1 as % of average AUM

22

1.3%

1.0%

1.1%

1.0%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

FY2013 H1-FY2014 FY2014 H1-FY2015

71.4%

68.2%

71.7% 71.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

FY2013 H1-FY2014 FY2014 H1-FY2015

Customer service: H1-FY2015

92% of the new business applications initiated using

the digital platform

45% of renewal premium payment through

electronic modes1

69% of all service transactions processed through

website, SMS and IVRS

92% of payouts through electronic mode

Grievance ratio2

stood at 193

1. Online, direct debit and electronic clearing services

2. Grievance ratio: grievances per 10,000 polices23

739.76

2424

Assets under management

Among the largest domestic fund managers

907.26

805.97

741.64

364.10 389.16 423.71

463.40

377.54 350.60

382.26

443.86

0

100

200

300

400

500

600

700

800

900

1,000

FY2013 H1-FY2014 FY2014 H1-FY2015

Rs b

n

Debt Equity

Fund performance

Inception Dates:

Preserver Fund: June 28, 2004; Protector Fund: April 2, 2002

Balancer Fund : April 2, 2002; Maximiser Fund: Nov 19, 2001

97.6% of the funds have outperformed benchmark since inception*

* As on September 30, 2014

Fund performance since inception*

25

6.9%6.4%

10.7%

17.3%

8.1%

7.3%

12.3%

20.2%

0%

3%

6%

9%

12%

15%

18%

21%

Preserver Protector Balancer Maximiser

Benchmark Fund

26

Safe harbor

Except for the historical information contained herein, statements in this release

which contain words or phrases such as 'will', 'would', ‘indicating’, ‘expected to’

etc., and similar expressions or variations of such expressions may constitute

'forward-looking statements'. These forward-looking statements involve a number

of risks, uncertainties and other factors that could cause actual results to differ

materially from those suggested by the forward-looking statements. These risks

and uncertainties include, but are not limited to our ability to successfully

implement our strategy, our growth and expansion in business, the impact of any

acquisitions, technological implementation and changes, the actual growth in

demand for insurance products and services, investment income, cash flow

projections, our exposure to market risks, policies and actions of regulatory

authorities; impact of competition; experience with regard to mortality and

morbidity trends, lapse rates and policy renewal rates; the impact of changes in

capital , solvency or accounting standards , tax and other legislations and

regulations in the jurisdictions as well as other risks detailed in the reports filed by

ICICI Bank Limited, our holding company, with the United States Securities and

Exchange Commission. ICICI Bank and we undertake no obligation to update

forward-looking statements to reflect events or circumstances after the date

thereof.

Thank you