Embed Size (px)

Citation preview

October 2008 Paul Braks

Food & Agribusiness Research and Advisory

Grain markets in motion

Impact of volatile commodity prices on the agri-food value chain

Who is Rabobank?

Rabobank is the largest Allfinanz financial service corporation in the Netherlands

Rabobank is an AAA rated financial institution

Rabobank has a international food & agri focus

Rabobank delivers financial solutions through a network of branches in 41 countries

2 Source: Rabobank, 2008

3

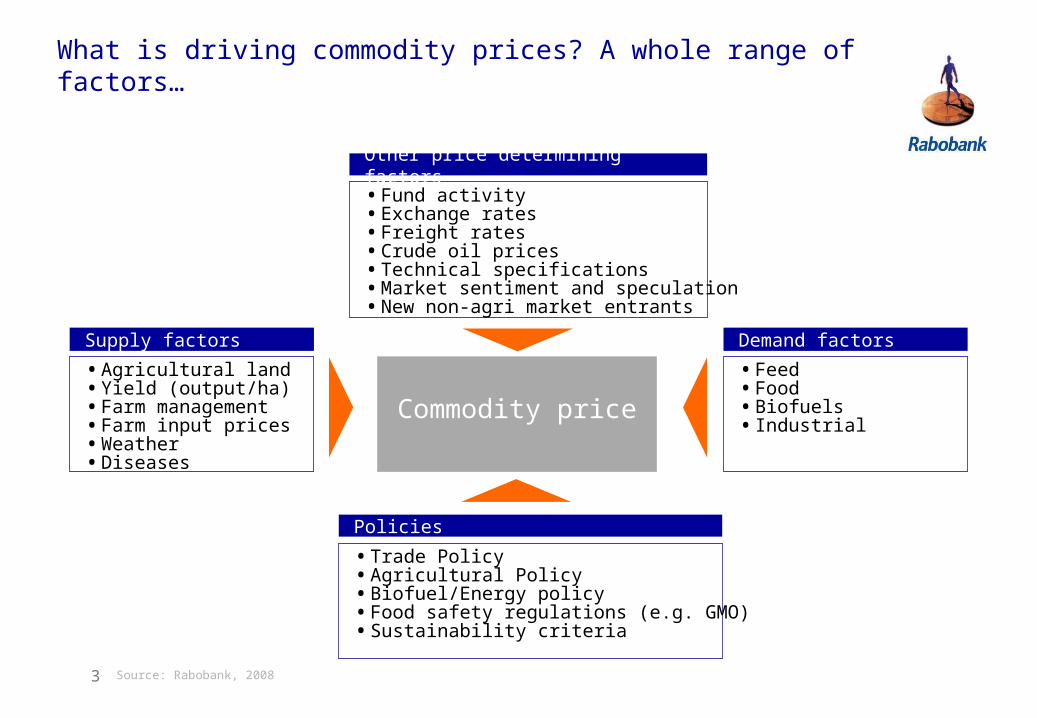

What is driving commodity prices? A whole range of factors…

Commodity price

• Agricultural land• Yield (output/ha)• Farm management• Farm input prices• Weather• Diseases

Supply factors

• Feed • Food• Biofuels• Industrial

Demand factors

• Fund activity• Exchange rates• Freight rates• Crude oil prices• Technical specifications • Market sentiment and speculation• New non-agri market entrants

Other price determining factors

• Trade Policy• Agricultural Policy• Biofuel/Energy policy• Food safety regulations (e.g. GMO)• Sustainability criteria

Policies

Source: Rabobank, 2008

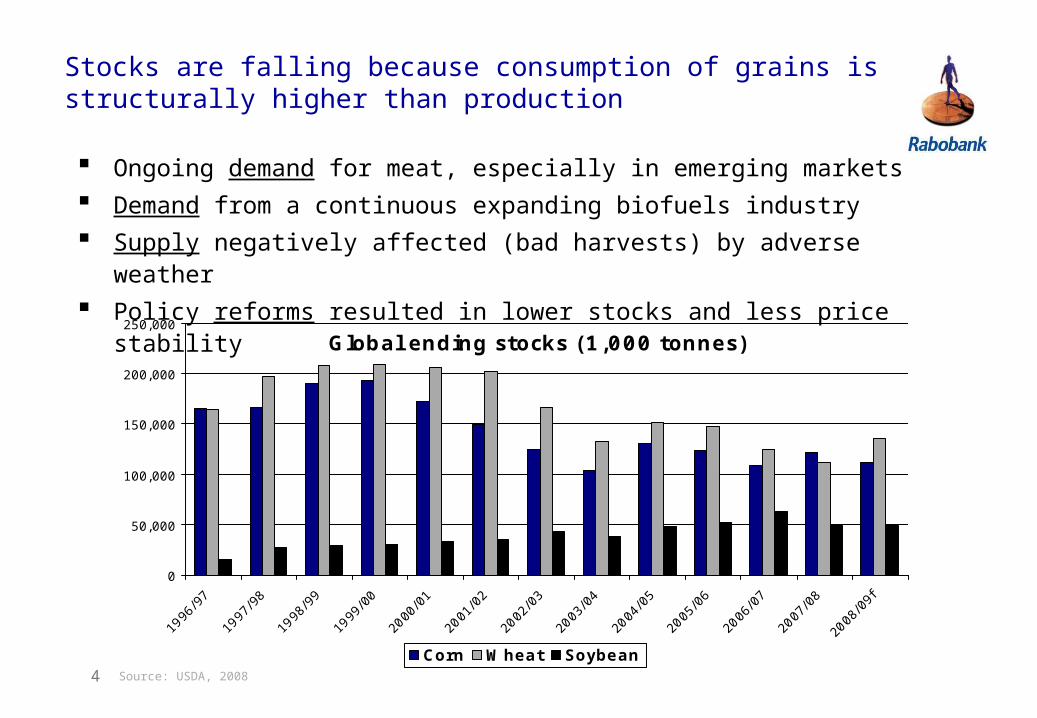

Stocks are falling because consumption of grains is structurally higher than production

Global ending stocks (1,000 tonnes)

0

50,000

100,000

150,000

200,000

250,000

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09f

Corn Wheat Soybean4 Source: USDA, 2008

Ongoing demand for meat, especially in emerging markets Demand from a continuous expanding biofuels industry Supply negatively affected (bad harvests) by adverse weather Policy reforms resulted in lower stocks and less price stability

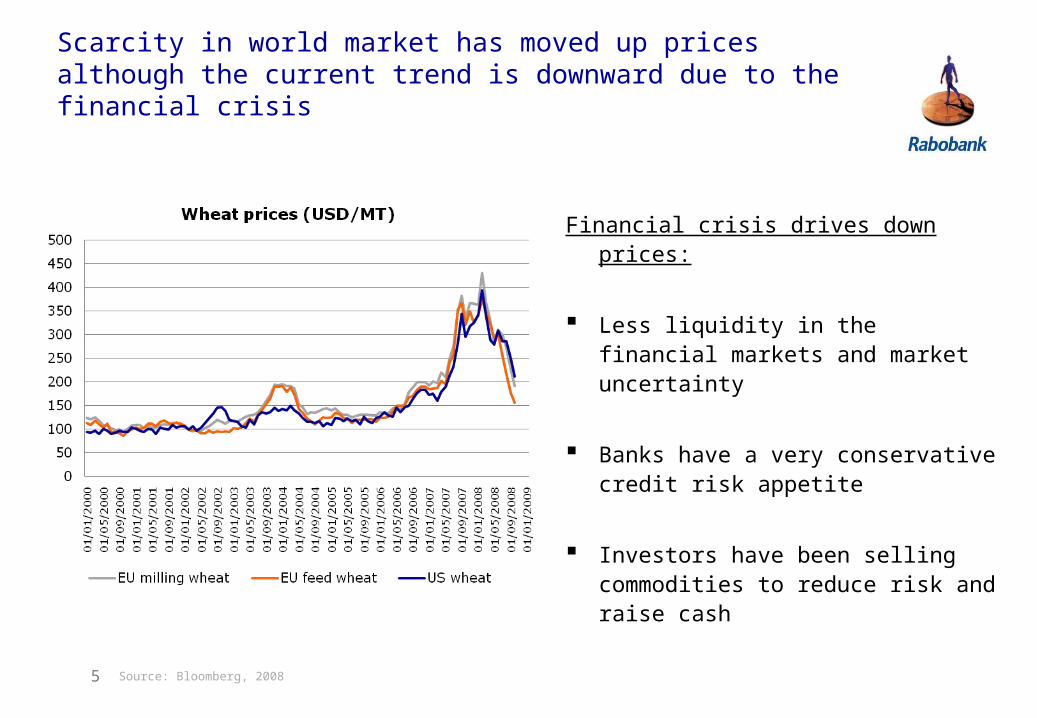

Scarcity in world market has moved up prices although the current trend is downward due to the financial crisis

Financial crisis drives down prices:

Less liquidity in the financial markets and market uncertainty

Banks have a very conservative credit risk appetite

Investors have been selling commodities to reduce risk and raise cash

5 Source: Bloomberg, 2008

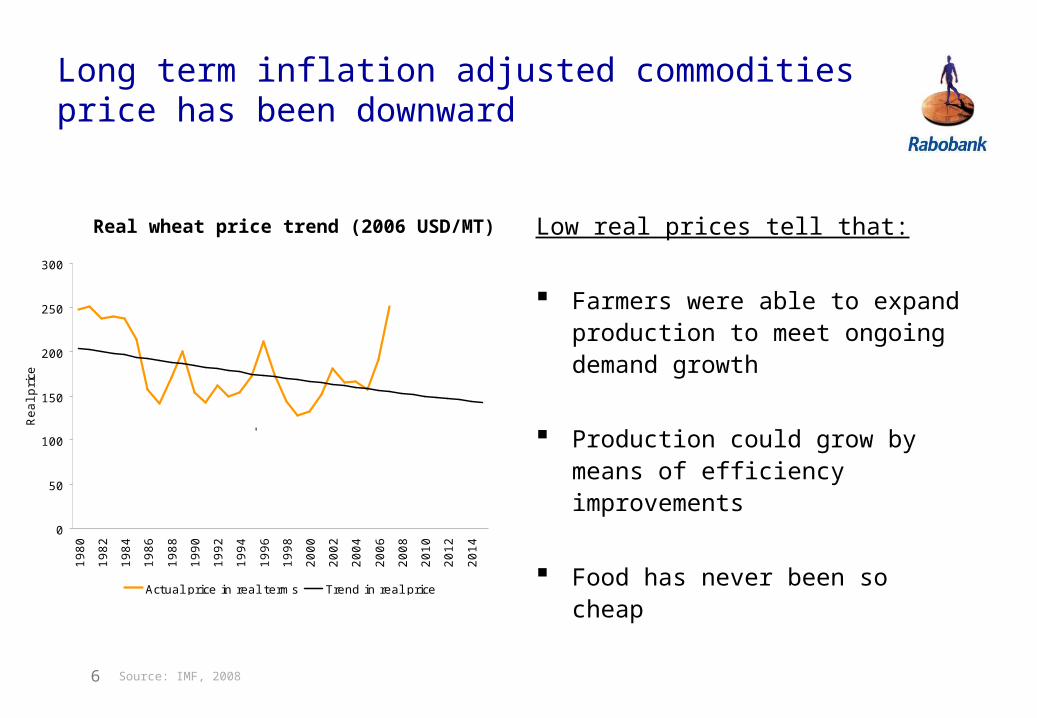

Long term inflation adjusted commodities price has been downward

Low real prices tell that:

Farmers were able to expand production to meet ongoing demand growth

Production could grow by means of efficiency improvements

Food has never been so cheap

6

0

50

100

150

200

250

300

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Real pri

ce

Actual price in real terms Trend in real price

'

Source: IMF, 2008

Real wheat price trend (2006 USD/MT)

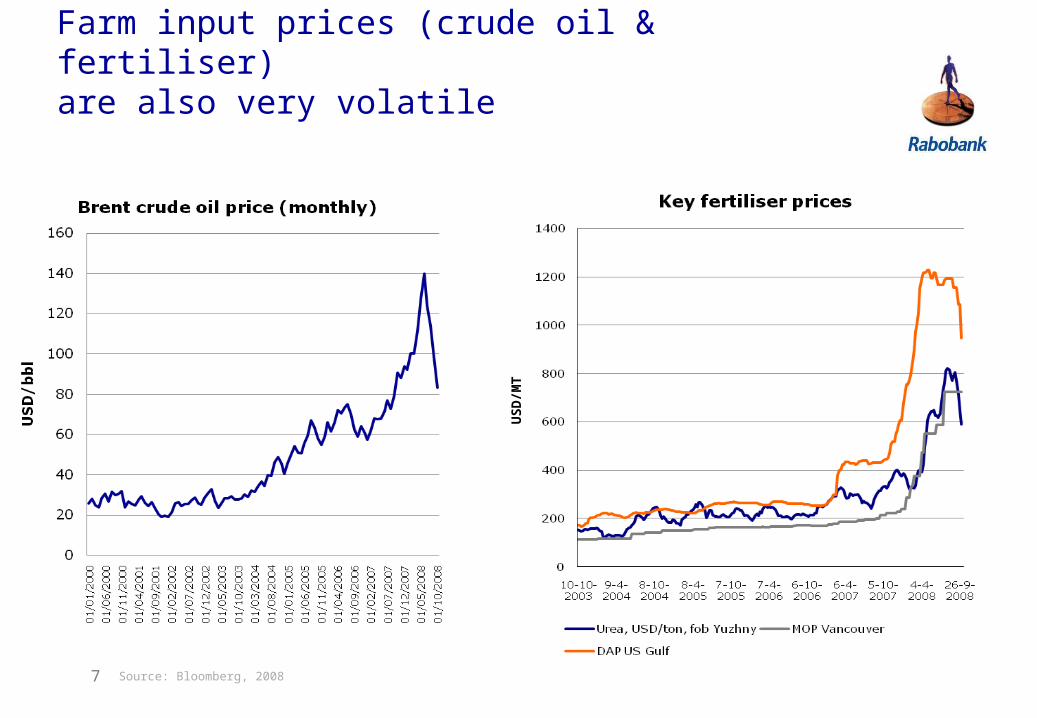

Farm input prices (crude oil & fertiliser) are also very volatile

7 Source: Bloomberg, 2008

US

D/M

T

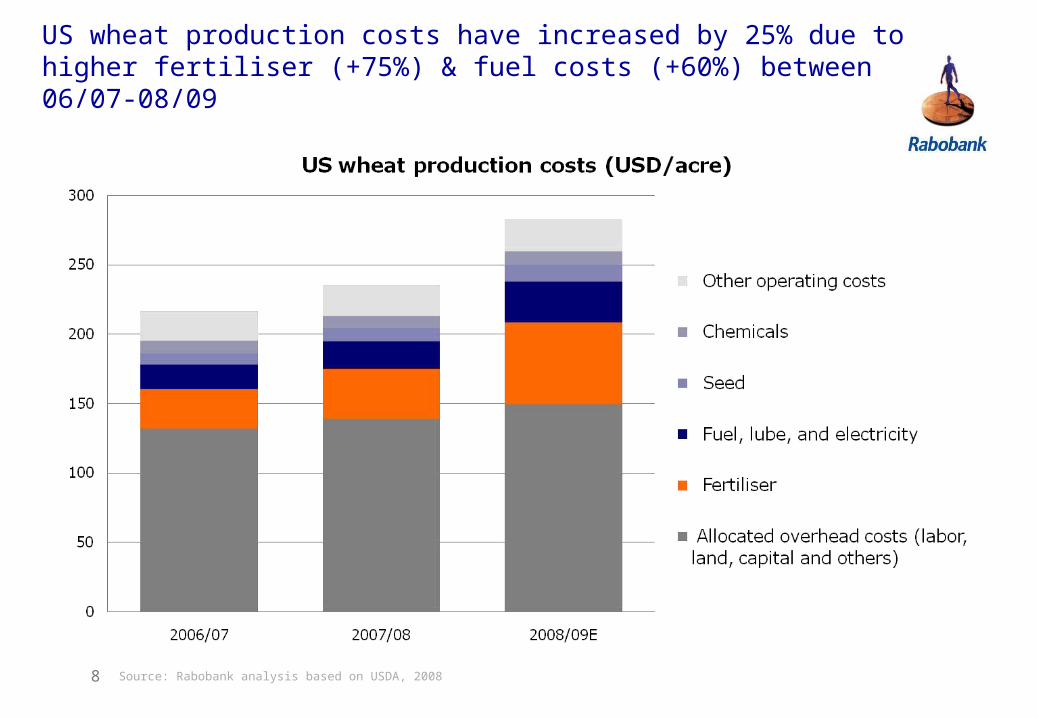

US wheat production costs have increased by 25% due to higher fertiliser (+75%) & fuel costs (+60%) between 06/07-08/09

8 Source: Rabobank analysis based on USDA, 2008

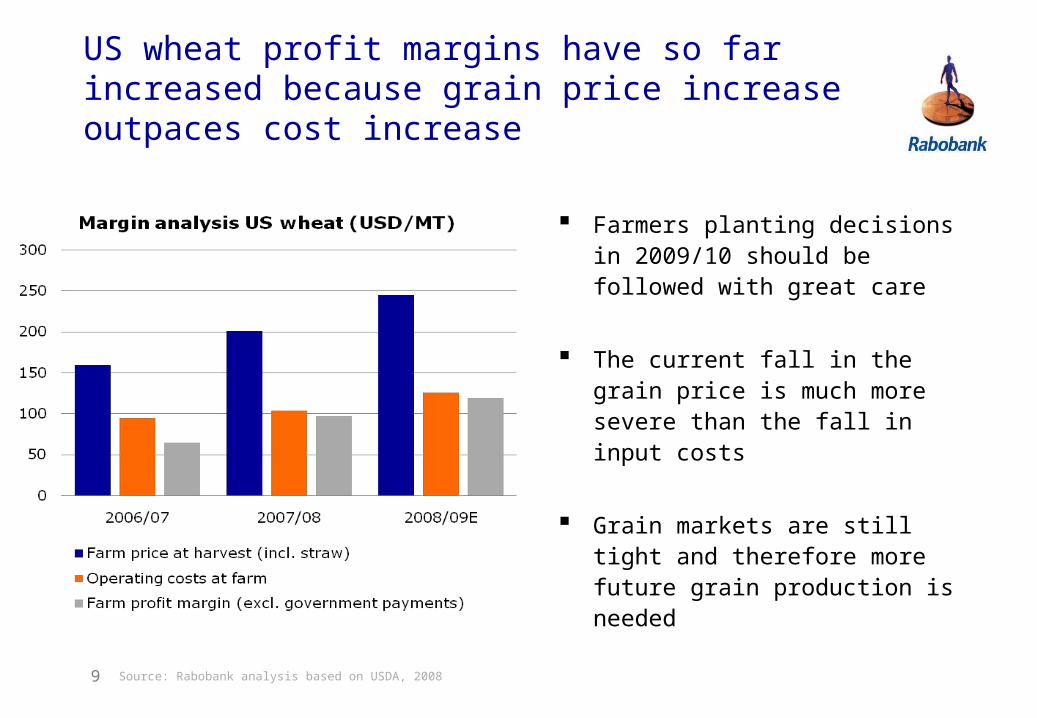

US wheat profit margins have so far increased because grain price increase outpaces cost increase

Farmers planting decisions in 2009/10 should be followed with great care

The current fall in the grain price is much more severe than the fall in input costs

Grain markets are still tight and therefore more future grain production is needed

9 Source: Rabobank analysis based on USDA, 2008

The European food industry is facing a higher and more uncertain costs base

Food processors have the following options:

Accepting pressure on margins / push volumesInternal costs savings measuresPassing through input cost inflationStrategic actions to address the cost base (M&A)

Source: Rabobank analysis, 200810

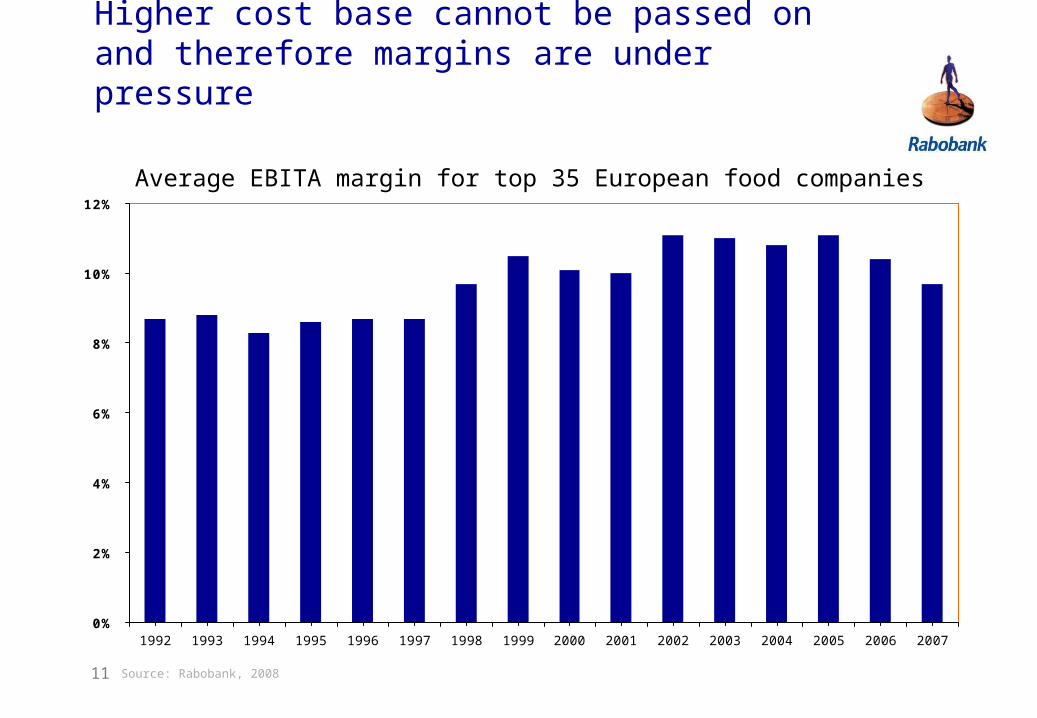

Higher cost base cannot be passed on and therefore margins are under pressure

Source: Rabobank, 200811

0%

2%

4%

6%

8%

10%

12%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Average EBITA margin for top 35 European food companies

Outlook

The current grains crop (2008/09) is considerably higher than last year. The good crop is especially driven by higher yields due to favourable weather and to some extent larger planted acreages

Prices of grains show a downward trend due to current situation in the financial markets. The grain markets are fundamentally still tight and therefore a future production expansion is needed

All players in the agri-food value chain continue to face volatile input and output costs, which will have an impact on profit margins

Commodity price risk management is getting more important for all players (from farmer to user) in the agri-food value chain

12 Source: Rabobank, 2008

13

“The financial link in the global food

chain”™