Embed Size (px)

Citation preview

O Transaksi dasar bisnis terjadi dalam beberapa siklus. Apa saja?

O Apakah siklus tersebut saling terkait? Berikan contohnya!

O Apa saja langkah-langkah mengubah data menjadi informasi?

DOCUMENTATION &

REVENUE CYCLE

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 3 of 119

• The data processing cycle consists of four steps:– Data input– Data storage– Data processing– Information output

TRANSACTION PROCESSING:THE DATA PROCESSING CYCLE

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 4 of 119

• Documentation includes the following types of tools:– Narratives (written descriptions)– Flowcharts– Diagrams– Other written material

Documentation

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 5 of 119

• In this chapter, we discuss two of the most common documentation tools:– Data flow diagrams

• Graphical descriptions of the sources and destinations of data. They show:– Where data comes from– How it flows– The processes performed on it– Where it goes

Documentation

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 6 of 119

• In this chapter, we discuss two of the most common documentation tools:– Data flow diagrams– Flowcharts

• Include three types:– Document flowcharts describe the flow of documents and

information between departments or units.– System flowcharts describe the relationship between inputs,

processing, and outputs for a system.– Program flowcharts describe the sequence of logical

operations performed in a computer program.

Documentation

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 7 of 119

• Documentation tools support organization in:– Organizing very complicated systems into a

form that can be more readily understood.– Helping new team members understand a

pre-existing system.

Documentation

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 8 of 119

INTRODUCTION TO DFD AND FLOWCHART

• Which method should you use—flowcharts or DVDs?– 62.5% of IS professionals use DFDs– 97.6% use flowcharts

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 9 of 119

DATA FLOW DIAGRAMS

• A data flow diagram (DFD) graphically describes the flow of data within an organization. It is used to:– Document existing systems– Plan and design new systems

• There is no black-and-white approach to developing a DFD.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart10 of

119

DFD Symbol

Menggambarkan agent/subyek

Menggambarkan proses yang terjadi

Menggambarkan data/informasi

Menggambarkan alur

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart11 of

119

DATA FLOW DIAGRAMS

Customer1.0

ProcessPayment

2.0Update

A/R

CreditManager

Bank

AccountsReceivable

Customerpayment

Remittancedata

ReceivablesInformation

Deposit

• Example of a data flow diagram of the customer payment process from Figure 3-3 in your textbook.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart12 of

119

FLOWCHARTS

• A flowchart is an analytical technique that describes some aspect of an information system in a clear, concise, and logical manner.

• Flowcharts use a set of standard symbols to depict processing procedures and the flow of data.

• Flowcharting History:– Introduced in 1950s by industrial engineers to document

business processes and document flows for process improvement.

– Sarbanes-Oxley 2002 increased importance by requiring companies to document business processes and internal controls procedures.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart13 of

119

FLOWCHARTS

• Every shape on a flowchart depicts a unique operation, input, processing activity, or storage medium.

• In the days of yore, flowcharts were manually created using plastic templates.

• Most flowcharts are now drawn using a software program such as Visio.– Microsoft and Power Point are also used.– The software uses pre-drawn shapes, and the

developer drags the shapes into the drawing.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart14 of

119

FLOWCHARTS

• There are four types of flowcharting symbols:– Input/output symbols

Input/output symbols indicate the type of device or media that provides input to or records output from a process.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart15 of

119

FLOWCHARTS

• There are four types of flowcharting symbols:– Input/output symbols– Processing symbols

Processing symbols indicate the type of device used to process the data or whether the data is processed manually.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart16 of

119

FLOWCHARTS

• There are four types of flowcharting symbols:– Input/output symbols– Processing symbols– Storage symbols

Storage symbols indicate the type of device used to store data while the system is not using it.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart17 of

119

FLOWCHARTS

• There are four types of flowcharting symbols:– Input/output symbols– Processing symbols– Storage symbols– Flow and miscellaneous symbols

• Flow and miscellaneous symbols may indicate:– The flow of data and goods– The beginning or end of the flowchart– The location of a decision– An explanatory note

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart18 of

119

FLOWCHARTS

• Click on buttons below if you wish to review symbols in the various categories.

Input/OutputSymbols

ProcessingSymbols

StorageSymbols

Flow & Misc.Symbols

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart19 of

119

INPUT/OUTPUT SYMBOLS

• Document Symbol– Represents a document or report that is

prepared by hand or printed by a computer.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart20 of

119

INPUT/OUTPUT SYMBOLS

• Multiple Copies of One Document– Indicates multiple copies of a paper document

or report.– The document copies should be numbered in

the upper, right-hand corner.

23

1

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart21 of

119

INPUT/OUTPUT SYMBOLS

• Input/Output; Journal/Ledger– Can represent any input or output on a

program flowchart.– Also represents accounting journals or

ledgers in a document flowchart.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart22 of

119

INPUT/OUTPUT SYMBOLS

• Display– Represents information displayed by an

online output device such as a terminal, monitor, or screen.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart23 of

119

INPUT/OUTPUT SYMBOLS

• Online Keying– Represents data entry by an online device

such as a terminal or personal computer.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart24 of

119

INPUT/OUTPUT SYMBOLS

• Terminal or Personal Computer– Combines the display and online keying

symbols to represent terminals and personal computers.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart25 of

119

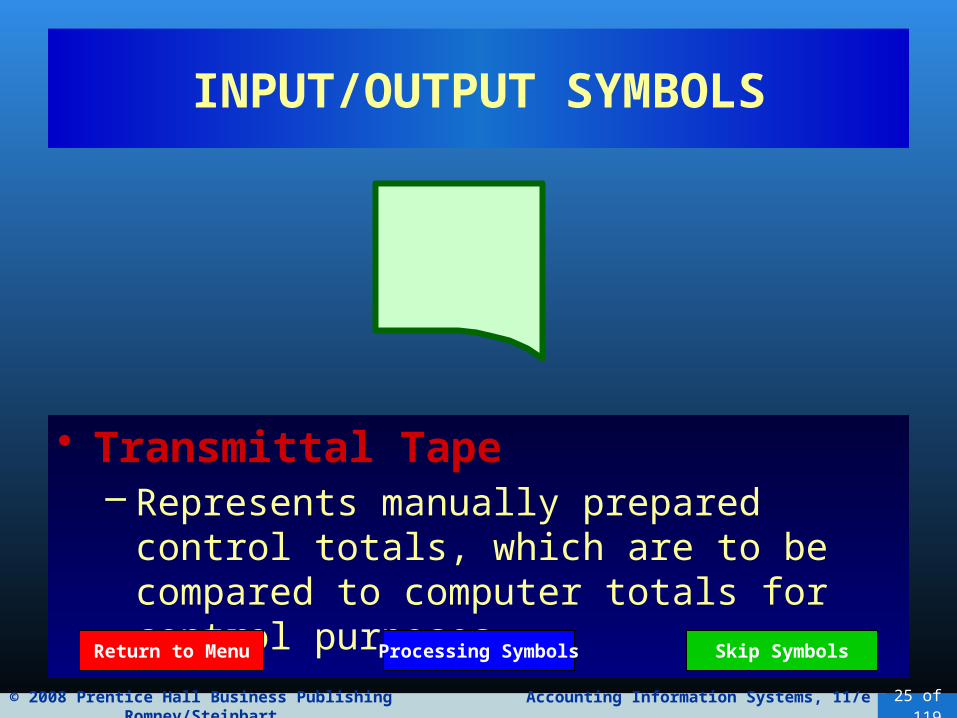

INPUT/OUTPUT SYMBOLS

• Transmittal Tape– Represents manually prepared control totals,

which are to be compared to computer totals for control purposes.

Return to Menu Processing Symbols Skip Symbols

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart26 of

119

PROCESSING SYMBOLS

• Computer Processing– Represents a process performed by a

computer, which usually results in a change in data or information.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart27 of

119

PROCESSING SYMBOLS

• Manual Operation– Represents a processing operation that is

performed manually.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart28 of

119

PROCESSING SYMBOLS

• Auxiliary Operation– Represents a processing operation carried

out by a device other than a computer, e.g., an optical character scanner.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart29 of

119

PROCESSING SYMBOLS

• Off-line Keying Operation– Represents an operation that uses an off-line

keying device, such as a cash register or keying to a disk.

Return to Menu Skip SymbolsStorage Symbols

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart30 of

119

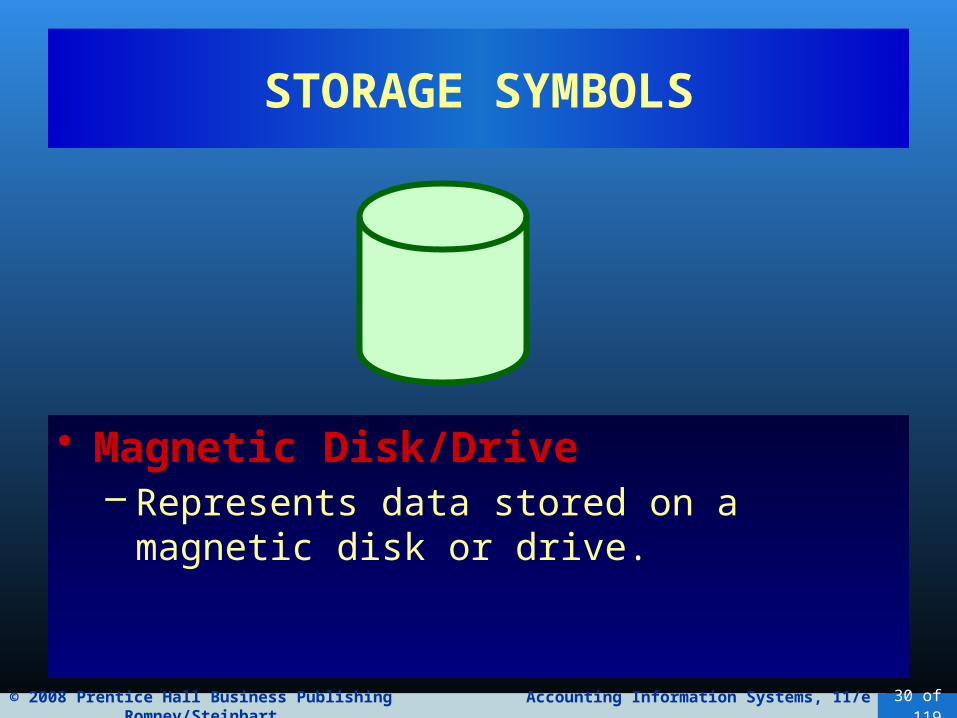

STORAGE SYMBOLS

• Magnetic Disk/Drive– Represents data stored on a magnetic disk or

drive.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart31 of

119

STORAGE SYMBOLS

• Magnetic Tape– Represents data stored on a magnetic tape.– Sometimes represents transaction files.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart32 of

119

STORAGE SYMBOLS

• File– Represents a file of documents that are manually

stored and retrieved.– Letter indicates the ordering sequence:

• A = Alphabetic order• D = Date order• N = Numeric order

A

Return to Menu Skip SymbolsFlow/Misc. Symbols

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart33 of

119

FLOW AND MISCELLANEOUS SYMBOLS

• Document or Processing Flow– Represents the direction of processing or

document flow.– Normal flow is top to bottom and left to right.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart34 of

119

FLOW AND MISCELLANEOUS SYMBOLS

• Data/Information Flow– Represents the direction of data/information

flow.– Often used to show data being copied from

one document to another.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart35 of

119

FLOW AND MISCELLANEOUS SYMBOLS

• Communication Link– Represents the transmission of data from one

location to another via communication lines.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart36 of

119

FLOW AND MISCELLANEOUS SYMBOLS

• On-page connector– Connects processing from one location to

another on the same page.– Used to avoid crisscrossing lines.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart37 of

119

FLOW AND MISCELLANEOUS SYMBOLS

• Off-page Connector– Connects the processing flow between two

different pages.– Signals the exit from one page and the

corresponding entrance on another page.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart38 of

119

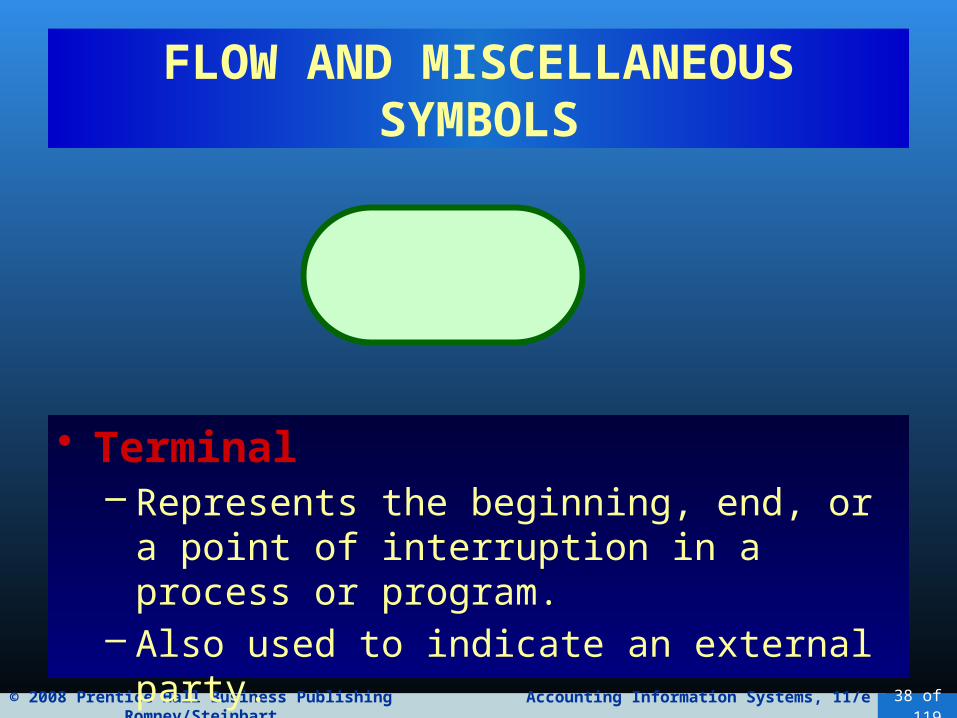

FLOW AND MISCELLANEOUS SYMBOLS

• Terminal– Represents the beginning, end, or a point of

interruption in a process or program.– Also used to indicate an external party.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart39 of

119

FLOW AND MISCELLANEOUS SYMBOLS

• Decision– Represents a decision-making step.– Used in a program flowchart to show

branching to alternate paths.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart40 of

119

FLOW AND MISCELLANEOUS SYMBOLS

• Annotation– Provides for the addition of descriptive

comments or explanatory notes as clarification.

Return to Menu Continue

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart41 of

119

TRIVIA 1

• Which man is credited with coining the term 'artificial intelligence' in 1955 and is considered one of the early pioneers in the field?

• Senator Joseph McCarthy

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart42 of

119

DOCUMENT FLOWCHARTS

• A document flowchart shows the flow of documents and information among areas of responsibility in an organization.

• These flowcharts trace a document from cradle to grave and show:– Where a document comes from– Where it’s distributed– How it’s used– It’s ultimate disposition– Everything that happens as it flows through the

system

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart43 of

119

DOCUMENT FLOWCHARTS

• Internal control flowcharts are document flowcharts used to evaluate the adequacy of internal controls, such as segregation of duties or internal checks.

• They can reveal weaknesses or inefficiencies such as:– Inadequate communication flows– Unnecessarily complex document flows– Procedures that cause wasteful delays

• Document flowcharts are also prepared in the system design process.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart44 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

• Let’s step through some guidelines for preparing flowcharts:– As with DFDs, you can’t effectively prepare a

flowchart if you don’t understand the system, so:• Interview users, developers, auditors, and

management• Administer questionnaires• Read through narratives• Walk through systems transactions

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart45 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

– Identify:• Entities to be flowcharted, e.g., departments,

functions, external parties (the parties who “do” things in the story)

• Documents or information flows• Processes

– As you read through a narrative, you may want to mark the preceding items with different shapes (e.g., drawing a rectangle around entities, circling documents, etc.).

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart46 of

119

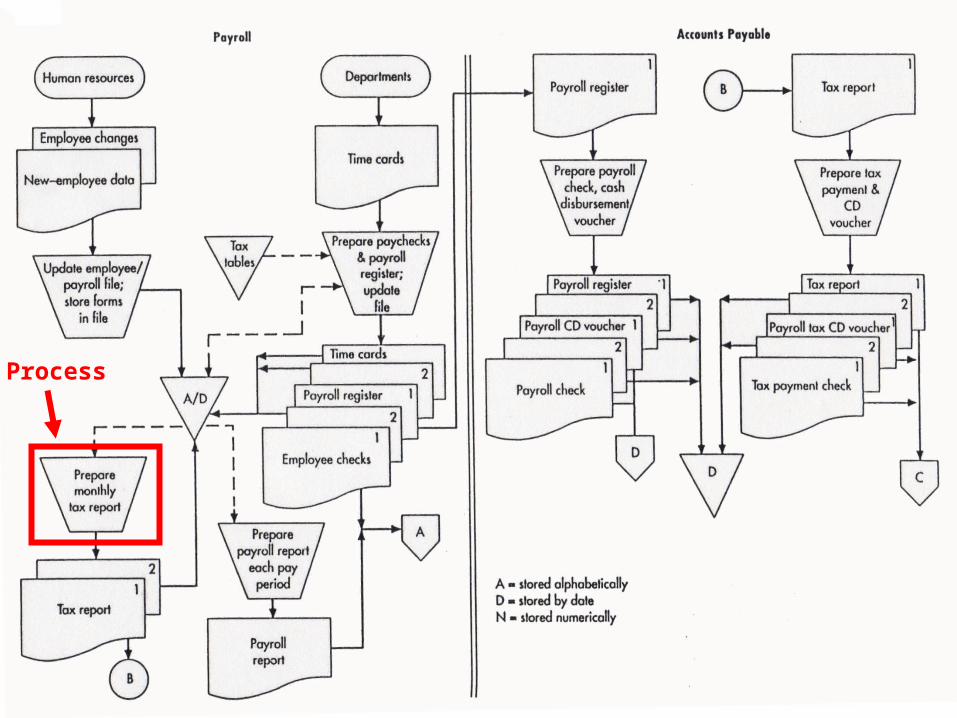

This is part of the document flowchart from Figure 3-9 in your textbook.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart47 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

–Use separate columns for the activity of each entity.• Example: If there are three different

departments or functions that “do” things in the narrative, there would be three columns on the flowchart.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart48 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

– Flowchart the normal course of operations, and identify exceptions with annotations.

– As much as possible, the flow should go from top to bottom and left to right.

– Use standard flowcharting symbols, and draw with a template or computer.

– Clearly label all symbols. Use annotations if necessary to provide adequate explanation.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart49 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

– Give the flowchart a clear beginning and ending.• Show where each document originated and its final

disposition.– One approach you can use is to read through

the narrative and for each step define:• What was (were) the input(s)• What process was carried out• What was (were) the output(s)

– Note on the next slide that the flow sequence is input—process—output.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart50 of

119

What are the entities in this flowchart?

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart51 of

119

Identifies where input is coming from

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart52 of

119

Inputs

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart53 of

119

Process

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart54 of

119

Output tostorage

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart55 of

119

Input fornext

process

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart56 of

119

Process

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart57 of

119

Output

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart58 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

– Every manual process should have at least one input and at least one output.

– Show all data entered into or retrieved from a computer file as passing through a process first.

– Do not show process symbols for:• Forwarding a document to another entity• Filing a document

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart59 of

119

Forwardinga document

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart60 of

119

Filinga document

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart61 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

–Do not connect two documents except when forwarding to another column.• When a document is forwarded, show it in

both locations.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart62 of

119

Show forwarded document in both

locations

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart63 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

–When using multiple copies of a document, place document numbers in the upper, right-hand corner.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart64 of

119

What happens to the document numbers as the documents

move to other locations?

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart65 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

–Show on-page connectors and label them clearly to avoid excess flow lines.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart66 of

119

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart67 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

–Use off-page connectors if the flow goes to another page.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart68 of

119

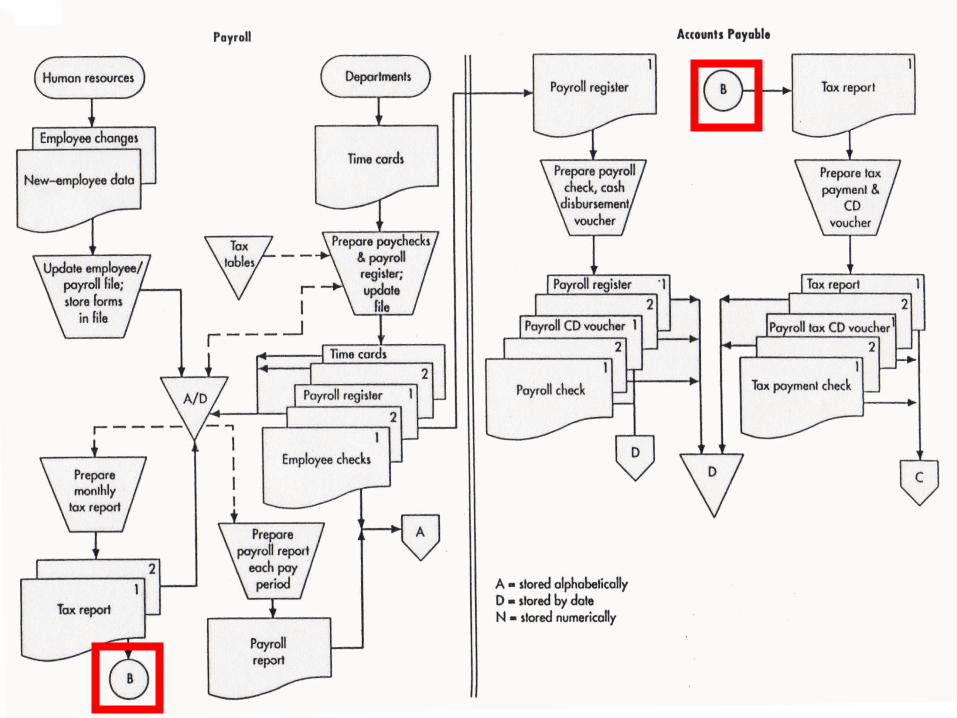

Are there other off-page connectors on

this flowchart?

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart69 of

119

GUIDELINES FOR PREPARING FLOWCHARTS

– If a flowchart takes more than one page, label the pages as 1 of 5, 2 of 5, 3 of 5, etc.

– Show documents or reports first in the column where they are created.

– Start with a rough draft; then redesign to avoid clutter and crossed lines.

– Verify the accuracy of your flowchart by reviewing it with users, etc.

– Place the flowchart name, the date, and the preparer’s name on each page of the final copy.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart70 of

119

TRIVIA

• What was the first computer virus? • Movie :

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart71 of

119

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 72 of 160

C HAPTER 10

The Revenue Cycle:

Sales to Cash Collections

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 73 of 161

INTRODUCTION

• In this chapter, we’ll look at:• Capturing and processing data.• Storing and organizing the data for decisions.• Providing controls to safeguard resources

(including data).

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 74 of 161

• The revenue cycle is a recurring set of business activities and related information processing operations associated with:– Providing goods and services to customers– Collecting their cash payments

• The primary external exchange of information is with customers.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 75 of 161

– What are the basic business activities and data processing operations that are performed in the revenue cycle?

– What decisions need to be made in the revenue cycle, and what information is needed to make these decisions?

– What are the major threats in the revenue cycle and the controls related to those threats?

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 76 of 161

• Information about revenue cycle activities flows to other accounting cycles, e.g.:– The expenditure and production cycles

• Receive information about sales transactions so they’ll know when to initiate the purchase or production of more inventory.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 77 of 161

• Information about revenue cycle activities flows to other accounting cycles, e.g.:– The expenditure and production cycles– The human resources/payroll cycle

• Uses information about sales to calculate commissions and bonuses.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 78 of 161

• Information about revenue cycle activities flows to other accounting cycles, e.g.:– The expenditure and production cycles– The human resources/payroll cycle– The general ledger and reporting function

• Uses information produced by the revenue cycle in preparing financial statements and performance reports.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart79 of

119

General Ledgerand Reporting

System

RevenueCycle

ExpenditureCycle

ProductionCycle

Human Res./Payroll Cycle

FinancingCycle

• The Revenue Cycle– Gets finished

goods from the production cycle.

– Provides funds to the financing cycle.

– Provides data to the general ledger and reporting system.

Finished Goods

FundsD

ata

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 80 of 161

• The primary objective of the revenue cycle:– Provide the right product in the right place at

the right time for the right price.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 81 of 161

• Decisions that must be made:– Should we customize products?– How much inventory should we carry and

where?– How should we deliver our product?– How should we price our product?– Should we give customers credit? If so, how

much and on what terms?– How can we process payments to maximize

cash flow?

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 82 of 161

• Management also has to evaluate the efficiency and effectiveness of revenue cycle processes:– Requires data about:

• Events that occur.• Resources used.• Agents who participate.

– The data needs to be accurate, reliable, and timely.

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 83 of 161

REVENUE CYCLE BUSINESS ACTIVITIES

• Four basic business activities are performed in the revenue cycle:– Sales order entry– Shipping– Billing– Cash collection

© 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/Steinbart 84 of 161

REVENUE CYCLE BUSINESS ACTIVITIES

• Four basic business activities are performed in the revenue cycle:– Sales order entry– Shipping– Billing– Cash collection