Embed Size (px)

Citation preview

N Wh t?Now What?

RAPAPORTInternational Diamond Conference 2009

September 10, 2009

A t ti b

1

A presentation by Christopher Ellis, President

2

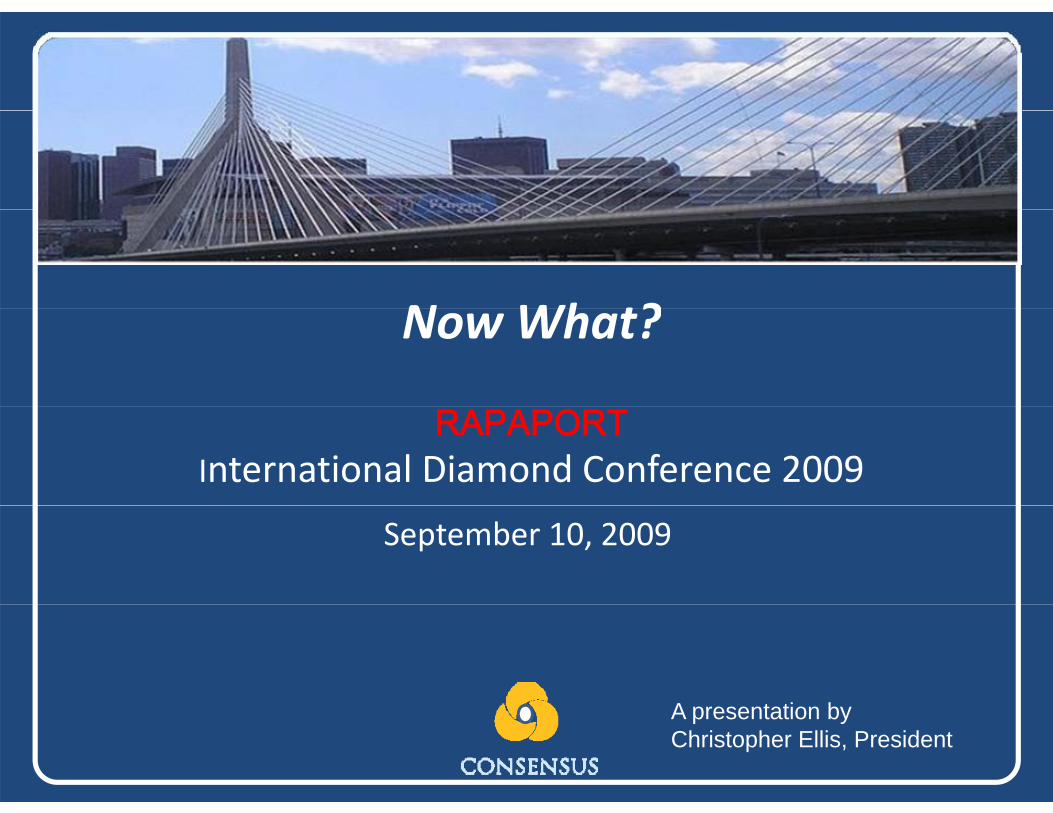

3

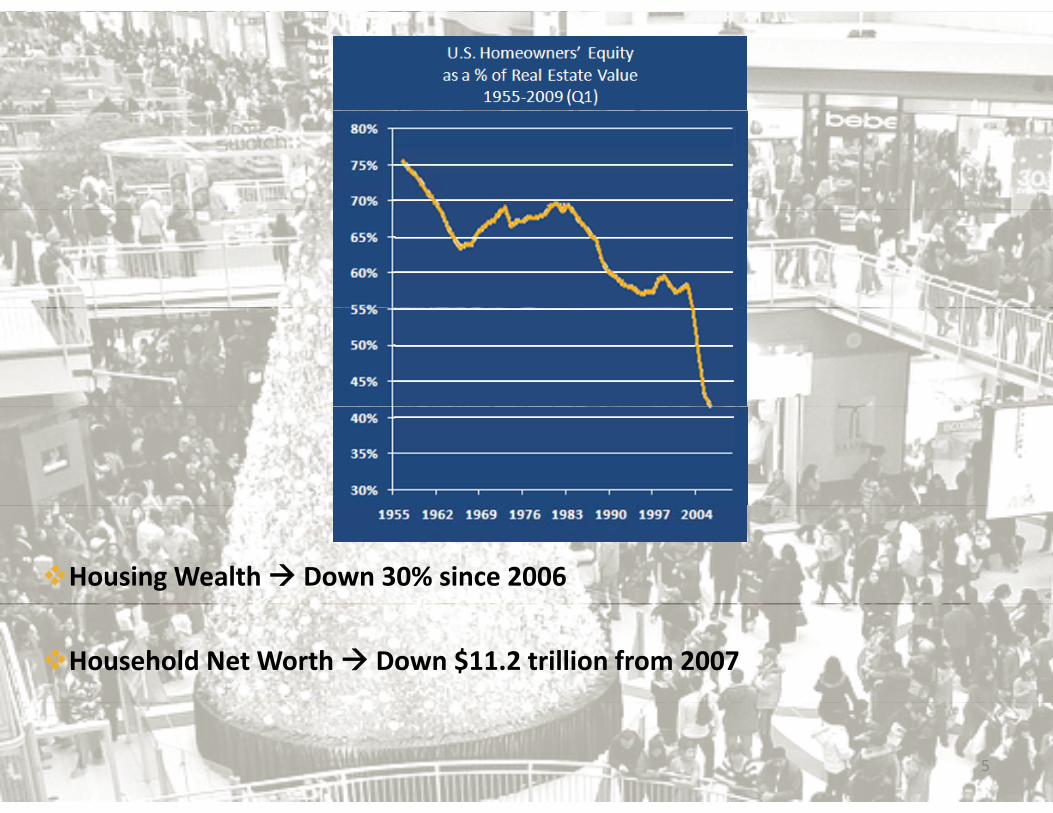

Housing Wealth Down 30% since 2006

4

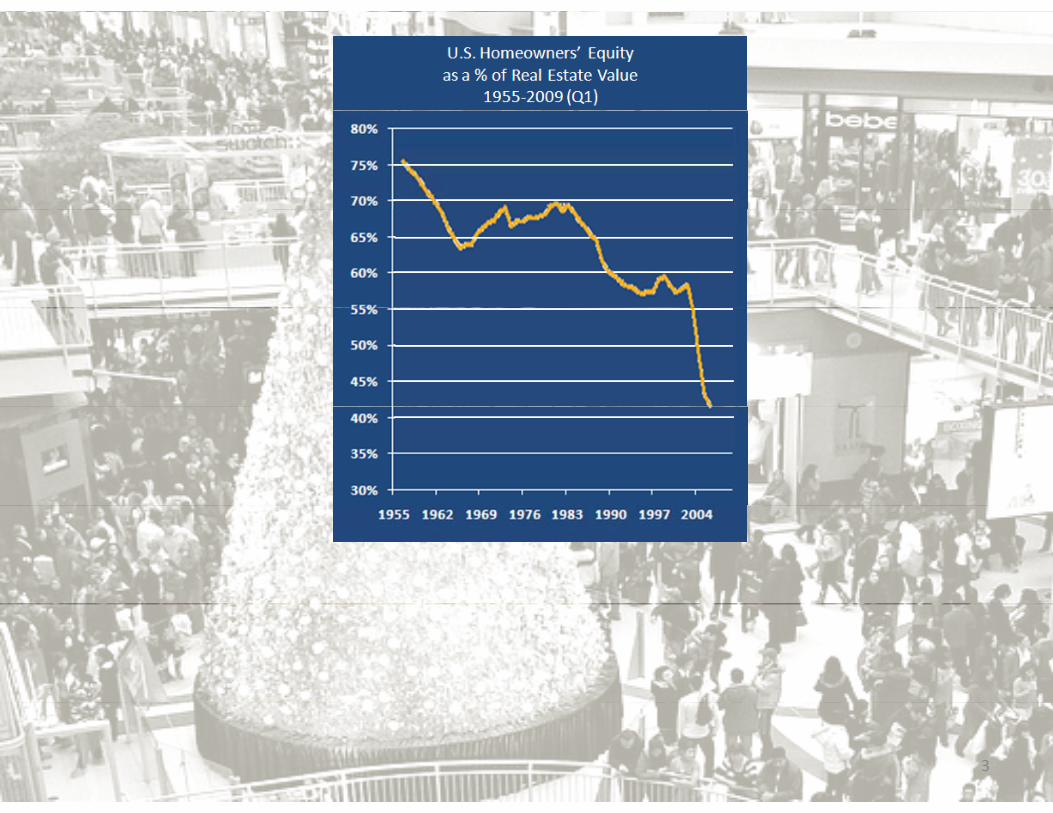

Housing Wealth Down 30% since 2006

Household Net Worth Down $11.2 trillion from 2007

5

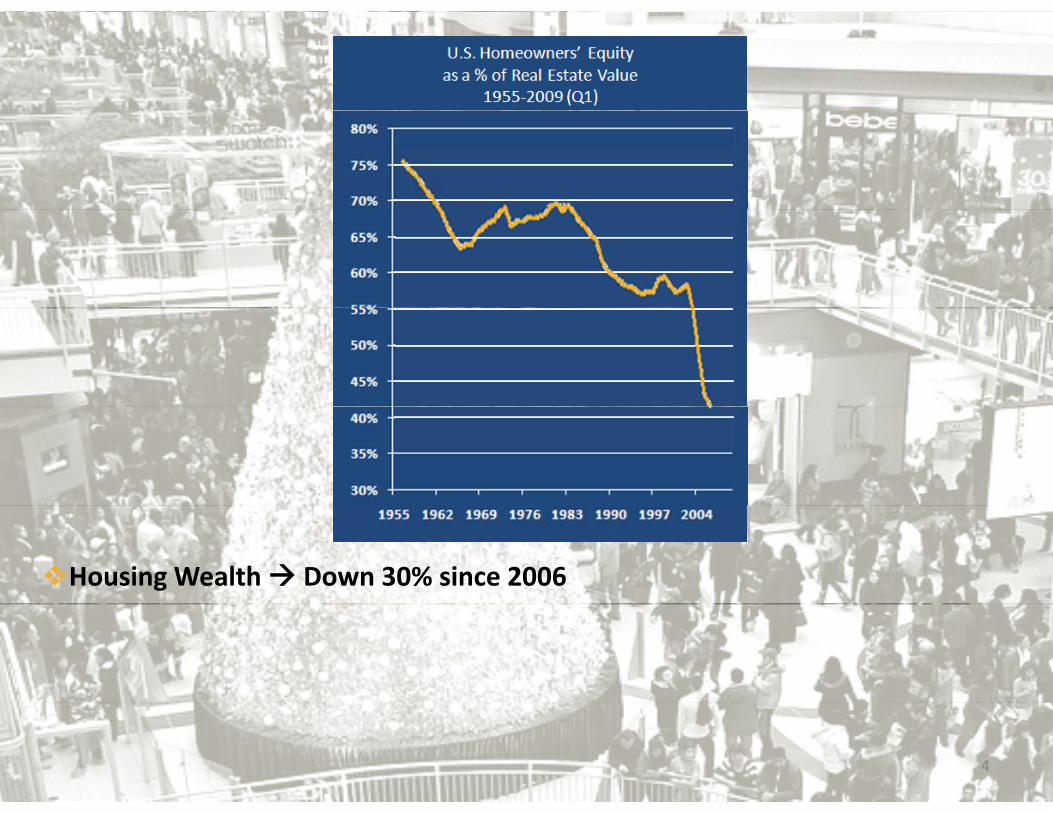

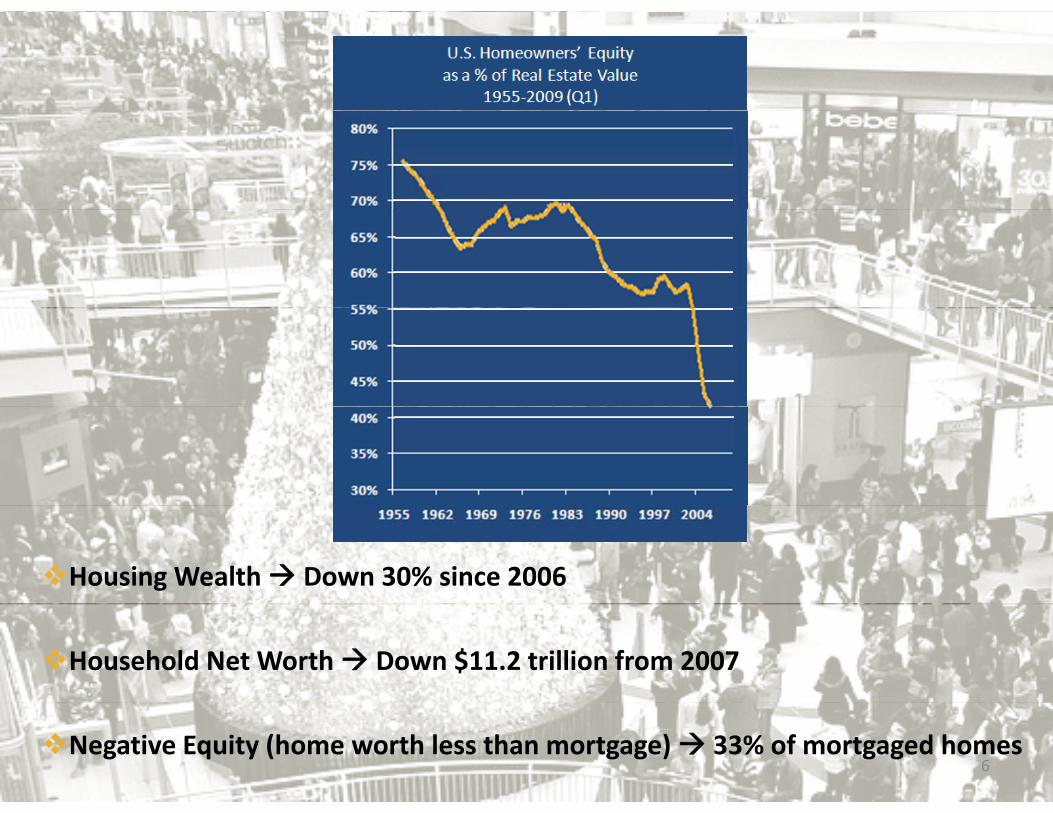

Housing Wealth Down 30% since 2006

Household Net Worth Down $11.2 trillion from 2007

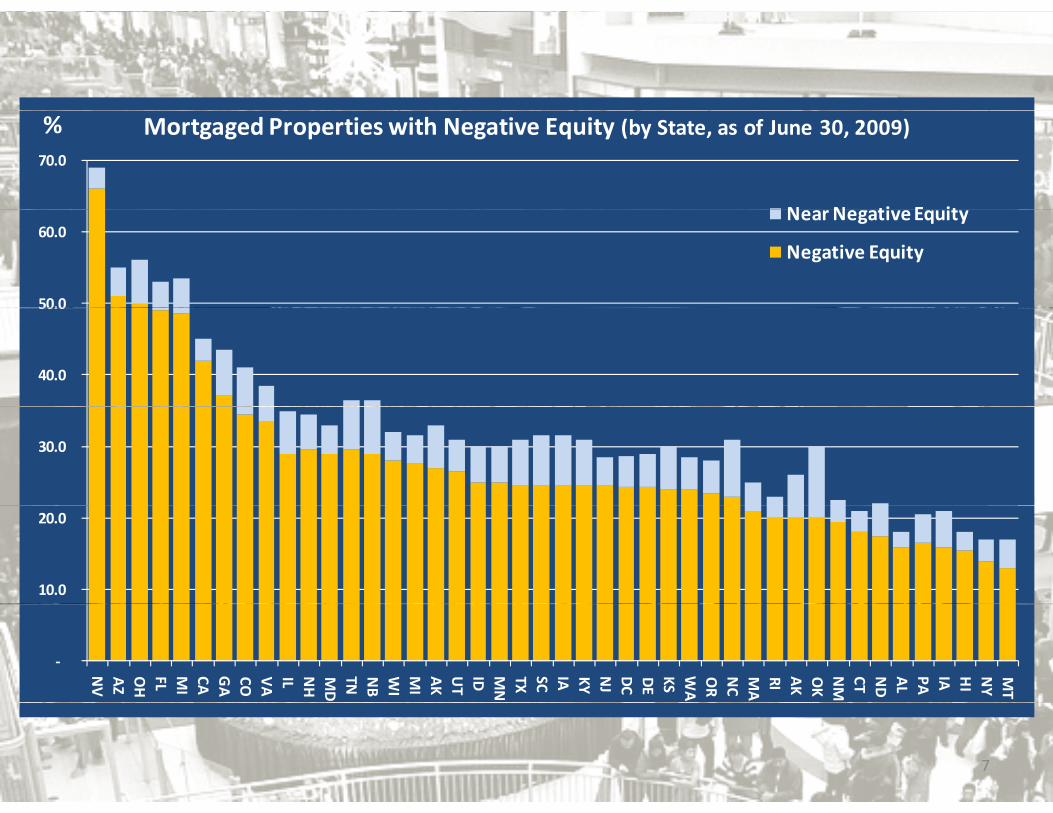

6Negative Equity (home worth less than mortgage) 33% of mortgaged homes

(as of June 30, 2009)70.0

Mortgaged Properties with Negative Equity (by State, as of June 30, 2009)

N N ti E it

%

50.0

60.0 Near Negative Equity

Negative Equity

40.0

50.0

30.0

10.0

20.0

‐

NV

AZ

OH

FL MI

CA GA

CO VA

IL NH

MD

TN NB

WI

MI

AK

UT

ID MN

TX SC IA KY NJ

DC DE

KS WA

OR

NC

MA

RI AK OK

NM

CT ND

AL

PA IA HI

NY

MT

7

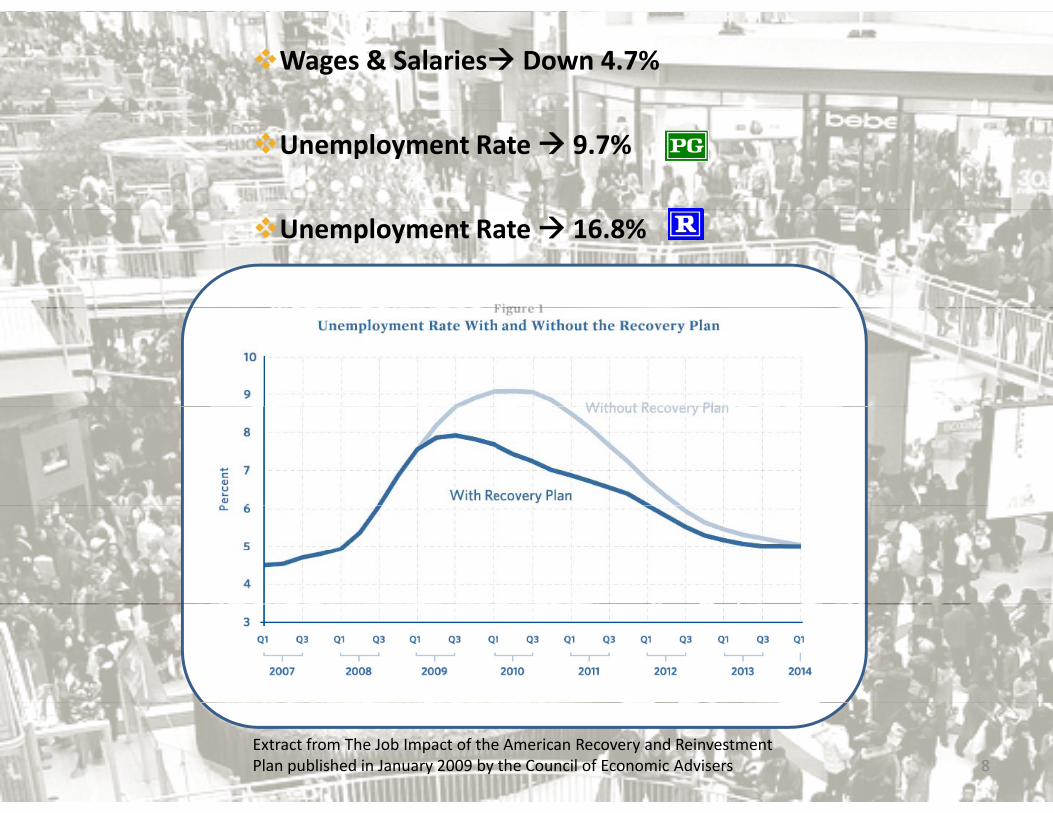

Wages & Salaries Down 4.7%

Unemployment Rate 9.7%

Unemployment Rate 16.8%

8Extract from The Job Impact of the American Recovery and Reinvestment Plan published in January 2009 by the Council of Economic Advisers

Retailers

9

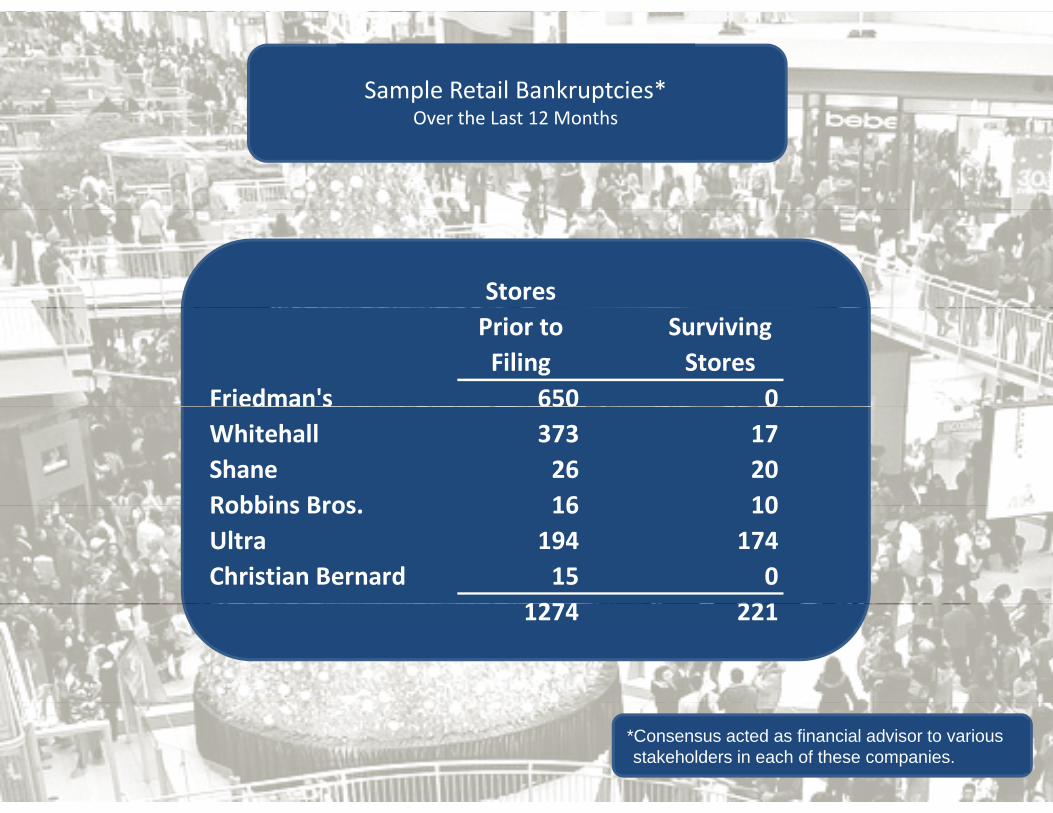

Sample Retail Bankruptcies*h hOver the Last 12 Months

Stores Prior to Filing

Surviving Stores

Friedman's 650 0ed a s 650 0Whitehall 373 17Shane 26 20Robbins Bros 16 10Robbins Bros. 16 10Ultra 194 174Christian Bernard 15 0

1274 2211274 221

10

*Consensus acted as financial advisor to various stakeholders in each of these companies.

Sales Change vs. Prior Year for Selected Public Specialty Jewelers

40%

20%

30%

0%

10%Zale

Tiffany

‐20%

‐10%Tiffany

Signet

Blue Nile

‐40%

‐30%

Q1 '07

Q2 Q3 Q4 Q1 '08

Q2 Q3 Q4 Q1 '09

Q2

11

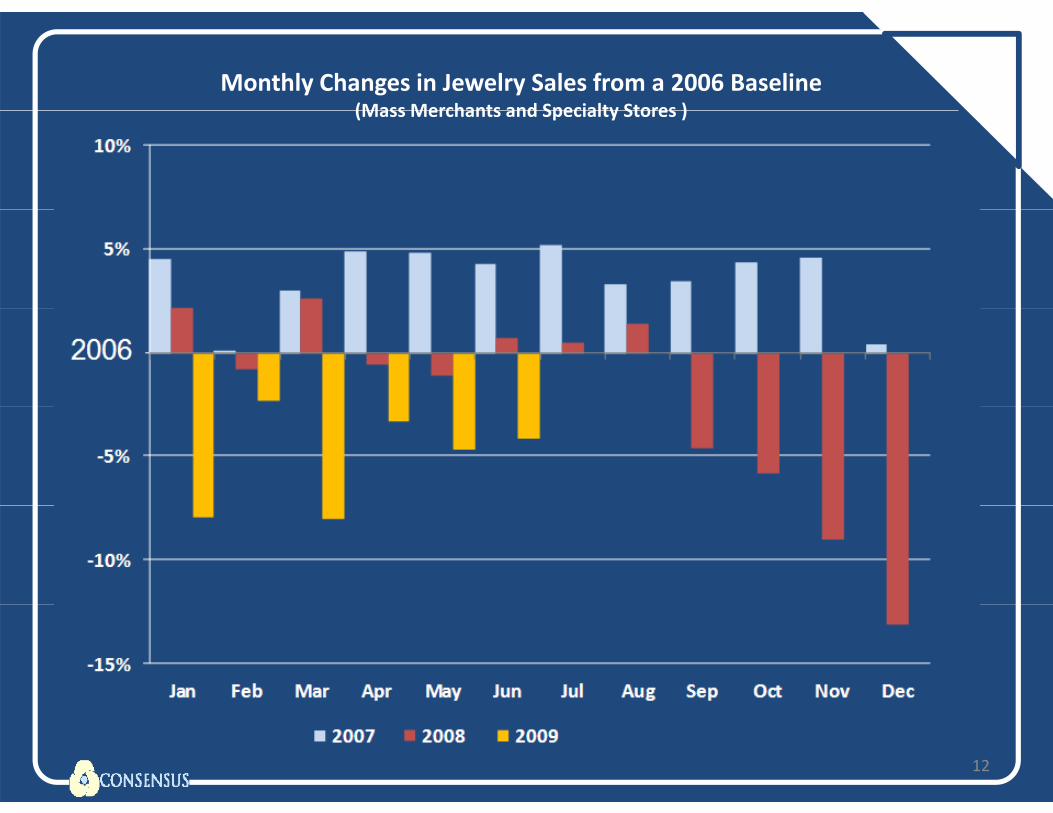

Monthly Changes in Jewelry Sales from a 2006 Baseline(Mass Merchants and Specialty Stores )(Mass Merchants and Specialty Stores )

12

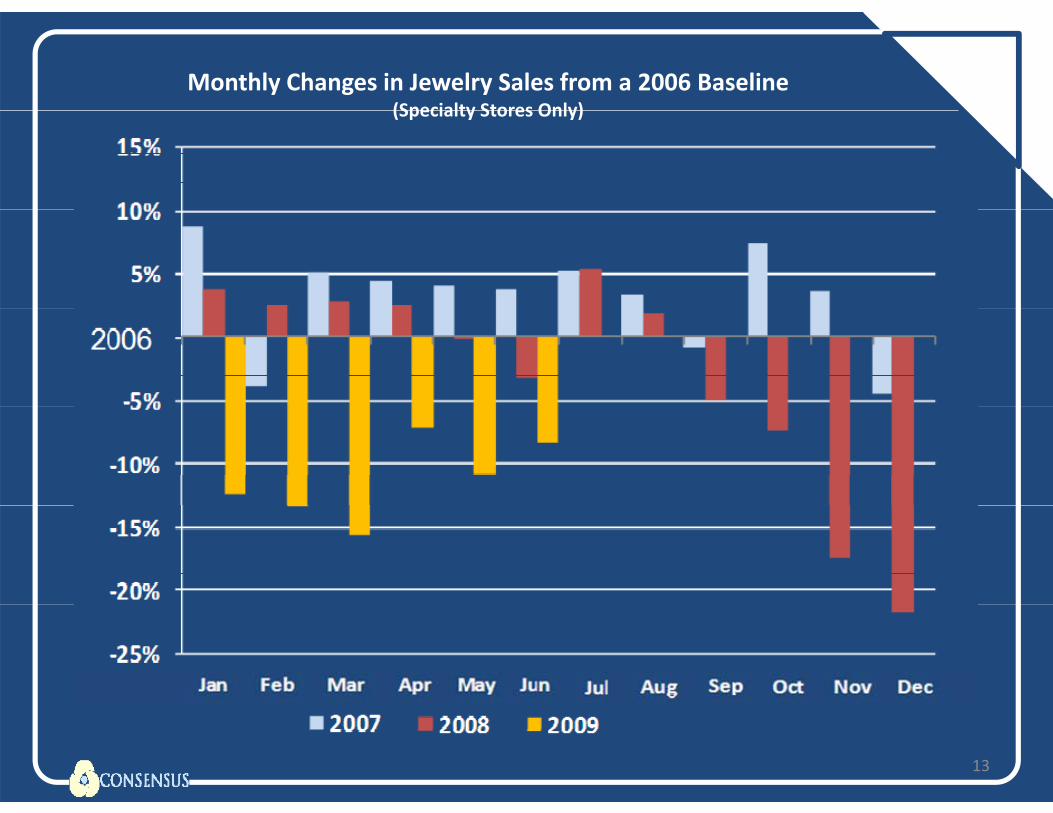

Monthly Changes in Jewelry Sales from a 2006 Baseline(Specialty Stores Only)(Specialty Stores Only)

13

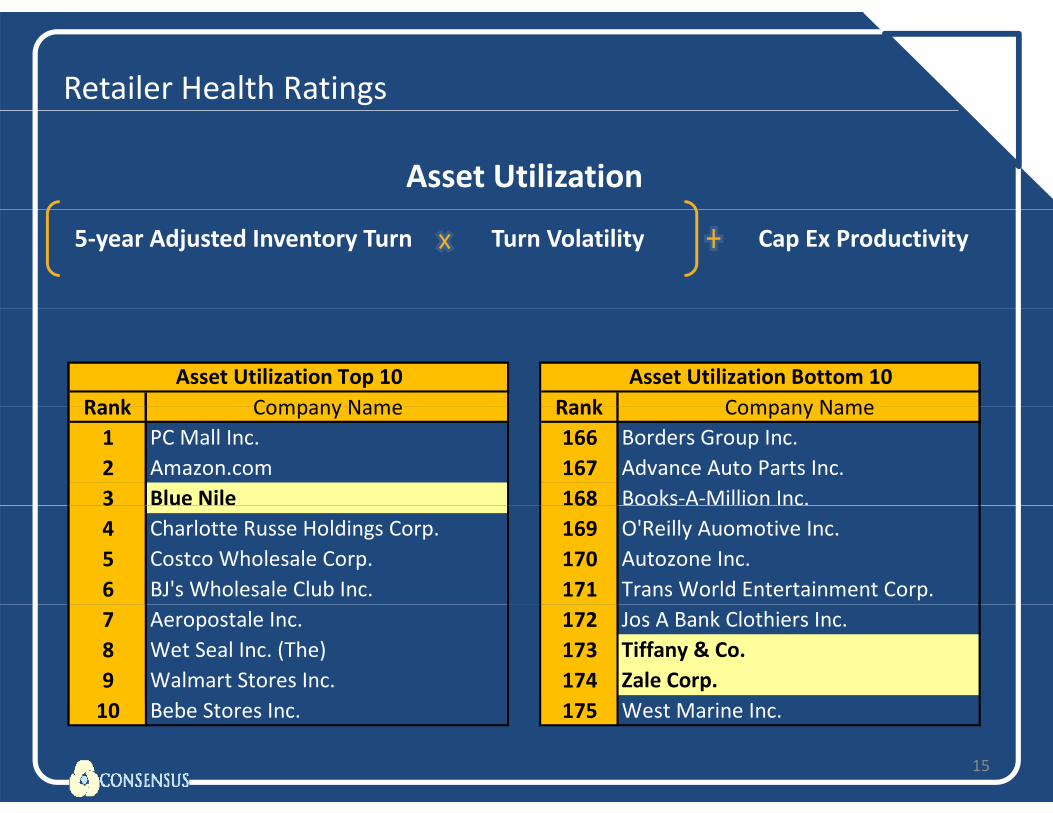

Consensus l l hRetailer Health Ratings

Healthy Growth Asset Utilization Pricing Power Balance Sheet Risk

Approximately 175 Publicly Traded Retailers

14

Retailer Health Ratings

Asset Utilization

5‐year Adjusted Inventory Turn Turn Volatility Cap Ex Productivity

Rank Company Name Rank Company NameAsset Utilization Top 10 Asset Utilization Bottom 10

Rank Company Name Rank Company Name1 PC Mall Inc. 166 Borders Group Inc.2 Amazon.com 167 Advance Auto Parts Inc.3 Blue Nile 168 Books‐A‐Million Inc.3 684 Charlotte Russe Holdings Corp. 169 O'Reilly Auomotive Inc.5 Costco Wholesale Corp. 170 Autozone Inc.6 BJ's Wholesale Club Inc. 171 Trans World Entertainment Corp.7 Aeropostale Inc. 172 Jos A Bank Clothiers Inc.8 Wet Seal Inc. (The) 173 Tiffany & Co.9 Walmart Stores Inc. 174 Zale Corp.

b S i

15

10 Bebe Stores Inc. 175 West Marine Inc.

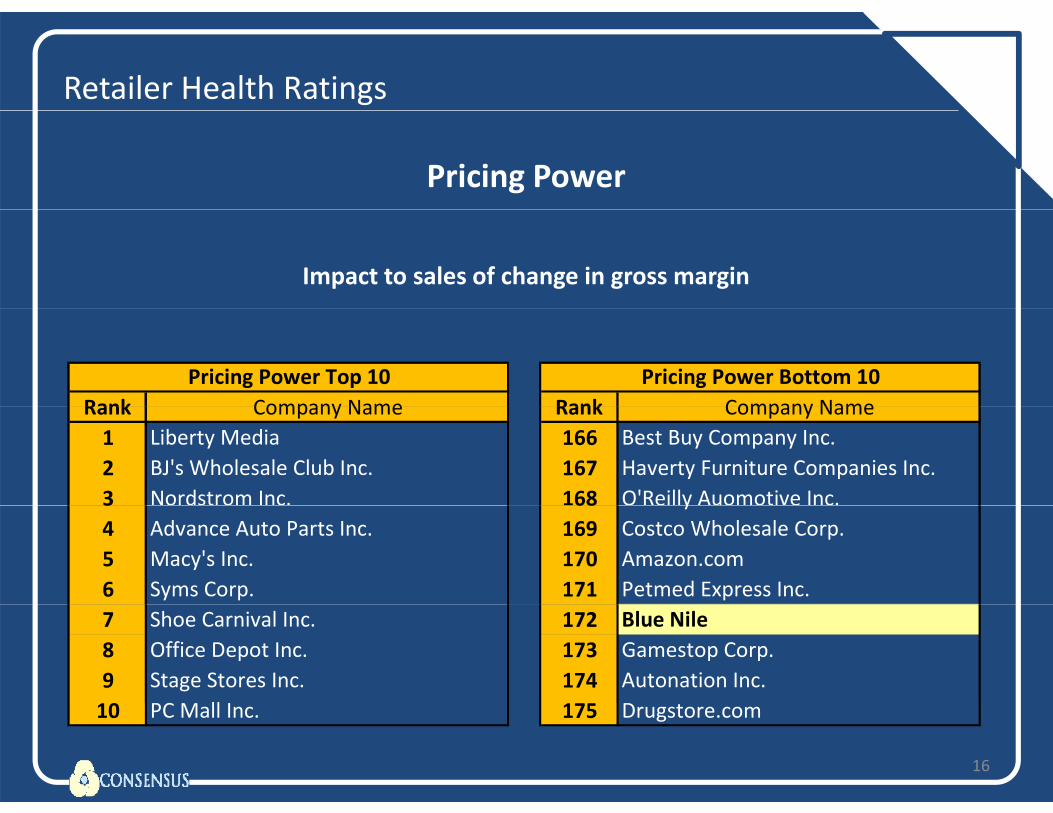

Retailer Health Ratings

Pricing Power

Impact to sales of change in gross margin

Rank Company Name Rank Company NamePricing Power Top 10 Pricing Power Bottom 10

Rank Company Name Rank Company Name1 Liberty Media 166 Best Buy Company Inc.2 BJ's Wholesale Club Inc. 167 Haverty Furniture Companies Inc.3 Nordstrom Inc. 168 O'Reilly Auomotive Inc.3 68 y4 Advance Auto Parts Inc. 169 Costco Wholesale Corp.5 Macy's Inc. 170 Amazon.com6 Syms Corp. 171 Petmed Express Inc.7 Shoe Carnival Inc. 172 Blue Nile8 Office Depot Inc. 173 Gamestop Corp.9 Stage Stores Inc. 174 Autonation Inc.

C ll

16

10 PC Mall Inc. 175 Drugstore.com

How to Survive & Thrive: Thoughts for Independents

17

How to Survive & Thrive: Thoughts for Independents

R i Thi ki• Revise Thinking

18

How to Survive & Thrive: Thoughts for Independents

R i Thi ki• Revise Thinking

• Clean Up the Balance Sheet

19

How to Survive & Thrive: Thoughts for Independents

R i Thi ki• Revise Thinking

• Clean Up the Balance Sheet

• Streamline and Spice Up Offerings

20

How to Survive & Thrive: Thoughts for Independents

R i Thi ki• Revise Thinking

• Clean Up the Balance Sheet

• Streamline and Spice Up Offerings

• Plan/Budget for Sales Levels Below Last Year

21

How to Survive & Thrive: Thoughts for Independents

R i Thi ki• Revise Thinking

• Clean Up the Balance Sheet

• Streamline and Spice Up Offerings

• Plan/Budget for Sales Levels Below Last Year

• Whatever You Have, Spend Less

22

N Wh t?Now What?

RAPAPORTInternational Diamond Conference 2009

September 10, 2009

A t ti b

23

A presentation by Christopher Ellis, President