Embed Size (px)

Citation preview

Northland Power Investor PresentationJune 2018

NPI.TO

1

Forward-Looking Statements Disclaimer

This written and accompanying oral presentation contains certain forward-looking statements which areprovided for the purpose of presenting information about management’s current expectations and plans.Readers are cautioned that such statements may not be appropriate for other purposes. Forward-lookingstatements include statements that are predictive in nature, depend upon or refer to future events orconditions, or include words such as “expects”, “anticipates”, “plans”, “believes”, “estimates”, “intends”,“targets”, “projects”, “forecasts” or negative versions thereof and other similar expressions, or future orconditional verbs such as “may”, “will”, “should”, “would” and “could”. These statements may include,without limitation, statements regarding future adjusted EBITDA or adjusted EBITDA, cash flows anddividend payments, the construction, completion, attainment of commercial operations, cost and output ofdevelopment projects, plans for raising capital, and the future operations, business, financial condition,financial results, priorities, ongoing objectives, strategies and outlook of Northland and its subsidiaries. Thisinformation is based upon certain material factors or assumptions that were applied in developing theforward-looking statements, including the design specifications of development projects, the provisions ofcontracts to which Northland or a subsidiary is a party, management’s current plans, its perception ofhistorical trends, current conditions and expected future developments, as well as other factors that arebelieved to be appropriate in the circumstances.

2

Over 30 years of successfully developing, constructing and operating independent power projects

Well-diversified, 2,458 MW (gross) modern fleet of high-quality assets

Over $10 billion of assets constructed since inception and currently under construction

Overall availability of 95% across 27 operating facilities

550+ MW in development (252 MW Deutsche Bucht in-construction; 300 MW of grid allocation secured in Taiwan)

Enterprise value of approximately $12 billion¹

Significant development opportunities across multiple markets and technologies

Management alignment through a 34% ownership interest

Management experience - Combined over 200 years of power industry experience

Northland Overview

1987-Present

Over 30 Years of Excellence1. As at May 11, 2018

3

1,165%

0

500

1,000

1,500

2,000

2,500

3,000

0%

200%

400%

600%

800%

1,000%

1,200%

1,400%

Renewables (MW)

Clean Gas and Biomass (MW)

Northland Returns (%)

Evolution of Northland

2009 20181997

Founding Merger

1987Private Developer

Publically Listed Income Fund

Private Entity Public Entity

Income Fund IPO

CurrentIncome Fund PhaseEarly Growth Phase

International expansion; Leverage greenfield expertise

into new markets

Canada-wide expansion; new technologies and larger-scale projects

Power generation projects in Ontario, Canada

1. Shareholder returns include capital appreciation and dividend reinvestment

Total GrossCapacity (MW)

2,458 MW

July 16, 2009Merger of NPI

and Income Trust

Northland has grown from a local Canadian developer to an internationally renowned Independent Power Producer

Total Returns1 (%)

April 15, 1997Northland IPO

4

Northland’s Asset Diversification

Under constructionIn operation

Technology: Operating1 Construction1

Thermal 1,001 MW -

Wind 1,326 MW 252 MW

Solar 131 MW -

Total (Gross) 2,458 MW 252 MW

Total (Net)2 2,029 MW 252 MW

1. As of December 31, 20172. Represents Northland’s net economic interest

Geography: Operating1 Construction1

Canada 1,526 MW -

Netherlands 600 MW -

Germany 332 MW 252 MW

Total (Gross) 2,458 MW 252 MW

Total (Net)2 2,029 MW 252 MW

5

Northland’s Successes in the Past Year

FY 2017: Adj. EBITDA of $765 million, a 22% increase over 2016; and Free Cash Flow per share of $1.46, a 4% increase over 2016

FY 2017: Operating income of $632 million, a 24% increase over 2016 Q1 2018: Adj. EBITDA of $290M (47% ) and Free Cash Flow per share of $0.84 (250% ) Increased common share dividend by 11% to $1.20 per share as of December 2017

Operating generating capacity increased to 2,029 MW (net), a 46% increase or 2,458 MW (gross), a 61% increase over 2016

Maintained operational excellence across 27 facilities Continued health and safety track record of no lost time incidents Northland Europe internalized management for strategic and financial reasons

European offshore wind projects totaling €4B achieved project completion:o 600 MW (net 360 MW) Gemini reached commercial operations on Apr. 2017o 332 MW (net 282 MW) Nordsee One reached commercial operations on Dec. 2017

Deutsche Bucht (DeBu) project achieved Financial Close and construction is underway

Secured 300 MW (net 180 MW) of grid allocation under FIT for Taiwan project (Hai Long 2) Advanced and positioned other projects in the development pipeline Established strong international presence with our head office in Toronto plus five

international locations

$ Results

Development

Construction

Operations

6

Gas & Biomass

25%

Onshore Wind

5%

Solar10%

Offshore Wind60%

Gas & Biomass,

80%

Onshore Wind, 20%

Northland’s Strong and Growing Results

Gas & Biomass,

50%

Onshore Wind, 15%

Offshore Wind, 30%

Solar, 5%

2012¹ 2017² Annual Growth

Assets $2.5 B $10.2 B 32%

Enterprise Value $3.7 B $11.9 B 26%

Market Capitalization $2.2 B $4.1 B 14%

Operating Capacity (Gross) 1,242 MW 2,458 MW 15%

Operating Capacity (Net) 1,005 MW 2,029 MW 15%

Share Price $18.67 $23.35 11%³

# Corporate Offices 1 5 38%

1. As at December 31, 20122. As at December 31, 20173. This number represents the 5-Year Total Shareholder Return (includes capital appreciation and dividend reinvestment)

Operating Capacity by Technology (Net MW)Adjusted EBITDA by Technology ($M)

Gas & Biomass,

75%

Onshore Wind, 25%

2012A 2018E

Since 2012, Adjusted EBITDA has substantially increased due to technological diversification and regional expansion

2012A 2018E

7

Total Shareholder Returns

6%

21%

11%14%

-20%

-10%

0%

10%

20%

30%

40%

YTD 3-year 5-year 10-year

Peer Group*

S&P/TSX Capped Utilities Index

Northland Power

3-Year 5-Year 10-YearYTD

Total Shareholder Returns

Northland has consistently delivered superior returns to shareholders over the years

* Includes Algonquin Power, Boralex, Brookfield Renewable, Capital Power, Innergex, TransAltaNote: Total return includes dividend plus appreciation over the specified period.Source: Bloomberg, May 11, 2018

8

Note: The above chart is illustrative of Management’s objectives. They are based upon Northland’s operating facilities continuing to perform in a manner consistent with operations in 2017, with additions to Adjusted EBITDA and Free Cash Flow from projects under construction and other adjustments resulting from power contract renewals primarily in Ontario as described in our MD&A and 2017 AIF. The illustrations do not constitute a financial forecast, projection or guidance and are based upon assumptions that are subject to change.

Continued Growth in Financial Results

Significant and visible growth in the future from projects in operationsand in construction

The following chart illustrates Northland’s growing Adjusted EBITDA and Free Cash Flow Per Share profile

Adjusted EBITDA Growth Free Cash Flow Per Share Growth

2012A 2014A 2016A 2018F 2020F 2012A 2014A 2016A 2018F 2020F

Growth ~200% Growth ~80%

9

World Class Offshore Wind Projects

1. Excludes the 17MW opportunity for two additional demonstration turbines utilizing suction bucket foundations. Final Investment Decision is subject to achieving certain development milestones

2. Awarded 300 MW grid allocation for 2024 COD

With the successful completion of Gemini and Nordsee One, Management is focused on construction of Deusche Bucht and development of Hai Long 2

Deutsche Bucht Hai Long 2

332 MW 85% Interest

COD Dec 2017

Gemini

252 MW1

100% Interest COD Late 2019

300 MW2

60% InterestCOD 2024

600 MW 60% InterestCOD Apr 2017

Nordsee One

10

Top Offshore Wind Projects in Operations

Current: Top 15 (Gross MW)

630600

576 573

504

402

332

LondonArray

Gemini Gwynt yMor

Race Bank GreaterGabbard

DudgeonEast

NordseeOne

2nd

15th

Gemini Project Snapshot

COD: • April 2017

Capacity: • 600 MW (gross)

Contract: • 15-year PPA with the Government of Netherlands

Type: • Offshore wind

Ownership: • Northland 60% • Siemens 20%

• Alte Leipziger & Hallesche 10%

• N.V. HVC 10%

Nordsee One Project Snapshot

COD: • December 2017

Capacity: • 332 MW (gross)

Contract: • Approx. 10-year PPA with the Government of Germany

Type: • Offshore wind

Ownership: • Northland 85%• Innogy 15%

11

Location North Sea, Germany

Capacity 252 MW1

Capital Cost €1.3 billion1

Northland Interest 100% (252 MW)

Power Contract 13y FIT subsidy under German REA

Ops & Maintenance MHI Vestas (~13y) – guarantees high op. availability

Commercial Ops Date End of 2019

Deutsche Bucht (DeBu) – Construction Update

Deutsche Bucht Construction Timeline

DeBu Offshore Wind Project

Aug 17 Jan 18 Jan 19 Dec 1920192018

TodayFin Close

Manufacturing

Foundations Installation

Cable Installation

Turbine Installation

Commercial Ops Date

• Monopile = 25%

• T. Pieces = 25%

• Cable = 5%

• Structural Design= 100%

• Electrical Design = 100%

• Offshore Substation = 33%

% Completion2

On-Time, On-Budget

Finish

1. Excludes the 17MW opportunity for two additional demonstration turbines utilizing suction bucket foundations. Final Investment Decision is subject to achieving certain development milestones

2. % completion with respect to manufacturing, transport and installation

12

Deutsche Bucht (DeBu) – Additional Facts

Grid Connection Borwin beta (AC/DC) Existing(TenneT (Utility)- Not Project’s Responsibility to Construct)

2) Van Oord EPCICable Supply & Install

Foundation Supply & Install

OSS Supply & Install

1) MHI Vestas33 Wind TurbinesSupply & Install

Deutsche Bucht Construction Structure (Two Contracts)

Northland continues to expand its leading European offshore wind platform

Capital deployment and returns consistent with Northland’s investment criteria

Opportunity to take advantage of lessons learnt from Gemini and Nordsee One while leveraging common infrastructure to generate operating synergies

Opportunity for two additional demonstration turbines utilizing suction bucket foundations

If built, additional yield of 17MW capacity, resulting in total project cost of €1.4 billion

Highlights

13

Northland Construction Track RecordProject Technology MW (gross) COD On/Ahead of Schedule Under Budget

Iroquois Falls Gas 120 1997

Mont Miller Onshore Wind 54 2005

Jardin d’Éole Onshore Wind 133 2009

Thorold Gas 265 2010

Mont Louis Onshore Wind 101 2011

Spy Hill Gas 86 2011

North Battleford Gas 260 2013

Northland Solar Solar 90 2013 – 15

McLean’s Mountain Onshore Wind 60 2014

Cochrane Solar Solar 40 2015 1

Grand Bend Onshore Wind 100 2016

Gemini Offshore Wind 600 2017

Nordsee One Offshore Wind 332 2017

Deutsche Bucht Offshore Wind 252 2019E 2 2

Total 2,493 MW

1. Cochrane Solar was over budget due to the failure, and subsequent commencement of restructuring proceedings, of the contractor2. Currently on time and on budget as of May 11, 2018

Northland has a Track Record of successfully delivering projects on-time and on-budget

14

Track Record of Innovation and Early Market Penetration

One of the First IPPs to Enter Saskatchewan, Canada, with Gas

Generation

One of the 1st Wind Farms Developed in Quebec, Canada (Mont Miller)2

One of the First Power Income Trusts

1st to Use LifeCo Financing for a Power Project in Canada

Cochrane Was 1st IPP in Canada to Attract Institutional Financing

1st Utility-Scale Biomass to Electricity Facility in Ontario

Cochrane Power

1st Long-Term Service Agreement With General Electric

1st to Successfully Match Western Canadian Natural Gas Supply With Ontario Electricity

Market,Cochrane Power (Gas Component)

Pioneer in Structuring Equity Partnerships With First Nations in Power Generation

ProjectsMcLean’s Mountain/Grand Bend/

Cochrane Solar

1. At Financial Close 2. Assets were subsequently sold after five years of operations

Largest Project Financing for Renewables Project1

1st Offshore Wind Project Financing With Only Commercial Financing

1st Canadian IPP to Enter European Offshore Wind

Northland Firsts

15

Multiple Development Markets & Technologies

Conducive to Project Finance

Execution

Credit Worthy Off-Takers

Stable Economic and Political Jurisdictions

Long Term Revenue Stability

Attractive Project Returns

Market and Technology Assessment Criteria

Northland Office (Toronto, Mexico City, London, Amsterdam, Hamburg, Taipei)

Potential Markets

JapanSouth Korea

Taiwan

Canada & United States

Asia

Europe

Mexico & Latin America

16

Taiwan Overview

FIT Program currently in place to support renewable policy targets FIT program designed to kick-start offshore wind sector

with 20 year FIT contracts

Current Taiwan Procurement Allocationso 2020 – 0.7GW (FIT no local content)o 2021-2025 – 3.1GW (FIT with local content)o Beyond – 1.7GW (price competitive auction)

Current Last estimate of upcoming major milestoneso Mid 2018 – FIT allocationo Q3 2018 – Price competitive auction

Water Depth: 0–20 mWater Depth: 20–50 m

Pacific Ocean

Taiwan StraitTaipeiCity

Established a meaningful presence in Taiwan Northland and its partners are currently in advanced

site development Continue all required regulatory/permit work in order

to secure approvals / secure FIT PPA Seek opportunities for further projects

Current Market Themes Site Location

Hai Long 2 was allocated 300 MW grid allocation under FIT

Development Strategy Hai Long 2 Project Snapshot

Status: • Awarded 300MW of grid allocation for 2024 COD

Capacity: • 300 MW (gross)

Contract: • 20-year PPA under FIT with TaiPower

Type: • Offshore wind

Ownership: • Northland 60%• Yushan 40%

17

>150 GW

Total Opportunity in Target Markets

Development Pipeline

Construction & Advanced Development

Identify and qualify potential markets with attractive fundamentals

Source and evaluate opportunities that meet our investment criteria

Includes achievement of major milestones / power contracts, supply agreements

finalized and/or project financing secured

>DeBu – 269 MW >Taiwan – 300 MW

Significant Development Opportunities

~6,000 MW

1. Includes the 17MW opportunity for two additional demonstration turbines utilizing suction bucket foundations. Final Investment Decision is subject to achieving certain development milestones

300 MW

269 MW1

18

Power Markets are ChangingOur industry has changed immensely over the past 10 years Supportive Government Policies – Governments have taken real action to reduce carbon Industry Evolution & Technological Advancement – Renewables are now a cost-effective

and feasible alternative to add new power Market Liberalization and Competition – Increased demand has attracted new players

ready to deploy capital in competition with traditional IPPs

The global investment opportunity set for Northland, driven by economic growth and decarbonization, has never been greater

19

Global Movement Towards Sustainability

Source: United Nations Department of Economic and Social Affairs

20

Focusing on clean and green technologies

Delivering strong and sustainable financial results

Generating and distributing economic value

Capitalizing on revenue generating opportunities through the transition to a low-carbon future

Supporting sustainable economies through clean energy and responsible business practices

Investing in our communities

Partnering with First Nations

Preserving the natural environment

Our Sustainability Pillars Northland’s vision is to be a top clean and green power producer, inspiring our people

to achieve a sustainable and prosperous future for all stakeholders

We will achieve this through our three strategic pillars:

Inspired Workforce

Top Clean & Green Power Producer

Prosperity for Stakeholders

Prioritizing health and safety

Fostering our values and culture

Providing meaningful career development opportunities

Hiring locally and providing international opportunities

21

Looking Ahead in 2018

Objectives:

We will build on the success of our first 30 years and continue to deliver on our promises and create long-term value for our shareholders

Continue to advance and secure high quality projects

Diversify across locations and technologies

Be a leading player in the global transition towards decarbonization

Continue track record: on-time, on-budget

Continue to execute on DeBu project constructionConstruction

Execution

Maintain excellent operating track record

Excellent health and safety and environmental record

Continue to improve operating portfolio

Operational Excellence

Development Focus

22

Investor Relations Contacts

Appendix

23

Reporting of Non-IFRS Financial Measures

This investor presentation includes references to Northland’s adjusted EBITDA and free cash flow, measures not prescribed by InternationalFinancial Reporting Standards (IFRS). Adjusted EBITDA and free cash flow, as presented, may not be comparable to other similarly-titledmeasures presented by other publicly-traded companies, as these measures do not have a standardized meaning under IFRS. These measuresshould not be considered in isolation or as alternatives to net income, cash flow from operating activities or other measures of financialperformance calculated in accordance with IFRS. These measures are also not necessarily indicative of operating income or cash flows fromoperating activities as determined under IFRS. Rather, these measures are provided to complement IFRS measures in the analysis ofNorthland’s results of operations, and are used by management to evaluate the performance of the company for internal assessmentpurposes. Management believes that adjusted EBITDA and free cash flow are widely-accepted financial indicators used by investors to assessthe performance of a company. These measures provide investors with additional information to assist them in understanding these criticalcomponents of the company’s financial performance, including its ability to generate cash through its current operations. These measures havebeen applied consistently for all periods presented in this document.

Adjusted EBITDAAdjusted EBITDA provides investors with an indication of Northland’s capacity to generate income from operations and investments beforetaking into account management’s financing decisions and the costs of consuming tangible and intangible capital assets, which vary accordingto asset type and management’s estimate of their useful lives.Adjusted EBITDA is calculated as income (loss) before income taxes adjusted for depreciation of property, plant and equipment, amortization ofcontracts and other intangible assets, net finance costs, Gemini subordinated debt earned by Northland, fair value losses (gains) on derivativecontracts, unrealized foreign exchange losses (gains), elimination of non-controlling interests and finance lease and equity accounting.

Free cash flowFree cash flow is calculated as cash flow provided by operating activities adjusted for net change in non-cash working capital balances, capitalexpenditures, interest paid, scheduled principal repayments on term loans, funds set aside for scheduled principal repayments and for assetpurchases, restricted cash (funding) for major maintenance, write-off of deferred development costs, consolidation of managed facilities,income from equity accounted investments, proceeds from sale of assets, and preferred share dividends. This measure, along with cash flowprovided by operating activities, is considered to be a key indicator for investors to understand Northland’s ability to generate cash flow fromits current operations.

Readers should refer to our MD&As accompanying our financial statements for an explanation of adjusted EBITDA and free cash flow, and for areconciliation of Northland’s reported adjusted EBITDA to its consolidated income (loss) before taxes and a reconciliation of Northland’s freecash flow to its cash provided by operating activities. These are filed from time to time on our company’s website www.northlandpower.ca.

24* Hub height measure from the sea level

Past and Present Wind Turbines

2009 2016 2017 2017 2019E 2022E

Grand BendManufacture: SiemensRated Power: 3.0 MW

Blade Length: 55 mRotor Diameter: 113 m

Hub Height: 115 m

Jardin d’ÉoleManufacture: GE Energy

Rated Power: 1.5 MWBlade Length: 31-37 mRotor Diameter: 77 m

Hub Height: 61 to 85 m

GeminiManufacture: SiemensRated Power: 4.0 MW

Blade Length: 63 mRotor Diameter: 130 m

Hub Height: 90 m *

Nordsee OneManufacture: SenvionRated Power: 6.15 MW

Blade Length: 62 mRotor Diameter: 126 m

Hub Height: 90 m *

Deutsche BuchtManufacture: MHI Vestas

Rated Power: 8.4 MWBlade Length: 80 m

Rotor Diameter: 164 mHub Height: 108 m *

12MW TurbineExpected to

Debut in ~2022

0

100

200

300

Hub

Heig

ht (m

)

The Statueof LibertyHeight: 93 m

Wind Turbine Evolution

25

0 5 10 15 20 25

North Battleford**

Ground Mounted Solar**

Jardin

Germany

Mt Louis

Kirkland*

Cochrane*

Spy Hill

Thorold

Kingston

Iroquois Falls

Producing and Maintaining Stable Cash FlowsRemaining PPA Term for Each Operating Facility

1. Represents Northland’s economic interest in the facility2. The weighted average PPA life is weighted by respective MW capacity. The thickness of each bar represents each facilities respective overall contribution to

2018 forecasted Adjusted EBITDA

Weighted Average Life of

12.6 years2

DeBu

Iroquois Falls

Thorold

Spy Hill

Kirkland Lake1

Jardin

North Battleford

McLean’s Mtn

Grand Bend

Gemini

NordseeOne

Ground-Mount Solar

Mont Louis

26

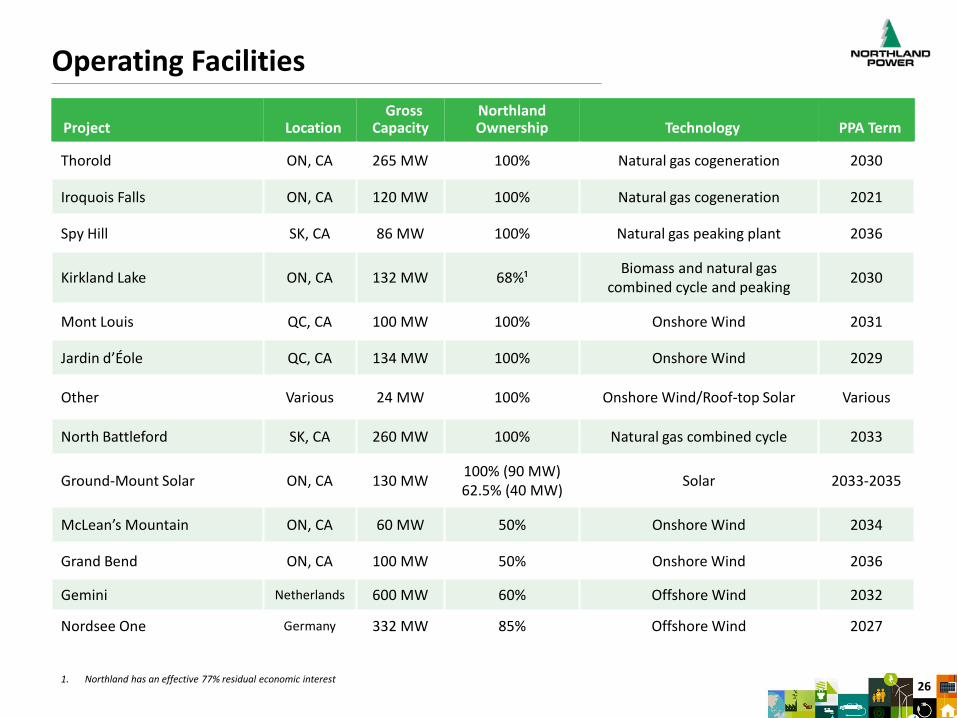

Operating Facilities

Project LocationGross

CapacityNorthland Ownership Technology PPA Term

Thorold ON, CA 265 MW 100% Natural gas cogeneration 2030

Iroquois Falls ON, CA 120 MW 100% Natural gas cogeneration 2021

Spy Hill SK, CA 86 MW 100% Natural gas peaking plant 2036

Kirkland Lake ON, CA 132 MW 68%¹ Biomass and natural gas combined cycle and peaking 2030

Mont Louis QC, CA 100 MW 100% Onshore Wind 2031

Jardin d’Éole QC, CA 134 MW 100% Onshore Wind 2029

Other Various 24 MW 100% Onshore Wind/Roof-top Solar Various

North Battleford SK, CA 260 MW 100% Natural gas combined cycle 2033

Ground-Mount Solar ON, CA 130 MW 100% (90 MW)62.5% (40 MW) Solar 2033-2035

McLean’s Mountain ON, CA 60 MW 50% Onshore Wind 2034

Grand Bend ON, CA 100 MW 50% Onshore Wind 2036

Gemini Netherlands 600 MW 60% Offshore Wind 2032

Nordsee One Germany 332 MW 85% Offshore Wind 2027

1. Northland has an effective 77% residual economic interest

27

European Offshore Wind Facility Details

Gemini Nordsee One Deutsche Bucht (DeBu)

Capacity 600 MW 332 MW 252 MW (+17 MW Demonstrators*)

Distance to Shore 85km 40km 95km

Wind Turbines 150 x Siemens 4 MW 54 Senvion x 6.15 MW 33 x MHI Vestas 8MW

Turbine Foundation Monopile Monopile Monopile*

Water Depth 28m to 36m 26m to 29m 39m to 41m

Total Project Costs €2.8 Billion €1.2 Billion €1.3 Billion*

Revenue Contract Type Contract for Differences (CFD)(FiT-Type) Feed in tariff Feed in tariff

Revenue Contract Term 15 years ~10 years ~13 years

Revenue Contract Price ~€169/MWh[No escalation]

€194/MWh for 8 years,€154/MWh for 1.5 years

[No escalation]

€184/MWh for 8 years,€149/MWh for 4.7 years

[No escalation]

Grid Connection Responsibility

Gemini responsible forconnection to shore

Tennet responsible forconnection to shore

Tennet responsible forconnection to shore

NPI Ownership 60% 85% 100%

* As previously announced, DeBu is investigating the development of two additional demonstration turbines utilizing suction bucket foundations. The final investment decision for these two turbines is subject to achieving certain development milestones. If built, they will contribute an additional 17 MW of capacity, and bring the total project cost to approximately €1.4 billion.

28

Financial Summary

Key Metrics

Recent¹ Share Price (TSX: NPI) $24.27

Shares (Common + Class A) 176 million

Institutional Ownership ~38%

Management Ownership ~34%

Annual Dividend $1.20

Annual Dividend Yield 4.9%

Total Debt, Net of Cash $6.5 billion

Convertible Debentures (NPI.DB.B, NPI.DB.C) $229 million

Preferred Shares (NPI.PR.A, NPI.PR.B, NPI.PR.C) $261 million

Market Capitalization (Common + Class A) $4.3 billion

Enterprise Value $12.3 billion

Credit Rating (S&P) BBB Stable

1. As of May 11, 2018

29

Investor Relations Contacts

Dhiraj ShangariManager, Corporate Finance647.288.5566

Barb BoklaManager, Investor Relations 647.288.1438