Embed Size (px)

Citation preview

Clearing House of

the year

2010 & 2011

Nordic Capital Market Forum 201317th January 2013

Heiko CassensDirector Germany, Nordics

SwapClear Sales & Marketing

Contents

• LCH.Clearnet

• EMIR and OTC Derivatives Clearing

• Impact of EMIR regulation on OTC Clearing

• Impact of EMIR regulation on CCPs

• OTC Derivatives Clearing Market Overview SwapClear

• Implementing Regulation – SwapClear Client Clearing

• Outlook

Private & Confidential | 2

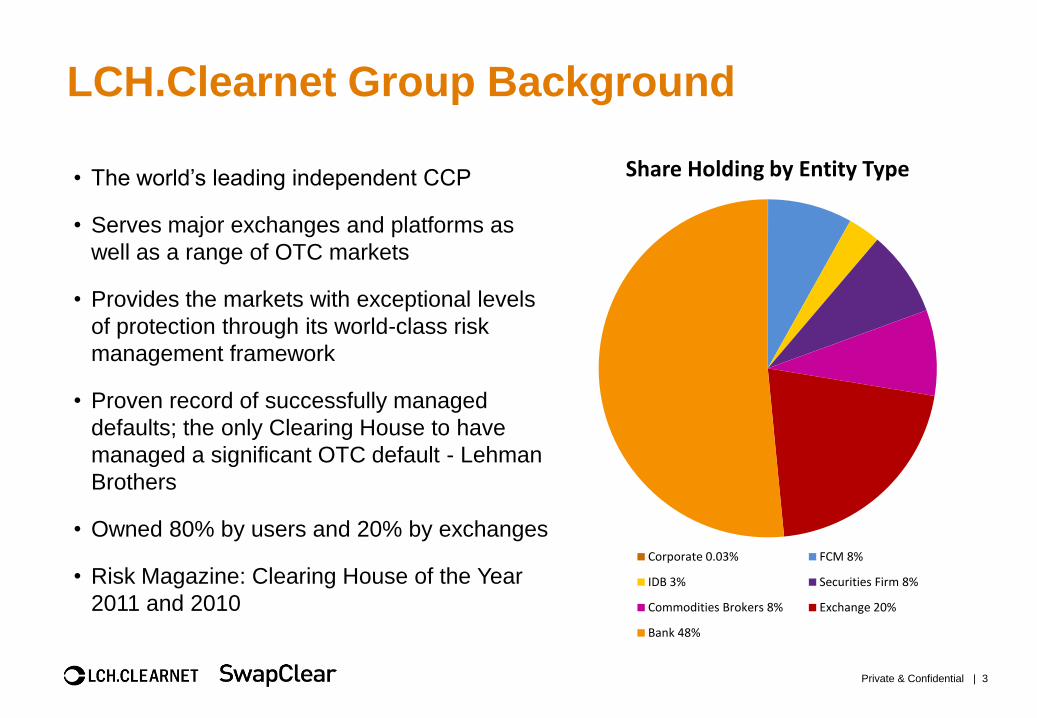

LCH.Clearnet Group Background

• The world’s leading independent CCP

• Serves major exchanges and platforms as

well as a range of OTC markets

• Provides the markets with exceptional levels

of protection through its world-class risk

management framework

• Proven record of successfully managed

defaults; the only Clearing House to have

managed a significant OTC default - Lehman

Brothers

• Owned 80% by users and 20% by exchanges

• Risk Magazine: Clearing House of the Year

2011 and 2010

Private & Confidential | 3

Share Holding by Entity Type

Corporate 0.03% FCM 8%

IDB 3% Securities Firm 8%

Commodities Brokers 8% Exchange 20%

Bank 48%

Market PositionLCH.Clearnet Group clears broadest range of OTC & exchange cash and derivative

products.Interest Rate

Swaps

SwapClear

Credit Default

Swaps

CDSClear

Equities

EquityClear

Commodities & Listed

Derivatives

LCH EnClear

Euroclear UK & Ireland

Euroclear Belgium

Euroclear France

Euroclear NL

Euroclear Bank

SUX SIS

Clearstream International

Clearstream Frankfurt

VPS

NCSD

Interbolsa

Monte Titoli

VP – Værdepapircentralen

National Bank of Belgium

Commodities

Cash

DTCC

SE

TT

LE

ME

NT

TR

AD

ING

VE

NU

ES

SE

RV

ED

*Soon to be launched

Fixed IncomeRepoClear &Bonds and Repo

Interest Rate SwapsSwapClear

Credit Default SwapsCDSClear

EquitiesEquityClear

Commodities & Listed

Derivatives

LCH EnClear

Foreign ExchangeForexClear

ICAP Electronic Broking

BGC

ETCMS

MTS

tpRepo

Luxembourg Stock

Exchange

NYSE BondMatch

MarkitSERV

Tradeweb

Bloomberg

DTCC Deriv/SERV

MarkitServ

Turquoise

LMAX

OTC Equities

BATS Chi-X Europe

Börse Berlin Equiduct

Trading

NYSE Euronext

London Stock Exchange

SIX Swiss Exchange

FEX*

HKMEx

NYSE Liffe

London Metal Exchange

Turquoise Derivatives

Nodal Exchange

OTC Commodities and

Freight Brokers

Cleartrade Exchange

Baltic Exchange

MarkitSERV

Traiana (Q1 2013)

Bloomberg (Q2 2013)

Regulatory Update

Private & Confidential | 5

The trading & clearing mandates

European Markets

Infrastructure Regulation

(EMIR)

OTC derivative

contracts

are to be cleared through

a CCP

and reported to a trade

repository

Markets in Financial

Instruments Regulation

(MiFIR)

Standardised and liquid

derivatives are to be

executed on Regulated

Markets, MTFs

(Multilateral Trading

Facilities) or OTFs

(Organised Trading

Facilities)

Dodd Frank Act

Swaps are to be cleared

through a DCO and,

in most cases,

executed on

an exchange or SEF

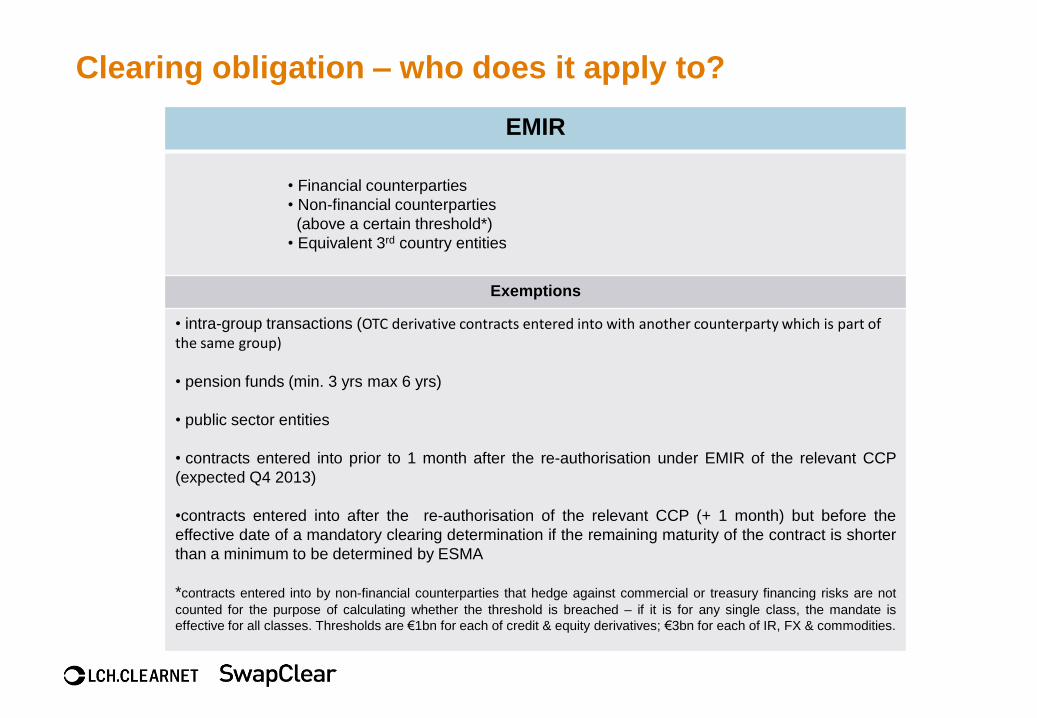

Clearing obligation – who does it apply to?

EMIR

• Financial counterparties

• Non-financial counterparties

(above a certain threshold*)

• Equivalent 3rd country entities

Exemptions

• intra-group transactions (OTC derivative contracts entered into with another counterparty which is part of the same group)

• pension funds (min. 3 yrs max 6 yrs)

• public sector entities

• contracts entered into prior to 1 month after the re-authorisation under EMIR of the relevant CCP

(expected Q4 2013)

•contracts entered into after the re-authorisation of the relevant CCP (+ 1 month) but before the

effective date of a mandatory clearing determination if the remaining maturity of the contract is shorter

than a minimum to be determined by ESMA

*contracts entered into by non-financial counterparties that hedge against commercial or treasury financing risks are not

counted for the purpose of calculating whether the threshold is breached – if it is for any single class, the mandate is

effective for all classes. Thresholds are €1bn for each of credit & equity derivatives; €3bn for each of IR, FX & commodities.

Criteria for clearing determinations - what does it apply to?

EMIR

The clearing obligation applies to derivatives as

defined in MiFID not traded on a

Regulated Market or foreign equivalent

Criteria

• degree of standardisation of the contractual terms and operational processes of the contracts;

• volume and liquidity;

• availability of fair, reliable and generally accepted pricing information.

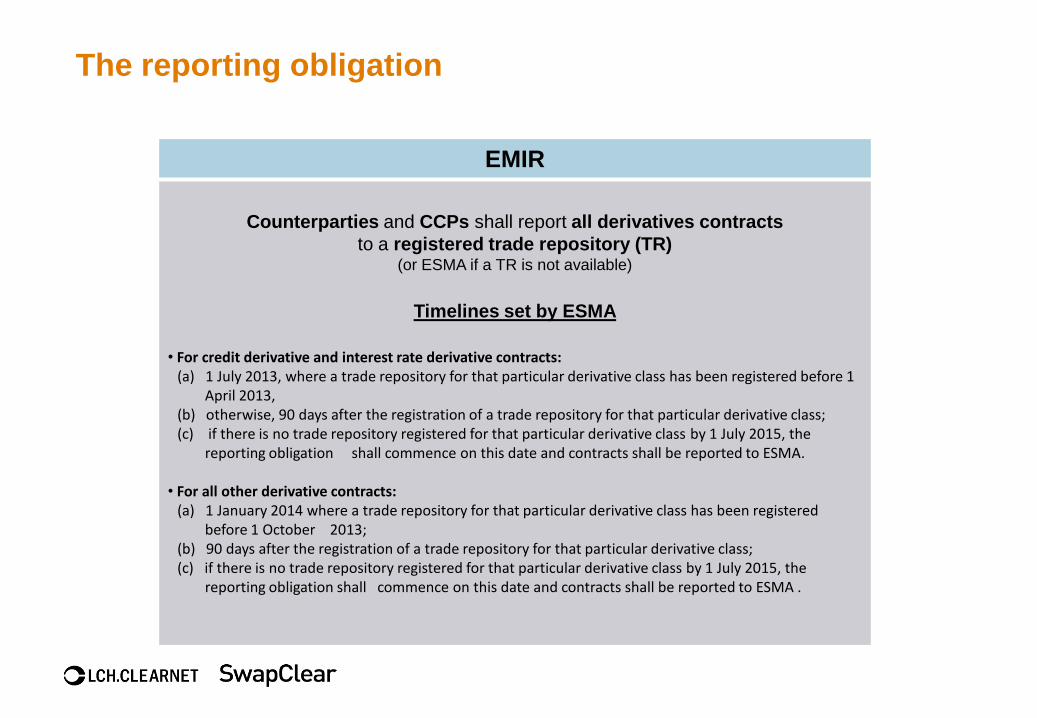

The reporting obligation

EMIR

Counterparties and CCPs shall report all derivatives contracts

to a registered trade repository (TR)(or ESMA if a TR is not available)

Timelines set by ESMA

• For credit derivative and interest rate derivative contracts:(a) 1 July 2013, where a trade repository for that particular derivative class has been registered before 1

April 2013, (b) otherwise, 90 days after the registration of a trade repository for that particular derivative class; (c) if there is no trade repository registered for that particular derivative class by 1 July 2015, the

reporting obligation shall commence on this date and contracts shall be reported to ESMA.

• For all other derivative contracts:(a) 1 January 2014 where a trade repository for that particular derivative class has been registered

before 1 October 2013; (b) 90 days after the registration of a trade repository for that particular derivative class; (c) if there is no trade repository registered for that particular derivative class by 1 July 2015, the

reporting obligation shall commence on this date and contracts shall be reported to ESMA .

EMIR timelines

Clearing

obligation

Reporting

CCPs’

authorisation

EMIR & RTS

entry into

force

16 Aug 2012 - EMIR entry into force

end Dec 2012 - Commission endorsement of RTS

Q1/2 2013 - RTS entry into force (20 days after publication on Official Journal)

within 6 months from RTS entry into force, therefore Q3/4 2013 - CCPs must apply

for authorisation

within 6 months of the above, therefore Q1/2 2014 - national authorities to authorise

CCPs which applied within the deadline and meet the EMIR requirements

within 1 month from RTS entry into force, therefore Q2/3 2013 - national authorities

notify ESMA of the classes of derivatives CCPs are already authorised to clear at

national level

within 6 months from the above therefore Q3/4 2013- ESMA to submit RTS on

clearing obligation (OTC classes, dates and minimum maturity as per slide 4)

Commission must then endorse the RTS. European Parliament and Council have the

right to object

Clearing obligation unlikely to be effective before 2014

1 July 2013 – reporting date for credit/IR derivs (where a TR is registered by 1 Apr

13; or 90 days after a TR is registered)

1 January 2014 – reporting date for all derivs (where a TR is registered by 1 Oct 13;

or 90 after a TR is registered)

1 July 2015 - Deadline for reporting all derivs to ESMA in the absence of a registered

TR

SwapClear

Private & Confidential | 11

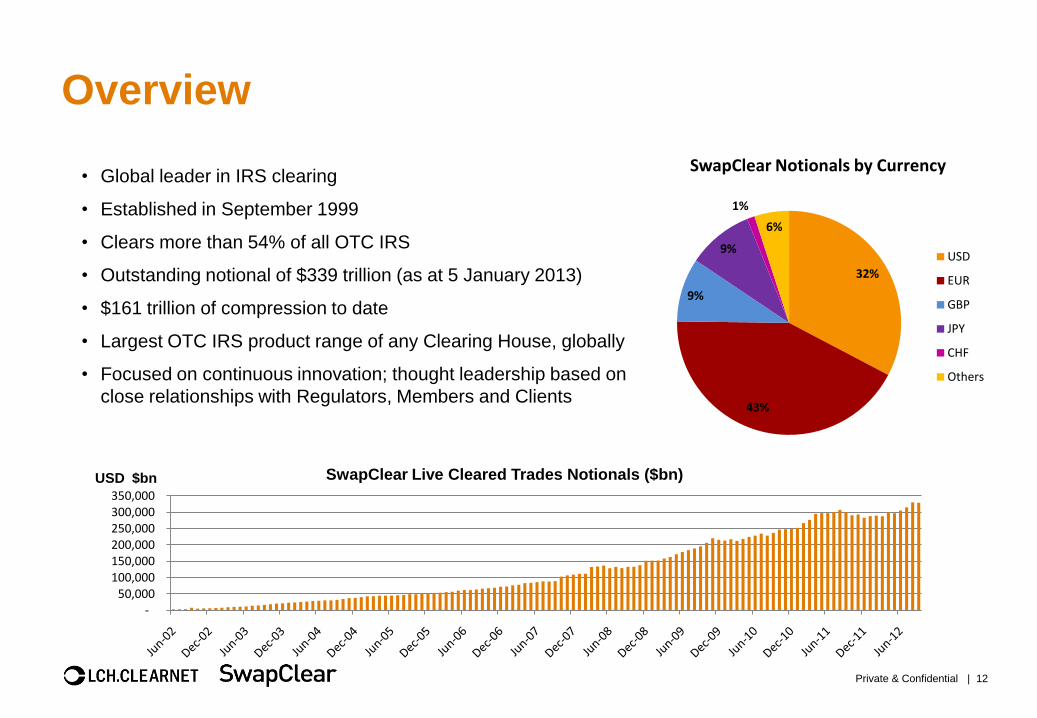

Overview

• Global leader in IRS clearing

• Established in September 1999

• Clears more than 54% of all OTC IRS

• Outstanding notional of $339 trillion (as at 5 January 2013)

• $161 trillion of compression to date

• Largest OTC IRS product range of any Clearing House, globally

• Focused on continuous innovation; thought leadership based on

close relationships with Regulators, Members and Clients

-50,000

100,000 150,000 200,000 250,000 300,000 350,000

SwapClear Live Cleared Trades Notionals ($bn)USD $bn

32%

43%

9%

9%

1%

6%

SwapClear Notionals by Currency

USD

EUR

GBP

JPY

CHF

Others

Private & Confidential | 12

SwapClear volumes and liquidity – how does it translate?

• SwapClear Product Coverage• Widest rage of OTC IRS eligible for clearing

• All ISDA day count fractions and business day

conventions

• Continuous extension of our IRS product range

• Non-linear structures in the pipeline (e.g.

Swaptions)

• Community• Long-standing relationships with our counterparties

• 72 Members/ 26 Members offering client clearing

services under the SCM model*

• Access to global IRS Markets

• Clients receive superior pricing and spreads

• Risk Management Excellence

• 13 years experience

• Robust and accurate Risk Management systems

• Proven Default Management Track record

(e.g. Lehman Brothers)

* Full list of Members can be found in the Appendix

Private & Confidential | 13

SwapClear Membership72 CLEARING MEMBERS CLEARING FOR 105 DEALERS (NOVEMBER 2012)

Abbey National Treasury Services plc

ABN AMRO Clearing Bank NV*

Banca IMI S.p.A*

Banco Bilbao Vizcaya Argentaria SA

Banco Santander

Bank of America NA*

Bank of Montreal

Bank of New York Mellon

Barclays Bank PLC*

Barclays Capital, Inc**

Bayerische Landesbank

Belfius Bank

BNP Paribas*

BNP Paribas Securities Corp**

Canadian Imperial Bank of Commerce

Citibank NA*

Citigroup Global Markets Ltd

Citigroup Global Markets, Inc.**

Commerzbank AG*

Credit Agricole Corp. and Inv. Bank*

Credit Suisse AG

Credit Suisse International*

Credit Suisse Securities (Europe) Limited*

Credit Suisse Securities (USA) LLC**

Danske Bank AS*

DekaBank Deutsche Girozentrale

Deutsche Bank AG*

Deutsche Bank Securities, Inc**

Deutsche PostBank AG*

Deutsche-Zentral-Genossenschaftsbank

AG*

DNB Bank ASA

Goldman Sachs & Co.**

Goldman Sachs Bank USA*

Goldman Sachs International*

HSBC Bank plc*

HSBC France*

HSBC Bank USA, NA

HSBC Securities (USA) Inc.**

Hongkong Shanghai Banking Corporation

Limited

ING Bank NV

JP Morgan Chase Bank NA*

JP Morgan Securities LLC**

Landesbank Baden-Württemberg *

Landesbank Hessen-Thueringen

Girozentrale

Lloyds TSB Bank PLC

Merrill Lynch Intl Bank Limited*

Merrill Lynch, Pierce, Fenner & Smith,

Inc.**

Mitsubishi UFJ Securities International plc

Mizuho Capital Markets Corporation

Morgan Stanley Capital Services LLC*

Morgan Stanley & Co. LLC**

Morgan Stanley International*

Natixis SA*

Nomura International PLC*

Nomura Global Financial Products Inc*

Nomura Securities International, Inc.**

Nordea Bank Finland

Rabobank International *

RBS Securities, Inc**

Royal Bank of Canada

SMBC Capital Inc

Société Générale*

Standard Chartered Bank

The Bank of Nova Scotia

The Royal Bank of Scotland NV*

The Royal Bank of Scotland PLC*

The Toronto-Dominion Bank

UBS AG*

UBS Securities, LLC**

Unicredit Bank AG

Wells Fargo Bank NA

Zurcher Kantonalbank

FCM Clearing Member

SCM Clearing Member

Offering Client Clearing

Private & Confidential | 14

SwapClear Client Clearing

Private & Confidential | 15

SwapClear Client Clearing

• The first chart shows notional values of client trades cleared each month. It illustrates the acceleration of

client clearing during 2012.

• The total notional value of client trades cleared during December 2012 over USD 3.7 trillion.

• Most of the decrease over the previous month came from OIS and basis swap trades. The average

notional of such trades is much higher than vanilla IRS; overall trade counts actually increased slightly in

October when compared to September. This is illustrated in the second chart.

• Client notional outstanding decreased slightly to USD 3.7 trillion; total cumulative client notional is now

over USD 13 trillion.

Note on terminology: cleared client trades are trades between LCH.Clearnet and a clearing member on behalf of a third-party

client.

0200400600800

100012001400160018002000

USD equiv

Bill

ion

s

SwapClear Client Clearing Notionals, USD bn.

FRA

OIS

Basis Swap

VNS

Zero coupon

IRS

01,0002,0003,0004,0005,0006,0007,0008,000

Monthly Trades

SwapClear Client Clearing Volumes

Monthly Trades Outstanding

• Launched 2009

• Total cumulative notional cleared more than USD 13 Trillion (5 January 2013)

Trade Submission(as of Q4 2012)

1.Trade Execution, Allocation & Affirmation – CP 1 and CP 2 agree to

a transaction on the SEF/affirmation platform:

CP1 updates the block trade with CB and allocation details

CP2 can also nominate a CB (and must accept CP1 allocations)

2. Eligibility Check – Once the matched and allocated trade is

received by SwapClear, an eligibility check is performed to validate Product/Participant/Fee Settlement

If trade passes these eligibility checks, SwapClear updates the SEF /

Affirmation Platform with status “Awaiting Acceptance”

If trade fails these checks, SwapClear informs the SEF / Affirmation Platform

with status “Rejected – Eligibility” with the rejection reason

3. Clearing Broker Risk Assessment – If trade passes eligibility checks, SwapClear sends the trade and allocation details

assigned to each CB by the Client for CB acceptance

If both trade sides are cleared by the same CB, two acceptance messages are required

Status messages are sent to SEF / Affirmation Platform

If a trade is rejected by a CB , CP1 can select a new CB via the SEF/affirmation platform

* Trade Registration – After CB acceptance, trades are registered in SwapClear. Post registration, all participants are

notified.

Private & Confidential | 17

Protection Options

LCH.Clearnet denotes LCH.Clearnet Ltd.

Gross Segregated

Client Account A

Clearing

Member

Net Omnibus

Client Account B

Net Omnibus

Client Account C

Sovereign QGross Segregated Client Account A

Protection at Individual Fund Level

Net Omnibus – Affiliated/Non Affiliated

Clients

Omnibus account - can be at Group level

Protection at Net Group Level

Asset ManagerX Fund 1

Asset ManagerX Fund 2

Asset ManagerX Fund 3

Net Omnibus – Non-Affiliated clients

Omnibus account - may contain different

entities

Futures-Style Model;

Partial Protection only

Hedge Fund Y

Regional Bank Z

VM

IM

VM

IM

IM

VM

IM

VM

LCH.Clearnet SwapClear Client Accounts

Private & Confidential | 18

Client Portability: Default Management

Timeline

Private & Confidential | 19

LCH.Clearnet denotes LCH.Clearnet Ltd.

Outlook

• Standardisation of OTC Derivatives

• Impact on number of market participants?

• CCPs

• Competition between CCPs?

• Interoperability?

• Scrutiny Risk Management procedures?

• Market prices

• Co- mingled stacking or price differentiation between CCPs ?

• Market makers to pass on cost of clearing to buy-side?

• Focus on eligible Collateral and Collateral Management

• Basel III – Cost of capital

Private & Confidential | 20

Contacts

LCH.Clearnet Limited Aldgate House

33 Aldgate High Street

London, EC3N 1EA

Heiko CassensDirector Germany, Nordics

SwapClear Sales & Marketing

+44 (0) 20 7392 1853

Private & Confidential | 21

Email : [email protected]

Browse: www.swapclear.com

Disclaimer

The contents of this document are a broad overview of the SwapClear Client Clearing Service and have been provided to you for information purposes only.

Nothing in this document should be considered to be legal advice. There is no substitute for analysing the Regulations, Rules and Procedures of LCH.Clearnet Limited as well as other transaction documentation. Accordingly, clients may not rely upon the contents of this document and should seek their own independent legal advice.

The information and any opinion contained in this document, does not constitute investment advice or a personal recommendation with respect to any applicable securities or other financial instruments. This document has not been prepared for a specific client and accordingly no reliance should be placed on it. Nothing in this document should be taken as a public offer to sell or to buy any applicable securities of financial instruments.

Your notice is drawn to the Notice to End Users of SwapClear Client Clearing Services at www.lchclearnet.com

Copyright © LCH.Clearnet Limited 2012

All rights reserved. No part of this document may be copied, whether by photographic or any other means, without the prior written consent of LCH.Clearnet Limited.

SwapClear is a registered trademark of LCH.Clearnet Limited.

Private & Confidential | 22