Embed Size (px)

Citation preview

nnovationINSIGHTi1 Florida’s Medical Technology Clusters

nnovationINSIGHTi

Florida’s Medical Technology ClustersSpring 2003

Sponsored by the Florida High Tech Corridor Council, Inc., the Tampa Bay Partnership, and the University of South Florida

nnovationINSIGHTi Florida’s Medical Technology Clusters 2 nnovation

INSIGHTi1 Florida’s Medical Technology Clusters

Table of Contents

I. Executive Summary 1

II. Background 3

III. Traditional Cluster Analysis 4Porter’s Factor “Diamond” 4

IV. Regional Targeted Cluster Comparisons 7Methodology and Sources 7Validity 7Geographic Distribution and Change 8Targeted Regional Comparisons by Establishments 10Targeted Regional Comparisons by Employment 12Targeted Regional Comparisons by Average Salary 14Targeted Regional Comparisons by Average Company Size 16Targeted Regional Comparisons by Patent Activity and Productivity 17Combined Rankings 19Florida High Tech Corridor and Combined Regions 19Combined Strategic Comparisons 22Summary Observations 24

V. Cluster Supply Chain Mapping and Opportunity Analysis 25Supply Chain Mapping 25Opportunity Analysis 27

VI. Strategic Survey Analysis 29Methodology 29Description of Companies 30Business Assistance 30Technology 31Financing and Investment 33State Incentives 34Import and Export 35Market and Product Development 36Network Capital 36Needs Assessment 38

VII. Concluding Comments and Recommendations 39

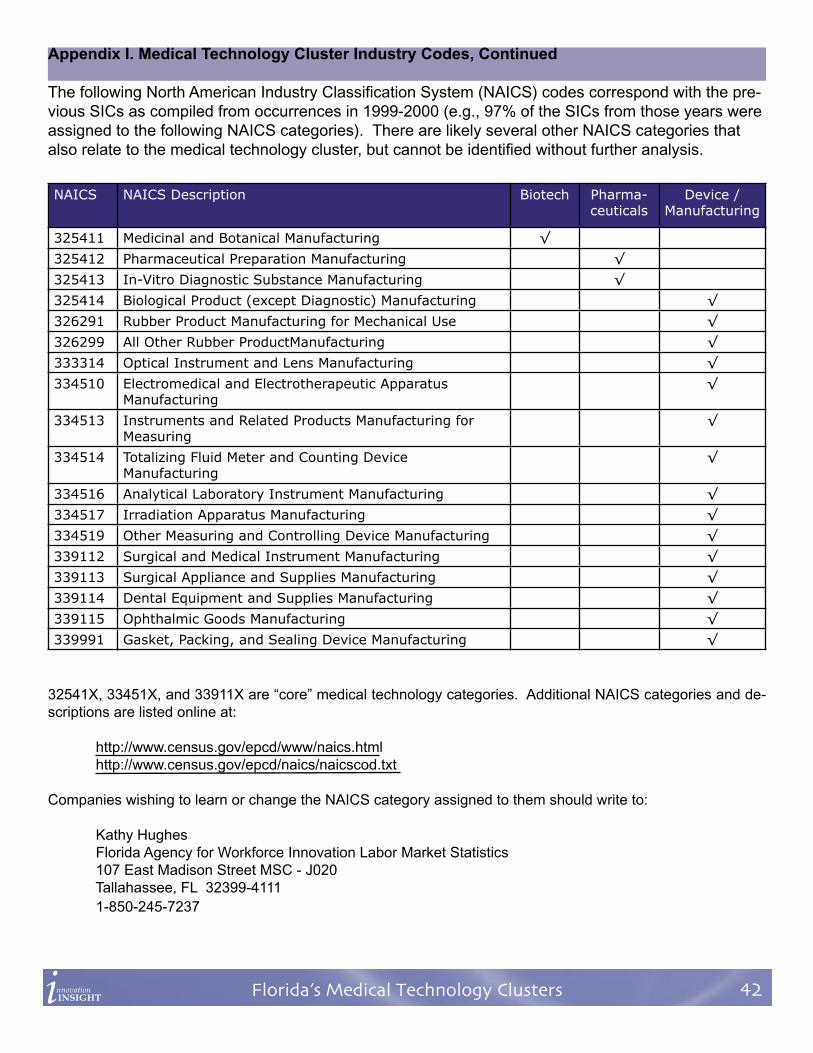

Appendix I. Medical Technology Cluster Industry Codes 41

Appendix II. Medical Technology Patent Categories 43

Appendix III. Glossary of Industry Terms 44

Appendix IV. Contact Information 45

nnovationINSIGHTi Florida’s Medical Technology Clusters 2 nnovation

INSIGHTi1 Florida’s Medical Technology Clusters

I. Executive Summary

This study was contracted by the Florida High Tech Corridor Council, Inc., the University of South Florida, and the Tampa Bay Partnership, and in partnership with the Florida Medical Manufacturing Consortium and the Gulf Coast Life Sciences Inititiative. The study was conducted between September and December, 2002 as a com-prehensive “cluster” analysis of medical technology industries in the Florida High Tech Corridor. “Medical tech-nology” describes companies in medical manufacturing, pharmaceuticals, clinical research and development, and biotech, and where appropriate bioinformatics and genomics as well. Selected findings from this report include:

• National industry trends: From 1999 to 2000, medical technology companies across the U.S. showed a slight consolidation as the number of establishments decreased approximately 10%, but overall employment stayed relatively stable. Overall, Florida medical technology clusters fared well compared to national trends.

• Florida industry activity: As a combined MSA region, the Florida High Tech Corridor ranks among the top 16 regions in the U.S. Separately, at least three Florida MSAs are competitive on a national scale: Tampa Bay, Miami, and Jacksonville. In general, these regions may be considered “Tier 1” U.S. medical technology clusters (within the top 20 regions compared against employment, salary, patents, and number of companies).Jacksonville has a suprisingly strong presence in 2001, however it is highly dependent upon two major employers; without which, its rank drops in almost every category beyond consideration as a significant cluster. Orlando and Gainesville also have high scorings in specific areas, but do not yet have a ‘critical mass’ of medical technology companies. In general, Florida medical technology clusters lag well behind the nation in terms of innovation and average salary, even after adjustment for cost-of-living and income tax. Like many of the smaller, relatively young U.S. medical technology clusters, Florida’s medical technology clusters have considerable potential for growth, especially in light of the fact that the very top clusters in the nation (southern California, the Boston region, and New Jersey) have suffered significant employment and company attrition from 1999 - 2000.

• Workforce recruitment targets: Based upon cost of living, state income tax, employment levels and relative average salaries, the best targets for specialized workforce recruitment for the Orlando and Tampa Bay regions include the New York, San Diego, Pittsburgh Pennsylvania, Tulsa Oklahoma and Riverside-San Bernardino Cali-fornia regions. Puerto Rico may also be an intriguing target due to its large workforce and severe layoffs.

• Business recruitment: The Boston region and southern California regions demonstrated significant medical technology company attrition in 1999-2000. These areas may be good candidates for recruiting entrepreneurs or vendors for relocation or expansion into Florida if presented a economic alternative to remaining in a declin-ing cluster.

• Import, export and competition: Most medical technology companies report the vast majority of their sales, vendors, and competition exist at the national (domestic U.S.) scale, with comparatively little activity at the state, local or international level. The low amount of international sales indicates a significant opportunity for export growth, and the lack of local / state competition and vendors demonstrates opportunity for local business devel-opment. Overall, these results show the medical technology cluster to be relatively strong and competitive.

• Vendor opportunities: Estimates of imports and insufficient local production capacity have identified several standard industry categories as opportunities for vendor development and recruitment. Encouraging growth and entrepreneurship in these categories should help strengthen the Florida High Tech Corridor’s medical technology cluster overall.

nnovationINSIGHTi Florida’s Medical Technology Clusters 2 nnovation

INSIGHTi3 Florida’s Medical Technology Clusters

• Network Capital: Network capital describes the ability to leverage professional networks to obtain resources. Florida High Tech Corridor medical technology companies report being fairly well connected regarding technol-ogy but poorly connected regarding financing and investment, being networked only with leaders at the local level. Access to external resources appears to depend mostly upon the networks of executive staff members, rather than board members. The implication is that while few companies felt their leaders were completely disconnected to key business resources, few businesses could tap into leadership at the Fortune 100 level or higher, and only a few company leaders had strong connections with U.S. or internationally elite business, tech-nology and finance leaders regarding medical technology. This represents a need for professional / executive networking events and activities.

• “Typical company” profile: Most medical technology companies in the Florida High Tech Corridor can be characterized as entrepreneurial, independent start-ups almost entirely self-financed (using vendor terms, boot-strapping and resources of the founder). There were few to no identified spin-outs or significant relocations. Most intellectual property is internally developed within the companies (as opposed to licensed from universities, research laboratories or other companies). Few have significant international exports. Significantly, almost all of the resources that a typical medical technology company will be able to access for much of its operation are established at startup, and are limited to the resources of the founder regarding intellectual property, financing, management, board members, and networks. Enabling and connecting entrepreneurs to resources should not only increase the survival rate of new companies, but their success and growth for several years.

• Research and technology needs: Many medical technology companies (40%) claim to have technologies available for partnership, demonstrating a need for a “clearinghouse” or other exchange forum. Universities are seen as a strong potential source of business and technology assistance in the fields of Business (marketing analysis help, business procedure development), Medical (biotech, cardiovascular), Biochemical (proteomics, microbiology and biochemistry), Engineering (mechanical and electrical, sensors, biomechanical), Materials (ba-sic materials, silicon, metallurgy – several respondents), and Information Technology. Participating companies stated the areas of most needed academic research include:

Materials characterization and development Proof of Principle verification Materials sciences

Wear resistance of medical instruments Clinical evaluations / studies Plasma physics

Algorithm and sensor technologies Applied pharmacology Materials (plastics)

Cardiovascular research Intuitive EMR Polymeric materials

Microelectromechanical systems Pharmacokinetics Animal testing

Information storage and transfer Lasers and cryogenics Proteomics

Incision closure research Interventional radiology Nanotechnology

• Needs assessment: Overall, the most critical industry issues are related to growth (marketing and sales, and research and product development) and federal regulation assistance. Tort and liability, availability of financ-ing and investment, and availability of technicians and skilled labor (versus unskilled or doctorate/specialist/professional level employees) are also important current industry needs. Assistance programs and activities in these areas will benefit medical technology companies most.

nnovationINSIGHTi Florida’s Medical Technology Clusters 2 nnovation

INSIGHTi3 Florida’s Medical Technology Clusters

II. Background

Research for this report was performed by Guy Hagen, President of Innovation Insight, Inc. under sponsorship from the Florida High Tech Corridor Council, Inc., the Tampa Bay Partnership, and the University of South Florida Office of Economic Development. The Florida High Tech Corridor Council, Inc., is an economic development partnership of the University of South Florida, the University of Central Florida, and regional economic develop-ment organizations. Work was performed from October 1st to December 14th, 2002.

Additional review, planning and oversight was contributed by Dr. Richard Streeter (USF Economic Development), Dr. Dennis Colie (USF Center for Economic Development Research), Mike Evans (Tampa Bay Partnership), Su-zanne Christman (Pinellas County Economic Development), Geary Havran (NDH Medical / Medical Manufactur-ing Consortium), Mike Poland (Gulf Coast Life Sciences Initiative), Phillis Intro and Paty Wright (Metro Orlando Economic Development Commission, Dr. Carol Steele (USF Marine Sciences / MEMS Center) and Bill Moline (Tampa Chamber of Commerce). Extensive edits and reviews were provided by Alberta Simmons of Enterprise Florida Inc., with additional participation by Michelle Bauer of the Tampa Bay Technology Forum, Trent Flood of Curley and Pynn, and staff of the Gulf Coast Life Sciences Initiative. Additional contributions were submitted by members of the Florida High Tech Corridor “core team” members. Recognition is also due Dr. Joe McCann (University of Tampa) for contributions to the survey questionnaire regarding regional competitiveness.

This report was performed in the context of three prior studies of the medical industry in central Florida:

Report on the Medical Products and Biomedical Industry (Spring, 1999). This study was the first to docu-ment the scale of medical industry in central Florida, but both the industry definition and methodology differed from this report. This report was authored and is available online from the USF Office of Economic Develop-ment.

Florida’s Medical Technology Patent Activity (Summer, 2001). This study analyzes technology transfer (as-signment and award) activity among Florida MSAs, was authored and is available online from the USF Office of Economic Development.

Medical Product Industries Cluster in Tampa Bay (Fall, 2002). The study is a cluster linkage and economic impact analysis. It has served to define the core and supporting industry categories for the medical technology cluster, and has been used as the basis for defining the industry for this research. It was authored and is avail-able from the USF Center for Economic Develeopment Research.

Unfortunately, “biotech” is becoming a buzzword that signifies different things to different people. Consequently, “Medical Technology” was selected as the description for this industry simply because it is not laden with prior and / or conflicting expectations. “Medical Technology” is used in this report as a blanket category for all primary health-science related industries, including devices, instruments, and electromedical products, biotech and bio-logical products, pharmaceutical and clinical development, and genomics and bioinformatics companies. Con-sumer services and healthcare providers are not included.

nnovationINSIGHTi Florida’s Medical Technology Clusters 4 nnovation

INSIGHTi5 Florida’s Medical Technology Clusters

III. Traditional Cluster Analysis

Although the concepts of aggregate economies and external scale benefits have existed for decades, the con-cept of industry clusters has been recently popularized by Dr. Michael Porter of Harvard University. Based upon his work (for example, “The Competitive Advantage of Nations” and “On Competition”), the cluster concept has become commonly discussed among business strategists and regional development professionals. Although his work provided few methodologies for measuring and objectively analyzing clusters, he has popularized a few heuristics which will be used in this chapter to examine the Florida High Tech Corridor medical technology cluster.

Based upon the work of Dr. Ed Feser (NC Chapel Hill), we simply define an economic cluster simply as compa-nies and organizations who are interdependent for their competitiveness.

Although geography remains a consideration, this definition de-emphasizes the role of geographic boundaries in clusters and emphasizes cluster analysis as an interactive “mode of inquiry” - a tool for enabling and guid-ing discussion, awareness, and communication between employers, producers, public sector and development professionals.

Porter’s Factor “Diamond”

The most recognized descriptive tool provided by Dr. Porter is the “Diamond” chart (below), which demonstrates the underlying and inter-related factors that effect a cluster’s competitiveness. The Diamond is used to catego-rize elements of the cluster environment that contribute to its specialization, competitiveness, and uniqueness. Essentially, the Diamond categorizes all aspects of the cluster that are external to individual companies, but that influence companies’ profitability, productivity, and growth. This tool is also useful for consideration of unique local or regional assets that are difficult replicate, and whose enhancement will benefit the cluster as a whole.

Porter’s Cluster “Diamond”

Context for FirmStrategy, Structure

and Rivalry

Factor and InputConditions

DemandConditions

Related andSupportingIndustries

nnovationINSIGHTi Florida’s Medical Technology Clusters 4 nnovation

INSIGHTi5 Florida’s Medical Technology Clusters

Context for Firm Strategy, Structure, and Rivalry: Medical technology companies in Florida (and particularly in Central Florida) have traditionally been very insular, interacting only minimally. However, over the past several years there have been many developments within this cluster that indicate a rapidly changing and growing envi-ronment. Most recently, two specialized industry associations have independently started, both based in Tampa Bay: the Florida Medical Manufacturing Consortium (MMC) and the Gulf Coast Life Sciences Initiative (GCLSI). Both organizations have missions to support the networking, competitiveness, and other needs of medical tech-nology firms, and to encourage innovation and entrepreneurism. For two years, there has been an informal “medical technology executive network” that meets throughout the year to promote social capital and networking among high-level executives, researchers, and dealmakers. Finally, several major corporate law, accounting, specialized real estate, and risk insurance firms have specialized “bio” and “medical” thrusts active in central Florida and throughout the state. While Florida’s venture capital money has traditionally come from money cen-ters in New York and Boston, more money than ever is now coming from venture funds based in Florida. There are between 15 and 20 funds based in Florida. Spurring this growth is the Florida Certified Capital Company (CAPCO) program, created in 1999. The CAPCO program’s three certified venture firms - Wilshire Partners, Advantage Capital Partners, and Stonehenge Capital - were allocated $150 million to invest solely in Florida-based companies less than two years old and are involved in developing an early-stage technology. Numerous institutional venture captial firms have offices in central Florida and a history of investing in biotech, including Lovett MIller, Advantage Capital and Stonehenge Capital. Volusia County alone documented over $150 million in medical technology capital investment expansions in 2002.

Florida has made investments in and developed the intellectual infrastructure that is critical for the biomedical technology industry’s growth. Florida has established a strong statewide advanced education network and is devoting more resources to biomedical technology and biomedical research. Florida universities and colleges produce graduates with degrees in medicine; biomedical sciences, molecular biology, biomedical engineering, materials science and engineering, biological computing, biochemical and molecular science, pharmacy, oph-thalmology, bioinformatics and medical technology, among others. Florida’s Community College System has adopted a sector consortia approach to develop new curricula in partnership with industry. In central Florida, the University of South Florida (USF), which already has a successful teaching and research medical school, College of Public Health, College of Nursing, and School of Physical Therapy has recently added new degree programs in bioengineering and bioinformatics and research centers in both biotech (neurosurgery and cell therapy) and bioengineering. USF also offers a specialized executive MBA programs for physicians. It is also home to the highly rated NCI-designated Moffitt Cancer Research center. On the East end of the Florida High Tech Corridor, the University of Central Florida (UCF) gains significant recognition for its Center for Research and Education in Optics and Lasers (CREOL),and its Institute for Simulation Technology (IST). The Florida High Tech Corridor has successful business incubators, including the award-winning University of Central Florida CFIC and the University of South Florida’s Center for Entrepreneurship and Technology, and Daytona Beach’s Medical Technologies Entrepreneurial Center complete with 2,000 square feet of “wet lab” space for biotech and pharmaceutical startups.

Several public development agencies have “biotech” or “medical tech” as a priority area, including Enterprise Florida, Pinellas County Economic Development, the Tampa Bay Partnership, the Florida High Tech Corridor Council, the Metro Orlando Economic Development Commission, the Economic Develompment Council of Col-lier County, the Business Devleopment Board of Palm Beach County, and others – not to mention the Bio Florida state industry association. Volusia County alone spends more than $400K annually marketing this sector, and reserves over $2 million in grants-in-aid to support expansions and relocations.

Demand Conditions: The principal demand consideration relates to demographics. The average age of U.S. citizens is skyrocketing as the “Baby Boomer” generation approaches retirement. This is creating a nationwide demand for senior healthcare as this sophisticated and relatively wealthy generation begins to experience senior healthcare concerns. According to a recent study by the Hudson Institute, Florida’s demographics are “ahead of the national aging curve,” wherin its average age is higher than the nation. In the Florida High Tech Corridor, this has resulted in a very extensive hospital and clinic base to support the healthcare concerns of its citizens; in

nnovationINSIGHTi Florida’s Medical Technology Clusters 6 nnovation

INSIGHTi7 Florida’s Medical Technology Clusters

Circle Diagram of Supporting Clusters

MedicalTechnology

Photonics

Aerospace /Microelectronics

InformationTechnology

Telecom-munications,Networks

Genomics,Bioinformatics,

Medical IT Services

MEMS,Sensors

Guidance andTrackingSystems

Microsensors,Instrumentation,Electromedical

Devices

Telesurgery,Virtual Anatomy

BiosensorsMedical Lasers

some rural counties, hospitals are the leading private-sector employers. This particularly demanding and large base of healthcare providers and patients encourages local development of new medical products, services, and technologies. Florida medical care is recognized internationally to the extent that it is considered an export industry (please refer to “The Economic Impact of Florida’s Hospitals” by the University of South Florida Center for Economic Development Research, 1999).

Factor and Input Conditions: Historically, Florida has had low wages and a large labor pool based upon ag-riculture and services. Since the 1950s, this has been complemented by a growing base of large aerospace manufacturers, which share many materials, education, quality control, transportation and export characteristics with medical device manufacturers. Together, this has created a strong base of precision and device manufac-turing capability within Florida and expecially the Florida High Tech Corridor region. In recent years, however, a pool of retired executives from medical sector companies throughout the U.S. has been accumulating here, and has been further augmented by highly skilled individuals entering the workforce from the University of South Florida and the University of Central Florida. In fact, St. Petersburg College has recently developed a special-ized degree program in quality manufacturing specifically designed to support medical manufacturers in the Tampa Bay region, with the financial support of the Florida High Tech Corridor Council. In addition to labor pool and manufacturing base, however, demographics again play an import part in medical technology input and cost considerations. Florida’s aging population makes an ideal test demographic for new products, devices, thera-pies and pharmaceuticals; many medical technology companies have indicated the value of research trials and corporate headquarters being located near a population that resembles the national age demographic roughly ten years from now.

Related and Supporting Industries: Central Florida, South Florida, and the Florida High Tech Corridor not only have strong manufacturing and technology industries that feed into the medical technology cluster supply chain, but there also exist several technology-based industries that complement the medical technology cluster in terms of research, technology, labor pool, innovation and entrepreneurial activity. The complementarity of these other clusters helps encourage diversification and development of “hybrid” and nontraditional applications, products and companies. The following overlapping circle diagram shows some of the most prevalent Florida clusters that complement medical technologies, partic-ularly the aerospace and microelectronics clusters (closely connected), the optics and photonics cluster, and the information technology cluster.

nnovationINSIGHTi Florida’s Medical Technology Clusters 6 nnovation

INSIGHTi7 Florida’s Medical Technology Clusters

IV. Regional Targeted Cluster Comparisons

Methodology and Sources

Regional analysis was performed using ES202 Covered Employment and Wages data for 1999 through 2001 (the most recent data available) provided by the U.S. Bureau of Labor Statistics and the Florida Bureau of Labor Statistics. Utility patent award data for 2001 were obtained by the U.S. Patent and Trademarks Office. Data from all sources was converted to standard Metropolitan Statistical Areas (MSAs) as defined by the U.S. Department of Census using the commercial ZipInfo geocode / MSA database. Although industry clusters can be smaller than, or much larger than MSA boundaries, the terms ‘cluster’ and ‘MSA’ will be used interchangably throughout this chapter. Cost-of-living data were obtained from ACCRA.

ES202 data for non-Florida regions have records withheld by the Bureau of Labor Statistics that could reveal proprietary information about individual companies. Consequently, small MSAs are more likely to have ommitted data, and as a result be under-represented in regional comparisons. Due to our aggregate definition of medical technology clusters, the combined error was expected to be sufficiently minimized for the top tiers of communi-ties for reasonable comparison.

For maximum accuracy, unomitted ES202 data were obtained for all Florida MSAs courtesy of the Florida BLS. As a result, all Florida MSA data should be fully accurate for comparison to national data and larger (particularly “Tier 1”) MSAs; however, certain MSA data must necessarily not be revealed to comply with ES202 disclosure agreements.

Standard industry codes used in this report to define “medical technology” were established by the University of South Florida’s Center for Economic Development Research (CEDR) cluster linkage and impact report, “Medical Product Industries Cluster in Tampa Bay“. These codes and their North American Industry Classification System (NAICS) statistical correlates were used to ensure consistency between studies, and are listed in Appendix I. Utility patent categories for medical technology were selected a priori based upon the definitions of the industry codes, and are listed in Appendix II.

Validity

The resources used to create this report were the best data for accomplishing the strategic and research objec-tives of the sponsoring organizations. However, there is a degree of error built into these datasets that is impor-tant to consider. First, the U.S. BLS converted from SIC-based to NAICS-based coding of their data in 2001, eliminating the possibility of historical analysis spanning that period. This study is necessarily a mix of SIC- and NAICS-based analysis. The U.S. Patent and Trademark Office switched from “Green Book” to “Red Book” en-coding of its data in 2001, which increased its utility for regional geographic analysis, but also created problems for historical comparison. The national ES202 data contains many undisclosed records, which can cause MSAs even as large as Tampa and Miami (and comparably sized MSAs across the U.S.) to be under-represented. Fi-nally, the “medical technology” industry itself was not defined based upon an empirical national analysis, but was based upon a definition of the industry as it manifested in the Tampa Bay area cluster. This has the potential to give a comparison of MSAs that may be weighted toward manufacturing as it is in the Tampa Bay area. Given these caveats, the analysis provided herein is as accurate as feasible and should be more than sufficient for purposes of strategic planning and allocation of resources to promote Florida’s medical technology clusters.

.

nnovationINSIGHTi Florida’s Medical Technology Clusters 8 nnovation

INSIGHTi9 Florida’s Medical Technology Clusters

383

0

191

2001 Florida Medical Technology Establishments by County

Geographic Distribution and Change

The following charts plot 2001 employment and wage data against a map of Florida counties. In these maps, the color (darkness) corresponds to number of establishments (from zero to 383), or number of medical technology employees (from zero to 9,200, bottom). In each map, two counties stand out: Pinellas and Miami-Dade. Duval, Hillsborough, Seminole and Palm Beach counties also are significant in the Establish-ments map.

9,200

0

4,600

2001 Florida Medical Technology Employment by County

nnovationINSIGHTi Florida’s Medical Technology Clusters 8 nnovation

INSIGHTi9 Florida’s Medical Technology Clusters

+480

-1,131

Florida Medical Technology Employment Change by County

Florida Medical Technology Establishment Change by County

+21

-21

The next two maps show employment and establishment change from 1999 to 2000. In the first map, green shades represent addition of new companies within counties (up to 21 companies), whereas red shades rep-resent attrition (up to 21 companies lost during the study period). In the second map, green shades represent the addition of up to 480 employees during the study period, and red shades represent a loss of up to 1,131 medical technology employees in one year. Consistent in both maps is a significant attrition of companies and employees from the Miami-Dade county and northwest Florida region, and a slight concentrating of companies and employees into the north Tampa Bay and Orlando Metro regions during the study period.

Overall, establishments are concentrat-ing in the urban Florida High Tech Cor-ridor counties and Broward county, and disappearing from rural Florida counties. Palm Beach county showed very strong company attrition from 1999-2000, as did Bay county.

Orange, Broward and Duval counties also show strong medical technology employment gains in from 1999-2000. Okaloosa and Miami-Dade showed the greatest employment losses.

Duval county stands out as losing com-panies and gaining employees, which represents a concentration effect dur-ing 1999-2000. Brevard county dem-onstrates the opposite, indicating an overall employment loss but probably entrepreneurial activity.

These maps show one-year change trends, which would be best considered as part of trend analysis over a longer period. As NAICS-based ES202 data become available, additional trend com-parisons are recommended beginning with the 2001 year.

nnovationINSIGHTi Florida’s Medical Technology Clusters 10 nnovation

INSIGHTi11 Florida’s Medical Technology Clusters

Targeted Regional Comparisons by Establishments

The following “bubble” chart displays U.S. medical technology clusters according to their growth / attrition (verti-cal axis), location quotient (horizontal axis), and relative number of companies (size of bubbles). The national average for 1999-2000 was an overall 10% attrition in medical technology companies. The Minneapolis region performed best over the period analyzed with over a 48% increase in number of establishments, and most of the Florida MSAs also added companies against the national trend. While it is generally considered positive to do better than the U.S. trend, if the U.S. as a whole continues to shrink in these industry sectors, individual MSAs that continue to grow may be increasing their share of a declining market.

The location quotient (LQ) simply describes how specialized a MSA is toward medical technology. A LQ of 1 signifies that MSA has exactly as the same share of medical technology companies in its economy as the nation. The LQ adjusts to the relative size of the MSA’s economy; however, the larger the economy, the less sensitive it is to individual companies for determining LQ. In this figure, Gainesville is particularly notable for having nearly six times as many medical technology companies than average, which indicates a high degree of specialization in its region’s economy. Most Florida MSAs in the figure have a positive LQ (1-1.5).

Overall, the leading Florida MSAs compare favorably against the nation regarding number of establishments. The leading MSA in terms of number of establishments is the Los Angeles - Long Beach California MSA (550

2001 Establishments

Medical Technology Clusters

Location Quotient0.5 1.0 1.5 2.0 2.5 3.0

% Change 1999-2000

-30

-20

-10

0

10

20

30

40

50

60

L.A.-Long Beach, Ca

Chicago, Il

Philadelphia, Pa-NJ

Mnpls.-St. Paul, Mn-Wi

San Jose, Ca

Dallas, Tx

Atlanta, Ga

Tampa Bay, FlMiami, Fl

St. Louis, Mo-Il

New Haven-Bridgeport, CT

Orlando, Fl

Baltimore, Md

Denver, Co

Jacksonville, Fl

Gainesville, Fl

nnovationINSIGHTi Florida’s Medical Technology Clusters 10 nnovation

INSIGHTi11 Florida’s Medical Technology Clusters

2001 Medical Technology Establishment Statistics by MSA

��� �� � ������ �������������� ����L.A.-Long Beach, Ca 0.89 -9.5 550 1Chicago, Il 1.81 16.3 487 2Philadelphia, Pa-NJ 2.81 -0.3 434 3Orange County, Ca 2.54 -8.2 397 4Boston-Brockton-Nashua, Ma-NH 1.56 -65.7 343 5Mnpls.-St. Paul, Mn-Wi 2.12 48.1 320 6San Diego, Ca 1.93 -4.2 284 7San Jose, Ca 2.77 -10.1 258 8Detroit, Mi 1.27 -6.4 177 9Cleveland-Lorain-Elyria, Oh 1.88 53.4 165 10New York-Newark, NY-NJ-Pa 0.40 32.7 155 11Nassau-Suffolk, NY 0.87 12.4 154 12Dallas, Tx 1.05 43.1 135 13Atlanta, Ga 0.68 34.5 134 14Oakland, Ca 0.93 -17.3 119 15Tampa Bay, Fl 1.33 -1.9 115.75 16Newark, NJ 1.36 3.7 109 17Bergen-Passaic, NJ 1.25 10.5 99 18Miami, Fl 0.67 -4.0 95.75 19St. Louis, Mo-Il 0.90 8.3 94 20New Haven-Bridgeport, CT 0.98 36.6 94 20Orlando, Fl 1.41 6.8 85.5 21San Juan-Bayamon, PR 1.62 0.0 83 22Houston, Tx 0.76 -49.0 80 23Baltimore, Md 1.04 16.0 77 25Kansas City, Mo-Ks 0.87 3.4 75 26Pittsburgh, Pa 0.78 -9.7 74 27Denver, Co 0.59 -26.6 66 29San Francisco, Ca 0.49 -2.0 64 30Fort Lauderdale, Fl 0.62 6.9 62.75 31Washington, DC-Md-Va-WV 0.27 751.7 55 34Cincinnati, Oh-Ky-In 0.65 21.1 45 38Jacksonville, Fl 1.06 0.0 36 42West Palm Beach-Boca Raton, Fl 0.47 -8.7 34.5 44Rochester, NY 0.83 -2.7 29 46Sarasota-Bradenton, Fl 1.02 -11.1 27.5 47Middlesex, NJ 0.60 -13.5 26 48Raleigh-Durham-Chapel Hill, NC 0.50 475.0 24 50Melbourne-Titusville-Palm Bay, Fl 1.00 13.3 18.75 53Lakeland-Winter Haven, Fl 1.07 -6.9 18 54Pensacola, Fl 1.86 -1.4 16.75 56Daytona Beach, Fl 1.43 -8.0 15.25 58Fort Pierce-Port St. Lucie, Fl 1.36 11.8 14 60Gainesville, Fl 1.52 -5.3 12.5 62Ocala, Fl 1.04 -12.5 9 65Fort Myers-Cape Coral, Fl 0.37 -8.1 8.25 66Naples, Fl 0.49 11.1 7.75 68Tallahassee, Fl 0.85 -2.0 6.75 70Huntsville, Al 0.68 30.9 6 71Fort Walton Beach, Fl 0.42 -3.2 3 72Panama City, Fl 0.43 -19.7 2.5 73Punta Gorda, Fl 0.25 -42.9 1 74

companies). Tampa Bay (Tampa-St. Petersburg - Clearwater MSA) is the leading Florida MSA with a rank of 16 (115 companies in 2001), although Miami and Orlando make very high showings. The previous table lists detailed statistics for the major medical technology MSAs, ranked by number of establishments.

nnovationINSIGHTi Florida’s Medical Technology Clusters 12 nnovation

INSIGHTi13 Florida’s Medical Technology Clusters

Targeted Regional Comparisons by Employment

In contrast with the number of establishments, clusters can also be measured by the number of employees that they support. Since this is ES202 unemployment/wage data, this includes all employees for medical technol-ogy companies regardless of job categories; it does not include medical technology employees in non-cluster companies.

Again, selected results are presented in the following bubble chart, wherein the vertical axis represents % change between 1999 and 2000, the horizontal axis represents the 2001 location quotient, and the bubble sizes represent the number of medical technology cluster employees in each MSA.

The nation as a whole lost only .2% of its medical technology employment from 1999-2000. Most notable in the following figure are the New Haven, St. Louis and Minneapolis MSAs for percentage change (St. Louis presum-ably had a few companies with significant hiring, since it only added about 10% to the number of establishments

2001 Employment

Medical Technology Clusters

Location Quotient0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5

%C

hang

e

-40

-20

0

20

40

60

80

100

120

140

160

Atlanta, GaBaltimore, Md

Chicago, IlDallas, Tx

Denver, CoGainesville, Fl

Jacksonville, FlL.A., Ca

Miami, Fl

Mnpls.-St. Paul, Mn-WiOrlando, Fl

Philadelphia, Pa-NJ

San Jose, Ca

St. Louis, Mo-Il

Tampa Bay, Fl

New Haven-Bridgeport-, Ct

nnovationINSIGHTi Florida’s Medical Technology Clusters 12 nnovation

INSIGHTi13 Florida’s Medical Technology Clusters

2001 Medical Technology Employment Statistics by MSA

��� �� � ������ ���������� ����Chicago, Il 1.94 14.0 37,179 1Philadelphia, Pa-NJ 3.65 2.7 33,562 2Mnpls.-St. Paul, Mn-Wi 2.92 41.2 27,458 3Boston-Brockton-Nashua, Ma-NH 1.93 -42.0 25,611 4San Jose, Ca 3.90 7.6 24,966 5Orange County, Ca 2.69 -0.9 24,095 6L.A.-Long Beach, Ca 0.92 2.4 23,379 7Newark, NJ 5.35 3.5 21,654 8San Juan-Bayamon, PR 5.59 -3.5 16,880 9San Diego, Ca 1.88 0.0 13,334 10Tampa Bay, Fl 1.89 1.7 9,590 11New York-Newark, NY-NJ-Pa 0.49 8.8 9,211 12Miami, Fl 1.55 -8.0 9,186 13Nassau-Suffolk, NY 1.34 13.9 9,020 14Cleveland-Lorain-Elyria, Oh 1.64 22.2 8,933 15Atlanta, Ga 0.65 3.6 7,697 16Dallas, Tx 0.80 14.9 7,133 17New Haven-Bridgeport-Stamford-Danbu 1.51 135.8 6,471 18Jacksonville, Fl 2.71 3.5 6,084 19Bergen-Passaic, NJ 1.90 10.3 5,898 20Detroit, Mi 0.61 27.3 5,342 21Oakland, Ca 0.91 -13.1 4,697 23San Francisco, Ca 0.73 34.2 3,869 26Denver, Co 0.64 -17.2 3,573 28St. Louis, Mo-Il 0.50 46.9 3,423 29Kansas City, Mo-Ks 0.65 2.2 3,306 31Houston, Tx 0.41 -46.1 3,175 33Pittsburgh, Pa 0.52 -26.8 2,803 36Orlando, Fl 0.86 25.4 2,762 37West Palm Beach-Boca Raton, Fl 0.84 3.0 2,495 39Cincinnati, Oh-Ky-In 0.52 1.2 2,418 40Baltimore, Md 0.39 8.8 1,894 45Daytona Beach, Fl 4.77 -2.7 1,830 46Rochester, NY 0.81 -12.0 1,570 51Fort Lauderdale, Fl 0.33 20.0 1,311 57Washington, DC-Md-Va-WV 0.09 812.2 1,163 60Raleigh-Durham-Chapel Hill, NC 0.46 497.5 1,128 62Sarasota-Bradenton, Fl 0.81 -9.4 1,105 64Middlesex-Hunterdon, NJ MS 0.47 -31.8 1,035 66Lakeland-Winter Haven, Fl 0.62 -15.1 559 76Melbourne-Titusville-Palm Bay, Fl M 0.62 -13.4 557 77Fort Myers-Cape Coral, Fl 0.62 0.7 549 78Pensacola, Fl 1.25 2.3 481 81Gainesville, Fl 1.06 -12.8 399 86Huntsville, Al 0.77 15.6 344 91Ocala, Fl 0.97 3.7 325 92Fort Pierce-Port St. Lucie, Fl 0.65 30.3 235 94Naples, Fl 0.35 16.1 197 95Panama City, Fl 0.69 0.8 168 96Tallahassee, Fl 0.10 18.6 32 97Fort Walton Beach, Fl 0.09 -76.5 24 98Punta Gorda, Fl 0.04 -57.1 6 99

during the same period). Denver lost significant cluster employment during this period (roughly 18%). Tampa Bay and Jacksonville MSAs remained roughly stable between 1999 and 2000, although Orlando added over 25% and Gainesville lost approximately 18%. Of the selected MSAs, Jacksonville suprisingly had the highest employment LQ (nearly three times higher than the average proportion of medical technology employment), although Tampa Bay and Miami had respectably high employment LQs as well (1.9 and 1.6 respectively). As shown on the previous table, the Chicago, Illinois MSA leads the U.S. for number of medical technology cluster employees (over 37,100), followed by the Philadelphia and Minneapolis MSAs. Tampa Bay and Miami are also significant leaders (over 9,500 and 9,100 employees in 2001, respectively). The preceding table lists detailed statistics for major medical technology clusters, ranked by medical technology employment.

nnovationINSIGHTi Florida’s Medical Technology Clusters 14 nnovation

INSIGHTi15 Florida’s Medical Technology Clusters

Targeted Regional Comparisons by Average Salary

Another indicator of technology cluster health is average salary; it represents competitiveness and demand for specialized labor, and relates at least indirectly to productivity (increasing labor costs usually precedes an increase in capitalization of production). However, average salaries can be difficult to compare without compen-sating for income taxes and relative costs of living, which are certainly factors considered by employees when considering job options. The statistics provided in the following figure compensate for both cost of living and state income taxes.

State income tax data was obtained from the Federation of Tax Administrators (web site), and based upon the av-erage raw medical technology cluster salary for all MSAs ($55,933, for 2001), and deductions for single income, one child (where deductions are allowed). Puerto Rico was not adjusted for state income tax. Rankings were based upon raw average salary adjusted only for income tax (as shown in the salary statistics table, preceding page), since consistent cost-of-living indicators were not available for all MSAs. Although the Melbourne-Titus-ville and Jacksonville MSAs (ranks #15 and #16) pay slightly more than the tax adjusted mean, Most Florida MSAs pay well below the average even compensating for the lack of state income tax and cost of living. It is worth noting that average salaries may be influenced by local labor market demand, as well as the specific skill requirements and industry specializations manifested within each region. For example, a particular MSA that has significantly more assembly and low-margin operations may exhibit lower overall average wages as well.

2001 Average Salaries Adjusted for Cost of LivingMedical Technology Clusters

2001 Adjusted Average Salary

$0 $1

0,0

00

$2

0,0

00

$3

0,0

00

$4

0,0

00

$5

0,0

00

$6

0,0

00

$7

0,0

00

MSA

L.A.-Long Beach, Ca

Dallas, Tx

Raleigh-Durham-Chapel Hill, NC

Denver, Co

Washington, DC-Md-Va-WV

Tampa Bay, Fl

Atlanta, Ga

St. Louis, Mo-Il

Orlando, Fl

Mnpls.-St. Paul, Mn-Wi

Philadelphia, Pa-NJ

Chicago, Il

Jacksonville, Fl 61,024

60,634

56,871

47,340

46,584

45,488

43,494

41,928

41,888

40,917

39,458

39,332

36,082

Blue box: Average medicaltechnology salary, entire U.S.Pink box: Average salary, entire U.S.

nnovationINSIGHTi Florida’s Medical Technology Clusters 14 nnovation

INSIGHTi15 Florida’s Medical Technology Clusters

2001 Medical Technology Salary Statistics by MSA

��������� �������������

��� ��������������

����������������

������ � ����������������� ����

Seattle-Bellevue-Everett, Wa 1.000 95,066 n/a n/a 1San Jose, Ca 0.907 83,244 n/a n/a 2Newark, NJ 0.945 82,701 n/a n/a 3San Francisco, Ca 0.907 75,681 1.992 37,992 4Philadelphia, Pa-NJ 0.972 68,757 1.209 56,871 5New York-Newark, NY-NJ-Pa 0.932 65,528 2.352 27,861 6Chicago, Il 0.970 63,423 1.046 60,634 8Boston-Brockton-Nashua, Ma-NH 0.947 62,745 n/a n/a 9Bergen-Passaic, NJ 0.945 62,621 n/a n/a 10Middlesex-Hunterdon, NJ MS 0.945 62,253 n/a n/a 11Oakland, Ca 0.907 61,227 n/a n/a 12New Haven-Bridgeport, CT 0.955 60,671 n/a n/a 13Melbourne-Titusville-Palm Bay, Fl 1.000 57,174 n/a n/a 15Jacksonville, Fl 1.000 56,936 0.933 61,024 16Huntsville, Al 0.950 56,613 0.961 58,911 17Fort Lauderdale, Fl 1.000 53,336 n/a n/a 22Mnpls.-St. Paul, Mn-Wi 0.930 53,329 1.127 47,340 23Tallahassee, Fl 1.000 50,622 1.090 46,443 24Baltimore, Md 0.952 50,352 n/a n/a 25Orange County, Ca 0.907 50,088 n/a n/a 26Miami, Fl 1.000 49,635 n/a n/a 30Detroit, Mi 0.958 47,933 n/a n/a 31San Diego, Ca 0.907 47,760 1.273 37,518 32Washington, DC-Md-Va-WV 0.905 47,291 1.129 41,888 35Orlando, Fl 1.000 46,445 0.997 46,584 38Fort Walton Beach, Fl 1.000 46,018 1.003 45,880 40Kansas City, Mo-Ks 0.940 45,744 n/a n/a 43Cincinnati, Oh-Ky-In 0.945 45,734 0.961 47,590 44Rochester, NY 0.932 45,518 n/a n/a 45L.A.-Long Beach, Ca 0.907 44,579 1.236 36,082 46West Palm Beach-Boca Raton, Fl 1.000 44,441 1.042 42,650 47St. Louis, Mo-Il 0.940 43,987 0.967 45,488 48Denver, Co 1.000 43,822 1.071 40,917 49San Juan-Bayamon, PR 1.000 43,713 n/a n/a 51Houston, Tx 1.000 43,534 0.929 46,886 53Atlanta, Ga 0.940 43,102 0.991 43,494 55Raleigh-Durham-Chapel Hill, NC 0.930 42,161 1.069 39,458 56Tampa Bay, Fl 1.000 41,697 0.995 41,928 60Daytona Beach, Fl 1.000 40,858 n/a n/a 63Naples, Fl 1.000 40,287 n/a n/a 64Dallas, Tx 1.000 40,158 1.021 39,332 65Nassau-Suffolk, NY 0.932 40,050 1.400 28,607 66Fort Pierce-Port St. Lucie, Fl 1.000 39,663 n/a n/a 70Lakeland-Winter Haven, Fl 1.000 38,623 n/a n/a 73Pittsburgh, Pa 0.972 38,032 1.030 36,924 74Gainesville, Fl 1.000 37,610 n/a n/a 75Cleveland-Lorain-Elyria, Oh 0.945 35,842 n/a n/a 82Sarasota-Bradenton, Fl 1.000 35,840 1.051 34,101 83

Further, average salary statistics only consider cash salary and not other compensation (e.g., stock and fringe beneftis).

nnovationINSIGHTi Florida’s Medical Technology Clusters 16 nnovation

INSIGHTi17 Florida’s Medical Technology Clusters

Targeted Regional Comparisons by Average Company Size

ES202 data can also provide information on average company size, which may reflect somewhat on the maturity of the cluster (more mature clusters may be expected to have larger companies, as its companies have had time to mature). The following chart and table present average company sizes, in terms of average number of employees per medical technology company. Puerto Rico ranks highest with over 200 employees per company in 2001; since it is not a large cluster (#22 in terms of companies), we can expect its cluster to be dominated by a few, probably international, companies. Jacksonville leads Florida with 169 employees per company. All Florida MSAs trail the national company size, with Miami and Tampa having 96 and 83 employees per company, respectively). The entrepreneurial nature of Gainesville’s and Orlando’s medical technology economies is well represented by their average company size statistics (32 employees per company; see table on next page). St. Louis only has 36 employees per company in 2001; most of the new hires discussed in previous sections are probably distributed among multiple companies.

Average Employees per Company0 20 40 60 80 100 120 140 160 180

MSA

Washington, DC-Md-Va-WVBaltimore, MdGainesville, Fl

Orlando, FlSt. Louis, Mo-Il

L.A.-Long Beach, CaRaleigh-Durham-Chapel Hill, NC

Dallas, TxDenver, CoAtlanta, Ga

New Haven-Bridgeport, CTChicago, Il

Philadelphia, Pa-NJTampa Bay, Fl

Mnpls.-St. Paul, Mn-WiMiami, Fl

San Jose, CaJacksonville, Fl 169.0

96.8

95.9

85.8

82.9

77.3

76.3

68.8

57.4

54.1

52.8

47.0

42.5

36.4

32.3

31.9

24.6

21.1

2001 Average Company SizeMedical Technology Clusters

Blue box: Average medical technology company size, entire U.S. (57.9 workers)

nnovationINSIGHTi Florida’s Medical Technology Clusters 16 nnovation

INSIGHTi17 Florida’s Medical Technology Clusters

2001 Medical Technology Company SizeStatistics by MSA

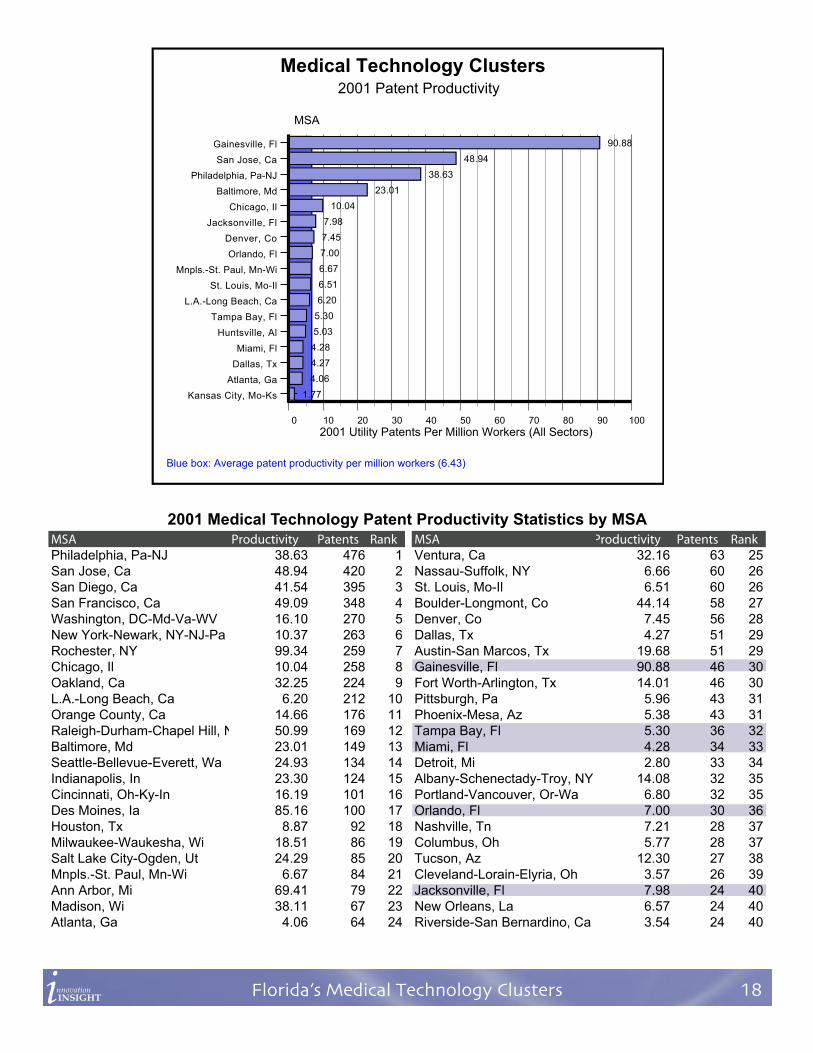

Targeted Regional Comparisons by Patent Activity and Productivity

Another critical indicator of an industry cluster’s strength is its use of innovation, research and development to increase its productivity and develop new products and markets, and one measure of innovation is the number of patent awards by region and specialty. Utility patent awards in medical technology categories (see Appendix II),

per million employees (all sectors), by U.S. MSA for 2001 are indicated in the following figure (next page).

Some factors should be considered when evaluating patent innovation. Specialized clusters with rela-tively small economies may stand out according to this statistic. Many patents are assigned to another company or institution which may be in another geo-graphic region as part of the award process. Further, the measure used in this report does not distinguish between private-sector and public-sector inventions (MSAs with federal laboratories or research agencies may have higher productivity rankings than MSAs with similar employment and establishment counts).

In 2001, the Philadelphia PA MSA is the leader in terms of “patent productivity”, with 38.6 medical tech-nology patents per million workers. The Gainesville, Florida MSA ranks #30 with an average of almost 91 medical technology patents per million workers (although Gainesville has fewer patents than Atlanta and has few medical technology companies, it has a disproportionately high patent production relative to its size). Baltimore, Maryland ranks #13 with over 23 patents per million workers, which is approximately four times the medical technology patent productivity of Tampa Bay (ranked #32) or Miami (ranked #33), although it ranks considerably lower in terms of overall employment (previous section). Of the Florida MSAs, only the Orlando, Jacksonville and Gainesville MSAs produce more than the national average. MSAs were ranked in this table by number of patents. The poor showing of the Boston MA and Newport CT regions regarding patent production is probably an artifact of inventor residence patterns or other geographic as-signment discrepancies.

MSA SizeSan Juan-Bayamon, PR 203.4Newark, NJ 198.7Jacksonville, Fl 169.0Daytona Beach, Fl 120.0San Jose, Ca 96.8Miami, Fl 95.9Mnpls.-St. Paul, Mn-Wi 85.8Tampa Bay, Fl 82.9Philadelphia, Pa-NJ 77.3Chicago, Il 76.3Boston-Brockton-Nashua, Ma-NH 74.7West Palm Beach-Boca Raton, Fl 72.3New Haven-Bridgeport, CT 68.8Panama City, Fl 67.2Fort Myers-Cape Coral, Fl 66.5Orange County, Ca 60.7San Francisco, Ca 60.5Bergen-Passaic, NJ 59.6New York-Newark, NY-NJ-Pa 59.4Nassau-Suffolk, NY 58.6Atlanta, Ga 57.4Huntsville, Al 57.3Cleveland-Lorain-Elyria, Oh 54.1Rochester, NY 54.1Denver, Co 54.1Cincinnati, Oh-Ky-In 53.7Dallas, Tx 52.8Raleigh-Durham-Chapel Hill, NC 47.0San Diego, Ca 47.0Kansas City, Mo-Ks 44.1L.A.-Long Beach, Ca 42.5Sarasota-Bradenton, Fl 40.2Middlesex, NJ 39.8Houston, Tx 39.7Oakland, Ca 39.5Pittsburgh, Pa 37.9St. Louis, Mo-Il 36.4Ocala, Fl 36.1Orlando, Fl 32.3Gainesville, Fl 31.9Lakeland-Winter Haven, Fl 31.1Detroit, Mi 30.2Melbourne-Titusville-Palm Bay, Fl 29.7Pensacola, Fl 28.7Naples, Fl 25.4Baltimore, Md 24.6Washington, DC-Md-Va-WV 21.1Fort Lauderdale, Fl 20.9Fort Pierce-Port St. Lucie, Fl 16.8Fort Walton Beach, Fl 8.0Punta Gorda, Fl 6.0Tallahassee, Fl 4.7

nnovationINSIGHTi Florida’s Medical Technology Clusters 18 nnovation

INSIGHTi19 Florida’s Medical Technology Clusters

2001 Utility Patents Per Million Workers (All Sectors)0 10 20 30 40 50 60 70 80 90 100

MSA

Kansas City, Mo-Ks

Atlanta, Ga

Dallas, Tx

Miami, Fl

Huntsville, Al

Tampa Bay, Fl

L.A.-Long Beach, Ca

St. Louis, Mo-Il

Mnpls.-St. Paul, Mn-Wi

Orlando, Fl

Denver, Co

Jacksonville, Fl

Chicago, Il

Baltimore, Md

Philadelphia, Pa-NJ

San Jose, Ca

Gainesville, Fl 90.88

48.94

38.63

23.01

10.04

7.98

7.45

7.00

6.67

6.51

6.20

5.30

5.03

4.28

4.27

4.06

1.77

2001 Patent Productivity

Medical Technology Clusters

Blue box: Average patent productivity per million workers (6.43)

2001 Medical Technology Patent Productivity Statistics by MSA��� ������������ ������� ����Philadelphia, Pa-NJ 38.63 476 1San Jose, Ca 48.94 420 2San Diego, Ca 41.54 395 3San Francisco, Ca 49.09 348 4Washington, DC-Md-Va-WV 16.10 270 5New York-Newark, NY-NJ-Pa 10.37 263 6Rochester, NY 99.34 259 7Chicago, Il 10.04 258 8Oakland, Ca 32.25 224 9L.A.-Long Beach, Ca 6.20 212 10Orange County, Ca 14.66 176 11Raleigh-Durham-Chapel Hill, NC 50.99 169 12Baltimore, Md 23.01 149 13Seattle-Bellevue-Everett, Wa 24.93 134 14Indianapolis, In 23.30 124 15Cincinnati, Oh-Ky-In 16.19 101 16Des Moines, Ia 85.16 100 17Houston, Tx 8.87 92 18Milwaukee-Waukesha, Wi 18.51 86 19Salt Lake City-Ogden, Ut 24.29 85 20Mnpls.-St. Paul, Mn-Wi 6.67 84 21Ann Arbor, Mi 69.41 79 22Madison, Wi 38.11 67 23Atlanta, Ga 4.06 64 24

��� ������������ ������� ����Ventura, Ca 32.16 63 25Nassau-Suffolk, NY 6.66 60 26St. Louis, Mo-Il 6.51 60 26Boulder-Longmont, Co 44.14 58 27Denver, Co 7.45 56 28Dallas, Tx 4.27 51 29Austin-San Marcos, Tx 19.68 51 29Gainesville, Fl 90.88 46 30Fort Worth-Arlington, Tx 14.01 46 30Pittsburgh, Pa 5.96 43 31Phoenix-Mesa, Az 5.38 43 31Tampa Bay, Fl 5.30 36 32Miami, Fl 4.28 34 33Detroit, Mi 2.80 33 34Albany-Schenectady-Troy, NY 14.08 32 35Portland-Vancouver, Or-Wa 6.80 32 35Orlando, Fl 7.00 30 36Nashville, Tn 7.21 28 37Columbus, Oh 5.77 28 37Tucson, Az 12.30 27 38Cleveland-Lorain-Elyria, Oh 3.57 26 39Jacksonville, Fl 7.98 24 40New Orleans, La 6.57 24 40Riverside-San Bernardino, Ca 3.54 24 40

nnovationINSIGHTi Florida’s Medical Technology Clusters 18 nnovation

INSIGHTi19 Florida’s Medical Technology Clusters

Combined Rankings

It should be apparent that some MSAs are relatively strong on some characteristics, and relatively weaker in oth-ers. As a result, an attempt was made to generate a balanced ranking of medical clusters by MSA that combines several of the characteristics reviewed in this chapter. The formula for the combined ranking follows:

This formula was primarily weighted toward size of the cluster by number of employees, but was sensitive to specialization in terms of number of companies, patent awards, and wages. The resulting combined ranking system should only be used as a rough rule-of-thumb comparison. Raw order rankings do not tend to be sensi-tive to scale (e.g., #1 may be 10 times bigger than #2, and so on). Combined rankings using other formula may result in different orderings.

The following table (next page) presents the combined ranking results. By breaking the ranks into tiers (ranks 1-20 as Tier 1, 21-40 as Tier 2, etc.), only two Florida medical technology clusters earn a Tier 1 position – Jackson-ville (rank #19) and Tampa Bay (rank #20). Philadelphia ranks first overall, with numerous southern California MSAs populating the first Tier. Chicago, Illinois ranks #5. Jacksonville’s strong ranking is worth note, however, it is highly dependent upon a small number of major employers without which its combined rank would drop well below #50.

Near the top of Tier 2, the Gainesville Florida MSA ranks #22 nationally almost entirely on the merit of its patent activity and establishment specialization in that MSA’s small economy. Orlando (rank #36) and Miami (rank #38) also are also positioned as Tier 2 clusters. No other Florida MSA lists within the top 3 tiers or the top 50 ranks.

Combined Rank=Cluster Medical Technology Employment x Cluster Establishment LQ x

Cluster Salary LQ x Cluster Patent LQ

Florida High Tech Corridor and Combined Regions

As noted previously, true industry clusters don’t always correlate to metropolitan statistical areas (MSAs) or any other arbitrary geographic boundary. As a result, it may be useful to combine (or even take apart) MSAs to provide a more intuitive comparison to other regions and the nation as a whole. This section provides tar-geted ES202 comparisons for multi-MSA regional definitions more commonly used in central Florida. These regions are defined as Greater Tampa Bay (Tampa-St. Petersburg-Clearwater MSA, Sarasota-Bradenton MSA, Lakeland-Winterhaven MSA), Metro Orlando / Space Coast / Volusia (Orlando MSA, Melbourne-Titusville MSA, Volusia-Flagler / Daytona Beach MSA), and the Florida High Tech Corridor (Greater Tampa Bay region plus the Metro Orlando / Space Coast / Volusia region). Combining MSAs does not result in a straightforward increase in ranking or statistics, as often the inclusion of less populous MSAs can reduce average salaries and other specialization statistics.

nnovationINSIGHTi Florida’s Medical Technology Clusters 20 nnovation

INSIGHTi21 Florida’s Medical Technology Clusters

Combined Rankings for Medical Technology Clusters

MSA Employment Estab LQ Salary LQ Patent LQ Combined RankPhiladelphia, Pa-NJ 33562 2.81 1.07 6.01 1San Jose, Ca 24966 2.77 0.86 7.61 2San Diego, Ca 13334 1.93 0.90 6.46 3Orange County, Ca 24095 2.54 0.89 2.28 4Chicago, Il 37179 1.81 1.00 1.56 5Boulder-Longmont, Co 2986 3.39 0.80 6.86 6Mnpls.-St. Paul, Mn-Wi 27458 2.12 0.91 1.04 7Boston-Brockton-Nashua, Ma-NH 25611 1.56 1.03 1.00 8San Juan-Bayamon, PR 16880 1.62 1.39 1.00 9Newark, NJ 21654 1.36 1.19 1.00 10State College, Pa 925 4.13 1.20 6.58 11Fort Worth-Arlington, Tx 5002 2.00 1.34 2.18 12Madison, Wi 2340 1.93 1.02 5.93 13Rochester, NY 1570 0.83 1.11 15.45 14Oakland, Ca 4697 0.93 0.99 5.01 15L.A.-Long Beach, Ca 23379 0.89 0.79 0.96 16San Francisco, Ca 3869 0.49 0.89 7.63 17Ventura, Ca 1409 1.66 0.92 5.00 18Jacksonville, Fl 6084 1.06 1.23 1.24 19Tampa Bay, Fl 9590 1.33 0.89 0.83 20Milwaukee-Waukesha, Wi 3371 1.25 0.77 2.88 21Gainesville, Fl 399 1.52 1.04 14.13 22Indianapolis, In 3689 0.63 0.95 3.62 23Bergen-Passaic, NJ 5898 1.25 1.00 1.00 24Seattle-Bellevue-Everett, Wa 2229 0.50 1.62 3.88 25Baltimore, Md 1894 1.04 0.98 3.58 26Cleveland-Lorain-Elyria, Oh 8933 1.88 0.71 0.55 27Nassau-Suffolk, NY 9020 0.87 0.74 1.04 28Austin-San Marcos, Tx 2377 0.88 0.89 3.06 29New Haven-Bridgeport-CT 6471 0.98 0.88 1.00 30Mayaguez, PR 2630 1.95 1.03 1.00 31Portland-Vancouver, Or-Wa 4174 1.59 0.74 1.06 32Providence-Warwick, RI 1948 2.60 1.01 1.00 33Santa Barbara-Santa Maria, Ca 1669 1.62 1.24 1.32 34New York-Newark, NY-NJ-Pa 9211 0.40 0.73 1.61 35Orlando, Fl 2762 1.41 1.00 1.09 36Ann Arbor, Mi 403 0.89 1.03 10.80 37Miami, Fl 9186 0.67 0.95 0.67 38Des Moines, Ia 438 0.69 0.96 13.24 39Raleigh-Durham-Chapel Hill, NC 1128 0.50 0.84 7.93 40Cincinnati, Oh-Ky-In 2418 0.65 0.92 2.52 41Akron, Oh 1499 1.70 0.82 1.57 42Dallas, Tx 7133 1.05 0.59 0.66 43Reading, Pa 1743 0.87 1.02 1.80 44Tulsa, Ok 1185 1.86 0.78 1.62 45St. Louis, Mo-Il 3423 0.90 0.88 1.01 46Atlanta, Ga 7697 0.68 0.72 0.63 47Detroit, Mi 5342 1.27 0.75 0.44 48Columbus, Oh 2967 0.75 1.08 0.90 49Houston, Tx 3175 0.76 0.61 1.38 50

TIE

R 1

TIE

R 2

TIE

R 3

nnovationINSIGHTi Florida’s Medical Technology Clusters 20 nnovation

INSIGHTi21 Florida’s Medical Technology Clusters

The following table presents wage and employment statistics for the combined central Florida regions. Most notably, the Florida High Tech Corridor (FHTC) region ranks a relative #8 in the nation for number of establish-ments, while demonstrating positive growth and a high level of medical technology specialization (a location quotient of 1.3)

The next table presents aggregated employment data for the combined MSAs. The employment data also dem-onstrate a high overall ranking for the FHTC and the greater Tampa Bay region (ranked #10 and #11 nationally in terms of medical technology employment). The FHTC and the Tampa Bay region both show specialization in medical technology employment as well (location quotients of 1.3 and 1.4 respectively).

The third table in this section (following page) presents patent and patent productivity statistics for the combined regions. Overall productivity levels (number of medical technology patents produced in 2001 per 1,000,000 workers) are relatively significant (national ranking in this category is based upon overall number of patent awards). In general, the patent statistics lag behind relative rankings in establishments and employment for the respective regions.

As with the MSA by MSA comparisons, the combined ranking formula was applied to the combined central Florida regions. Since regional medical technology employment levels are a consideration in the combined rank-ing, all three combined regions show very significant national rankings. The Florida High Tech Corridor ranks #16 in the nation overall. The greater Tampa Bay region ranks #19 in the nation, and the Orlando / Space Coast / Volusia region weighs in at #23. In light of the fact that the combined rankings are notably lower than these regions’ employment and establishment rankings, this indicates that their combined ranks have been reduced due to low relative salary and/or patent specializations. Efforts to increase productivity and innovation in central Florida may have a significant overall effect for improving the profile of these regions.

���� ��� � ������ ���� ������ ���������������������������� ��� ������ �� ����

Florida High Tech Corridor 280.75 0.49 1.27 8Greater Tampa Bay 161.25 -3.73 1.23 11Orlando / Space Coast / Volusia 119.5 5.98 1.33 15

���� ��� � ������ ���� ������ �������������������� ��� ������ �� ����

Florida High Tech Corridor 16,403 2.10 1.26 10Greater Tampa Bay 11,254 -0.48 1.39 11Orlando / Space Coast / Volusia 5,149 8.08 1.04 23

���� ���� ������ ���� ������ ��������� ������� ������������ �� ����

Florida High Tech Corridor 94 5.9 0.9 15Greater Tampa Bay 50 5.1 0.8 21Orlando / Space Coast / Volusia 44 7.3 1.2 22

�������� ����Florida High Tech Corridor 16Greater Tampa Bay 19Orlando / Space Coast / Volusia 23

nnovationINSIGHTi Florida’s Medical Technology Clusters 22 nnovation

INSIGHTi23 Florida’s Medical Technology Clusters

Strategic Workforce Recruitment Targets for Orlando

��� ��� �������� ������ ������ � ��� �������� ������ � ������ ����������Orlando, Fl 46,445 46,584 25.4 2,762Phoenix-Mesa, Az 42,103 38,241 -5.5 1,108Dayton-Springfield, Oh 42,152 44,185 -2.0 1,482Atlanta, Ga 43,102 43,494 3.6 7,697Houston, Tx 43,534 46,886 -46.1 3,175Grand Rapids-Muskegon, Mi 43,641 41,016 -41.7 4,033San Juan-Bayamon, PR 43,713 n/a -3.5 16,880Denver, Co 43,822 40,917 -17.2 3,573L.A.-Long Beach, Ca 44,579 36,082 2.4 23,379Rochester, NY 45,518 n/a -12.0 1,570Cincinnati, Oh-Ky-In 45,734 47,590 1.2 2,418Kansas City, Mo-Ks 45,744 n/a 2.2 3,306Charlotte-Gastonia-Rock Hill, NC-SC 45,957 46,351 -27.2 1,388

Combined Strategic Comparisons

The data presented in this chapter are very relevant for targeted development and outreach activities, particularly concerning the attraction of qualified and specilialized labor and the fostering of productive technology partner-ships. Regarding workforce activities, strategic analysis would ideally identify regions with a critical mass of medical technology cluster employees, but that had an adjusted average salary well below that of Florida clus-ters. Such regions are at a competitive disadvantage with Florida MSAs for the attraction of talent, particularly if those regions are also declining in overall medical technology employment (e.g., demonstrate a net loss / layoff of cluster jobs during the study period). In other words, Florida strengths should be matched against the selected weaknesses of other MSAs. Of course, workforce attraction activities should not be performed if the Florida region is itself losing medical technology jobs (such as Gainesville, Miami, Sarasota and Melbourne-Titusville-Palm Bay during this study period).

As shown in the following figure, strategic workforce targets for Orlando may include Grand Rapids Michigan area (lower average salary, large workforce, signifcant layoffs), Denver Colorado (slightly lower average sal-ary and layoffs, large workforce), Los Angeles California (lower average salary, slight growth, large workforce), Rochester New York (slightly lower average salary, slight growth, large workforce), and Houston Texas (lower average salary, significant layoffs).

Since the Tampa Bay MSA has a lower average medical technology salary than the Orlando MSA, strategic tar-gets for Tampa Bay also apply to Orlando. Reasonable workforce recruitment targets for the Tampa Bay MSA are limited to New York (significantly lower average salary, slight growth, large workforce), San Diego (Large workforce, lower adjusted average salary), Pittsburgh, PA (lower average salary, large layoffs, large workforce), Tulsa, OK and Riverside-San Bernardino, CA regions (lower average salary and very significant layoffs). Puerto Rico may also be an intriguing target due to large workforce and severe layoffs. Overall, New York / New Jersey, southern California, Ohio and Oklahoma appear to be consistently good recruitment targets for Florida clusters. Since the “raw” salaries (not adjusted for cost of living or income tax) for some of these regions are very high, however, recruitment efforts may have to overcome a large perceptual disparity despite the increased spending power of Tampa Bay and Orlando versus these regions.

Generally, it is preferable to “grow your own” local companies than to recruit companies to relocate from outside of a region. However, a few medical technology clusters demonstrated significant company attrition during the study period. These areas may be good candidates for recruiting entrepreneurs or vendors for relocation or ex-

nnovationINSIGHTi Florida’s Medical Technology Clusters 22 nnovation

INSIGHTi23 Florida’s Medical Technology Clusters

Strategic Workforce Recruitment Targets for Tampa Bay

��� �� � ������ ��� ������Boston-Brockton-Nashua, Ma-NH 1.46 -65.7 343Oakland, Ca 0.87 -17.3 119San Jose, Ca 2.59 -10.1 258L.A.-Long Beach, Ca 0.83 -9.5 550Orange County, Ca 2.38 -8.2 397San Diego, Ca 1.81 -4.2 284

Strategic Corporate Recruitment Targets

��� ��� �������� ������ ������ � ��� �������� ������ � ������ ����������Tampa Bay, Fl 41,697 41,928 1.7 9,590New York-Newark, NY-NJ-Pa 65,528 27,861 8.8 9,211San Diego, Ca 47,760 37,518 0.0 13,334Ventura, Ca 40,964 n/a 4.0 1,409Milwaukee-Waukesha, Wi 39,883 n/a -7.2 3,371Buffalo-Niagara Falls, NY 38,802 37,418 15.2 1,404Pittsburgh, Pa 38,032 36,924 -26.8 2,803Fort Wayne, In 37,584 n/a -17.2 3,189Tulsa, Ok 37,166 40,223 -67.2 1,185Nashville, Tn 36,064 39,087 15.2 1,037Akron, Oh 33,001 32,149 -3.4 1,499Provo-Orem, Ut 32,695 33,126 6.0 1,636Riverside-San Bernardino, Ca 31,533 28,417 -73.6 1,777Louisville, Ky-In 27,811 28,495 1.8 1,013Mayaguez, PR 23,981 n/a -48.4 2,630

Strategic Technology Partnership Targets for Florida Medical Technology Clusters

Targeted technology outreach activities may necessarily be based less on strategic advantages of Florida clus-ters, but should identify U.S. medical technologies with the highest innovation productivity. Of course, all Florida clusters would be best served to partner first with leading Florida MSAs such as Gainesville and/or leverage its innovation to link to other regions, as Gainesville has some of the highest per-worker medical technology patent production in the nation.

��� ������ ������������ ������� ��� ������Gainesville, Fl 90.88 46 50Raleigh-Durham-Chapel Hill, NC 50.99 169 55San Francisco, Ca 49.09 348 64Boulder-Longmont, Co 44.14 58 74Oakland, Ca 32.25 224 119Ventura, Ca 32.16 63 56Seattle-Bellevue-Everett, Wa 24.93 134 64Baltimore, Md 23.01 149 77Milwaukee-Waukesha, Wi 18.51 86 67Washington, DC-Md-Va-WV 16.10 270 55Fort Worth-Arlington, Tx 14.01 46 79New York-Newark, NY-NJ-Pa 10.37 263 155

pansion into Florida, on the premise that if presented a viable alternative to remaining in a declining cluster, they may opt to contribute to Florida’s clusters instead. The most significant medical technology company attrition in 1999-2000 occurred in the Boston region and southern California regions.

nnovationINSIGHTi Florida’s Medical Technology Clusters 24 nnovation

INSIGHTi25 Florida’s Medical Technology Clusters

Targeted Analysis Summary Observations

Nationally, the wage and employment data show a slight consolidation during the study period - a slight decrease in number of establishments, but very little change in overall employment. The ES202 data and patent analysis generates a few consistent observations about Florida’s medical technology clusters. First, at least three Florida regions are competitive on a national scale: Tampa Bay, Miami, and Jacksonville. In general, these regions may be considered borderline “Tier 1” U.S. medical technology clusters (within the top 20 regions compared against multiple factors). Orlando and Gainesville also have high scorings in particular areas that are worth note, but may not yet have a ‘critical mass’ for true cluster specialization. Jacksonville has a suprisingly strong presence in 2001, however it is highly dependent upon a small number of major employers; without which, its rank drops in almost every category beyond consideration as a significant cluster.

In general, Florida medical technology clusters lag well behind the nation in terms of innovation and average salary, even after adjustment for cost-of-living and income tax. Many of the top medical technology clusters benefit from the presence of government research institutions, very high standards of living, high salaries and specialized workforce, and proximity of multiple nationally recognized research universities specializing in the life sciences. One possible result may be that Florida medical technology companies are statistically oriented less toward research and development, and more toward assembly and other operations requiring relatively few Ph.D.s and specialized professionals per company (this would need to be validated by occupational analysis).

Like many of the smaller, adolescent U.S. medical technology clusters, Florida’s medical technology clusters have considerable potential for growth, especially in light of the fact that the very top clusters in the nation (south-ern California, the Boston region, and New Jersey) have suffered significant employment and company attrition from 1999 -2000. Proper positioning and commitment of resources can help claim much of the market repre-sented by these regions. It will be important to monitor fast growing medical technology clusters such as the Research Triangle (Raleigh-Durham-Chapel Hill, NC), the Newhaven CT MSA, and the Washington DC area.

Because southern California and a few other MSAs may be top medical technology clusters in terms of both size and innovation, Florida partnership activities might get “lost in the crowd” in these large, “Tier 1” clusters. As an alternative, the following table lists some of the most innovative “small to mid-size” MSAs in the U.S. in terms of medical technology patents and patent productivity. Technology outreach activities might be more effective as targeted against these smaller clusters, which are more comparable in size, visibility and influence to leading Florida MSAs such as the Baltimore,Boulder, and Seattle regions.

nnovationINSIGHTi Florida’s Medical Technology Clusters 24 nnovation

INSIGHTi25 Florida’s Medical Technology Clusters

V. Cluster Supply Chain Mapping and Opportunity Analysis

The previous section was essentially an inter-regional comparison. This chapter will largely focus on an intra-regional comparison of the medical technology cluster within the Florida High Tech Corridor region.

Supply Chain Mapping

Underlying data for this chapter were obtained from the Florida 2000 ES202 unedited unemployment and wage records (see previous chapter, the U.S. Bureau of Labor Services 2000 public employment and wage data by MSA, and the U.S. Department of Commerce 1997 industry input-output data.

Having defined the 4-digit SICs that make up the medical technology cluster, the supply chain map presented on the next page represents all SICs that buy from, or sell to medical technology SICs, with the following con-siderations:

• Only the top 99% of transactions were considered, to filter out relatively inconsequential vendor-client activity on the national level

• Transportation, personal and professional services, agriculture and mining, and selected other SICs that are common vendors to all industry categories were not selected. Analysis of only “residual” SICs is a common practice in cluster analysis, and emphasizes primary, core cluster activity.

• Evaluated SICs include both consumables and production capital purchases - in other words, all sales activity between SICs.

Although supply chains are often portrayed as linear, the vendor-customer relations within the medical tech-nology industry are multidirectional and complex. The supply chain map on the following page is a graphical representation of those relations on the national level, with ovals representing industry codes, and arrows repre-senting significant flow of goods between the ovals they connect. The ovals are colored roughly according to the industry subcluster to which they belong, with pink indicating device and instrument manufacturing subcluster, green presenting the pharmaceuticals subcluster, and blue representing the biotech subcluster. White ovals are multisector (e.g., serving multiple subclusters). “Structurally equivalent” SICs – that is, SICs that buy and sell to exactly the same other groups – are aggregated into single ovals. The graph has been arranged using a variant of the Kamada-Kawai force directed algorithm, which attempts to “disentangle” linkages and place ovals that are connected near one another. A listing of SIC category descriptions is available in this chapter.

Graphical supply chain maps such as this can be useful for quickly identifying what type of company is likely to buy or sell to companies within the local medical technology cluster. For example, if you know the SIC of a medi-cal technology company, you can use the map to idenity SICs of companies that would make likely vendors or clients, which could be matched against industry databases to provide business leads or vendor opportunities.

nnovationINSIGHTi Florida’s Medical Technology Clusters 26 nnovation

INSIGHTi27 Florida’s Medical Technology Clusters

Pro

du

ct “

Su

pp

ly C

hai

n”

for

the

Nat

ion

al M

edic

al T

ech

no

log

y In

du

stry

nnovationINSIGHTi Florida’s Medical Technology Clusters 26 nnovation

INSIGHTi27 Florida’s Medical Technology Clusters

Opportunity Analysis

The supply chain map also represents an abstract “ideal” structure of U.S. medical technology clusters. On the national scale, the level of sales between medical technology SICs requires certain capacity and employment in each SIC category. By comparing the relative size of each of these SIC categories at the local level, we can see if there is sufficient industrial presence to support a proportional level of sales among all medical technology categories. In other words, if a SIC category is under-represented compared to the national industry, that SIC may represent local undercapacity and lost wealth as that product is imported from elsewhere.

The table on the next page maps the total purchases from medical technology SICs at the national level, their relative representation at the local level, and the combined estimated purchases from that SIC by local medical technology companies. In this table, “local” is categorized as “West Florida High Tech Corridor MSAs” (Tampa - St. Petersburg - Clearwater, Sarasota - Bradenton, Lakeland - Winter Haven) and “East Florida High Tech Cor-ridor MSAs” (Orlando Metro, Melbourne - Titusville). The table is sorted by SIC in order of decreasing national sales to medical technology companies.

The “location quotient” measures the size of each SIC’s employment relative to the entire cluster, compared to that SIC’s proportion at the national level. In simpler words a location quotient of 1 indicates the local cluster has the same proportion of companies in that SIC as the national medical technology industry; anything less represents undercapacity relative to local medical technology production needs, and anything more represents overcapacity. Overcapacity is not necessarily bad, as “overcapacity” SICs may be supporting other industry clusters as well.

The estimated potential sales describes the amount of sales to that SIC by local medical technology compa-nies. This estimation is based upon several key assumptions: (1) sales are proportional to employment (e.g., productivity and local cost-of-business factors are not considered), and (2) the 1997 industry input-output tables continue to be accurate. All figures are adjusted for inflation to 2002 US dollars.

Highlighted SIC categories were identified as reasonable targets for vendor development through recruitment or entrepreneurship activities. They have been selected on the premise that if that category is under-represented in either the East or West halves of the Florida High Tech Corridor (e.g., has a location quotient of .6 or less), and there is a significant amount of purchases by local companies from that SIC, that there is an untapped op-portunity to increase local production capacity and sales in that SIC. “Opportunity” categories do not consider other factors for desirability (e.g., wage and salary levels or other characteristics of desirable company types). By attracting or growing companies in these categories, theoretically the capacity of the local medical technology cluster will be increased, and its production costs will be decreased.

Estimated national sales represents the estimated sales volume to that SIC by all U.S. medical technology companies, combined. Estimated potential FHTC Vendor Sales by SIC represent potential sales to local medical technology companies, not how much is currently spent locally. It is assumed that all sales in excess of capacity are imported, with an additional percentage imported due to other considerations (contracts, specific product requirements, previous business relations, etc.).

Based upon insufficient local production capacity and significant estimated and potential local purchases, the following industry categories are expected to make the most successful development targets: 2821, 2833, 3479, 3053, 3081, 3825, and 8731.

Categories marked with an asterisk (*) are expected to be relevant to the Florida Sales Tax Rebate program, if applied to medical technologies. Combined Florida High Tech Corridor medical technology sales to these SICs is estimated to be $55.2 per year.

nnovationINSIGHTi Florida’s Medical Technology Clusters 28 nnovation

INSIGHTi29 Florida’s Medical Technology Clusters

Est

imat

ed F

lori

da

Hig

h T

ech

Co

rrid

or

Med

ical

Tec

hn

olo

gy

Clu

ster

Sal

es a

nd

Ven

do

r R

epre

sen

tati

on

by

Ind

ust

ry C

ateg

ori

es

������

���

������

��������

���������

������

��������

���������

���������

�������������

����������

���������

���������

������

��������

���������������

���������

���������

������

��������

���������������

��������������

8731

0.21

0.23

18,947.6

116.9

154.3CommercialPhysicalandBiologicalResearch