Embed Size (px)

Citation preview

NAFANEWS NATIONAL AIRCRAFT F INANCE ASSOCIAT ION

M A R C H 2 0 0 4

Professional ClosingCompanies 4

AMSTAT ResaleMarket Data 6

Title Insurance10

NAFA B.O.D12

Letter From OurPresident 3

The USA Patriot Act5

Cape Town Treaty9

NAFA Director’s andOfficers Listing 2

Annual ConferenceREGISTRATION 15

Annual ConferenceAGENDA 14

www.nafa-us.org

2003-2004N A F A O F F I C E R S & D I R E C T O R S

JAMES F. DICKERSON, PresidentBank of America231 S. LaSalle Street, Suite 332Chicago, IL 60697312/828-4483 Fax: 312/[email protected]

DAVID DAVIS1st Source Bank100 N. Michigan, 3rd FloorSouth Bend, IN 46601800/348-2406Fax: 219/[email protected]

BUD WALKERMBNA America1100 N. King StreetWilmington, DE 19884302/458-0204Fax: 302/[email protected]

DAVID D. WARNERJaffe, Raitt, Heuer & Weiss, P.C.One Woodward Avenue, Suite 2400Detroit, MI 48226-3422313/961-8380Fax: 313/[email protected]

SHARON HOAGLIN SCHROEDERAero Records & Title Company P. O. Box 19246 Oklahoma City, OK 73144 405/239-2507Fax: 405/681-2047 [email protected]

KEN DUFOUR Aviation Management Consulting 3645 Foxborough Lane, #1011ARockford, IL 61114 815/633-1684Fax: 815/633-1696 [email protected]

RICHARD CROFTONCIT Group1540 W. Fountainhead ParkwayTempe, AZ 85282480/784-1801Fax: 480/[email protected]

JOHN W. PUFFERNational Aircraft Finance Company3907A Aero Place Lakeland, FL 33811 863/644-8463Fax: 863/646-1671 [email protected]

JOSEPH J. DINI, Vice PresidentMerrill Lynch CapitalBusiness Aviation Finance380 Hanscom Drive, Hanscom FieldBedford, MA 01730781/274-0909Fax: 781/[email protected]

KAREN GRIGGS, Exec.Director/TreasurerNational Aircraft Finance Assoc.P. O. Box 85Poolesville, MD 20837301/349-2070 Fax: 301/[email protected]

TONY KIOUSSIS, SecretaryJSSI® (Jet Support Services, Inc.)4310 Starwood DriveViewtown, VA 22746540/937-2299 Fax: 540/[email protected]

2

GREETINGS! During the winter months in Chicago, it is always nice to look forward to the annual

NAFA Conference in the spring. This year we will meet in beautiful Napa Valley at the Silverado

Resort on May 12-14. This year’s conference will be preceded with our fourth annual NAFA/ASA

Appraisal Education Seminar. This is an excellent opportunity for aircraft credit underwriters and others to

gain a better understanding of collateral values and the appraisal process. The NAFA Conference this year

will have a new feature, a Vendors Forum on Wednesday morning May 12. This will be a good opportunity to

meet many of our Associate members and receive an update on their products and services that support the

aircraft finance process. Wednesday afternoon will include our annual golf outing and a special wine tour of

several of the local vineyards and wineries. The reception and buffet on Wednesday evening will be at

Mondavi’s Copia Room.

We have a full program scheduled for May 13, with leading industry representatives on current issues affect-

ing our industry. The popular afternoon breakout sessions will provide insightful panel discussions on a range

of issues, and time for Q & A with each presenter. Dinner on Thursday night will feature Doc Blakely, a pop-

ular humorist. On Friday morning May 14, we will all have time for visiting over a breakfast buffet prior to

departure.

I am pleased to announce that the NAFA Board of Directors has amended the By Laws to expand the Board

to 11 members, including an increased representation from the Associate members to 5 from 3. (Please see

the article from our General Counsel David Warner). Nominees for election to the NAFA Board are Michael

Amalfitano from Fleet Capital Leasing, Keith Graham from First Essex Bank, and Associate Members Andrew

Young from Amstat, Nel Sanders-Stubbs from Conklin & de Decker and David Warner from Jaffe, Raitt, Heuer

& Weiss. Nominations for NAFA officers for 2004-2005 are Joe Dini from Merrill Lynch as President of NAFA,

David Davis of 1st Source Bank and Richard Crofton of CIT as Vice Presidents, David Warner as General

Counsel and Anthony Kioussis from JSSI® as Secretary of the of the NAFA Board. Please join me in congrat-

ulating these NAFA members in their leadership positions. I would also like to thank Bud Walker from MBNA

America Bank for his many contributions. Bud’s 3-year term on the board expires this year.

I look forward to seeing you all in May in Napa Valley.

Best regards,

Jim

g NAFA News - March 20043

A LETTER FROM OUR

PRESIDENT

PROFESSIONALCLOSING COMPANIES

By Kenneth G. MayfieldVice President & General Counsel, Aero Records & Title Company

The ultimate objective in any aircraft transaction is thetransfer of ownership and/or creation of a securityinterest in favor of a lender. There are many ways to

join the two links of the chain, i.e., from the seller to thebuyer and lender. Professional aircraft closing companiesprovide this link through one stop shopping for title servic-es, escrow closing services, aircraft title insurance andassistance with §1031 like-kind exchanges. Using theseservices costs only a fraction of the money spent in sellingor acquiring an aircraft. Indeed the cost is often little morethan one or two fuelings for the aircraft. The result is asavings of thousands of dollars that might otherwise bespent on years of litigation in resolving problems that areprevented from happening in the first place.

Ideally, the prospective aircraft purchaser will order a titlereport early in the transaction. The title report is preparedfrom a search of all of the relevant records maintained bythe FAA Aircraft Registration Branch. Since there are nomarketable title acts for aircraft comparable to those forreal estate that limit the life of various claims and defectsagainst the title, the records for each aircraft are searchedfrom the beginning of the file, whether that is six months orsixty or more years. The title report will show the followinginformation:

1. A complete description of the aircraft including

registration number and serial number;

2. Name and address of current registered owner;

3. Type of registration, e.g., individual, corporate, etc.;

4. How and from whom title was passed along withthe dates and recording data of the document passing title;

5. Encumbrances recorded against the aircraft thathave not been released of record;

6. Any additional information regarding unrecordeddocuments or other documents in the file affecting titleto or an interest in the aircraft.

Since the FAA does not determine ownership of aircraft,the certificate of registration is not a certificate of title anddoes not establish ownership, and the priority of liens andvalidity of documents is controlled by state law, there is lit-tle advantage to having a legal opinion instead of a titlereport. An attorney examines the same documents as atitle examiner and neither one will go beyond the FAArecords. Only Aircraft Title Insurance can offer protectionfrom claims not shown in the FAA records.

The escrow and closing services offered by the profession-al aircraft closing company are one of the most valuableservices available to the aviation public. By its nature, avi-ation is mobile and global. Buyers, sellers and lenders areusually in different states and frequently in different coun-tries. All are usually strangers and may only know eachother by reputation, if even that.

The professional closing company offers a neutral, con-venient, experienced, cost-effective, insured and bondedvehicle for receiving, and the simultaneous exchange of,money and documents, and the prompt filing of appropri-ate documents with the FAA through escrow.

“Escrow” by definition means neutral, independent fromthe parties to the transaction. In popular usage, the term“escrow” is used to refer to the general arrangement underwhich property is delivered to a third person to hold untilthe occurrence of a condition, and upon occurrence of thecondition, relinquishment of the property to the intendedrecipient. The purpose of escrow is to carry out an obliga-tion that is already contracted for. Since an escrow agentis a trustee with respect to property held, each party to thetransactions has assurance the property deposited is safeuntil released by the depositor.

NAFA News - March 20044

THE CRITICAL LINK IN THE CHAIN OFAIRCRAFT OWNERSHIP TRANSFER

CONTINUED ON PAGE 8...

NAFA News - March 20045

On October 26, 2001, President Bush signed theUSA PATRIOT Act,1 giving the government newpowers against terrorism. Passage of Title III of

the Act, entitled International Money LaunderingAbatement and Anti-Terrorist Financing Act of 2001,opened a new chapter in the ongoing efforts of financecompanies and aircraft sellers to guard against the use ofaircraft finance or sale transactions for disguising, or “laun-dering,” money from illegal or illicit activities.

Although the full impact of the Act on finance companiesand aircraft sellers is not yet entirely clear, the primaryimpacts thus far have been to cause them to further focustheir pre-USA PATRIOT Act anti-money laundering effortsand take steps to institute anti-money laundering pro-grams. Aircraft lenders and sellers have always been onguard against money laundering, since they are motivatedto avoid losses and to be promptly paid in good funds.Obtaining credit applications, credit reports, credit refer-ences, financial statements, tax returns, confirmation ofthe good standing of business entities and checking thegovernment lists of known or suspected terrorists andother criminals

2 are steps taken by lenders to avoid credit

losses. They are also part of a lender’s anti-money laun-dering “know your customer” program. Similarly, havingwell-established relationships with their customers, obtain-ing names, addresses, phone numbers and other informa-tion about their customers, visiting customers personallywhen reasonable and practicable, and checking govern-ment denied persons lists are steps that aircraft manufac-turers have taken for many years, since they do not wantto build an aircraft unless they are sure the customer cantake delivery and pay them with good funds. The samesteps that guard against credit losses, fraud and lost salesalso protect against doing business with customers who

are involved in criminal activities and, potentially, in dis-guising the proceeds of their crimes.

In this regard, the General Aviation ManufacturersAssociation, the National Aircraft Resale Association andmembers of the National Aircraft Finance Association haveworked together to produce GAMA’s “Guidelines forEstablishing Anti-Money Laundering Procedures andPractices Related to the Purchase of General AviationAircraft.” These guidelines can be viewed at GAMA’s web-site at http://www.ama.aero and are required reading forall aircraft lenders and dealers.

These ongoing efforts, as well as the existence of tradi-tional institutional and legal safeguards, combine to detectand prevent potential attempts to launder money in con-nection with the sale or financing of aircraft. Legal safe-guards include the Federal Aviation Act, which provides,among other things, a system of aircraft registration, own-ership data and marking. Other safeguards include exportcompliance laws, restrictions on transactions with embar-goed countries, international treaties, such as the GenevaConvention on the International Recognition of Rights inAircraft, and the specific laws and regulations applicable tothe payment system operated by the banking industry.

Section 352 of the Act amends the Bank Secrecy Act in 31U.S.C. §5318(h) to provide that each “financial institution”shall establish anti-money laundering programs. Theseprograms are required to include (1) the development ofinternal policies, procedures and controls; (2) the designa-tion of a compliance officer; (3) an ongoing employee

By David L. BlakemoreVice President & General Counsel, Cessna Finance Corporation

CONTINUED ON PAGE 8...1 Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act, Public Law 107-56, 115 Stat. § 101 et seq. (October 26, 2001).

2 The four most commonly checked lists are the U.S. Treasury’s Specially Designated Nationals (SDN) List, the U.S. Department of Commerce’s Denied Persons List, the U.S. Department ofCommerce, Bureau of Industry and Security’s Entity List, and the U.S. Department of State’s Debarred Persons List. These lists can be accessed through the Bureau of Industry and Security’s websiteat http://www.bxa.doc.gov, among other methods.

THE USA PATRIOT ACTTHE IMPACT ON FINANCE COMPANIES

AND AIRCRAFT SELLERS

NAFA News - March 20046

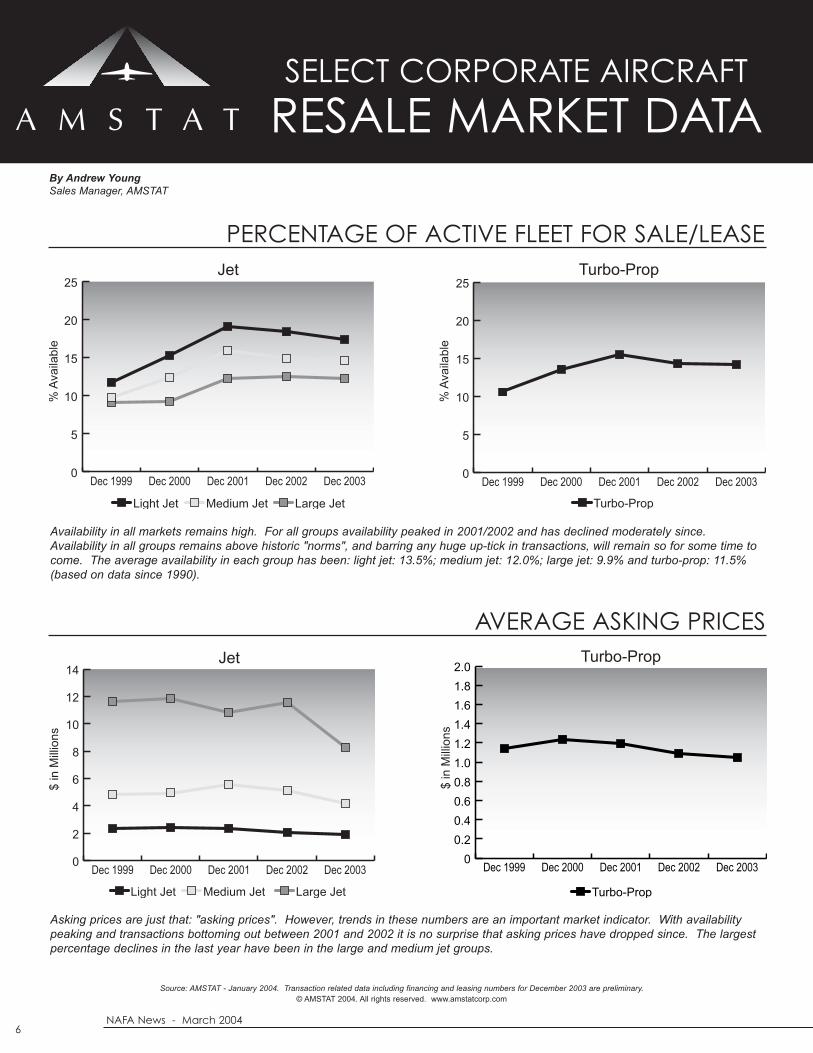

0

5

10

15

20

Availability in all markets remains high. For all groups availability peaked in 2001/2002 and has declined moderately since.Availability in all groups remains above historic "norms", and barring any huge up-tick in transactions, will remain so for some time tocome. The average availability in each group has been: light jet: 13.5%; medium jet: 12.0%; large jet: 9.9% and turbo-prop: 11.5%(based on data since 1990).

0

2

4

6

8

10

12

14

0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

AVERAGE ASKING PRICES

Asking prices are just that: "asking prices". However, trends in these numbers are an important market indicator. With availabilitypeaking and transactions bottoming out between 2001 and 2002 it is no surprise that asking prices have dropped since. The largestpercentage declines in the last year have been in the large and medium jet groups.

SELECT CORPORATE AIRCRAFT

RESALE MARKET DATA

0

5

10

15

20

25

PERCENTAGE OF ACTIVE FLEET FOR SALE/LEASE

By Andrew YoungSales Manager, AMSTAT

Source: AMSTAT - January 2004. Transaction related data including financing and leasing numbers for December 2003 are preliminary.© AMSTAT 2004. All rights reserved. www.amstatcorp.com

NAFA News - March 20047

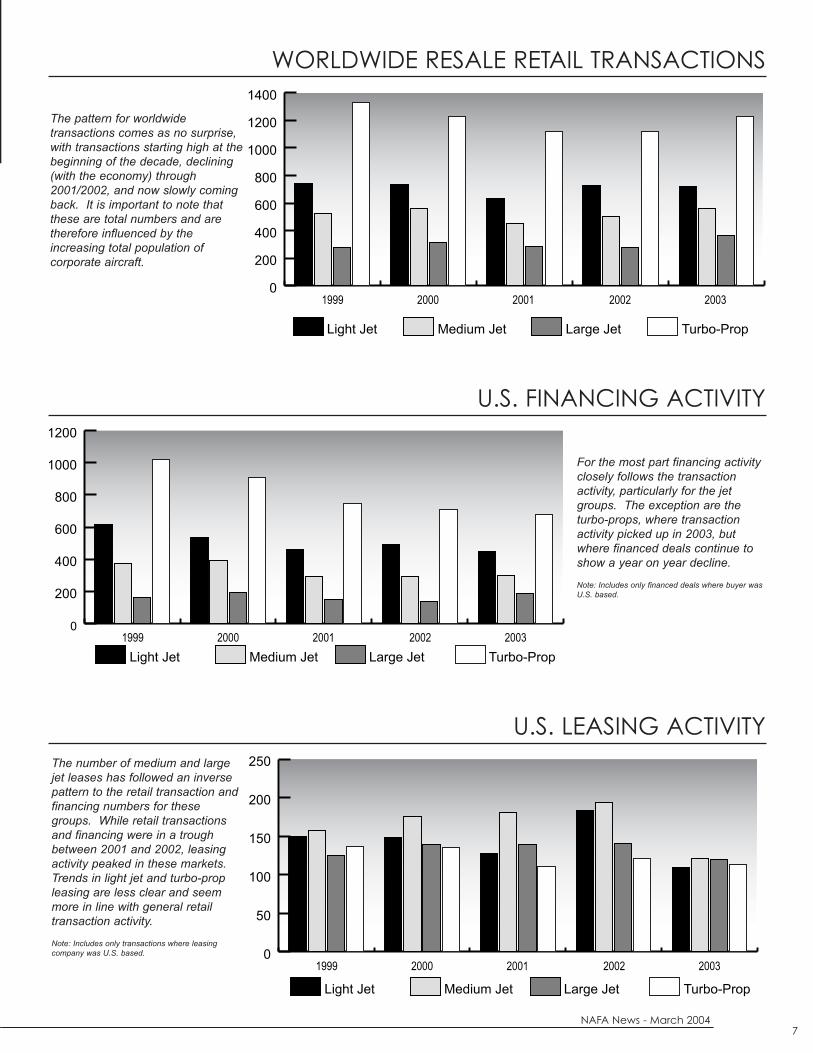

WORLDWIDE RESALE RETAIL TRANSACTIONS

The pattern for worldwide transactions comes as no surprise,with transactions starting high at thebeginning of the decade, declining(with the economy) through2001/2002, and now slowly comingback. It is important to note thatthese are total numbers and aretherefore influenced by the increasing total population ofcorporate aircraft.

U.S. FINANCING ACTIVITY

U.S. LEASING ACTIVITY

For the most part financing activityclosely follows the transactionactivity, particularly for the jetgroups. The exception are theturbo-props, where transactionactivity picked up in 2003, butwhere financed deals continue toshow a year on year decline.

Note: Includes only financed deals where buyer wasU.S. based.

The number of medium and largejet leases has followed an inversepattern to the retail transaction andfinancing numbers for thesegroups. While retail transactionsand financing were in a troughbetween 2001 and 2002, leasingactivity peaked in these markets.Trends in light jet and turbo-propleasing are less clear and seemmore in line with general retailtransaction activity.

Note: Includes only transactions where leasingcompany was U.S. based.

NAFA News - March 20048

training program; and (4) an independent audit function.The statutory definition of “financial institutions” in theBank Secrecy Act includes “loan or finance companies”and “a business engaged in vehicle sales, including auto-mobile, airplane and boat sales.” However, subparagraph(2) of section 352 of the Act allows the Secretary of theTreasury to (i) prescribe minimum standards for such anti-money laundering programs, and (ii) exempt from theapplication of those standards any financial institution notsubject to the implementing regulations contained in part103 of Code of Federal Regulations Title 31.

Since neither “a loan or finance company,” nor “a businessengaged in vehicle sales, including automobile, airplane,and boat sales” is subject to the current U.S. Treasury reg-ulation, which is contained in 31 C.F.R. § 103.11(m),another impact of the Act has been that aircraft sellers andaircraft finance companies, including GAMA and variousGAMA and NAFA members have, for a wide variety of rea-sons (including that the industry’s voluntary guidelines andthe established legal and institutional safeguards alreadyin place make it highly likely that illicit activity can be iden-tified and avoided) encouraged the Secretary of theTreasury to exempt them from any standards prescribedfor anti-money laundering programs under section 352 ofthe Act. This was done in response to an Advance Noticeof Proposed Rulemaking (ANPRM) regarding Anti-MoneyLaundering Programs for Businesses Engaged in Vehicle

Sales, which was issued by the Department of Treasury,Financial Crimes Enforcement Network (FinCEN), onFebruary 24, 2003, in Vol. 68, No. 36, of the FederalRegister. The ANPRM can be viewed at FinCEN’s websiteat http://www.fincen.gov, under USA Patriot Act Info.,Federal Register Notices.

All aircraft lenders and lessors, not just finance companies,could potentially be included in a regulatory category ofbusinesses engaged in aircraft sales, since they may sellrepossessed aircraft. In addition, re-sale of aircraft comingoff lease makes aircraft lessors potentially subject to regu-lation as aircraft sellers. In this way, aircraft lenders andlessors could become subject to more than one set of reg-ulations. For example, a finance company could be sub-ject to regulation as such, in addition to being subject to asecond set of potentially inconsistent regulations as an air-craft seller.

What, if any, further impacts the Act has on finance com-panies and aircraft sellers will largely depend on whetherapplicable regulations are ultimately issued by the U.S.Treasury Department. Because no Notice of ProposedRulemaking (an “NPRM,” as opposed to an “ANPRM”)regarding anti-money laundering programs for financecompanies or for businesses engaged in vehicle saleshave been issued by the Department of Treasury, it is notknown if regulations applicable to finance companies oraircraft sellers will be proposed or if these businesses willbe exempted from any such regulations by the Secretaryof the Treasury. (

Escrows are easy to establish. There must be an agree-ment between a buyer and seller for the purchase/sale ofan aircraft and an agreement to use a neutral third partyas the escrow agent to receive and relinquish property.The designated escrow agent must agree to act as theescrow agent. There must be a delivery of property (i.e.,funds and or documents) to the escrow agent along withinstructions stating the conditions that must occur beforethe property is relinquished to the intended recipient.Finally, when the parties are ready to close, the buyer andseller will inform the escrow agent the conditions of deliv-ery are satisfied and to relinquish the property in escrow tothe intended recipient. In an aircraft transaction, thismeans the seller and lien holders of record are paid andthe bill of sale, application for registration, lien releases orother curative documents and new security agreement arefiled with the FAA for recording.

In post-U.S.A. Patriot Act America, there are special con-siderations that must be recognized in connection with thereceipt and disbursement of funds in an aircraft transac-tion. To avoid being engaged in the money transmissionor money services business, the receipt and disbursementof funds must be an integral part of the execution and

settlement of a transaction other than the funds transactionitself (for example, in connection with a bona fide sale ofproperty). Integral means essential for completion of thetransaction. This means that funds deposited into escrowmust only come from the buyer identified in the purchasecontract or the new lender who will be receiving a securityinterest in the aircraft. Funds disbursed from escrow mayonly go to the seller of record, lien holders of record pro-viding releases, brokers identified with the transaction frominception of escrow.

The acquisition of an aircraft is expensive. The cost of agood broker, pre-purchase inspection, sales or use taxes,hull insurance, travel expenses and time is substantial.The cost of the professional closing company’s services,including aircraft title insurance is usually less than 1% ofthe costs of the aircraft. Trying to save money here isfalse economy.

Adverse claims and title defects can be a minefield for thenovice and experienced aircraft buyer alike. While mosttransactions are trouble free, the same thing can be saidabout walking through a low-density minefield. If you don’tstep on a mine, there is no problem. If you do step on amine, the consequences can be catastrophic. Fortunately,for relatively nominal cost, others will walk through theminefield for you. (

PROFESSIONAL CLOSING COMPANIES

...CONTINUED FROM PAGE 4

PATRIOT ACT

...CONTINUED FROM PAGE 5

As everyone interested knows, the Conventionand Protocol (aircraft equipment) were signed inCape Town on November 16, 2001.

As of this date, four countries have deposited docu-ments evidencing ratification of both Convention andProtocol with UNIDROIT. (None of the countries havedeclared designated entry points within their countries).As to those countries, the Convention only comes intoforce in early spring 2004.

The Protocol requires eight countries for ratification. Itis not anticipated that the additional required four coun-tries will ratify until later this year. That means that forall purposes we are not likely to see the Protocol inforce until much later this year. (Eighth country todeposit ratification documents with UNIDROIT plus 90days).

U.S. Government agencies and industry are hopefulthat, not only will the Treaty (Convention and Protocol)come into force later this year, but that in the next sev-eral months the United States will ratify the Treaty. Tothat end, the White House has submitted the Treaty tothe U.S. Senate. Presently, U.S. Government andindustry are actively seeking early review by theSenate Foreign Relations Committee. No opposition toU.S. ratification is anticipated and it is expected thatthe Treaty will come up early on the Senate’s agenda.

U.S. ratification will be premised upon FAA being theU.S. entry point to the International Registry.

In closely related activity, in November, 2003,Transportation Secretary Mineta forwarded to theSenate and the House of Representatives, proposedconforming amendments to the Transportation Code

with in clued making FAA the entry point to theInternational Registry.

Early in 2003, FAA had briefed Congressional stafferson the proposed legislative changes and everythingwent smoothly. The staffers will be briefed again verysoon. (Aviation committees in both House andSenate).

It is hoped that Treaty ratification and legislation toamend the Transportation Code will be enacted closeto one another. Funds have recently become availableto ICAO as acting Supervisory Authority to initiate theRequest for Tender to establish the InternationalRegistry. Earlier in January 2004, the ICAO SecretaryGeneral on behalf of the Preparatory Commission forthe International Registry gave general notice that theRequest for Tender may be obtained by contactingICAO by February 18, 2004. Tenders will likely have tobe submitted by offerors by the middle of April 2004.The submissions will then be evaluated and it is likelythat an award will be made by the PreparatoryCommission acting in special session in Montreal, bythe end of May 2004. Following development, testing,and commissioning, the International Registry shouldbe ready for operation when the Treaty comes intoforce.

The FAA Aircraft Registry is also gearing up, coming upwith procedures and forms necessary for transmissionof information related to international interests andprospective international interests to the InternationalRegistry.

It appears that 2004 is likely to be the year we see an oper-ational International Registry and FAA entry point. (

NAFA News - March 20049

CAPE TOWNTREATY

STATUS REPORT:FEBRUARY 1, 2004

By Joseph R. StandellAeronautical Center Counsel

Title Insurance in the aircraft industry is a relatively newdevelopment. Relative in the sense that the central air-craft registry has been operational since 1958 when the

Federal Aviation Administration Civil Aircraft registry was firstauthorized. Title insurance has only been available since themid-1980’s. The concept of title insurance was applied to air-craft by Bill Cheek, an attorney in Oklahoma City. Bill’s fatherwas also a lawyer in Oklahoma City. They issued title opin-ions and handled closing escrows for many years. By thetime Bill was ready to retire in the late 1980’s he had foundthat aircraft titles had become much more complex bothbecause of the increasing complexity of the law and the num-ber of transactions in the chain of title. Bill had handled anumber of real estate transactions in his career and was ableto see the value of title insurance in those transactions. Hebelieved there was no reason why aircraft transactions, whichmany times involve dollar amounts equal to or exceeding realestate, should not have a similar product available. The earlyaircraft policies only insured the accuracy of the FAA records.The policies have developed to the point that they can nowprovide protection against risks, many of which are not evidentfrom the FAA records.

The truth is that aircraft transactions benefit far greater fromtitle insurance than real estate. From a legal standpoint, realestate law and personal property law have developed fromsimilar but very different roots. In the English common lawlegal system, real estate was the primary source of power andwealth. Personal property was secondary. This caused differ-ent rules to develop between personal property and real prop-erty. From a practical standpoint, land is stationary. Personalproperty, particularly aircraft, are mobile. Real estate titlerecords must be in writing and are found in the courthouse inthe county where the land is located. If an interest is not partof the public records in that location, it is generally unenforce-able. The laws of that locale control real estate ownership andlien rights, without regard to the citizenship of the owner.Ownership of personal property, on the other hand, is general-

ly determined by the laws of the state of residence of theowner no matter where the property is located. Ownershipmay be transferred by change of possession, not a writtendocument. Consensual lien rights can be controlled by thelaws of the state of the owner’s residence, the location of thepersonal property or some other locale agreed upon by theparties. Non-consensual liens (mechanics and materialmenliens) are often controlled by the location of the personal prop-erty when the lien attaches. Often, there are no ownershiprecordation requirements for personal property. Even whenthere are recordation requirements, recordation can be for pur-poses of taxation rather than ownership and are usually not acomplete history. Once one finds the real estate, ownershipcan be determined by looking at public records where thatproperty will always be located. Once one locates personalproperty, they have no better idea who owns it or has a lien onit than they did before they located it. These are only a few ofthe inherent issues created by the history and mobility of per-sonal property.

Aircraft are and will always be personal property first and air-craft second. Aircraft by their nature are very mobile. It wasdetermined early in aviation history that a central registrywould be necessary in the regulation of aircraft. In the late50’s, the FAA was charged with the responsibility of maintain-ing the records necessary for this aircraft regulation.Ownership was one of the necessary pieces of informationbecause only an owner can register an aircraft. Secured par-ties’ rights were captured because under the GenevaConvention, a plane cannot be exported to another countrywithout the lienholder’s consent. However, the FAA was neverintended to be the exclusive repository of ownerships records.This is probably most evident by the express language of theTransportation Code that expressly prohibits federal tax liensfrom being filed at the FAA. They are filed locally in the countyof the residence of the taxpayer. However, they do become alien on the aircraft once filed locally. There are other exam-ples, many of which I will explore later in this article, but the

NAFA News - March 200410

By David A. CheekPresident, Aircraft Title Insurance Agency, Inc.V.P., McKinney & Stringer, P.C.

ITS TIME IS NOW

TITLEINSURANCE

federal tax lien is the best example of the fallacy of the com-mon myth that the FAA’s records are conclusive on the issueof aircraft ownership.

The FAA registration system is somewhat unique from manyrecordation systems. Not everything that is “filed” must be“recorded”. The FAA reviews every filing and only if it meetsthe FAA standards is it subsequently made part of the officialrecord by “recordation”. This gap between filing and recorda-tion can be weeks or months. If rejected, the “filed” docu-ments may never become part of the official record. It createssome interesting potential issues for both owners and lenders.

Every chain of title contains multiple documents. Some aresubject to interpretation. I have seen very old leases that haveexpired by their express terms, but never expressly released,reported on one title report as an exception. I have seen thesame plane reported as having a “clean title” by a differentreporting source. There are no uniform reporting standards, itis left to the discretion of the reporting agency.

The enforceability of specific agreements is always determinedunder state law and not federal law. Requirements forenforceability of agreements can vary significantly from stateto state. Which state’s laws apply can itself be an unclearissue. Just because a document is recorded at the FAA doesnot mean that it is enforceable under applicable state law.Many of these issues cannot be detected from the face of thedocuments. An example is whether an individual is of majorityage. It will be determined by the laws of that particular state.Majority age varies from state to state. The age of a transferoris not available from the FAA records. Other examples ofcapacity that are not ascertainable from the documentsinclude mental capacity, corporate or other representativecapacity.1

A related but distinct issue is authority to act. An individualmay be the duly appointed trustee, but that trustee’s powersmay be expressly limited in the trust agreement or by applica-ble state law. The FAA maintains some records as to the exis-tence of corporate and other business entities, but there is nofollow-up as to the entity’s continuing charter in the state of ori-gin. The potential risk is increased even more when oneunderstands that most of these transactions occur based onunauthenticated documentation.

I have heard it said that transferor’s capacity and authority isnever an issue because the purchaser/lender can verify it atthe time of the transaction independent of the FAA records.Assuming that to be true in the most current transaction, howcan anyone possibly verify prior transferors’ capacity and/orauthority in each of the transactions in the chain of title. Alongthe same lines, but a somewhat different issue is the one offorgery, either in the transfer of title or release of a lien or secu-rity agreement. As the U.S. fleet gets older, there are moreand more transactions in each chain of title. It is axiomatical

that the risk that one of them may be subject to challengeincreases. The base documents involving prior transactionsare not available to check even if one were able to invest thetime.

Another issue resolved solely by applicable state law is the rel-ative priority of competing interests, including liens. This isalso always determined by the applicable state law and isnever determined by federal law although the interests mightbe filed of record under federal law.

Neither the FAA, nor any title company or lawyer, no matterhow hard they try or how accomplished they might be in theirdue diligence throughout the transaction and review of the cur-rent transactional documents, can detect these potential prob-lems. Every title report and legal opinion is very careful tostate that they are reporting what is on file at the FAA and pre-sume the accuracy of the documents of record. As previouslynoted, there are no uniform reporting standards. These obser-vations are by no means intended to be in any way a deroga-tory remark on the FAA, any title company, FAA counsel orlawyers. It is just a statement of recognition of the inherentlimitations of the current system.

As the world becomes smaller, imports are more often anissue. The potential issues can vary depending on whether animport comes from a treaty country2 or other registry. Underthe Geneva Convention, a plane cannot be exported off of anaircraft registry unless the lienholder consents or there is nolien. There is a difference of opinion as to whether consent toderegister releases the lien or only consents to its deregistra-tion on the one registry to be rerecorded on the new registry.Some countries make no effort to even note lien status on thederegistration certificate. A “clean” certificate of deregistrationis no assurance that there is no lienholder. Many non-treatycountries do not even attempt to register owners, just opera-tors. Forged deregistrations from other countries haveoccurred. Insuring proper deregistration is important. TheTransportation Code is clear that an airplane can only be reg-istered on one registry at a time.

Title insurance is now available to insure against loss from allof these risks not only in the transaction insured, but also in allof the prior transactions throughout the chain of the title. Tenyears ago, title insurance was virtually unknown. Today, titleinsurance is often considered for known and obvious problemsin the FAA records. However, the time has come to incorpo-rate title insurance into every transaction just as the real estateindustry has done. The potential pitfalls and losses are muchgreater in the aircraft industry. The dollar value at risk is equalor greater. The number of transactions in each chain of title isincreasing. The benefit of insuring against loss from thesesources is apparent. The added cost is very reasonable.

NAFA News - March 200411

CONTINUED ON PAGE 13...1 When Limited Liability Companies were initially authorized, the Transportation Code had no provision for such an entry owning an aircraft. The FAA used the corporate forms for registration. It wasnot uncommon for the manager of an LLC to sign as “president” even though the entity had no such office because that was a corporate title the the FAA recognized.

2 This refers to a country that is signatory to the Geneva Convention. Those countries can be located at http://www.jurisint.org.

NAFA News - March 200412

By David D. Warner, NAFA Board MemberGeneral Counsel, Jaffe, Raitt, Heuer & Weiss

Arenewed emphasis on corporate governance issweeping the country in the wake of Enron,Worldcom, Tyco, Kmart, etc. Most of you have

heard of the Sarbanes-Oxley Act, which imposes numer-ous strict requirements on corporations and their boards,executives, officers, accountants and attorneys – all aimedat improving the integrity of the corporate governance sys-tem. SOX applies most directly to public companies, anddoesn’t apply directly to a non-profit association like NAFA,but still the goals and principles of that law – and theboard-room improvements being implemented as a result– serve as a good example for NAFA.

Your board is committed to ensuring that NAFA continuesto serve the interests of its members. To that end, yourBoard recently completed a review of our corporate gover-nance structure and policies, intended to assess andimprove how we go about fulfilling our mission to serve ourmembership. As a result of that review, your Board haschanged its structure and composition, and adopted poli-cies for seeking nominees for Board positions that fit ourdesire for enhanced representation of member constituen-cies on our Board.

Our review considered the composition of our members –both full and associate – and how we could structure ourBoard so as to be as representative as possible of allmembership constituencies. One of our starting observa-tions was that although we have always included associaterepresentatives on the Board, historically associate partici-pation has been limited. This is in keeping with NAFA’sbasic philosophy that it is first and foremost an associationof aviation financiers. Prior to this review, associate mem-bers have been limited under our Bylaws to no more than3 seats on our Board. However, in recent years our mem-bership ranks have grown to the point that we now have afairly even balance between full and associate members.

Your Board believes that we can – and should – increaseassociate participation on the Board while remaining trueto our founding philosophy of service to our aviation-finan-cier members.

With that as a background, your Board has implementedthe following restructuring:

● First, we have amended the Bylaws to:

•Remove the “3 associate member” cap on the number ofBoard seats that may be filled by associate members

•Retain the requirement that a majority of directors must befull members

•Permit associate Board members to count towards thequorum requirement for Board meetings

● Second, we have retained the “Class” structure of our Board,which provides for the Board to be divided into 3 classes witheach class serving a 3-year term – so as to have only 1/3 of theBoard up for election in any given year

● Third, we have increased the size of our Board from 10 to 11seats, with the new seat being added to the Class that is up forelection at this year’s annual members’meeting

● And, last, we adopted a policy statement (intended to guide,but not limit, future actions by the Board) that in consideringnominations for prospective Board members and officers, theBoard shall:

•Strive for balance on the Board, by seeking a number ofAssociate members that shall be one less than a majority of themembers of the Board

•Seek to ensure that there shall be 2 full members in eachBoard Class

•Appoint only full members as President and Vice President

•Normally appoint the Vice President to succeed thePresident in office, with one-year terms

•Seek balance and representative composition amongBoard members

RECENT CHANGES MADE TO IMPROVETHE NAFA BOARD OF DIRECTORS

NAFA News - March 200413

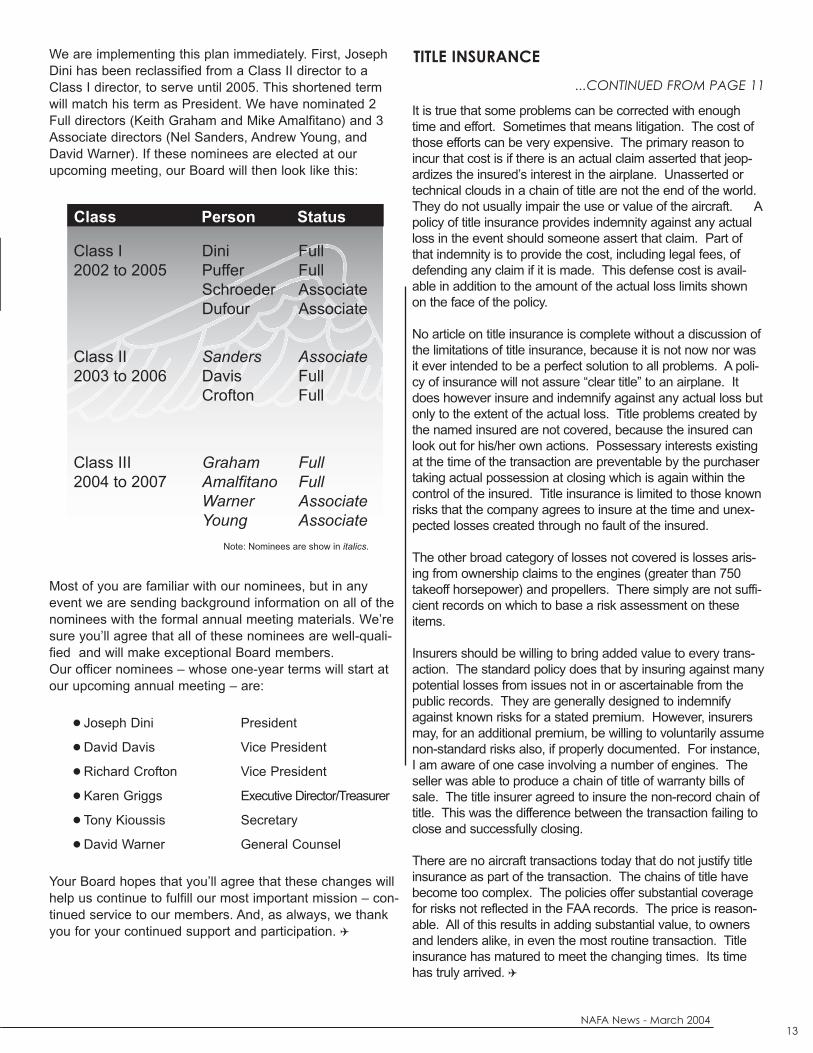

We are implementing this plan immediately. First, JosephDini has been reclassified from a Class II director to aClass I director, to serve until 2005. This shortened termwill match his term as President. We have nominated 2Full directors (Keith Graham and Mike Amalfitano) and 3Associate directors (Nel Sanders, Andrew Young, andDavid Warner). If these nominees are elected at ourupcoming meeting, our Board will then look like this:

Most of you are familiar with our nominees, but in anyevent we are sending background information on all of thenominees with the formal annual meeting materials. We’resure you’ll agree that all of these nominees are well-quali-fied and will make exceptional Board members.Our officer nominees – whose one-year terms will start atour upcoming annual meeting – are:

● Joseph Dini President

● David Davis Vice President

● Richard Crofton Vice President

● Karen Griggs Executive Director/Treasurer

● Tony Kioussis Secretary

● David Warner General Counsel

Your Board hopes that you’ll agree that these changes willhelp us continue to fulfill our most important mission – con-tinued service to our members. And, as always, we thankyou for your continued support and participation. (

Class I2002 to 2005

Class II2003 to 2006

Class III2004 to 2007

DiniPufferSchroederDufour

SandersDavisCrofton

GrahamAmalfitanoWarnerYoung

FullFullAssociateAssociate

AssociateFullFull

FullFullAssociateAssociate

Class Person Status

Note: Nominees are show in italics.

It is true that some problems can be corrected with enoughtime and effort. Sometimes that means litigation. The cost ofthose efforts can be very expensive. The primary reason toincur that cost is if there is an actual claim asserted that jeop-ardizes the insured’s interest in the airplane. Unasserted ortechnical clouds in a chain of title are not the end of the world.They do not usually impair the use or value of the aircraft. Apolicy of title insurance provides indemnity against any actualloss in the event should someone assert that claim. Part ofthat indemnity is to provide the cost, including legal fees, ofdefending any claim if it is made. This defense cost is avail-able in addition to the amount of the actual loss limits shownon the face of the policy.

No article on title insurance is complete without a discussion ofthe limitations of title insurance, because it is not now nor wasit ever intended to be a perfect solution to all problems. A poli-cy of insurance will not assure “clear title” to an airplane. Itdoes however insure and indemnify against any actual loss butonly to the extent of the actual loss. Title problems created bythe named insured are not covered, because the insured canlook out for his/her own actions. Possessary interests existingat the time of the transaction are preventable by the purchasertaking actual possession at closing which is again within thecontrol of the insured. Title insurance is limited to those knownrisks that the company agrees to insure at the time and unex-pected losses created through no fault of the insured.

The other broad category of losses not covered is losses aris-ing from ownership claims to the engines (greater than 750takeoff horsepower) and propellers. There simply are not suffi-cient records on which to base a risk assessment on theseitems.

Insurers should be willing to bring added value to every trans-action. The standard policy does that by insuring against manypotential losses from issues not in or ascertainable from thepublic records. They are generally designed to indemnifyagainst known risks for a stated premium. However, insurersmay, for an additional premium, be willing to voluntarily assumenon-standard risks also, if properly documented. For instance,I am aware of one case involving a number of engines. Theseller was able to produce a chain of title of warranty bills ofsale. The title insurer agreed to insure the non-record chain oftitle. This was the difference between the transaction failing toclose and successfully closing.

There are no aircraft transactions today that do not justify titleinsurance as part of the transaction. The chains of title havebecome too complex. The policies offer substantial coveragefor risks not reflected in the FAA records. The price is reason-able. All of this results in adding substantial value, to ownersand lenders alike, in even the most routine transaction. Titleinsurance has matured to meet the changing times. Its timehas truly arrived. (

TITLE INSURANCE

...CONTINUED FROM PAGE 11

NAFA News - March 200414

“BUILDING THE FOUNDATIONS FOR RECOVERY - PREPARING FOR GROWTH”

TUESDAY, MAY 118:00-5:00pm NAFA/ASA Appraisal Education Seminar

Napa Valley Airport

WEDNESDAY, MAY 129:00 -11:30am REGISTRATION & CONTINENTAL BREAKFAST9:00 -11:30am VENDORS FORUM - Meet and Greet12:30pm NAFA ANNUAL GOLF CLASSIC - Silverado Resort Golf Course, including lunch12:30pm WINE TOUR OF NAPA VALLEY, including lunch7:30pm COCKTAIL RECEPTION & DINNER - Copia Room at Mondavi Vineyard

THURSDAY, MAY 138:00 - 8:30am REGISTRATION & CONTINENTAL BREAKFAST8:30 - 8:45am ANNUAL BUSINESS MEETING & OPENING REMARKS

James F. Dickerson, President, NAFA / Sr. VP Bank of America, Chicago, IL8:45 - 9:30am STATE OF THE INDUSTRY

Ed Bolen, President & CEO, GAMA, Washington, DC9:30 - 10:15 am AIRCRAFT VALUES & THE PROVERBIAL CYCLE

Moderator: William J. Quinn, CEO, Aviation Management Systems, Inc., Portsmouth, NHAndrew Young, Sales Manager, AMSTAT, Trinton Falls, NJFletcher Aldredge, Publisher, VREF, shawnee Mission, KSCarl Janssens, Analyst, Aircraft Blue Book, Overland Park, KS

10:15 - 10:30 am COFFEE BREAK10:30 - 11:15 am INDUSTRY FORECAST

Richard L. Aboulafia, Director of Aviation Consulting, Teal Group, Fairfax, VA11:15 - Noon PRE-TRANSACTIONAL PLANNING & AIRCRAFT SELECTION PROCESS

Barry Justice, President, CAAP, Inc., Grapevine, TXNoon - 1:30 pm LUNCH1:30 - 4:30 pm BREAKOUT SESSIONS: 5 sessions running concurrently, 1 hr. each

1. RISK MITIGATION STRATEGIESModerator: Joseph J. Dini, VP, Merrill Lynch CapitalKieth Block, Block, Markus, Williams (Legal Risks)Anthony Kioussis, JSSI® (Engine Risks)Nel Sanders-Stubbs, Conklin & de Decker (Tax Risks)Stephen Johns, LL Johns (Insurance Risks)CAMP Systems, (Maintenance Risks)

2. FRACTIONAL INDUSTRY - CHANGING DYNAMICS AND FLEET MAKEUPModerator: William J. Quinn, CEO, Aviation Management Systems, Inc., Portsmouth, NHMike Riegel, President, Fractional InsiderFrank Polk, Attorney, McAfee & Taft, Oklahoma City, OKEileen Gliemer, Attorney, Crowell & Moring, LLP, Washington DC

3. AIRCRAFT TAXATION FOR THE CLOSELY HELD BUSINESS - OPPORTUNITIES & PITFALLSLou Meiners, Advocate Aircraft Taxation Co., Indianapolis, IN

4. PISTON AIRCRAFT ROUNDTABLEJohn W. Puffer, President, NAFCO, Lakeland, FLWade Young, Owner, Air Values, Wichita, KS

5. TITLE INSURANCEKen Mayfield, Aero Records & Title, Oklahoma City, OKJohn Casbon, President, First American Transportation Title Ins. Co.

6:00pm COCKTAIL RECEPTION & DINNERDoc Blakely, Pilot/Humorist/Musician/Author

FRIDAY, MAY 148:00 - 11:00 am NETWORKING BREAKFAST BUFFET

AGENDANAFA’S 33RD ANNUAL CONFERENCE & EDUCATION SEMINAR

MAY 11-14, 2004 - THE SILVERADO RESORT, NAPA VALLEY, CALIFORNIANAFA’S 33RD ANNUAL CONFERENCE & EDUCATION SEMINAR

MAY 11-14, 2004 - THE SILVERADO RESORT, NAPA VALLEY, CALIFORNIA

NAFA News - March 200415

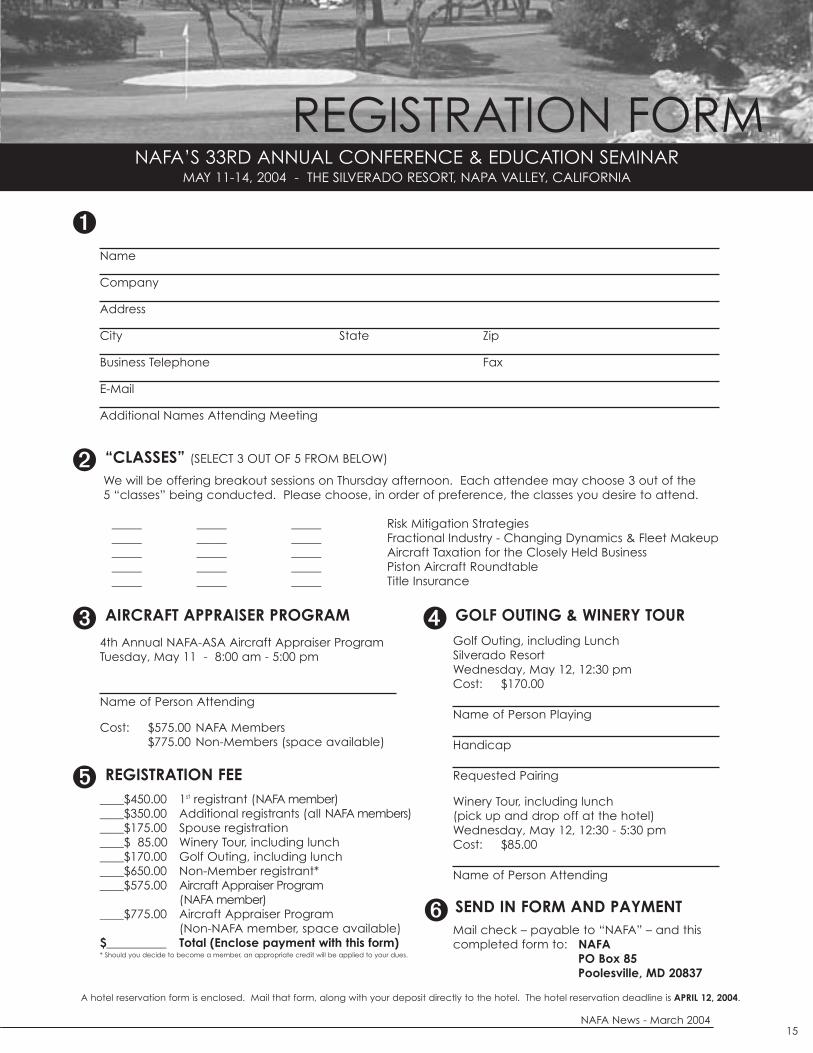

Name

Company

Address

City State Zip

Business Telephone Fax

Additional Names Attending Meeting

A hotel reservation form is enclosed. Mail that form, along with your deposit directly to the hotel. The hotel reservation deadline is APRIL 12, 2004.

We will be offering breakout sessions on Thursday afternoon. Each attendee may choose 3 out of the5 “classes” being conducted. Please choose, in order of preference, the classes you desire to attend.

_____ _____ _____ Risk Mitigation Strategies_____ _____ _____ Fractional Industry - Changing Dynamics & Fleet Makeup_____ _____ _____ Aircraft Taxation for the Closely Held Business_____ _____ _____ Piston Aircraft Roundtable_____ _____ _____ Title Insurance

“CLASSES” (SELECT 3 OUT OF 5 FROM BELOW)

4th Annual NAFA-ASA Aircraft Appraiser ProgramTuesday, May 11 - 8:00 am - 5:00 pm

Name of Person Attending

Cost: $575.00 NAFA Members$775.00 Non-Members (space available)

Golf Outing, including LunchSilverado ResortWednesday, May 12, 12:30 pmCost: $170.00

Name of Person Playing

Handicap

Requested Pairing

Winery Tour, including lunch(pick up and drop off at the hotel)Wednesday, May 12, 12:30 - 5:30 pmCost: $85.00

Name of Person Attending

Mail check – payable to “NAFA” – and thiscompleted form to: NAFA

PO Box 85Poolesville, MD 20837

____$450.00 1st registrant (NAFA member)____$350.00 Additional registrants (all NAFA members)____$175.00 Spouse registration____$ 85.00 Winery Tour, including lunch____$170.00 Golf Outing, including lunch____$650.00 Non-Member registrant*____$575.00 Aircraft Appraiser Program

(NAFA member)____$775.00 Aircraft Appraiser Program

(Non-NAFA member, space available)$__________ Total (Enclose payment with this form)* Should you decide to become a member, an appropriate credit will be applied to your dues.

AIRCRAFT APPRAISER PROGRAM

REGISTRATION FEE

GOLF OUTING & WINERY TOUR

SEND IN FORM AND PAYMENT

Ê

Ë

Ì Í

Î

Ï

REGISTRATION FORMNAFA’S 33RD ANNUAL CONFERENCE & EDUCATION SEMINAR

MAY 11-14, 2004 - THE SILVERADO RESORT, NAPA VALLEY, CALIFORNIA

NAFAPO Box 85Poolesville, MD 20837

MARCH 2004

NANATIONAL AIRCRAFT FINANCE ASSOCIATIONAL AIRCRAFT FINANCE ASSOCIATION’S TION’S

33r33rd ANNUAL MEETINGd ANNUAL MEETING

4th ANNUAL NAF4th ANNUAL NAFA - ASA A - ASA APPRAISER EDUCAAPPRAISER EDUCATION SEMINAR TION SEMINAR

May 12-14, 2004May 12-14, 2004The Silverado ResortThe Silverado Resort

Napa, CaliforniaNapa, California

EVENT DETAILS INSIDE...EVENT DETAILS INSIDE...