Embed Size (px)

Citation preview

RURAL CONNECTIVITY IN AFRICANicolas BARAVALLE – Director Line of Business Data

Fuelled by the growing public appetite for new services and smart devices,the mobile data boom has placed huge demands on wireless networks,prompting a seismic change in performance and capacity. In the readily-accessible urban centers and populated regions of the world, mobileoperators have been willing to invest in new technologies, building out theirnetworks to fulfill the growing demand.

As these markets reach saturation, the next challenge will be to expand datacapabilities into regions that are more economically challenging and so havebeen underserved, whether in the less accessible corners of the developedworld or in the unconnected rural areas of the emerging economies.

STATEMENTS

5Informa Telecoms & Media

The mobile business in most African markets has slowed down due to saturation.

Most of the new subs are coming from churn, resulting in flat growth.

With the fast roll out of smart phone in the continent, the data consumption increases but the price competition pressurizes revenues and ARPU.

The continent has benefited form the massive roll our of fiber to its coast and the creation of network capillarity within the countries.

Submarine cable operators and terrestrial fiber operators are even beginning to interconnect their network offering service redundancy.

Urban and suburban areas are now well covered with an improving reliability and service quality.

THE SITUATION IN 2014

6

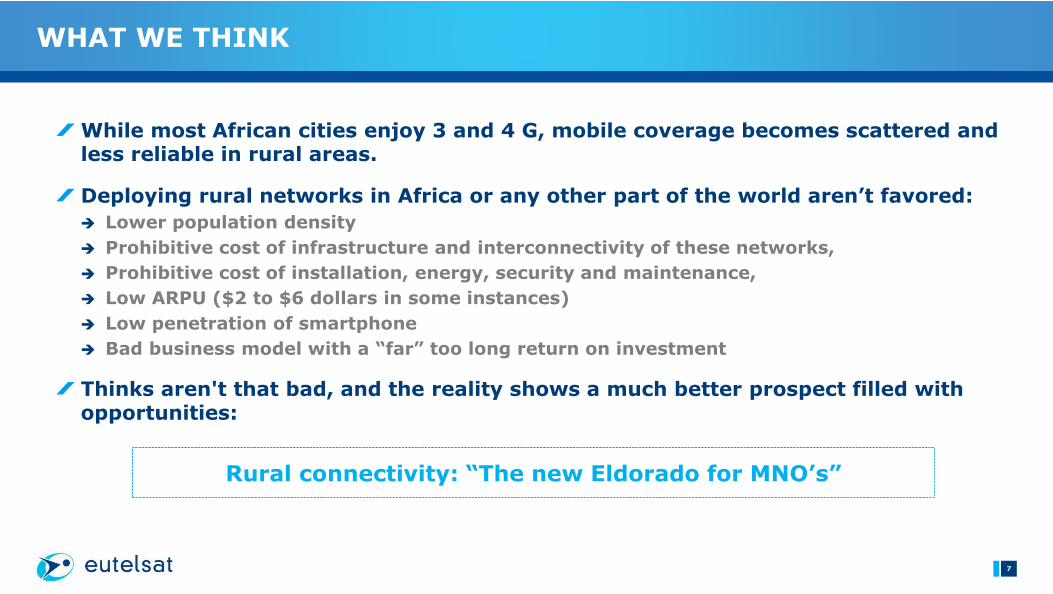

While most African cities enjoy 3 and 4 G, mobile coverage becomes scattered and less reliable in rural areas.

Deploying rural networks in Africa or any other part of the world aren’t favored:

� Lower population density

� Prohibitive cost of infrastructure and interconnectivity of these networks,

� Prohibitive cost of installation, energy, security and maintenance,

� Low ARPU ($2 to $6 dollars in some instances)

� Low penetration of smartphone

� Bad business model with a “far” too long return on investment

Thinks aren't that bad, and the reality shows a much better prospect filled with opportunities:

WHAT WE THINK

7

Rural connectivity: “The new Eldorado for MNO’s”

Rural connectivity is an opportunity for MNO’s, Governments and the rural population.

Rural connectivity enables basic day to day requirements:

� Bridge / closure of digital divide

� Easier / faster Communication and trade

� Mobile money and means of electronic payments

Rural connectivity in a more structured and developed form also bring:

� Health, education and prevention – E-Health

� School, Knowledge and education – E-School

� Government services, Post Services, …

� Entertainment with Kiosks and content distribution

Rural connectivity is an opportunity to develop revenues and services, structure society and develop micro services.

RURAL CONNECTIVITY CAN GENERATE REVENUES

8

RURAL CONNECTIVITY CAN BE COST EFFECTIVE - USE SATELLITE

9

The more fiber and telecom infrastructure in a market, the more telecommunications are consumed by the end user, the more satellite becomes relevant.

� Relevant in DTH, Broadband, and voice-data backhaul.

When fiber requires as many individual links and connections as there are PoPs, Cable head end, towers or BTS’s, satellite requires “ONE” single link whether you interconnect 2 or 2 million points.

� One satellite link, one cost!

� One satellite link can be shared amongst all the points (DVB – TDMA services)

� One satellite link can be increased / decreased anytime and on demand

� One satellite link can reach any point of the network at any given time.

Satellite offers Flexibility, Scalability, cost effectiveness and unlimited reach.

Satellite services best suit the needs of rural networks.

Urban

Sub-urban

Rural

Next wave ofrural build-out

MRCMRC

MRC

MRC

MRC

MRC

MRC

MRCMRC

MRCMRC

MRC

MRC

MRC

MRC

MRC

MRC

MANAGED RURAL COVERAGE

10

TECHNICAL SOLUTION OVERVIEW FOR 2G, 3G OR LTE WITH SATELLITE

11

Operator Core Network

Terminals

ServicesMNO responsibility

POTENTIAL REVENUE / SITE / YEARWHEN MINIMUM UNDERTAKING OF 50 MRC SITES

12

CURRENCY: USD MRC IN SMALL/MEDIUM/LARGE VILLAGES

Average population in villages 5,000

Mobile penetration rate 50%

Number of subscribers 2,500

ARPU level 3

Revenue per site and year 90,000

Annual revenue with 50 sites: USD 4,500,000

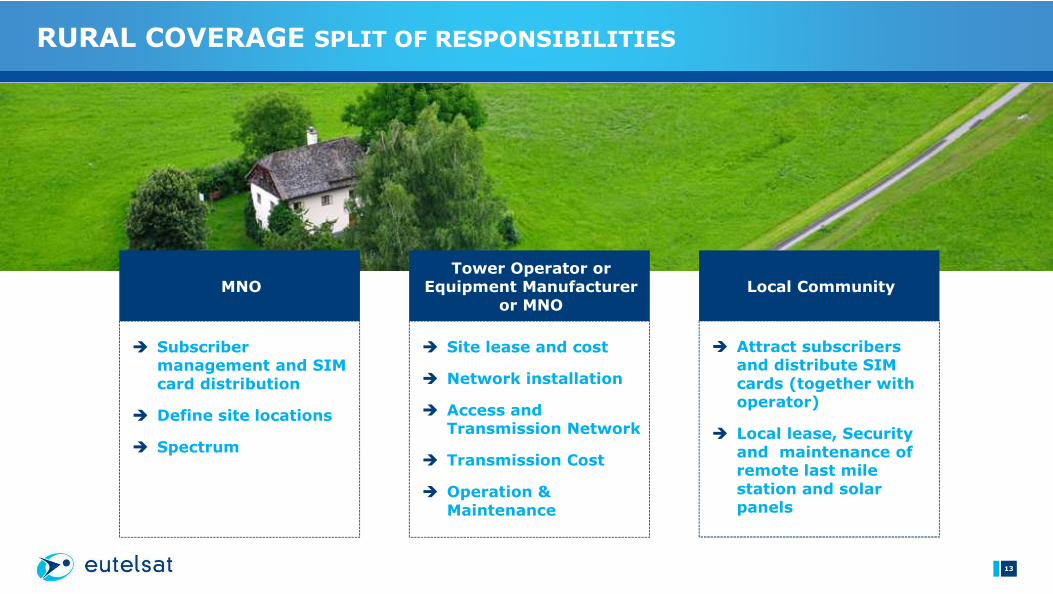

RURAL COVERAGE SPLIT OF RESPONSIBILITIES

13

MNO

� Subscriber management and SIM card distribution

� Define site locations

� Spectrum

Tower Operator or Equipment Manufacturer

or MNO

� Site lease and cost

� Network installation

� Access and Transmission Network

� Transmission Cost

� Operation & Maintenance

Local Community

� Attract subscribers and distribute SIM cards (together with operator)

� Local lease, Security and maintenance of remote last mile station and solar panels

Rural connectivity offers MNO’s a new pockets of growth,

First movers will take a considerable advantage (incl. government contracts & services)

Rural connectivity roll our can be cost effective:

� Use satellite services to interconnect the last mile remotes

� Use Time Division Multiple Access to optimize bandwidth use and efficiency

� Share the infrastructures between multiple MNO’s

Whoever own the last mile infrastructure owns a unique and valuable piece of network.

Last mile remotes depend on Solar energy (environment friendly + low maintenance)

Rural connectivity will enhance trade and communication ���� generate GDP growth.

THE VALUE PROPOSITION FOR RURAL CONNECTIVITY

14

MNO’s are changing the model by transferring all Capex into Opex.� In other words MNO’s want to transfer the cost of acquisition of the last mile

remotes into a monthly operational cost, along with maintenance and satellite capacity.

MNO are separating the traffic management from the network� MNO’s are specializing & focusing on the core business

Owning & Rolling out last mile remote infrastructures is Capex hungry but creates a wonderful business opportunity for the likes of : � Tower Operators� Equipment vendors (ZTE, Huawei…)� Financial investors or institutions.

THE BUSINESS MODEL

15

THANK YOU !Nicolas BARAVALLE – Director Line of Business Data