Embed Size (px)

Citation preview

Nick Bloom, Macro Topics, Spring 2009 1

Comments on: “Investment and Employment Dynamics in the Short-Run and the Long-Run”, Avinash Dixit, OEP (1997)

Why I chose this paper:

•Very clearly written paper which pushed the intuition and relegates the details to other texts

•These models of adjustment costs in multiple dimensions are important in aggregate setting as the generate distributions and interesting responses (as we’ll see). EG:

• Prices• Employment• Consumption (housing)• Share trading

Nick Bloom, Macro Topics, Spring 2009 2

Comments on: “Investment and Employment Dynamics in the Short-Run and the Long-Run”, Avinash Dixit, OEP (1997)

Good framework for micro to macro:• distribution of units: across this space reflects history• shifts in this distribution: productivity shock• shifts in the thresholds: regulations, expectations, uncertainty etc

Nick Bloom, Macro Topics, Spring 2009 3

Nick Bloom

Investment and Uncertainty

Nick Bloom, Macro Topics, Spring 2009 4

What are the real options models predictions?

Investment and hiring/firing will be lumpy:•Evidence from Micro Data (Davis and Haltiwanger, 1992)

Investment and hiring/firing will respond slowly to shocks:•Wide range of evidence from micro and macro data

Investment and hiring/firing response effected by adjustment costs•No direct evidence that I know of (Bertola & Bentolila,

1990)

Investment and hiring/firing response effected by uncertainty:•Will discuss this today…

Nick Bloom, Macro Topics, Spring 2009 5

John Leahy and Toni Whited (1996)

“The Effects of Uncertainty on Investment: Some stylized facts”

Journal of Money, Credit and Banking

Nick Bloom, Macro Topics, Spring 2009 6

OverviewPanel estimation of the effect of uncertainty on investment

The fundamental idea was to:•Use yearly volatility of daily returns of stock as a measure

of uncertainty (σi,y≈ Σd(ri,y,d2) where ri,y,d is the stock returns for

firm i, in year y on day d)•Estimate yearly firm investment as a function of this•Use firm and year controls to try and deal with other

omitted variables•Use GMM to try to deal with exogeneity

An important paper:(i) First general test of investment-uncertainty literature(ii) Good econometrics – GMM and panel estimation(ii) Used interesting data – firm returns variance

Nick Bloom, Macro Topics, Spring 2009 7

Many cites - the rewards for being first…

Nick Bloom, Macro Topics, Spring 2009 8

Basic results

• Uncertainty reduces investment• Covariance has no impact• Tobin’s Q controls removes uncertainty effects, but note:

•Tobin’s Q also not significant•Tobin Q = Marginal Q both PC & CRS hold, real options

assumes either PC or CRS does not hold

Nick Bloom, Macro Topics, Spring 2009 9

Message is no large direct impact of uncertainty (at yearly frequency)

Good paper – how could you build on this:

•Theory – take a structural approach. No link with theory• Use Dixit & Pindcyk (1994), Abel & Eberly (1996)

•Identification – everything moves together so not clear what is identifying what (GMM is no magic bullet)

•Data – better measures of uncertainty, for example use implied volatility (forward looking) or a direct measure

Nick Bloom, Macro Topics, Spring 2009 10

Luigi Guiso and Giuseppe Parigi (1999)

“Investment and Demand Uncertainty”

Quarterly Journal of Economics

Nick Bloom, Macro Topics, Spring 2009 11

Overview

Paper also estimates the effect of uncertainty on investment

Contribution is a great uncertainty measure – a survey of firms distribution of demand growth expectations

•Used to generate a mean and variance of expected demand

•So can estimate effects of variance controlling for the meanThe authors basically persuade the BOI to run this – ingenious!

Also had a range of tests of other implications of the real options theory – so much closer to the theory

Nick Bloom, Macro Topics, Spring 2009 12

The rewards for ingenious data organisation…

Nick Bloom, Macro Topics, Spring 2009 13

Basic setup

The paper is heavily (and appropriately) orientated around the description of the empirical uncertainty measure

One important innovation is they changed the specification for the uncertainty from levels to an interaction

But they do not always include levels of uncertainty as a control! [Note: whenever estimating interactions you must always always include the levels of all variables as well, otherwise mis-specified!]

Nick Bloom, Macro Topics, Spring 2009 14

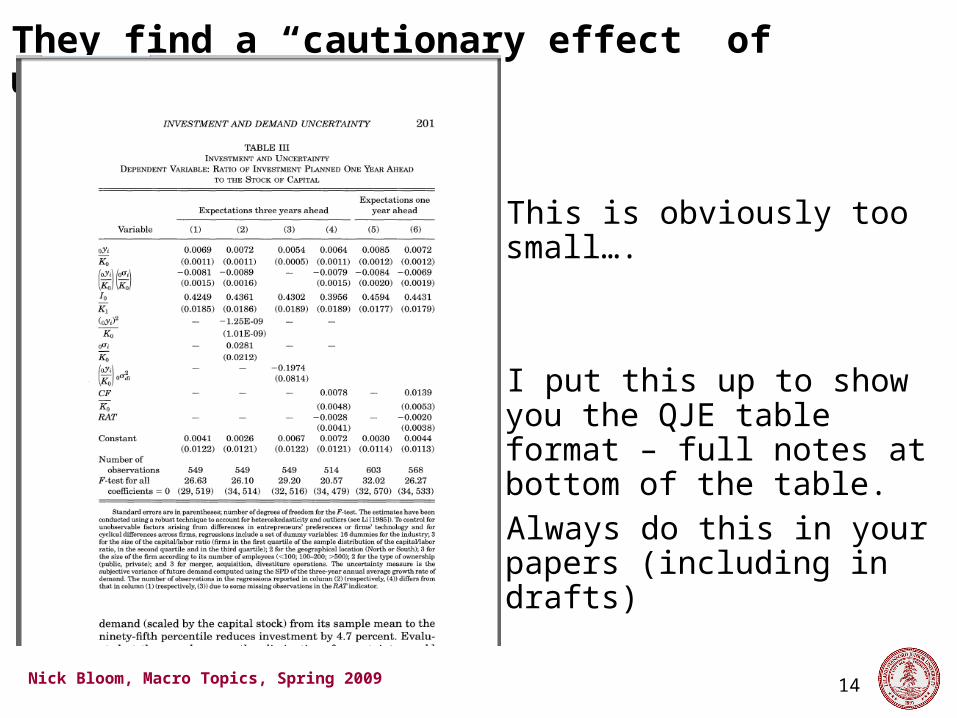

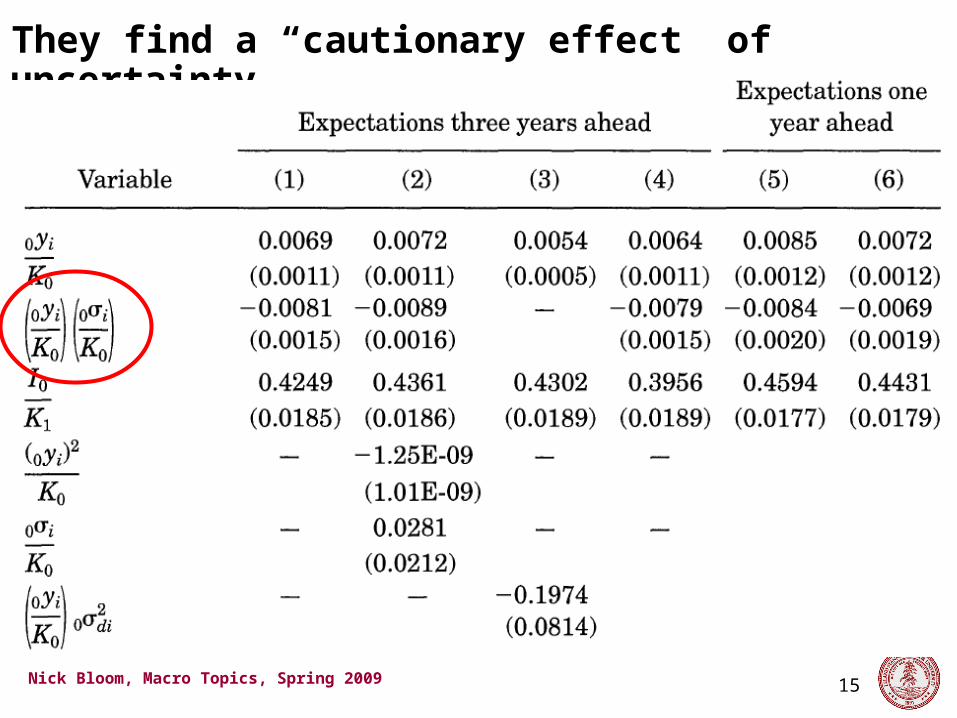

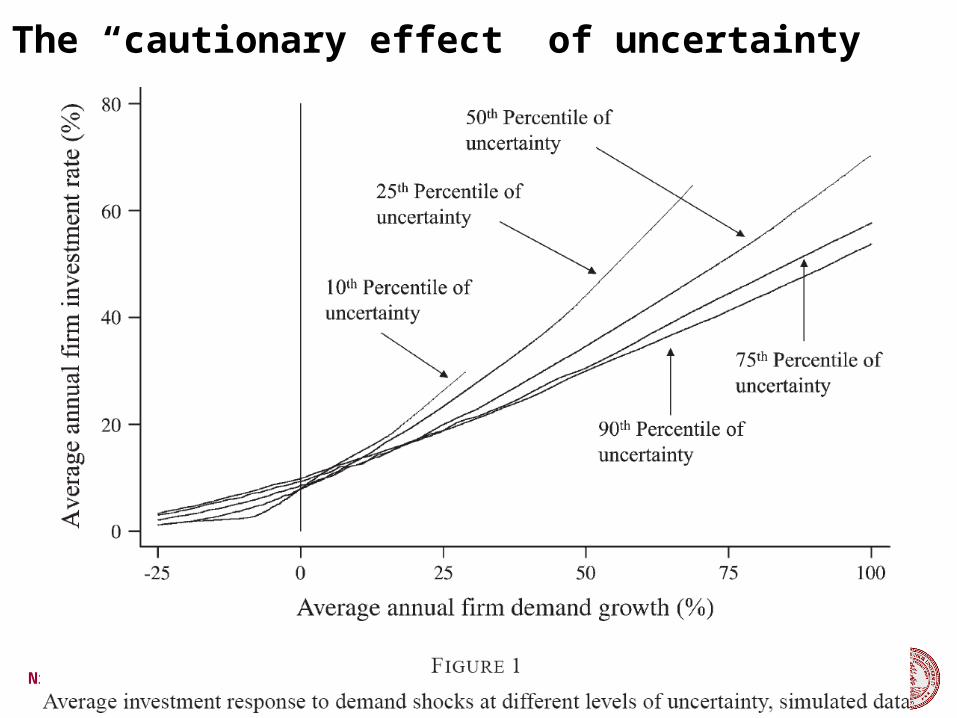

They find a “cautionary effect” of uncertainty

This is obviously too small….

I put this up to show you the QJE table format – full notes at bottom of the table. Always do this in your papers (including in drafts)

Nick Bloom, Macro Topics, Spring 2009 15

They find a “cautionary effect” of uncertainty

Nick Bloom, Macro Topics, Spring 2009 16

Other parts of the paper

The paper also has other tests of the real-options, finding for σ:•More impact for irreversible capital (directly measured and

indirectly measured using Shleifer and Vishny (1992))•More impact at higher market power•Occurs in structures, machinery & vehicle investment

Look reasonable and good to push the empirics with these additional tests – although small sample size (500 obs) so tenuous

My guess is these were – appropriately – requested during the refereeing process

Nick Bloom, Macro Topics, Spring 2009 17

Message is uncertainty reduces responsiveness

Good paper – how could you build on this:

•Theory – take a more structural approach. Again no real link between theory and empirics

•Identification – cross-sectional data without any IV

•“So what” factor – push some interesting implication if uncertainty varies by time, region, industry etc..

Nick Bloom, Macro Topics, Spring 2009 18

Nick Bloom, Steve Bond & John Van Reenen (2007)

“Uncertainty and Investment Dynamics”

Review of Economic Studies

Nick Bloom, Macro Topics, Spring 2009 19

Overview

Paper also estimates the effect of uncertainty on investment…

Contribution is goes directly from theory to empirics to derive robust predictions and test these

•Shows higher uncertainty generates a large and robust “caution effect”: 1 SD increase in σ ½’s investment response

•Shows this is robust to aggregation (cross-section & time)•Takes a matched theory-empirics approach (panel, GMM)

Also has a range of tests of impacts of different types of adjustment costs, uncertainty effects and functional forms

Nick Bloom, Macro Topics, Spring 2009 20

The rewards of impressive modelling

Nick Bloom, Macro Topics, Spring 2009 21

Cites pretty good for its age, and a lesson on not changing paper titles

Nick Bloom, Macro Topics, Spring 2009 22

Basic setupThe paper is split between theory and empirics

Theory is simulation based (this is possible, but put code on-line):•Solves for time varying σ•Shows σ induces “caution” – like an adjustment cost•Shows this is robust to aggregation – empirically important

Shows on simulated data this effect can be estimated (by GMM)

Shows on actual data find similar results (by GMM)Show robust to various tests (correctly requested by referees)

Nick Bloom, Macro Topics, Spring 2009 23

The “cautionary effect” of uncertainty

Nick Bloom, Macro Topics, Spring 2009 24

Estimated by GMM on simulated data

Nick Bloom, Macro Topics, Spring 2009 25

Estimated by GMM on actual data

Nick Bloom, Macro Topics, Spring 2009 26

Use empirical results to show variations in σ matter

Nick Bloom, Macro Topics, Spring 2009 27

Message is theory and empirics show uncertainty reduces responsiveness

How could you build on this:

•Identification – everything moves together so not clear what is identifying what (GMM is no magic bullet).

• Find some exogeneous shift in σ which does not effects levels?

•Data – better measures of uncertainty, for example use implied volatility (forward looking) or a direct measure. Also could use higher frequency data (quarterly Compustat data)

•Other outcomes – look at labor, R&D, productivity etc…

Nick Bloom, Macro Topics, Spring 2009 28

.51

1.5

22.

5U

unc

erta

inty

pro

xy

1965 1970 1975 1980 1985 1990 1995 2000 2005Year

I think this is an interesting research area as uncertainty also looks like it is counter-cyclical

Shaded areas are recessions