Embed Size (px)

Citation preview

The Next Generation of Thai IndustryThe Next Generation of Thai Industry

Mr. Arkhom Termpittayapaisith Secretary General

Office of the National Economic and Social Development Board (NESDB)

December 2013, Thailand

Outline of Presentation

2 Facing New Challenges in Changing

Global Contexts

Current Performance of Thailand’s

Competitiveness1

Readiness of Thai Industries Ready in

the Challenging Global Arena

www.nesdb.go.th - 2 -

Next Steps of Thai Industries Towards

Sustainable Competitiveness

3

4

Outline of Presentation

2 Facing New Challenges in Changing

Global Contexts

Current Performance of Thailand’s

Competitiveness1

Readiness of Thai Industries Ready in

the Challenging Global Arena

www.nesdb.go.th - 3 -

Next Steps of Thai Industries Towards

Sustainable Competitiveness

3

4

Thailand�s economic performance, in comparison with some selected countries

GDP Growth (Q2/ 2013) of Thailand and selected countries

ASEAN BRIC Innovation-led economy

GDP Growth: %

Source : World Bank and and National Economic and Social Development Board

• Thailand’s GDP growth in 2012 ranked the 31st in the world and the 2nd in Asia. Though the GDP

growth in Q2/2013 recorded only 2.8%; declining from 5.4% in Q1/2013, it remained higher than

those of Russia, Japan, and the U.S.

• It is projected that in 2012 the GDP growth rate of ASEAN countries will increase, higher than other

regions, and the Philippines’s growth will reach 7.5%, at the similar level of China’s, representing the

highest rank among Southeast Asian countries.

2.8 4.3 5.8 7.5 3.3 1.2 4.4 7.5 0.9 1.6 3.8

ThaiMalaysia

IndonesiaPhilippines

BrazilRussia

IndiaChina

JapanUSA

Singapore

www.nesdb.go.th - 4 -

2020 20201818

15151212 1212

19191717 1818

28282626 2525

3232 3333

2727 2626 2626 27273030

27273030

3232 3333

2828 2828

34343636

3838 3939 3838 3737

0

5

10

15

20

25

30

35

40

Competitiveness and Ease of doing business of Thailand (2003-2013)

Ham

bu

rge

r C

risi

s

cou

p d

'éta

t

Eu

ro C

risi

s

Flo

od

3838 3939 3838 373740

45

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

� Thailand’s competitiveness performance has been in the middle tier.

� Over the past 10 years Thailand’s competitiveness ranking remained unchanged, or even

dropped slightly.

� Among ASEAN countries, Thailand’s competitiveness was in the 3rd rank, following Singapore

and Malaysia and advancing only Indonesia and the Philippines.

Source : Doing Business report (EoDB) by world bank [data analysis since 2005], Global Competitiveness Report by World

Economic Forum, and World Competitiveness Yearbook by IMD

Ham

bu

rge

r C

risi

s

cou

p d

'éta

t

Eu

ro C

risi

s

Flo

od

www.nesdb.go.th - 5 -

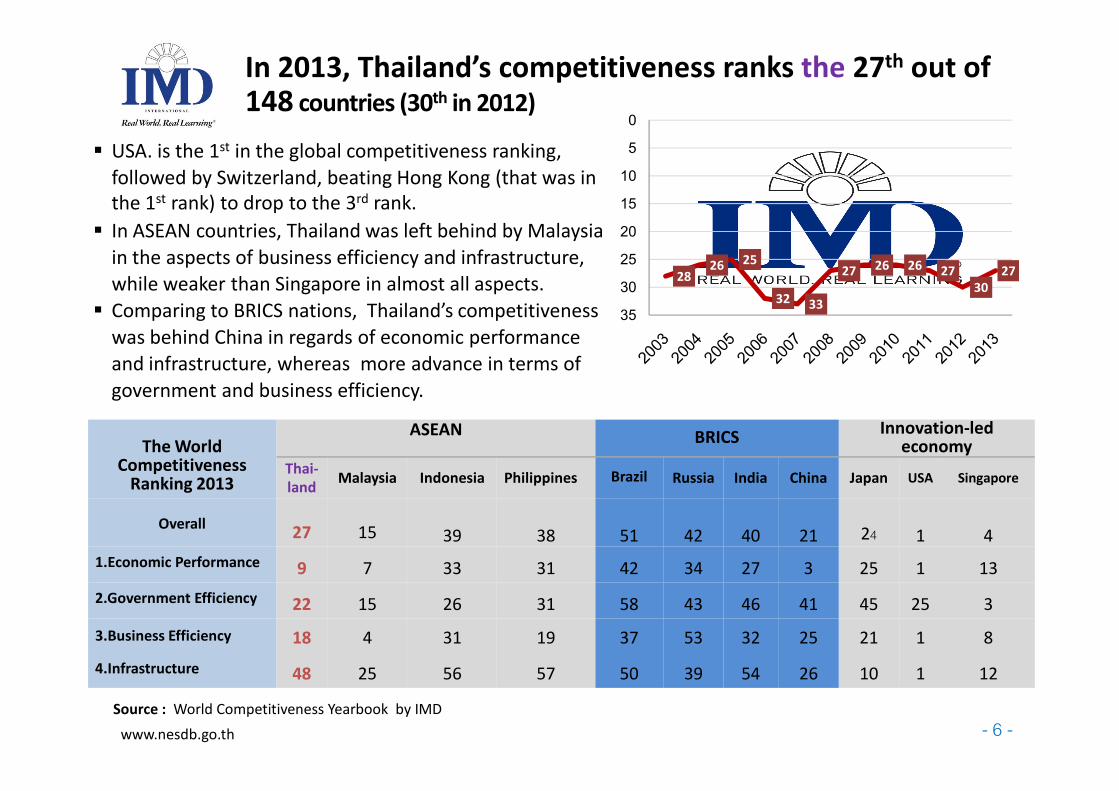

In 2013, Thailand’s competitiveness ranks the 27th out of 148 countries (30th in 2012)

� USA. is the 1st in the global competitiveness ranking,

followed by Switzerland, beating Hong Kong (that was in

the 1st rank) to drop to the 3rd rank.

� In ASEAN countries, Thailand was left behind by Malaysia

in the aspects of business efficiency and infrastructure,

while weaker than Singapore in almost all aspects.

� Comparing to BRICS nations, Thailand’s competitiveness

was behind China in regards of economic performance

and infrastructure, whereas more advance in terms of

government and business efficiency.

2826 25

32 33

27 26 26 27

30

27

0

5

10

15

20

25

30

35

The World Competitiveness

Ranking 2013

ASEAN BRICSInnovation-led

economy

Thai-

landMalaysia Indonesia Philippines Brazil Russia India China Japan USA Singapore

Overall27 15 39 38 51 42 40 21 24 1 4

1.Economic Performance 9 7 33 31 42 34 27 3 25 1 13

2.Government Efficiency 22 15 26 31 58 43 46 41 45 25 3

3.Business Efficiency 18 4 31 19 37 53 32 25 21 1 8

4.Infrastructure 48 25 56 57 50 39 54 26 10 1 12

government and business efficiency.

Source : World Competitiveness Yearbook by IMD

www.nesdb.go.th - 6 -

3434 3636

2828 2828

3434 3636 3838 3939 3838 3737

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Thailand

Malaysia

Indonesia

Philippines

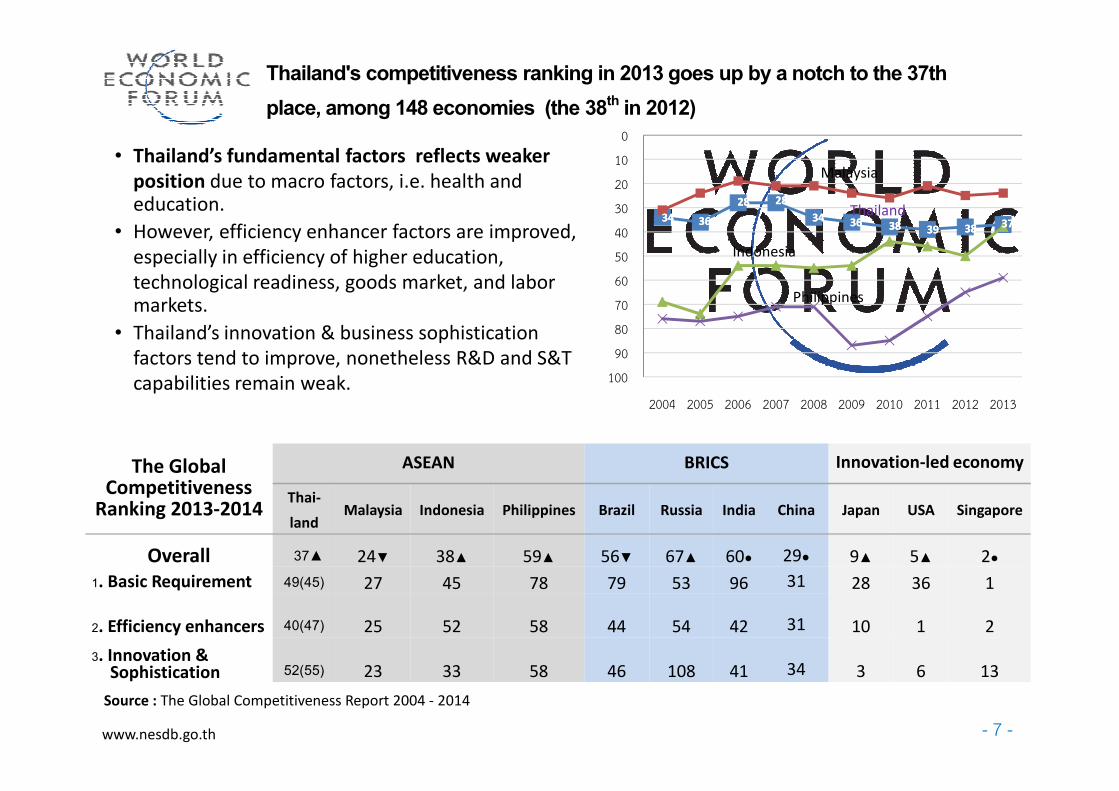

• Thailand’s fundamental factors reflects weaker

position due to macro factors, i.e. health and education.

• However, efficiency enhancer factors are improved,

especially in efficiency of higher education,

technological readiness, goods market, and labor markets.

• Thailand’s innovation & business sophistication

factors tend to improve, nonetheless R&D and S&T

capabilities remain weak.

Thailand's competitiveness ranking in 2013 goes up by a notch to the 37th

place, among 148 economies (the 38th in 2012)

The Global Competitiveness

Ranking 2013-2014

ASEAN BRICS Innovation-led economy

Thai-

landMalaysia Indonesia Philippines Brazil Russia India China Japan USA Singapore

Overall 37▲ 24▼ 38▲ 59▲ 56▼ 67▲ 60● 29● 9▲ 5▲ 2●

1. Basic Requirement 49(45) 27 45 78 79 53 96 31 28 36 1

2. Efficiency enhancers 40(47) 25 52 58 44 54 42 31 10 1 2

3. Innovation & Sophistication 52(55) 23 33 58 46 108 41 34 3 6 13

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source : The Global Competitiveness Report 2004 - 2014

www.nesdb.go.th - 7 -

Ease of Doing Business

Ranking, 2013

Investor Protection

TradingAcross

Borders

Property Registration

Access toCredit

Start-upBusiness

Tax Payment

Start-upBusiness

Singapore 1● 2● 1 36▼ 12▼ 4● 5▼ 2●

Thailand 18▼ 13● 20▼ 26▲ 70▼ 85▼ 96▲ 58▼Malaysia 12▲ 4 11▲ 33 1 54▼ 15▲ 49▼

Brunei 79 117 40 115 129 135 22 46

Vietnam 99 169 74 48 40 108 138 149

128 49 37 98 129 166 131 148

In 2013 Thailand was ranked the 18th in the Ease of Doing Business

Ranking, dropping from the 17th in 2012

AS

EA

N

Indonesia 128 49 37 98 129 166 131 148

Philippines 138 128 53 122 129 161 143 165

Cambodia 133 82 118 115 53 175 66 152

Laos 163 184 160 74 167 81 126 185

Myanmar n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

New Zealand 3 1 25 2 4 1 21 13

South Korea 8 49 3 75 12 24 30 14

Australia 10 70 44 37 4 2 48 18

Japan 24▼ 19▼ 19▼ 64▼ 23▲ 114▼ 127▼ 1●

China 91● 100▼ 68▼ 44▼ 70▼ 151● 122● 82▼

India 132 49 127 94 23 173 152 116

Source : DOING BUSINESS 2013

AS

EA

N

- 8 -

2 Facing New Challenges in Changing

Global Contexts

Current Performance of Thailand’s

Competitiveness1

Outline of Presentation

Readiness of Thai Industries Ready in

the Challenging Global Arena

www.nesdb.go.th - 9 -

Next Steps of Thai Industries Towards

Sustainable Competitiveness

3

4

1 Technological

Change

Six contexts influencing the changes in competition platform, business model and social system.

Emergence of

“the Second

Economy”

(digital economy)

2 Climate

Change

6Political Change

•Conflict

•People

•Disaster•Energy

Major Global Changes

Transforming

Competition

Platform &

Business

Model

(digital economy)

3 International

Economic Platform Change

4 Demographical

Structure

Change

5Cultural

Change

Aging Society

•People

participation

• Social value change

• More individualism

Economic

integration &

connectivity

•Energy & food security

Transforming

Social System

& Interaction

www.nesdb.go.th - 10 -

Physical-based business process

Digital-based business process

Emergence of

Change in Competition

Platform & Business

Model

Changing Global Contexts: Technological Change

• Processes in the physical economy are

being entered into the digital economy.

• New business model: “Internet of

Things”

Emergence of

“the Second

Economy���� Digital

Economy”

Change in Social

System and

Interaction

www.nesdb.go.th - 11 -

• More online interaction and communication

• Create networking and social movement through social media

• Enable the mobilization of limited global resources for better quality of life

o The technology is increasingly more sophisticated and rapidly changing.

o Consumers are more interested in software application than hardware.

o Higher Technology Accessibility: Develop technology to serve diverse and complicated

demands.

o Global sourcing and fiercer competition in acquiring power from occupying sources of

technologies.

Changing Global Contexts : Technological Change

www.nesdb.go.th - 12 -

• In 2030, the increasing demand in energy in Asia, particular in China and India, will create fiercer

competition in seizing scarce source of energy.

• In the meantime, the global energy resources are expected to be available for consumption only

for the next 50-100 years.

Energy consumption by sector (2008-2035)

54.2 Years

Reserves

Oil 1.65 Trillion barrels

Reserves/Production Ratio

Changing Global Contexts : Climate Changes /Energy Crisis

barrels

208.4 Trillion cubic metres

Natural Gas

Coal 860,938Million tonnes

112 Years

63.5 Years

Source : BP Statistical Review of World Energy, June 2012 and Energy policy and planning officewww.nesdb.go.th - 13 -

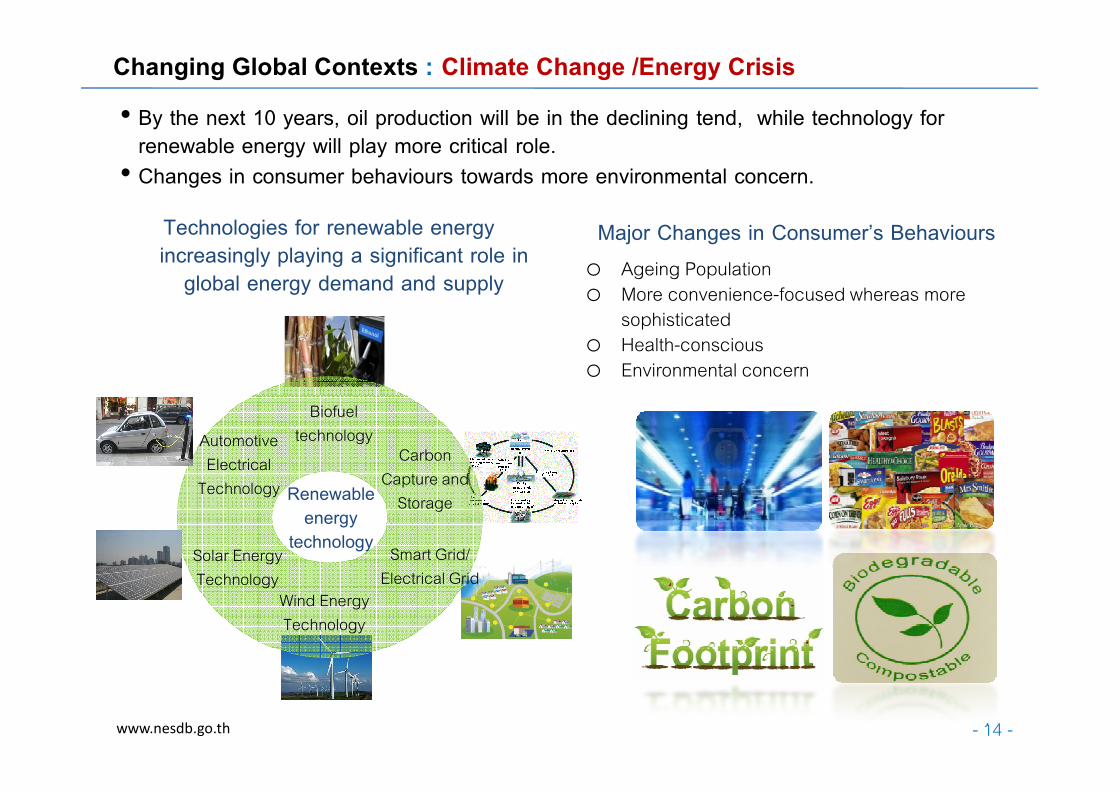

• By the next 10 years, oil production will be in the declining tend, while technology for renewable energy will play more critical role.

• Changes in consumer behaviours towards more environmental concern.

Technologies for renewable energy increasingly playing a significant role in

global energy demand and supply

Biofuel

Major Changes in Consumer2s Behaviourso Ageing Population o More convenience-focused whereas more

sophisticated o Health-consciouso Environmental concern

Changing Global Contexts : Climate Change /Energy Crisis

Biofuel technology

Carbon Capture and

Storage

AutomotiveElectrical

Technology

Solar Energy Technology

Wind Energy Technology

Smart Grid/ Electrical Grid

Renewable energy

technology

www.nesdb.go.th - 14 -

The global economy will more likely to be unstable and complex.

34

35

36

37THB/USD

QE1+

1.25 trillion USD

QE2

600 Thousand USD

Tha

i bat

h/U

SD

QE3

o The emergence of 'Currency War0 in accordance with Quantitative Easing Measures has created

crucial impacts on the fluctuation of exchange rates and Thailand4s competitiveness in goods.

Changing Global Contexts : International Economic Platform Change

28

29

30

31

32

33

34

Nov 08 May 09 Nov 09 May 10 Nov 10 May 11 Nov 11 May 12 Nov 12 May 13

QE1

500 Thousand USD

Source : Bank of Thailand

29.6

28.7

Tha

i bat

h/U

SD

32.1

QE3

40 Thousand USD QE4

45 Thousand USD

www.nesdb.go.th - 15 -

• Single Market Production Base: Larger and more complicated markets

• Free flow of goods, services, capitals, investments, and

Change in Competition Platform & Business Model

Global economic power has been shifting to Asia. Economic Integration and connectivity are major factors for competitiveness empowerment of nations.

Changing Global Contexts : International Economic Platform Change

• Free flow of goods, services, capitals, investments, and skilled labours.

• Expanding regional supply chains

• Human adaptation in cultural diversity

• Free flow of people will probably create social problems, such as labour, public health, crime

Change in Social System and Interaction

www.nesdb.go.th - 16 -

Global demographical structure is changing towards ageing society

o The trend of increasing number of ageing population in global demographical structure becomes

one of the important conditions in economic and social policy planning.

30

35

40

45 The total world population aged over 60%

Changing Global Contexts : Demographical Structure Change

0

5

10

15

20

25

30

2503250825132518252325282533253825432548255325582563256825732578258325882593

Asia World China Indonesia Japan Malaysia Europe USA Thai

Source : UN Statistics Division

www.nesdb.go.th - 17 -

0%

10%

20%

30%

40%

50%

60%

70%

80%

25

43

25

45

25

47

25

49

25

51

25

53

25

55

25

57

25

59

25

61

25

63

25

65

25

67

25

69

25

71

25

73

• Thailand is expected to enter ageing

society within 8 years.

• Proportion of elderly (60 + years) of

Thailand is likely to be higher, while the

proportion of children (0-14 years) and

working age (15-59 years) is decreasing.

• In contrast, industrial sectors are requiring

higher number of labours.

• The more the access to higher levels of

education, the later the labours enter to

market.

Thai population by age Year 2000-2030

Future labour issues in Thailand

60+ yrs

15-59 yrs

0-14 yrs

Changing Global Contexts : Demographical Structure Change

25

43

25

45

25

47

25

49

25

51

25

53

25

55

25

57

25

59

25

61

25

63

25

65

25

67

25

69

25

71

25

73

market.

Source: NESDB, Ministry of Industry, The National Wages and Productivity Commission (NWPC)

$2.0 $2.5 $3.0 $5.0 $8.4 $9.6 $9.7

$61.7

0

10

20

30

40

50

60

70

• Regarding cost of labour, Thailand ranks

the 3rd in ASEAN (higher than that of

Malaysia but at the same level as the

Philippines )

Minimum wages by country in the region. (Unit: USD)

• Problems of cost and quantity of labour

are currently affecting industrial sectors,

especially in labour-intensive ones,

possessing workforce of more than 5.7

million people in August 2012

www.nesdb.go.th - 18 -

More individualism

Social value change

• Growth in online business

• Value creation from branding

• Expansion of telecommunication business

Change in Competition Platform & Business Model

Change in Social

Changing Global Contexts : Cultural Change

More individualism

• More consumerism/materialism and give respect to people based on their social status rather than their merit/moral

• Focus more on self-interest than public interest

• Corruption is acceptable as long as it contributes to own interests

Change in Social System and Interaction

- 19 -www.nesdb.go.th

• Business / Industry must realize the impact and understanding on the community

Change in Competition Platform & Business Model

Change in Social System and

Changing Global Contexts : Political Change

Globalization affects information access of people including politics and development country

• Political conflict generated serious argument

in Thai society

• Public sector=s role in developing countries

• Inequality reduction and empowering people is a key development issues

Change in Social System and Interaction

- 20 -www.nesdb.go.th

2 Facing New Challenges in Changing

Global Contexts

Current Performance of Thailand’s

Competitiveness1

Outline of Presentation

Readiness of Thai Industries Ready in

the Challenging Global Arena

www.nesdb.go.th - 21 -

Next Steps of Thai Industries Towards

Sustainable Competitiveness

3

4

Critical issues impacting industrial sector in the near future

Stagnation of national

competitiveness and the

delay in infrastructure development projects

Highly susceptible to

changes in the world

economy due to high

dependence on export

• Growth tends to be concentrated only on some particular industries.

• Issues of low productivity and low value added productions remain

The trend of ageing

society brings about

higher risks from labour

1

2

4

5

Environmental problems

create considerable impacts

on ecological systems and quality of life of people

dependence on export

market and weak domestic markets.

higher risks from labour

shortage in the future

Decline of domestic

energy supply affects

on more reliance on

high-cost energy import in the future

3 6

www.nesdb.go.th - 22 -

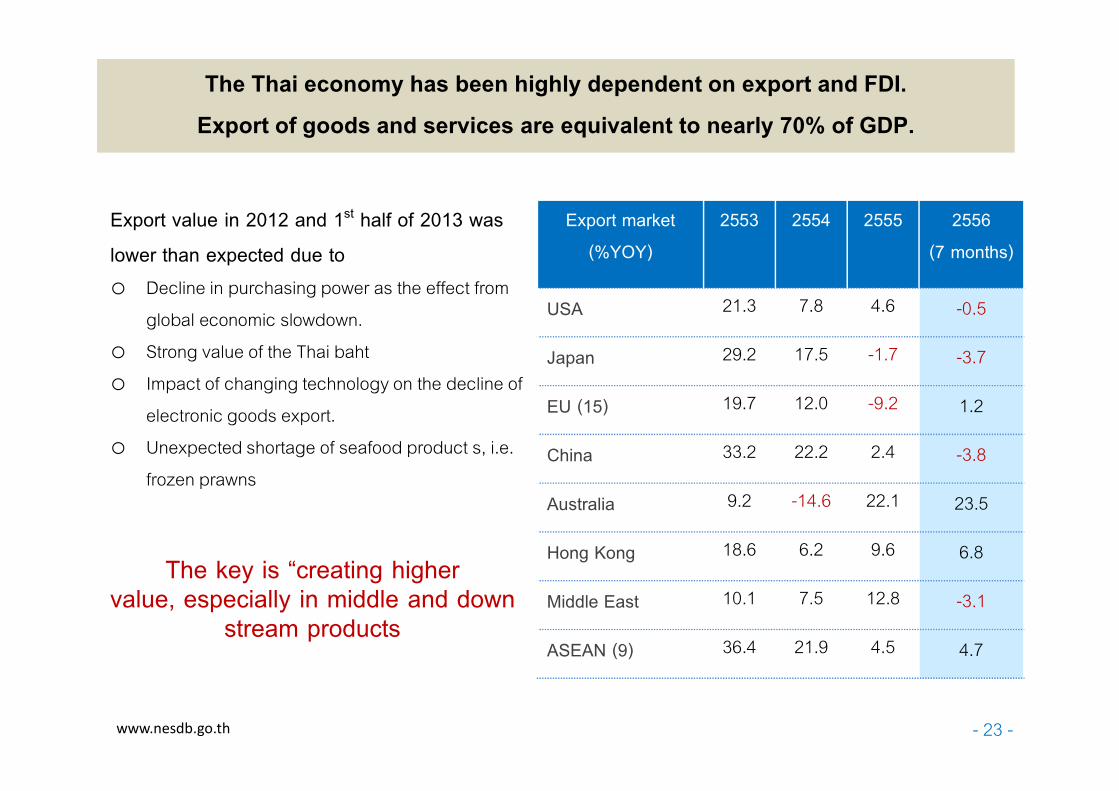

The Thai economy has been highly dependent on export and FDI.

Export of goods and services are equivalent to nearly 70% of GDP.

Export value in 2012 and 1st half of 2013 was

lower than expected due too Decline in purchasing power as the effect from

global economic slowdown. o Strong value of the Thai baht o Impact of changing technology on the decline of

Export market

(%YOY)

2553 2554 2555 2556

(7 months)

USA 21.3 7.8 4.6 -0.5

Japan 29.2 17.5 -1.7 -3.7

EU (15) 19.7 12.0 -9.2 1.2o Impact of changing technology on the decline of

electronic goods export.o Unexpected shortage of seafood product s, i.e.

frozen prawns

EU (15) 19.7 12.0 -9.2 1.2

China 33.2 22.2 2.4 -3.8

Australia 9.2 -14.6 22.1 23.5

Hong Kong 18.6 6.2 9.6 6.8

Middle East 10.1 7.5 12.8 -3.1

ASEAN (9) 36.4 21.9 4.5 4.7

- 23 -www.nesdb.go.th

The key is Acreating higher value, especially in middle and down

stream products

Thailand R&D’s investment is remaining at low level as compared to other economies.

• According to the IMD competitiveness,

out of 144 countries, Thailand’s R&D

expenditure was recorded the 60th rank.

• Thailand’s technological readiness was in the

78th rank, whereas innovation capability was

ranked the 66th.

• The ratio of R&D investment to GDP of

Thailand was lower than many countries,

including Malaysia, only 0.2% of GDP in 2012

0.2

2.8

1.8 1.8

3.4 3.8

2.8 2.7

Thai Singapore Malaysia China Japan South Korea USA Australia

Research and Development Expenditure (% of GDP) in 2012

source: UNESCO Institute for Statistics, July 2011, The World Bank @AB World Competitiveness Yearbook by IMD

www.nesdb.go.th - 24 -

82.173.5

39.4 39.229.8

13.0

7.6

65.2

23.5 28.0

11.8 9.9 10.83.5

0

1020

30

40

50

60

70

80

90

Natural Gas

Oil

USA

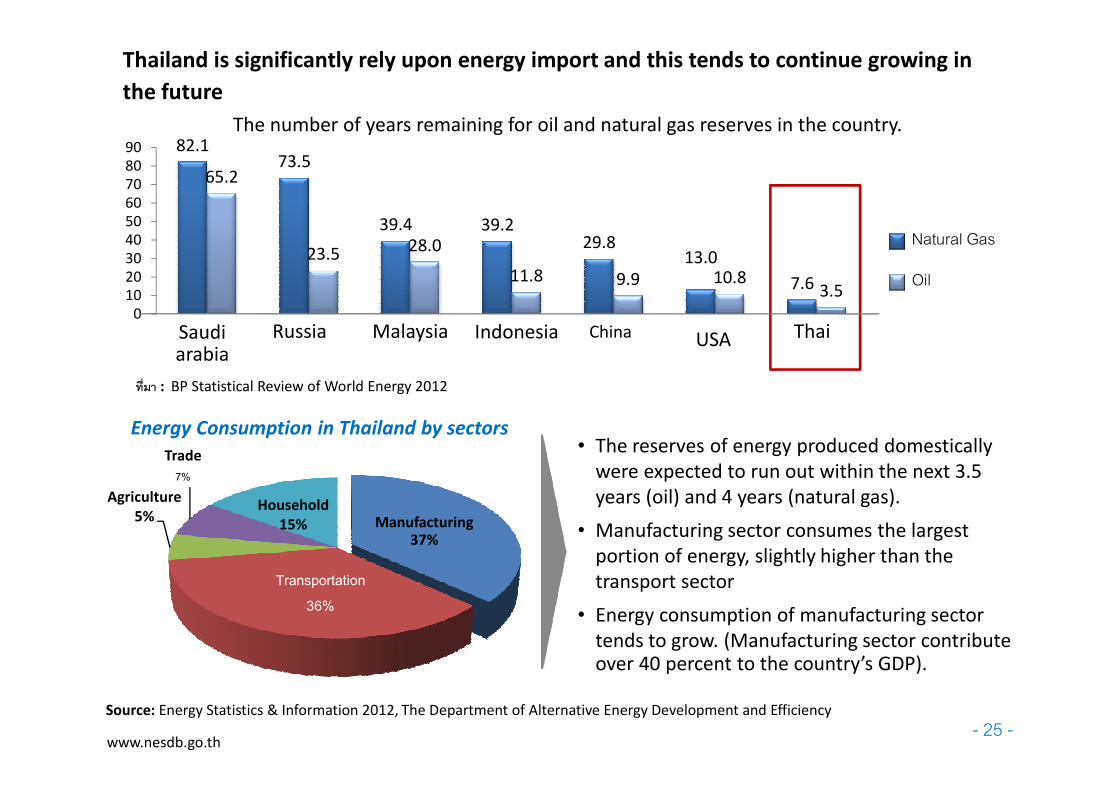

The number of years remaining for oil and natural gas reserves in the country.

Saudi arabia

Russia Malaysia Indonesia China Thai

Thailand is significantly rely upon energy import and this tends to continue growing in

the future

BCDEF : BP Statistical Review of World Energy 2012

Agriculture

5%

Trade

7%

Household

15%

Transportation

36%

Energy Consumption in Thailand by sectors• The reserves of energy produced domestically

were expected to run out within the next 3.5

years (oil) and 4 years (natural gas).

• Manufacturing sector consumes the largest

portion of energy, slightly higher than the

transport sector

• Energy consumption of manufacturing sector

tends to grow. (Manufacturing sector contribute over 40 percent to the country’s GDP).

Source: Energy Statistics & Information 2012, The Department of Alternative Energy Development and Efficiency

BCDEF

www.nesdb.go.th- 25 -

Manufacturing 37%

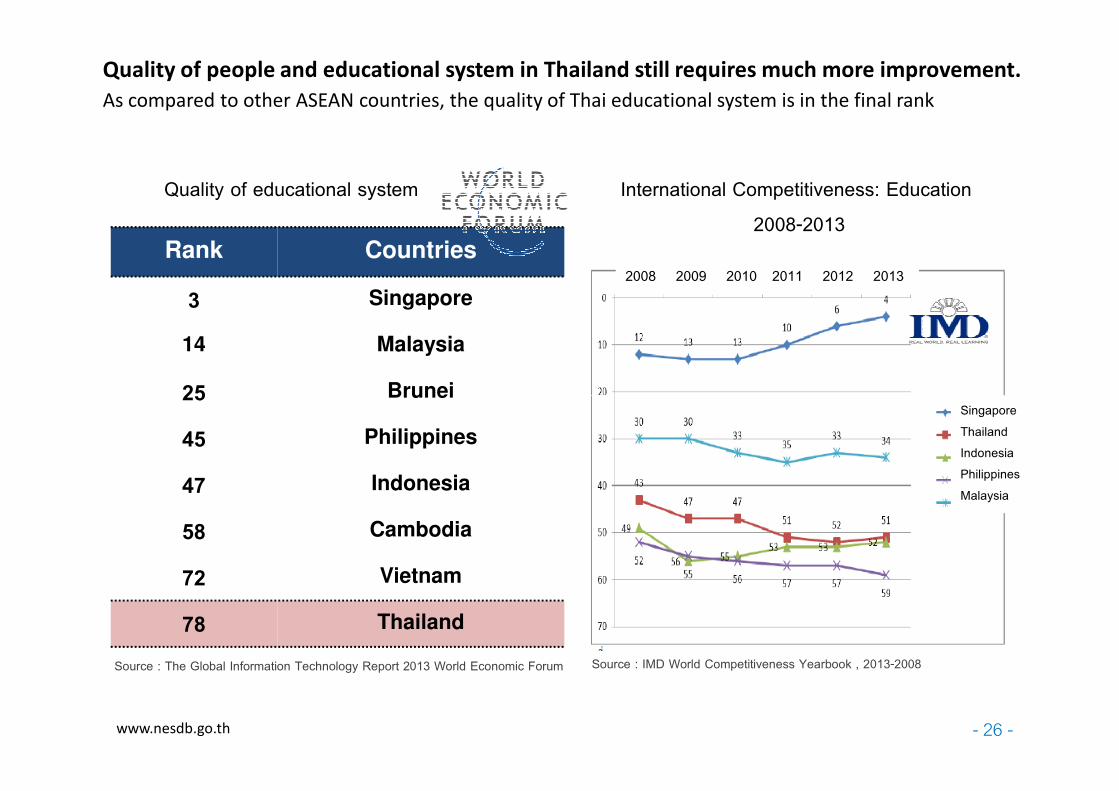

Quality of people and educational system in Thailand still requires much more improvement.

As compared to other ASEAN countries, the quality of Thai educational system is in the final rank

Rank Countries

3 Singapore

14 Malaysia

25 Brunei

Quality of educational system International Competitiveness: Education

2008-2013

2008 2009 2010 2011 2012 2013

25 Brunei

45 Philippines

47 Indonesia

58 Cambodia

72 Vietnam

78 Thailand

Source : The Global Information Technology Report 2013 World Economic Forum Source : IMD World Competitiveness Yearbook , 2013-2008

www.nesdb.go.th - 26 -

SingaporeThailandIndonesiaPhilippinesMalaysia

8.47.4

8.5

13.6

10

15

Average growth rate of labour productivity per GDP of the ASEAN member countries

(Year 2000-2008, 2008, 2009, 2010)

Productivity of Thai labours is in a good position as compared to other ASEAN countries

Labour productivity of Thailand in 2010 was 5.7 percent, higher than the ASEAN average (4.3

percent); however this figure still lags behind that of Singapore (13.6 percent).

3.5 3.4 3.32

0.4

2.6

4.83.6

5.3

0.9

3.5

7.4

2.1

-6.3

0.5

3.4

2.1

-4.5

2.6

-3.9

-1.7-2.9

-4

2.5

0.4

2.1

3.94.6

3.44.6

5.7

4.3 4.3

-10

-5

0

5

Cambodia Indonesia Malaysia Myanmar Philippines Singapore Thailand Vietnam ASEAN

2543-2551

2551

2552

2553

Source : IMD World Competitiveness Yearbook , 2013-2008

www.nesdb.go.th - 27 -

2000-2008

2008

2009

2010

40000

60000

80000

100000

120000

140000

Japan

China

South Korea

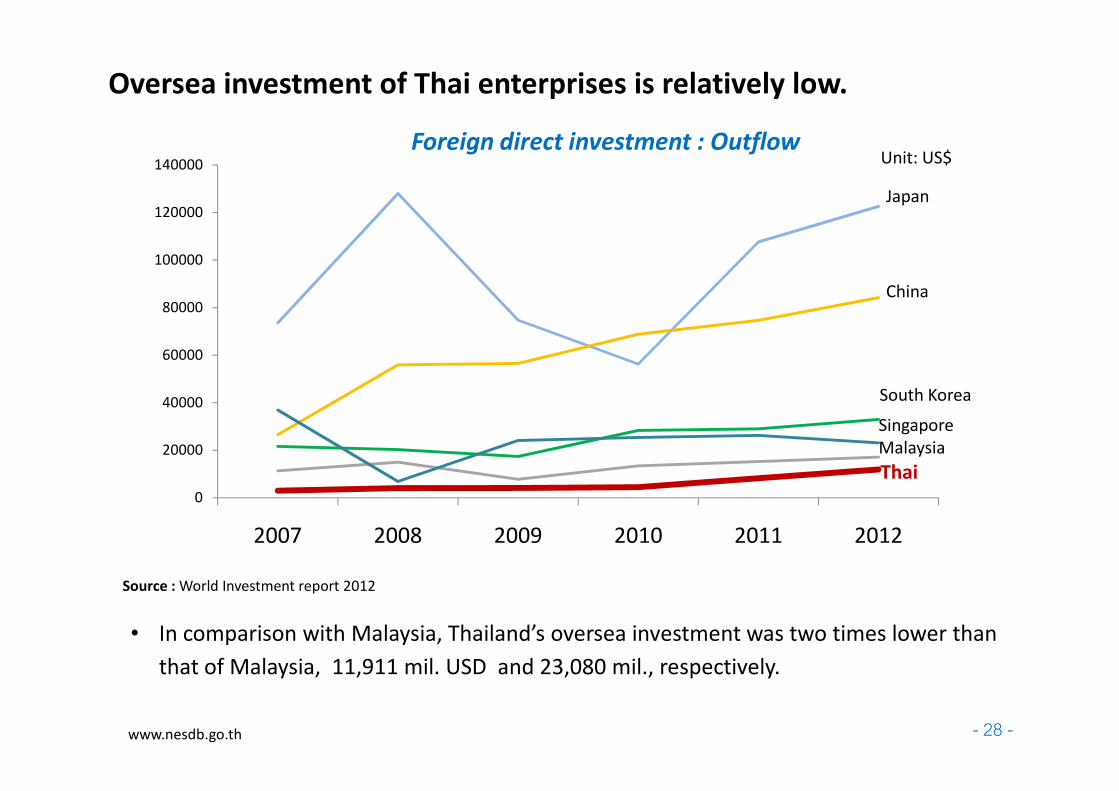

Oversea investment of Thai enterprises is relatively low.

Unit: US$Foreign direct investment : Outflow

0

20000

40000

2007 2008 2009 2010 2011 2012

South Korea

Singapore

Thai

Malaysia

• In comparison with Malaysia, Thailand’s oversea investment was two times lower than

that of Malaysia, 11,911 mil. USD and 23,080 mil., respectively.

Source : World Investment report 2012

www.nesdb.go.th - 28 -

Reasonable Costs

Service & Hospitality

Hi-Technological Hardware

Human Resource Quality1

Competitive Advantage

Although Thailand in overall still has several weaknesses, some manufacturing and service sectors have shown high potentials, e.g. medical service. Thai medical service sector has strong advantage in terms of price, service, friendliness, especially when combining with the attractive locations for tourism.

Thailand Singapore Hong Kong Malaysia India

Human Resource Quality

Human Resource Supply

International Accredited Hospital

Preemptive Move

Synergy/ Strategic Partner

Accessibility/Market Channel

Tourist AttractionRemark: 1 Lower quality in aspect of International Communication onlySource : Data Analysis by private hospital association less more

www.nesdb.go.th- 29 -

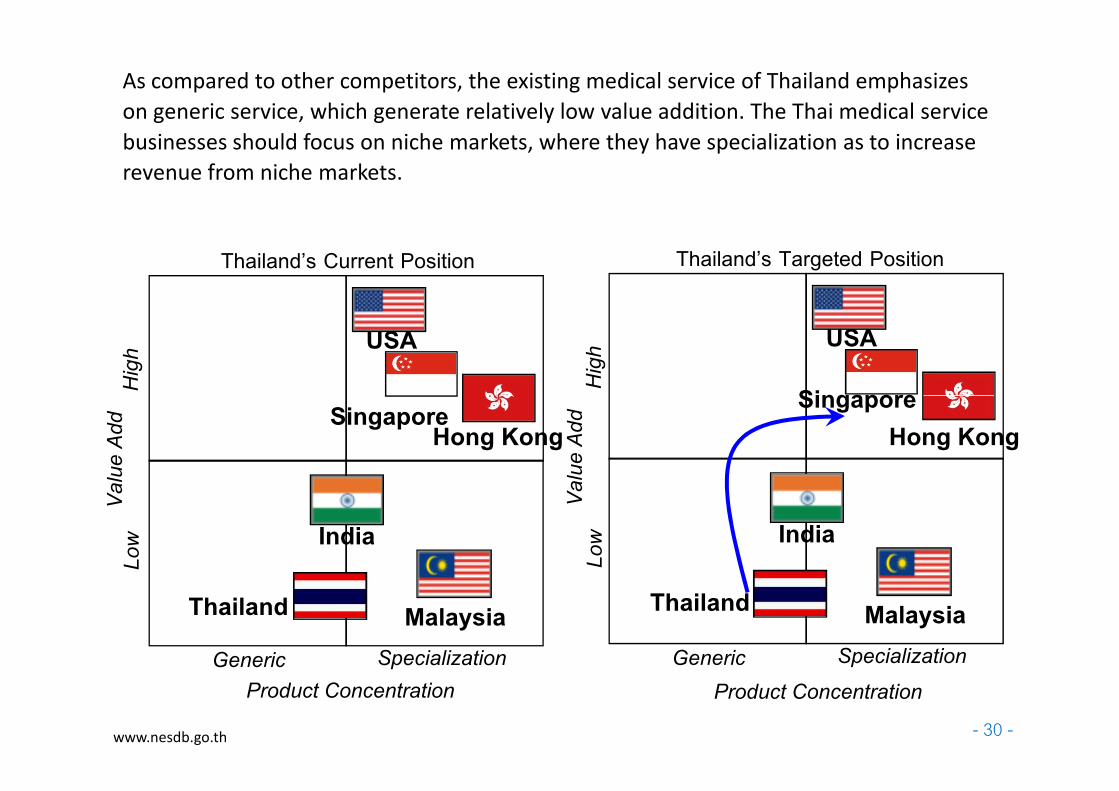

As compared to other competitors, the existing medical service of Thailand emphasizes

on generic service, which generate relatively low value addition. The Thai medical service

businesses should focus on niche markets, where they have specialization as to increase

revenue from niche markets.

High

Singapore

USA

High

Singapore

USA

Thailand2s Current Position Thailand2s Targeted Position

DEFGH : CMU Data Compilation and Analysis

Product Concentration

Generic Specialization

Value Add

Low

Singapore

India

Malaysia

Hong Kong

Generic Specialization

Value Add

Low

Singapore

India

Malaysia

Hong Kong

Product Concentration

- 30 -www.nesdb.go.th

ThailandThailand

58,848

23,874

3,186 2,687 2,392

4,4643,543

4,474

7,759

2,535

10.8

49.8

23.44

16.21

1.4

11.72

18.57

5.01

12.8715.45

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0

10

20

30

40

50

60

China Thai UAEIndiaHong Turkey Malay- Viet- Mexico Singapore

4

World Ranking

Top 10 Exporters of Design Products Among Developing Economies, 2008 Growth (%)

Value (million US$)� Thailand is the major exporter

of design products among

developing countries, ranked

the 4th among developing countries in 2008.

Thailand’s creative and design industries are highly competitive internationally.

� Major exported design products

of Thailand include interior

design, graphic design, fashion and jewelry design, and toy

design.

Source: UNCTAD, based on official

data in UN COMTRADE database

China Thailand

UAEIndiaHong Kong

Turkey Malay-sia

Viet-nam

Mexico Singapore

84,807

33,254

5,047 4,7603,524

4,272

9,450

5,3695,0775,167

14.96

9.13

16.92

5.996.33

15.7

10.31

1.05

12.86

44.77

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

0

5

10

15

20

25

30

35

40

45

50

China Thai-land

UAEIndiaHong Kong

Turkey MalaysiaKoreaMexico Singa-pore

6

World Ranking

Growth (%)

Value (mil. US$)

Top 10 Exporters of Creative Products Among Developing Economies, 2008

� Thailand is the 1st exporter of creative goods in ASEAN and the 6th among developing countries, with the export value of 5,077 Mil. USD, accounting 1.25% of market share.

� In terms of growth, Thai export of creative products grew by 10.31% in 2008, higher than that of Malaysia, Singapore, and South Korea

www.nesdb.go.th- 31 -

design.

Outline of Presentation

2 Facing New Challenges in Changing

Global Contexts

Current Performance of Thailand’s

Competitiveness1

Readiness of Thai Industries Ready in

the Challenging Global Arena

www.nesdb.go.th - 32 -

Next Steps of Thai Industries Towards

Sustainable Competitiveness

3

4

The Future of Thailand

Out of middle-income countries

• Increase income per capita

The center of economic linkage in the region.

• The center of trade and investment of the region with modern regional transportation and ICT networks that connect ASEAN to the world.

• Enhance the quality of life and the effective systems of education, health and justice throughout Thailand

Alleviate social inequality

More environmental friendly

• Reduce greenhouse gas emissions

Enhance the national competitiveness

Promote Thailand to be:

• Production source of the quality and safe food, halal food, eventually leading to become the kitchen of the world

• The center of automotive and parts manufacturing, R&D and automotive testing of Asia.

• The hub of medical services, tourism and clean energy production and services in the ASEAN region.

www.nesdb.go.th - 33 -

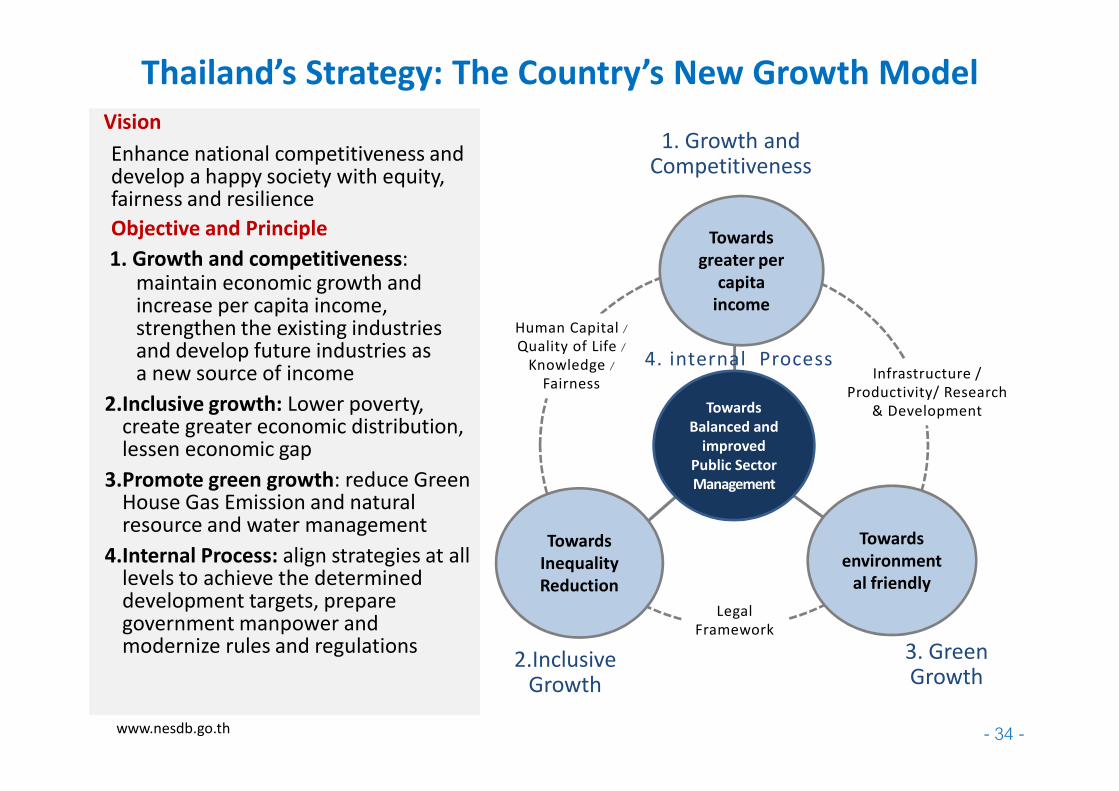

Thailand’s Strategy: The Country’s New Growth Model

Vision

Enhance national competitiveness and develop a happy society with equity, fairness and resilience

Objective and Principle

1. Growth and competitiveness: maintain economic growth and increase per capita income, strengthen the existing industries and develop future industries as a new source of income

2.Inclusive growth: Lower poverty,

Human Capital / Quality of Life /

Knowledge / Fairness

Infrastructure /

Productivity/ Research

1. Growth andCompetitiveness

Towards

greater per

capita

income

4. internal Process

2.Inclusive growth: Lower poverty, create greater economic distribution, lessen economic gap

3.Promote green growth: reduce Green House Gas Emission and natural resource and water management

4.Internal Process: align strategies at all levels to achieve the determined development targets, prepare government manpower and modernize rules and regulations

www.nesdb.go.th - 34 -

Productivity/ Research

& Development

Towards

Inequality

Reduction

Towards

environment

al friendly

Towards

Balanced and

improved

Public Sector

Management

Legal

Framework

2.InclusiveGrowth

3. GreenGrowth

Potential Manufacturing and Service Sectors of Thailand

Tourism

Retails

Rubber

Field Corn

Rice

Agriculture

ServiceRubber products

Petrochemical and Plastic

Develop future industries

Healthcare products(alternative medicines including

Health Herbs Remedies, Cosmetics

& Beauty Supply)

Clean Energy

6655

Strengthen existing industries

Food Processing

Retails

Construction

Fisheries

Bio Energy(Cassava/Sugarcane/Palm oil)

LivestockMedical service

Electrical and

Electronics

Industry

Fruits Biochemical products/Bio-plastics/ Bio Materials

Creative Industry(Fashion/ Design/ Advertisement

/Architecture/ Jewelry/ Robot/ OTOP)

Transportation &Telecommuni-cation

Source: NESDB and Ministry of Industry 2012-2031

Aviation & Aerospace Industries

35

Biodiesel/Ethanol

Automotive and parts

Research and DevelopmentResearch and Development

ProductivityGreen

From country strategy to industrial development

More environmental-friendly industries:

developing and adjusting manufacturing

processes to reduce the impact on

environment, in order to ensure a quality

product to customers.

R&D and innovation development:

promote commercialization of research

works to reduce foreign technology

reliance and meet real needs of markets.

Enhance productivity:

developing manufacturing

process to reduce costs

and eliminate non-

value-added activities Productivity

ClusteringInclusive

Growth

Inclusive

Growth

Poverty and Income Distribution• Emphasize on local

employment and skill development.

• Promote the use of local raw materials

• Industries can sustainably coexist with society and community

www.nesdb.go.th - 36 -

value-added activities

Collaboration and linkage

within industry: promote

clustering of local firms with

strong collaboration between

government and community

to be able to connect to

global cluster.

Local Entrepreneurs

Outbound Investment

Joint Venture

ASEAN Player

Combination Strategy

Strategy implementation for production and service sectors should take into account on characteristics of entrepreneurs that are different in terms of capabilities and needs for support. The government should provide appropriate incentives, measures and resources to drive the strategies effectively and efficiently.

Formulate strategies that fits to characteristics of entrepreneurs

Combination Strategy

Strengthening current mechanisms

Integrating several mechanisms towards

more united policy alignment

Collaborating between mechanisms of central government and local

authorities (both in public and private

sectors)

www.nesdb.go.th - 37 -

Implementing mechanism for production and service sector development