Embed Size (px)

Citation preview

Details of USDA’s CFAP farmer aidThe Coronavirus Food Assistance Program (CFAP) includes $9.5 billion from the CARES Act and $6.5 billion from USDA’s Commodity Credit Corporation. We have payment rates on News page 3 and analysis of the program on News page 4.

Helpful links on the payment rates: • youtube.com/watch?v=Rne7_cIVeFU• farmers.gov/cfap/faq

Update on the next Covid-19 aidThe GOP-controlled Senate wants to assess impacts from current aid before considering an alternative to the $3 tril-lion-plus economic relief bill passed with Democratic votes in the House. Senate Republicans plan to push for return-to-work incentives and big investment in infrastructure in the next aid package. Meanwhile, President Donald Trump says he won’t close the country if a second wave of Covid-19 hits.

Tours find smaller HRW cropsA crop tour coordinated by Kansas Wheat estimated the state’s wheat crop at 284.4 million bushels. Crop scouts noted dryness, freeze damage and stripe rust clipped yields. Separate crop tours pegged the Oklahoma wheat crop at 96.5 million bu., Colorado at 54.2 million bu. and Nebraska at 42.1 million bushels. USDA estimated the wheat crop at 305.5 million bu. in Kansas, 102.6 million bu. in Oklahoma, 61.1 million bu. in Colorado and 41.8 million bu. in Nebraska.

Covid-19 impacts on meat stocksUSDA reported pork stocks of 614.8 million lbs. at the end of April, down 1.9 million lbs. (0.3%) from March compared with an average 26.8-million-lb. increase the previous five years. Pork stocks were down 6.6 million lbs. (1.1%) from last year. Beef stocks at 490.0 million lbs. dropped 12.3 mil-lion lbs. (2.5%) last month versus the usual 6.6-million-lb. decline. Beef stocks were still 59.8 million lbs. (13.9%) greater than last year. While beef production declined 3.8% from year-ago and pork output fell 4.4% in April, demand was cut by Covid-19 restaurant/foodservice shutdowns.

More uninspiring trade — Grain and livestock markets continued to drift sideways to most-ly lower last week amid a lack of supportive news. Corn futures continued to hold above their early May and April contract lows. Soybeans moved to new lows for the month but remained above their contract lows from April. Barring a bullish event, seasonals point corn and soybeans lower after May. SRW and HRS wheat futures gave back a good portion of earlier gains by Friday, while HRW futures declined for the week. With winter wheat harvest nearing, it’s going to be difficult to generate buyer interest — even if crop estimates decline. Cattle futures traded sideways, despite their big discounts to the cash market. Hog futures continued to pull back from the early May highs as traders anticipate contra-seasonal cash weakness into summer.

U.S., China rhetoric escalatesTrump tweeted Chinese President Xi Jinping is behind a “disinformation and propaganda attack on the United States and Europe.” He says China “could have easily stopped the plague, but didn’t,” referring to Covid-19. The U.S. is also upset about China’s new national security laws in Hong Kong to thwart protests. Plus, the U.S. Senate is making a push against U.S. stock exchange listings of some Chinese companies. Beijing has turned more aggressive against Trump and the U.S. in anti-American propaganda.

Despite the growing tensions, China is pledging to meet its Phase 1 trade commitments and has increased purchas-es of U.S. goods, including purchases of ag products.Perspective: Some China watchers believe Trump will

turn very aggressive against Beijing later this year if he believes he will lose the November election.

Shipment of U.S. ethanol rerouted to ChinaChina is expected to receive a shipment of U.S. ethanol

later this month that was originally sold to a Saudi buyer. A similar transaction happened earlier this year with a U.S. ethanol shipment to Malaysia that eventually ended up in China. The last direct shipment of U.S. ethanol to China was in March 2018. China is also expected to reopen its market to U.S. dried distillers grain imports soon.

China clears more meat, seafood and dairy plantsChina’s list now includes 499 beef, 457 pork, 470 poultry,

397 seafood and 253 dairy facilities eligible to export.

Slight boost in RFS proposalsBloomberg reported EPA’s proposed level of advanced bio-fuels would rise to 5.17 billion gallons for 2021, from 5.09 billion gallons for 2020. The mandate for conventional corn-based ethanol would remain at 15 billion gallons. The plan would increase the 2022 biodiesel mandate to 2.76 bil-lion gallons, up from 2.43 billion gallons for 2021.

Administrator Andrew Wheeler told Congress no decision has been made on requests to reduce 2020 biofuel blending mandates, but EPA is considering ways to help small refineries.

`News this week...2 — What fast planting pace may mean for soybean yields.3 — Payment rates for the coming CFAP aid. 4 — Analysis of USDA’s CFAP payment program.

May 23, 2020 Vol. 48, No. 21

Go to ProFarmer.com

May 23, 2020 / News page 2

Follow us on Twitter:@ProFarmer@BGrete

@ChipFlory@JWilson29

@DavisMichaelsen@MeghanVick

Plentiful rains expected this summerThe extended forecast from the National Weather Service (NWS) calls for increased odds of above-normal precip over virtually all major corn and soybean producing areas for June through August. The forecast shows “equal chances” for above-, below and normal temperatures dur-ing the three-month period, with above-normal temps for the remainder of the country.

A b o v e - n o r m a l rainfall and neutral to warm temps would suggest favor-able conditions for crop development.

The extended NWS forecast fits with the Climate Prediction Center’s (CPC) outlook call-ing for roughly two-thirds odds that ENSO-neutral con-ditions will persist through summer. Odds of La Niña

developing (warmer and drier conditions) during the growing season are put at only 25% to 38% by CPC.

S. Plains drought shrinks — a littleRains across the Southern Plains allowed the drought foot-print to shrink a little during the week ended May 19. But the U.S. Drought Monitor shows some form of dryness/drought remains across 77% of Colorado (including moder-ate to extreme drought over much of the eastern part of the state), 52% of Kansas (including some severe and extreme drought in southwestern areas), 38% of Texas (including much of the panhandle) and 28% of Oklahoma (including most of the western third of the state). Southern Nebraska is also covered by abnormally dry conditions.

HRW crop rating slightly improvesUSDA trimmed the amount of winter wheat rated “good” to “excellent” by a percentage point to 52%, while the “poor” to “very poor” rating held at 16%. On the weighted Pro Farmer Crop Condition Index (0 to 500 point scale, with 500 being perfect), the HRW wheat crop improved 1.0 point to 328.6 points, while the SRW crop dropped 3.4 points to 361.0 points. This marked the first weekly improvement in the HRW crop this spring; the CCI rating is still down 21 points from the beginning of April. The CCI rating for the SRW crop is now down 1.9 points from the beginning of April.

Soybean planting passes half doneSoybean planting jumped to 53% complete as of May 17, which was 15 percentage points ahead of the five-year average. Of the top 13 production states, only Arkansas (47% done vs. 57% on average), Missouri (27% vs. 29%) and North Dakota (9% vs. 35%) were behind average. USDA reported 18% of the soybean crop had emerged, six points ahead of the five-year average.

What the rapid bean planting pace could mean for yieldsSince 1974 there have been 17 years in which soybean

planting reached at least half done by May 20. In those years, yields averaged 98.9% of the previous record. Applying that to the current record yield of 51.9 bu. per acre would equate to 51.3 bu. per acre. But two of those were the drought years of 1988 and 2012. Removing them, the average of the other 15 years is 100.7%, equating to a yield of 52.3 bu. per acre. If we limit the study to the seven years that set records, the average is 105.6%, which would equate to 54.8 bu. per acre. For the 10 years (including 1988 and 2012) that were not a record, the average was 94.2%, equal to 48.9 bu. per acre.

Barring a drought year like 1988 or 2012, the rapid plant-ing pace this year implies a yield of 48.9 bu. to 54.8 bu. per acre compared with USDA’s trendline of 49.8 bu. per acre.

Corn planting 80% completeUSDA reported 80% of the U.S. corn crop was planted, nine percentage points ahead of the five-year average. Of the top 12 production states, only Missouri and North Dakota were lagging their normal planting rates. Corn emergence jumped 19 percentage points to 43%, which was three points ahead of average.

Spring wheat seeding still well behindU.S. spring wheat seeding jumped 18 points to 60% com-plete, though that was still 20 points behind normal. Planting remains behind in North Dakota (41% planted versus the usual 76%), Montana (75% vs. 77%) and Minnesota (70% vs. 86%). Crop emergence was 16 points behind the five-year average at 30%.

North Dakota is the trouble spotBased on March planting intentions, North Dakota still had 2.6 million acres (80%) of corn, 6 million acres (91%) of soybeans and 3.6 million acres (59%) of spring wheat left to plant as of May 17. The final crop insurance plant date for most of the state is May 25 for corn, June 5 for wheat and June 10 for soybeans.

NWS 90-day Temps

A: Above-normalB: Below-normalEC: Equal chances June-Aug.

NWS 90-day Precip

A: Above-normalB: Below-normalEC: Equal chances June-Aug.

May 23, 2020 / News page 3

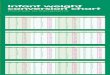

Finalized payment rates for CFAPUSDA’s Coronavirus Food Assistance Program (CFAP) will make direct payments to farmers from the CARES Act and Commodity Credit Corporation (CCC). Producers will receive 80% of their eligible payment upon approval of the application. The remaining portion, not to exceed the pay-ment limit, will be paid later — funds permitting.

CropCARES Act

Payment RateCCC Payment

Rate

Barley — malting only (per bu.) $0.34 $0.37

Canola (per lb.) $0.01 $0.01

Corn (per bu.) $0.32 $0.35

Upland Cotton (per lb.) $0.09 $0.10

Millet (per bu.) $0.31 $0.34

Oats (per bu.) $0.15 $0.17

Sorghum (per bu.) $0.30 $0.32

Soybeans (per bu.) $0.45 $0.50

Sunflowers (per lb.) $0.02 $0.02

Durum (per bu.) $0.19 $0.20

HRS wheat (per bu.) $0.18 $0.20

Livestock EligibleCARES Act

Payment Rate

CCC Payment

Rate

Cattle (per head)Feeders: Less than 600 lbs.

$102.00 $33.00

Feeders: 600 lbs. and more

$139.00 $33.00

Slaughter Cattle: Fed

$214.00 $33.00

Slaughter Cattle: Mature

$92.00 $33.00

All Other Cattle $102.00 $33.00

Hogs and Pigs(per head)

Pigs: Less than 120 lbs.

$28.00 $17.00

Hogs: 120 lbs. and more

$18.00 $17.00

Lambs and Yearlings(per head)

All Sheep Less than 2 Years Old

$33.00 $7.00

Dairy (per lb.) Milk $0.0471 $0.0147

Non-specialty crops — CARES: 50% of the eligible inventory on Jan. 15 times the payment rate. Eligible inven-tory is the lower of unpriced inventory as of Jan. 15, or 50% of the producer’s 2019 production of that commodity.

CCC: 50% of the eligible inventory times the payment rate.Livestock — CARES: Sales volume between Jan. 15 and

April 15 times the rate. CCC: Highest inventory from April 16-May 14 times the rate.Dairy — CARES: Producer’s certified milk production for

the first quarter of calendar year 2020 times the rate. CCC: A national adjustment to each producer’s pro-

duction in the first quarter times the rate.

Producer Crop Comments...Please send crop comments to [email protected].

Kankakee Co. (east-central) Illinois:“It’s a mess around here. We’ve had 8-plus inches of rain since April 19.”

Iroquois Co. (east-central) Illinois:“Mother Nature always wins. We went from almost done with planting to prepping to replant overnight. At least we won’t be replanting in dry dirt.”

Macon Co. (central) Illinois:“There are geese on the ponds in the middle of fields. Planting percentages are all over the board in this area. Wet farms will be a struggle.”

Wood Co. (northwest) Ohio:“I’m not sure what’s worse... 2019 where we didn’t get the chance to plant or this year where we had a beau-tiful window, got all our crops in and then watched one system flood it all.”

Ross Co. (central) Ohio:“It looks like June will be interesting. Replant corn and soybeans, sidedress and spray corn, spray soybeans, harvest barley and wheat, and plant double-crop beans.”

Dodge Co. (southeast) Minnesota:“Another year, another 3-plus inch rain storm leaves us wondering how long corn can stay under water.”

Red Willow Co. (southwest) Nebraska:“Corn planting is done and early stands look good. The recent 1.8 inches of rain boosted rough looking wheat.”

Campbell Co. (north-central) South Dakota:“I have more 2019 corn still standing unharvested in fields than I have planted for 2020. Let that sink in.”

Stevens Co. (southwest) Kansas:“We are bone dry. Can’t sniff a rain.”

Carroll Co. (north-central) Missouri:“We were patientlt waiting for better conditions to plant, but we decided it won’t grow in a bag. What is planted and emerged hasn’t seen sunshine in three weeks.”

Signs of limited summer beef featuresLast week we highlighted our concerns about beef losing demand due to surging retail prices, which will cause con-sumers to seek cheaper proteins. There’s proof in wholesale trade to signal the concerns extend to the wholesale level.

The amount of beef sold on a forward basis suggests retail features and restaurant promotions of beef will be lighter than normal through summer. For the week ended May 15, packers sold only 283 loads of beef for delivery 22 to 60 days forward, down from 880 loads during the same week last year and the five-year average of 773 loads. Only 30 loads were sold for delivery 61 to 90 days out. Retailers and restaurants will need to buy more beef on the spot market, which creates more price uncertainty.

May 23, 2020 / News page 4

USDA’s top officials say more Covid-19-related ag sec-tor aid is needed beyond the $16 billion Coronavirus

Food Assistance Program (CFAP). That’s a clear sign the program just unveiled has gaping holes.

USDA did not design an easy-to-understand paymentBecause the funds come from two different sources,

there are different payment rates (see tables on News page 3). Payment rates are largely derived in a similar fashion: Estimating the price drop from the week of Jan. 13-17, 2020, to the week of April 6-9. Do payment stipulations penalize those that marketed crops before mid-January? Yes, but USDA insists there must be downside price risk to participate in the payments, as directed by Congress.

Signup runs from late May through late AugustSignup begins May 26 and ends Aug. 28, with the initial

payment coming seven to 10 days after your application is approved. USDA will have a payment calculator ready to roll when signup begins. You can download the applica-tion tool and required forms at farmers.gov/CFAP.

Payment limits are double the initial proposalPayments are limited to $250,000 per person or legal

entity. For many producers, the payment limit will be a critical factor. For example, a dairy with just over 600 cows will hit the payment limit — nearly two-thirds of the nation’s dairy cows are on operations with 600 or more cows; over half have more than 1,000 cows. The same applies to larger crop and livestock farms. If there were no payment limits, producers of all eligible com-modities could have qualified for $19 billion.

Participants that are corporations, limited liability com-panies, and limited partnerships are eligible for up to $750,000 (if at least three shareholders meet certain labor or management contribution requirements).

An individual or legal entity is ineligible for CFAP if their adjusted gross income (AGI) is greater than $900,000 unless 75% or more of the AGI is derived from farming, ranching, or forestry-related activities. For general partnerships and joint ventures, the provision is applied to each member.

Aid is limited to 2019 or earlier for non-specialty cropsWhy? USDA Secretary Sonny Perdue insisted that pay-

outs not impact current plantings. A future but different program should deal with 2020 crop impacts.

Some restrictions apply for CFAP eligibilityThose commodities that did not suffer a 5% or greater

price decline from mid-January to mid-April are not eligi-ble for CFAP. Ineligible commodities include sheep more than two years old, eggs/layers, soft red winter wheat, hard red winter wheat, white wheat, rice, flax, rye, peanuts, feed barley, extra long staple cotton, alfalfa, forage crops, hemp and tobacco. Except for hemp and tobacco, USDA may reconsider a payment if credible evidence is provided that supports a 5% or greater price decline. Note: We expect USDA to make more wheat varieties

available, and some egg product producers.

Concerns raised by cattle producersA producer who sold cattle weighing at least 600 lbs.

between Jan. 15 and April 15 will receive $139 per head compared with a producer marketing cattle after April 15, who will receive $33 per head. USDA says limited funding is the reason. Another concern: Treatment of cattle sold from a feedlot to a packer after a feedlot finishing period.

Some contract growers are eligibleA contract grower who does not own livestock is eligible

for CFAP if they have price risk in the contracted livestock.

What’s not in CFAP... and what’s likely coming• Funding beyond the current $16 billion in direct pay-

ments will be part of the aid package coming in June.• USDA can tap $14 billion in additional CCC funding

after June. Congress should honor USDA’s $50 billion increase in CCC borrowing authority request.

• There’s an effort to do away with payment caps for CFAP and future ag aid payouts.

• Indemnity payments for livestock producers who had to euthanize animals will be a part of coming aid.

• Some lawmakers want to expand liability protections for meat plants. Exceptions would be lawsuits proving criminal misconduct or gross negligence.

• The biofuel sector will also get some aid utilizing USDA’s CCC funds. A proposed bill from Senators Chuck Grassley (R-Iowa) and Amy Klobuchar (D-Minn.) would require USDA to reimburse biofuel producers for feedstock purchases from Jan. 1 through March 31 via the CCC.

• There’s a push to help the cotton industry with costs associated with delayed and cancelled sales/shipments and increased stocks.

CFAP ag aid: What’s in, what’s not... and what’s aheadby Editor Brian Grete and Washington Policy Analyst Jim Wiesemeyer

News alert and analysis exclusively for Members of Professional Farmers of America® 402 1/2 Main St. Cedar Falls, Iowa 50613-9985General Manager Joel Jaeger • Editor Brian Grete • Editor Emeritus Chip Flory • Sr. Market Analyst Jeff Wilson • Chief Economist Bill Nelson • Washington Policy Analyst Jim Wiesemeyer

Digital Managing Editor Meghan Vick • Inputs Monitor Editor Davis Michaelsen • Sr. Economist Alan BarrettSubscription Services: 1-800-772-0023 • Editorial: 1-888-698-0487

©2020 Professional Farmers of America, Inc. • E-mail address: [email protected] Journal CEO, Andrew Weber • Division President Grey Montgomery

Feed MonitorFEED

Corn Game Plan: We have advised cover-ing all your corn-for-feed needs in the cash market through the end of May. We plan to go hand to mouth and wait for confirma-tion of a low before adding to coverage.

Meal Game Plan: You should have all soybean meal purchases covered in the cash market through the end of May. The next sharp break may offer long-term buying opportunities.

Corn II’20 67% III’20 0% IV’20 0% I’21 0%

Meal II’20 67% III’20 0% IV’20 0% I’21 0%

Analysis page 1

$317.30

$304.10

DAILY JULY MEAL

DAILY JULY LEAN HOGS

Position Monitor

HOGS - Fundamental AnalysisFutures fell to three-week lows before stabilizing on speculation the rapidly improving slaughter rate won’t lead to a collapse in cash bids. Summer futures remain at historical discounts to the CME Lean Hog Index. Pork stole the meat case spotlight last week with lots of ribs for Memorial Day on sale. Pork cuts will continue to garner more featuring with rising supplies. Market-ready hog supplies remain burdensome, limiting strength in pork and cash hog prices. China canceled prior purchases for a second straight week, but it continued to actively take shipments of U.S. pork. New sales to China are needed to sustain a recovery.

Game Plan: Fu-tures are trading below the cash in-dex. We’ll evalu-ate late-summer and fall hedges af-ter the next rally. Strong exports will remain price supportive.

CASH CATTLE PRICE ($/CWT.)

CASH LEAN HOG PRICE ($/CWT.)

Position MonitorGame Plan: Hedges are risky with futures trad-ing far below the cash market. We are willing to keep all risk in the recovering cash market at this time.

Feds Feeders II’20 0% 0% III’20 0% 0% IV’20 0% 0% I’21 0% 0%

A close above $101.50 would target resistance at $108.25.

Initial support at the uptrending line near $96.70 is backed by the 40-day moving average (green line) near $92.50.

A close above the 40-day moving average (green line) near $58.21

could trigger a test of horizontal resistance at $66.10.

Initial support is at $54.25.Strong support is the April 6 contract low at $49.00.

DAILY AUGUST LIVE CATTLE

$101.50

CATTLE - Fundamental AnalysisPackers continue to bring slaughter operations back on line with daily kills rising to a six-week high. Top cash bids held about steady at $120. Worries that cash bids have plateaued and will decline into summer amid weakening wholesale beef prices capped the futures rally. Still, the drop in beef cutouts has been slower than expected, suggesting good domestic demand. But beef faces increasing competitive pressure from pork and chicken over the coming months due to much cheaper wholesale prices and greater availability. Beef will have to fight its way back into the spotlight over the summer as retail prices will stay high.

$314.60

$108.25

$76.875

$66.10

$80.50

$297.50

May 23, 2020ANALYSIS

Lean Hogs II’20 0% III’20 0% IV’20 0% I’21 0%

Initial resistance is the broken support line at $297.50.

The contract low at $282.00 is initial support, followed by $278.00 on the continuation chart. $282.00

$49.00$49.00

May 23, 2020 / Analysis page 2

$5.30 1/2

DAILY JULY SRW WHEAT

WHEAT - Fundamental AnalysisSRW - Futures rebounded from key support as dry conditions in Europe and the Black Sea region and smaller U.S. crop estimates from this week’s tours of fields in the Plains encouraged fund short-covering. Export demand has been routine and more business is needed to sustain rallies.

Position Monitor

Game Plan: On May 20, we advised taking small profits on short hedges covering 20% of 2020-crop. Be prepared to sell into additional strength if disappointing rainfall and cover-age occurs in Europe and the Black Sea areas.

Initial resistance at $5.30 1/2 is backed bythe 40-day moving average (green line)

near $5.31 1/2. Key resistance is thedowntrend line near $5.55.

Initial support is the March low at $4.94 1/4. Stronger supportis at $4.60 (not shown). $4.94 1/4

CORN EXPORT BOOKINGS (MMT)AVERAGE CORN BASIS (JULY)

CORN - Fundamental AnalysisFutures popped to a four-week high but quickly retreated amid beneficial U.S. weather and routine export demand. With few current signals for a Midwest drought, funds seem unwilling to exit large short positions. China’s corn futures tumbled last week on news the government will begin auctioning inventories to boost domestic supplies. The market is waiting to see China begin replacing those state-owned reserves with imports. Weekly ethanol production rose to a six-week high, pushing inventories to the lowest since late January, but gasoline use fell. The slow improvement ethanol output helped to firm corn basis. Cheap Brazilian sugar ethanol will dominate the world export market.

Initial resistance at the 40-day moving average (green line)

near $3.41 1/2 is backedby resistance at $3.43.

Initial support is the April 21 contract low at $3.25 1/2. Stronger support is at $3.10 on the continuation chart (not shown).

DAILY DECEMBER CORN

$3.55 1/4

$3.25 1/2

$3.75

$3.43

DAILY JULY CORNPosition Monitor

Game Plan: Make sure the stop-close-only or-ders for old- and new-crop hedges are in place as a close above the April 23 highs in corn futures could trigger an extended price cor-rection. Keep stop-close-only orders at $3.31 in July corn and $3.43 in December corn on hedges covering 50% of old- and new-crop supplies. Cash marketers should be prepared to increase old-crop sales on rallies.

Strong resistance begins at the 40-day moving average (green line)

near $3.26 and is backed by horizontal resistance at $3.31.

Initial support is the April 21 contract low at $3.09. Stronger support from the weekly continuation chart is at $3.01 and then $2.90 (not shown).

$3.31

$3.09

’19 crop ’20 crop

Cash-only: 60% 0% Hedgers (cash sales): 50% 0% Futures/Options 50% 50%

’19 crop ’20 crop

Cash-only: 100% 30% Hedgers (cash sales): 100% 30% Futures/Options 0% 0%

May 23, 2020 / Analysis page 3

DAILY JULY HRS WHEATDAILY JULY HRW WHEAT

HRW - Prices followed rallies in Paris and Black Sea futures before forecasts turned wetter for this week. Coverages and amounts will provide direction after the holiday because smaller supplies will likely trigger a quick boost in importer buying. When world wheat crop outlooks decline, wheat tends to bottom in April and May.

$8.87

DAILY NOVEMBER SOYBEANS

HRS - Spring wheat futures firmed on slow planting progress across the Northern Plains and Canadian Prairies, increasing risks for lower output. Record Russian domestic wheat and flour prices are increasing demand for stockpiling high-protein wheat supplies. Funds are covering record short positions in spring wheat futures.

$8.36 3/4

$9.00

Downtrending resistance near $5.26 must be

cleared to signal a low.

A close below the contract low at $5.02 would target support at $4.88.

A close above old support at $4.73 would turn the trend back higher.

$4.73

Key support is at the contract low of $4.27 1/4. $5.02

$8.31

$4.27 1/4

Initial resistance at the 40-day moving average (green line) near $8.56 is backed by thedowntrend line near $8.69.

Initial support at the March 18 low of $8.36 3/4 is backed by contract-lowsupport at $8.31.

SOYBEAN EXPORT BOOKINGS (MMT)AVERAGE SOYBEAN BASIS (JULY)

WHEAT EXPORT BOOKINGS (MMT)

AVERAGE WHEAT BASIS (JULY)

SOYBEANS - Fundamental AnalysisA lull in Chinese purchases after big sales a week earlier encouraged funds to cut bullish bets. Futures also fell on favorable Midwest weather forecasts for this summer after national plantings reached 50% done. Escalating U.S./China political conflict added to late-week selling as President Xi Jinping sent a clear message to Washington that it will do what it wants in Hong Kong. China’s new security law on Hong Kong threatens to trigger a U.S. reprisal. Questions are rising as to whether China will fulfil its purchase commitments in the Phase 1 trade deal, despite Beijing’s assurances it would. Brazil is headed for a record month of shipments to China in May. Soymeal fell to new lows, adding to soybean weakness.

Initial support is the March 18 low at $8.29. Stronger support is at the April 21 contract low at $8.18 1/2.

$9.20 1/2

$8.29

$8.61 1/4

Position Monitor ’19 crop ’20 crop

Cash-only: 70% 0% Hedgers (cash sales): 70% 0% Futures/Options 0% 0%

Game Plan: We want to increase old-crop cash sales on price strength tied to new China purchases and reopening economies. We have advised selling 70% of old-crop inventories. Rallies toward $8.60 to $8.70 in July futures should be rewarded with new sales. We want to be patient on mak-ing new-crop sales with November futures below the spring crop insurance price.

DAILY JULY SOYBEANS

$8.18 1/2

$8.95 3/4

$8.77 1/2

A close above $8.61 1/2 wouldwould target stronger resistance

at $8.77 1/2 and $8.95 3/4.

May 23, 2020 / Analysis page 4

’19 crop ’20 cropCash-only: 100% 10% Hedgers (cash sales): 100% 0% Futures/Options 0% 25%

75.61

New Member App Download the Pro Farmer app, included with your membership! Search for “Pro Farmer” in your app store. Available on Apple and Android devices.

USDA Export Sales ReportWatching for more China business.

FRI 5/29 7:30 a.m. CT

5

U.S. Personal IncomeApril income & spending dropped.

FRI 5/297:30 a.m. CT

4

USDA Crop Progress ReportWarmer weather aids emergence.

TUE 5/263:00 p.m. CT

3

USDA Export Inspections Corn shipments remain active.

2

Memorial Day HolidayPlease remember all who served.

MON 5/2510:00 a.m. CT

1

WATCH LIST

TUE 5/2610:00 a.m. CT

market closer to the renewal of a major bear market. Similar years warn that bear markets often renew sooner than later.

Last week, the market reached nearly a four-week high but failed to hold the rally. If the corn market is going to rally on fund short-covering, like the 80¢ rally last year, the bullish catalyst will likely have to come from major Chinese purchases or a strong wheat rally on deteriorating world crop conditions.

Soybeans often “fail” after Memorial Day or by June when the U.S. crop is planted early and gets off to a good start. Funds increased longs on May 12 to more than 32,454 contracts, the most since November, which was then followed by a 50¢ price drop during the next four weeks.

Money managers extended their net short in corn futures and options to 214,054 contracts through May 12, the most bearish positioning in a year.

Funds added more than 107,000 shorts to their corn position during the prior six weeks as July futures fell about 25¢.

Corn prices have been under heavy pressure since the onset of the Covid-19 pandemic. Falling oil demand slashed ethanol output and livestock producers curbed feed use as packing plants closed or slowed. U.S. farmers are also in the early stages of growing what is expected to be a record crop, pointing ending stocks to the highest since 1988.

Each week that passes from now through the end of June likely brings the

By Sr. Market Analyst Jeff WilsonFROM THE BULLPEN

Crude Oil: Just a few weeks ago, crude oil was akin to industrial waste, something you had to pay people to take away. Now prices are surging, up about 78% since the end of April.

The turnaround came quicker than most expected. Larger-than-expected OPEC+ and U.S. output cuts and the world’s first steps out of Covid-19 lock-downs have helped the crude oil mar-ket out of the abyss of negative prices.

GENERAL OUTLOOKChinese oil demand reportedly

almost rebounded to pre-pandemic lev-els. Gasoline and diesel are leading the oil recovery, boosting ethanol produc-tion to a six-week high while inventories dropped to the lowest since late January.

Crude oil is now rising above down-trending resistance. A confirmed low would signal the world economies are coming out of shutdowns quicker, pro-viding an inflationary lift to ag markets.

DAILY DECEMBER COTTON

Game Plan: On May 20, we advised selling December futures to hedge 25% of 2020-crop. We advised cash marketers to sell 10% of 2020 with hedge-to-arrive contracts.

Position Monitor AVERAGE COTTON BASIS (JULY)

COTTON - Fundamental AnalysisFutures rose near resistance at 60.00¢ and retreated. The specter of a big U.S. cotton crop, rising global carryover and slack worldwide consumer demand for clothes and textiles was plenty of ammunition to stall the fledg-ling price recovery.

COTTON EXPORT BOOKINGS (’000 BALES)

DAILY CRUDE OIL FUTURES

Crude oil prices would confirm a cyclical low on a close above $41.05.That would likely providean inflationary lift to allag markets, especially corn.

Initial support at the uptrend line near 57.60¢ is backed bythe 40-day moving average (green line) near 56.15¢. Strong support is the April 2 contract low at 50.18¢. 50.18¢50.18¢

Initial resistance is at $59.50¢.Stronger resistance is

the downtrend line near 64.45¢.

59.50¢59.50¢

$41.05$41.05