Embed Size (px)

Citation preview

MOODYS.COM

2 AUGUST 2012

NEWS & ANALYSIS Corporates 2 » Veto of TNK-BP Dividend and Russian Court Ruling Are Credit

Negative for BP » Lowe’s Bid for RONA, if Successful, Will Improve its Credit Profile » Hess to Finance Bakken Expansion Partly with Higher Borrowing, a

Credit Negative » Weak Platinum Outlook Is Credit Negative for Anglo American » Insider Trading Charge Against Well Advantage Is Credit Negative

for Glorious Property

Infrastructure 7 » Oncor’s Dividend Increase to Parent EFH Is Credit Negative

Banks 8 » Brazil’s New Funding Tool for Specialized Midsize Banks Is Credit

Positive » Margin De-Dollarization Is Credit Negative for Argentina’s Futures

and Options Clearinghouses » China’s Friendlier Rules for Investors Are Credit Positive for

Chinese Securities Firms » Executive Resignations at Nomura Are Credit Negative

Sovereigns 14 » Power Outages in India Highlight Acute Credit-Negative

Infrastructure Constraints » Bahamas’s Nationalization of Telecom Would Be Credit Negative

for Sovereign and CWC » Slovak Government’s New Tax Measures Are Credit Positive » Jordan Reaches Preliminary Stand-By Arrangement with the IMF, a

Credit Positive

CREDIT IN DEPTH US Corporates 20

Defaults by US companies slowed in the second quarter from the elevated pace of the prior two quarters, and our default forecast remains benign as spec-grade companies maintain good liquidity. We expect the US speculative-grade default rate to peak at 4.0% in October and decline to 3.0% by June 2013.

RECENTLY IN CREDIT OUTLOOK » Articles in last Monday’s Credit Outlook 25

» Go to last Monday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Corporates

Veto of TNK-BP Dividend and Russian Court Ruling Are Credit Negative for BP Last Monday, Alfa Group-Access-Renova (AAR, unrated), a consortium of Russian investors with a 50% stake in TNK-BP International Ltd. (Baa2 negative), rejected a proposal from BP Plc (A2 stable), which owns the other 50%, for TNK-BP to pay an interim dividend of $1 billion. This latest development came just days after a Siberian court on 27 July ordered BP to pay TNK-BP $3.1 billion in damages over its aborted strategic alliance with OJSC Oil Company Rosneft (Baa1 stable). These setbacks are credit negative for BP, and they coincide with the company’s weak second-quarter financial performance. However, we do not see these developments posing a material risk to BP’s rating.

Although BP would benefit from a TNK-BP dividend, the loss or delay of its $500 million share will not have a significant effect on its strong liquidity profile, which at the end of second-quarter 2012 included $14.9 billion of cash. News of AAR’s rejection comes less than a week after BP announced that it had entered negotiations to sell its 50% stake in TNK-BP to Rosneft. Relations between BP and AAR have long been strained as the two sides have struggled to align their respective interests in TNK-BP. Last month, AAR notified BP that it was prepared to purchase half of BP’s stake in TNK-BP, triggering a 90-day period of “good faith” negotiations as required by the TNK-BP shareholder agreement.

Meanwhile, the $3.1 billion award to TNK-BP by the Tyumen Arbitration Court in Siberia relates to compensation for unrealised gains from a potential offshore Arctic partnership with Rosneft. A minority shareholder in TNK-BP Holding, the Russian holding subsidiary of TNK-BP International, filed the lawsuit to challenge a proposed strategic alliance between BP and Rosneft to jointly explore offshore reserves in the Kara Sea and swap shares. However, strong opposition from AAR, which argued that the proposed deal breached the terms of its shareholder agreement, derailed the alliance after AAR was able to get the deal blocked in the courts.

Given the rank of the court that awarded TNK-BP the $3.1 billion, and BP’s plan to appeal the ruling, we believe TNK-BP is unlikely to receive funds anytime soon. However, if the ruling stands it would be credit negative for BP and positive for TNK-BP since the proceeds of the award would contribute an amount equal to more than 50% of TNK-BP’s 2012 cash flow.

Although the reported production and dividends that BP has received from its stake in TNK-BP have been sizable, those benefits are counterbalanced by the political risk and governance challenges surrounding this investment. This potential award to TNK-BP would be a substantial call on BP, particularly amid its protracted and ongoing efforts to resolve its litigation and liabilities related to the 2010 Deepwater Horizon oil spill in the Gulf of Mexico.

James Thomson Associate Analyst +44.20.7772.8658 [email protected]

Julia Pribytkova Vice President - Senior Analyst +7.495.228.6071 [email protected]

Thomas S. Coleman Senior Vice President +1.212.553.0365 [email protected]

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Lowe’s Bid for RONA, if Successful, Will Improve its Credit Profile Home-improvement retailer Lowe’s Companies Inc. (A3 stable) on Tuesday said it had made a non-binding, unsolicited offer to acquire Canadian retailer RONA Inc. (unrated) for about CAD1.8 billion, an offer RONA rejected. We believe there is a reasonable likelihood that Lowe’s will return with a higher offer. If Lowe’s proves successful in its bid for RONA, the transaction will have positive credit implications for Lowe’s over the next couple of years because it will accelerate its push into Canada.

With 800 corporate, franchise and affiliate stores under several banners, and annual revenue of CAD4.8 billion, RONA will quickly make Lowe’s the largest home-improvement retailer in Canada, based on revenue, helping it counterbalance its slowing sales growth in the US. RONA would also provide Lowe’s with local expertise in the Canadian market.

In addition, RONA’s network of 14 distribution centers will strengthen Lowe’s distribution network in Canada, eliminating the need for it to build out its own distribution network. Furthermore, the combined entities would likely provide cost-saving opportunities from purchasing and merchandising.

Although we view the offer to acquire RONA as credit positive, there is no current impact on Lowe’s A3 long-term rating or its Prime-2 commercial paper rating. We view the unsolicited offer as part of a more aggressive financial policy, and we expect the transaction will temporarily weaken Lowe’s credit metrics.

Indeed, Lowe’s will likely need to borrow money to finance the transaction, and RONA has about CAD450 million in existing debt. At this transaction size, we expect that Lowe’s debt-to-EBITDA ratio will remain below 2.75x, the level we cite as prompting a potential downgrade. A higher offer for RONA could increase the amount that Lowe’s may need to borrow, placing further pressure on its credit metrics and potentially hurting Lowe’s ratings.

Maggie Taylor Vice President - Senior Credit Officer +1.212.553.0424 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Hess to Finance Bakken Expansion Partly with Higher Borrowing, a Credit Negative Hess Corporation (Baa2 stable) on 25 July announced during its second-quarter earnings call that it planned to expand its capital spending this year by 25%, to about $8.5 billion. The bigger spending program and resulting negative free cash flow are credit negative for Hess. However, we do not expect the program to put negative pressure on the exploration and production company’s rating or outlook.

Hess plans a far bigger outlay in the Bakken Shale formation in North Dakota, which by itself will account for some $3 billion, or roughly 35% of Hess’s capital spending this year. But Hess plans to reduce any debt increase by selling some $2 billion in assets, and will benefit from the effects of high oil prices on its mostly oil-linked production base.

The 25% increase in Hess’s 2012 capital and exploration budget would widen its projected cash flow deficit for the year to what the company estimates will be $3 billion. Much of the increase stems from its higher spending in the Bakken. Production in the unconventional oil play has boomed in the past couple of years and Hess wants to accelerate its development there while oil prices remain high enough to justify the cost of producing in the remote region.

Beyond the Bakken, Hess is drilling appraisal wells in the Eagle Ford and Utica Shale formations and continuing major production and development in the deepwater Gulf of Mexico, Equatorial Guinea, the Valhall field in Norway, and field expansion in the Gulf of Thailand. Hess is also conducting large exploration and seismic programs in Ghana, Brunei, the deepwater Gulf of Mexico, and Kurdistan.

To finance the Bakken and its other capital expansion, Hess is borrowing under its committed bank revolver, with plans to sell a range of assets by mid to late 2013. More borrowing would raise Hess’s balance-sheet debt to a peak of about $8 billion, depending on oil prices, up from just over $6 billion at the end of 2011.

Much of Hess’s anticipated debt increase had already occurred by mid-year 2012 — its balance-sheet debt stood at $7.85 billion at 30 June — but the capital expansion could push its bank debt higher, raising Hess’s total debt/proven developed reserves to about $10 per barrel of oil equivalent (boe) and its total debt/average daily production to $20,000 per boe, based on current crude prices and the higher budget.

Hess’s stable rating outlook hinges on our view of continued strong oil prices and our expectation that its planned asset sales will help bring leverage metrics down to levels more in line with its Baa2 rating by mid-2013. The company has announced more than $850 million in asset sales this year and indicated plans for an additional $2 billion in asset sales, which would help reduce its financial leverage by mid to late 2013 and ease the pressure from rising debt. The stable outlook depends on good operational performance, delivery on production growth in 2012-13, and timely completion of its planned asset sales.

In the meantime, Hess is transforming its portfolio to refocus and reduce risk in its exploration and development programs. Hess draws considerable benefit from its oil-based production profile, strong cash margins, and good cash flow metrics, all of which we expect will ease the effects of what we think will be a temporary spike in its financial leverage.

Thomas S. Coleman Senior Vice President +1.212.553.0365 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Weak Platinum Outlook Is Credit Negative for Anglo American On 27 July, Anglo American Plc (Baa1 stable) published half-year results that showed that the group’s platinum business’s operating profits fell 85% compared with the first six months of 2011. The decline is the result of continued macroeconomic weakness, falling vehicle sales in Europe, and rising global supplies from new and extended mines, all credit negative factors that have pushed average platinum prices down 13% over the past year. Moreover, lower platinum prices, combined with an inflationary environment in South Africa, the location of 75% of global platinum production, and a weak outlook for end-user markets, portend Anglo American’s platinum operations remaining a drag on the company’s financial performance over the next 12-18 months.

Platinum prices have fallen steadily to $1,450 per ounce in June from $1,789 in January 2011 as a 7% decrease in new European vehicle sales lowered demand for autocatalysts, which are a key component in vehicle exhaust systems. Autocatalysts account for around 38% of the world’s platinum consumption and European vehicle demand alone accounts for around 18% of total platinum demand. At the same time, total global platinum supplies increased to around 6.5 billion ounces in 2011, a 7% increase over 2010 levels, as new capacity in South Africa and North America entered production. Given the increased global supply base and limited probability of a rapid recovery in new European vehicle sales, we expect the platinum market to remain in a structural state of oversupply, limiting any potential for major price appreciation this year.

Anglo American’s platinum business, which accounted for 16% of revenue in the first half of 2012, but just 2% of operating profits, saw refined platinum sales fall 21% by weight owing to weak demand, curtailed operations, strikes and safety stoppages across South Africa. Despite the weakening fundamentals across the platinum business, cash costs of production per refined equivalent ounce increased by 11%, the result of inflationary pressures on labour, electricity and fuel. We expect this underlying trend of weakening demand and inflationary pressure to continue in the second half.

Although Anglo American is the world’s leading global producer of platinum, we do not expect the current weakness in the platinum business to have a negative ratings impact because the company is highly diversified and has a significant project pipeline that will improve its commodity and geographic mix. Management is also taking steps to address the underlying problems at the platinum business. Since placing the business under strategic review in February, the company has suspended production at the high-cost Marikana mine, and cut the business’s capital expenditures for this year to $900 million from $1.2 billion. In addition, the group is considering selling, closing, or placing under care and maintenance some of the smaller, higher cost platinum mines.

UK-based Anglo American is a global leader in the mining and natural resources sector. The group operates in more than 40 countries across Africa, Europe, South and North America, Australia and Asia, and its core mining portfolio is well balanced between precious (platinum and diamonds), bulk (coal and iron ore) and base metals (copper and nickel). In 2011, the group reported sales of $30.6 billion, excluding revenues from non-consolidated associates.

Andrew Metcalf Associate Analyst +44.20.7772.1464 [email protected]

Shruti Kulkarni Associate Analyst +44.20.7772.1388 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Insider Trading Charge Against Well Advantage Is Credit Negative for Glorious Property On 27 July, The US Securities and Exchange Commission (SEC) accused Hong Kong-based Well Advantage Ltd. (unrated) of insider trading. The SEC claimed that Well Advantage, a private company indirectly owned by Zhang Zhirong, purchased shares of Canadian energy producer Nexen Inc. (Baa3 review for upgrade) ahead of the public disclosure that Chinese state-owned oil company CNOOC Limited (Aa3 stable) had planned to acquire Nexen for $15 billion.

The insider trading allegation is credit negative for Glorious Property Holdings Limited (B3 negative), a Hong Kong-listed company of which Mr. Zhang controls 68.39% and is its founder and chairman, as the charges harm Mr. Zhang’s reputation and could hurt Glorious Property’s access to the equity capital markets.

The SEC said that Well Advantage and “other unknown traders” used accounts in Hong Kong and Singapore to purchase Nexen shares based on confidential information about the acquisition. The SEC claimed that Well Advantage bought more than 830,000 shares of Nexen on 19 July, four days before the merger announcement, resulting in an unrealized gain of around $7.2 million.

Although the SEC did not specifically accuse Mr. Zhang of wrongdoing, it asserted that he had close ties to CNOOC. The US regulator also obtained an emergency court order freezing the assets of Well Advantage and others implicated in the matter.

Following news of the SEC’s allegation, the stock prices of Glorious and China Rongsheng Heavy Industries Group Holdings Ltd. (unrated), a ship-making company that is around 46%-owned by Mr. Zhang, began trading as if investors were rattled by the incident. Glorious’s stock price dropped around 12% in the two days following the news. Meanwhile Rongsheng’s shares fell approximately 23%, although some of the decline also may be linked to the company issuing a profit warning.

The pressure over Glorious’s share price implies that it would have difficulty accessing the equity capital markets to improve its liquidity and strengthen its capital position. Such a development is negative to Glorious, which has already been affected by the weak property market. Moreover, investors likely will have concerns about any financial liabilities that Mr. Zhang may have arising from the insider trading allegations.

However, we expect this incident will have a limited immediate direct impact on Glorious’s credit profile, and will not affect its day-to-day operations. Well Advantage only has a small stake in Glorious (less than 0.4% as of December 2011), and Glorious’s management team beyond Mr. Zhang will continue running the operation. The company has already clarified that its board makes all decisions regarding material projects and investment projects, similar to the practice of other listed companies in Hong Kong.

Given the complexity of a US-based investigation into non-US entities, and the web of rather convoluted corporate relationships, the SEC’s probe is likely to be lengthy. However, if there are any adverse developments, including, but not limited to, bank refinancing activities, a material change of control event, or actions by the Hong Kong Stock Exchange, it would affect Glorious’s credit profile.

Franco Leung Assistant Vice President - Analyst +852.3758.1521 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Infrastructure

Oncor’s Dividend Increase to Parent EFH Is Credit Negative On Tuesday, Oncor Electric Delivery Company LLC (Baa1 negative) disclosed in its June quarterly filing a higher dividend payment to its parent, Energy Future Holdings Corp. (EFH, Caa2 CFR negative), which brings Oncor’s annualized upstream dividend to $220 million. That figure, which is materially higher than the $145 million dividend paid in 2011, is credit negative.

The upstream dividend payments exacerbate the contagion risk that Oncor has to majority owner-parent EFH, which is under financial stress and is likely to need some form of restructuring in 2013-14. Although a strong suite of ring fence structures insulate Oncor’s creditors from EFH, only a bankruptcy court can determine whether the protections are sufficient, and Oncor, EFH or the Public Utility Commission of Texas (PUCT), its primary regulator, do not want to see that ring fence put to the test.

On 27 February, we changed Oncor’s rating outlook to negative from stable because of two primary issues that are beyond the control of both Oncor and PUCT. The first issue is the contagion risk to EFH. The second issue is EFH’s indirect leveraging of Oncor’s implied equity value, which has now risen to over $5 billion and is likely to approach at least $6 billion over the next 12 months.

Despite the ring fence provisions, EFH has used its implied equity value in Oncor as a primary source of liquidity. As EFH pledges more of its equity in Oncor for funding, we start looking through the ring fence protections to assess its credit quality. In addition, we note that EFH’s indirect financing structure of using Oncor’s equity does not benefit Oncor, and that Oncor is not legally liable for its parent’s debt service obligations.

Jim Hempstead Senior Vice President +1.212.553.4318 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Banks

Brazil’s New Funding Tool for Specialized Midsize Banks Is Credit Positive Last Friday, the Brazilian Monetary Council (CMN) announced a new enhanced guaranteed time deposit that will replace the existing guaranteed time deposit (DPGE) that expires in December 2015. The new instrument, which the CMN calls DPGE II, is a permanent funding alternative that will help specialized midsize banks diversify their funding mix with an instrument that better matches their maturity needs, a credit positive.

The CMN’s announcement demonstrates that regulators recognize the difficult liquidity conditions that specialized banks face, and that these banks have been important players in consumer lending. As the large Brazilian retail banks announce reductions in their loan growth guidance for 2012 owing to high delinquency levels and macroeconomic deceleration, the viability of the specialized banks becomes more important for loan origination. The creation of a permanent funding instrument that can adequately support these banks’ operations is a critical regulatory boost to the segment.

The CMN structured the new instrument as a time deposit guaranteed by Brazil’s deposit insurance fund, Fundo Garantidor de Créditos (FGC, unrated), and will require that banks post collateral in the form of eligible loans equal to 120% of the value of the banks’ deposits. Such a collateralization requirement will substantially reduce FGC’s risk. Under the current mechanism, FGC bears the full risk of the guaranteed banks.

FGC will charge banks a lower fee in exchange for the collateral (see Exhibit 1). In addition, DPGE II will involve deposits with shorter tenors, which will ensure that that bank liabilities more closely match assets and loan guarantees based on market dynamics.

EXHIBIT 1

Differences Between Brazil’s Enhanced Guarantee Time Deposit Programs

Original DPGE DPGE II

Tenor 2 to 5 years 1 to 3 years

Cost to FGC 1% per year 0.3% per year

Collateral None 120% in credit receivables

Maximum Amount to be Issued per Bank

2x Tier 1 equity at year-end 2008 or 1x total deposits at June 2008

1x Tier 1 equity, increasing to 2x after 5 years, or up to BRL5 billion

Source: Central Bank Resolution no. 4115/2012 and Moody’s

Although the CMN is phasing out the original DPGE, banks can still issue time deposits within their available limits. As of July, the volume of DPGE issued by FGC was BRL26 billion ($12.8 billion), as shown in Exhibit 2. The amount corresponds to 85% of FGC’s total funds.

Ceres Lisboa Vice President - Senior Credit Officer +55.11.3043.7317 [email protected]

Alexandre Albuquerque Assistant Vice President - Analyst +55.11.3043.7356 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

EXHIBIT 2

Total Volume of DPGE Issued in Brazil

Source: CETIP and Moody’s

DPGE II will benefit specialized payroll lenders that have fully utilized their DPGE limits under the previous rules. Such lenders include Banco Bonsucesso S.A. (B1 negative; E+/b1 stable)1 and Banco Cruzeiro do Sul S.A. (Caa1 negative; E/caa1 negative).

We also see an opportunity for consumer lenders and other wholesale funded banks, such as Banco Panamericano S.A. (Ba2 stable; E+/b1 stable), Banco BVA S.A. (B2 stable; E+/b2 stable) and Banco Maxima S.A. (B2 stable; E+/b2 stable). These banks rely heavily on securitizing their loans to third-party banks or to investment funds. However, over the past two years, the attractiveness of securitizations has declined substantially following the discovery of accounting problems and fraud by some securitizing banks.

The loans that the banks will use as collateral will be registered at the central credit clearing (locally known as C3), minimizing control issues. The first DPGE II will be issued in September.

1 The ratings shown are the bank’s foreign-currency deposit ratings, its standalone bank financial strength rating/baseline credit

assessment and the corresponding rating outlooks.

-

5

10

15

20

25

30

Apr-09 Apr-10 Apr-11 Apr-12

BRL

Billi

on

Jul-12YTD

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Margin De-Dollarization Is Credit Negative for Argentina’s Futures and Options Clearinghouses Last Friday, Mercedes Marcó del Pont, the president of Argentina’s central bank, announced the government’s intention to require that guarantees and margins in the country’s futures markets be held in pesos instead of dollars or other foreign currencies. The de-dollarization of margins is credit negative for local clearinghouses such as Mercado a Término de Buenos Aires S.A. (MATBA, B1 stable) and the Rosario Futures Exchange (ROFEX, unrated) because it will introduce currency risk into their operations. This currency risk comes from the mismatch between commodity contracts priced in dollars and the peso-denominated margins. We also expect trading volumes in the exchanges to decline, as the mismatches render trading less attractive.

Under the proposed new regulatory framework, margins must be replenished frequently to reflect variations not only in commodity prices but also in the exchange rate, where the official exchange rate lags the informal dollar rate by roughly 40%.

Argentina is one of the world’s largest exporters of corn, soybeans, and wheat, and a top supplier of soybean oil and soybean meal. Its local grains futures market operates in foreign currencies, in line with international commodities prices, and serves as a partial hedge against domestic inflation, which private economists estimate will be 20%-25% a year in a scenario in which the country’s currency devalues further.

Unlike CME Group Inc.’s (Aa3 stable) Chicago Board of Trade (CBOT), most futures contracts in Argentina include the delivery of physical merchandise, functioning as a forward sales market and using the US soy futures at the CBOT as their key pricing reference. Any buyer of a contract for future grain delivery makes a margin deposit in dollars at the exchange to guarantee the purchase. The government now wants these margin deposits held in pesos, although futures contracts would still be priced in US dollars.

This announcement comes at a time when commodity exchanges report sustainable growth of trading volumes (see exhibit). Volumes soared more than 80% in the first half of 2012 from a year earlier, boosted by traditional soybean, wheat and corn contracts.

EXHIBIT 1

Argentina Exchange Volumes

Source: Mercado a Término de Buenos Aires S.A. and Rosario Futures Exchange

The central bank’s latest move adds to a growing list of recent measures introduced by the authorities to foster the de-dollarization of the economy, and therefore, the preservation of dollar reserves, which have declined as the economy slows and inflation remains high.

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-120.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Mill

ions

Ton

s

ROFEX MATBA

Valeria Azconegui Assistant Vice President - Analyst +54.11.5129.2611 [email protected]

Christian Pereira Associate Analyst +54.11.5129.2634 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Since the announcement of potential changes in margins, both local clearinghouses have seen their business volumes fall by more than 50%, as investors seek clarity on the impact of such measures.

We expect local commodities trading volumes will be seriously hurt if Argentina requires that grains futures be listed in Argentinean pesos, which has been mentioned as a possibility. Farmers will not sell in pesos given that their costs are usually dollar denominated, and this mismatch could cause price distortion and a lack of market transparency. In addition, it would be very difficult to reach agreement on their value given the widening difference in exchange rates.

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

China’s Friendlier Rules for Institutional Investors Are Credit Positive for Chinese Securities Firms On 27 July, the China Securities Regulatory Commission (CSRC) lowered the minimum requirements to participate in the Qualified Foreign Institutional Investors (QFII) program, a gateway into China’s capital markets for foreign investors. The announced measures include a simplified approval process for applicants and the opening up of allowable investment to the interbank bond market and private placements by small and medium-size enterprises.

The relaxation of the requirements is credit positive for China’s securities firms as it will result in more institutional investors participating in the QFII program, creating more business for those firms able to serve foreign investors. The CSRC’s action also is another step towards gradual capital account liberalization.

Although many large institutional investors with QFII licenses and quotas will use their in-house teams for their investments in China, there are other players, including certain fund-of-funds, sovereign wealth funds, university funds, and pension funds, that we expect will find services provided by Chinese securities firms useful.

We expect the large Chinese securities firms that provide advisory and trade execution services to international clients will benefit from an expansion of QFII. Those firms include CITIC Securities (CITICS, unrated), China International Capital Corporation Limited (unrated), Haitong Securities Co, Ltd. (unrated), and Shenyin & Wanguo Securities Co. Ltd. (unrated).

Firms with more international business development will benefit the most. For example, CITICS last month announced its acquisition of Credit Agricole SA’s Asian CLSA unit and will be able to leverage CLSA’s customers to strengthen its pipeline of QFII clients. Foreign securities firms such as The Goldman Sachs Group Inc. (A3 negative) and its joint ventures in China would also benefit as they can leverage their existing relationships with foreign investors.

Under the new rules, CSRC lowered the minimum assets under management requirement to $5 billion from $10 billion for securities companies and commercial banks. For foreign asset-management institutions, insurers and other institutional investors such as pension funds and government-backed investment companies, the regulator cut the minimum to $500 million from $5 billion.

How significantly and how quickly the new rules will expand the QFII sector will depend on many factors including market conditions and investor preference. One important consideration could be the regulatory approval process for QFII licenses and quota. For example, although the CSRC raised the QFII quota to $80 billion from $30 billion in April, the total quota it approved was only $28.5 billion as of 20 July. The pace of the regulatory approval process will affect the number of new QFIIs and their investment activities.

In addition, with more Chinese companies issuing debt and raising equity outside China, QFII is not the only path for foreign investors to gain China exposure. We see only limited QFII-channeled investments in China’s onshore bond market, despite this being one area that the new rules have opened up, because China’s onshore bond markets are still developing and carry risks and costs for which their yields may not fully compensate investors. At the same time, investors can buy offshore bonds issued by Chinese companies. These offshore markets are more transparent and have a better market and legal environment. For example, there are virtually no covenants (even as basic as cross default) in bonds issued in onshore markets. That said, the QFII program remains appealing as a channel that allows for more diverse selection of sectors and companies for investors.

Yi (Yvonne) Zhang Vice President - Senior Analyst +86.10.6319.6562 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Executive Resignations at Nomura Are Credit Negative On 26 July, Nomura Holdings, Inc. (Baa3 stable) announced that CEO Kenichi Watanabe, COO Takumi Shibata, and five other senior managers had resigned. The senior manager resignations included Yugo Ishida, COO of Nomura Asset Management; Hitoshi Tada, chairman of Nomura Securities; and Philip Lynch, regional CEO of Asia ex-Japan. Such wholesale management disruption at Nomura is credit negative and adds to the significant stress the company is facing.

The resignations follow Nomura’s earlier admission that it was involved in the alleged leaking of confidential information about public offerings in Japan. Although Nomura has taken steps to improve internal controls and regain client trust following its admission, it has incurred tangible damage to its core brokerage business in Japan, which is the foundation of its creditworthiness and rating.

Issuers in recent weeks have excluded Nomura from bond underwritings, and the bank has lost mandates to lead manage equity offerings from major customers. The executive resignations are an attempt to draw a line under the problem, while the installation of new management from within the firm ensures continuity and avoids a management vacuum during a difficult time.

However, the new management team faces a significant challenge restoring a reputation tarnished by allegations of loose internal controls. It will be important for the new team to demonstrate quickly, particularly to regulators and clients, that its recent troubles are a rarity and not systemic.

Nomura’s challenges come at a time when its earnings have been volatile as a result of a difficult operating environment and the bank’s international wholesale banking business having a relatively weak 4.2% market share. That weak market share adds to the uncertainty about the business prospects and profitability of Nomura’s international capital market activities, particularly after Nomura’s wholesale business, despite cost cuts, recorded a pre-tax loss of ¥8.6 billion for the first quarter of fiscal year ending 31 March 2013.

The announced management changes are not on their own enough to affect Nomura’s rating at this point. That rating reflects the strengths of its domestic business counterbalanced by weaknesses in its international operations. If Nomura’s domestic business, with its solid retail client base and its leading position in domestic equity and investment banking activities, remains strong, then we see no reason to change the rating. However, if the scandal begins to affect the domestic business, or if negative surprises emerge from the international wholesale business following the management changes, then it could negatively affect the rating.

Maki Hanatate Vice President - Senior Credit Officer +81.3.5408.4029 [email protected]

Elisabeth Rudman Senior Vice President +44.20.7772.1684 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Sovereigns

Power Outages in India Highlight Acute Credit-Negative Infrastructure Constraints

The widespread power blackouts that hit India’s (Baa3 stable) north, east and northeast regions on Monday and Tuesday have had a credit negative effect on the country’s economic activity. The power failure underscores the inadequacy of India’s infrastructure, which inhibits the country’s growth by discouraging investment and impeding productivity improvements. Power disruptions will further depress business sentiment, already dampened by slowing growth and the government’s inability to implement measures to revive investment.

Although power supply interruptions are common in India, the scale of this week’s disruption surpasses all others. Monday’s blackout hit eight states, while Tuesday’s reportedly affected 20 states, which have a combined population of about 700 million people.

The breakdown in the power grid appears to have been the result of a mismatch between electricity demand and supply. India’s power sector suffers from inadequate fuel supplies for the country’s predominantly coal-fired power generation capacity, an inability to transport imported fuels to power stations located inland, and aging and unreliable distribution networks that struggle to deliver generated electricity to consumers. In addition, the sector reports higher-than-usual losses associated with distributing energy across an inefficient infrastructure and losses related to fraud and corruption by consumers who don’t pay for the energy their use. India’s prevalent subsidy system artificially depresses end-prices, leaving state-owned power companies to incur losses and making the sector unattractive for private investment.

Indians’ use of and access to electricity is thus lower than in other fast-growing emerging markets. For instance, the latest available World Development Indicators reveal that as of 2009, just 66.3% of the population had access to electricity, compared with 98.3% for Brazil and 99.4% for China.2 Also, India’s consumption of electricity in 2009 was 571 kilowatt-hours (kWh) per capita, compared with 2,206 for Brazil and 2,631 for China.3

In addition, unreliable power supply limits the private sector’s international competitiveness. Existing and new facilities tend to invest in contingency generators and diesel stockpiles, thus diverting capital and undermining the scope for productivity improvements. As infrastructure constraints raise the relative cost of doing business in India, they also feed its persistent inflation via supply-side bottlenecks.

Such deficits limit the ability of the country’s large working age population to participate fully in the economy.

As the exhibit shows, the high growth rates India enjoyed in the middle of the past decade were largely the result of an acceleration in investment activity, which contributed to over half the increase in real GDP growth during 2001-07.4

2

Gross fixed capital formation peaked after achieving real growth rates of 13.8% in 2006 and 16.2% in 2007, and decelerated to 5.9% during 2008-10, and to 5.5% in 2011. India’s investment activity is unlikely to accelerate to levels required to meet the government’s medium-term goal of 9%-10% real GDP growth targets until the government addresses infrastructure inadequacies. This week’s outages are a reminder of the acute nature of these inadequacies.

World Bank World Development Indicators. 3 World Bank World Development Indicators. 4 Haver Analytics.

Atsi Sheth Vice President - Senior Analyst +1.212.553.4873 [email protected]

Matt Robinson Vice President - Senior Research Analyst +44.20.7772.5635 [email protected]

Andrew Schneider Associate Analyst +1.212.553.4749 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Contribution to India’s Real GDP Growth in Market Prices

Source: Haver Analytics

The potential financial liability from the blackouts for the central and state governments is unclear. Given the frequency of power disruptions, most of India’s larger commercial enterprises produce their own energy supply, while others have their own backup generation capacity. As a result, it is unlikely the government or the state-owned power grid operators will have explicit obligations to provide compensation to consumers suffering disruptions. Nevertheless, the magnitude of this week’s disruptions will increase political pressure on the government to commit to greater capital expenditures in the power sector, which will put further pressure on the government’s already stretched fiscal position.

-10%

-5%

0%

5%

10%

15%

2005 2006 2007 2008 2009 2010 2011

Private Final Consumption Expenditure Government Final Consumption Expenditure Gross Fixed Capital Formation

Change in Stocks Acquisitions Less Disposals of Valuables Net Exports of Goods and Services

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Bahamas’s Nationalization of Telecom Would Be Credit Negative for Sovereign and CWC On Monday, the government of the Bahamas (A3 negative) formed a committee to negotiate the acquisition of a majority equity stake in Bahamas Telecommunications Company (BTC, unrated) as part of an effort to partially reverse a privatization that took place in 2011. The move is credit negative for the sovereign as it raises fundamental concerns about policy predictability and could damage the country’s investment climate. The transaction would also be credit negative for BTC’s parent, British telecom conglomerate Cable & Wireless Communications Plc (CWC, Ba2 negative), as it would lose a majority equity stake in its strongest Caribbean operation and, in a worst-case scenario, management control of a key asset.

Credit negative for the Bahamas. We expect the direct fiscal costs associated with the government’s acquisition of an additional 2% of equity will be relatively modest. However, the government will have to secure scarce funds to finance the share purchase and cover penalty fees and potential litigation costs at a time when its finances are deteriorating. We expect the fiscal deficit will be around 7.4% of GDP in 2012, and that government debt has accelerated to over 51% of GDP from around 30% in 2007.

Credit negative for CWC. CWC has controlled and operated BTC since April 2011, when it purchased a 51% stake in the company for $204 million in cash (and $7 million in taxes) from the Bahamian government’s previous administration. BTC holds exclusive mobile service operation rights in the Bahamas until 2014.

Tony Rice, CWC’s CEO, recently indicated that although he was open to exploring options with the Bahamian government for BTC, he preferred not to negotiate away CWC’s majority equity stake, and for good reason. BTC accounted for 12% of CWC’s fully consolidated revenues and 10% of its EBITDA in fiscal 2012, which ended 31 March, and is CWC’s only Caribbean asset that is currently performing strongly. The rest of CWC’s operations in the region remain under pressure. We expect BTC to be one of the key contributors to CWC’s future EBITDA growth amid continued macroeconomic pressures in the Caribbean and stiff mobile competition in Panama, where CWC also has a presence.

A re-nationalization of BTC will negatively affect CWC’s EBITDA on a proportionately consolidated basis. In the most probable scenario, CWC would be compelled to sell a 2% equity stake to the government. However, we expect CWC to negotiate with Bahamian government to retain management control of BTC. Losing management control of BTC would be a significant credit negative for CWC, preventing the company from being able to fully consolidate BTC in its audited accounts.

Although CWC’s financial guidance calls for a broadly stable fully consolidated EBITDA in fiscal 2013, we believe its leverage by year end could marginally exceed the high end of its own proportionate leverage guidance of net debt/proportionate EBITDA of 1.5x-2.5x because we expect continued negative free cash flow in fiscal 2013. However, we expect free cash flow generation to improve starting in fiscal 2014, largely because of CWC’s decision to rebase its dividend to $0.04 per share in fiscal 2013 from $0.08 per share in fiscal 2012.

Delay telecom deregulation. The buyout negotiations demonstrate the government’s erratic approach to its participation in the telecom sector, and is a reversal of the government’s previous position on divesting and liberalizing the sector. We had expected the liberalization of the telecommunications sector to occur in 2014. Such an about face is a signal of broader policy uncertainty and a deterioration of the operating climate for foreign investors.

Edward Al Hussainy Assistant Vice President - Analyst +1.212.553.4840 [email protected]

Gunjan Dixit Assistant Vice President - Analyst +44.20.7772.8628 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Slovak Government’s New Tax Measures Are Credit Positive Last Thursday, Slovakia’s (A2 negative)

Starting 1 October, the government will extend to retail deposits a 0.4% tax on corporate bank deposits that it introduced on 1 January. Slovak Prime Minister Robert Fico has said that local banks and regulated firms are making large profits in a difficult economy, and therefore are in a position to help the state reduce its deficit.

parliament approved additional taxes on bank deposits and regulated companies’ profits, aiming to use the revenue to support its efforts to cut the budget deficit below the European Union’s (EU) ceiling of 3% of GDP next year. The new taxes, which complement other revenue measures the government has adopted throughout the year, are credit positive as they will help the country rein in its deficit and comply with EU rules.

We estimate the new taxes will boost state budget revenues by €27.5 million, or 0.1% of GDP, this year, and by €110 million, or 0.2% of GDP, next year. Additionally, companies that make at least 50% of their revenues from operations in regulated sectors5

Private sector companies point out that the new measures are unfriendly toward businesses and discourage investment. According to the Slovak Banking Association, banks will pay, on average, 55% of their profits in taxes and levies, which will negatively affect their capital and diminish their ability to provide new loans for economic activity. Finance Minister Peter Kazimir has acknowledged this risk and has said that if the taxes endanger banks’ capital adequacy, the government will respond by amending the law.

will pay an extra 0.363% corporate tax on annual profits exceeding €3 million, which will also provide windfall revenues to the government.

The government’s reliance on revenue measures to narrow its fiscal imbalance makes for a suboptimal consolidation strategy, as revenues could underperform if economic growth and corporate profits disappoint. So far this year, tax revenues have been lower than the government expected: an analysis by the Finance Ministry’s Financial Policy Institute estimates this year’s shortfall in tax revenues will be €250 million (0.4% of 2012 GDP), and that next year’s will be €320 million (0.4% of 2013 GDP).

Given this year’s revenue shortfall, we estimate the budget gap could increase to 5.3% of GDP from a target of 4.6% if the government does not take corrective measures. In addition to the new taxes, the Finance Ministry is considering spending freezes and other cuts worth €

500 million to keep the budget on target. This new position seems prudent given that the deficit will have to be narrowed to 3% of GDP in 2013 to comply with EU rules.

5 Energy firms, telecoms, transport and insurance companies.

Jaime Reusche Assistant Vice President - Analyst +1.212.553.0358 [email protected]

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Jordan Reaches Preliminary Stand-By Arrangement with the IMF, a Credit Positive On 25 July, the International Monetary Fund (IMF) announced a preliminary $2 billion, 36-month stand-by arrangement (SBA) with Jordan (Ba2 negative) that the country will use to address weaker fiscal and external accounts. The SBA is credit positive because it will provide Jordan access to funds equal to 6.5% of 2012 GDP. The final SBA will also likely require mutually agreed upon quantitative targets for Jordan’s fiscal and external accounts, providing greater transparency into the country’s consolidation efforts.

Jordan’s finances have been hurt by higher energy costs, regional turmoil, and lower growth. As the exhibit below shows, official foreign reserves have been particularly hard hit, dropping $3.6 billion since last August, a loss of almost 30% of all reserves in a nine-month period.

Jordan’s Official Reserves Under Pressure

Source: Central Bank Of Jordan

Jordan imports almost all of its hydrocarbon needs. Throughout 2011, saboteurs repeatedly damaged the gas pipeline that links Egypt to Jordan, requiring Jordan to seek alternative energy sources. Because Egypt’s gas is cheaper than oil imports, those alternatives created negative balance of payments for Jordan. Compounding the situation is that Jordan’s subsidy system shelters much of the population from higher energy prices, thereby keeping demand artificially high. Increased external payments have reduced official reserves, raising Jordan’s external debt metrics. Our external vulnerability indicator, the sum of short-term external debt and currently maturing long-term external debt divided by official foreign exchange reserves, will likely rise to more than 100% this year from 86% in 2011, reversing a steady decline since 2008, when it reached 162%.

The agreement announced on 25 July was between Jordan’s authorities and IMF staff, and still requires final approval by the IMF’s executive board, which we expect in the next few months. The IMF loan disbursements will provide much-needed external liquidity and we expect further external support for Jordan in the near future.

The IMF funds follow an announcement on 1 July by Jordan’s Finance Minister Suleiman Hafez that his country had received a $1.25 billion grant from Kuwait (Aa2 stable) that will go toward Jordan’s 2012 capital spending. Kuwait’s grant is equal to 4% of Jordan’s GDP and part of a five-year, $5 billion support program from the Gulf Cooperation Council.

6 See

6

Kuwait’s $1.25 Billion Grant to Jordan Is Credit Positive, Weekly Credit Outlook, 9 July 2012.

$8

$9

$10

$11

$12

$13

Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12

$ bi

llion

s

Gabriel Torres Vice President - Senior Credit Officer +1.212.553.3769 [email protected]

CREDIT IN DEPTH Detailed analysis of an important topic

19 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Pace of US Defaults Slows from Elevated Levels of Last Two Quarters

Default forecast remains benign as speculative-grade companies maintain good liquidity Number of US corporate family defaults declines. There were eight defaults of rated US non-financial corporate families representing more than $5.5 billion of debt in the second quarter of 2012. This compares with 15 defaults representing about $7 billion of debt in the first quarter of 2012 and 16 defaults totaling about $10 billion of debt in the fourth quarter of 2011. There were just four defaults in the year-ago second quarter.

Default rate forecast remains benign. The US speculative-grade default rate was 3.1% at the end of the second quarter, up from 2.9% at the end of the first quarter. Currently, we forecast the default rate peaking at 4.0% in October and declining to 3.0% by June 2013, still well below the late-2009 peak above 14% and the historical average of 4.6% (June 1992-present).

EXHIBIT 1

US Corporate Family Defaults

Note: Includes only the initial default of a non-financial corporate family in a calendar year. Source: Moody’s

Speculative-grade liquidity holding up. Consistent with the benign default rate forecast, speculative-grade companies have good liquidity overall, as indicated by Moody’s Liquidity-Stress Index, which remains at historically low levels. The threat to speculative-grade liquidity is that contagion from Europe’s sovereign-debt problems could depress the US economy and corporate profits, and also cause US credit markets to tighten.

Defaults spanned sectors. The corporate defaults in the second quarter spanned numerous sectors including consumer packaged food and beverage, specialty retail, publishing and gaming. Our one-year default rate forecast is highest for the US corporate sectors listed in Exhibit 2.

0

2

4

6

8

10

12

14

16

18

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

Lenny J. Ajzenman Senior Vice President +1.212.553.7735 [email protected]

CREDIT IN DEPTH Detailed analysis of an important topic

20 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

EXHIBIT 2

US Sectors with the Highest Default Rate Forecast

Industry One-Year Default

Rate Forecast

Services: Consumer 3.66%

Media: Advertising, Printing & Publishing 3.50%

Metals & Mining 3.04%

Services: Business 3.01%

Hotel, Gaming, & Leisure 3.00%

Source: Moody’s

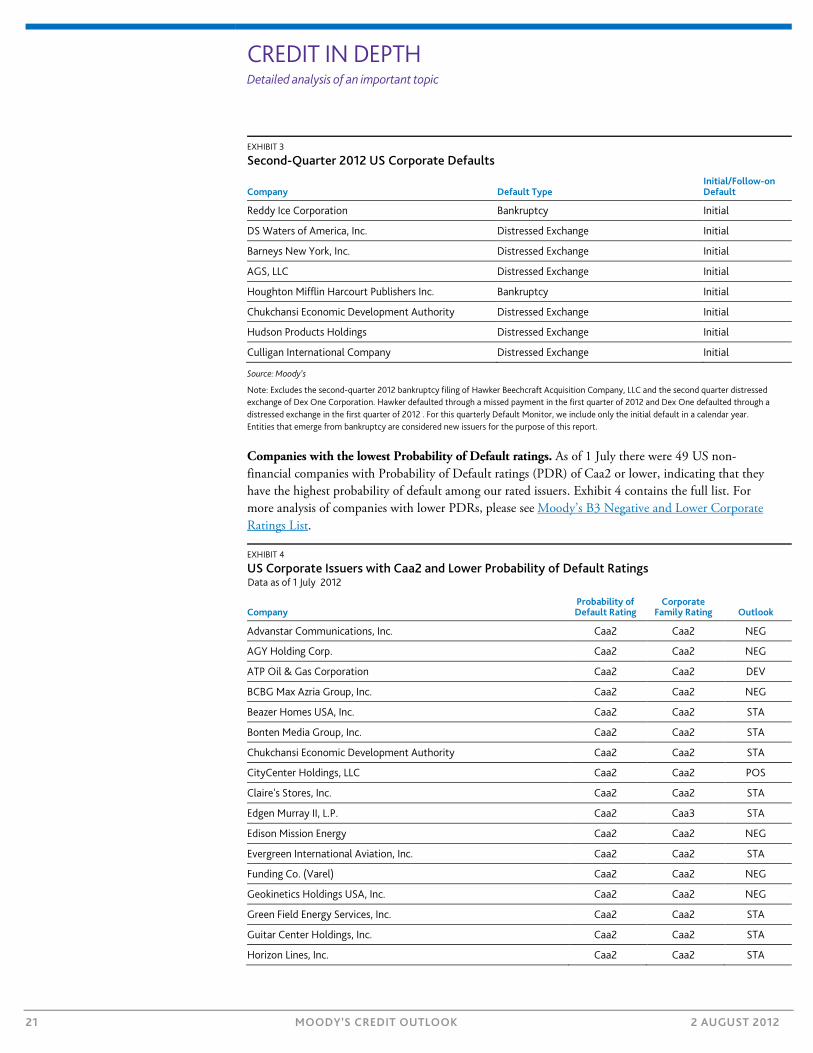

Houghton Mifflin was the largest defaulter. Houghton Mifflin Harcourt Publishers Inc. (ratings withdrawn),7 the education publisher focused on the K-12 market, defaulted on more than $3 billion of debt in connection with its prepackaged Chapter 11 bankruptcy filing in May, the largest default in the second quarter. Reddy Ice Holdings, Inc. (ratings withdrawn), the manufacturer and distributor of packaged ice products, defaulted on more than $450 million of debt in connection with its prepackaged Chapter 11 filing. Both Houghton and Reddy Ice emerged from bankruptcy in the second quarter.

Distressed exchanges were the most prevalent type of default. Of the eight defaults during the second quarter, six were distressed exchanges and two were prepackaged Chapter 11 filings. Distressed exchanges accounted for approximately 40% of total defaults across our rated companies globally in 2010 and 2011. We expect distressed exchanges to remain a common restructuring strategy as the preponderance of higher-ranking loans in the capital structures of leveraged companies will likely persuade junior bondholders to agree to debt exchanges rather than risk low recovery in a bankruptcy. In addition, private equity sponsors, which are prevalent among lower-rated companies, favor distressed exchanges because they often preserve ownership and buy time to restore value to the equity capital.

Distressed exchange detail: Barney’s. Barneys New York, Inc. (ratings withdrawn), the luxury retailer, completed a recapitalization in which it retired an aggregate of $590 million in principal amount of its senior secured term loan and the PIK mezzanine notes in exchange for $50 million in principal amount of newly issued debt and equity.

Distressed exchange detail: Chukchansi. Chukchansi Economic Development Authority (Caa2 stable), a casino operator, completed a restructuring that involved a cash tender offer to acquire notes due 2012 and 2013 (Old Notes) at certain discounts and to exchange notes not purchased by the Authority into new notes due 2020 at certain discounts. Approximately 98% of all Old Notes previously outstanding were either tendered or submitted for exchange, resulting in a total reduction of original debt principal of approximately $60 million.

Distressed exchange detail: Culligan. Culligan International Company (Caa3 negative) exchanged its first-lien term loan for cash and new first- and second-lien term loans. As part of this transaction, the second-lien debt was exchanged for equity in the recapitalized entity.

7 Ratings withdrawn after Chapter 11 filing. We assigned a B2 Corporate Family Rating to the reorganized entity in

connection with its emergence from bankruptcy in the second quarter.

CREDIT IN DEPTH Detailed analysis of an important topic

21 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

EXHIBIT 3

Second-Quarter 2012 US Corporate Defaults

Company Default Type Initial/Follow-on Default

Reddy Ice Corporation Bankruptcy Initial

DS Waters of America, Inc. Distressed Exchange Initial

Barneys New York, Inc. Distressed Exchange Initial

AGS, LLC Distressed Exchange Initial

Houghton Mifflin Harcourt Publishers Inc. Bankruptcy Initial

Chukchansi Economic Development Authority Distressed Exchange Initial

Hudson Products Holdings Distressed Exchange Initial

Culligan International Company Distressed Exchange Initial

Source: Moody’s

Note: Excludes the second-quarter 2012 bankruptcy filing of Hawker Beechcraft Acquisition Company, LLC and the second quarter distressed exchange of Dex One Corporation. Hawker defaulted through a missed payment in the first quarter of 2012 and Dex One defaulted through a distressed exchange in the first quarter of 2012 . For this quarterly Default Monitor, we include only the initial default in a calendar year. Entities that emerge from bankruptcy are considered new issuers for the purpose of this report.

Companies with the lowest Probability of Default ratings. As of 1 July there were 49 US non-financial companies with Probability of Default ratings (PDR) of Caa2 or lower, indicating that they have the highest probability of default among our rated issuers. Exhibit 4 contains the full list. For more analysis of companies with lower PDRs, please see Moody’s B3 Negative and Lower Corporate Ratings List.

EXHIBIT 4

US Corporate Issuers with Caa2 and Lower Probability of Default Ratings Data as of 1 July 2012

Company Probability of Default Rating

Corporate Family Rating Outlook

Advanstar Communications, Inc. Caa2 Caa2 NEG

AGY Holding Corp. Caa2 Caa2 NEG

ATP Oil & Gas Corporation Caa2 Caa2 DEV

BCBG Max Azria Group, Inc. Caa2 Caa2 NEG

Beazer Homes USA, Inc. Caa2 Caa2 STA

Bonten Media Group, Inc. Caa2 Caa2 STA

Chukchansi Economic Development Authority Caa2 Caa2 STA

CityCenter Holdings, LLC Caa2 Caa2 POS

Claire's Stores, Inc. Caa2 Caa2 STA

Edgen Murray II, L.P. Caa2 Caa3 STA

Edison Mission Energy Caa2 Caa2 NEG

Evergreen International Aviation, Inc. Caa2 Caa2 STA

Funding Co. (Varel) Caa2 Caa2 NEG

Geokinetics Holdings USA, Inc. Caa2 Caa2 NEG

Green Field Energy Services, Inc. Caa2 Caa2 STA

Guitar Center Holdings, Inc. Caa2 Caa2 STA

Horizon Lines, Inc. Caa2 Caa2 STA

CREDIT IN DEPTH Detailed analysis of an important topic

22 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

EXHIBIT 4

US Corporate Issuers with Caa2 and Lower Probability of Default Ratings Data as of 1 July 2012

Company Probability of Default Rating

Corporate Family Rating Outlook

Hovnanian Enterprises, Inc. Caa2 Caa2 NEG

Jacuzzi Brands Corp. Caa2 Caa2 STA

Lantheus Medical Imaging Caa2 Caa2 NEG

LBI Media, Inc. Caa2 Caa2 STA

National Air Cargo Holdings, Inc. Caa2 Caa2 STA

Orleans Homebuilders, Inc. Caa2 Caa1 STA

Quality Home Brands Holdings LLC Caa2 Caa2 NEG

Shingle Springs Tribal Gaming Authority Caa2 Caa2 NEG

Synagro Technologies, Inc. Caa2 Caa2 STA

Waterford Gaming LLC Caa2 Caa3 NEG

Western Express, Inc. Caa2 Caa2 NEG

YRC Worldwide Inc. Caa2 Caa3 STA

AGS, LLC Caa3 Caa3 NEG

AMF Bowling Worldwide, Inc. Caa3 Caa3 NEG

ATI Acquisition Company Caa3 Ca NEG

Bon-Ton Stores Inc., (The) Caa3 Caa1 NEG

Broadview Networks Holdings, Inc. Caa3 Caa2 NEG

Clear Channel Communications, Inc. Caa3 Caa2 STA

Clearwire Communications LLC Caa3 Caa2 STA

Dex One Corporation Caa3 Caa3 NEG

Energy Future Holdings Corp. Caa3 Caa2 NEG

GateHouse Media Operating, Inc. Caa3 Ca STA

GMX Resources Inc. Caa3 Caa3 NEG

Milagro Oil & Gas, Inc. Caa3 Caa3 NEG

OnCure Holdings, Inc. Caa3 Caa3 NEG

Realogy Corporation Caa3 Caa2 STA

SuperMedia Inc. Caa3 Caa3 NEG

Xinergy Corp. Caa3 Caa3 NEG

Golden Nugget, Inc. Ca Ca STA

LifeCare Holdings, Inc. Ca Caa3 NEG

Merrill Corporation Ca Caa3 RUR

WasteQuip, Inc. Ca Ca NEG

CREDIT IN DEPTH Detailed analysis of an important topic

23 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

Appendix

Moody’s Definition of Default

Our definition of default is applicable only to debt or debt-like obligations (e.g., swap agreements). Four events constitute a debt default under our definition:

a) a missed or delayed disbursement of a contractually obligated interest or principal payment (excluding missed payments cured within a contractually allowed grace period), as defined in credit agreements and indentures;

b) a bankruptcy filing or legal receivership by the debt issuer or obligor that will likely cause a miss or delay in future contractually obligated debt-service payments;

c) a distressed exchange whereby 1) an obligor offers creditors a new or restructured debt, or a new package of securities, cash or assets that amount to a diminished financial obligation relative to the original obligation and 2) the exchange has the effect of allowing the obligor to avoid a bankruptcy or payment default in the future; or

d) a change in the payment terms of a credit agreement or indenture imposed by the sovereign that results in a diminished financial obligation, such as a forced currency re-denomination (imposed by the debtor itself, or its sovereign) or a forced change in some other aspect of the original promise, such as indexation or maturity.

Our definition of default does not include so-called “technical defaults,” such as maximum leverage or minimum debt coverage violations, unless the obligor fails to cure the violation and fails to honor the resulting debt acceleration that may be required. Also excluded are payments owed on long-term debt obligations that are missed due to purely technical or administrative errors which are 1) not related to the ability or willingness to make the payments and 2) are cured in very short order (typically, one to two business days).

RECENTLY IN CREDIT OUTLOOK Select any article below to go to last Monday’s Credit Outlook on moodys.com

24 MOODY’S CREDIT OUTLOOK 2 AUGUST 2012

NEWS & ANALYSIS European Sovereign and Bank Crisis 2 » Draghi Reaffirms ECB’s Willingness to Buy Time, but ECB Cannot

Resolve Debt Crisis

Corporates 3 » VMware's Purchase of Nicera Puts Cisco and Juniper on

the Defensive » Owens & Minor's Planned Acquisition of Movianto Is

Credit Positive » Telefonica's Dividend Suspension Is Credit Positive » Koninklijke KPN's Dividend Cut Is Credit Positive but Does Not

Fully Offset Weaker Performance » Russia's JSC Acron Secures Apatite and Potash Supplies, a

Credit Positive » Fourth License in UK Spectrum Auction Is Credit Positive for

Hutchison Whampoa » In China, Low Prices and High Iron Ore Inventories Weigh on CITIC

Pacific and Fosun » Consumers' Shift Is Credit Positive for Japan's Convenience Stores

and Beverage Companies » Australia's Online Shopping Growth Is Negative for Retail REITs » Mounting European Defaults and Credit Insurance Costs Will Hurt

Asian Exporters

Banks 17 » Lower Loan Growth Is Credit Negative for Bradesco and

Itau Unibanco » Higher Reserve Requirements Are Credit Negative for

Uruguay's Banks » New Hong Kong Policy on Renminbi Banking Services Is

Credit Positive » Korean Bank Report Will Likely Spark Louder Calls for Credit-

Negative Reforms

Insurers 25 » Decision on Loan Insurance Profit Sharing Is Credit Negative for

French Banks and Insurers

Asset Managers 27 » Europe's Exchange-Traded Fund Guidelines Are Credit Negative for

Asset Managers

Sovereigns 29 » Peru's Cabinet Change Reflects Inability to Resolve Conga Mining

Conflict, a Credit Negative » Fewer Flights and Tourists Are Credit Negative for Malta » Expansion of Value-Added Tax Trial Is Credit Positive for China

Public Finance 32 » Massachusetts State Lottery Profit Is Credit Positive for

Local Governments

Structured Finance 34 » US Private Student Loan Dischargeability Is Credit Negative

for Securitizations

RATINGS & RESEARCH Rating Changes 36

Last week we downgraded Nokia Oyj, Peugeot, Nova Ljubljanska banka, Nova Kreditna banka Maribor and Abanka Vipa, Banque PSA Finance, Clientis, Convergex Holdings, Sicily, 12 CMBS notes from five Italy-exposed deals, 15 Italian structured finance transactions; and upgraded Atlantic Path, among other rating actions.

Research Highlights 48

Last week we published on US consumer durables, corporate refinancing risk in Europe, US apparel, North American solid waste, Japanese property and casualty insurance, Japanese life insurance, Russian and CIS banks, Munich Re, the Czech Republic, US local governments, US not-for-profit healthcare, US private colleges and universities, US credit card ABS and CLOs, among other research reports.

MOODYS.COM

Report: 144413

© 2012 Moody’s Investors Service, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. (MIS”) AND ITS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Any publication into Australia of this document is by MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657, which holds Australian Financial Services License no. 336969. This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001.

Notwithstanding the foregoing, credit ratings assigned on and after October 1, 2010 by Moody’s Japan K.K. (“MJKK”) are MJKK’s current opinions of the relative future credit risk of entities, credit commitments, or debt or debt-like securities. In such a case, “MIS” in the foregoing statements shall be deemed to be replaced with “MJKK”. MJKK is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO.

This credit rating is an opinion as to the creditworthiness or a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be dangerous for retail investors to make any investment decision based on this credit rating. If in doubt you should contact your financial or other professional adviser.

EDITORS PRODUCTION ASSOCIATE News & Analysis: Jay Sherman and Elisa Herr Amanda Kissoon