Embed Size (px)

Citation preview

VAT Department MaltaVAT Department Malta

New VAT FormsNew VAT Forms

For Intra-Community RegimeFor Intra-Community Regime

Applicable as fromApplicable as from

11stst May 2004 May 2004

New Forms as from May 1, 2004:•Form 001/2004 – The VAT Registration Form

•Form 002/2004 – The Recapitulative Statement

•Form 002A/2004 – Additional Sheets to the Recapitulative Statement

•Form 003/2004 – VAT Return for Persons registered under Article 10

•Form 004/2004 – VAT Payment on Intra-Community Acquisitions by Persons registered under Article 12

•Form 005/2004 – Declaration by Persons registered under Article 12

•Form 006/2004 – VAT Payment on Services taxable in Malta by taxable persons not registered under Article 10

•Form 007/2004 – VAT Payment on New Means of Transport

•Form 008/2004 – Claim for Refund by persons not established in Malta

Form 001/2004

The New VAT Registration Form

• To be used by persons who wish to register for VAT purposes under Articles 10, 11 and 12 of the VAT Act

Form 001/2004 - New VAT Registration Form – front and back

Form 002/2004

The Recapitulative Statement

This statement has to be completed by persons who are:

•Registered under Article 10

AND

•Who make exempt intra-community supplies to persons in other member states outside Malta who have a valid VAT number issued in another member state

•Statement is to be sent for every calendar quarter

Form 002A/2004

The Recapitulative Statement

Additional Sheets

•These additional sheets are to be used if information to be reported exceeds 10 customers (and therefore form 002/2004 is full)

•The number of additional sheets have to be accounted for also in the form 002/2004 for reconciliation purposes

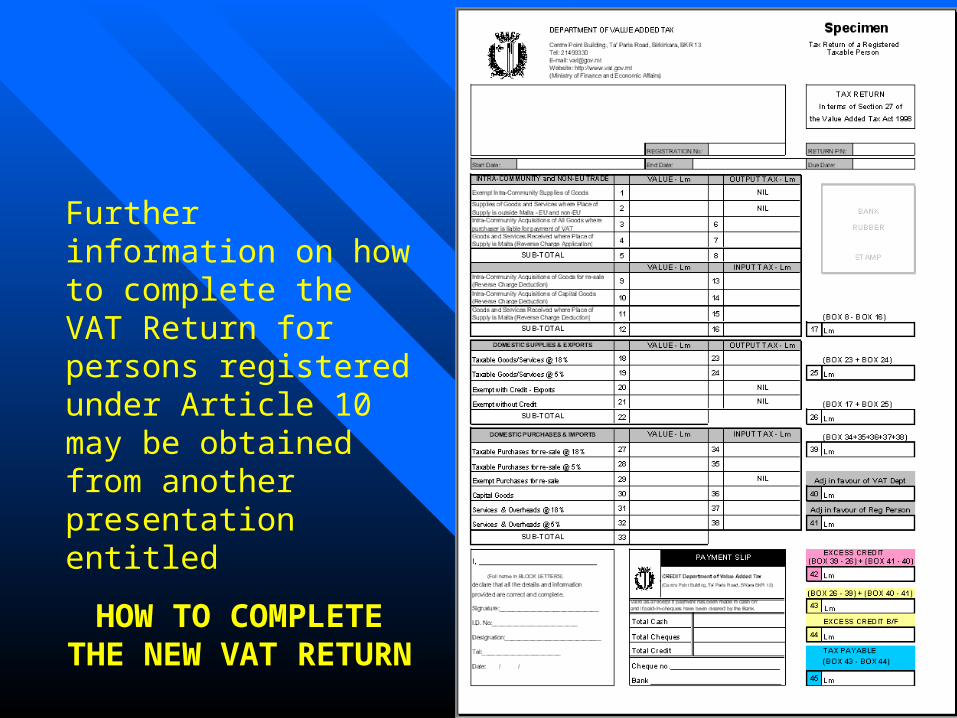

INTRA-COMMUNITY & NON-E.U. TRADE

DOMESTIC SUPPLIES & EXPORTS

DOMESTIC PURCHASES & IMPORTS

The New VAT Return for Persons registered under Article 10 has now been divided as follows:

Further information on how to complete the VAT Return for persons registered under Article 10 may be obtained from another presentation entitled

HOW TO COMPLETE THE

NEW VAT RETURN

Form 004/2004

Payment Form for VAT on Intra-Community Acquisitions

•This form shall be obtained from the department of VAT (or downloaded from internet)

•It is to be used by a person who is registered under Article 12 and who makes an intra-community acquisition on which VAT is due to be paid in Malta

•Form has to accompany payment and is to be submitted each time a consignment is received

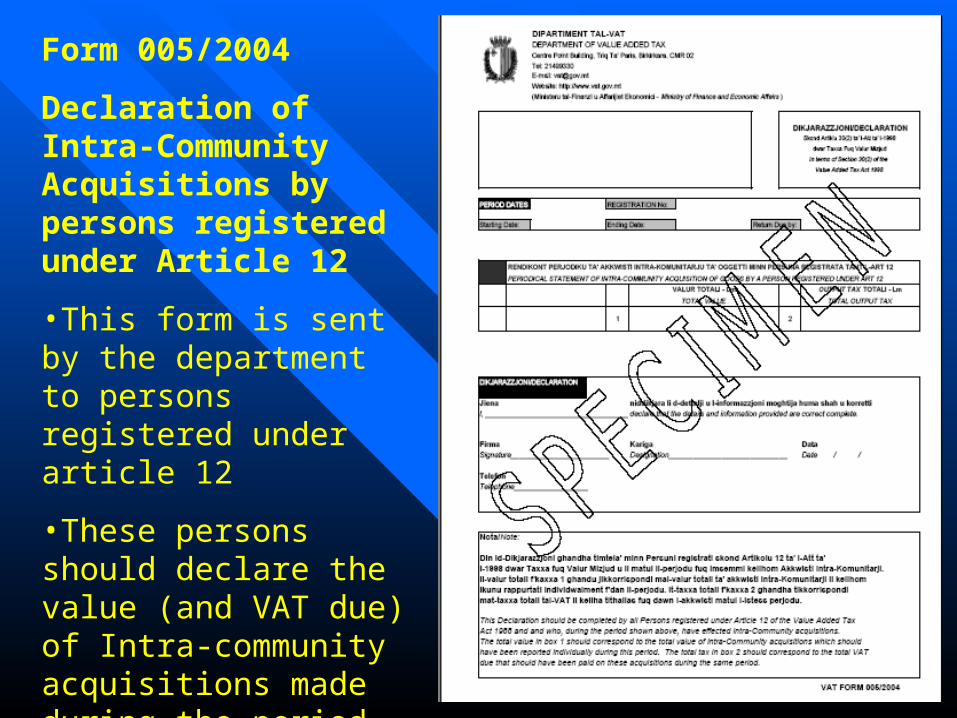

Form 005/2004

Declaration of Intra-Community Acquisitions by persons registered under Article 12

•This form is sent by the department to persons registered under article 12

•These persons should declare the value (and VAT due) of Intra-community acquisitions made during the period referred to in the statement (normally one year)

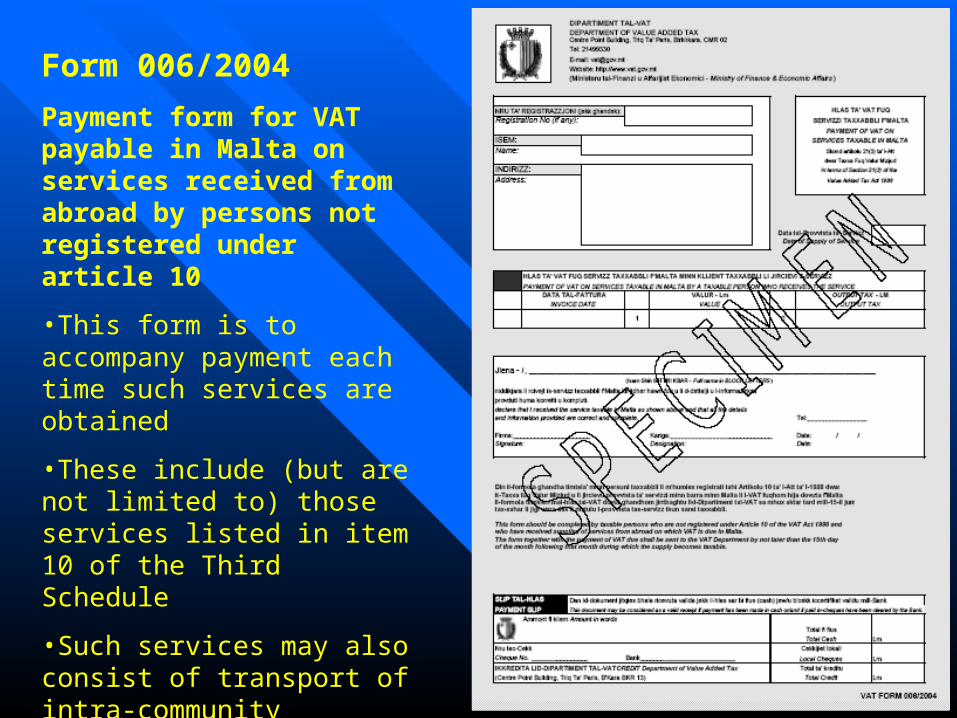

Form 006/2004

Payment form for VAT payable in Malta on services received from abroad by persons not registered under article 10

•This form is to accompany payment each time such services are obtained

•These include (but are not limited to) those services listed in item 10 of the Third Schedule

•Such services may also consist of transport of intra-community acquisitions of goods by a person registered under article 12

Form 007/2004

Payment form for VAT payable in Malta on New Means of Transport

•This form has to be completed by persons who are not registered under article 10 and who make an intra-community acquisition of a New Means of transport

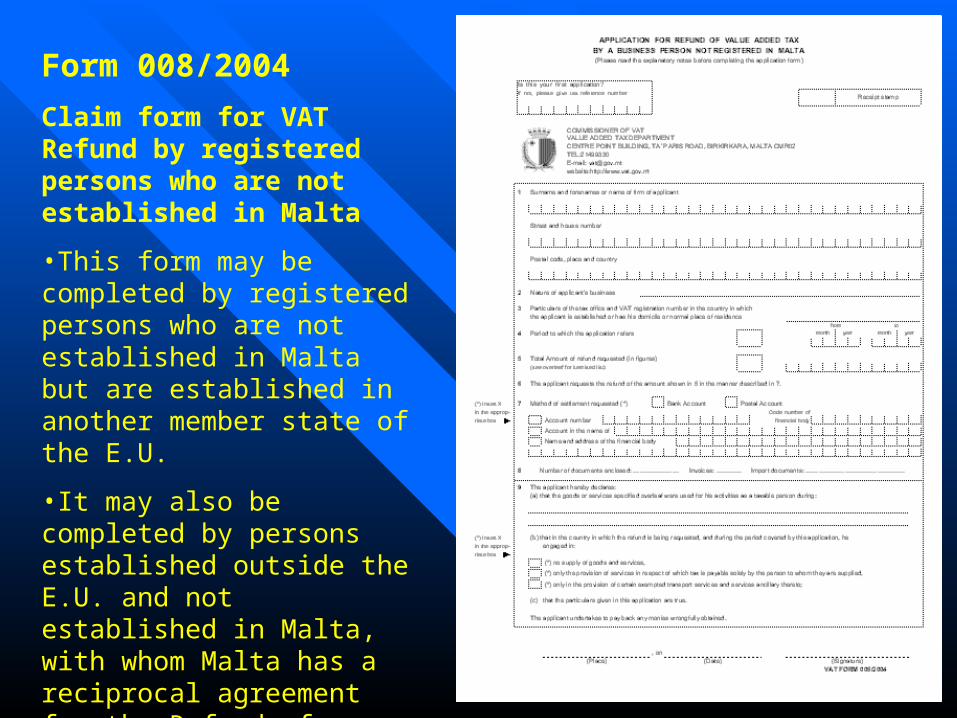

Form 008/2004

Claim form for VAT Refund by registered persons who are not established in Malta

•This form may be completed by registered persons who are not established in Malta but are established in another member state of the E.U.

•It may also be completed by persons established outside the E.U. and not established in Malta, with whom Malta has a reciprocal agreement for the Refund of Turnover Taxes.

Form 008A/2004 – Claim form for VAT Refund page 2