Embed Size (px)

DESCRIPTION

New Trends in Globalisation. Conference on Medium Term Economic Assessment Iasi, September 26 2008 Koen De Backer OECD. Pervasive globalisation. Geographical scope: developed and emerging countries Organisational scope global value chains Sector scope - PowerPoint PPT Presentation

Citation preview

NEW TRENDS IN GLOBALISATION

Conference on Medium Term Economic Assessment

Iasi, September 26 2008

Koen De Backer OECD

PERVASIVE GLOBALISATION

• Geographical scope: developed and emerging countries

• Organisational scopeglobal value chains

• Sector scopemanufacturing and services

• Functional scopeproduction/distribution and R&D/innovation

Source : OECD.

International trade and financial links have deepened

The global expansion is continuing

Cross-border lending and investment, in % of world GDP

% growth in real GDP1Non-OECD share in % of world GDP

Imports of goods and services, in % of world GDP

The importance of non-OECD economies has grown

22

24

26

28

30

99 2000 01 02 03 04 05 06

0

2

4

6

8

10

12

99 2000 01 02 03 04 05 06

China

IndiaRussia

Brazil

OECD40

41

42

43

44

45

46

47

99 2000 01 02 03 04 05 06

At purchasing power parity

At market exchange rates

6

8

10

12

14

16

99 2000 01 02 03 04 05

At market exchange rates

GLOBALISATION IS ADVANCING RAPIDLY

FAST AND DEEP GLOBALISATION

0

50

100

150

200

250

1870 1950 20000

50

100

150

200

250

Population of integrating economies as a ratio of that in advanced countries

GDP per capita gap between integrating and advanced economies

%

Entry of North America and peripheral Europe

Entry of Japan Entry of China and India

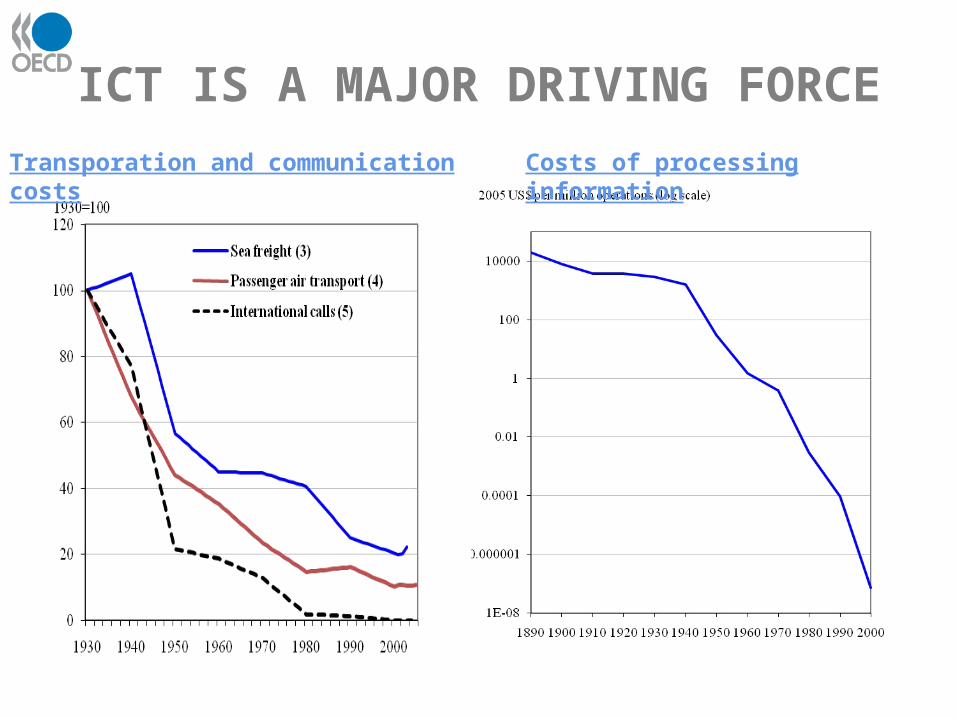

ICT IS A MAJOR DRIVING FORCE

Transporation and communication costs Costs of processing information

THE EMERGENCE OF GLOBAL VALUE CHAINS

distribution

productionR&D

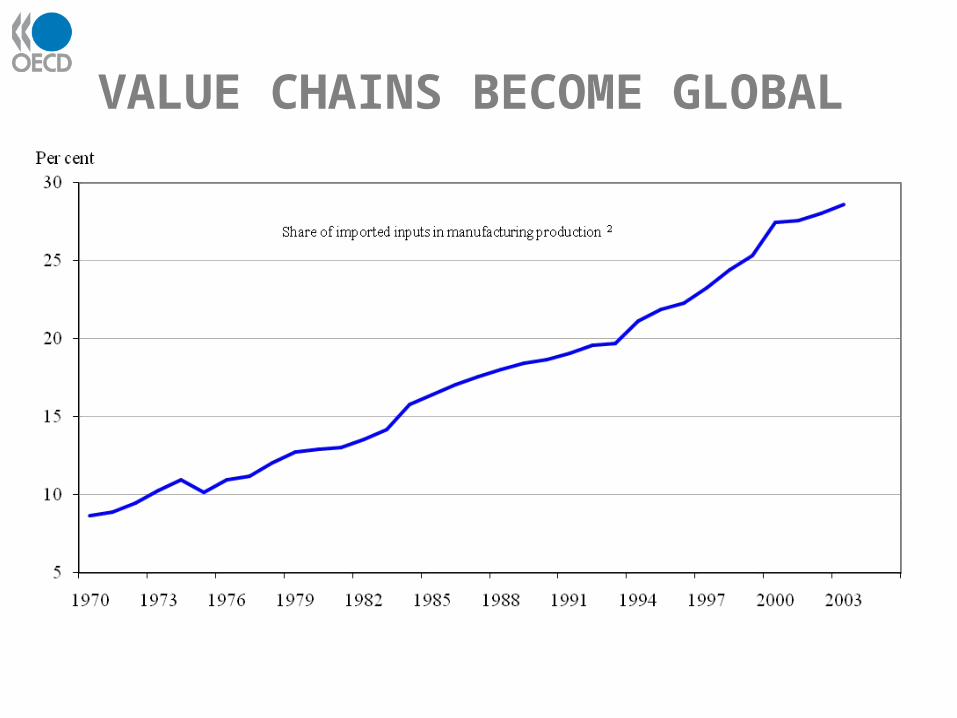

VALUE CHAINS BECOME GLOBAL

MULTINATIONAL ENTERPRISES (MNES)

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

5 500

6 000

6 500

7 000

7 500

8 000

1995 2003

Thousands

6 581

7 712

Japan

Other OECD (1)

France

United Kingdom

United States

Germany

18.3%

24.9%

16.5% 6.6%

7.5%2.1%

Italy

34.7%

10.8%

10.9%

1.5%

27.5%

11.1%

13.4%

14.3%

Employment in manufacturing industries

The story of a ‘particular’ American car:

30% to Korea: assembly 17,5% to Japan: components and advanced technology

7,5% to Germany: design4% to Taiwan and Singapore: minor parts

2,5% to UK: marketing 1,5 to Ireland and Barbados: data processing

37% in USA

Source: Grossman and Rossi-Hansberg (2006)

IN MORE TRADITIONAL MANUFACTURING INDUSTRIES (1)

Design: California,USA

Body material: Taiwan

Nylon hair: Japan

Clothing: China

Moulds, paint pigments: USA

Assembly: Indonesia and Malaysia

Quality testing: USA

Marketing: USASource: Grossman and Rossi-Hansberg (2006)

IN MORE TRADITIONAL MANUFACTURING INDUSTRIES (2)

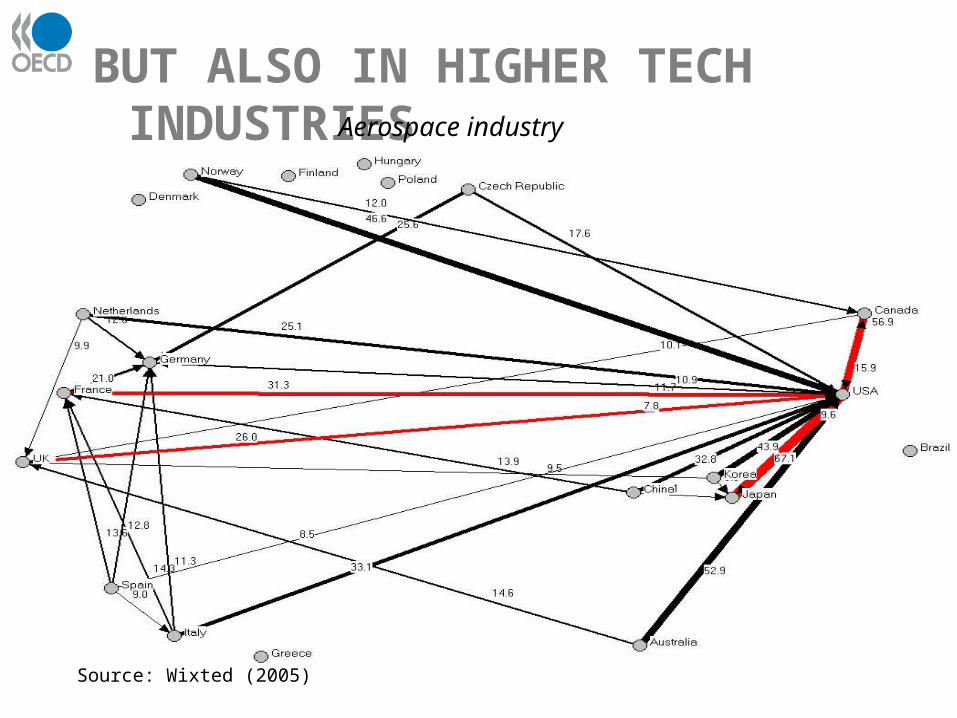

Source: Wixted (2005)

BUT ALSO IN HIGHER TECH INDUSTRIES Aerospace industry

There seems to be no clear relationship between GVCs and overall employment

USA

TUR

SWE

SVK

PRT

POL

NZL

NOR

NLD

MEX

LUXKOR

JPN

ITA

ISL

IRL

HUNGRC

GBR

FRA

FIN

ESP

DNK

DEU CZE

CHE

CAN

BEL

AUT

AUS

40

45

50

55

60

65

70

75

80

85

0 50 100 150 200 250 300

Trade openness

Em

plo

ym

en

t-p

op

ula

tio

n r

ati

o

EFFECTS OF GVCS (1)

More traditional manufacturing industries

Low skilled workers

Differences between USA and Europe:

wages vs unemeployment

Services offshoring: also higher skilled

‘Stuck in the middle?’

There are winners and losers on the labour market

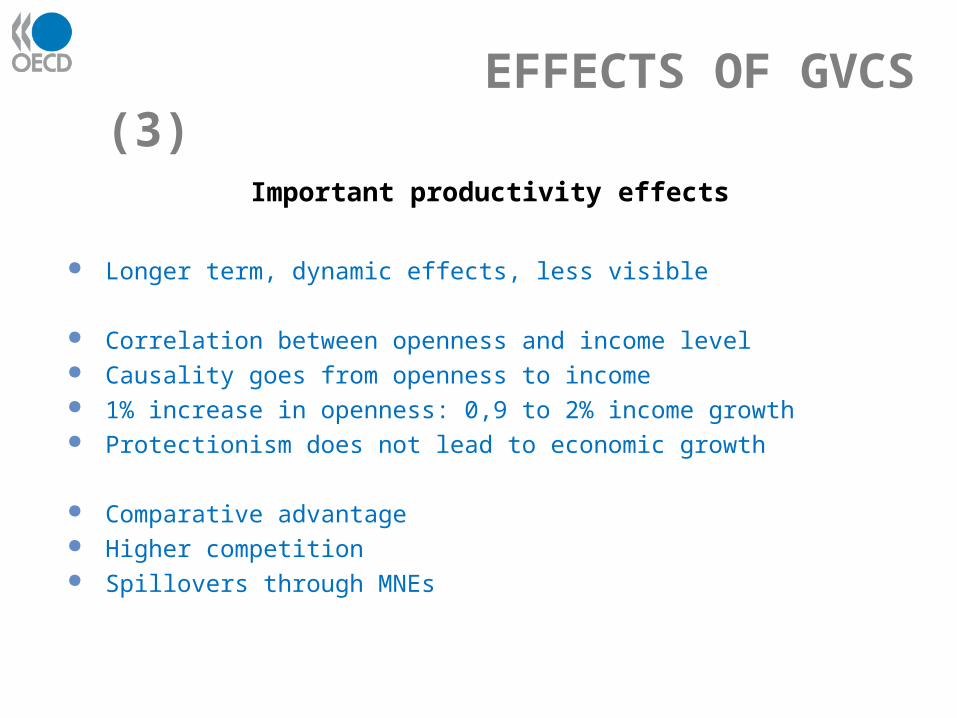

EFFECTS OF GVCS (2)

Longer term, dynamic effects, less visible

Correlation between openness and income level Causality goes from openness to income 1% increase in openness: 0,9 to 2% income growth Protectionism does not lead to economic growth

Comparative advantage Higher competition Spillovers through MNEs

Important productivity effects

EFFECTS OF GVCS (3)

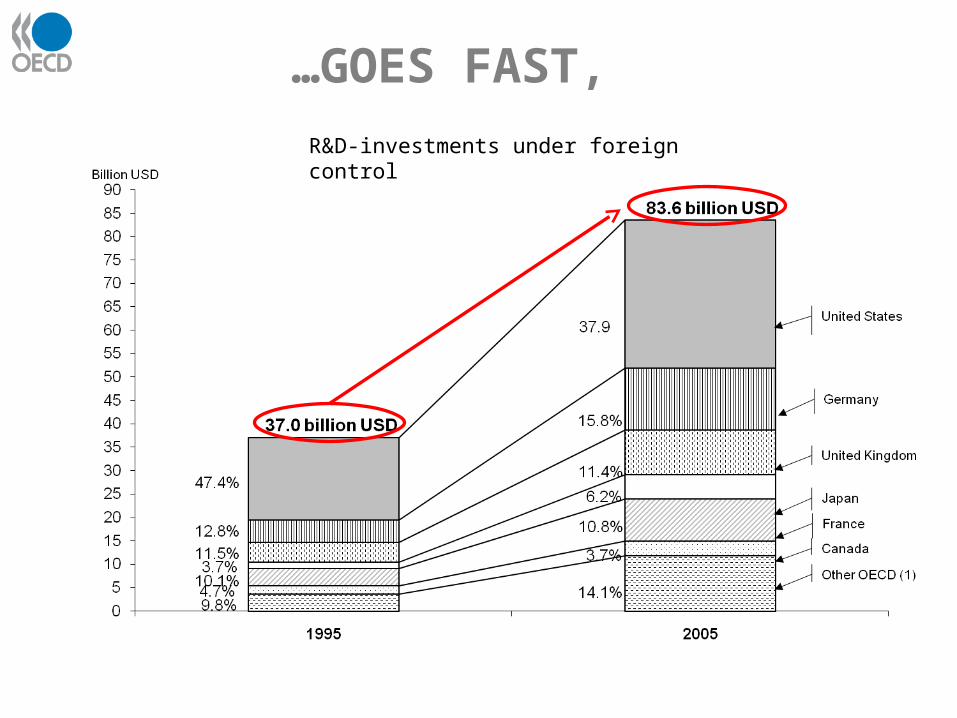

THE INTERNATIONALISATION OF R&D…

distribution

productionR&D

…GOES FAST,

R&D-investments under foreign control

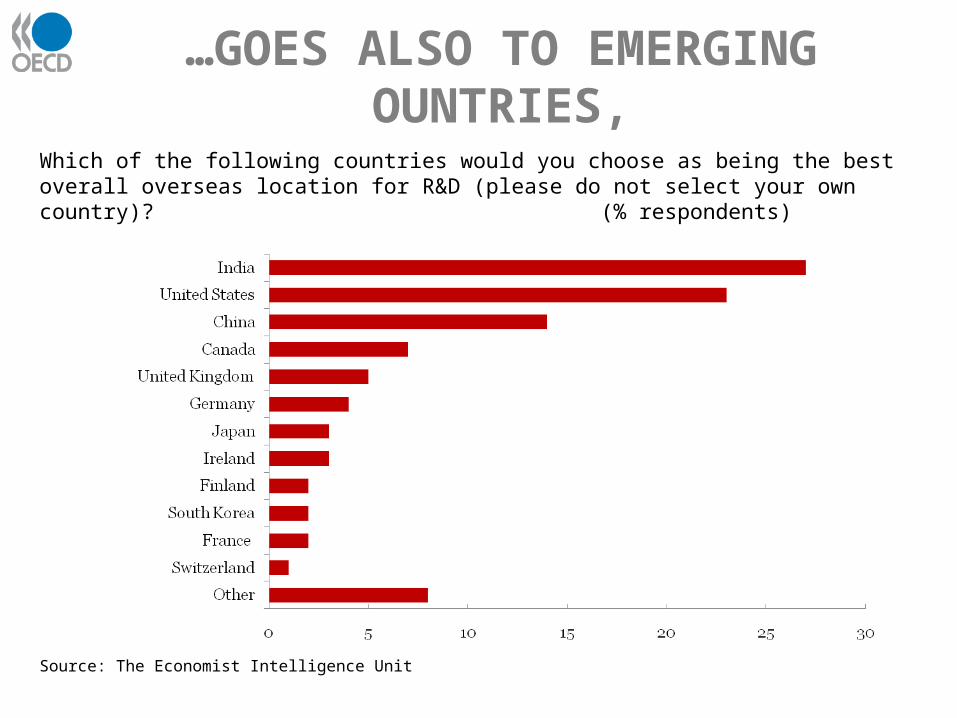

…GOES ALSO TO EMERGING OUNTRIES,

Source: The Economist Intelligence Unit

Which of the following countries would you choose as being the best overall overseas location for R&D (please do not select your own country)? (% respondents)

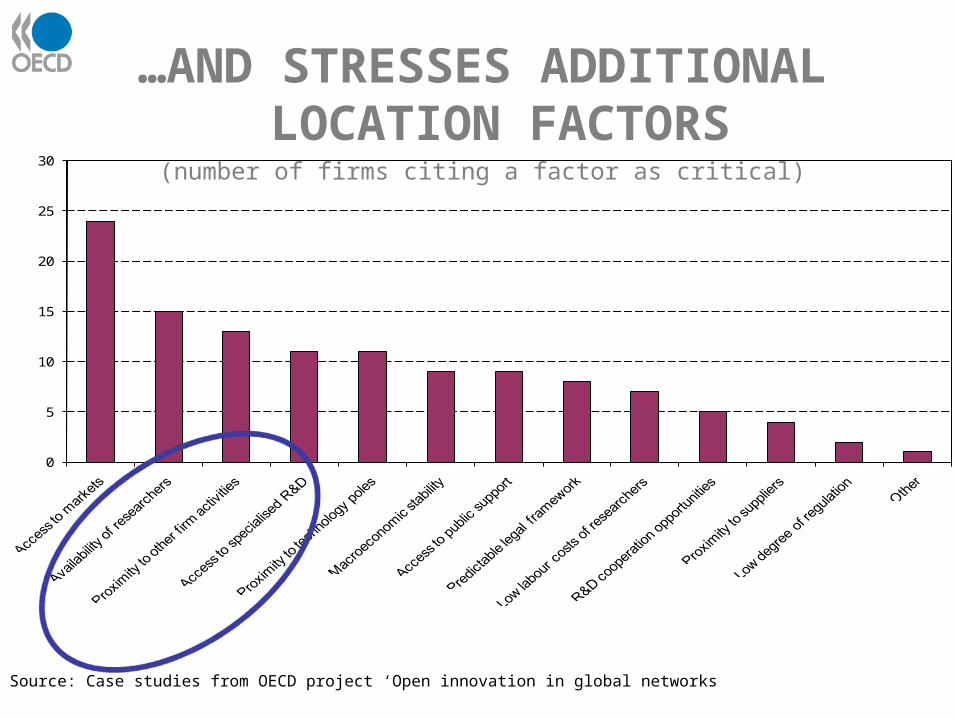

…AND STRESSES ADDITIONAL LOCATION FACTORS(number of firms citing a factor as critical)

Source: Case studies from OECD project ‘Open innovation in global networks

0

5

10

15

20

25

30

GLOBAL INNOVATION NETWORKS

distribution

productionR&D

MATCHING OF GLOBAL DEMAND …

• New customers• Increasing customer needs • Global and intense

competition• Shorter product life cycles

… AND OF GLOBAL SUPPLY OF INNOVATION

• Multidisciplinary research• Converging technologies• Increasing costs and risks of

R&D• Global S&T supply

LARGE SUPPLY OF S&T, ALSO IN EMERGING COUNTRIES

324

231

131

71

24

17

144

0

2

4

6

8

10

12

0 1 2 3 4GERD as % of GDP

Researchers per 1 000 employment (2)

R&D expendituresin billions of current PPP (1)

Japan

United States

Russian Federation

ChinaSouth Africa

BrazilIndia

EU27

CHINA STILL SPECIALIZED IN LOWER TECHNOLOGY INDUSTRIES

WRAPPING UP: NEW TRENDS IN GLOBALISATION

• Geographical scope:Truly global character and increasing importance of emerging countries

• Organisational scopeGlobal value chains, not only transfer of goods/services, but increasingly activities and capital

• Sector scope:Manufacturing industries and services industries

• Functional scope:Production/distribution but also R&D/innovation

POLICY IMPLICATIONS (1)

• Do governments still have a role to play in an increasing global world?

• Protectionism appears to risk a lot, instead open and pro-active policies seem to do the job

• Accommodating globalisation

• Moving up the value chain

Adjusting to globalisation

• Balanced perspective of cost and benefits of globalisation

• Accommodating structural change

• Spreading the benefits of globalisation

• Avoid policies that distort structural change

POLICY IMPLICATIONS (2)

Need for moving up the value chain

– Science, technology and innovation– Human resources– Entrepreneurship– Network and cluster policies– Attractiveness– IPR– Trade and investment policies

POLICY IMPLICATIONS (3)

RELEVANT OECD-WORK

• Emergence of global value chainsStaying competitive in a global economy: moving up the value

chain (2007)Staying competitive in a global economy: compendium of

studies on global value chains (2008)

• R&D- internationalisationThe internationalisation of business R&D: evidence, impacts

and implications (2008)

• Open innovationOpen innovation in global networks (2008)