Embed Size (px)

Citation preview

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Neue Energierealitäten –

Bewältigung der Grossen

Wende

Christoph Frei | Secretary General | World Energy Council

November 2016 @chwfrei

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

World population

1970-2060

0

2

4

6

8

10

12

-

2

4

6

8

10

12

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

2.0 x

1.4x

Forecast

(2015-2060)

Billi

on

s o

f P

eo

ple

Billio

ns

of P

eo

ple

Source: UN Population Forecasts to 2100

Actuals

(1970-2015)

UN Population Growth (Billions of People)

1.2x

1.6x

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

0.6

%

-0.4

%

2.7

%

-0.7

%

0.4

%

2.2

% 2.9

%

1.0

%

0.2

%

1.4

% 1.9

%

0.2

%

2.5

%

2.1

% 3.3

%

1.0

%

0.5

%

0.2

%

2.4

%

-0.4

%

1.0

% 2.2

%

3.0

%

1.0

%

6%

China India Germany Saudi Arabia Spain United StatesUnited

KingdomWorld

Average1000 GtCO2

by 2100

1970-2000 2000-2014 1970-2014

Growth in the past 45 years (1970-2015)

Climate Change Challenge

Carbon Intensity % reduction p.a. 1970-2015

(GtCO2/GDP USD)

Note: Positive % changes denote a reduction in CO2 per USD of GDP

Source: Total Economy Database, BP (2015) Statistical Review, IPCC (2015) “AR5, Synthesis Report”;

2015-2060

(GtCO2/GDP USD)

Note: Assumes global

GDP growth of 2.6%

De-carbonization for

1000 GtCO2

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

New business models:

Rural electrification

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

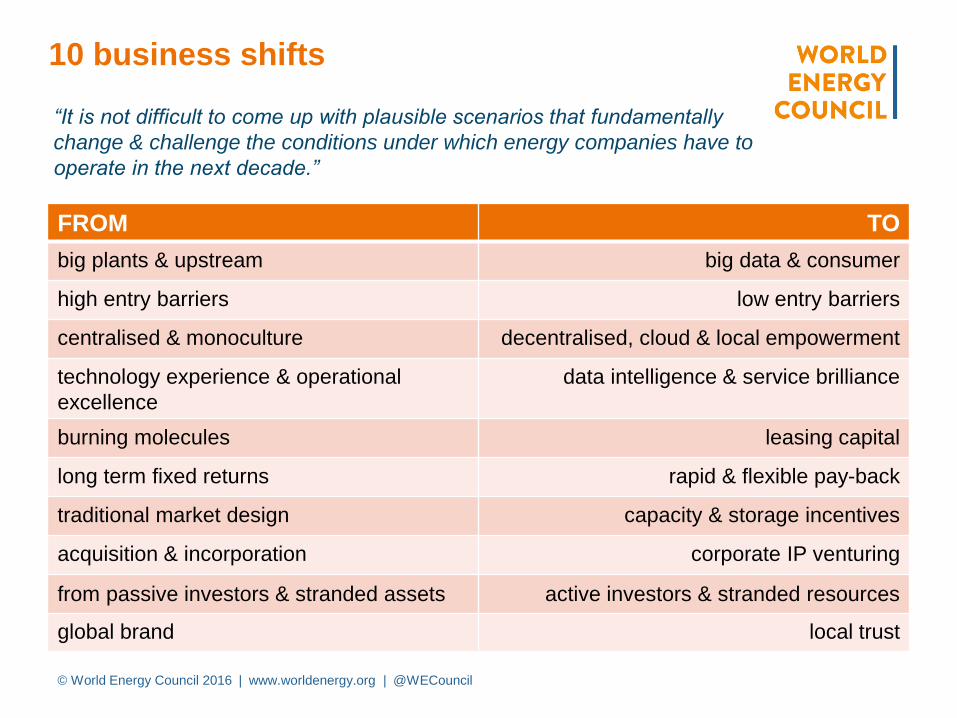

“It is not difficult to come up with plausible scenarios that fundamentally

change & challenge the conditions under which energy companies have to

operate in the next decade.”

FROM TO

big plants & upstream big data & consumer

high entry barriers low entry barriers

centralised & monoculture decentralised, cloud & local empowerment

technology experience & operational

excellence

data intelligence & service brilliance

burning molecules leasing capital

long term fixed returns rapid & flexible pay-back

traditional market design capacity & storage incentives

acquisition & incorporation corporate IP venturing

from passive investors & stranded assets active investors & stranded resources

global brand local trust

10 business shifts

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Financing Resilient Energy Infrastructure

Extreme Weather Events

Number of natural catastrophes,

1970-2014: factor 4

Insured catastrophe losses,

1970-2014

Source: WEC Financing Resilience Report, 2015 (October

1); also Swiss Re, 2015: Sigma report No 2/2015

0

20

40

60

80

100

120

140

160

180

200

1970 1975 1980 1985 1990 1995 2000 2005 2010

Natural catastrophes

Source: Swiss Re Sigma 02/2015

• Comparing the last 5 years to the last 20 years: The occurrence of extreme

events has roughly quadrupled; according to IPCC this is largely related to the

40% increase of carbon dioxide in the atmosphere.

• From impact-resistant “hard”/‘safe-fail’ components to “soft”/‘fail-safe’ systems.

• The solution appears to be ‘smarter not stronger’.

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Cyber & monoculture risks

2016

Cyber – a monoculture risk?

80’000 blacked out

hardware destroyed‘massive damage’ to

industrial equipment

critical power plant

design data stolen

Financing Resilient Energy Infrastructure

Managing Cyber Risks

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

From hard resilience to soft resilience

2015

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015© World Energy Council 2015

World Energy Issues Monitor 2017

Global map

. . . . .. . . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate frameworklarge scale accidents

economic growth

capital markets

commodity prices

electricity prices

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

China

India

Russia

EU CohesionMiddle East dynamics

US policy

trade barriers

regional integration

market design

energy subsidies

decentralised systemssustainable cities

energy efficiency

coal

ccs

renewable energies

biofuels

digitalisation

innovative transport

electric storage

nuclear

hydro

unconventionals

LNG

hydrogen economy

weak

signals need for action:

what keeps energy

leaders busy at work

critical uncertainties:

what keeps energy

leaders awake at night

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015© World Energy Council 2015

World Energy Issues Monitor 2017

Global map

. . . . .. . . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate frameworklarge scale accidents

economic growth

capital markets

commodity prices

electricity prices

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

China

India

Russia

EU CohesionMiddle East dynamics

US policy

trade barriers

regional integrationmarket design

energy subsidies

decentralised systemssustainable cities

energy efficiency

coal

ccs

renewable energies

biofuels

digitalisation

innovative transport

electric storage

nuclear

hydro

unconventionals

LNG

hydrogen economy

► Global key insomnia issues are of macro nature: new

growth normal, commodity price volatility, climate

framework uncertainty and regional integration /

cohesion.

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015© World Energy Council 2015

World Energy Issues Monitor 2017

Global map

. . . . .. . . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate frameworklarge scale accidents

economic growth

capital markets

commodity prices

electricity prices

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

China

India

Russia

EU CohesionMiddle East dynamics

US policy

trade barriers

regional integrationmarket design

energy subsidies

decentralised systemssustainable cities

energy efficiencycoal

ccs

renewable energiesbiofuels

digitalisation

innovative transport

electric storage

nuclear

hydro

unconventionals

LNG

hydrogen economy

► Global key action priorities remain constant:

renewables, energy efficiency, followed by subsidies

and electricity prices – and, talent.

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015© World Energy Council 2015

World Energy Issues Monitor 2017

. . . . .. . . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate frameworklarge scale accidents

economic growth

capital markets

commodity prices

electricity prices

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

China

India

Russia

EU CohesionMiddle East dynamics

US policy

trade barriers

regional integration

energy subsidies

sustainable cities

energy efficiency

coal

ccs

biofuels

innovative transport

nuclear

hydro

unconventionals

LNG

hydrogen economy

► The innovation cluster continues to move up: e-

storage, digitalisation, decentralised systems and

relevant market design.

market designdigitalisation

renewable energies

decentralised systems

electric storage

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015© World Energy Council 2015

World Energy Issues Monitor 2017

. . . . .. . . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate frameworklarge scale accidents

economic growth

capital markets

commodity prices

electricity prices

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

China

India

Russia

EU CohesionMiddle East dynamics

US policy

trade barriers

regional integration

market design

energy subsidies

decentralised systemssustainable cities

energy efficiency

coal

ccs

renewable energies

biofuels

digitalisation

innovative transport

electric storage

nuclear

hydro

unconventionals

LNG

hydrogen economy

Global map: key downward trends

► CCS, unconventionals, nuclear and coal are issues

which have seen the biggest cooling down over past

years.

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015© World Energy Council 2015

World Energy Issues Monitor 2017

. . . . .. . . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate frameworklarge scale accidents

economic growth

capital markets

commodity prices

electricity prices

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

China

India

Russia

EU CohesionMiddle East dynamics

US policy

trade barriers

regional integrationmarket design

energy subsidies

decentralised systemssustainable cities

energy efficiencycoal

ccs

renewable energiesbiofuels

digitalisation

innovative transport

electric storage

nuclear

hydro

unconventionals

LNG

hydrogen economy

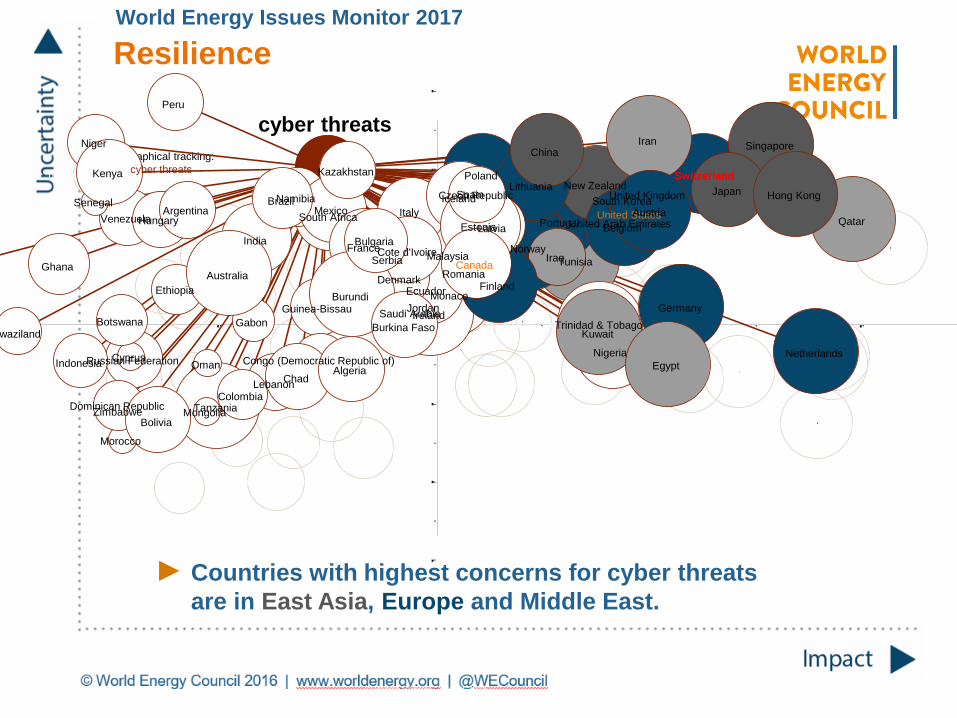

Resilience

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015© World Energy Council 2015

► Countries with highest concerns for cyber threats

are in East Asia, Europe and Middle East.

Resilience

World Energy Issues Monitor 2017

cyber threats

. . . . .. . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate frameworklarge scale accidents

economic growth

capital markets

commodity prices

electricity prices

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

China

India

Russia

EU Cohesion

Middle East dynamics

US policy

trade barriers

regional integration

market design

energy subsidies

decentralised systemssustainable cities

energy efficiency

coal

ccs

renewable energies

biofuels

digitalisationinnovative transport

electric storage

nuclear

hydro

unconventionals

LNG

hydrogen economy

geographical tracking:

Zimbabwe

Venezuela United States

United Kingdom

United Arab Emirates

Tunisia

Trinidad & Tobago

Tanzania

Switzerland

Swaziland

SpainSouth Korea

South Africa

Singapore

Serbia

Senegal

Saudi Arabia

Russian Federation

Romania

QatarPortugal

Poland

Peru

Oman

Norway

Nigeria

Niger

New Zealand

Netherlands

Namibia

Morocco

Mongolia

Monaco

Mexico

Malaysia

Lithuania

Lebanon

Latvia

Kuwait

Kenya Kazakhstan

Jordan

Japan

Italy

Ireland

Iraq

Iran

Indonesia

India

Iceland

Hungary

Hong Kong

Guinea-Bissau

Ghana

Germany

Gabon

France

FinlandEthiopia

Estonia

Egypt

Ecuador

Dominican Republic

Denmark

Czech Republic

Cyprus

Cote d'Ivoire

Congo (Democratic Republic of)

Colombia

China

Chad

Canada

Burundi

Burkina Faso

Bulgaria

Brazil

Botswana

Bolivia

Belgium

Austria

Australia

Argentina

Algeria

cyber threats

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015

Switzerlandfor StromKongress

supported by VSE

impact© World Energy Council 2015

. . . .. . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate framework

large scale accidents

economic growth

capital markets

exchange rates

energy water nexus

land use

talent

energy access

energy affordability

extreme weather risks

cyber threats

corruption

terrorism

ChinaIndia

Russia

Middle East dynamics

US policytrade barriers

regional integration

market design

sustainable cities

energy efficiencycoal

ccs

biofuels

digitalisationinnovative transport

nuclear

hydro

unconventionals

LNG

hydrogen economy

EU Cohesionenergy subsidies

commodity prices

renewable energieselectric storage

decentralised systems

► Digitalisation, market design / EU and price

uncertainties keep CH leaders most awake and this

even more so than last year.

► Renewables, e-storage & decentralised systems keep

energy leaders most busy.

electricity prices

© World Energy Council 2016 | www.worldenergy.org | @WECouncil© World Energy Council 2015© World Energy Council 2015 impact© World Energy Council 2015

. . . .. . . . . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

climate framework

large scale accidentseconomic growth

capital markets

commodity priceselectricity prices

exchange rates

land use

talent

energy access

energy affordability

cyber threats

corruption

ChinaIndia

Russia

EU Cohesion

Middle East dynamics

US policytrade barriers

regional integration

market design

energy subsidies

decentralised systems

sustainable cities

energy efficiencycoal

ccsrenewable energies

biofuels

digitalisationinnovative transport

electric storage

nuclear

hydro

unconventionals

LNG

hydrogen economy

► On the new risks / resilience front, cyber clearly

dominates the agenda and this even more clearly so

than last year.

Switzerlandfor StromKongress

supported by VSE

terrorism

energy water nexus

extreme weather risks

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Three Scenarios

Modern Jazz

Market-driven approach to achieving individual access and affordability of energy through economic growth

Market mechanisms

Technology innovation

Energy access for all

Unfinished Symphony

Government-driven approach to achieving sustainability through internationally coordinated politics and practices

Strong policy

Long-term planning

Unified climate action

Hard Rock

Fragmented approach driven by desire for energy security in a world with low global cooperation

Fragmented policies

Local content

Best-fit local solutions

23

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

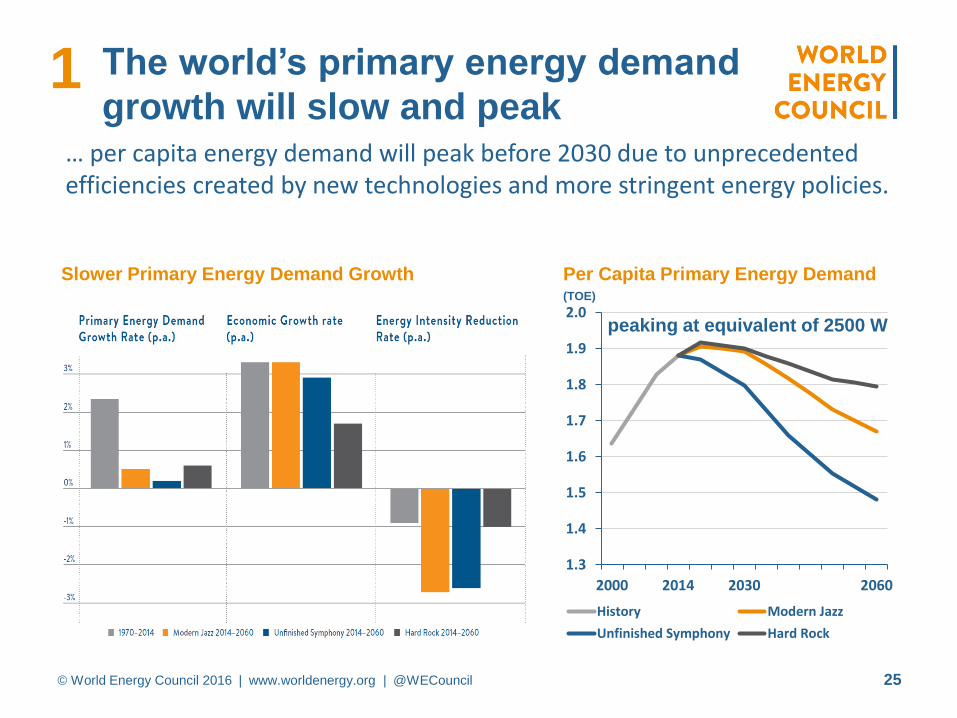

The world’s primary energy demand

growth will slow and peak… per capita energy demand will peak before 2030 due to unprecedented efficiencies created by new technologies and more stringent energy policies.

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2000 2014 2030 2060

History Modern Jazz

Unfinished Symphony Hard Rock

Per Capita Primary Energy Demand(TOE)

1

Slower Primary Energy Demand Growth

25

peaking at equivalent of 2500 W

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Demand for electricity will double

… by 2060. Meeting this demand with cleaner energy sources will require substantial infrastructure investments and systems integration to deliver benefits to all consumers.

Electricity Generation(TWh)

2

26

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

The phenomenal rise of solar and

wind energy will continue… at an unprecedented rate and create both new opportunities and challenges for energy systems.

0.2

5.7

7.9

3.3

2014

Modern Jazz2060

UnfinishedSymphony

2060

Hard Rock2060

0.7

8.8

9.3

5.6

Solar Electricity Generation(‘000 TWh)

3

Wind Electricity Generation(‘000 TWh)

27

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Demand peaks for coal and oil

… have the potential to take the world from “Stranded Assets” to “Stranded Resources”.

0

1

2

3

4

5

6

2000 2014 2030 2060

50

60

70

80

90

100

110

2000 2014 2030 2060

0

1

2

3

4

5

6

2000 2014 2030 2060

Coal Demand(‘000 MTOE)

Oil Demand(mb/d)

Natural Gas Demand(‘000 MTOE)

4

History Modern Jazz Unfinished Symphony Hard Rock

28

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

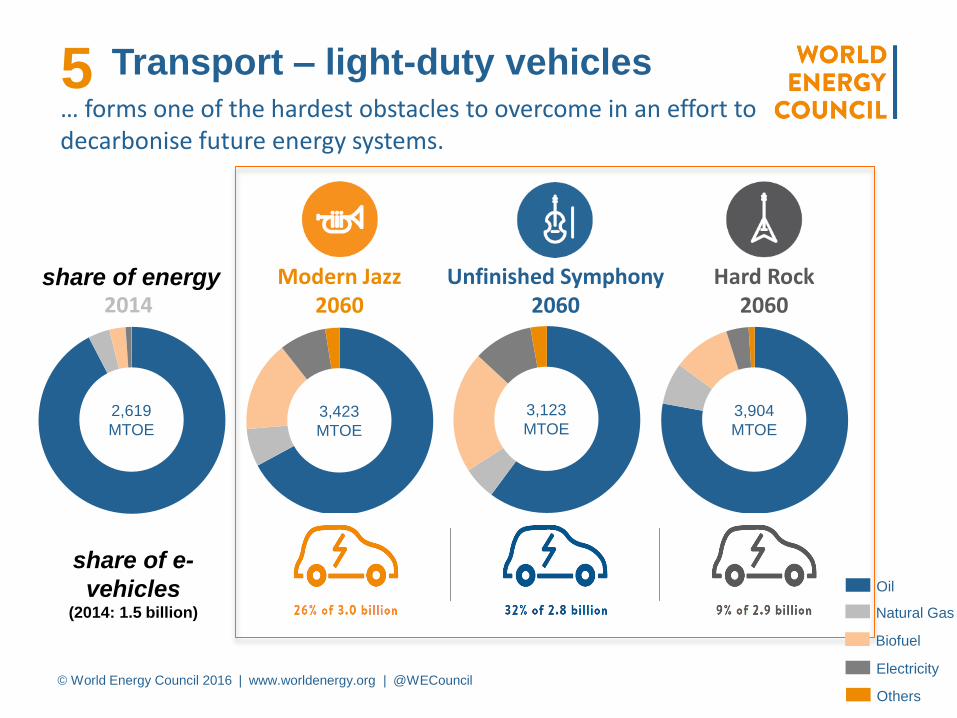

share of energy

2014

2,619

MTOE

2060

Modern Jazz

3,423

MTOE

2060

Unfinished Symphony

3,123

MTOE

2060

Hard Rock

3,904

MTOE

Unfinished Symphony 2060

Hard Rock2060

Modern Jazz20602014

share of e-

vehicles(2014: 1.5 billion)

Others

Electricity

Natural Gas

Oil

Biofuel

… forms one of the hardest obstacles to overcome in an effort to decarbonise future energy systems.

5 Transport – light-duty vehicles

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Limiting global warming

… to no more than a 2°C increase will require an exceptional and enduring effort, far beyond already pledged commitments and with very high carbon prices.

0

5

10

15

20

25

30

35

40

2000 2014 2030 2060

History

Modern Jazz

Unfinished Symphony

Hard Rock

IPCC 2°C Target

Annual Carbon Emissions (Gt CO2)

6

Cumulative Carbon Emissions 2015-2060(Gt CO2)

0

200

400

600

800

1'000

1'200

1'400

1'600

1'800

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

Modern Jazz

Unfinished Symphony

Hard Rock

Carbon

Budget

year of reaching

& exceeding

carbon budget

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

Energy Security

The effective management of primary energy supply

from domestic and external sources, the reliability

of energy infrastructure, and the ability of energy

providers to meet current and future demand.

Environmental Sustainability

Encompasses the achievement of supply

and demand side energy efficiencies and the

development of energy supply from renewable

and other low-carbon sources.

Energy Equity

Accessibility and affordability of energy supply

across the population.

Balancing the

‘Energy Trilemma’

World Energy Trilemma

© World Energy Council 2015

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

World Energy Scenarios 2060 UK

7 ENERGY TRILEMMA IN 2060

© World Energy Council 2016 | www.worldenergy.org | @WECouncil

World Energy Trilemma 2016 UK

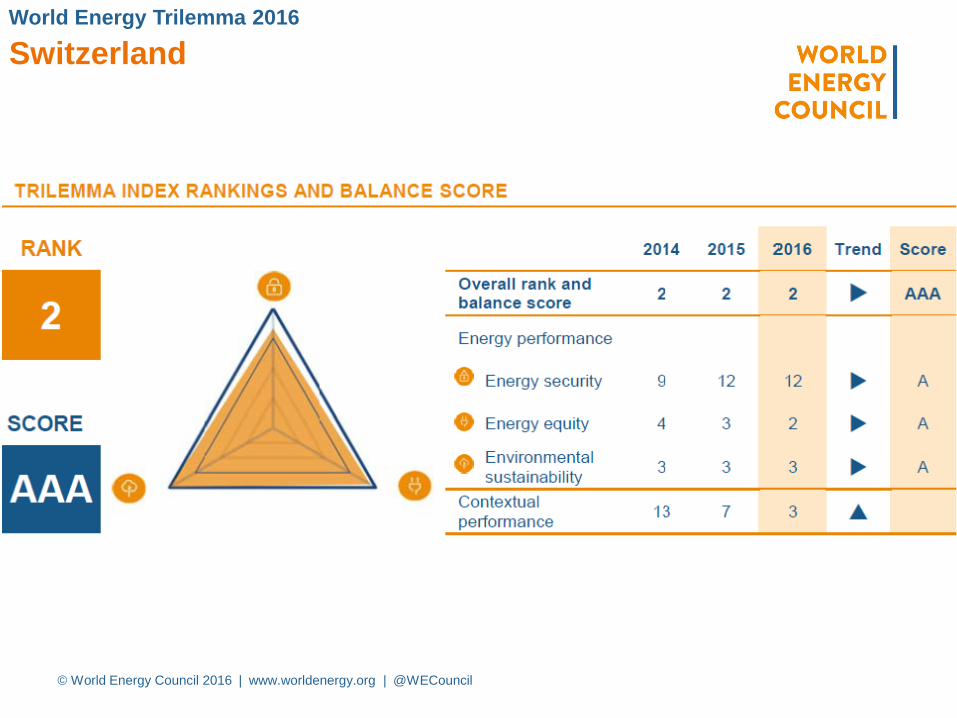

Switzerland