Embed Size (px)

Citation preview

IJI~(tC A- - 1'1- I 1 3/' t

NEPAL: PRIVATIZATION OF STATE-OWNED ENTERPRISES Recommended Assistance Plan

Final Report

u.s. Agency for International Development

Prepared for:

Prepared by:

Sponsored by:

December 1996

Coopers &Lybrand

USAID Nepal

Bruce Carrie, Coopers & Lybrand, L.L.P. James Ryan, Cargill Technical Services, Inc. Kieran Crowley, Cargill Technical Services, Inc.

Private Enterprise Development Support Project ill Contract No. PCE-0026-Q-OO-3031-00 Delivery Order No. 62 Prime Contractor: Coopers & Lybrand, L.L.P.

TABLE OF CONTENTS

LIST OF ABBREVIATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 1

I EXEC~S~Y ................................. 2

II INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 3

ill BACKGROUND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 4

IV THE CURRENT PRIVATIZATION PROCESS ................... , 5

V REVIEW OF ENTERPRISES ..... . . . . . . . . . . . . . . . . . . . . . . . . .. 8

VI ASSISTANCE REQUIRED . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 9

vn OTIIER DONORS ...................................... 10

Vill RECOMMENDED PLAN .................................. 13

XI INDICATIVE BUDGETS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

X CONCLUSION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

ANNEXES

Annex I Annex IT Annex III Annex IV Annex V Annex VI Annex vn Annex vm Annex IX Annex X

Institutions and Individual Interviewed Documents Collected and Reviewed Enterprises Covered by the Privatization Program Enterprise Reviews Enterprise Financial and Performance Figures The Dairy Sector aDA Draft Project Memorandum Indicative Budget Proposed Privatization Schedule Monitoring Questionnaire

ABC ADB ADBN BMSS ALI APROCS BJM BSM DANIDA DDC HMG HMSS HPP HTI IRIS JCF KMSS LMSS LSM MOA MPA MPCS MSS NGO NDDB NTDC ODA PMSS STC USAID UNDP

LIST OF ABBREVIATIONS

Agro Enterprise Centre Asian Development Bank Agricultural Development Bank of Nepal Biratnagar Milk Supply Scheme Agricultural Lime Industry Agricultural Project Services Biratnagar Jute Mill Birganj Sugar Factory Ltd. Danish International Development Assistance Dairy Development Corporation His Majesty's Government of Nepal Hetauda Milk Supply Scheme Herbs Production & Processing Co. Ltd. Hetauda Textile Industry Institutional Reform and the Informal Sector Janakpur Cigarette Factory Kathmandu Milk Supply Scheme Lumbini Milk Supply Scheme Lumbini Sugar Mills Ministry of Agriculture Milk Producers Association Milk Producers Cooperative Society Milk Supply Scheme Non-Governmental Organization National Dairy Development Board Nepal Tea Development Corporation Overseas Development Administration Pokhara Milk Supply Scheme Salt Trading Corporation Ltd. United States Agency for International Development United Nations Development Program

UNITS

Nepalese Rupee (Rs) = 100 paisa Rate of ExchJnge (September 1996) U.S.$1 = Rs56 Quintal = 100,000 grams "MT"ton and "Ton" refer to a metric ton = 1,000 kg

1

I EXECUTIVE SUMMARY

USAID was and still is the lead donor in promoting privatization in Nepal. When a communist government came to power in early 1995 and progress on privatization slowed, USAID suspended the majority of their assistance to the privatization program. The new center-right coalition government, which came to power at the end of 1995, has made commitment to privatization and has requested USAID's assistance with this effort. USAID has approximately $1.65 million available (consisting of local currency, and new and existing U.S. dollar funds) with which to provide support. A study team from Coopers & Lybrand L.L.P. and Cargill Technical Services, Inc. visited Nepal during September and October 1996 to review Nepal's privatization program, make an assessment of agribusinesses that could be included in the program, and prepare a recommended assistance plan for USAID.

Twelve enterprises have been privatized under Nepal's privatization program to date. The legal and institutional framework under which these enterprises were privatized functions reasonably satisfactorily, although some aspects could be improved. However, the system has yet to be tested on any large or politically sensitive enterprises; the 12 enterprises privatized so far represent only an estimated three percent of the government's investment in state-owned enterprises.

The study team identified fifteen agribusiness enterprises as being suitable for inclusion in the privatization program. These range from small enterprises in which the government owns only a minority interest and which could be sold easily, to the Dairy Development Corporation, which is wholly owned, large, and politically sensitive. The Privatization Cell, which manages HMG's privatization program, will need a range of assistance to implement the program. This will include the provision of foreign and local consultants as well as other assistance such as training, developing a public education program, and dealing with the redundancies created by the privatization of enterprises under the program.

The Overseas Development Administration (ODA) is the only other donor currently planning to assist directly Nepal's privatization program. The ODA's plans are very similar to those proposed in this report for USAID' s new U. S. dollar funds. The two agencies and the Nepalese government will need to reach agreement on the integration of the two assistance programs to ensure that aid resources are put to their best use.

The recommended assistance plan has three separate components corresponding to the three sources of funds available. The new U.S. dollar funds should be used to cover the cost of a resident advisor for a period of 18 months, as well as a limited amount of short term technical advice. The local currency funds should be used to meet the costs of all local consultants employed in the privatization of the agribusiness enterprises included in the program. In addition, the funds should be used to develop and implement a public awareness program, train the Privatization Cell staff and other senior officials, meet some of the redundancy and retraining costs associated with the privatization of agribusinesses, and provide general support to the

2

Privatization Cell. Quarterly budgets for the use of the local currency funds should be prepared by the long term advisor and approved by the Privatization Committee.

The pipeline funds, as required by the terms of their commitment, should be used for the support of private dairy enterprises. Based on USAID's experience with local contractors, the Agro Enterprise Centre should first be asked to develop projects for the use of these funds. If the Centre does not come up with suitable proposals within a specified time, a general request for proposals should be issued.

Although His Majesty's Government of Nepal (HMG) has made important steps towards implementing a privatization program over the last five years, political and economic constraints may mean that there will be significant delays in implementing the privatization program recommended in this report. Should such delays occur, particularly with the privatization of the dairy sector, USAID should review its assistance for privatization in Nepal.

II INTRODUCTION

USAID was and still is the lead donor in promoting privatization in Nepal. Technical assistance, including the provision of a long term advisor, was furnished to the Privatization Cell, the body within the Ministry of Finance charged with implementing HMG's privatization program. With the change to a communist government in early 1995, this long term assistance effort was suspended. Currently, USAID is only providing modest amounts of assistance to the Privatization Cell through the Global Bureau's IRIS project and through the mission's Development Training Project.

With the formation of a new government at the end of 1995, the situation changed again. The new coalition government has stated its commitment to moving forward with privatization of state-owned enterprises. As part of this effort, the government requested the support of USAID. Although privatization is no longer a focus of the USAID's work in Nepal, the mission has agreed to provide assistance to the Privatization Cell for a period of 12-18 months.

The mission has approximately US$700,000 of newly appropriated funds available for use on privatization and approximately $250,000 of pipeline funds earmarked for encouraging private investment in the dairy subsector. In addition, the mission has reached agreement with the Government of Nepal to use Rs39.24 million (approximately U.S. $700,(00) of local currency from the mission's PIA80, Section 416(B) Program to support the privatization of agribusiness parastatals. (Note, the situation with regard to the amounts available and uses of the funds have changed since the scope of work for this delivery order was written.)

In September 1996, USAID contracted Coopers & Lybrand L.L.P., with Cargill Technical Services, Inc. (CTS) as a subcontractor, to prepare a plan for providing technical assistance in Nepal for the privatization of agricultural enterprises. The contract requires the proposed plan

3

to cover a period of 12-18 months and utilize the funds identified above. In addition, the scope of work for the contract requires:

• a review of the privatization analyses already conducted by the Privatization Cell; • meetings with key players involved in privatization to determine priorities; • a review of the legislative and regulatory framework for privatization of agricultural

enterprises to determine if major legislative or administrative changes are required; • meetings with the management/staff of those agricultural enterprises assessed to be most

easily privatized to determine which are most appropriate to be privatized first, an assessment of alternative mechanisms, and the identification of the type and level of assistance required;

• a detailed assessment of the dairy sub sector; • a review and assessment of local consulting capacity and the methods by which the

Ministry of Finance identifies and selects local contract assistance.

A team, consisting of Bruce Carrie of Coopers & Lybrand, and Jim Ryan and Kieran Crowley of CTS, visited Nepal variously from 9 September to 17 October 1996 to undertake the work. This report is the outcome of that visit. A list of the institutions and individuals interviewed is contained in Annex I, and a list of the documents collected and reviewed is contained in Annex II.

m BACKGROUND

By the early 1990s, the Nepalese government had acquired an extensive portfolio of state-owned enterprises. HMG fully owned 63 enterprises, held a controlling interest in a further 15, and had a minority share holding in an additional 17 enterprises. The majority of these enterprises performed poorly and failed to earn profits.

The government first announced its intention to initiate a program of privatization in the Seventh Plan (1985-90). However, it was not unti11991 that a firm commitment was made by the newly elected government and plans laid out in a white paper and in the 1991192 budget. A high level Privatization Committee chaired by the Minister of Finance was established, and in this first phase of privatization, three enterprises were sold. All three enterprises were privatized by way of asset sales and without the benefit of a specific privatization law. Assistance for the program was provided by the UNDP under the management of the World Bank.

The second phase of privatization was carried out utilizing the provisions of the Privatization Bill, which was drafted during the second phase but not fully enacted by Parliament. During this phase, a further seven enterprises were privatized. Five of the enterprises were privatized through share sales, and two were liquidated. Assistance for this phase of the privatization program was provided by US AID .

4

The third phase of the privatization program, which is still under way, has been conducted under the provisions of the Privatization Act, which was given royal assent on 3 January 1994. To date, two enterprises have been privatized, negotiations with potential buyers are under way with another two, valuations have been completed on a further two enterprises, and a pre-privatization study is being conducted on another enterprise. Assistance is being provided by USAID through the IRIS program. A list of all the enterprises covered by the privatization program to date is provided in Annex m.

The third phase of the privatization program came to a virtual halt during the nine month rule of the United Marxist-Leninist Party. USAID's long term technical assistance to the program was terminated during this period. With the formation of the new coalition government in November 1995, the privatization program was revived but has been hampered by the lack of a Minister of Finance, who chairs the Privatization Committee, and limited donor assistance.

IV THE CURRENT PRIVATIZATION PROCESS

The current privatization program in Nepal is conducted under the Privatization Act, 1994. This law provides for a Privatization Committee to recommend programs and priorities for privatization to HMG. The committee is required to evaluate enterprises and recommend to HMG "on the process of privatization." The committee also must evaluate proposals received from the private sector relating to the privatization of enterprises. The basis for the evaluation is specified in the Act. In addition, the committee can conduct studies or research in order to formulate privatization programs and is entrusted with removing hindrances faced by the privatization program. The committee is chaired by the Minister of Finance and has nine other members, mainly politicians and government officials. The President of the Federation of the Nepalese Chambers of Commerce and Industry is the only private sector member of the committee. The committee does have the power to invite outside persons, including foreign consultants, to its meetings.

The Act allows for a range of methods for the privatization of enterprises, as well for their liquidation. The Act also provides for, on the recommendation of the committee, the retirement and compensation of employees that can not continue to be employed as a consequence of the privatization process. The Act also requires that the present employees of a privatized enterprise be offered shares in the enterprise free of cost or at a discount. Various other provisions are included in the Act covering administrative matters such as the procedures for the meetings of the committee, the formation of sub-committees, and the issuance of orders and directives.

The Privatization Cell has adopted a number of standard procedures and documents, within the parameters of the Privatization Act, for carrying out the privatization process. These include: having a standard format for offering memoranda; and using a standard program and timetable for the offering of an enterprise, receipt of bids, and negotiation and signing of a sales contract. A standard sales contract also is used as the basis for negotiations with potential purchasers. Regulations to facilitate privatization and govern procedures under the Privatization Act currently

5

are being prepared by the Privatization Cell with the assistance of the USAID-funded IRIS project.

a. Comment

The Privatization Act is a relatively short and straight forward act, providing a considerable degree of latitude for most of the commercial decisions that must be made as part of the privatization process. Some of the matters that are prescribed in the Act, however, potentially could cause problems. As noted above, the Privatization Committee consists of ten members, only one of whom is from the private sector. Such a large committee has the potential to cause delays with decision making. Further, as the committee makes recommendations mainly on commercial matters, such as the valuation of enterprises and their method of sale, it would be desirable to have greater representation from the private sector, rather than having such representation at the discretion of the committee.

The provision relating to the evaluation of bids is also of concern. Although the flrst item specifled for consideration in evaluating bids is the price, the second and third items relate to "management of the enterprise without changing its nature," and "retention of services of present workers and employees." As a major aim of privatization is to change the way in which enterprises are managed and operated, both these provisions could lead to negating some of the beneflts of privatization.

Evidence to date suggests that neither of the issues noted above have caused any problems with the privatization process. In fact, as the current government is a coalition, the extensive political representation on the Privatization Committee may be beneflcial in helping to resolve the differences generated by a highly political program such as privatization.

A more general criticism of the privatization program made by a number of observers is that the process is not well understood by the public, the employees of enterprises being privatized, and even by some key decision makers in the government. The process of offering enterprises for sale, receiving and evaluating bids, and negotiating and concluding a contract appears to be conducted on a fair and open basis. However, the reasons the government selects particular enterprises for privatization, chooses a privatization method, and determines other parameters of the program are not well understood by the public. More importantly, the employees of enterprises being privatized, who potentially may lose their jobs, appear not to understand the privatization process, nor their rights or place in the process. This has lead to significant problems with the labor force with a number of the privatizations undertaken to date. Some efforts have been made to educate the public, employees, and decisions makers about the privatization process, but clearly not enough has been done and a greater effort in those area is required.

Some improvements could be made to the standard procedures and documents used by the Privatization Cell. The standard contract appears to be vague with regard to the continued employment of workers, and no provisions are included to adjust the sales price or place controls

6

on the enterprise for the period between the signing of the sales contract and the hand over of the business to the new owner. Similarly, there are no provisions to cover a failure by HMG to disclose all liabilities. With the poor quality of financial reporting practiced by many stateowned enterprises, this has caused, and is likely to continue to cause, significant problems. The cashing out of gratuity liabilities for redundant workers is another issue that warrants further study to ensure that the policy is not creating perverse incentives.

On the positive side, the fact that the Privatization Act explicitly recognizes the need for liquidating some enterprises, laying off employees, and dealing with outstanding debts has proved beneficial. All these provisions have been used in the 12 privatizations undertaken so far: two enterprises have been liquidated, the work force at a number of enterprises have been rationalized prior to sale, and the government has taken over some or all of the debts of other enterprises. Flexibility and a willingness to take what may be politically unpopular commercial decisions is necessary if a privatization program is to make real progress.

h. Conclusion

Overall, the mechanical aspects of the privatization process have worked reasonably well in Nepal. Some aspects of the process could be improved, but no major changes appear to be necessary. However, the 12 enterprises that have been privatized under the program so far have all been relatively small, representing in aggregate approximately three percent of the HMG's total investments in state-owned enterprises. None of the larger or more politically sensitive enterprises have been dealt with yet. The ability and willingness of the government to deal with these more difficult enterprises has yet to be demonstrated.

c. Current Enterprises

Throughout the five year history of privatization in Nepal, various lists of enterprises for privatization have been approved by the government. The list of enterprises currently approved by the Privatization Committee for privatization, although not yet approved by HMG, are:

1. Bhaktapur Brick Factory Ltd. 2. Herbs Production and Processing Co. Ltd. 3. Janakpur Cigarette Factory Ltd. 4. Nepal Rosin and Turpentine Ltd. 5. Rimal Cement Company Ltd. 6. Morang Sugar Mills Ltd. 7. Biratnagar Jute Mills Ltd. 8. Pokhara Milk Supply Scheme 9. Industrial District Management Ltd.

10. Nepal Transport Corporation (Trolley Bus Service only) 11. Royal Nepal Airlines Corporation 12. Gorkhapatra Corporation 13. Nepal Bank Ltd.

7

14. Rastriya Banijaya Bank 15. Nepal Industrial Development Corporation 16. Nepal Housing Development Finance Co.

It should be noted that the list includes only six of the 15 enterprises that are proposed to be privatized under the USAID assistance program recommended below. The Privatization Cell has undertaken to have the additional enterprises approved by the Privatization Committee in the near future. As a matter of practical policy, the Privatization Cell does not ask the government to approve enterprises for privatization until the majority of the valuation and other preparatory work has been completed and the Privatization Cell has reasonably detailed information to provide to the government.

V REVIEW OF ENTERPRISES

Twenty one agribusiness enterprises, identified by USAID as potential privatization candidates, were reviewed by the study team. Of the enterprises reviewed, 15 were assessed to be suitable candidates for inclusion in the proposed assistance program. (The Dairy Development Corporation is counted as two enterprises for privatization purposes as the Privatization Committee has already made the decision that the corporation should be split into two for privatization.) Three enterprises are in sectors which do not operate on a competitive basis, and so are not suitable candidates for privatization at this stage. Two enterprises are more closely related to the fmancial sector; they should be privatized as part of that sector. Of the two remaining enterprises, one is in the last stages of being privatized, and the existence of the other could not be verified. This classification of enterprises is only preliminary and should be reviewed by the long term advisor as part of developing the work program, as described below. The fifteen enterprises identified as being suitable for inclusion in the proposed assistance program are:

1. Agricultural Lime Industry 2. Agricultural Project Services Centre 3. Biratnagar Jute Mill 4. Birganj Sugar Factory Ltd. 5. Cotton Development Board 6. Dairy Development Corporation (excluding Pokhara Milk Supply Scheme) 7. Herbs Production & Processing Co. Ltd. 8. Hetauda Textile Industry Ltd. 9. Janakpur Cigarette Factory

10. Lumbini Sugar Mills Ltd. 11. Morang Sugar Mill Ltd. 12. Nepal Rosin and Turpentine Ltd. 13. Nepal Tea Development Corporation 14. Pokhara Milk Supply Scheme 15. Salt Trading Corporation Ltd.

8

Visits were made to the majority of the enterprises identified by USAID as potential privatization candidates. Of those enterprises visited, all in which HMG held a majority share or was in control were in poor financial or operational condition. All would benefit from early privatization. Those enterprises identified by USAID but not included in the list to be privatized as part of the this assistance program were excluded because of policy issues requiring resolution or because the enterprises have non-competitive operations. All of these enterprises should be transferred to private ownership as soon as those matters are resolved.

Commentary on each of the enterprises reviewed, including a preliminary recommendation on the appropriate modality for sale, is provided in Annex IV. Summary financial and physical performance figures for a number of the enterprises are provided in Annex V. Although these figures were obtained from official government sources, independent checks indicated that many of the figures are not accurate. Therefore, no reliance should be placed on these figures. Given the importance of the dairy industry and the Dairy Development Corporation to the agricultural sector and HMG's privatization program, this sector is covered separately in Annex VI. Financial and performance figures for the dairy sector are included in the dairy annex.

VI ASSISTANCE REQUIRED

The Privatization Cell currently has a staff of only five professionals plus one long term local advisor. The staff are seconded from the Ministry of Finance and other government bodies for periods of two to three years. With such a small staff, the cell must contract out a significant proportion of its work. Asset and business valuations, financial audits, marketing studies, redundancy studies, and legal work are typically contracted out. This system has worked well to date, and the Privatization Cell has decided that it will continue to operate with a small core staff. This means that it will have to continue to contract out much of its work.

As noted below in section IX, Local Consulting Capacity, most of the required consulting services can be obtained locally. However, for business valuations and some legal work, the use of foreign consultants will be necessary. For certain industrial sectors, such as tea, cotton, and dairy, industry specialists will be required. As well as these specialists, a long term advisor with general privatization experience in different countries would assist further refinement and implementation of the whole program. This advisor would be able to assist in reviewing existing policies and procedures. The long term advisor should have a strong commercial background to assist in developing realistic privatization options for enterprises, locating potential investors, and assisting in negotiations.

As noted previously, work is needed to develop and implement a public awareness program. This will require extensive use of local consultants, preferably with oversight by a foreign advisor. Other local costs for advertising, printing, holding seminars, etc., would be involved in implementing the program. Assistance with training of the members of the Privatization Cell

9

members and other key decision makers also would be desirable. This should be in the form of short courses or study visits.

Assistance with funding these foreign advisors will be necessary and, given the constraints on HMO's budget, assistance with funding the local consultants also would be desirable. In addition, the Privatization Cell would benefit from receiving additional general office support. This would cover funding of administrative staff to help manage contracting and finances, additional computing facilities, communications, transportation, upgrading the office facilities etc.

A large part of the assistance described above would benefit the whole of HMO's privatization program, regardless of which sectors the enterprises are in. Of the fifteen agribusinesses recommended to be included under the USAID funded privatization assistance program, only three or four need foreign sector-specialist assistance. Some of the other enterprises on the current privatization list will, however, need extensive sector specialist assistance. This applies particularly to the banking sector. As noted below, privatization of the banking sector will facilitate the privatization of enterprises in all other sectors. Privatization of utilities, which are not yet scheduled for privatization but will need to be dealt with soon, is another area that will require considerable assistance as little thought has yet been given to the question of how to regulate these industries. Overall, as the privatization program is extended, the range of assistance required will broaden.

VII OTHER DONORS

A number of donors have in the past provided assistance to HMO with its privatization program. A more limited number are currently planning to provide assistance. A review of the current plans of major donors is provided below.

a. Overseas Development Administration (ODA)

Although the ODA is a major donor to HMO, to date it has not provided assistance with privatization. However, on 2 October 1996, the ODA proposed to the Ministry of Finance the funding of a long term advisor to provide general assistance to the Privatization Cell for a period of 18 months commencing in December 1996. A limited amount of short term assistance was also included in the offer. (A copy of the "Draft Project Memorandum" is attached as Annex VII.) This offer was made as part of the general assistance that the ODA is providing to the Ministry of Finance. It followed the June 1996 visit of a short term advisor who was contracted to recommend a privatization assistance plan to the DDA. Following the consultant's visit, the Privatization Cell were advised that the offer of assistance would cover both help with the privatization of the Nepal Telecommunications Corporation (NTC) as well as general support for the Privatization Cell. With the government encountering difficulties in the telecommunications sector, and a commitment by the Danes to provide assistance to NTC, the ODA decided to focus its assistance solely on long term general support for the Privatization

10

Cell. The Ministry of Finance currently is considering accepting the offer but on modified terms to try and minimize any overlap with the assistance being proposed by USAID.

Although the ODA has provided considerable support in the past to agriculture and the tea sector in particular, they have no plans to provide specific assistance with privatization of agricultural industries.

b. Danida

Danida has provided considerable assistance to the dairy sector, most recently with efforts to assist with the privatization of the Dairy Development Corporation (DDC). (These efforts are detailed in the dairy annex.) As little progress has been made with the privatization of the DDC, and privatization and the dairy sector no longer fits within Danida's priorities for Nepal, Danida has curtailed its assistance in this area. The only program Danida currently has in the dairy sector is the provision of a long term advisor to the National Dairy Development Board (NDDB). This assistance is to be provided for five years, but may be terminated sooner if certain conditions relating to the independence of the NDDB are not met by HMG.

Danida has agreed to provide assistance with the privatization of the NTC. However, this assistance will be provided directly to the NTC to help the corporation restructure and prepare itself for privatization. Although coordination with the Privatization Cell will be required, there should be no conflict with the assistance being provided to the Privatization Cell by other donors.

c. The World Bank

The World Bank and the UNDP provided support to HMG for the initial round of privatization. With the subsequent provision of assistance by USAID, both the Bank and UNDP withdrew from the area. The World Bank is currently negotiating with HMG over the provision of assistance for the privatization of the fmancial sector. Agreement may prove difficult to reach as the Bank is proposing to provide the assistance mainly in the form of a loan, with only a minor technical assistance grant component. At this stage, HMG is reluctant to enter into a loan agreement for privatization. Should agreement be reached with the World Bank, it would be unlikely to have a significant impact on the assistance being provided by other donors to the Privatization Cell. The major risk is that the work load from the privatization of the financial sector could overwhelm the existing relatively small Privatization Cell.

Privatization of the financial sector in fact would be beneficial to the overall privatization program. Currently the government provides virtually no subsidies to state-owned enterprises in the agricultural sector, the Agricultural Inputs Corporation being the one major exception. However, many state-owned enterprises do borrow significant amounts of money from the major state-owned banks. Although the interest rates on these loans is nominally at market rates, the loans can not be considered commercial as no private sector bank would lend money to these state enterprises given their poor fmancial status. It is only because the banks are state-owned

11

that the loans are made. The government is therefore indirectly subsidizing state-owned enterprises through its ownership in the fmancial sector. Privatizing the financial sector would stop this subsidy and highlight the poor fmancial status of many state-owned enterprises, perhaps forcing some of them into liquidation, or at least hastening their privatization.

d. UNDP

As noted above, the UNDP provided assistance, together with the World Bank, during the initial round of privatization. Along with the World Bank, the UNDP curtailed its support for privatization when USAID funding started. The UNDP's current three year plan does not provide for any support for privatization, nor would privatization easily fit into their overall program for Nepal. However, ifHMG requested assistance with privatization in the future, the UNDP would be willing to consider the request. The Privatization Cell has been advised that they should notify the UNDP now that they may have a need for assistance with privatization in approximately 18 months.

e. Germany/KfW

The German government is currently providing assistance through KtW for the privatization of the Himal Cement Company. The company is relatively small and the assistance is well advanced, so the activity should have little impact on the assistance being proposed by USAID.

f. The Asian Development Bank (ADB)

The ADB has provided considerable assistance to Nepal, including support for the agricultural sector. Although at a policy level they support the government's privatization program, at this stage they have no plans to provide fmancial assistance for privatization. The ADB would consider providing assistance for privatization in the future. This would probably be in the form of a loan with only limited technical assistance. Ad hoc assistance on a particular project, such as the privatization of the airline, is also a possibility.

g. Other Donors

A number of other donors have provided support for the agricultural sector, for example the Finns and Australians with forestry. In general, donors are cutting back their programs and, as far as could be established, none are planning to provide assistance with privatization. The Canadian government has provided assistance to Royal Nepal Airways Corporation. However, this assistance was provided directly to the Corporation and, although it should facilitate privatization, is not directly related to it.

h. The Future

No donor currently plans to provide assistance to HMG with its privatization program beyond the 18 month period that is envisioned for the USAID and ODA programs. The UNDP, ADB,

12

and the World Bank could all be in a position to provide limited assistance in the future, although in the cases of the World Bank and the ADB it would be loan financing which HMG is reluctant to use. Thus, at this stage, there is no obvious candidate to take over the position that USAID held in the past.

VIII RECOMMENDED PLAN

The assistance program recommended for USAID is divided into three parts, corresponding to the three sources of funds available. A description of each of the three components is provided below. Section XI outlines an indicative budget for the use of the funds; Annex vrn provides detailed estimates for the use of the local currency funds and the new U.S. dollar funds.

a. Local Currency Funds - 416(B)

The 4l6(B) funds should be provided directly to the Privatization Cell, under the Ministry of Finance, as project funds. Control of the funds should be through a quarterly budget, prepared by the long term advisor and approved by the Privatization Committee. Assistance provided by these funds should cover both support for the privatization of individual enterprises as well as general support for the Privatization Cell and the strengthening of the overall privatization program.

i. Enterprise Sales Support

The Privatization Cell currently draws on local consultants to help prepare offering memoranda. It is recommended that this process continue and that part of the local currency funds available be used to meet the costs of these consultants.

The Privatization Act requires that an evaluation of each enterprise be conducted. These evaluations always include an asset valuation carried out by local valuers. In preparing offering memoranda, accountants/fmancial analysts are used to review and prepare fmancial statements and forecasts for each enterprise. A redundancy study is also carried out for most enterprises. This study estimates the number of employees that will need to be made redundant as part of the privatization process and calculates the cost of meeting all gratuity liabilities and any other redundancy costs. Local consultants typically are employed to undertake these three studies, which are required for each enterprise where HMO holds a majority stake.

For certain enterprises, other consultants will need to be employed. For example, where a new company must be established with the break up of a single enterprise, as in the case of the Pokhara Milk Supply Scheme and possibly the Nepal Tea Development Corporation, legal assistance will be required. For other enterprises, sector specialists will be required. For example, an agricultural specialist with expertise in cotton should be employed to assist with the evaluation of the Cotton Development Board. Such consulting expertise should be available

13

locally. Where HMG holds only a minority stake in an enterprise, or the shares are already listed on the Nepal Stock Exchange, more limited consulting services will be required.

In total, it is estimated that approximately Rs9 million will be required to meet the costs of all the consultants needed for the privatization of the 15 enterprises proposed to be covered by this assistance program. It is recommended that all of these costs be met out of the local currency funds. Details of the projected needs for the use of local consultants are included in the indicative budget in Annex VITI.

li. Public Awareness Program

As noted above, public awareness is an area where considerably more work needs to be done. It is recommended that approximately Rs5. 7 million of local funds be allocated to a public awareness program. The public awareness program should target three main groups: the general public; key decision makers; and the employees of enterprises being privatized. Other areas covered by the program would include international advertising of enterprises for sale and public relations for the Privatization Cell and the Ministry of Finance.

The General Public. The program aimed at the general public should focus on providing the public with a general understanding of privatization and the workings of HMG's privatization program. Material should cover the failings of the existing state-owned enterprise system, the need for and benefits of a privatization program, the way the program operates in Nepal, the successes achieved so far in Nepal and elsewhere in the region, and the way in which HMG's program will effect the general public. The program should make use of radio, newspapers, and television, producing articles and programs for publication as well as paid advertisements. Seminars and workshops also could be presented around the country. Politicians and experts from nearby countries with successful privatization programs, such as Malaysia, should be brought in to describe the successes and problems of the programs in their own country.

Key Decision Makers. The program aimed at key decision makers would be based mainly on seminars and workshops and would seek to provide participants with an in-depth understanding of privatization and HMG's program in particular. It is estimated that there are close to 1,000 politicians, senior government officials, academics, journalists, and union leaders who should be targeted. A series of one day residential seminars or workshops are recommended, with a maximum of 40 people attending any seminar. One or two small teams would organize and present the seminars, covering all major centers in the country over the 18 month period of the assistance program. This program also should make use of politicians and experts from nearby countries.

A small number of selected opinion makers could also be taken on organized study tours of neighboring countries to observe directly the impacts of privatization.

Employees. The program aimed at the employees of enterprises being privatized would seek to inform the employees in detail of the privatization process as it applied to them and their

14

enterprise. As soon as an enterprise enters the privatization process, a specialist team should visit the enterprise to explain the whole privatization process including the proposed timetable, the likely impact on the employees, and their rights, particularly with regard to redundancy, gratuity payments, and purchasing shares in the enterprise. The team should include one or two specialist consultants who would be core members of each team, at least one member of the Privatization Cell and, where possible, a senior officer of a private sector enterprise from the same industry. Separate meetings with the union leaders of the enterprise should be an integral part of the program.

A standard audio-visual package for use at all enterprises may be a useful tool to be employed by the team. Visits by the team should continue throughout the privatization process to keep employees informed of progress up until the enterprise is handed over to the new owner. A total of three to four visits per enterprise may be necessary.

Public Relations. Assistance should be provided to the Privatization Cell and the Ministry of Finance to help them manage the public relations aspect of their work. This assistance would include generating press releases, answering questions in Parliament, and organizing interviews with journalists. A specialist public relations firm could be contracted to carry out this work or, more practically, the full time local consultant recommended below should have the appropriate skills to carry out this task.

International Advertising. A limited amount of local funds could be used to pay for advertising in regional newspapers, magazines, and selected trade journals, for enterprises where there is a reasonable probability of foreign investors being interested in buying the enterprise. This is likely to occur with the tea, herbs, and turpentine companies.

Managing the Program. It is recommended that the Privatization Cell employ one full time local consultant to help develop and oversee all aspects of the public awareness program. This person would be responsible for contracting out the major components of the program, and supervising and coordinating the work of the consultants. Provided they had the appropriate skills, the consultant would also be directly responsible for the public relations component of the program. [During interviews with various media consultants and companies, one individual was identified with suitable skills. He was Bishnu Raj Adhikari, ex-executive director of the Management Association of Nepal.]

iii. Training

It is recommended that approximately Rs4.25 million of local funds be allocated to short term training for the Privatization Cell members and selected politicians or senior government officials.

Most of the existing Privatization Cell members have received some training abroad, usually a two to three week general course on privatization. Some have had subsequent, specialized training, for example on valuation. However, in the near future it is likely that two or three

15

members of the cell will be replaced. When this happens, the new cell members should receive a similar basic level of privatization training. Other members of the cell should be sent on more advanced courses or for suitable study visits. Provision has been included in the indicative budget for the cost of six two to three week training courses including travel, per diem, and course fees.

In addition to the training of the Privatization Cell members, provision has been included in the indicative budget for sending three politicians or senior government officials on general privatization training courses. Should this aspect of the training program prove to be productive, money allocated to the public awareness program could be used to fund training courses for additional candidates.

iv. Legislative Review

The Privatization Act, as described above, is a new act and reasonably satisfactory. Although this is the main act controlling privatization, many other acts impinge on the overall privatization process. For example, the Companies Act is frequently used to establish a limited liability company to replace a state enterprise being privatized; the limited liability company becomes the new legal entity which is actually sold in the privatization process.

Other general acts that may also impinge on the privatization process are the Cooperatives Act, the Labour Act, acts relating to contract law, and anti-monopoly legislation. Although some general laws have been revised recently, for example a new Companies Act was passed this year, other general legislation relating to privatization is in need of revision. One important case is the Cooperatives Act, which is likely to playa large part in the privatization of the dairy sector. This Act contains provisions which need to be changed if newly established cooperatives are to function properly.

Other acts may directly affect one particular sector. For example, the National Dairy Development Act contains provisions relating to milk price fixing. It is likely that there is much sector specific legislation which will need to be changed so that newly privatized companies operate in a truly competitive market. If the full benefits of privatization are to be realized, it is essential that markets be liberalized and that the entry of new enterprises to compete in the market place be freely allowed.

Approximately Rs284,OOO has been included in the budget to allow for a review of all general legislation relating to privatization, as well as sector specific legislation relating to the industries being covered by this assistance program. A number of local NOOs and consulting firms have the necessary experience to carry out this work. A single contract could be let out covering all the work, or one contract could cover general legislation with separate contracts for sector specific legislation. Commencing this work as soon as possible should be a high priority.

16

v. Gratuity Payments

A major fmandal cost to HMG in implementing its privatization program is the cost of meeting accrued liabilities for gratuity payments for workers that are made redundant through the privatization process. Gratuity payments normally accrue at the rate of one and a half months salary for each year employed. state-owned enterprises, which generally operate on a modified cash accounting basis, do not show these liabilities on their balance sheet. In general they also fail to hold any funds to meet the cost of paying out the gratuities when employees are made redundant or retire.

In privatization, these costs typically end up as a liability of HMG. With some of the larger enterprises that are planned to be dealt with under this program, these costs will be substantial and may become a significant hindrance to the privatization process. For example, at Janakpur Cigarette Factory, in excess of 500 employees may need to be made redundant. Based on an average of one year's gratuity payment per employee, the total liability would be in excess of Rs6 million. Approximately RsI1.3 million has been included in the budget to cover the major part of the gratuity payments that will be incurred in privatizing the enterprises covered by this assistance program. The exact costs that will be incurred by HMG for each enterprise are calculated as part of the redundancy study that is carried out when evaluating enterprises being privatized .

vi. Skills Retraining

In addition to meeting the accrued gratuity cost of employees made redundant through the privatization process, it would assist the privatization program if redundant workers were provided with skills retraining. Programs should be developed which would be implemented at enterprises with major redundancy problems. These programs would cover skills retraining and support to help redundant employees establish new businesses. A number of NGOs are already providing training in this area. Proposals should be sought from them and any other interested parties to provide a program covering the enterprises where the redundancy studies indicate the greatest need. Approximately Rs2.8 million has been included in the indicative budget to cover skills retraining.

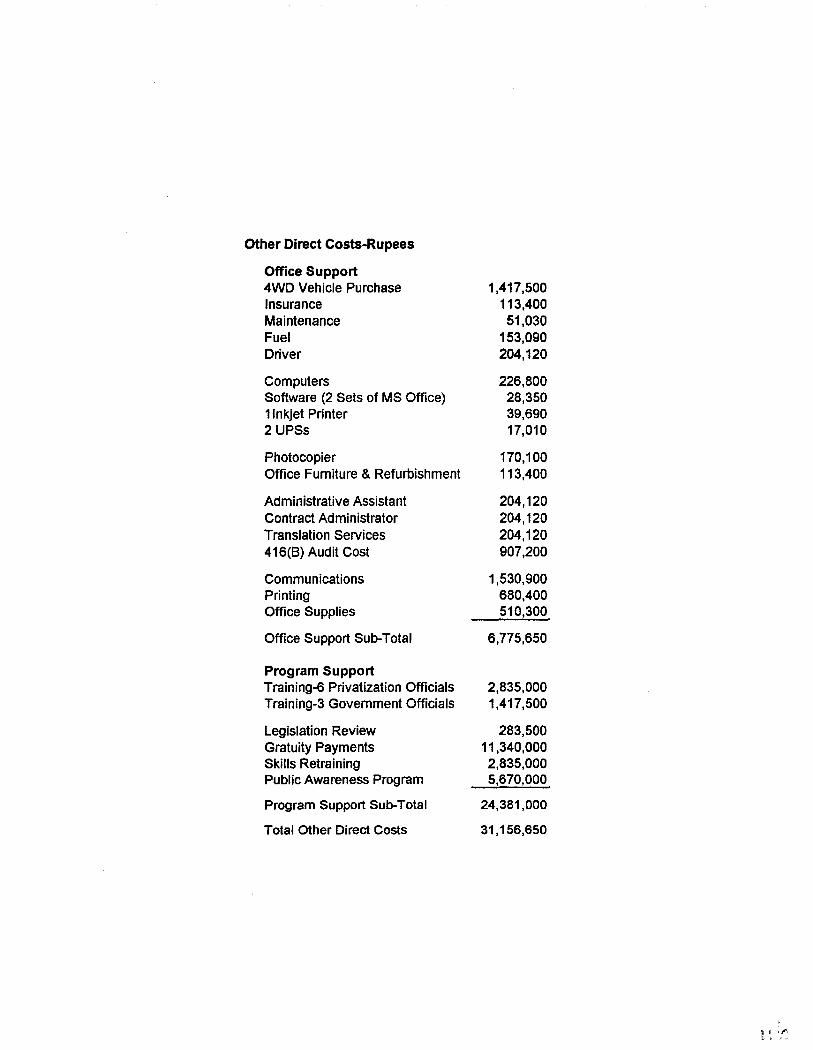

vii. Office Support

Limited office support for the Privatization Cell currently is being provided through the IRIS project. However, this support is likely to cease in November 1996. Further, with the increase in work load planned for the cell, the level of office support will need to be increased. Approximately Rs5. 9 million has been included in the indicative budget to cover the cost of office support for the 18 month period of the assistance program. This money is intended to cover the cost of an upgrade of the office and its equipment as well as normal operating costs. As it is planned to let a large number of contracts for outside consultants, potentially in excess of 70, and incur significant local costs on other aspects or the program, the cost of employing an administrative assistant and a contract administrator have been included. Much of the written

17

work for the Privatization Cell must be prepared in both English as well as Nepalese, so provision has been made to cover translation costs. Details are provided in the indicative budget below.

viii. Management of the Local Funds

The local funds should be transferred from the existing account at the DDC to an interest bearing account managed by the Privatization Cell. Officials of the Privatization Cell have yet to determine the mechanism through which they can establish such an account within current regulations, but are confident that it will be possible. The Privatization Cell should commence this process, with USAID approval, as soon as possible so that expenditure of these funds will not be delayed.

General control of the funds should be through a quarterly budget prepared by the long term advisor and approved by the Privatization Committee. No expenditure should be allowed outside that approved budget. The office administrator should assist in ensuring that adequate records are kept and controls are maintained on expenditure. The indicative budget provided in Annex VIII should not be treated as binding when the quarterly budgets are being prepared. Rather, it should be used as a guide to the areas where expenditure should be directed and an indicator of the level of support which is considered appropriate for each area. If any major divergences from the indicative budget are contemplated, they should be agreed with USAID first.

The Privatization Cell should prepare a manual detailing the procedures to be followed in spending the local funds. This procedures manual should be approved by the USAID (Nepal) controller. Audits of local fund expenditure should be carried out after one year and at the end of the project. A provision has been included in the budget to cover the cost of two audits.

If a long term advisor is not in place when expenditure of these funds commences, it is recommended that the Privatization Cell should develop the first quarterly budget with the approval of the USAID project officer.

It should be noted that gratuity payments are only made at the time an enterprise is privatized. Similarly, the majority of expenditure on skills retraining should be incurred only after an enterprise has been privatized. This means that over one third of the local funds can be accessed only when actual privatizations have been completed. This does provide some incentive component to the local fund program.

b. US Dollar Funds - New Funds

It is recommended that the $700,000 of new funds be used to meet the cost of providing a long term advisor to work at the Privatization Cell, together with the provision of short term advisors to assist with the sale of selected enterprises. As the cost of supporting a long term advisor for 18 months will use more than 70 percent of the funds available, only limited short term support can be provided.

18

It is recommended that the scope of work for the long term advisor cover the following:

• assist the Privatization Cell in all matters relating to HMO's privatization program for agricultural based industries;

• recommend suitable methods for sale of enterprises and assist in preparing offering memoranda;

• assist in identifying and selecting potential investors; • assist in negotiations with potential investors; • review HMG's privatization program and recommend ways in which the program could

be improved; • assist the Privatization Cell, in consultation with the ODA long term advisor, in refining

their work program for the following 18 months, in particular identifying the enterprises to be included in the program, the external resources needed to assist with the privatization, and the target dates on which the enterprises will be offered for sale;

• approve the quarterly budget prepared by the Privatization Cell for the expenditure of the local currency fund;

• help identify and supervise the work of short term advisors selected to assist with the privatization of individual enterprises;

• assist in developing and overseeing the public awareness and skills retraining programs; • assist with the training of the local staff.

The above scope of work for the long term advisor was developed on the basis that the ODA will have a long term advisor working in the Privatization Cell for the same period as the USAID long term advisor. No final agreement had been reached between the Ministry of Finance and the two donor agencies as to how work would be divided between the two advisors at the time this report was prepared. The scope of work proposed for the USAID long term advisor therefore may need to be modified in light of any subsequent agreement between the parties on the distribution of work.

Foreign short term assistance has been included for six enterprises in the indicative budget. These enterprises are the Pokhara Milk Supply Scheme and the remainder of the Dairy Development Corporation, the two sugar mills, Janakpur Cigarette Factory, and the Herbs Production and Processing Company. Short term assistance definitely will be necessary for the privatization of the Nepal Tea Development Corporation, but this has not been included in the budget due to the shortage of funds. As ODA provided considerable assistance to the tea sector in the past, it has been assumed that they will be willing to provide the necessary assistance. Should this assistance not be forthcoming, reductions to or the total elimination of assistance to other enterprises will be necessary. Similarly, it would be desirable to have some short term assistance in developing the public awareness program, reviewing legislation, and developing and overseeing the skills retraining program. However, limitations on funding preclude this.

As there is potential for overlap with the assistance being provided to the Privatization Cell by different donors, it is recommended that USAID take the initiative in organizing regular

19

coordination meetings between donors. These meetings should occur on a monthly basis at the working level, with less frequent meetings scheduled for more senior donor officials.

c. US Dollar Funds - Pipeline Funding

The exact amount available in this fund is not known at this stage, but is estimated to be approximately $250,000. This fund originally was committed for use on the dairy sector and must continue to be used in that sector under this program. This fund should be directed at helping privatize DDC and strengthening private sector participation in the dairy sector. It is recommended that this money be used to fund a range of projects aimed at achieving these objectives. A selection of projects which could be funded with this money are described below, but it is recommended that proposals for additional projects be sought from contractors before a final selection is made by USAID.

i. Suggested Projects

One project which would directly boost private sector participation in the dairy sector as well as facilitate the privatization of the DOC is giving new impetus to the program of converting Milk Producers Associations (MPA) into Milk Producers' Cooperatives Associations (MPCS). MP As are under the control of the ODC, whereas MPCSs are independent privately-owned cooperatives. Converting MP As into MPCSs directly increases the portion of the dairy sector that is under private sector control. In addition, greater flexibility is provided for the privatization of DOC if all collection centers are separated legally from the rest of the DDC. This is particularly urgent in the case of the Pokhara Milk Supply Scheme which is to be privatized first, but is also important for the rest of the ODC if the remainder of the DDC is to be sold in parts, as is currently proposed.

Another project to strengthen the private sector is providing assistance to existing and new MPCSs to improve their operations. Available evidence suggests that the majority of the existing MPCSs are operating at a loss. Although in part this is due to current DDC policies, many MPCSs would benefit from adopting a more commercial approach to their operations. Assistance in basic business skills is needed to help them meet this objective. Newly established MPCSs are likely to have an even greater need for assistance.

There are a number of other areas where assistance would strengthen the dairy sector, and in particular the private sector. The current surplus of milk produced during the flush season and the corresponding shortfall during the lean season causes considerable difficulty for the whole dairy sector. Apart from a change in pricing policy by the DOC, there are a number of specific measures that could be implemented to alleviate this problem. There are various long life products such as ice cream and milk based desserts that could be produced during the flush season to help smooth out the demand for fresh milk throughout the year. A study on the demand for such products and the feasibility of producing them could be prepared and distributed widely to assist the private sector in establishing and expanding this new segment of the industry.

20

An issue which is likely to cause political problems for the privatization of DDC is the number of existing milk producers who do not produce sufficient milk or are too remote from transport or population centers to make their operations economically viable. If the dairy sector is ever to be privatized fully and operate on a competitive basis, these uneconomic milk producers will need to get out of producing milk. A project that would assist in the privatization process would be to identify the uneconomic milk producers and recommend programs to facilitate these farmers withdrawing from milk production. Should any of these programs be judged worthwhile, money could be allocated to implement them.

The above represent only some of the projects that could be undertaken to strengthen private sector participation in the dairy sector and facilitate the privatization of DDC.

ii. Contracting out the Projects

In the normal course of events, proposals should be sought from contractors to carry out the above projects and any other projects that they may suggest which would achieve the desired objectives.

The Agro Enterprise Centre (AEC), which was established with USAID funding, is one local consulting group that has the capability to carry out the above and related projects. USAID has used the AEC to carry out successfully projects similar to those above. As the Coopers & Lybrand/CTS team did not have the opportunity to review all local agricultural consulting capability, the team is not in a position to make any recommendation on the capability of other contractors to carry out such projects.

Based on the USAID experience, a waiver could be obtained for AEC. The AEC should be asked to make a detailed proposal for the expenditure of the pipeline funds based on the above guidelines. They should be allowed only a limited time, say a maximum of one month, to prepare their proposal. They should be encouraged to develop their own proposals which would achieve the objectives of strengthening private sector participation in the dairy sector and facilitating the privatization of DOC. Should the AEC not come up with a satisfactory proposal within the specified time frame, other contractors should be given the opportunity to make proposals covering all or some of the funds. Defining benchmarks for measuring the success of each of the projects should be an integral part of any proposal, whether made by the AEC or another contractor.

In selecting the projects that will be funded with this money, care should be taken to ensure that the benefits accrue to the whole dairy sector. No project in any way should go towards further consolidating the dominant position the DDC holds in the sector. Working through the two newly established private sector dairy associations would help to achieve this objective.

21

IX LOCAL CONSULTING CAPACITY

The above recommended assistance plan provides for extensive use of local consultants. In light of this, and the requirements of the scope of work, a brief review of local consulting capabilities was carried out.

The Privatization Cell currently makes use of a range of local consultants and, in general, they provide adequate service. The major work for which the cell currently uses local consultants is to carry out asset valuations. This will continue to be the case under the proposed work plan. USAID previously provided training to approximately 50 local asset valuers. The Privatization Cell relies on approximately 15 of these valuers to carry out its asset valuations. All of these valuers have proved to provide adequate service. The Privatization Cell selects valuers on the basis of competitive tenders, with a minimum of three proposals being sought. The use of this selection procedure should continue and be employed wherever possible for the employment of all local consultants.

Currently all business valuations are carried out by foreign consultants. This will need to continue until training of local consultants is undertaken, as no local consultants have the necessary skills. If short term consulting resources permit, delivery of a business valuation training course should be included in the scope of work of one or more of the foreign business valuers brought to Nepal.

There are approximately 7,000 registered accountants in Nepal, but only 105 of these are qualified at the" A grade" level. Of these, only half are thought to be in practice, usually as sole practitioners. Only one local firm has an affiliation with a big six international accounting firm. For the limited range of services normally required by the Privatization Cell, such as preparing financial statements, local consultants provide an adequate service. It is recommended that the Privatization Cell only make use of "A grade" accountants. No evidence was available to indicate that more sophisticated financial analysis services are available.

There are approximately 5,000 lawyers in Nepal. Most are sole practitioners offering a full range of services. Specialization of service is only just beginning to occur. As with accountants, for the services normally required by the Privatization Cell, such as preparing articles of association or contracts, local services are adequate. For tasks such as reviewing legislation, outside assistance would be desirable to provide an international business perspective. The Privatization Cell is assisted by a lawyer from the Ministry of Law during contract negotiations with investors.

Specialist market consultants and consultants with the skills to carry out redundancy studies are in more limited supply. For these services only one consultant with the required skills or experience may be available. The quality of work produced by these consultants is highly variable. General marketing consultants were interviewed as part of developing the plan for a public awareness campaign. The quality and range of services offered by those interviewed was limited.

22

Overall, the availability and quality of local consultants should prove no hindrance to HMG's privatization program or the proposed USAID assistance plan. In some specialist areas, such as business valuation and public awareness campaign development, outside assistance will be required.

X BENCHMARKS AND POST-PRIVATIZATION MONITORING

Identification of benchmarks for measuring the success of the privatization program is a necessary part of the assistance program. Suggested benchmarks, together with comments on their applicability, for each of the major parts of the recommended assistance program are provided below.

a. Enterprise Sales Program

The successful completion of the sale of the state's share in each of the 15 enterprises covered by the assistance program provides the most appropriate benchmarks to measure the achievements of the recommended sales program. Measuring the number of enterprises privatized is a good way of assessing the success of the expenditure of all the new dollar funds and a large portion of the local funds. A proposed privatization schedule for the completion of the sale of all 15 enterprises in provided in Annex IX. This timetable will be updated by the long term advisor within two months of arrival in country.

It needs to be emphasized that the proposed schedule was developed on the basis of the time necessary to carry out all the technical aspects of the privatization process. No allowance was made for delays caused through the political processes associated with the program or any legislative changes that may be required to ensure that the relevant sector is operating in a fully competitive manner. Any such delays need to be added directly to the time taken to successfully complete each privatization. As several of the enterprises proposed for privatization are politically sensitive, it is highly likely that delays will occur. However, should these delays become excessive, a review of the entire assistance program should be undertaken.

Monitoring and measuring the impact on the economy of the privatization of the targeted enterprises should be based on the monitoring work that is already undertaken by the Privatization Cell. The cell collects a significant amount of data from privatized enterprises through a written questionnaire that is sent to all enterprises on an annual basis. A copy of the questionnaire is included in Annex X. This information will continue to be collected by the Privatization Cell even after USAID's assistance to the cell has ceased and so will allow continued monitoring of the impact of the privatization program.

Care needs to be used in making use of the information collected from privatized enterprises. No single measure should be used to judge the success or otherwise of the privatization program. An increase in investment, employment, and sales of a privatized enterprise clearly represents a success. However, for some enterprises, liquidation may count as a success for the

23

privatization program. Even for enterprises that continue to operate after privatization, a reduction in sales may represent an improvement in performance if the enterprise went from operating as a state-owned monopoly to being a privately owned business operating in a competitive market.

b. A wareness and Training Program

For the local funds that cover the public awareness program and training, no simple benchmarks are available apart from monitoring the delivery of the awareness program and the completion of training. Improvements in public awareness could be measured through surveys, but such efforts and expense are not justified.

c. Dairy Sector Program

In general, benchmarks for the pipeline funds used for dairy sector projects should be specific to each project undertaken, although an obvious benchmark for the program as a whole would be the number of new private dairy enterprises or the percentage of milk processed by the private sector. Benchmarks for the projects outlined above are suggested below. Recommended benchmarks should be included as part of the project proposals where additional proposals are sought from outside consultants.

For the project of converting MPAs to MPCSs, the most appropriate benchmark would be the number of MPAs converted to MPCSs. The project for offering business advisory assistance to MPCSs is more problematic. A reduction in the number of MPCSs operating at a loss would be one measure, but this could be significantly affected by weather conditions during the year and the entry of a large number of newly formed and inexperienced MPCSs.

Benchmarks for the long life milk product project could be the production of marketing and feasibility studies. In terms of measuring actual impacts, a reduction in the number of milk holidays (days when milk is not purchased from suppliers due to a lack of processing capacity) would be appropriate, although it could take several years for any impacts of the project to be felt. Weather conditions and other changes in the dairy sector would also need to be considered. Lastly, the assistance to uneconomic farmers project could be evaluated against the number of farmers helped out of milk production.

XI INDICATIVE BUDGETS

Indicative budgets covering the local currency fund and the new US dollar funds are provided below. Details of the budgets are provided in Annex vm. As described in Section vn, the local currency funds should be used to meet all local costs associated with the enterprise sales as well as to fund a public awareness program, training, a legislation review, general office support, skills retraining, and meeting some enterprise redundancy costs. The funds should be

24

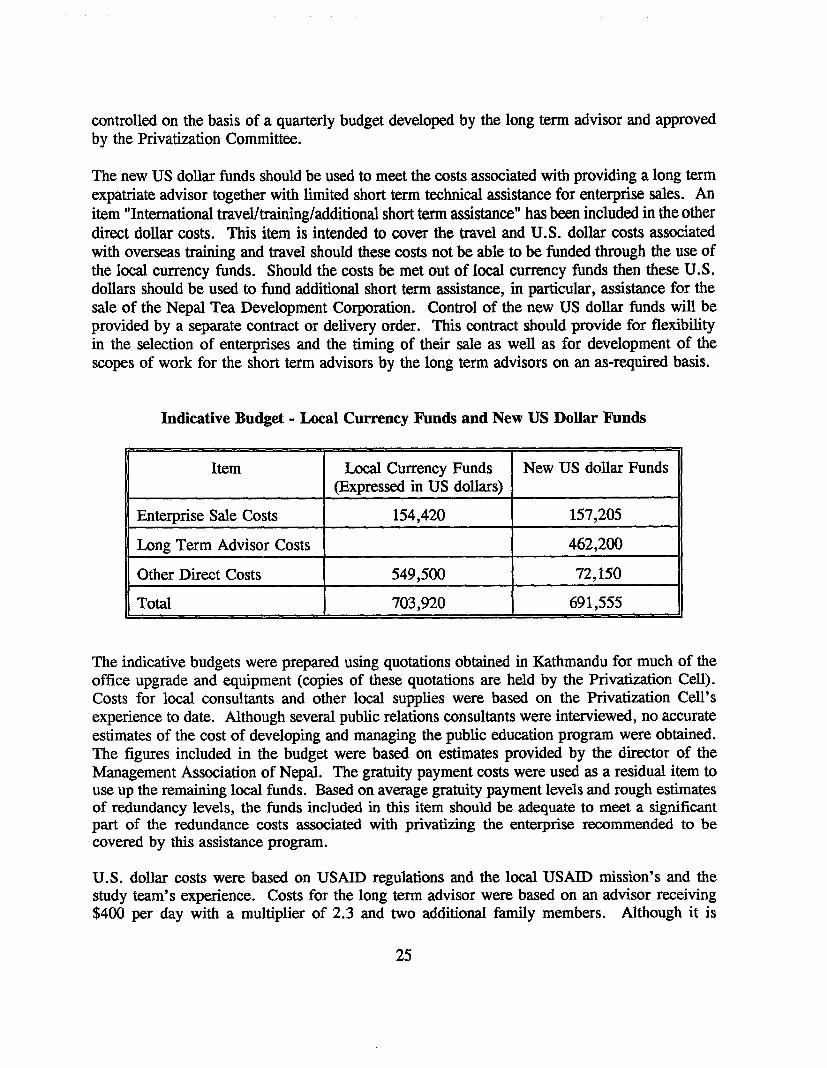

controlled on the basis of a quarterly budget developed by the long term advisor and approved by the Privatization Committee.

The new US dollar funds should be used to meet the costs associated with providing a long term expatriate advisor together with limited short term technical assistance for enterprise sales. An item "International travel/training/additional short term assistance" has been included in the other direct dollar costs. This item is intended to cover the travel and U.S. dollar costs associated with overseas training and travel should these costs not be able to be funded through the use of the local currency funds. Should the costs be met out of local currency funds then these U.S. dollars should be used to fund additional short term assistance, in particular, assistance for the sale of the Nepal Tea Development Corporation. Control of the new US dollar funds will be provided by a separate contract or delivery order. This contract should provide for flexibility in the selection of enterprises and the timing of their sale as well as for development of the scopes of work for the short term advisors by the long term advisors on an as-required basis.

Indicative Budget - Local Currency Funds and New US Dollar Funds

Item Local Currency Funds New US dollar Funds (Expressed in US dollars)

Enterprise Sale Costs 154,420 157,205

Long Term Advisor Costs 462,200

Other Direct Costs 549,500 72,150

Total 703,920 691,555

The indicative budgets were prepared using quotations obtained in Kathmandu for much of the office upgrade and equipment (copies of these quotations are held by the Privatization Cell). Costs for local consultants and other local supplies were based on the Privatization Cell's experience to date. Although several public relations consultants were interviewed, no accurate estimates of the cost of developing and managing the public education program were obtained. The figures included in the budget were based on estimates provided by the director of the Management Association of Nepal. The gratuity payment costs were used as a residual item to use up the remaining local funds. Based on average gratuity payment levels and rough estimates of redundancy levels, the funds included in this item should be adequate to meet a significant part of the redundance costs associated with privatizing the enterprise recommended to be covered by this assistance program.

U.S. dollar costs were based on USAID regulations and the local USAID mission's and the study team's experience. Costs for the long term advisor were based on an advisor receiving $400 per day with a multiplier of 2.3 and two additional family members. Although it is

25

possible that savings could be made on this figure, particularly if the advisor does not have a family, it is also possible that the costs could be higher. If this is the case, additional funds could be used from the "additional short term assistance" item included under "other direct costs. "

It should be noted that the definition of "Other Direct Costs" used in the indicative budgets does not follow strictly the USAID definition of the term. Some costs, such as local travel, that would be included in this item under the USAID definition have been included under "Enterprise Sale Costs" where the costs are strictly related to the sale of an enterprise.

A specific budget for the pipeline funds has not been prepared as this budget will be based on the projects selected by USAID from the proposals made by contractors.

X CONCLUSION

HMG has taken important steps over the past five years in developing its privatization program. The legal and institutional framework that has been established appears reasonably sound, although it has not been tested on large or politically sensitive enterprises. All of the stateowned agribusinesses evaluated as part of this project would benefit from privatization, although some require the government to implement policy reforms first. Many enterprises in other sectors are also urgently in need of privatization. With coordinated assistance by donors, the Privatization Cell should have the resources necessary to implement a comprehensive privatization program. Political constraints may, however, lead to delays in the execution of the proposed plan. Should significant delays occur, particularly with the privatization of the dairy sector, USAID should review its continued assistance of privatization in Nepal.

26

ANNEXES

ANNEX I

INSTITUTIONS AND INDIVIDUALS INTERVIEWED

Institutions and Individuals Interviewed

USAID

Dr. Frederick Machmer. Director David Johnston. Deputy Director Amanda Levenson. Controller Sribindu Bajracharya. Program Specialist Shubha Banskota. Program Specialist James Gingerich. Program Officer

Ministry of Finance

Ram Binod Bhattarai. Secretary Tirtha Sharma. Joint Secretary, Corporations Co-ordination Division Tanka Khanal. Director, Privatization Cell Narenda Man Shrestha. Privatization Cell Gopal Ghimire. Privatization Cell Durga Achary. Privatization Cell Animesh Upadhayay. Legal consulant to Privatization Cell

Ministry of Agriculture

Dan Bahadur Shahi. Secretary Jagannath Thapaliya. Joint Secretary

National Planning Commission

Prithvi Raj Ligal. Vice Chairman

Ministry of Industry

Bimal Prasad Koirala. Joint Secretary

Nepal Securities Board

Dambar Dhungel. Chairman

Danish Embassy

Liz Garvel. Counsellor Lief Kristensen. Administrative Counsellor Peter Lund. Advisor to the NDDC

British Embassy

Michael Alcock. First Secretary, Development and Commercial John Abington. Agricultural Research Coordinator

World Bank

Para Suriyaarachchi. Senior Economist

Asian Development Bank

Young Baek Lee. Senior Project Administration Specialist

United Nations Development Program

Caroll C. Long. Resident Representative (By telephone) B. K. L. Jossi. Program Officer

National Dairy Development Board

Dhruba Limbu. Executive Director

Dairy Development Corporation

Gabya Nath Pant. Acting Manager

Pokara Milk Supply Scheme

Siyaram. Plant Manager Ieswari Raj. Assistant Plant Manager

Milk Producers Associations/Cooperative Societies

Eighteen selected chairmen

Private Dairies

Ram Malan Upadyaya. Director, Sitaram Goku! Milks Ltd K.P. Thapa. Plant Manager, Pokhara Dairy Ltd

Nepal Tea Development Corporation

Y.P. Gartavla. General Manager Hari Narayan Shah. Chief Manager, Tokla Tea Estate Shiv Acherya. Manager, Barne Tea Estate

Lumbini Sugar Mills Ltd.

Madan Prasad Koirala. General Manager

Birganj Sugar Factory Ltd.

Bhupal Lamichhaney. Executive Chairman

Hetauda Textile Industry Ltd.

Upendra Shumshere J.B. Rana. General Manager

Agricultural Lime Industry, Chovar, Katmandu

Ghan Shyam Rajauriya, Acting General Manager

Herbs Production & Processing Co. Ltd.

Rana B. Rawal. General Manager

Janakpur Cigarette Factory Ltd.

Hari Gavtam. Chairman Dr. Gopal Prasad Shrestha. General Manager