Embed Size (px)

Citation preview

Natural Rubber review

-1-

Natural rubber market review – Aug2010

Fundamental developments

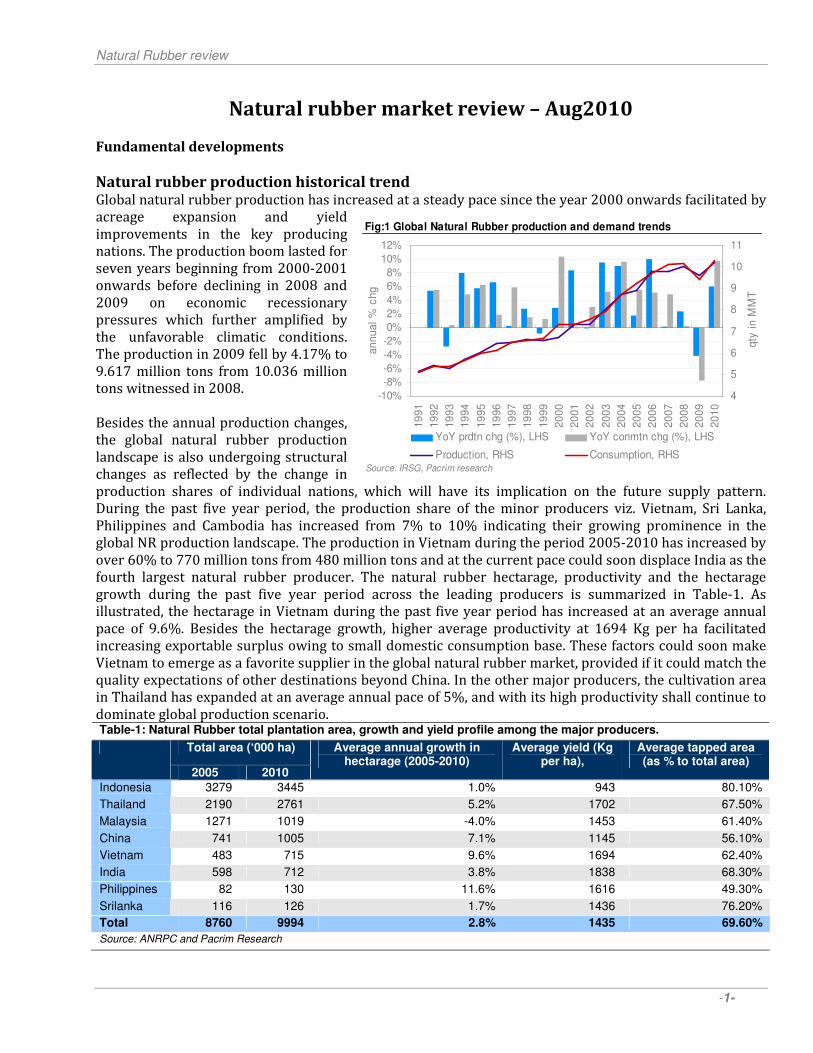

Natural rubber production historical trend Global natural rubber production has increased at a steady pace since the year 2000 onwards facilitated by acreage expansion and yield

improvements in the key producing

nations. The production boom lasted for

seven years beginning from 2000-2001

onwards before declining in 2008 and

2009 on economic recessionary

pressures which further amplified by

the unfavorable climatic conditions.

The production in 2009 fell by 4.17% to

9.617 million tons from 10.036 million

tons witnessed in 2008.

Besides the annual production changes,

the global natural rubber production

landscape is also undergoing structural

changes as reflected by the change in

production shares of individual nations, which will have its implication on the future supply pattern.

During the past five year period, the production share of the minor producers viz. Vietnam, Sri Lanka,

Philippines and Cambodia has increased from 7% to 10% indicating their growing prominence in the

global NR production landscape. The production in Vietnam during the period 2005-2010 has increased by

over 60% to 770 million tons from 480 million tons and at the current pace could soon displace India as the

fourth largest natural rubber producer. The natural rubber hectarage, productivity and the hectarage

growth during the past five year period across the leading producers is summarized in Table-1. As

illustrated, the hectarage in Vietnam during the past five year period has increased at an average annual

pace of 9.6%. Besides the hectarage growth, higher average productivity at 1694 Kg per ha facilitated

increasing exportable surplus owing to small domestic consumption base. These factors could soon make

Vietnam to emerge as a favorite supplier in the global natural rubber market, provided if it could match the

quality expectations of other destinations beyond China. In the other major producers, the cultivation area

in Thailand has expanded at an average annual pace of 5%, and with its high productivity shall continue to

dominate global production scenario. Table-1: Natural Rubber total plantation area, growth and yield profile among the major producers.

Total area (‘000 ha)

2005 2010

Average annual growth in hectarage (2005-2010)

Average yield (Kg per ha),

Average tapped area (as % to total area)

Indonesia 3279 3445 1.0% 943 80.10%

Thailand 2190 2761 5.2% 1702 67.50%

Malaysia 1271 1019 -4.0% 1453 61.40%

China 741 1005 7.1% 1145 56.10%

Vietnam 483 715 9.6% 1694 62.40%

India 598 712 3.8% 1838 68.30%

Philippines 82 130 11.6% 1616 49.30%

Srilanka 116 126 1.7% 1436 76.20%

Total 8760 9994 2.8% 1435 69.60%

Source: ANRPC and Pacrim Research

Fig:1 Global Natural Rubber production and demand trends

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

an

nu

al

% c

hg

4

5

6

7

8

9

10

11

qty

in

MM

T

YoY prdtn chg (%), LHS YoY conmtn chg (%), LHS

Production, RHS Consumption, RHSSource: IRSG, Pacrim research

Natural Rubber review

-2-

Current scenario, NR production expected to rebound in the year 2010….

The natural rubber production is seen rebounding in 2010 from the depressed production levels witnessed in 2009. The production in the leading

producers viz. Thailand, Indonesia, Malaysia

and India which together accounted for 75%

of the global production in 2009, witnessed

good increase in the first half of 2010

compared to the corresponding period

previous year level as illustrated in Fig-2.

This coupled with the expected production

growth in the minor producers viz. Vietnam,

Sri Lanka and Cambodia could facilitate a

positive growth for the year 2010. Following

the growth in the first half of 2010, the

production in 2010 is currently projected at

10.2 million tons, higher by around 6% from

the previous year level of 9.617 million tons.

Natural Rubber consumption

Natural rubber on account of its

elasticity, resilience and toughness is

used in a variety of industrial and

durable goods components, among

which automobile is the major

segment that accounts for 70% of the

total consumption. Thus the natural

rubber demand closely tracks

automobile production trends as

illustrated in Fig-3. The natural

rubber demand grew uninterrupted

at an annual average rate of 5.58%

during the period 2002 to 2007

facilitated by the rapid growth in

automobile segment and booming

economic climate before succumbing

to the global recessionary pressures

in 2008 and 2009. As illustrated in

the chart, the global automobile production slumped in 2009, which has declined by 12.5% to 61.71 million

units from the previous year production level of 70.52 million units. Natural rubber consumption also

witnessed its worst annual decline in 2009, which fell by 7.7% to 9.39 million tons from the previous year

peak consumption level of 10.17 million tons. Major declines were observed in US and Japan followed by

other nations. The change in consumption in 2009 over 2008 across the major nations is illustrated in Fig-

4.

Fig-2: NR production changes in 1h 2010 over 1h 2009

21.1%

14.3%

13.9%

6.5%3.1% 0.2%

9.7%46.7%

0

200

400

600

800

1000

1200

1400

1600

Th

aila

nd

(Jn

-Ju

n)

Ind

on

esia

(Jn

-My)

Ma

laysia

(Jn

-Ju

n)

Ind

ia (

Jn

-

Jly

)

Vie

tna

m

(Jn

-Jly

)

Ch

ina

(Jn

-

Ju

n)

Sri

lan

ka

(Jn

-Jly

)

Ca

mb

od

ia

(Jn

-Jly

)

pro

duction in '000 T

ons

200820092010

change in 2010 over 2009

Source: ANRPC and Pacrim research

Fig-3: Global automobile production vs. natural rubber

consumption, Year on year changes

-15%

-10%

-5%

0%

5%

10%

15%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

an

nu

al c

hg

40

45

50

55

60

65

70

75

au

to p

rod

tn, m

ln u

nit

s

Automobile production (mln units), RHS

YoY NR conmptn chg (%), LHS

YoY % auto chg (%), LHS

prodtn in 2007:

73.26 mln. 2010 est:

67.7 mln.

Source: OCIA, Pacrim research

Natural Rubber review

-3-

Consumption to pickup in 2010, albeit at a slower rate than initially anticipated…

The rubber consumption is seen improving in the year 2010 following the pick up in the automobile

demand as reflected by an increase in sales during the first half of the year. The automobile sales at the

global front were estimated at 41.852 million units during the period Jan-Jul2010, higher by 16% over the

same period previous year level of 36.06 million units. Following the growth in automobile segment and

taking clues from the increase in import demand from leading consuming nations viz. China, India, Malaysia

and Japan, the natural rubber consumption for the year 2010 was initially expected to grow at an annual

rate of 10.7% to 10.4 million tons, which after wards was revised lower taking into account the growing

fears over double dip recession. The natural rubber consumption is currently projected at 10.2 million tons,

higher by 8.63% over the 2009 level. Much would depend upon the economic performance in the second

half of the 2010 following the evidence of slowing down economic growth in the developed economies and

economy cooling off measures like higher interest rates being initiated in China, as the same might impact

the automobile segment performance.

Natural rubber balance sheet

Given the current expectations, the global natural production and consumption could balance each other in

absolute terms thus leaving the ending stocks unchanged from the previous year level at 1.613 million tons.

However, in relative terms, the stock to use ratio is expected to decline from 17.18% in 2009 to 15.81% in

2010 on account of the higher consumption base. The supply and demand balances in the past two decades

is summarized in the Table-2. As illustrated, faster growth in demand relative to production is expected to

reduce the ending stocks in months to use to 1.9 in 2010 from the previous year level of 2.06 and shall

support the prices over the important support levels in the remaining part of the year. On the cautionary

note, although the production growth at 6% seems possible given the increases in the first half of the year,

much would depend upon the consumption growth in the remaining part of the year following the fears of

double dip recession. Any reduction in consumption could ease the current tight situation and might weigh

on the prices.

Leaving aside the immediate implications, a glance on the months to use trends during the past two decade

period hints that natural rubber market has tilted down from a well supplied scenario (with ending stocks

greater than four months of usage) in 1990’s to a balanced scenario in 2000s where in stocks hovered

0

1000

2000

3000

4000

5000

6000

7000

8000

Chin

a

U.S

.A

India

Japan

Mala

ysia

Indonesia

Thaila

nd

Rep.o

f

Kore

a

Oth

ers

co

nsu

mp

tn i

n '000 t

on

s

-80%

-60%

-40%

-20%

0%

20%

40%

% c

han

ge2008 2009 % change in 2009 over 2008 (RHS)

Fig-4: Natural rubber consumption in 2009 vs. 2008 in important countries

Source: IRSG, Rubberboard, India and Pacrim research

Natural Rubber review

-4-

between 1.5 to 2 months of usage. This is a major supportive factor for the prices in the long run and clearly

indicates that market is more prone for wide swings for the slightest hint of any possible deviations from

the normal supply and demand trends owing to decline in margin of comfort. Although the measures

initiated by several players in expanding the rubber plantations might help to restore the balance, it could

be a while before those increased supplies find their way into the market.

Table-2: Natural rubber supply and demand balance sheet

1991 1995 2000 2005 2006 2007 2008 2009 2010

Production, MMT 5.16 6.04 6.76 8.90 9.79 9.80 10.04 9.62 10.20

Consumption, MMT 5.09 6.00 7.34 9.20 9.68 10.14 10.17 9.39 10.20

Production deficit/ surplus, MMT 0.07 0.04 -0.58 -0.30 0.11 -0.34 -0.14 0.23 0.00

Ending stocks, MMT 2.38 2.45 2.18 1.75 1.87 1.52 1.39 1.61 1.61

Stocks to use ratio (%) 46.8% 40.8% 29.7% 19.0% 19.3% 15.0% 13.6% 17.2% 15.8%

Stocks in months to use 5.61 4.90 3.57 2.29 2.31 1.80 1.63 2.06 1.90

Average price, RSS3, US$ per Kg 0.85 1.56 0.75 1.50 2.16 2.32 2.61 1.98 3.18

Source: IRSG, Pacrim research