Embed Size (px)

Citation preview

National accounts: Part 3

MEASUREMENT ECONOMICS

ECON 4700

2

This chapter

• Some more thoughts on GDP– Net vs. Gross

– Principle components of the IEA

– Seasonal adjustment

3

Some additional thoughts on GDP

• Net vs. Gross: Gross" means depreciation of capital stock is not subtracted. If we substitute gross investment by net investment (which is gross investment minus depreciation) in the equation (C + I + G + XN), then we obtain the formula for net domestic product.

• Depreciation is a term used in accounting, economics and finance with reference to the fact that assets with finite lives lose value over time.

• Capital refers to already-produced durable goods available for use as a factor of production. Steam shovels (equipment) and office buildings (structures) are examples.

• "Capital as such is not evil; it is its wrong use that is evil. Capital in some form or other will always be needed." Mahatma Gandhi

4

Some additional thoughts on GDP

About 12% of GDP

Basic price ???

5

Some additional thoughts on GDP

6

Some additional thoughts on GDP

7

Some additional thoughts on GDP

8

Some additional thoughts on GDP

• Basic prices: A basic price valuation includes the costs of production factors (labour and capital) and indirect taxes and subsidies on production factors. Income measures are estimated at basic prices or market prices.

• Since its inception, GDP has been measured at factor cost. This measure differs from the more prevalent market price measure found in the income and expenditure accounts by its exclusion of taxes on production (formerly called indirect taxes) and the inclusion of subsidies. While the market price measure represents the value of GDP as paid for by final consumers, the factor cost measure, more appropriately in the case of industrial production, takes the point of view of producers.

9

Some additional thoughts on GDP

• GDP will no longer be measured at factor cost, but instead at basic prices. This new measure adds to the factor cost measure some taxes on production (such as property and payroll taxes, but not federal or provincial sales taxes), and subtracts some subsidies (such as labour-related subsidies, but not product-related subsidies). The end result is that the new basic prices measure of GDP stands somewhere in between the lower and upper bounds defined by the factor cost and market price measures, respectively.

10

Some additional thoughts on GDP

• GDP at factor cost excludes all taxes on production and includes all subsidies whether they are on intermediate inputs or labour and capital. In the basic price approach only taxes and subsidies on intermediate inputs are treated in this manner. Payroll taxes are payments to government arising out of the input of labour services, and property taxes are levies on the capital services of buildings and other property. They are both part of production and are included in the basic price measure. On the other hand, subsidies to labour and capital are deducted from the gross revenues of these factors as they are payments by governments rather than earnings.

• By calculating GDP at basic prices, Statistics Canada makes its estimates of economic activity more comparable to those produced by a majority of other OECD countries.

11

Some additional thoughts on GDP

GDP, GNP:Q4, 2008 X 1 000 000

Gross Domestic Product (GDP) at market prices

393 562

Add: Net investment income from non-residents -4 875

(Always negative)

Gross National Product (GNP) at market prices 388 687

Deduct: Capital consumption allowances 49 719

Deduct: Statistical discrepancy 1 345

Deduct: Taxes less subsidies on products 26 449

Net national income at basic prices 311 174

12

Some additional thoughts on GDP2006

Gross Domestic Product (GDP) 1446307 100%††Personal expenditure on consumer goods and services 803502 56%††††Durable goods 105716 7%††††Semi-durable goods 66818 5%††††Non-durable goods 195572 14%††††Services 435396 30%††Net government current expenditure on goods and services 279806 19%††Government gross fixed capital formation 40336 3%††††Structures 28692 2%††††Machinery and equipment 11644 1%††Government investment in inventories -41 0%††Business gross fixed capital formation 277885 19%††††Residential structures 98386 7%††††Non-residential structures 85698 6%††††Machinery and equipment 93801 6%††Business investment in inventories 7824 1%††††Non-farm 8369 1%††††Farm -545 0%††Exports of goods and services 816460 56%††††Exports to other countries 524706 36%††††Exports to other provinces 291754 20%††Deduct: Imports of goods and services 779414 54%††††Imports from other countries 487660 34%††††Imports from other provinces 291754 20%††Statistical discrepancy -51 0%Final domestic demand 1401529 97%

13

Seasonal adjustment

• What is seasonal adjustment of a time series such as the CPI, GDP, unemployment rate…?

• Seasonal adjustment is a statistical method for removing the seasonal component of a time series used when analyzing non-seasonal trends.

• Series are made up of four components:– St : The Seasonal Component (Not interesting)– Tt : The Trend Component (Good for long term analysis)– Ct : The Cyclical Component (Most important to analysts)– It : The Error, or irrelevant component.

• Unlike the trend and cyclical components, seasonal components, theoretically, happen at in the same magnitude during over the same period of time each year. The seasonal component of a series are often considered uninteresting and cause a series to be ambiguous. By removing the seasonal component, it is easier to focus on other components.

14

Seasonal adjustment

• Examples of seasonal effects include a July drop in automobile production as factories retool for new models, increases in heating oil production during September in anticipation of the winter heating season, and higher consumer expenditure in December.

• Seasonal movements are often large enough that they mask other characteristics of the data that are of interest to analysts of current economic trends. For example, if each month has a different seasonal tendency toward high or low values it can be difficult to detect the general direction of a time series' recent monthly movement (increase, decrease, turning point, no change, consistency with another economic indicator, etc.). Seasonal adjustment produces data in which the values of neighbouring months are usually easier to compare. Many data users prefer seasonally adjusted data because they want to see those characteristics that seasonal movements tend to mask, especially changes

in the direction of the series.

15

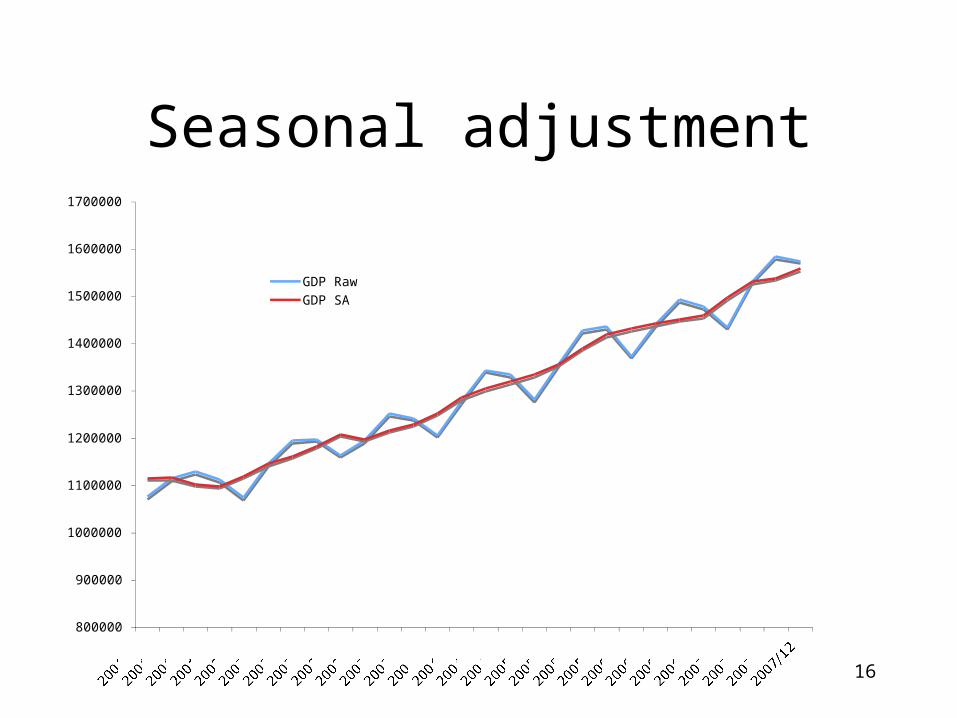

Seasonal adjustment

• The seasonal adjustment technique DOES NOT for example eliminate the higher consumer expenditure in December but redistributes the recursive peak in December (4th quarter) among the other quarters of the year.

• It then becomes possible to observe the underlying trend through the 3d and 4th quarter.

• Most analysis of economic events is mostly done in terms of seasonally adjusted data.

• Here is an example:

16

Seasonal adjustment

800000

900000

1000000

1100000

1200000

1300000

1400000

1500000

1600000

1700000

2001/032001/062001/092001/122002/032002/062002/092002/122003/032003/062003/092003/122004/032004/062004/092004/122005/032005/062005/092005/122006/032006/062006/092006/122007/032007/062007/092007/12

GDP RawGDP SA

17

Seasonal adjustmentSeasonal adjustment factors

0.92

0.94

0.96

0.98

1

1.02

1.04

2001/032001/092002/032002/092003/032003/092004/032004/092005/032005/092006/032006/092007/032007/09

18

Seasonal adjustment

• What is an annual rate? Why are seasonally adjusted data often shown as annual rates?

• Very generally, what we call the seasonally adjusted annual rate for an individual quarter is an estimate of what the annual total would be if non-seasonal conditions were the same all year, i.e., the value that would be registered if the seasonally adjusted rate of activity measured for a quarter were maintained for a full year. Annual rates are used so that periods of different lengths–for example, quarters and years–may be

easily compared. • This "rate" is not a rate in a technical sense but is a level estimate.• The seasonally adjusted annual rate is the seasonally adjusted quarterly

value multiplied by 4 (12 for monthly series). • The benefit of the annual rate is that we can compare one month's data

or one quarter's data to an annual total, and we can compare a month to a quarter.

19

Seasonal adjustment

• Seasonal factor: are estimates of average weather effects for each quarter. For example, the average January decrease in new home construction due to cold and storms.

• Seasonal adjustment does not account for abnormal weather conditions or for year-to-year changes in weather. It is important to note that seasonal factors are estimates based on present and past experience and that future data may show a different pattern of seasonal factors.

20

Seasonal adjustment

• The following steps are followed to calculate seasonal factors:– An annual average is calculated for each year.– Each quarterly data point is divided by the corresponding

annual average. This variable represents the percentage of the annual average.

• The quarterly percentages are averaged across the same quarter for ten years of data = The seasonal factor.

21

Seasonal adjustment

• One last thought on S.A.

• http://www.mises.org/story/493

22

Introduction to I-O

• The construction of the input output table first occurred back in the mid-1930s, created by a man called Wassily Leontief. They were used to analyse the American economy at the time. From this beginning input output analysis has grown to be regarded as one of the most important tools of economic analysis.

• An input output table is simply a table made up of a set of rows and columns that analyse a firm, or multiple firms, inputs and outputs.

• Numerical values are placed in these rows and columns, which turns into a complicated picture of all the flows of goods and services between three types of organisation and the rest of the world. These organisations are (i) households, (ii) productive organisations (firms and farms) and (iii) the government. Although, specific government departments who engage in producing marketable outputs are considered productive organisations.

23

Introduction to I-O

• Whenever there is a transfer of a good or service between any two organisations and the rest of the world, usually a cash flow in the opposite direction will correspond. For example, Alpha Cotton Fabric Co Ltd transfers 20000 yards of cotton fabric to Beta Clothing Factory Ltd then unless Alpha Cotton fabric is a charitable organisation; Beta Clothing Factory will make a cash payment in return. This transaction of goods and services and cash flows between the three types of organisations and the rest of the world forms a complicated set of relationships, the basis of the complex modern economy.

24

Introduction to I-O

• Purpose of input output tables. They are used to trace the flow of intermediate production as it makes its way through the structure of industry and to show how production, all along the line form primary to intermediate, to finished goods, is affected by the demand for final goods and services.

• If we take an example with the assumption that the economy does not engage in foreign trade and that the productive sector has been divided into three producing industries.

25

Introduction to I-O

Table 1

Inter industry Sales 1 2 3 Final Demand Gross Output Inter industry 1 X11 X12 X13 Y1 X1 Purchases 2 X21 X22 X23 Y2 X2

3 X31 X32 X33 Y3 X3

Value Added V1 V2 V3 ∑ Yi = ∑Vj Gross output X1 X2 X3 ∑ Xi = ∑Xj

The rows represent the value of the industry sales and the columns represent the value of purchases.

X12 represents industry 1 sales to industry 2

X23 represents industry 3 purchases from industry 2

X23 represents industry 2 sales to industry 3

26

Introduction to I-O

• The rows represent the value of the industry sales and the columns represent the value of purchases. For example, X11 represents the sale of industry 1 to itself that is retained production. X12 represents industry 1 sales to industry 2 and X13 represents industry 1 sales to industry 3. The industry sales to users of the final goods and services is the industry’s final demand represented by Y and the industry’s Gross output is the combination of inter industry sales plus the final demand and is represented by an X. The other 2 industries listed follow exactly the same pattern with industry 2 having (X21 + X22 + X23) inter industry sales plus a final demand Y2 and industry 3 has inter industry sales of (X31 + X32 + X33) plus a final demand Y3.

• Whereas the rows represent the sales of the industry denoted by an i, the column shows the purchase of the industry, denoted by a j. So X11, X12 and X13 represent the inter-industry purchase made by industry 1. Likewise X21, X22, X23 and X31, X32, X33 represent the purchase of industries 2 and 3 respectively.

27

Introduction to I-O

• The gross output of each industry minus the inter-industry purchases must equal the value added by industry.

• This value added consists of wage, interest and rental payments and the profits of the industry. The final demand must equal the sum of all value added at each stage of production.

• Then by denoting value added as Vj it must be that

• SUM Yi = SUM Vj

• The input output table is perfectly consistent with accounting concepts. In the input output table the sum of all gross outputs minus inter-industry sales must equal gross output for all industries minus inter-industry purchases.