Embed Size (px)

Citation preview

Experts in numerical algorithms and HPC services

NAG for HPC Finance

John Holden

15th May 2012

Computational Methods and

Technologies for Finance

HPCFinance Conference

Tampere, Finland

2

NAG Introduction

NAG for HPC Finance

Why Quants Love NAG

Accelerators NVIDIA

Intel Xeon-Phi

Algorithmic Differentiation

Summary

Agenda

3

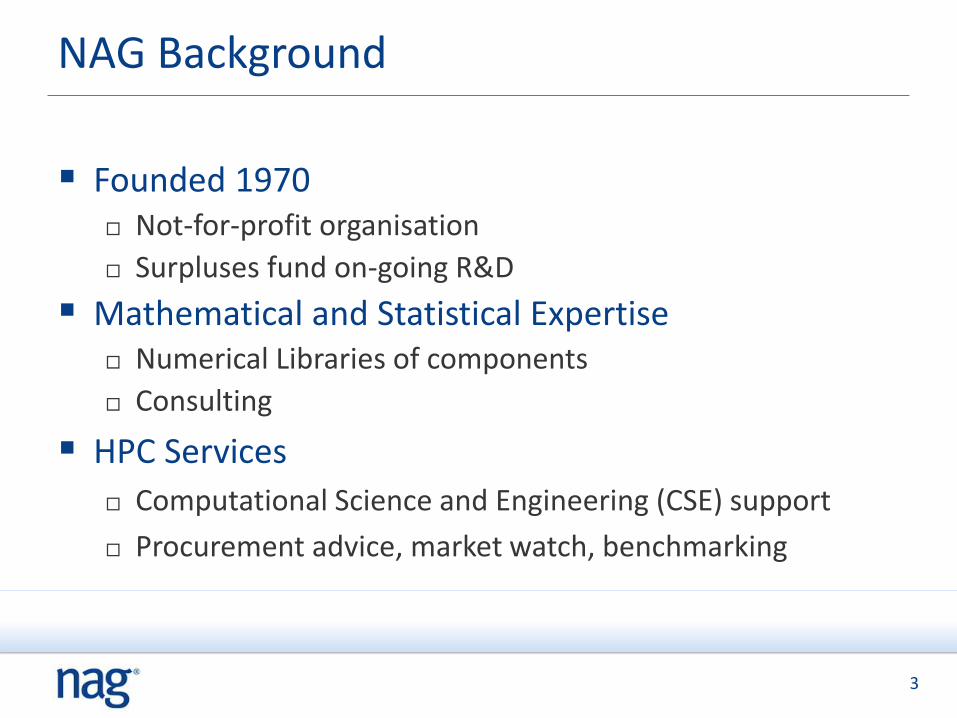

Founded 1970 Not-for-profit organisation

Surpluses fund on-going R&D

Mathematical and Statistical Expertise Numerical Libraries of components

Consulting

HPC Services

Computational Science and Engineering (CSE) support

Procurement advice, market watch, benchmarking

NAG Background

4

HPC Services

Government, Academic and Commercial

Full CSE service

Code porting, tuning, scaling, rewriting…

Training

1-20 FTEs per annum

Procurement advice/benchmarking

5

Financial Services

Many clients in FSI

Most Tier 1 Banks have licences

> 60% have global licences

Typically the NAG Library is embedded in the banks own “quant” libraries (C++, . NET, Java,…)

6

HPCFinance.eu

All HPCFinance fellows can

get access to NAG software for their HPCFinance.eu work

get HPC Services training from NAG (direct, or via HECToR) OpenMP, CUDA, MPI, Algorithmic Differentiation,

Good collaborations on HPC Finance codes with

University of Manchester and SWIP Professor Poon + fellows

Aarhus University PhD / HPCFinance fellow secondment pending

7

NAG Introduction

NAG for HPC Finance

Why Quants Love NAG

Accelerators NVIDIA

Intel Xeon-Phi

Algorithmic Differentiation

Summary

Agenda

8

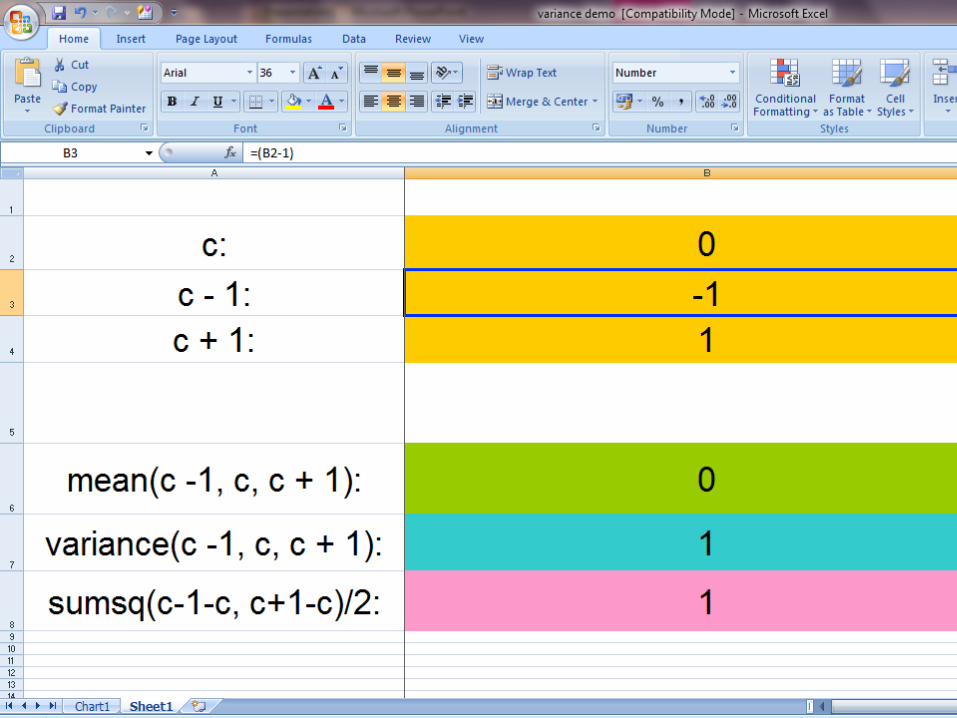

An example: sample variance

For a collection of observations

the mean is defined as

and the variance as

}...1,{ nixi }...1,{ nixi

2

1

2 )(1

1xx

ns

n

i

i

n

i

ixn

x1

1

}...1,{ nixi

2

1

2 )(1

1xx

ns

n

i

i

n

i

ixn

x1

1

2

1

2 )(1

1xx

ns

n

i

i

n

i

ixn

x1

1

11

What’s gone wrong?

Instead of

Excel uses an (analytically identical) formula

faster to calculate (one pass)

accuracy problems if variance is small compared to x

2

11

22 1

1

1 n

i

i

n

i

i xn

xn

s

2

1

2 )(1

1xx

ns

n

i

i

12

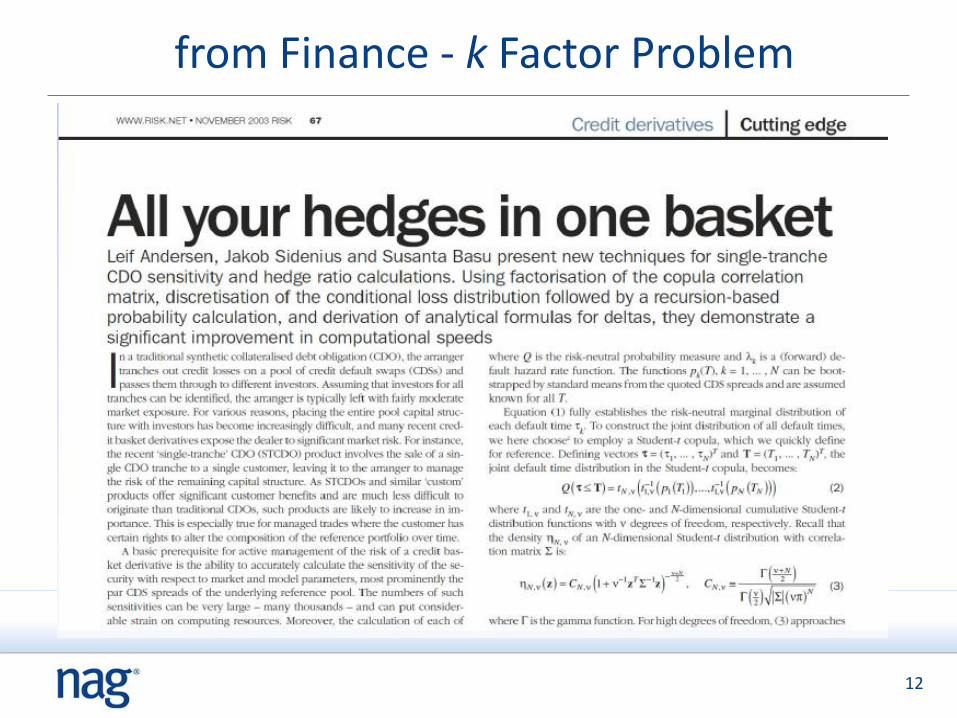

from Finance - k Factor Problem

13

from Finance - k Factor Problem

Nonlinear objective function with convex quadratic

constraints.

NAG function (G02AE) based on spectral projected

gradient method

(Borsdorf, Higham & Raydan, 2010)

Respects constraints, exploits convexity, converges to a

feasible stationary point

Principal Factors method (Andersen et al., 2003)

No convergence theory and can converge to an incorrect

answer

14

Why Quants use NAG Libraries and Toolboxes?

Global reputation for quality – accuracy, reliability and robustness…

Extensively tested, supported and maintained code

Reduces development time

Allows concentration on your key areas

Components

Fit into your environment

Simple interfaces to your favourite packages

Regular performance improvements!

Give “qualified error” messages e.g. tolerances of answers

15

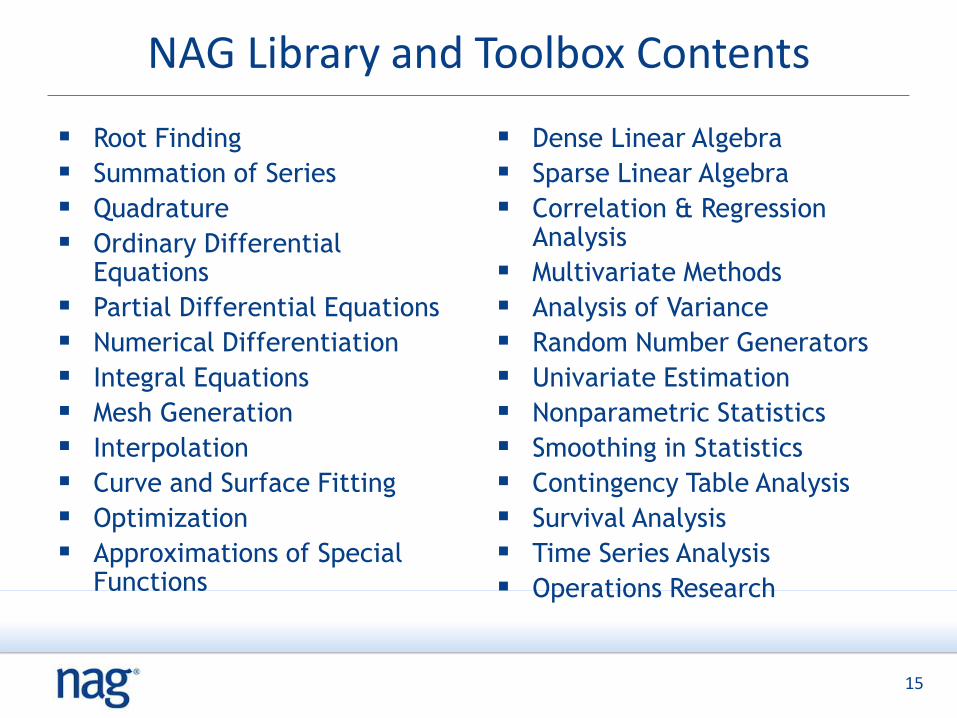

NAG Library and Toolbox Contents

Root Finding

Summation of Series

Quadrature

Ordinary Differential Equations

Partial Differential Equations

Numerical Differentiation

Integral Equations

Mesh Generation

Interpolation

Curve and Surface Fitting

Optimization

Approximations of Special Functions

Dense Linear Algebra

Sparse Linear Algebra

Correlation & Regression Analysis

Multivariate Methods

Analysis of Variance

Random Number Generators

Univariate Estimation

Nonparametric Statistics

Smoothing in Statistics

Contingency Table Analysis

Survival Analysis

Time Series Analysis

Operations Research

16

Use of NAG Software in Finance

Portfolio allocation / Risk management /Stress testing Optimization , interpolation, linear algebra, RNGs, Distributions,

Copulas…

Derivative pricing, Hedging PDEs, RNGs, multivariate normal, curve & surface fitting,

quadrature…

Calibration Optimisation, Interpolation , Root Finders, Splines

Data analysis Time series, GARCH, principal component analysis, data smoothing,

Data Mining…

Monte Carlo simulation RNGs, Brownian Bridge constructor, Linear Algebra

…

17

Why Quantitative Analysts Love NAG?

General Problem

To build asset models and risk engines in a timely manner that are Robust

Stable

Quick

Solution

Use robust, well tested, fast numerical components

This allows the “expensive” experts to concentrate on the modelling and interpretation avoiding distraction with low level numerical components

18

Problem 1: Simulation (Monte Carlo)

Simulation is important for scenario generation

Several different numerical components needed

Random Number Generators

Brownian bridge constructor

Interpolation/Splines

Principal Component Analysis

Cholesky Decomposition

Distributions (uniform, Normal, exponential gamma, Poisson, Student’s t, Weibull,..)

..

19

Problem 1: Simulation (Monte Carlo)

Simulation is important for scenario generation

NAG to the rescue (CPU or GPU)

Several different numerical components needed

Random Number Generators √

Brownian bridge constructor √

Interpolation/Splines √

Principal Component Analysis√

Cholesky Decomposition √

Distributions (uniform, Normal, exponential gamma, Poisson, Student’s t, Weibull,..)√

.. √ √

20

Problem 2: Calibration

Financial institutions all need to calibrate their models

Several different numerical components needed

Optimisation functions (e.g. constrained non-linear optimisers)

Interpolation functions (used intelligently*)

Spline functions

..

*interpolator must be used carefully –must know the properties to pick appropriate method

21

Problem 2: Calibration

Financial institutions all need to calibrate their models

NAG to the rescue

Several different numerical components needed

Optimisation functions (e.g. constrained non-linear

optimisers) √

Interpolation functions (used intelligently*) √

Spline functions √

.. √ √

*interpolator must be used carefully –must know the properties to pick appropriate method

22

NAG fits into your favourite environments

Supporting Wide Range of Operating systems…

Windows, Linux, Solaris, Mac, …

…and a number of interfaces

C, C++,

Fortran,

VB, Excel & VBA,

C#, F#, VB.NET,

CUDA, OpenCL,

Java,

Python

…

Excel,

LabVIEW,

MATLAB,

Maple,

Mathematica

R, S-Plus,

Scilab, Octave

…

23

NAG Introduction

NAG for HPC Finance

Why Quants Love NAG

Accelerators NVIDIA

Intel Xeon-Phi

Algorithmic Differentiation

Summary

Agenda

24

Escalator?: Want more performance? Buy the next processor!

To get performance/efficiency we have to go (massively) parallel

Disruption causing serious look at ‘other’ technologies and algorithms!

Even CPUs with tens of cores per node

Hybrid, shared-memory and distributed-memory parallelism

Painful whichever way we turn!

Where has my Escalator gone?

25

Loose definition: hardware on which to run your software better than on your (general purpose) CPU

Generally NOT an easy win

Significant learning curve and effort

Offload disadvantages

…

Accelerators

26

ClearSpeed

Similar to GPU

Lacked a good software eco-system

IBM Cell

Lacked a good software eco-system

GPGPU

NVIDIA invested in the software eco-system (AMD not!)

Intel Phi

Early days – an encouraging start

Accelerators

27

We provide

A suite of Numerical Routines for Monte Carlo simulation from a collaboration with Professor Mike Giles

also MAGMA based Linear Algebra from Jack Dongarra

on-going work with Professor William Shaw to implement new Inverse CDFs (new distributions and speed up to existing code)

“Bespoke” consultancy codes PDE Solver for Stochastic Local Volatility

FX Basket Option, Local Vol Model

..

Training courses for CUDA and Open CL

NAG and GPGPUs (NVIDIA)

28

NAG GPU Gamma Inverse CDF Benchmarks

What follows are times in milliseconds to compute the gamma inverse CDF for 107 uniform variates GPU = NVIDIA GeForce GTX 480

CPU = Intel Core 2 Duo E7400

OS = Ubuntu Server 11.10

Times in bold are for double-precision; other times are for single-precision

Accuracy: maximum ulp errors are always ≤ 8

29

Shape

parameter

NAG Boost

GPU CPU CPU

1 77.9

154.0

1016.4

1168.0

2693.4

3511.6

2 86.0

162.9

886.9

1229.7

6937.3

8417.9

4 94.4

157.8

834.8

1199.5

7564.4

8621.1

8 94.4

164.7

838.4

1176.9

5361.6

8937.7

16 94.4

164.7

823.2

1169.3

4738.7

8923.2

30

Relatively easy to take existing OpenMP based code and port to Phi

NAG and Intel Xeon-Phi

Tuning for Phi takes some learning and expertise

… but feedback into Xeon code is often very strong

Performance Issues As always, need large enough problems to make the offload

worthwhile

Seem to have some start-up issues

NAG Library Linux implementation release imminent, early access can be arranged.

31

0

50

100

150

200

250

300

350

400

450

0 5000 10000 15000 20000 25000 30000

Tim

e (

s)

Problem Size (n)

Distance Matrix (g03ea)

32 threads original Phi offload original Phi offload opt 32 threads opt

n=30k; m=3k

Xeon 32t: 192s

Xeon 32t*: 75.7s

Phi 240t*: 40.6s

Phi gain ~5x over

original or ~2x over

optimised

32

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

100 10,000 1,000,000 100,000,000

Tim

e (

s)

Size of problem (n, log scale)

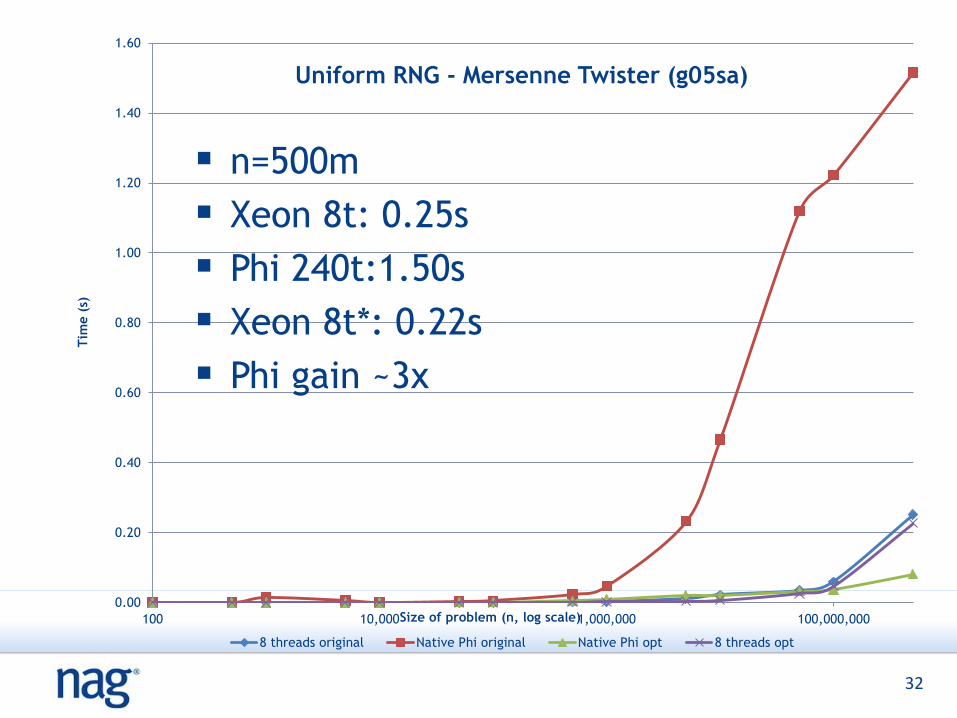

Uniform RNG - Mersenne Twister (g05sa)

8 threads original Native Phi original Native Phi opt 8 threads opt

n=500m

Xeon 8t: 0.25s

Phi 240t:1.50s

Xeon 8t*: 0.22s

Phi gain ~3x

33

To get acceleration look at the algorithms

0

50

100

150

200

250

300

350

50 100 150 200

Runti

me (

s)

Number of inputs (size of Delta)

5000 gradient evaluations of LIBOR Market Model*

using finitedifferences(bumping)

using adjoints

2nd-orderadjoints(projectedHessian)

*M.B. Giles and P.

Glasserman. `Smoking

adjoints: fast Monte Carlo

Greeks', RISK, January

2006

34

To get acceleration look at the algorithms

Adjoint AD reduces Runtime

With Prof. Uwe Naumann & RWTH Aachen University we are delivering Algorithmic Differentiation (AD) tools and services to the finance community for C and C++ codes.

Our example codes include

LIBOR Market Model

PDE based Local Volatility model

35

NAG Introduction

NAG for HPC Finance

Why Quants Love NAG

Accelerators NVIDIA

Intel Xeon-Phi

Algorithmic Differentiation

Summary

Agenda

36

NAG is keen to collaborate in building models and risk engines

Requirements are likely to be varied across FSI

We want to make sure we have what you need

The importance of HPC Finance is growing and will involve a LOT of computation (Basel III, CVA,…)

NAG has significant experience in HPC libraries, services, consulting and training

We know how to do large scale computations efficiently

This is non-trivial! Our expertise has been sought out and exploited by organisations such as (AMD, HECToR, Microsoft, Oracle, major banks, major oil & gas cos,…….)

HPC Finance - Summary